Management Accounting Report: A Comparison of Costing Systems

VerifiedAdded on 2021/06/18

|15

|2683

|127

Report

AI Summary

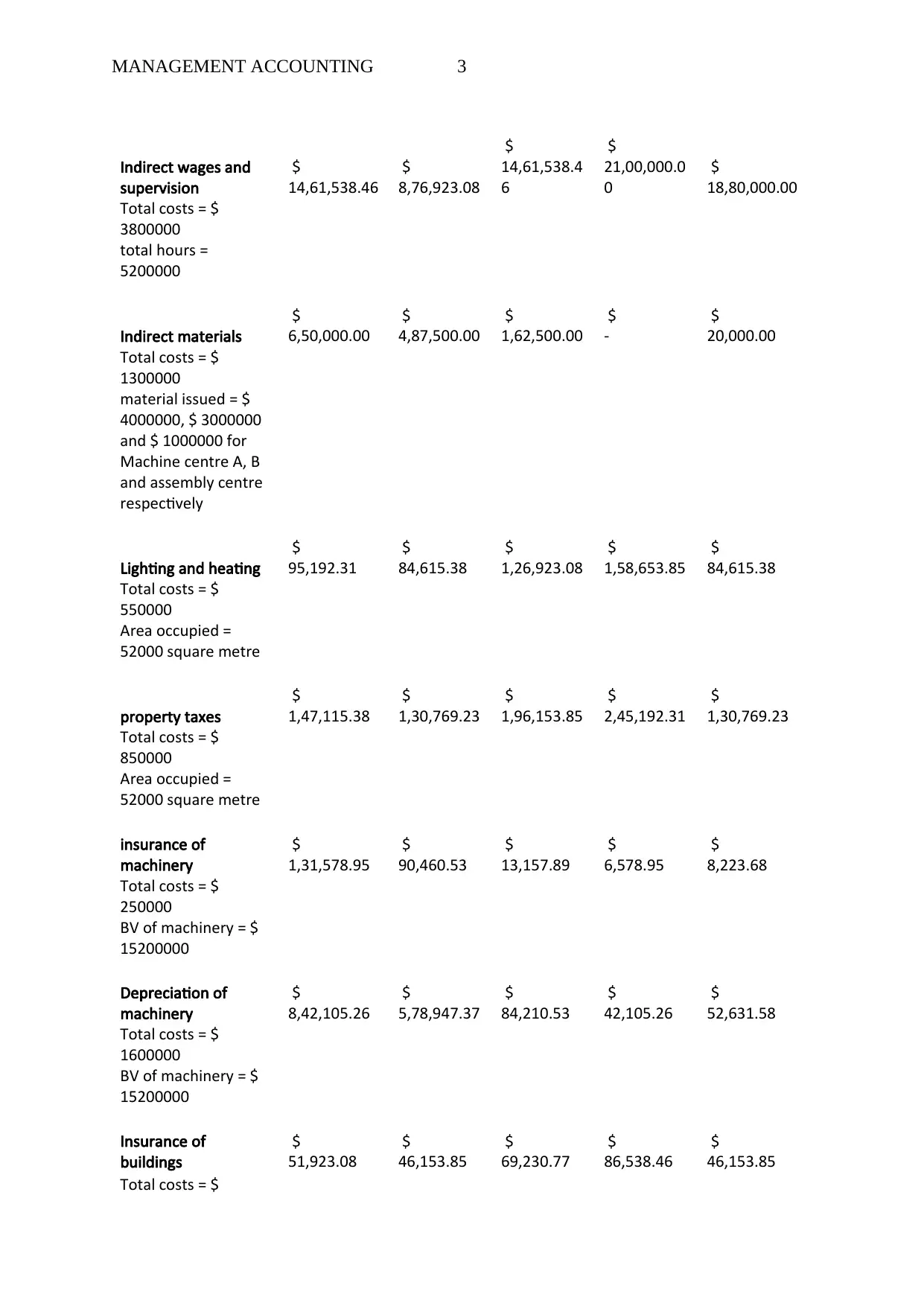

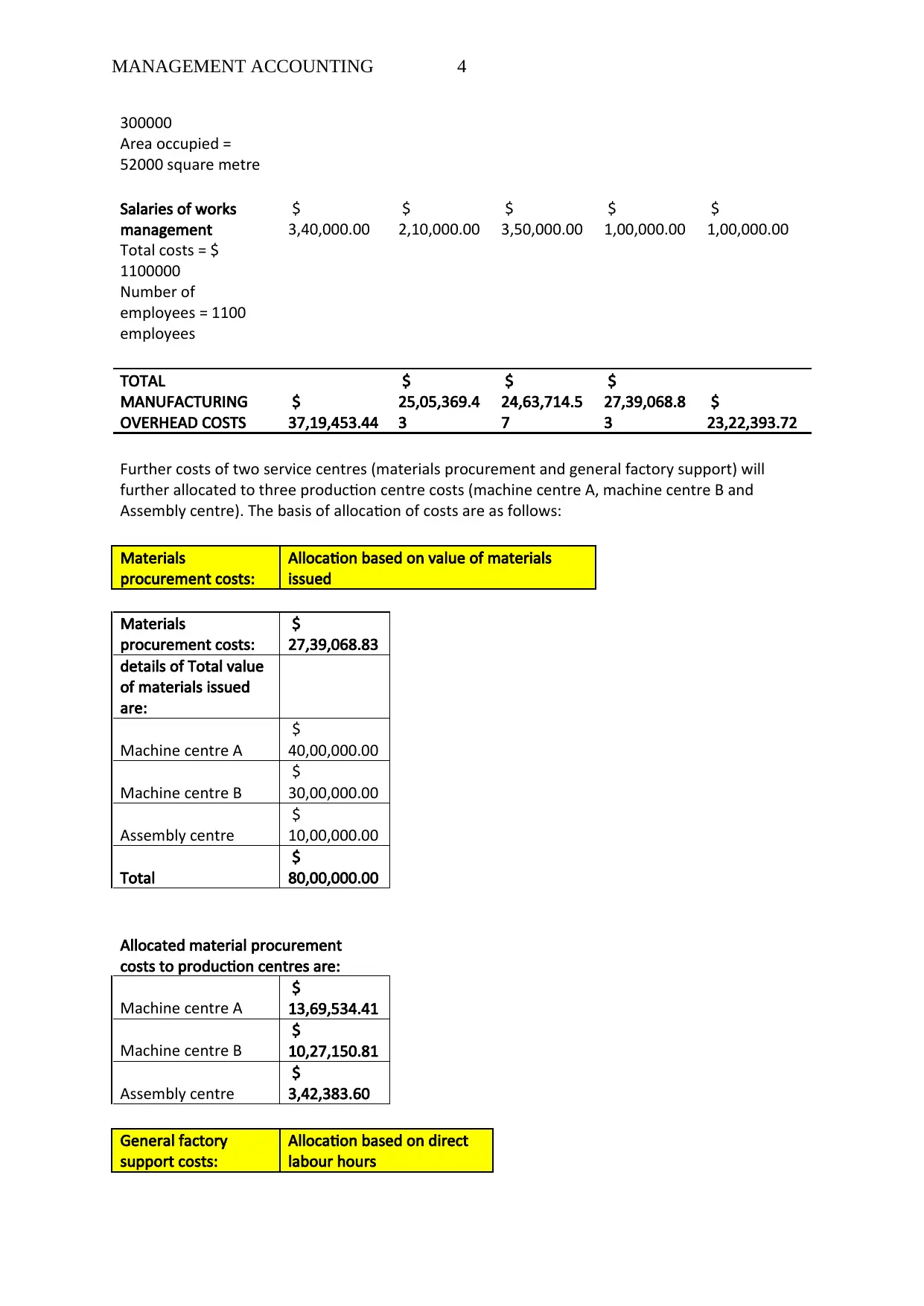

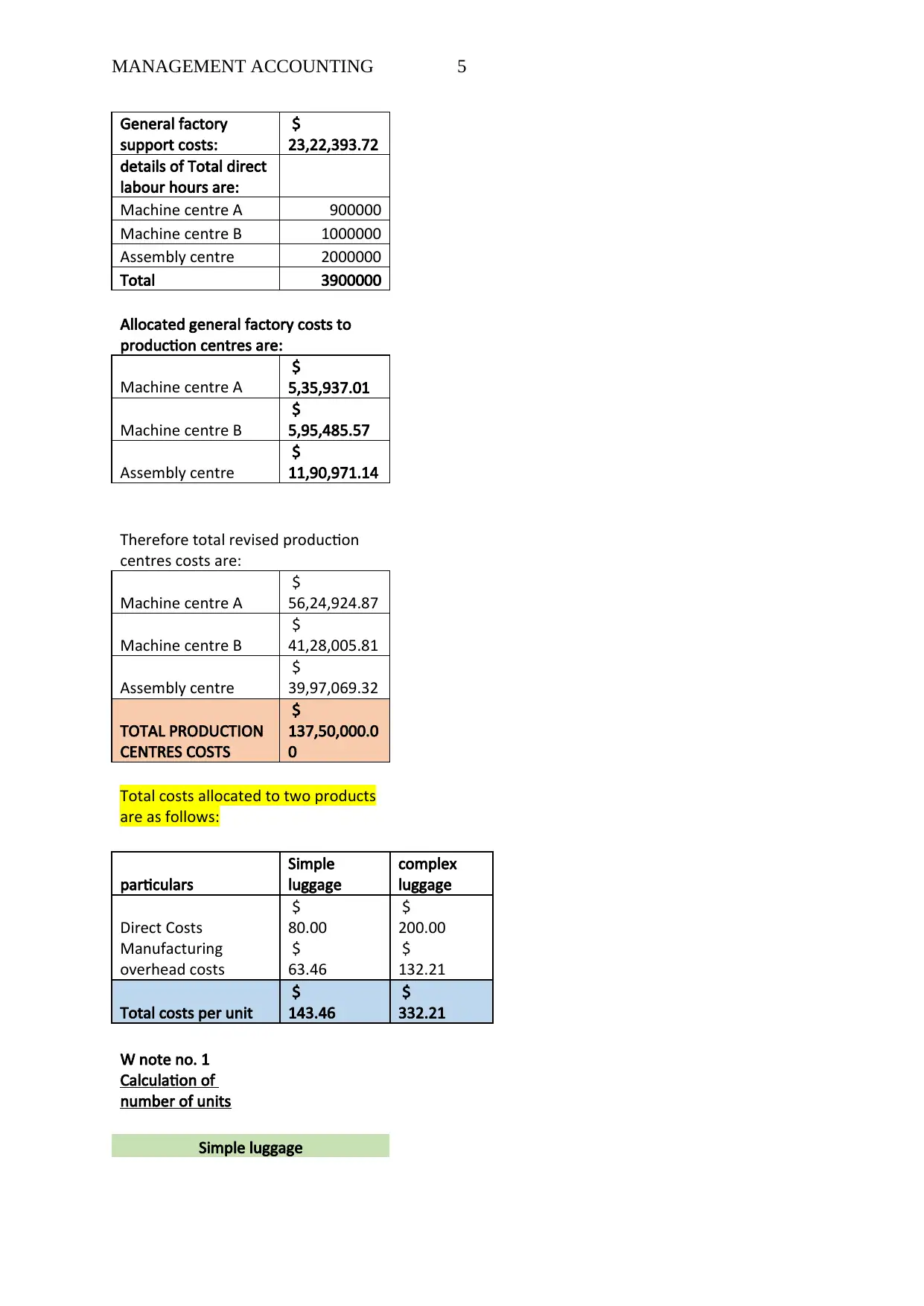

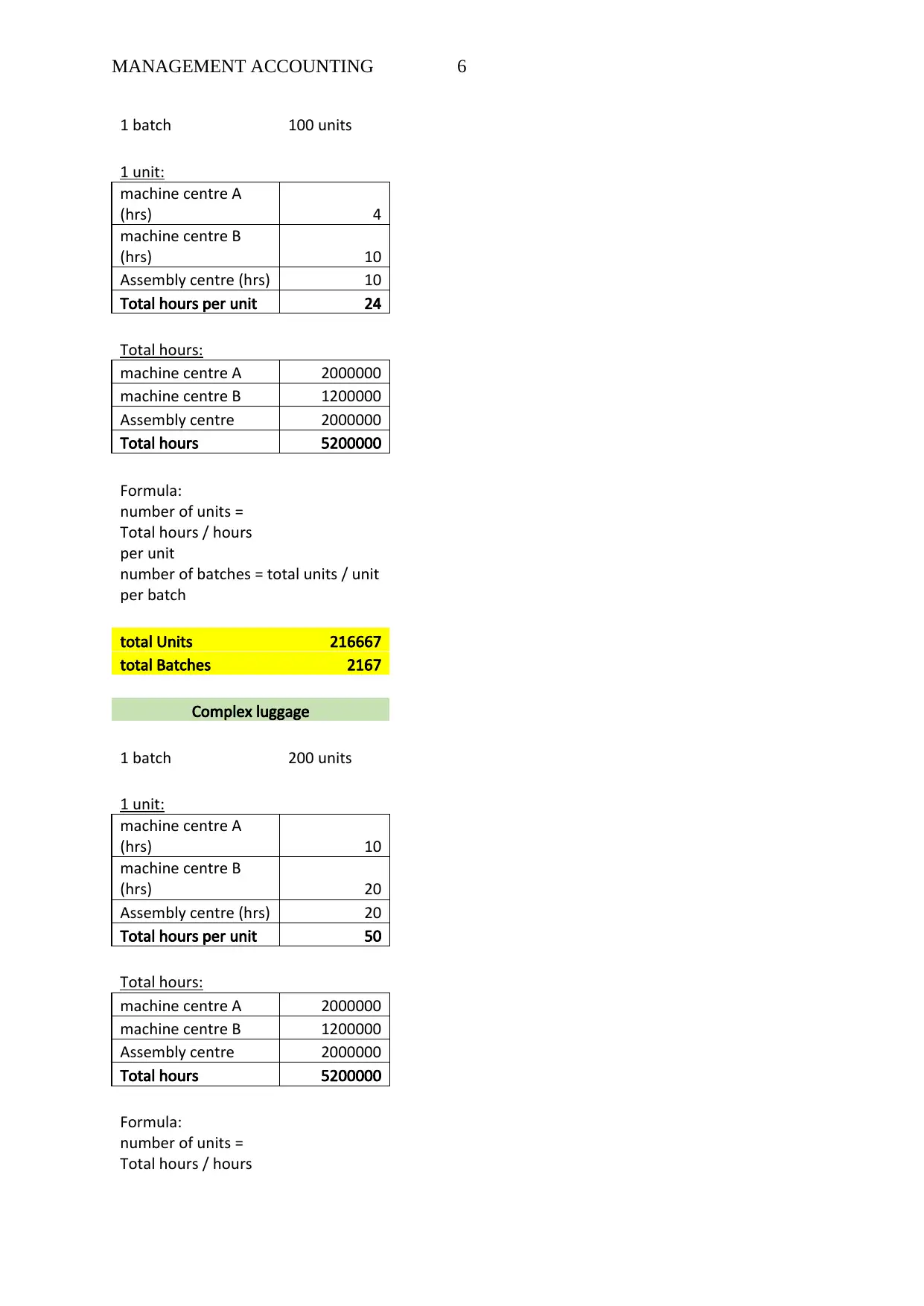

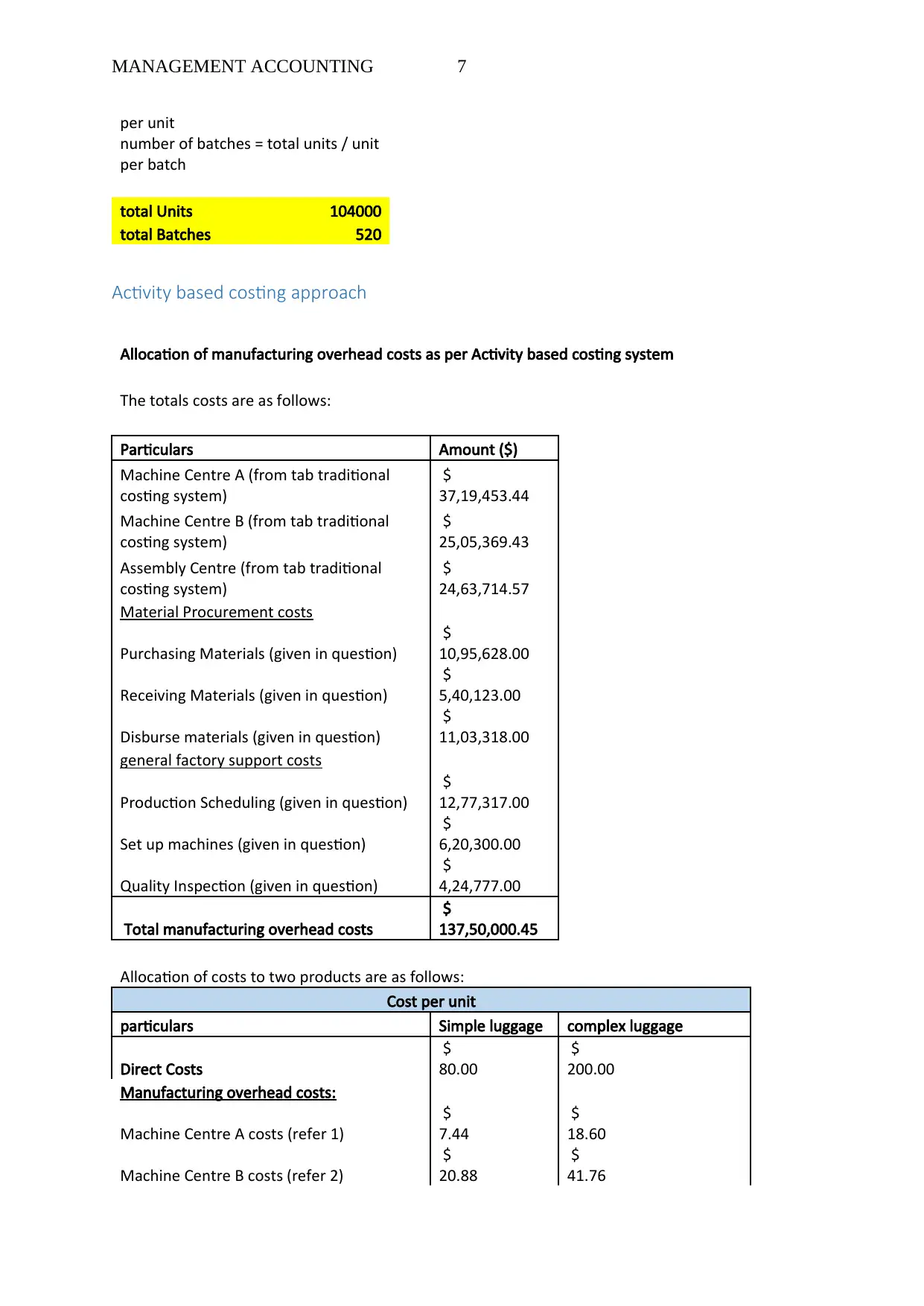

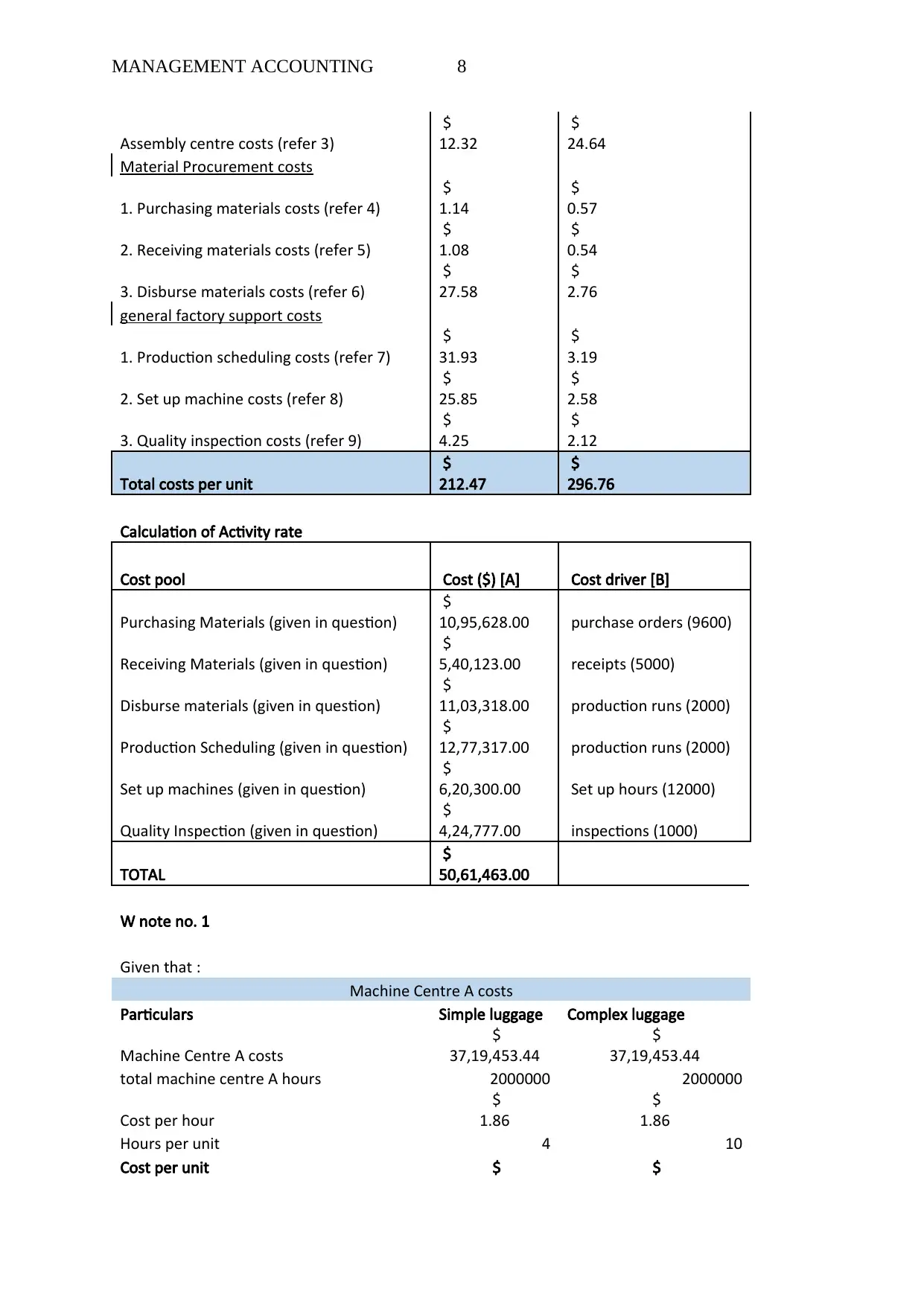

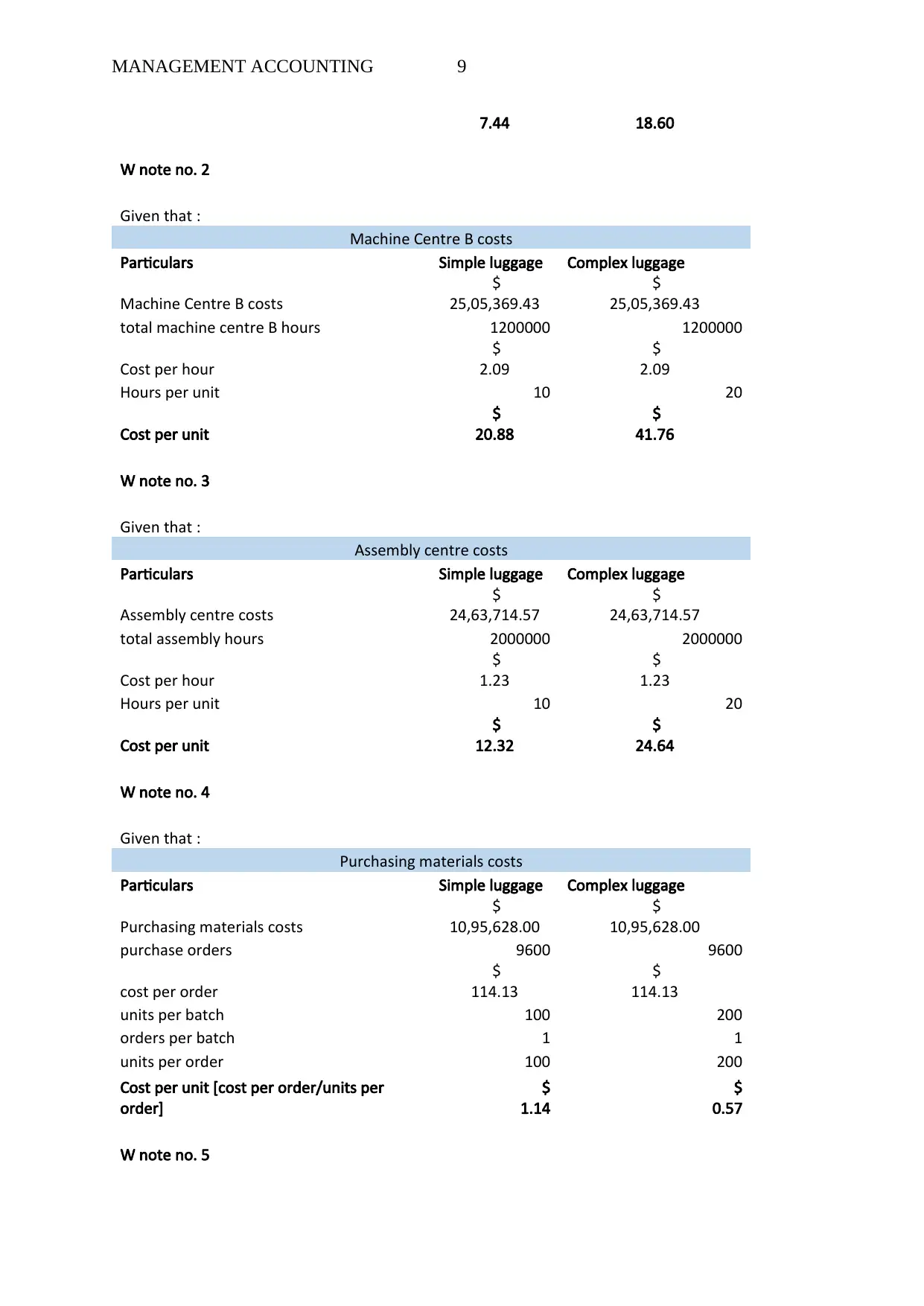

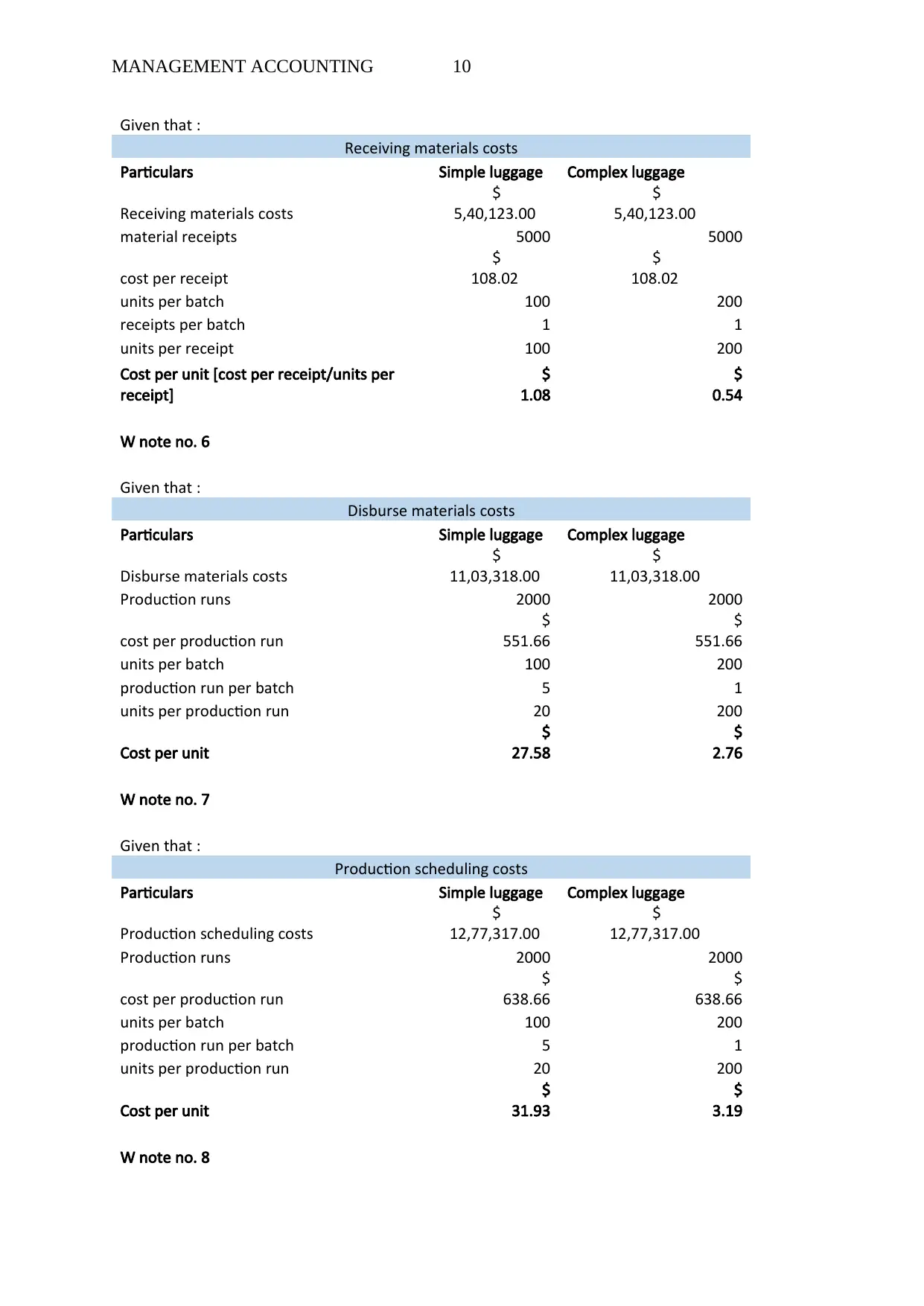

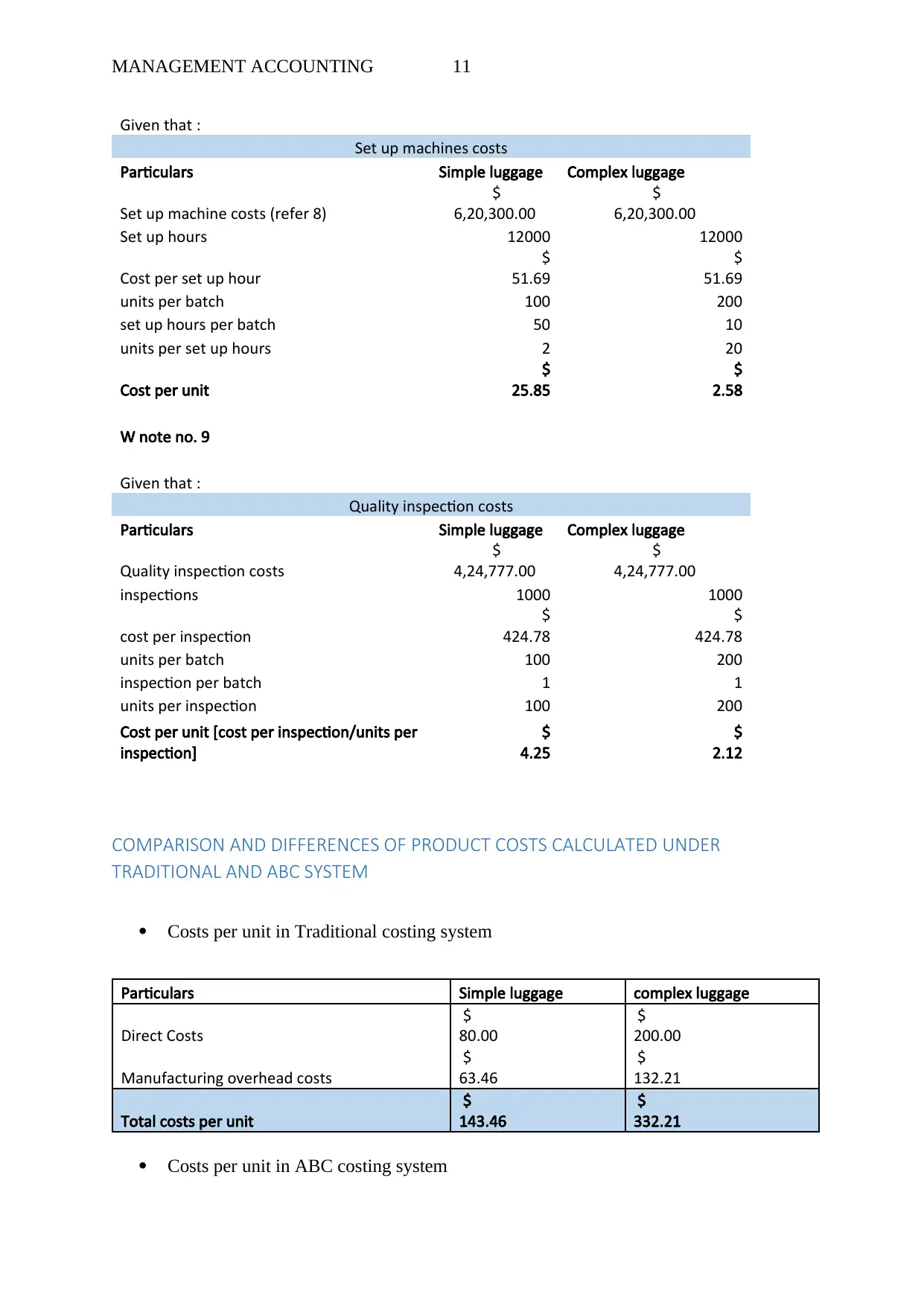

This report analyzes the application of traditional and activity-based costing (ABC) methods within the context of Happy Traveller Ltd., a manufacturing company producing simple and complex luggage. The report's purpose is to compare the two costing approaches, highlighting their significance and calculating the cost per unit for each product under both systems. The traditional costing approach uses a single overhead rate, while ABC assigns costs based on multiple cost drivers. The report details the allocation of manufacturing overhead costs, including indirect wages, materials, and facility expenses, across various production and service centers. It then compares the resulting cost per unit for simple and complex luggage under both systems, showing how the ABC method provides a more detailed and potentially more accurate cost allocation. The analysis also considers the costs and benefits of adopting ABC, concluding with an overview of other relevant factors influencing the choice of costing method.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.