Costing Methods: Comparative Analysis of Traditional and ABC Costing

VerifiedAdded on 2023/05/27

|10

|1966

|67

Report

AI Summary

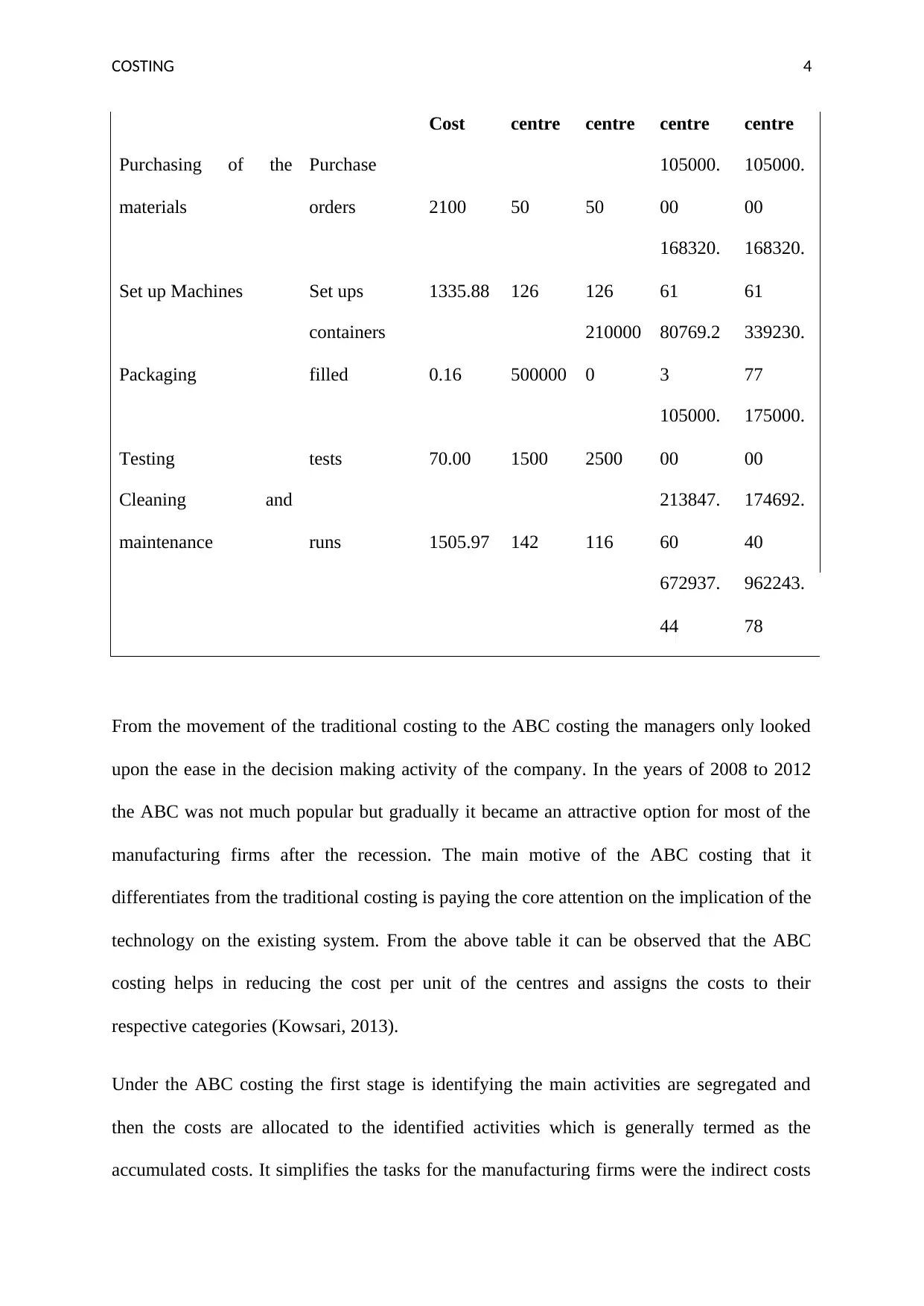

This report provides a comprehensive comparison of traditional and Activity-Based Costing (ABC) methods. It begins by outlining the disadvantages of traditional costing, highlighting its limitations in providing non-financial information, its reliance on single overhead pools, and its inability to adapt to modern manufacturing environments. The report then contrasts traditional and ABC costing through a detailed example, illustrating how ABC allocates costs based on activities and cost drivers, leading to more accurate cost assignments. The analysis further explores the reasons for the shift from traditional to ABC costing, emphasizing the shortcomings of traditional methods in representing cost information and the influence of Cooper and Kaplan's work. The report concludes by examining the inability of traditional costing to account for product diversity, volume diversity, and product complexity, underscoring the need for the more refined and adaptable ABC approach in contemporary business environments.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.