Taxation Laws Assignment - Finance, Module XYZ, Semester 2

VerifiedAdded on 2020/04/01

|13

|2134

|50

Homework Assignment

AI Summary

This assignment solution addresses various aspects of Australian taxation laws. It begins with the valuation of trading stock, recommending the absorption costing method and considering relevant sections of the law. The assignment then delves into bad debt deductions, differentiating between allowable deductions and provisions for bad debts, referencing relevant case law. Further, it covers the implications of GST on the disposal of capital assets. The assignment also examines fringe benefits tax on loans to employees and associates, and capital gains tax implications for residents and non-residents selling assets. Finally, it analyses the capital gains or losses from the sale of shares. Each section cites relevant laws and applies them to the given scenarios, offering a comprehensive overview of the tax implications.

Running head: TAXATION LAWS

Taxation Laws

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Laws

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAWS

Table of Contents

Answer to question A:................................................................................................................2

Answer to question B:................................................................................................................3

Answer to question C:................................................................................................................5

Answer to question D:................................................................................................................6

Answer to question E:................................................................................................................7

Answer to question F:................................................................................................................8

Answer to question G:................................................................................................................9

Reference List:.........................................................................................................................11

Table of Contents

Answer to question A:................................................................................................................2

Answer to question B:................................................................................................................3

Answer to question C:................................................................................................................5

Answer to question D:................................................................................................................6

Answer to question E:................................................................................................................7

Answer to question F:................................................................................................................8

Answer to question G:................................................................................................................9

Reference List:.........................................................................................................................11

2TAXATION LAWS

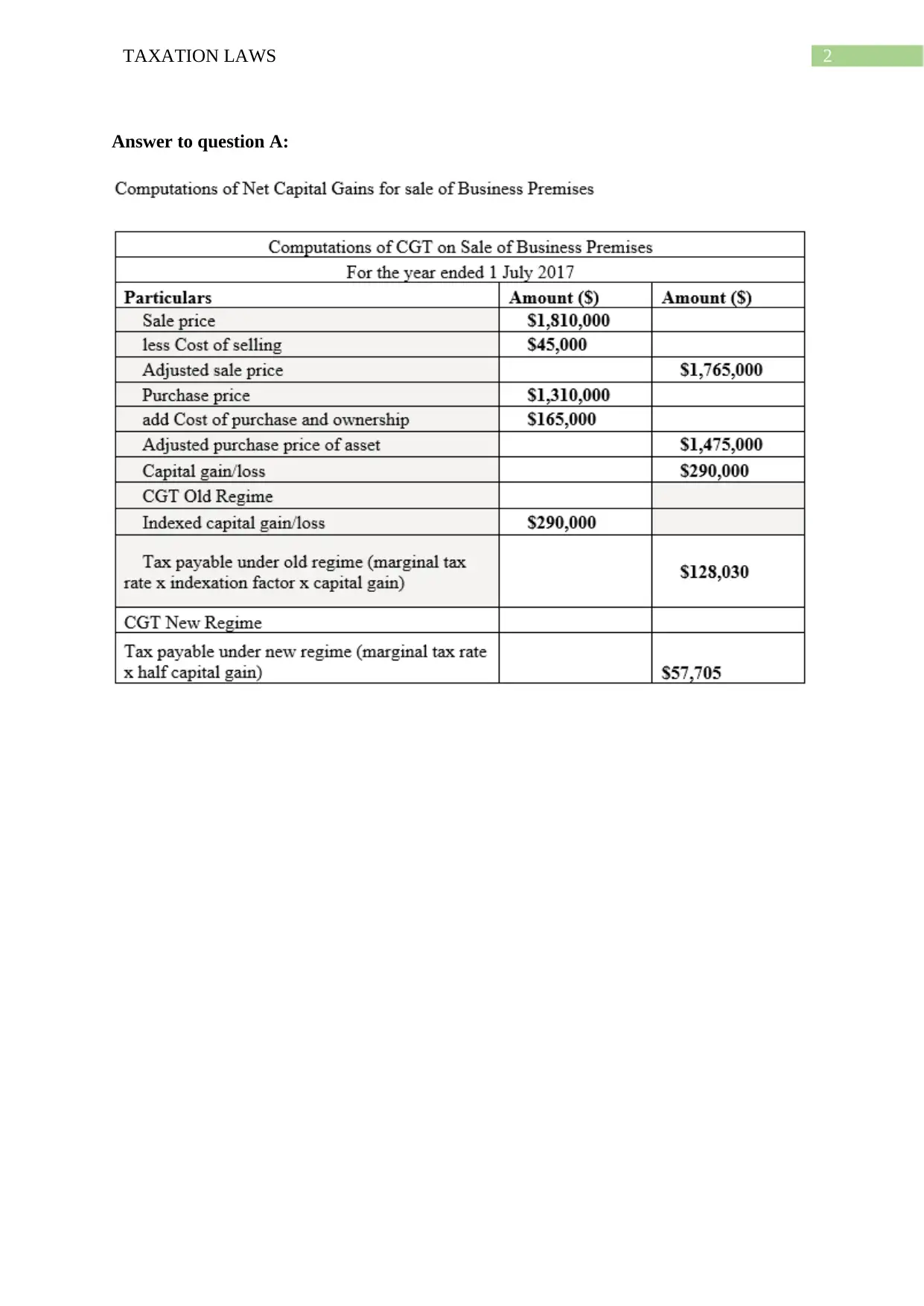

Answer to question A:

Answer to question A:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAWS

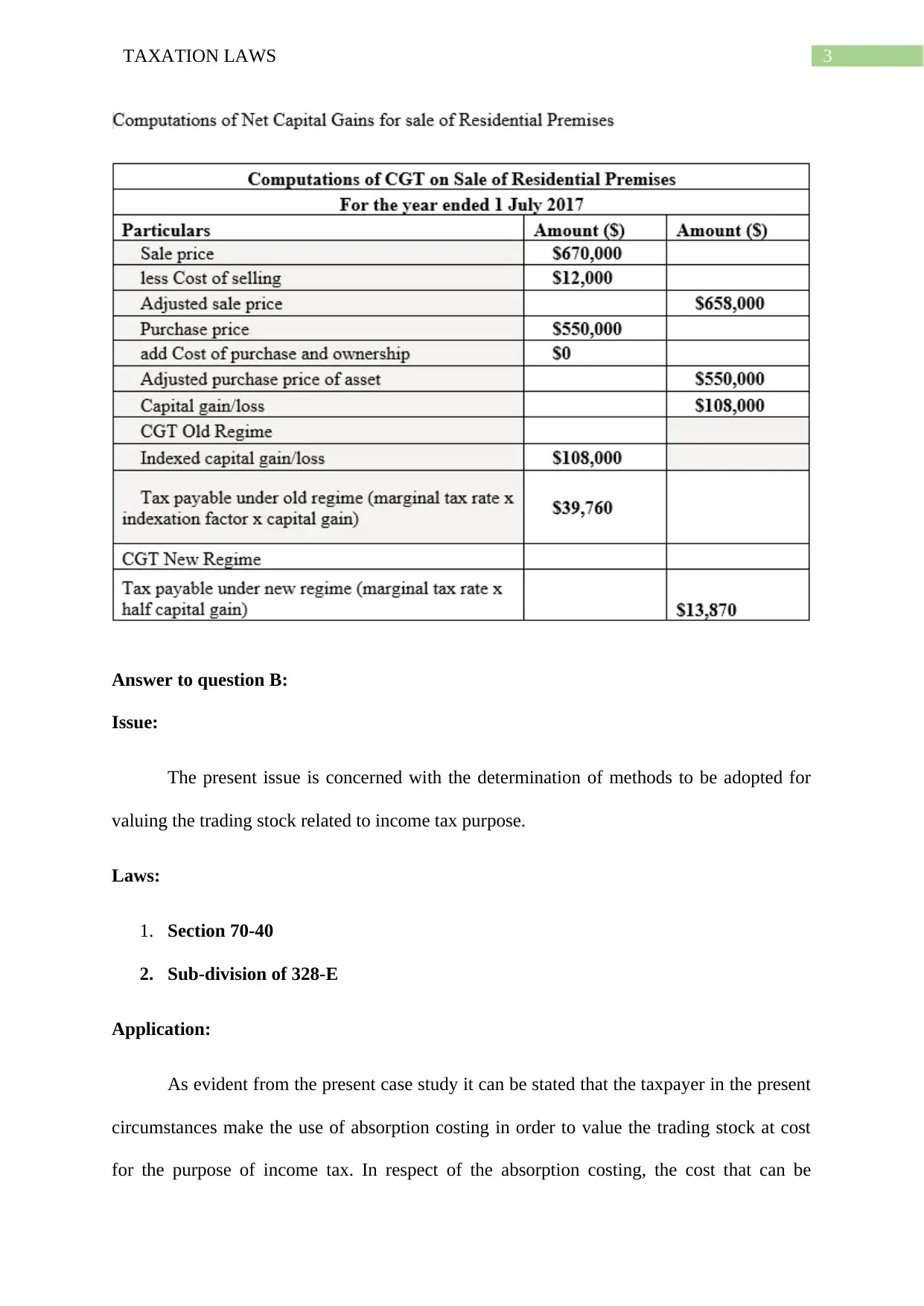

Answer to question B:

Issue:

The present issue is concerned with the determination of methods to be adopted for

valuing the trading stock related to income tax purpose.

Laws:

1. Section 70-40

2. Sub-division of 328-E

Application:

As evident from the present case study it can be stated that the taxpayer in the present

circumstances make the use of absorption costing in order to value the trading stock at cost

for the purpose of income tax. In respect of the absorption costing, the cost that can be

Answer to question B:

Issue:

The present issue is concerned with the determination of methods to be adopted for

valuing the trading stock related to income tax purpose.

Laws:

1. Section 70-40

2. Sub-division of 328-E

Application:

As evident from the present case study it can be stated that the taxpayer in the present

circumstances make the use of absorption costing in order to value the trading stock at cost

for the purpose of income tax. In respect of the absorption costing, the cost that can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAWS

absorbed relating to the income tax will be able to account for the cost involved in purchase

along with the direct and the indirect expenditure that has been incurred by the taxpayer

concerning the inventory (Barkoczy, 2016).

As defined under the “section 70-40” it is necessary to value the trading stock at the

beginning of the income year. The amount inventory that is in hand for the trading stock at

the beginning of the income year reflects the same amount which is considered in respect to

the “sub-division 328-E” upon the conclusion of the income year (Braithwaite, 2017). As

evident in the present case study of EEG, it is recommended that valuation of the trading

stock of inventory can be performed with the help of working out the cost at market selling

value of the inventory upon the conclusion of the year in which income is derived. It will be

beneficial in disregarding the sum relating to the input tax credit for which EEG is entitled at

the time of acquisition relating to the creditable purpose.

In addition to this, it is further recommended that EEG must take in to the account at

the beginning of the income year and EEG can subtract the exceeding sum of value at the

beginning of the income year over the sum upon the conclusion of the year in which income

is derived (Cao et al., 2015). The stock that has been ordered from Malaysia must be

accounted under the absorption method of costing since this will assist in including the cost

of purchase along with the direct and indirect cost that has been occurred concerning the

trading stock to its current location.

Conclusion:

Hence, it can be concluded that the trading stock must be valued under the method of

absorption costing, as this will help EEG in calcimining input tax credit.

absorbed relating to the income tax will be able to account for the cost involved in purchase

along with the direct and the indirect expenditure that has been incurred by the taxpayer

concerning the inventory (Barkoczy, 2016).

As defined under the “section 70-40” it is necessary to value the trading stock at the

beginning of the income year. The amount inventory that is in hand for the trading stock at

the beginning of the income year reflects the same amount which is considered in respect to

the “sub-division 328-E” upon the conclusion of the income year (Braithwaite, 2017). As

evident in the present case study of EEG, it is recommended that valuation of the trading

stock of inventory can be performed with the help of working out the cost at market selling

value of the inventory upon the conclusion of the year in which income is derived. It will be

beneficial in disregarding the sum relating to the input tax credit for which EEG is entitled at

the time of acquisition relating to the creditable purpose.

In addition to this, it is further recommended that EEG must take in to the account at

the beginning of the income year and EEG can subtract the exceeding sum of value at the

beginning of the income year over the sum upon the conclusion of the year in which income

is derived (Cao et al., 2015). The stock that has been ordered from Malaysia must be

accounted under the absorption method of costing since this will assist in including the cost

of purchase along with the direct and indirect cost that has been occurred concerning the

trading stock to its current location.

Conclusion:

Hence, it can be concluded that the trading stock must be valued under the method of

absorption costing, as this will help EEG in calcimining input tax credit.

5TAXATION LAWS

Answer to question C:

Issue

The current issue is based on the determination of whether the writing off the debt can

be regarded as the allowable deductions.

Laws:

1. “section 63”

2. “Crane Sales Pty Ltd v F C of T (1971)”

3. “Anderson and Halstead Ltd v. Birrell (1932)”,

4. “Subsection 705-70 (1)”

Application:

The bad debt must be written off in the year in which the income is derived before

considering the bad debt deductions will be considered as the allowable deductions under

section 63. The judgement passed in the case of “Crane Sales Pty Ltd v F C of T (1971)” a

debt will be viewed as the bad debt where the amount cannot be recovered or in

circumstances where and individual taxpayer has equitable entitlement to the debt (Saad,

2014). In the current context of EEG bad debt written off would be allowed as the allowable

deductions for income tax purpose.

In addition to this, it can be stated that provision for bad debt would not be treated as

the allowable deductions. To consider the provision as the allowable deductions the bad debt

must be more than simply doubtful. Furthermore, there are certain conditions that requires to

be fulfilled. As held in the case of “Anderson and Halstead Ltd v. Birrell (1932)” no

claims relating to provision for doubtful debt would be considered as allowable deductions

Answer to question C:

Issue

The current issue is based on the determination of whether the writing off the debt can

be regarded as the allowable deductions.

Laws:

1. “section 63”

2. “Crane Sales Pty Ltd v F C of T (1971)”

3. “Anderson and Halstead Ltd v. Birrell (1932)”,

4. “Subsection 705-70 (1)”

Application:

The bad debt must be written off in the year in which the income is derived before

considering the bad debt deductions will be considered as the allowable deductions under

section 63. The judgement passed in the case of “Crane Sales Pty Ltd v F C of T (1971)” a

debt will be viewed as the bad debt where the amount cannot be recovered or in

circumstances where and individual taxpayer has equitable entitlement to the debt (Saad,

2014). In the current context of EEG bad debt written off would be allowed as the allowable

deductions for income tax purpose.

In addition to this, it can be stated that provision for bad debt would not be treated as

the allowable deductions. To consider the provision as the allowable deductions the bad debt

must be more than simply doubtful. Furthermore, there are certain conditions that requires to

be fulfilled. As held in the case of “Anderson and Halstead Ltd v. Birrell (1932)” no

claims relating to provision for doubtful debt would be considered as allowable deductions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAWS

(Lang, 2014). As evident in the current scenario of EEG provision for bad debt cannot be

regarded as the merely bad just because the time has passed with being the payment received.

On the other hand, the employee yearly leave is regarded as the accounting liability

cannot be regarded as the allowable deductions in the year in which it accrues. In regard to

“Subsection 705-70 (1)” employee annual leave is an accounting liability and would not be

allowed for allowable deductions (Miller & Oats, 2016).

Conclusion:

The analysis can be concluded by stating that bad debt written off would qualify as

deductions but the provision for bad debt and employee annual leave cannot be claimed as

allowable deductions.

Answer to question D:

Issue:

The present issue is based on the disposal of capital asset and the determination of

GST under the new tax system of GST Act 1999.

Laws:

1. “Goods and Service Tax Act 1999”

Application:

Capital asset is viewed as that asset that is retained by a commercial entity for

generating income. As defined by the Australian taxation office, a person transferring or

selling the capital asset with registered business or required to be registered for the purpose of

GST it would be treated as the assessable sale and the individual taxpayer is required to

(Lang, 2014). As evident in the current scenario of EEG provision for bad debt cannot be

regarded as the merely bad just because the time has passed with being the payment received.

On the other hand, the employee yearly leave is regarded as the accounting liability

cannot be regarded as the allowable deductions in the year in which it accrues. In regard to

“Subsection 705-70 (1)” employee annual leave is an accounting liability and would not be

allowed for allowable deductions (Miller & Oats, 2016).

Conclusion:

The analysis can be concluded by stating that bad debt written off would qualify as

deductions but the provision for bad debt and employee annual leave cannot be claimed as

allowable deductions.

Answer to question D:

Issue:

The present issue is based on the disposal of capital asset and the determination of

GST under the new tax system of GST Act 1999.

Laws:

1. “Goods and Service Tax Act 1999”

Application:

Capital asset is viewed as that asset that is retained by a commercial entity for

generating income. As defined by the Australian taxation office, a person transferring or

selling the capital asset with registered business or required to be registered for the purpose of

GST it would be treated as the assessable sale and the individual taxpayer is required to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAWS

record the GST relating to the sale (Woellner et al., 2016). As evident in the current situation

of EEG, an assertion can be bought forward that the sum that is generated from the sale of the

asset would be regarded as the assessable sale of capital asset that will be liable for GST

under the new tax system of “Goods and Service Tax Act 1999”. In addition to this, EEG

will be additionally required to account for the sum received in business activity statement for

the current tax year.

Conclusion:

The discussion conducted above can be concluded by stating that sale of capital asset

by EEG would be taxable under the “GST Act of 1999”.

Answer to question E:

Issue:

The present issue is based on the determination of the fringe benefit of loan made to

an associate or an employee under the Fringe Benefit Act 1986.

Laws:

1. “Fringe Benefit Tax Assessment Act 1986”

2. “Division 7 A”

Application:

Any form of loan made to the associate as the employee or an associate that is an

employee of the private company would result in fringe benefit tax given the fact that such

kind of loan is in compliance with the complying loan. Nevertheless, loans are generally not

subjected to Division 7A and will be treated as the loan fringe benefit under the “Fringe

Benefit Tax Assessment Act 1986” (Robin, 2017). The loan undertaken by Mrs Smith in the

record the GST relating to the sale (Woellner et al., 2016). As evident in the current situation

of EEG, an assertion can be bought forward that the sum that is generated from the sale of the

asset would be regarded as the assessable sale of capital asset that will be liable for GST

under the new tax system of “Goods and Service Tax Act 1999”. In addition to this, EEG

will be additionally required to account for the sum received in business activity statement for

the current tax year.

Conclusion:

The discussion conducted above can be concluded by stating that sale of capital asset

by EEG would be taxable under the “GST Act of 1999”.

Answer to question E:

Issue:

The present issue is based on the determination of the fringe benefit of loan made to

an associate or an employee under the Fringe Benefit Act 1986.

Laws:

1. “Fringe Benefit Tax Assessment Act 1986”

2. “Division 7 A”

Application:

Any form of loan made to the associate as the employee or an associate that is an

employee of the private company would result in fringe benefit tax given the fact that such

kind of loan is in compliance with the complying loan. Nevertheless, loans are generally not

subjected to Division 7A and will be treated as the loan fringe benefit under the “Fringe

Benefit Tax Assessment Act 1986” (Robin, 2017). The loan undertaken by Mrs Smith in the

8TAXATION LAWS

current scenario it can be stated that loan Fringe Benefit is applicable under the “Fringe

Benefit Tax Assessment Act 1986”.

In contrary to the situation, it has been noticed that motor vehicle was also sold by

Mrs Smith that can be regarded as the selling of capital asset that was held for the purpose of

long term investment to derive revenue. The disposal of motor vehicle is a capital asset and

would be treated as the taxable sale under the GST supplies that is derived during sale.

Conclusion:

The above stated analysis can be concluded by stating the loan taken by Mrs Smith

will be treated as Fringe benefit and will be liable for tax. Additionally, sale of capital asset

would be treated as GST supplies.

Answer to question F:

Issue:

The present issue is based on the determination of Capital gains for the sale of

property in Australia by the taxpayer.

Laws:

1. “Section 108-10 of the Income Tax Assessment Act 1997”

Application:

A person leaving Australia permanently and disposing off the asset would be

considered for tax under the “Section 108-10 of the Income Tax Assessment Act 1997”

(Barkoczy et al., 2016). This evidently puts forward that a person selling off their asset would

be held liable for taxation purpose under the “Section 108-10 of the Income Tax

Assessment Act 1997”for the capital gains made. In addition to this, an individual is required

to account for the sum derived as the capital gains or loss in the taxable return and pay tax on

current scenario it can be stated that loan Fringe Benefit is applicable under the “Fringe

Benefit Tax Assessment Act 1986”.

In contrary to the situation, it has been noticed that motor vehicle was also sold by

Mrs Smith that can be regarded as the selling of capital asset that was held for the purpose of

long term investment to derive revenue. The disposal of motor vehicle is a capital asset and

would be treated as the taxable sale under the GST supplies that is derived during sale.

Conclusion:

The above stated analysis can be concluded by stating the loan taken by Mrs Smith

will be treated as Fringe benefit and will be liable for tax. Additionally, sale of capital asset

would be treated as GST supplies.

Answer to question F:

Issue:

The present issue is based on the determination of Capital gains for the sale of

property in Australia by the taxpayer.

Laws:

1. “Section 108-10 of the Income Tax Assessment Act 1997”

Application:

A person leaving Australia permanently and disposing off the asset would be

considered for tax under the “Section 108-10 of the Income Tax Assessment Act 1997”

(Barkoczy et al., 2016). This evidently puts forward that a person selling off their asset would

be held liable for taxation purpose under the “Section 108-10 of the Income Tax

Assessment Act 1997”for the capital gains made. In addition to this, an individual is required

to account for the sum derived as the capital gains or loss in the taxable return and pay tax on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAWS

their assessable gains (Roe, 2017). In respect of the current situation of Mr and Mrs Smith

they would be treated as the foreign resident for leaving Australian and shifting to New

Zealand. This would ultimately result in cessation of their Australian resident and the sale of

asset made by them would be treated as the capital gains which would be liable for

assessment under “Section 108-10 of the Income Tax Assessment Act 1997”.

Conclusion:

It can be concluded that both Mr and Mrs would not be treated as the Australian

resident since they moved to New Zealand permanently and the sale of asset would be held

liable for taxation purpose.

Answer to question G:

Issue:

The present issue is based on the determination of the capital gains or losses from the

sale of shares.

Laws:

“Section 110-20 of the ITAA 1997”

Application:

As defined by the Australian taxation office, an individual taxpayer selling capital

asset and deriving gains from such would be treated for assessment for the gains derived

(Tran-Nam & Walpole, 2016). The sale of shares in this context by Mr Smith represents

capital gains and would be treated for basement under “Section 110-20 of the ITAA 1997”.

Conclusion:

their assessable gains (Roe, 2017). In respect of the current situation of Mr and Mrs Smith

they would be treated as the foreign resident for leaving Australian and shifting to New

Zealand. This would ultimately result in cessation of their Australian resident and the sale of

asset made by them would be treated as the capital gains which would be liable for

assessment under “Section 108-10 of the Income Tax Assessment Act 1997”.

Conclusion:

It can be concluded that both Mr and Mrs would not be treated as the Australian

resident since they moved to New Zealand permanently and the sale of asset would be held

liable for taxation purpose.

Answer to question G:

Issue:

The present issue is based on the determination of the capital gains or losses from the

sale of shares.

Laws:

“Section 110-20 of the ITAA 1997”

Application:

As defined by the Australian taxation office, an individual taxpayer selling capital

asset and deriving gains from such would be treated for assessment for the gains derived

(Tran-Nam & Walpole, 2016). The sale of shares in this context by Mr Smith represents

capital gains and would be treated for basement under “Section 110-20 of the ITAA 1997”.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAWS

In compliance with “Section 110-20 of the ITAA 1997”, Mr Smith would be liable

for tax on the capital gains made from the sale of shares.

In compliance with “Section 110-20 of the ITAA 1997”, Mr Smith would be liable

for tax on the capital gains made from the sale of shares.

11TAXATION LAWS

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K., & Richardson, G. (2016). Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag

GmbH.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Roe, A. (2017). The doctrine of sham in Australian taxation law. AUSTRALIAN TAX

REVIEW, 46(2), 99-119.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Tran-Nam, B., & Walpole, M. (2016). Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), 319.

Woellner, R. H., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K., & Richardson, G. (2016). Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Lang, M. (2014). Introduction to the law of double taxation conventions. Linde Verlag

GmbH.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Roe, A. (2017). The doctrine of sham in Australian taxation law. AUSTRALIAN TAX

REVIEW, 46(2), 99-119.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Tran-Nam, B., & Walpole, M. (2016). Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), 319.

Woellner, R. H., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.