Trading Income: Badges of Trade, Allowable Expenditure Analysis

VerifiedAdded on 2021/04/27

|20

|2145

|63

Homework Assignment

AI Summary

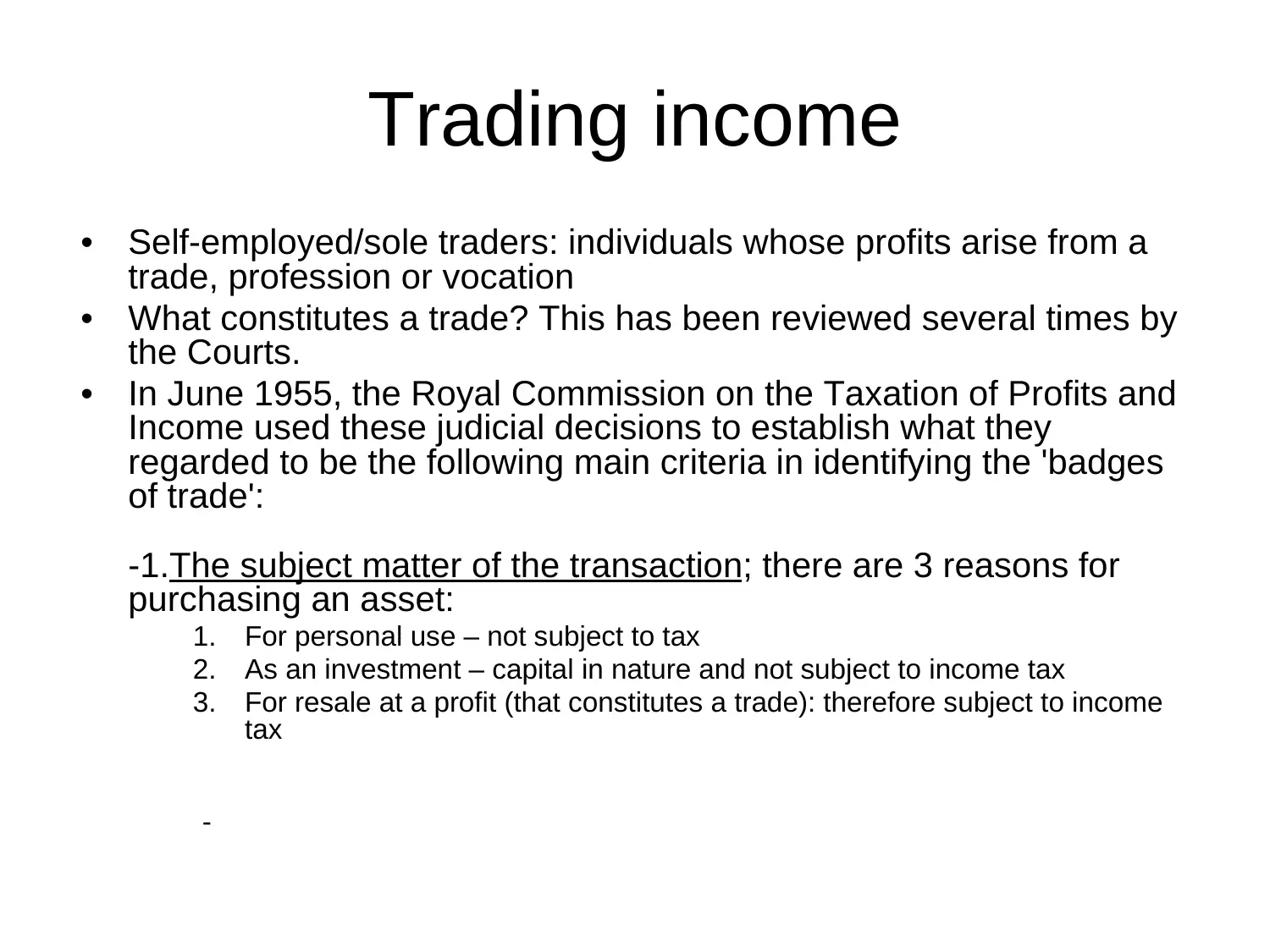

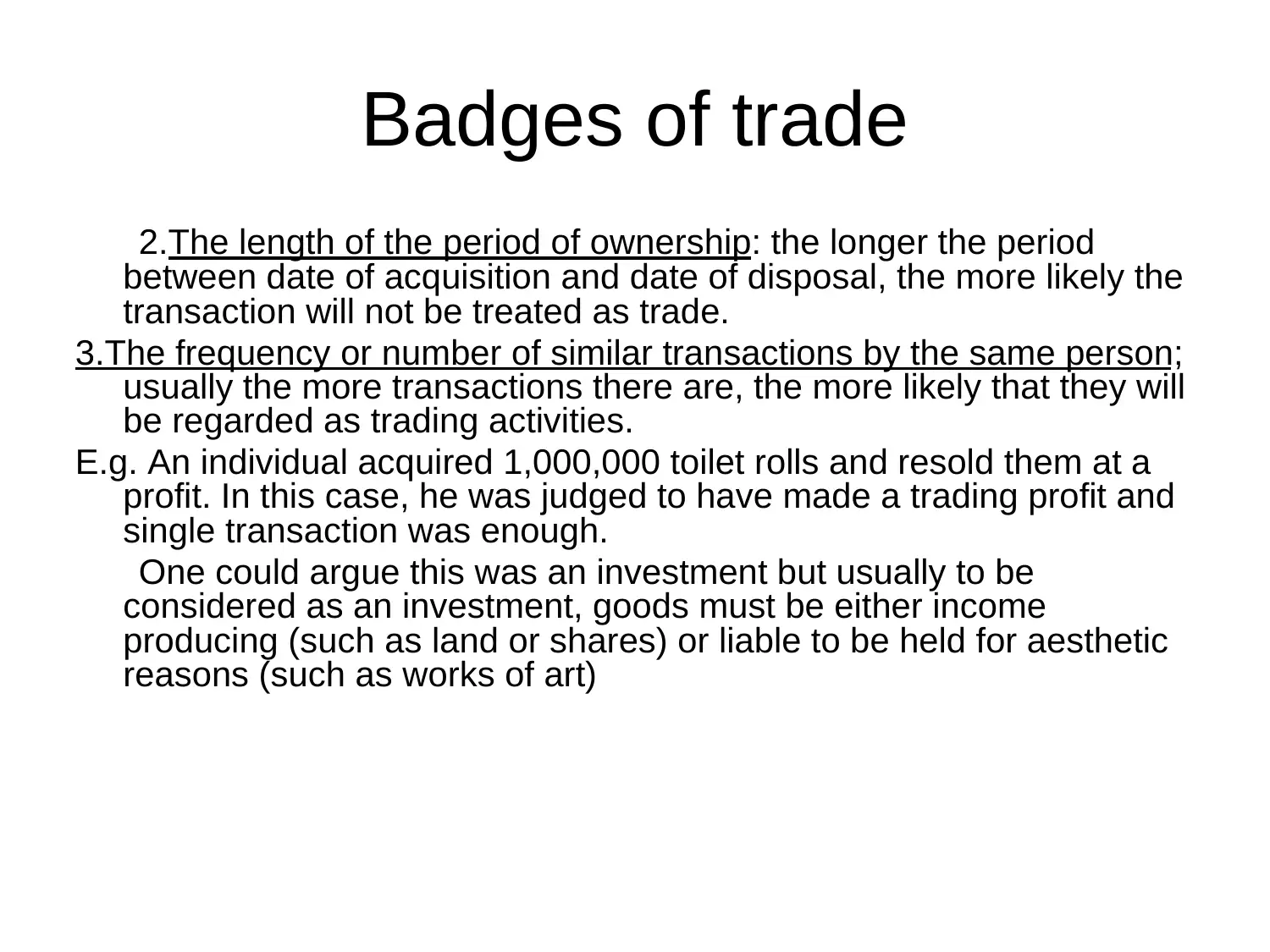

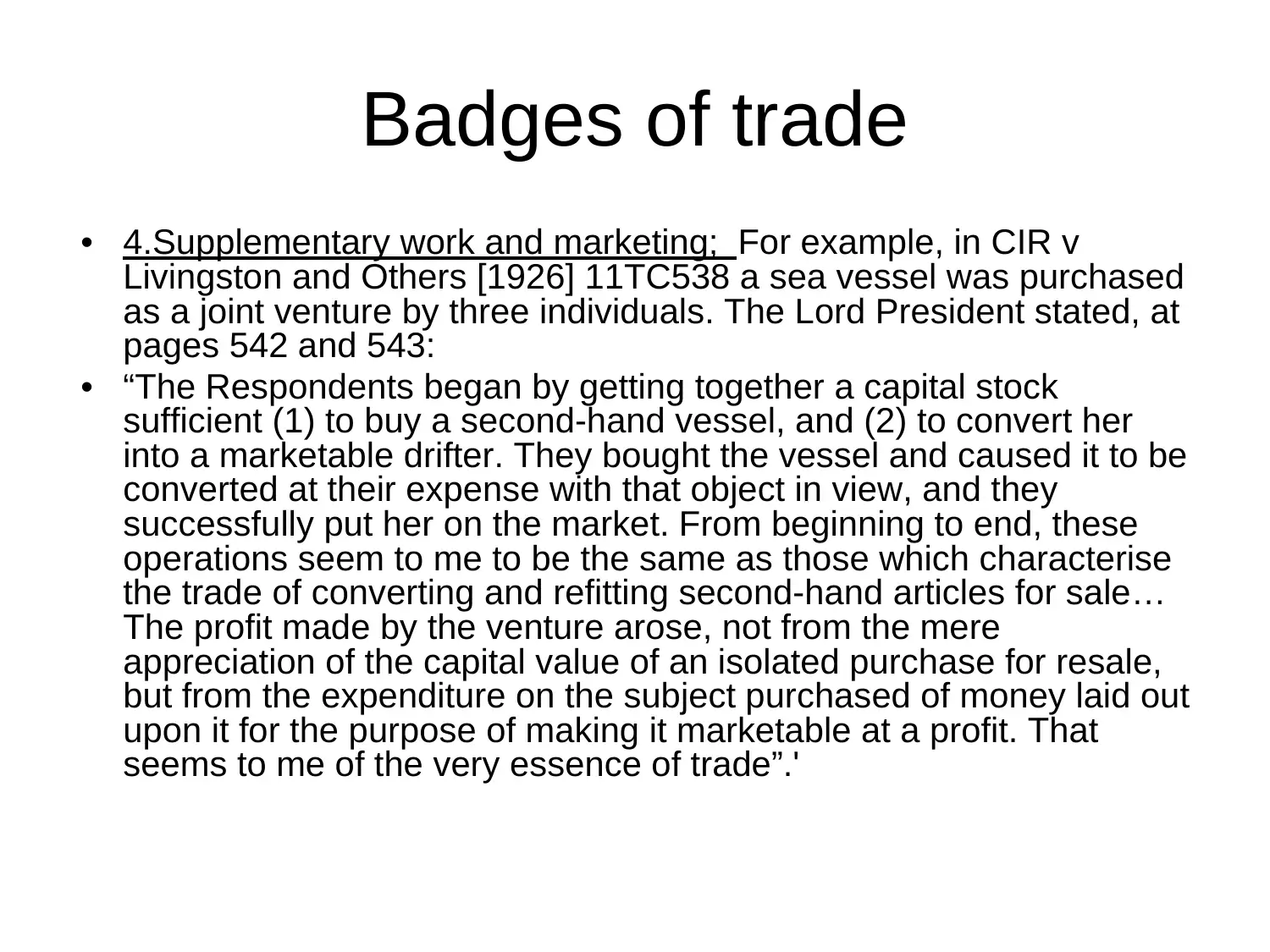

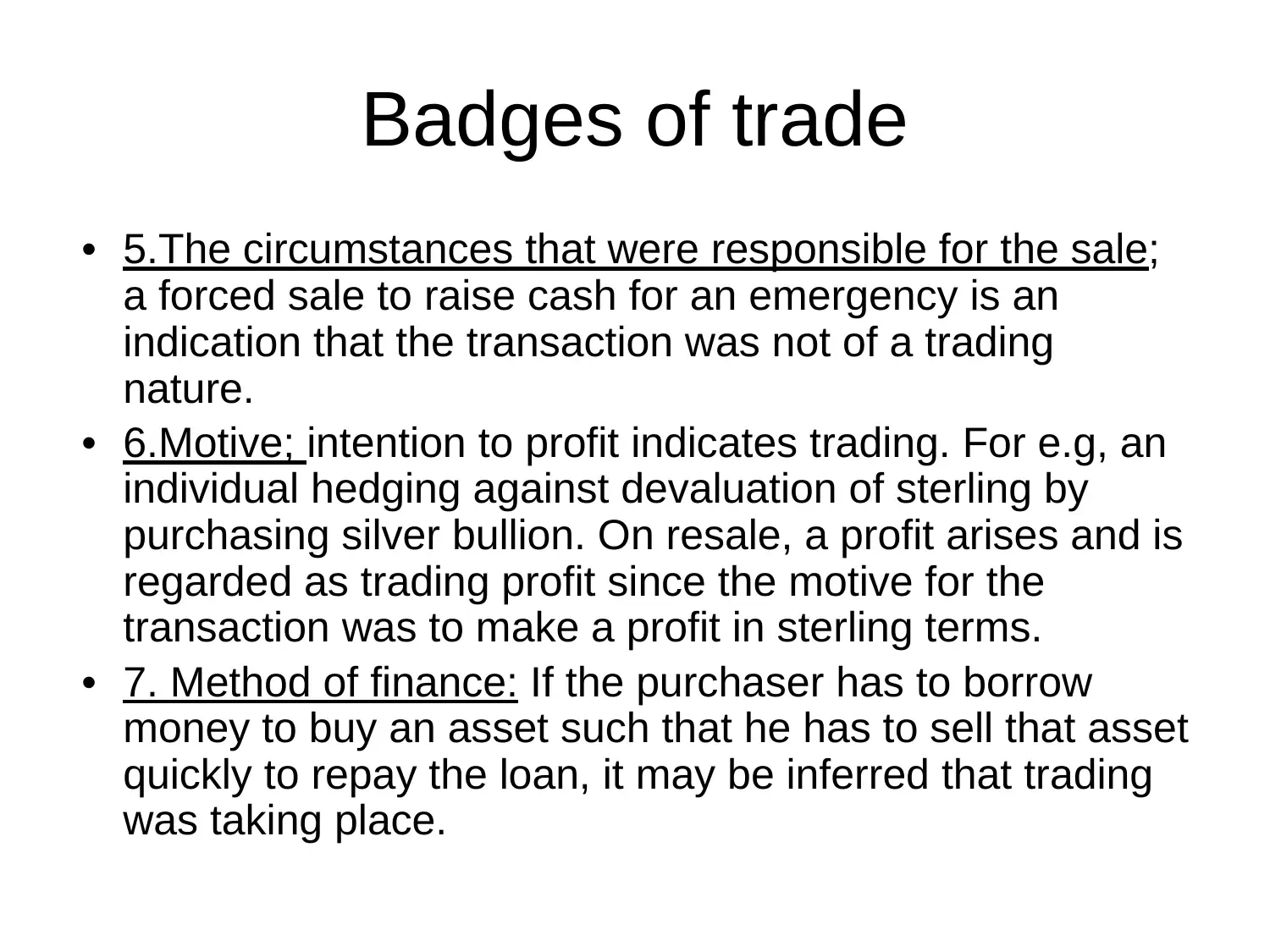

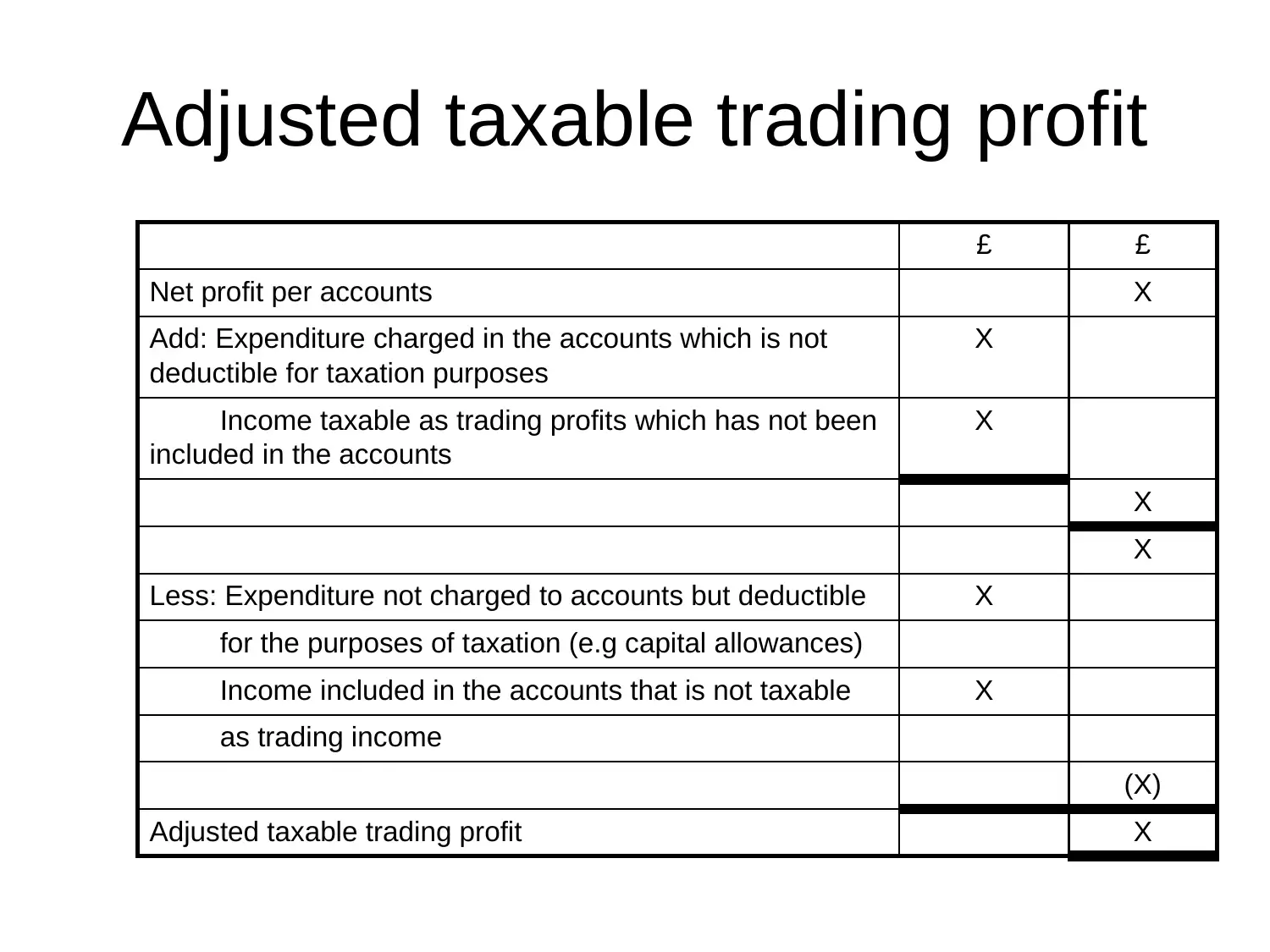

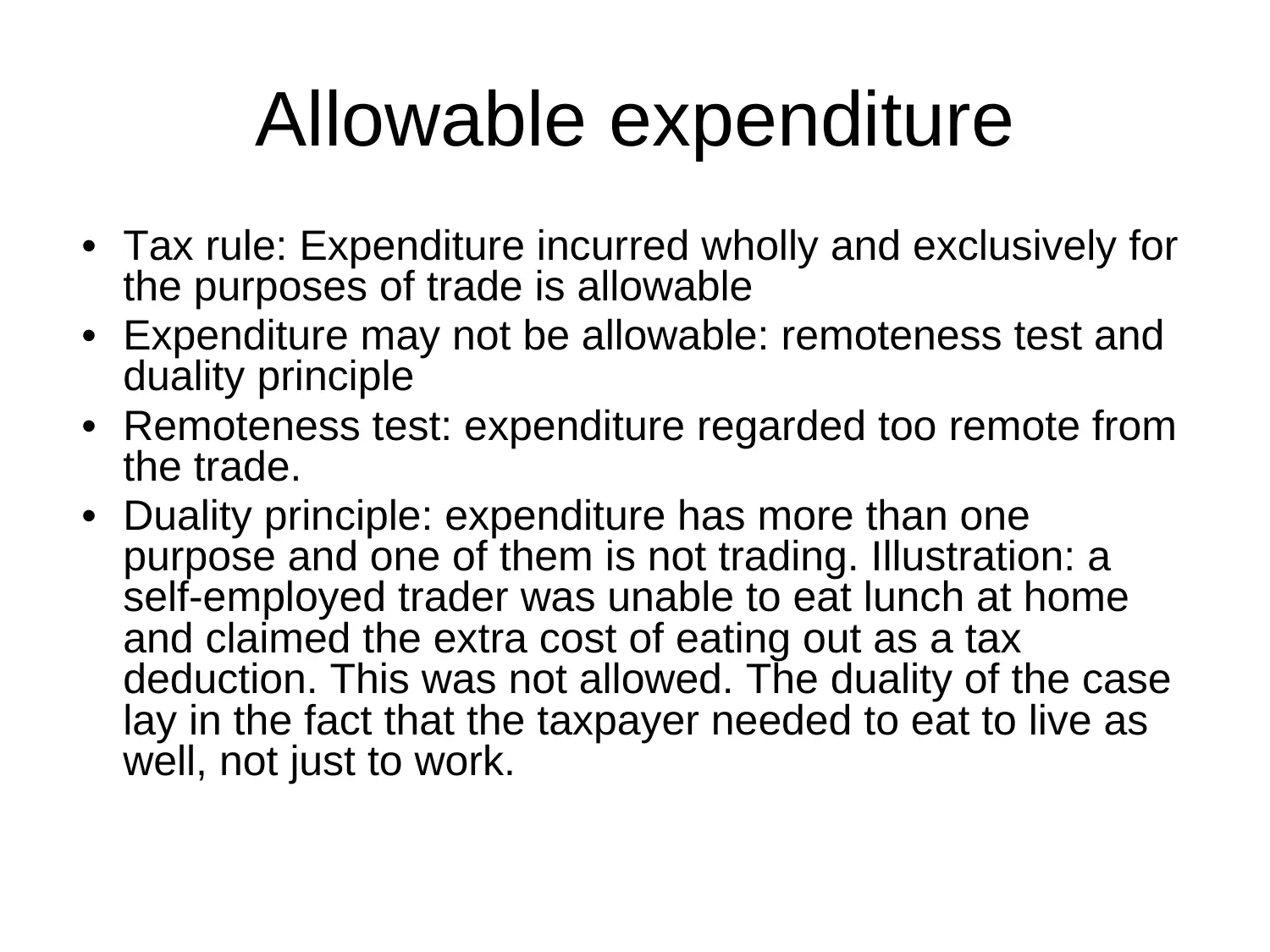

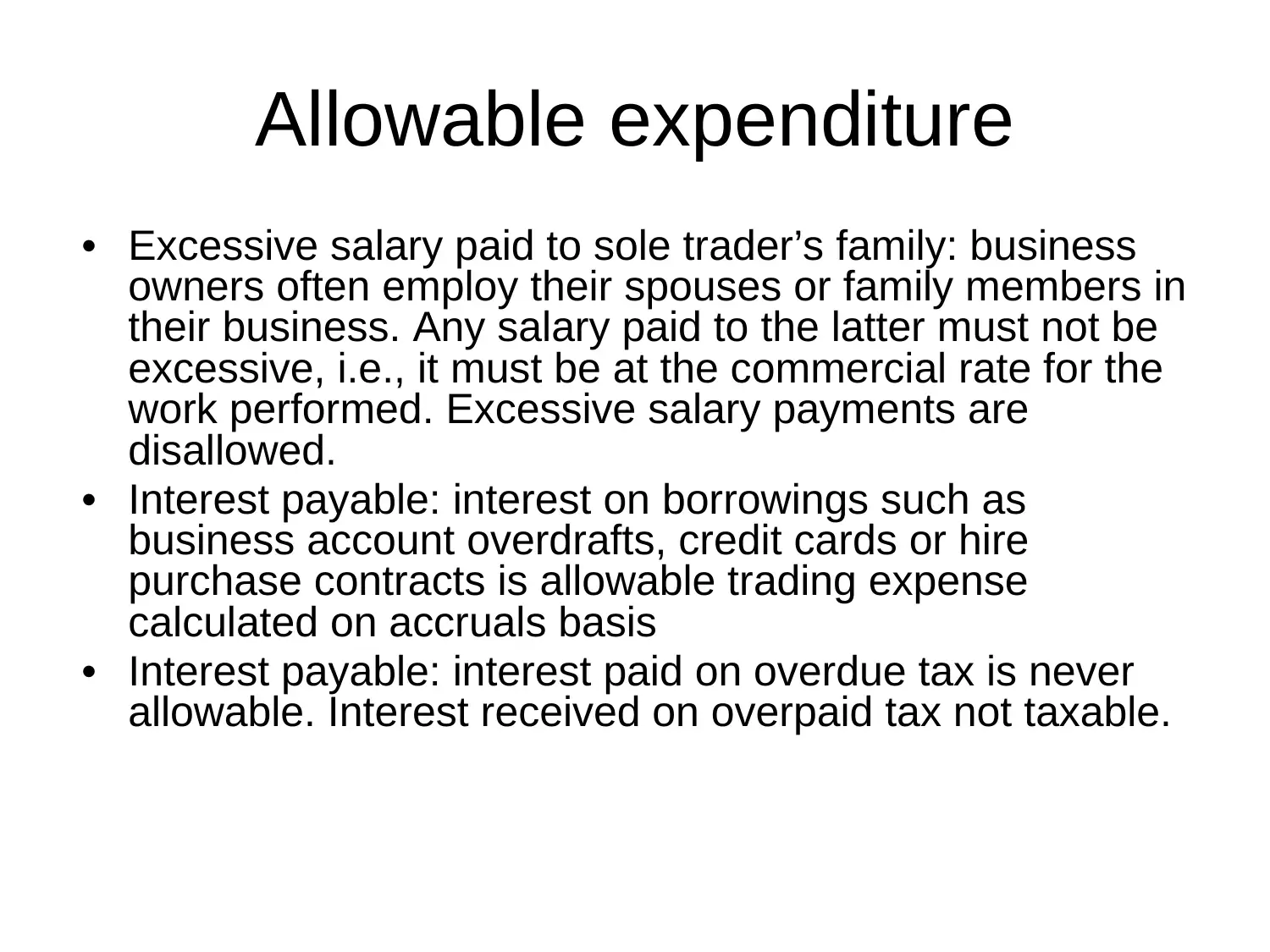

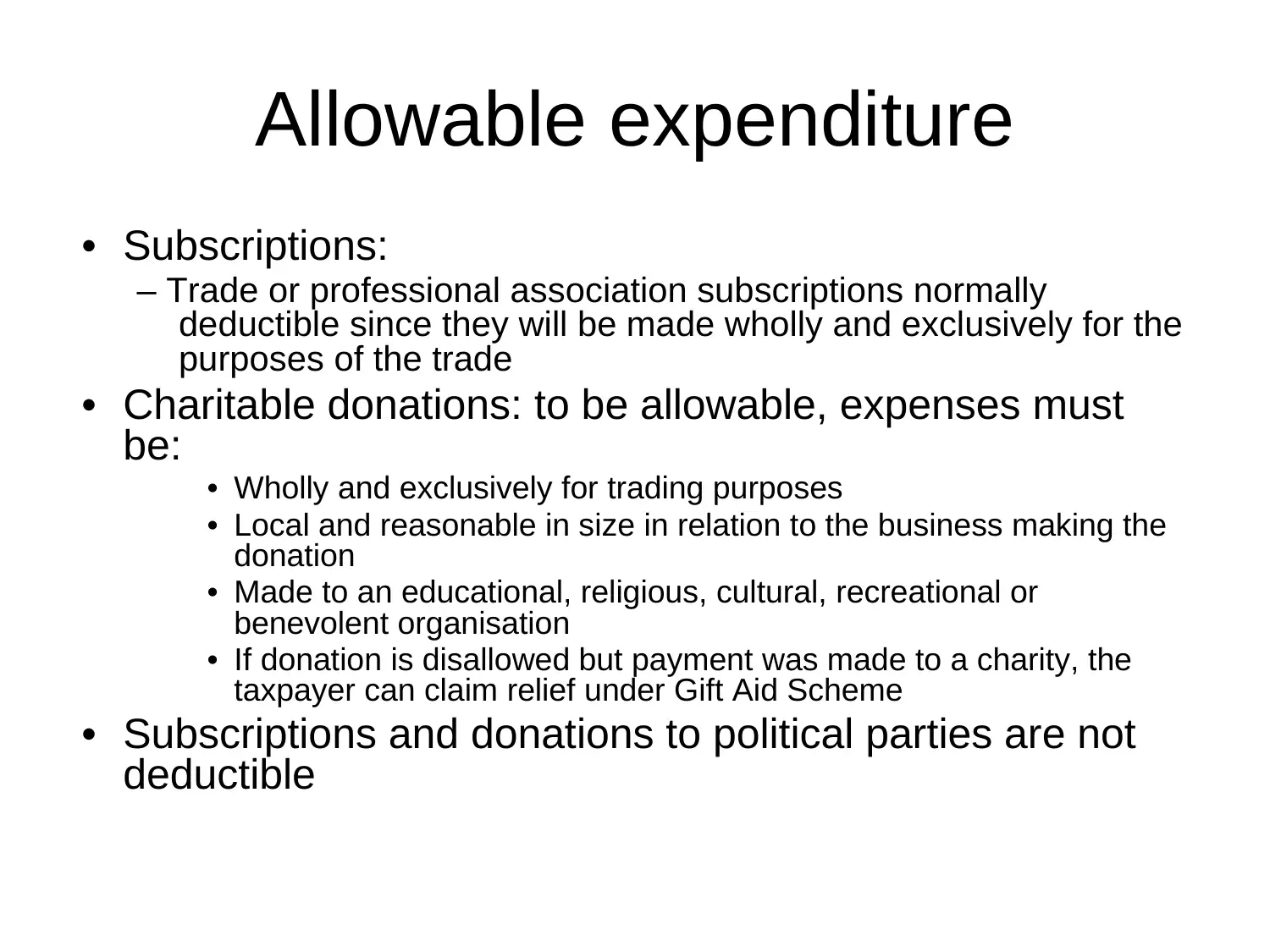

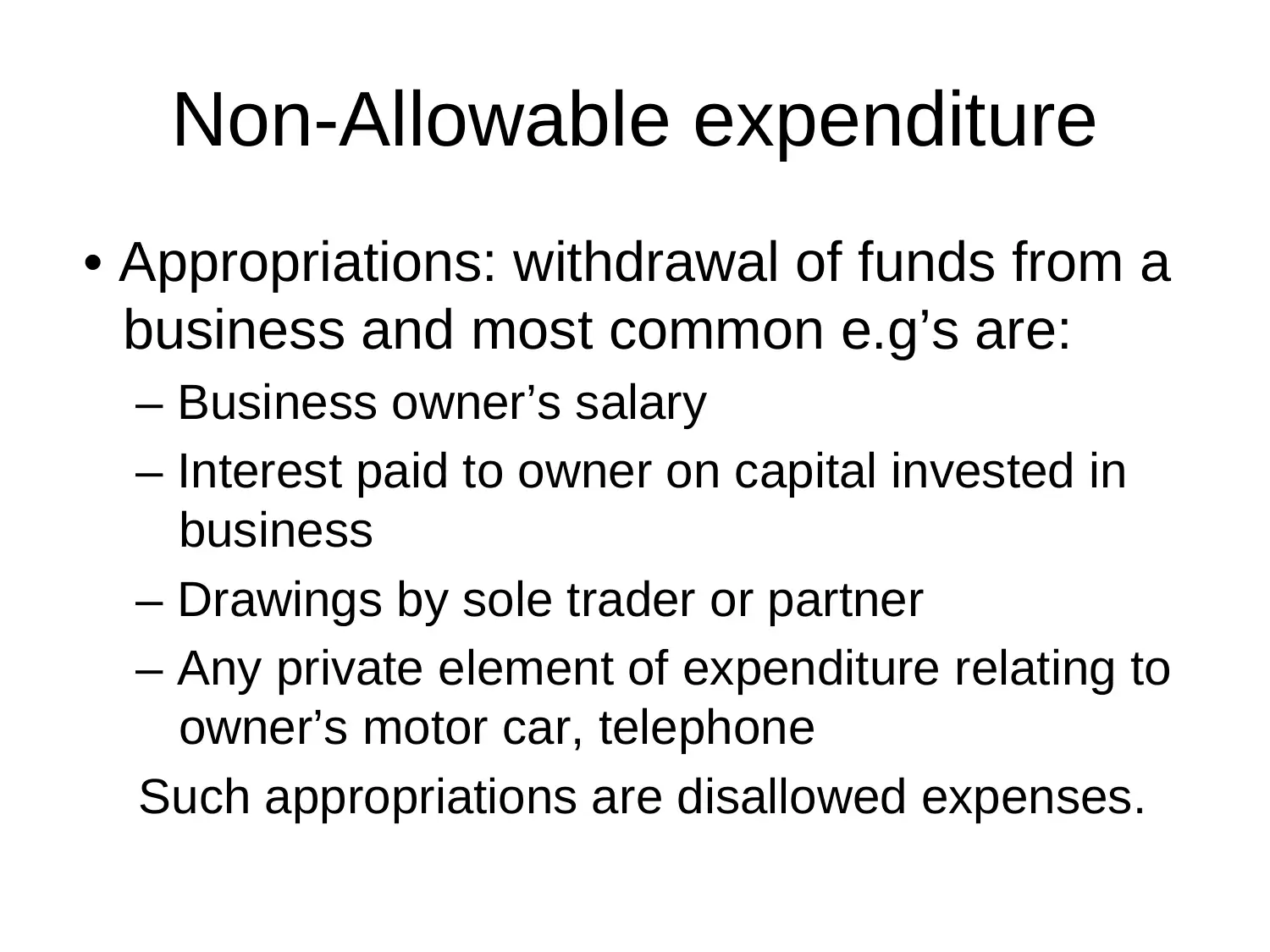

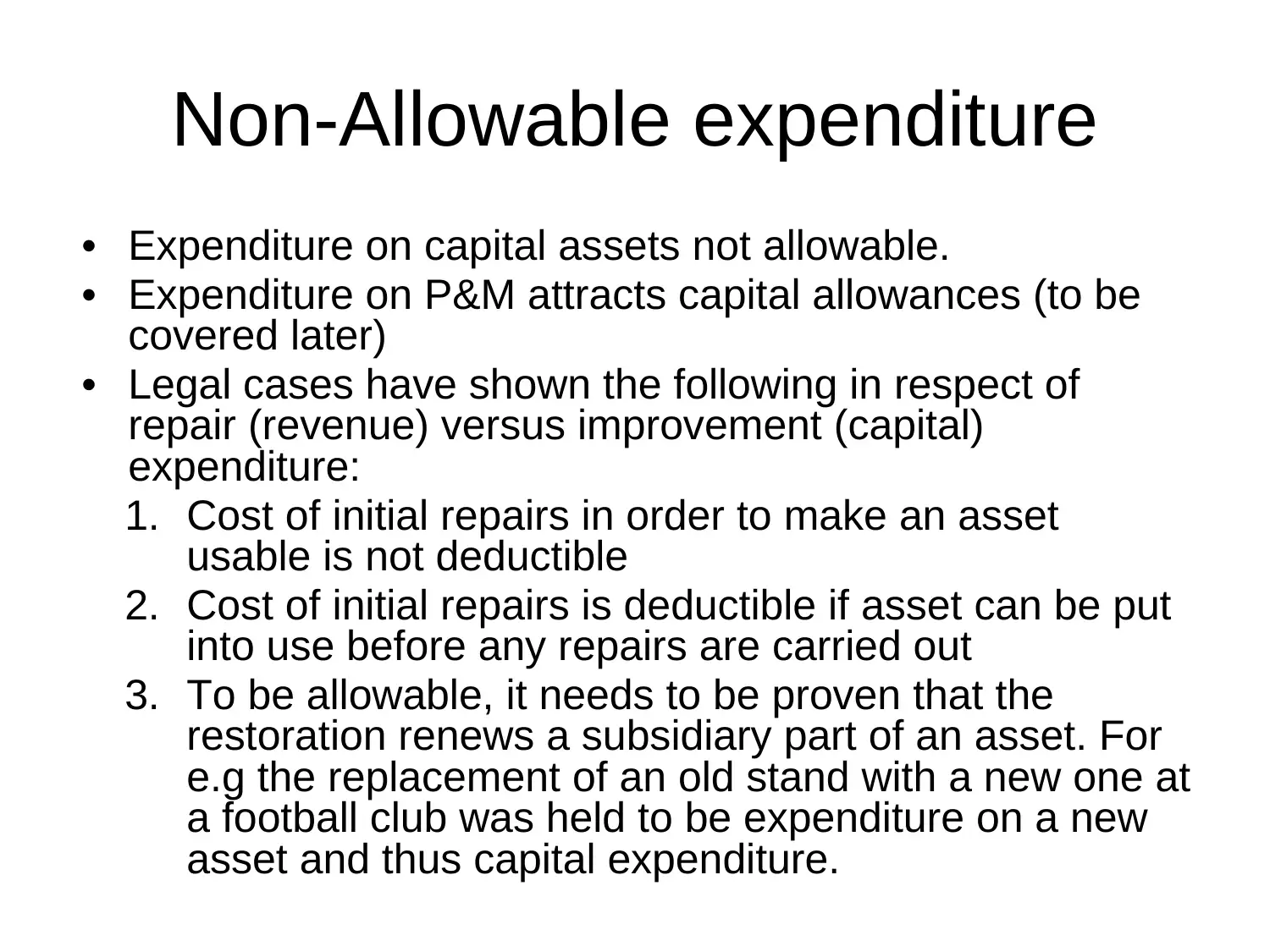

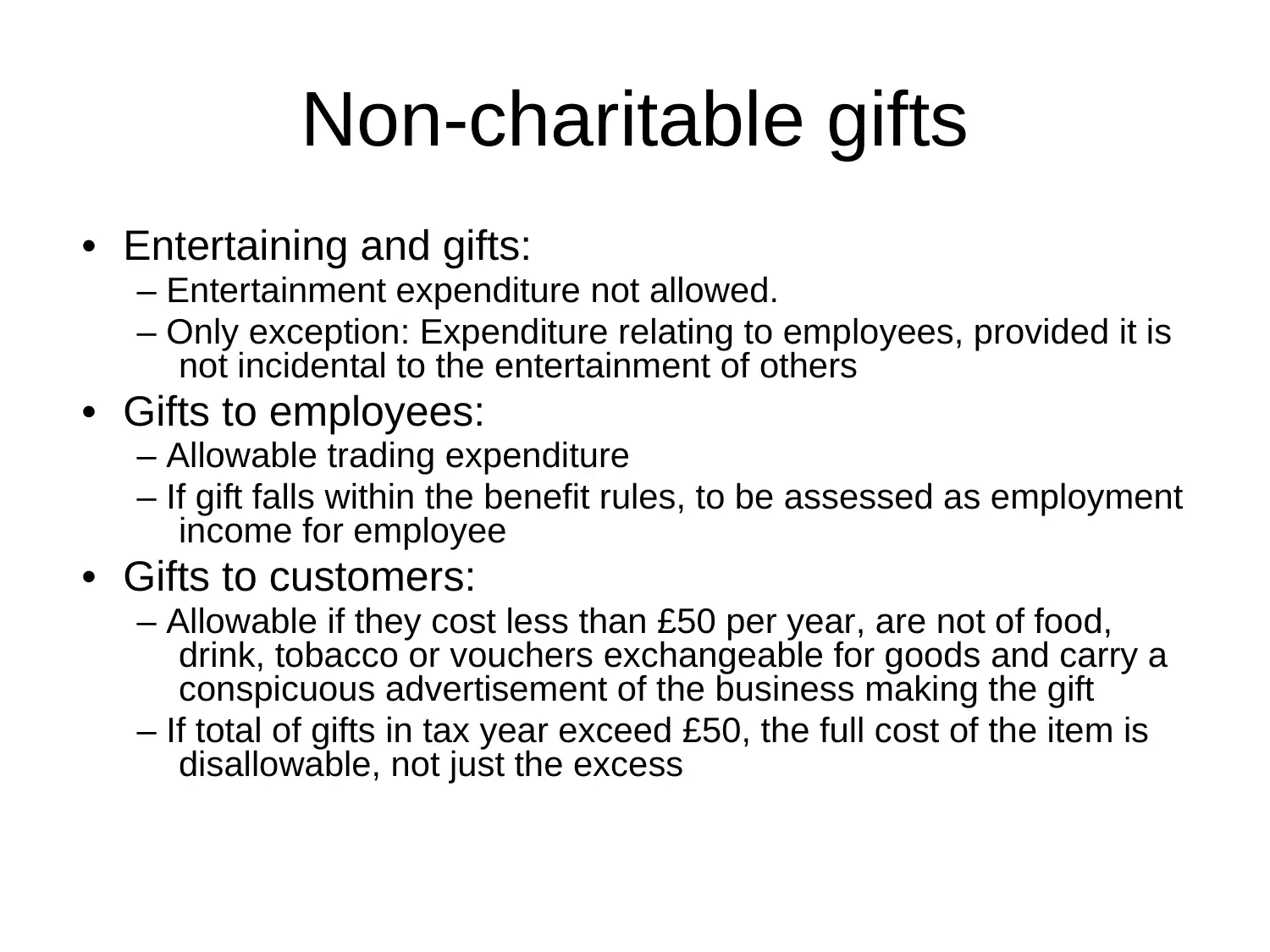

This document offers a detailed exploration of trading income, primarily focusing on the taxation of self-employed individuals or sole traders. It defines what constitutes a trade, referencing judicial decisions and the 'badges of trade' criteria established by the Royal Commission on the Taxation of Profits and Income, including the subject matter of the transaction, the length of ownership, frequency of transactions, supplementary work, circumstances of sale, motive, method of finance, and the existence of similar trading activities. The document also covers tax-adjusted trading profit, allowable and non-allowable expenditure, including items like subscriptions, charitable donations, appropriations, and capital assets. It delves into specific examples such as excessive salaries, interest, repairs versus improvements, and restrictions on car leasing costs based on CO2 emissions. The document provides practical examples and calculations to illustrate the application of these tax principles.

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.