Transfer Pricing Strategy for Cameco Corporation - Case Study Analysis

VerifiedAdded on 2023/06/09

|18

|3259

|71

Case Study

AI Summary

This case study examines the transfer pricing challenges faced by Cameco Corporation in 1999, focusing on the agreement with its subsidiary, Cameco Europe Limited. The assignment analyzes the problem of determining the most appropriate transfer pricing agreement to mitigate tax risks and potential disputes. It explores three alternatives: variable contract pricing, advance pricing agreements (APA), and commissionaire arrangements. The analysis includes a detailed impact assessment on stakeholders and evaluates the alternatives based on reduced litigation, cost-effectiveness, and ease of implementation. The study recommends the best alternative and provides a detailed action plan for its execution, emphasizing the importance of transfer pricing in international business and its impact on corporate image, shareholders, and government revenue. The case underscores the significance of the arm's length principle and the benefits of proactive transfer pricing strategies in avoiding future tax disputes and financial losses.

ASSIGNMENTTRANSFER PRICING ANALYSIS –

BENCHMARKING & ADVANCE PRICING AGREEMENT

1

BENCHMARKING & ADVANCE PRICING AGREEMENT

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

I

TA

TA

Executive Summary..............................................................................3

Introduction..........................................................................................5

Identification of problem......................................................................6

Analysis of problem..............................................................................7

Possible Alternatives............................................................................8

Impact Analysis...................................................................................11

Criteria for Evaluation of Alternatives................................................12

Evaluation of Alternatives..................................................................13

Uncertainities involved.......................................................................15

Analysis of the best alternative..........................................................16

Action Plan..........................................................................................17

Bibliography........................................................................................18

2

TA

TA

Executive Summary..............................................................................3

Introduction..........................................................................................5

Identification of problem......................................................................6

Analysis of problem..............................................................................7

Possible Alternatives............................................................................8

Impact Analysis...................................................................................11

Criteria for Evaluation of Alternatives................................................12

Evaluation of Alternatives..................................................................13

Uncertainities involved.......................................................................15

Analysis of the best alternative..........................................................16

Action Plan..........................................................................................17

Bibliography........................................................................................18

2

Executive Summary

Cameco is proposing to enter into marketing agreement1 with Cameco Europe Limited,

Switzerland (wholly owned subsidiary) for marketing its good in Europe. The transaction

falls within the purview of transfer pricing as the said transactions is between two associated

enterprises as the ownership exceeds 26%. The management of the company is seeking to

explore the terms of the agreement in order to mitigate any tax disputes or levy of penalty in

near term or long term. In this regard, various alternatives have been explored to determine

the terms of agreement. (Transfer Pricing, 2018) The alternatives have been detailed here-in-

under:

(a) Alternative-1-Variable Contract Pricing: Under this alternative, the company can decide

on terms and condition of transfer of goods to Cameco Europe Limited at the rate

prevalent in the market i.e. goods are sold at spot price (External CUP).

(b) Alternative-2-Advance Pricing Agreement: Cameco Group can enter into an agreement

with Tax Authorities of both jurisdictions whereby they agree to the terms and transfer

price of goods beforehand and transact.

(c) Alternative-3-Commissionaire Arrangement: Under this alternative, company can enter

into an commissionaire arrangement whereby a fixed commission is paid to Cameco

Europe Limited, Switzerland for its marketing service rendered. The rate of service shall

be determined on the basis of Functions Performed, Risk Undertaken and Asset

employed.

I. Criteria for evaluation the alternatives:

The above alternatives have been tested on three parameters. The snapshot of the test has

been detailed here-in-below:

(a) Reduced Litigation: Best Advance Pricing Agreement;

(b) Cost Effectiveness: Best Variable Contract and Commissionaire Arrangement;

(c) Simple and Easy to implement: Best Advance Pricing Agreement.

II. Selection of the best

On the basis of above analysis, points were allotted to each alternative and the second

alternative ranks 1st among three.

1 Since we are standing in 1999

3

Cameco is proposing to enter into marketing agreement1 with Cameco Europe Limited,

Switzerland (wholly owned subsidiary) for marketing its good in Europe. The transaction

falls within the purview of transfer pricing as the said transactions is between two associated

enterprises as the ownership exceeds 26%. The management of the company is seeking to

explore the terms of the agreement in order to mitigate any tax disputes or levy of penalty in

near term or long term. In this regard, various alternatives have been explored to determine

the terms of agreement. (Transfer Pricing, 2018) The alternatives have been detailed here-in-

under:

(a) Alternative-1-Variable Contract Pricing: Under this alternative, the company can decide

on terms and condition of transfer of goods to Cameco Europe Limited at the rate

prevalent in the market i.e. goods are sold at spot price (External CUP).

(b) Alternative-2-Advance Pricing Agreement: Cameco Group can enter into an agreement

with Tax Authorities of both jurisdictions whereby they agree to the terms and transfer

price of goods beforehand and transact.

(c) Alternative-3-Commissionaire Arrangement: Under this alternative, company can enter

into an commissionaire arrangement whereby a fixed commission is paid to Cameco

Europe Limited, Switzerland for its marketing service rendered. The rate of service shall

be determined on the basis of Functions Performed, Risk Undertaken and Asset

employed.

I. Criteria for evaluation the alternatives:

The above alternatives have been tested on three parameters. The snapshot of the test has

been detailed here-in-below:

(a) Reduced Litigation: Best Advance Pricing Agreement;

(b) Cost Effectiveness: Best Variable Contract and Commissionaire Arrangement;

(c) Simple and Easy to implement: Best Advance Pricing Agreement.

II. Selection of the best

On the basis of above analysis, points were allotted to each alternative and the second

alternative ranks 1st among three.

1 Since we are standing in 1999

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

III. Proposed Action Plan

The detailed plan for execution of the aforesaid alternative has been attached as a part of

report. It shall take 3 months to 6 months for execution.

4

The detailed plan for execution of the aforesaid alternative has been attached as a part of

report. It shall take 3 months to 6 months for execution.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

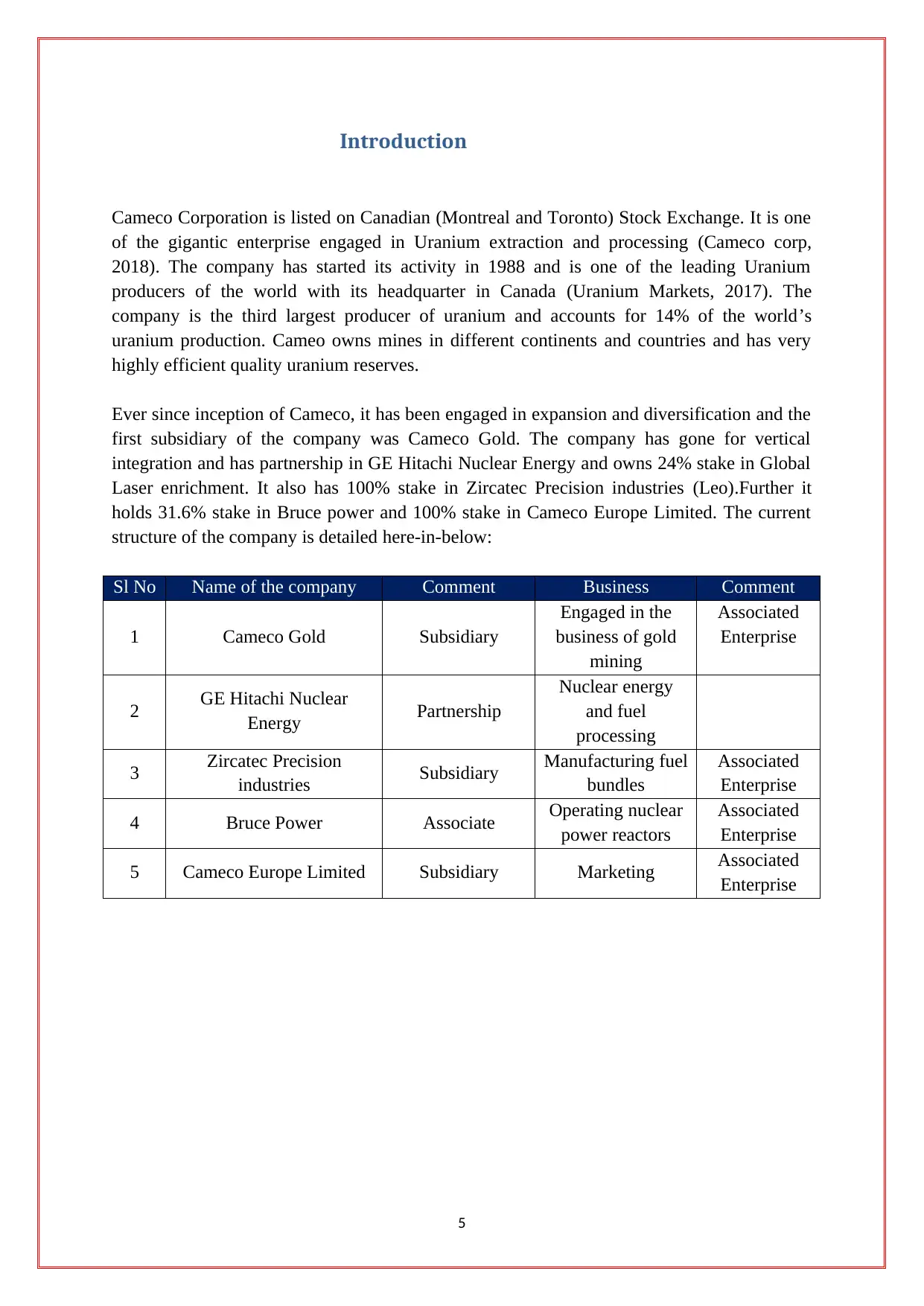

Introduction

Cameco Corporation is listed on Canadian (Montreal and Toronto) Stock Exchange. It is one

of the gigantic enterprise engaged in Uranium extraction and processing (Cameco corp,

2018). The company has started its activity in 1988 and is one of the leading Uranium

producers of the world with its headquarter in Canada (Uranium Markets, 2017). The

company is the third largest producer of uranium and accounts for 14% of the world’s

uranium production. Cameo owns mines in different continents and countries and has very

highly efficient quality uranium reserves.

Ever since inception of Cameco, it has been engaged in expansion and diversification and the

first subsidiary of the company was Cameco Gold. The company has gone for vertical

integration and has partnership in GE Hitachi Nuclear Energy and owns 24% stake in Global

Laser enrichment. It also has 100% stake in Zircatec Precision industries (Leo).Further it

holds 31.6% stake in Bruce power and 100% stake in Cameco Europe Limited. The current

structure of the company is detailed here-in-below:

Sl No Name of the company Comment Business Comment

1 Cameco Gold Subsidiary

Engaged in the

business of gold

mining

Associated

Enterprise

2 GE Hitachi Nuclear

Energy Partnership

Nuclear energy

and fuel

processing

3 Zircatec Precision

industries Subsidiary Manufacturing fuel

bundles

Associated

Enterprise

4 Bruce Power Associate Operating nuclear

power reactors

Associated

Enterprise

5 Cameco Europe Limited Subsidiary Marketing Associated

Enterprise

5

Cameco Corporation is listed on Canadian (Montreal and Toronto) Stock Exchange. It is one

of the gigantic enterprise engaged in Uranium extraction and processing (Cameco corp,

2018). The company has started its activity in 1988 and is one of the leading Uranium

producers of the world with its headquarter in Canada (Uranium Markets, 2017). The

company is the third largest producer of uranium and accounts for 14% of the world’s

uranium production. Cameo owns mines in different continents and countries and has very

highly efficient quality uranium reserves.

Ever since inception of Cameco, it has been engaged in expansion and diversification and the

first subsidiary of the company was Cameco Gold. The company has gone for vertical

integration and has partnership in GE Hitachi Nuclear Energy and owns 24% stake in Global

Laser enrichment. It also has 100% stake in Zircatec Precision industries (Leo).Further it

holds 31.6% stake in Bruce power and 100% stake in Cameco Europe Limited. The current

structure of the company is detailed here-in-below:

Sl No Name of the company Comment Business Comment

1 Cameco Gold Subsidiary

Engaged in the

business of gold

mining

Associated

Enterprise

2 GE Hitachi Nuclear

Energy Partnership

Nuclear energy

and fuel

processing

3 Zircatec Precision

industries Subsidiary Manufacturing fuel

bundles

Associated

Enterprise

4 Bruce Power Associate Operating nuclear

power reactors

Associated

Enterprise

5 Cameco Europe Limited Subsidiary Marketing Associated

Enterprise

5

Identification of problem

The company is facing the problem of determining the terms of the contract between

Cameco and its wholly owned subsidiary for export of products. The company wishes to

avoid any future litigation (Refer Note Below) or disputes arising on account of the said

transaction and hence is looking for alternative solutions for the same. The problem

relates to 1999 and hence we are acting from 1999.

Note: The company is considering a view point that in future tax dispute of base erosion

and profit shifting might not arise on account of shifting of profits to lower tax jurisdiction

i.e Zug , Switzerland.

6

The company is facing the problem of determining the terms of the contract between

Cameco and its wholly owned subsidiary for export of products. The company wishes to

avoid any future litigation (Refer Note Below) or disputes arising on account of the said

transaction and hence is looking for alternative solutions for the same. The problem

relates to 1999 and hence we are acting from 1999.

Note: The company is considering a view point that in future tax dispute of base erosion

and profit shifting might not arise on account of shifting of profits to lower tax jurisdiction

i.e Zug , Switzerland.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of problem2

Cameco is proposing to enter an agreement with Cameco Europe Ltd in 1999 for the purpose

of expanding its business operations in Europe. The company shall act as a marketing unit of

the Cameco and goods shall be transferred at a transfer price determined under the contract.

The contract shall be binding for a period of seventeen years subject to

addendum/modification as required. The terms of the contract need to pay special attention to

the provisions of transfer pricing and determination of Arm’s Length Price. The company has

identified following problems that might crop up in future if the terms of agreement are not

within the legal corridors of the tax laws of Canada or Switzerland:

(a) Transactions between two associated enterprises shall be carried at Arm’s Length price

in terms of transfer pricing laws;

(b) Differential tax rate in two jurisdictions i.e. 27% (average) in Canada and 10% in

Switzerland;

(c) Shifting of profits to lower tax jurisdiction and thus enjoying tax advantage;

(d) Modification of Terms of contract with the changes in the economic scenario;

(e) Tax Burden on account of tax evasion and corresponding negative sentiments in the

market if Canadian Revenue Agency wins the litigation and fall in prices of share.

(f) Taxation in Canada with no corresponding reduction in Switzerland.

The company under the present circumstance is exploring to decide on the terms of contract

that shall be in the interest of the company and government.

2 Since the said is about the current problem and we are thinking of correcting it retrospectively, we are writing

the current problem and relating it to past

7

Cameco is proposing to enter an agreement with Cameco Europe Ltd in 1999 for the purpose

of expanding its business operations in Europe. The company shall act as a marketing unit of

the Cameco and goods shall be transferred at a transfer price determined under the contract.

The contract shall be binding for a period of seventeen years subject to

addendum/modification as required. The terms of the contract need to pay special attention to

the provisions of transfer pricing and determination of Arm’s Length Price. The company has

identified following problems that might crop up in future if the terms of agreement are not

within the legal corridors of the tax laws of Canada or Switzerland:

(a) Transactions between two associated enterprises shall be carried at Arm’s Length price

in terms of transfer pricing laws;

(b) Differential tax rate in two jurisdictions i.e. 27% (average) in Canada and 10% in

Switzerland;

(c) Shifting of profits to lower tax jurisdiction and thus enjoying tax advantage;

(d) Modification of Terms of contract with the changes in the economic scenario;

(e) Tax Burden on account of tax evasion and corresponding negative sentiments in the

market if Canadian Revenue Agency wins the litigation and fall in prices of share.

(f) Taxation in Canada with no corresponding reduction in Switzerland.

The company under the present circumstance is exploring to decide on the terms of contract

that shall be in the interest of the company and government.

2 Since the said is about the current problem and we are thinking of correcting it retrospectively, we are writing

the current problem and relating it to past

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

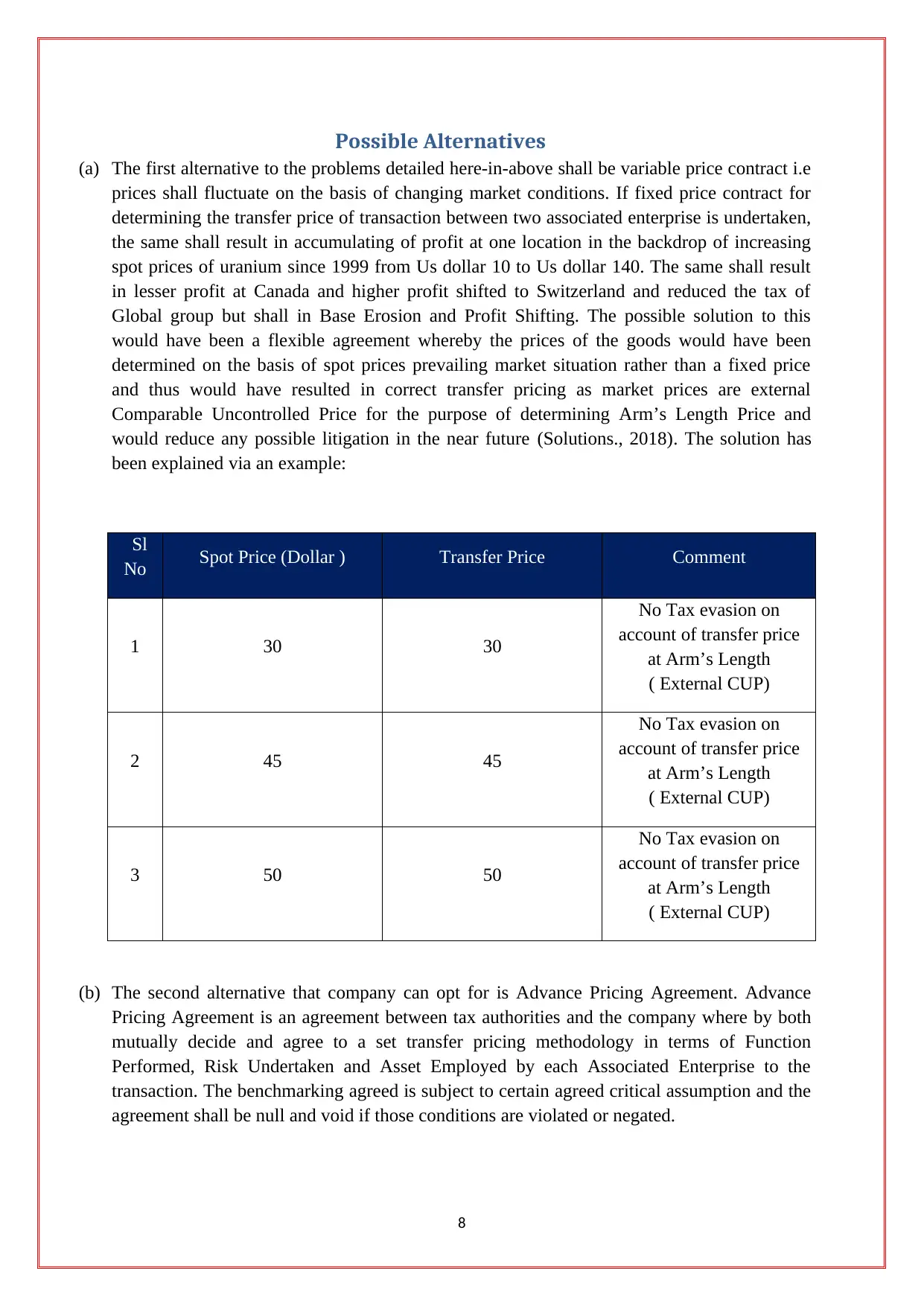

Possible Alternatives

(a) The first alternative to the problems detailed here-in-above shall be variable price contract i.e

prices shall fluctuate on the basis of changing market conditions. If fixed price contract for

determining the transfer price of transaction between two associated enterprise is undertaken,

the same shall result in accumulating of profit at one location in the backdrop of increasing

spot prices of uranium since 1999 from Us dollar 10 to Us dollar 140. The same shall result

in lesser profit at Canada and higher profit shifted to Switzerland and reduced the tax of

Global group but shall in Base Erosion and Profit Shifting. The possible solution to this

would have been a flexible agreement whereby the prices of the goods would have been

determined on the basis of spot prices prevailing market situation rather than a fixed price

and thus would have resulted in correct transfer pricing as market prices are external

Comparable Uncontrolled Price for the purpose of determining Arm’s Length Price and

would reduce any possible litigation in the near future (Solutions., 2018). The solution has

been explained via an example:

Sl

No Spot Price (Dollar ) Transfer Price Comment

1 30 30

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

2 45 45

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

3 50 50

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

(b) The second alternative that company can opt for is Advance Pricing Agreement. Advance

Pricing Agreement is an agreement between tax authorities and the company where by both

mutually decide and agree to a set transfer pricing methodology in terms of Function

Performed, Risk Undertaken and Asset Employed by each Associated Enterprise to the

transaction. The benchmarking agreed is subject to certain agreed critical assumption and the

agreement shall be null and void if those conditions are violated or negated.

8

(a) The first alternative to the problems detailed here-in-above shall be variable price contract i.e

prices shall fluctuate on the basis of changing market conditions. If fixed price contract for

determining the transfer price of transaction between two associated enterprise is undertaken,

the same shall result in accumulating of profit at one location in the backdrop of increasing

spot prices of uranium since 1999 from Us dollar 10 to Us dollar 140. The same shall result

in lesser profit at Canada and higher profit shifted to Switzerland and reduced the tax of

Global group but shall in Base Erosion and Profit Shifting. The possible solution to this

would have been a flexible agreement whereby the prices of the goods would have been

determined on the basis of spot prices prevailing market situation rather than a fixed price

and thus would have resulted in correct transfer pricing as market prices are external

Comparable Uncontrolled Price for the purpose of determining Arm’s Length Price and

would reduce any possible litigation in the near future (Solutions., 2018). The solution has

been explained via an example:

Sl

No Spot Price (Dollar ) Transfer Price Comment

1 30 30

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

2 45 45

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

3 50 50

No Tax evasion on

account of transfer price

at Arm’s Length

( External CUP)

(b) The second alternative that company can opt for is Advance Pricing Agreement. Advance

Pricing Agreement is an agreement between tax authorities and the company where by both

mutually decide and agree to a set transfer pricing methodology in terms of Function

Performed, Risk Undertaken and Asset Employed by each Associated Enterprise to the

transaction. The benchmarking agreed is subject to certain agreed critical assumption and the

agreement shall be null and void if those conditions are violated or negated.

8

Further, there are three types of Advance Pricing Agreement:

(i) Unilateral Advance Pricing Agreement: This agreement is entered between government

of one jurisdiction and company in that jurisdiction;

(ii) Bilateral Advance Pricing Agreement: This Agreement is entered into between the

government (Tax authorities) of two jurisdictions and the associated enterprise of each

jurisdiction with their respective tax authorities; (Taxpayers benefits associated with

APA)

(iii) Multilateral Advance Pricing Agreement: This Agreement is entered when more than 2

parties are involved in the transaction. It is an agreement among many governments and

the associated party and government.

Under the present scenario, the company can enter into bilateral or unilateral APA as the

transaction involves two parties. The price set under APA is 5 years with a provision for

rollback of 4 years. The company can opt for any of the APA, however bilateral APA is more

advantageous in terms of tax certainty in both jurisdictions. The APA offers the following

advantages:

Certainty in determination of Arm’s Length Price of the product;

Reduced Litigation;

Cost Effective.in long term ( Tax point of view)

(c) The third possible solution to the company is to enter into a commissionaire arrangement

with Cameco Europe Limited whereby Cameco shall provide commission at a certain

specified rate as decided in terms of the agreement to Cameco Europe Limited for rendering

marketing services in Europe. The company shall act as an independent agent of Cameco

procuring orders but such orders and terms of contract shall not be binding to the company as

the same shall result in fixed place of business for Cameco (OECD releases additional

guidance on attribution of profits to a permanent establishment under BEPS Action 7).

Further, the rate of fees shall be determined on the basis of Functions Performed, Risk

Undertaken and Asset employed by the respective parties to the agreement.

Cameco shall directly dispatch the goods on the basis of order procured by Cameco Europe

Limited from its manufacturing plant.

9

(i) Unilateral Advance Pricing Agreement: This agreement is entered between government

of one jurisdiction and company in that jurisdiction;

(ii) Bilateral Advance Pricing Agreement: This Agreement is entered into between the

government (Tax authorities) of two jurisdictions and the associated enterprise of each

jurisdiction with their respective tax authorities; (Taxpayers benefits associated with

APA)

(iii) Multilateral Advance Pricing Agreement: This Agreement is entered when more than 2

parties are involved in the transaction. It is an agreement among many governments and

the associated party and government.

Under the present scenario, the company can enter into bilateral or unilateral APA as the

transaction involves two parties. The price set under APA is 5 years with a provision for

rollback of 4 years. The company can opt for any of the APA, however bilateral APA is more

advantageous in terms of tax certainty in both jurisdictions. The APA offers the following

advantages:

Certainty in determination of Arm’s Length Price of the product;

Reduced Litigation;

Cost Effective.in long term ( Tax point of view)

(c) The third possible solution to the company is to enter into a commissionaire arrangement

with Cameco Europe Limited whereby Cameco shall provide commission at a certain

specified rate as decided in terms of the agreement to Cameco Europe Limited for rendering

marketing services in Europe. The company shall act as an independent agent of Cameco

procuring orders but such orders and terms of contract shall not be binding to the company as

the same shall result in fixed place of business for Cameco (OECD releases additional

guidance on attribution of profits to a permanent establishment under BEPS Action 7).

Further, the rate of fees shall be determined on the basis of Functions Performed, Risk

Undertaken and Asset employed by the respective parties to the agreement.

Cameco shall directly dispatch the goods on the basis of order procured by Cameco Europe

Limited from its manufacturing plant.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

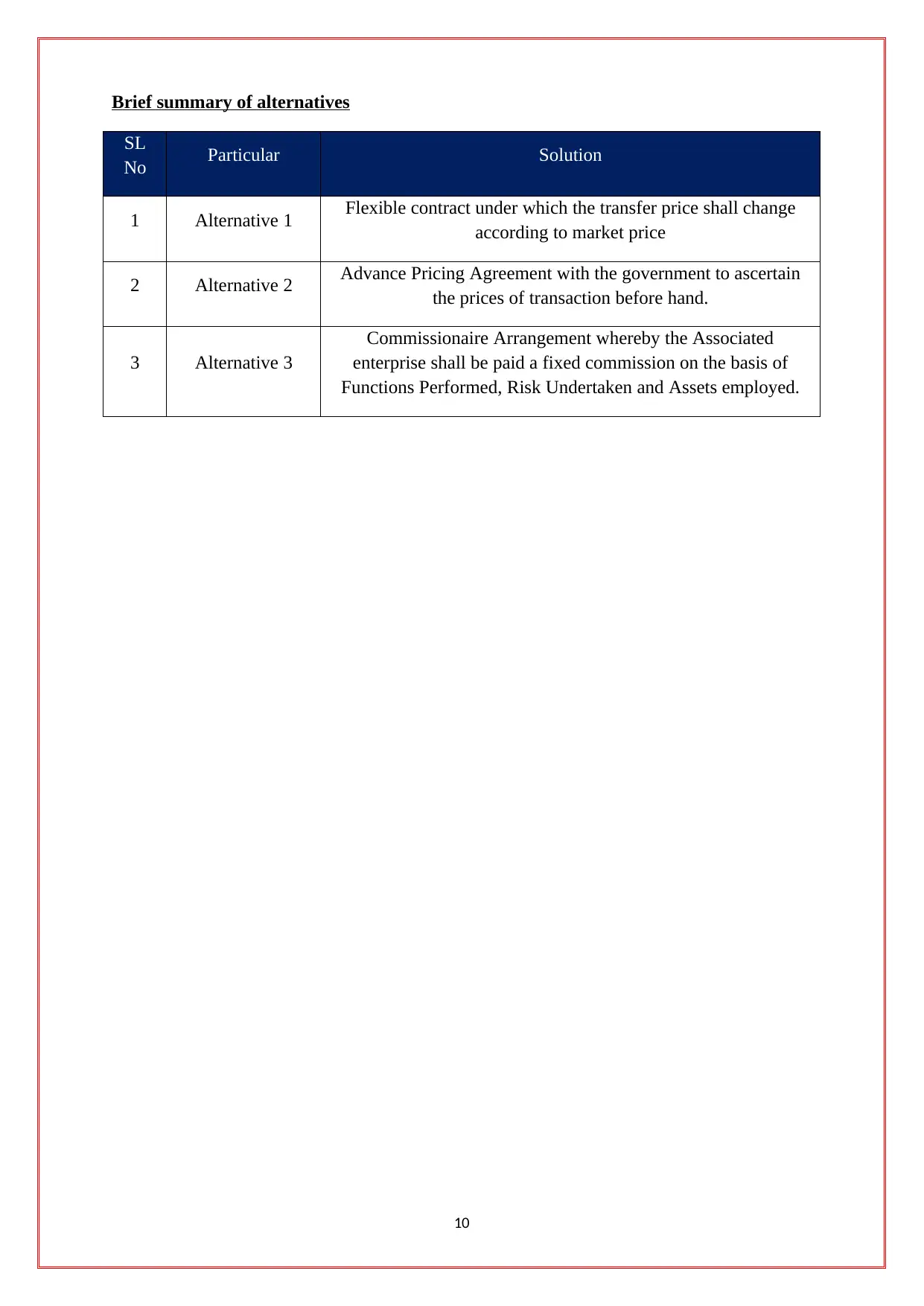

Brief summary of alternatives

SL

No Particular Solution

1 Alternative 1 Flexible contract under which the transfer price shall change

according to market price

2 Alternative 2 Advance Pricing Agreement with the government to ascertain

the prices of transaction before hand.

3 Alternative 3

Commissionaire Arrangement whereby the Associated

enterprise shall be paid a fixed commission on the basis of

Functions Performed, Risk Undertaken and Assets employed.

10

SL

No Particular Solution

1 Alternative 1 Flexible contract under which the transfer price shall change

according to market price

2 Alternative 2 Advance Pricing Agreement with the government to ascertain

the prices of transaction before hand.

3 Alternative 3

Commissionaire Arrangement whereby the Associated

enterprise shall be paid a fixed commission on the basis of

Functions Performed, Risk Undertaken and Assets employed.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact Analysis

Under the present scenario, the corporate image of the organisation shall be highly impacted

on account of negative news of tax evasion if the transactions are not carried out at Arms

Length. The company image shall be hampered which shall impact its business globally as

huge amount of tax litigation shall be imposed on the company( as the amount involved in the

transaction is substantial). Further, the same shall challenge business ethics, Corporate Social

Responsibility and efficacy of management. The sentiment of investor shall be highly

impacted resulting in falling prices of share of the company.

The problems identified in the above scenario have an impact on the following stakeholders

of the company:

(a) Shareholders: In initial years, though Shareholders shall be highly benefitted on account

of lower tax and higher EPS but the same shall be ephemeral on account of tax scrutiny

and tax litigation, share prices of the company shall fall on account of negative

sentiments in the market for the company. Further, there shall be a tax burden on the

company which may hamper the normal business cycle of the company on account of

cash crunch.

(b) Government: The Government of Canada and Switzerland shall be highly impacted

under the scenario. There shall be a huge loss to the exchequer on account of shifting of

profits of the company to a different jurisdiction. Thus government interests are of major

concern under the present scenario.

(c) Investors: Investors are also highly impacted from the negative news of the company as

majority of the capital invested in the company shall be washed out on account of

inefficacy of management of the company. They are hit as hard as the government.

(d) Other stakeholders: These groups of holders are influenced but the impact is not as hard

or strong as the others. They include customers, suppliers, financers etc.

11

Under the present scenario, the corporate image of the organisation shall be highly impacted

on account of negative news of tax evasion if the transactions are not carried out at Arms

Length. The company image shall be hampered which shall impact its business globally as

huge amount of tax litigation shall be imposed on the company( as the amount involved in the

transaction is substantial). Further, the same shall challenge business ethics, Corporate Social

Responsibility and efficacy of management. The sentiment of investor shall be highly

impacted resulting in falling prices of share of the company.

The problems identified in the above scenario have an impact on the following stakeholders

of the company:

(a) Shareholders: In initial years, though Shareholders shall be highly benefitted on account

of lower tax and higher EPS but the same shall be ephemeral on account of tax scrutiny

and tax litigation, share prices of the company shall fall on account of negative

sentiments in the market for the company. Further, there shall be a tax burden on the

company which may hamper the normal business cycle of the company on account of

cash crunch.

(b) Government: The Government of Canada and Switzerland shall be highly impacted

under the scenario. There shall be a huge loss to the exchequer on account of shifting of

profits of the company to a different jurisdiction. Thus government interests are of major

concern under the present scenario.

(c) Investors: Investors are also highly impacted from the negative news of the company as

majority of the capital invested in the company shall be washed out on account of

inefficacy of management of the company. They are hit as hard as the government.

(d) Other stakeholders: These groups of holders are influenced but the impact is not as hard

or strong as the others. They include customers, suppliers, financers etc.

11

Criteria for Evaluation of Alternatives

The criteria for evaluating the proposed alternatives above shall be such that satisfies the

requirement of the organisation and helps in taking an effective solution to the problems of

the company. The criteria that have been important for making decision shall be:

(a) Certainty in reducing litigation: The alternatives shall be such that the litigations and

other legal procedure involved in decision making shall be reduced to minimum.

Further, there shall be a precise estimation of arm’s length price for transfer of goods.

(b) Cost effectiveness : The measure should be most cost effective but reliable in reducing

future disputes and shall avoid any such future event;

(c) Simple and easy to implement: The alternative to be selected must be simple and

there shall not be much hassle in determining the transfer price. Further, the impact on

the group as a whole on account of such alternative shall be minimal.

12

The criteria for evaluating the proposed alternatives above shall be such that satisfies the

requirement of the organisation and helps in taking an effective solution to the problems of

the company. The criteria that have been important for making decision shall be:

(a) Certainty in reducing litigation: The alternatives shall be such that the litigations and

other legal procedure involved in decision making shall be reduced to minimum.

Further, there shall be a precise estimation of arm’s length price for transfer of goods.

(b) Cost effectiveness : The measure should be most cost effective but reliable in reducing

future disputes and shall avoid any such future event;

(c) Simple and easy to implement: The alternative to be selected must be simple and

there shall not be much hassle in determining the transfer price. Further, the impact on

the group as a whole on account of such alternative shall be minimal.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.