Corporate Hedging and Currency Risk Management

VerifiedAdded on 2021/04/17

|12

|2552

|30

AI Summary

This assignment provides an in-depth analysis of corporate hedging practices, including currency risk management policies and procedures used by companies listed on the Nairobi Security Exchange. It also examines the impact of hedging on companies' financial performance and explores the determinants of hedging practices. The assignment draws on research from various sources, including academic journals and industry reports, to provide a comprehensive understanding of corporate hedging practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TREASURY AND RISK MANAGEMENT

Treasury and Risk Management

Name of the Student:

Name of the University:

Authors Note:

Treasury and Risk Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TREASURY AND RISK MANAGEMENT

1

Table of Contents

Answer to question 1: Affirming the hedge used by exporters, while depicting the main

reason behind de-pegging of Franc............................................................................................2

Question 2:.................................................................................................................................4

a.1) Unhedged strategy for the payment of ABC:......................................................................4

a.2) Forward hedge strategy for the payment of ABC:..............................................................6

a.3) Money Market hedge strategy for the payment of ABC:....................................................7

a.4) Option hedge strategy for the payment of ABC:................................................................9

b) Depicting the most optimal hedge for ABC:.......................................................................11

Reference and Bibliography:....................................................................................................13

1

Table of Contents

Answer to question 1: Affirming the hedge used by exporters, while depicting the main

reason behind de-pegging of Franc............................................................................................2

Question 2:.................................................................................................................................4

a.1) Unhedged strategy for the payment of ABC:......................................................................4

a.2) Forward hedge strategy for the payment of ABC:..............................................................6

a.3) Money Market hedge strategy for the payment of ABC:....................................................7

a.4) Option hedge strategy for the payment of ABC:................................................................9

b) Depicting the most optimal hedge for ABC:.......................................................................11

Reference and Bibliography:....................................................................................................13

TREASURY AND RISK MANAGEMENT

2

Answer to question 1: Affirming the hedge used by exporters, while depicting the main

reason behind de-pegging of Franc

During 2011, Switzerland National Bank took a relative measure to reduce the

valuation of Swiss Franc, due to the continuous increase in its currency valuation in

comparison to other countries. In addition, the Swiss Franc was increasing in value in

comparison to USD, GBP and Euro, which was drastically hampering the actual economy of

the country. This is due to the exports that is conducted by Switzerland all over the world,

which got hit due to the higher valuation of the currency. The exporters were not able to

compete in the international market, which reduce their actual income. The export business of

Switzerland mainly comprises 70% of its total GDP, which was one of the drastic condition

presented to Switzerland National Bank (Reuters.com 2018). Therefore, in view of declining

revenues and GDP the Switzerland National Bank started to the value of Peggy their Swiss

Franc to reduce this valuation in the international market. this paging system relatively

allowed Swiss National Bank to reduce the actual valuation of the currency, while boosting

the economy.

Therefore, Switzerland National Bank started to accumulate Euro in their reserve,

which tampered with the overall Swiss Franc and helped the bank to control its valuation.

The more Euro was bought by Switzerland National Bank, the more Swiss Franc was printed

and distributed in the market. This relatively decrease the overall valuation of Swiss Franc in

the international market and help the bank to boost exports in Swiss Zealand. This relatively

increased the accumulation of Swiss Franc within the Switzerland National Bank, which

drastically helped in improving the economic conditions of the country (Admiralmarkets.com

2018). The measure used by Swiss National Bank to control its currency was discontinued

2

Answer to question 1: Affirming the hedge used by exporters, while depicting the main

reason behind de-pegging of Franc

During 2011, Switzerland National Bank took a relative measure to reduce the

valuation of Swiss Franc, due to the continuous increase in its currency valuation in

comparison to other countries. In addition, the Swiss Franc was increasing in value in

comparison to USD, GBP and Euro, which was drastically hampering the actual economy of

the country. This is due to the exports that is conducted by Switzerland all over the world,

which got hit due to the higher valuation of the currency. The exporters were not able to

compete in the international market, which reduce their actual income. The export business of

Switzerland mainly comprises 70% of its total GDP, which was one of the drastic condition

presented to Switzerland National Bank (Reuters.com 2018). Therefore, in view of declining

revenues and GDP the Switzerland National Bank started to the value of Peggy their Swiss

Franc to reduce this valuation in the international market. this paging system relatively

allowed Swiss National Bank to reduce the actual valuation of the currency, while boosting

the economy.

Therefore, Switzerland National Bank started to accumulate Euro in their reserve,

which tampered with the overall Swiss Franc and helped the bank to control its valuation.

The more Euro was bought by Switzerland National Bank, the more Swiss Franc was printed

and distributed in the market. This relatively decrease the overall valuation of Swiss Franc in

the international market and help the bank to boost exports in Swiss Zealand. This relatively

increased the accumulation of Swiss Franc within the Switzerland National Bank, which

drastically helped in improving the economic conditions of the country (Admiralmarkets.com

2018). The measure used by Swiss National Bank to control its currency was discontinued

TREASURY AND RISK MANAGEMENT

3

during 2015, which led to a drastic change in its currency valuation and stock market. The de-

pegging was relatively conductor due to certain factors which are depicted below,

Protest given from Switzerland citizens regarding the accumulation of Euro currency:

In Switzerland they were relevant protest against the measure that was used by Swiss

National bank for controlling their currency, which actually inflated the Swiss economy. the

measure used by the bank was to print more Swiss Franc to purchase Euro, which increased

circulation of the currency in the market, which relatively depicted an alarming rate for the

citizens of Switzerland. The citizens mainly feared the rise of inflation within the economy,

due to the printing of Swiss Franc for buying Euro currency. Swiss National Bank

accumulated 480 billion of foreign reserves, which comprise only of Euro (Bbc.com 2018).

This extreme accumulation of the currency is relatively depicting the problems, which might

in Swiss Franc. Therefore, the continuous pressure from citizens Swiss National Bank be the

decision of de-pegging the Swiss Franc and to start selling Euro in the currency market.

Reduction in the currency value of Euro:

The second main reason behind the debugging of Swiss Franc was the reduction in

value of Euro, which was being conducted, due to the measures taken by European National

Bank. The European National Bank mainly injected capital within the economy to increase

inflation rate with the process of monetary easing. This process relatively increased the

circulation of Euro within the Euro-Zone, which declined its overall valuation. This

continuous devaluation of euro, due to measures taken by the European National Bank

directly affected the actual valuation of Swiss Franc. The Swiss National Bank intended to

keep a relevant value for the Swiss Franc, which was drastically reduced due to the

depreciating Euro. The reason behind pegging was happening due to the excessive exposure

of Swiss National Bank to the Euro currency. Therefore, the continuation of pegging measure

3

during 2015, which led to a drastic change in its currency valuation and stock market. The de-

pegging was relatively conductor due to certain factors which are depicted below,

Protest given from Switzerland citizens regarding the accumulation of Euro currency:

In Switzerland they were relevant protest against the measure that was used by Swiss

National bank for controlling their currency, which actually inflated the Swiss economy. the

measure used by the bank was to print more Swiss Franc to purchase Euro, which increased

circulation of the currency in the market, which relatively depicted an alarming rate for the

citizens of Switzerland. The citizens mainly feared the rise of inflation within the economy,

due to the printing of Swiss Franc for buying Euro currency. Swiss National Bank

accumulated 480 billion of foreign reserves, which comprise only of Euro (Bbc.com 2018).

This extreme accumulation of the currency is relatively depicting the problems, which might

in Swiss Franc. Therefore, the continuous pressure from citizens Swiss National Bank be the

decision of de-pegging the Swiss Franc and to start selling Euro in the currency market.

Reduction in the currency value of Euro:

The second main reason behind the debugging of Swiss Franc was the reduction in

value of Euro, which was being conducted, due to the measures taken by European National

Bank. The European National Bank mainly injected capital within the economy to increase

inflation rate with the process of monetary easing. This process relatively increased the

circulation of Euro within the Euro-Zone, which declined its overall valuation. This

continuous devaluation of euro, due to measures taken by the European National Bank

directly affected the actual valuation of Swiss Franc. The Swiss National Bank intended to

keep a relevant value for the Swiss Franc, which was drastically reduced due to the

depreciating Euro. The reason behind pegging was happening due to the excessive exposure

of Swiss National Bank to the Euro currency. Therefore, the continuation of pegging measure

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TREASURY AND RISK MANAGEMENT

4

would drastically affect the actual value of currency and negatively impact its economy.

Consequently, the Swiss National Bank decided to discontinue the pegging measure used for

devaluating their currency (Snbchf.com 2017).

Therefore, the exporters could use different hedging measure such as future contracts,

option contracts, swap contract and forward contracts to hedge the exposure in the currency

market. These derivative instruments could eventually help the exporters of Switzerland to

reduce the negative impact of volatile currency market and maintain the level of profits. After

the de-pegging the currency value of Switzerland was valued at 1.2 to 0.8 in a single day.

This reflected the overall anxiety and confusion among the investors regarding the actual

value of Swiss Franc. The most viable hedging choice which could be used by Switzerland

exporters are option hedging and Swaps, which would allow the exporters to get high

leverage on their trades by contributing low premium. This derivative instrument relatively

allows the investor to increase is exposure in the current market for a nominal amount, which

helps them to reduce blockage of essential capital (Wahab et al. 2017).

Question 2:

a.1) Unhedged strategy for the payment of ABC:

The value of the deal according to the current exchange rate.

Current exchange rate: $1.10

€50,000,000 × $1.10 = $55,000,000

Future spot rate: $0.80

€50,000,000 × $0.80 = $40,000,000

Profit: $40,000,000 - $55,000,000 = -$15,000,000

4

would drastically affect the actual value of currency and negatively impact its economy.

Consequently, the Swiss National Bank decided to discontinue the pegging measure used for

devaluating their currency (Snbchf.com 2017).

Therefore, the exporters could use different hedging measure such as future contracts,

option contracts, swap contract and forward contracts to hedge the exposure in the currency

market. These derivative instruments could eventually help the exporters of Switzerland to

reduce the negative impact of volatile currency market and maintain the level of profits. After

the de-pegging the currency value of Switzerland was valued at 1.2 to 0.8 in a single day.

This reflected the overall anxiety and confusion among the investors regarding the actual

value of Swiss Franc. The most viable hedging choice which could be used by Switzerland

exporters are option hedging and Swaps, which would allow the exporters to get high

leverage on their trades by contributing low premium. This derivative instrument relatively

allows the investor to increase is exposure in the current market for a nominal amount, which

helps them to reduce blockage of essential capital (Wahab et al. 2017).

Question 2:

a.1) Unhedged strategy for the payment of ABC:

The value of the deal according to the current exchange rate.

Current exchange rate: $1.10

€50,000,000 × $1.10 = $55,000,000

Future spot rate: $0.80

€50,000,000 × $0.80 = $40,000,000

Profit: $40,000,000 - $55,000,000 = -$15,000,000

TREASURY AND RISK MANAGEMENT

5

The unhedged strategy was unsuccessful.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

Profit: $45,000,000 - $55,000,000 = -$10,000,000

The unhedged strategy was unsuccessful.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

Profit: $52,500,000 - $55,000,000 = -$2,500,000

The unhedged strategy was unsuccessful.

Future spot rate: $1.13

€50,000,000 × $1.13 = $56,500,000

Profit: $56,500,000 - $55,000,000 = $1,500,000

Unhedged strategy was successful.

Future spot rate: $1.20

€50,000,000 × $1.20 = $60,000,000

Profit: $60,000,000 - $55,000,000 = $5,000,000

Unhedged strategy was successful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

Profit: $62,500,000 - $55,000,000 = $7,500,000

5

The unhedged strategy was unsuccessful.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

Profit: $45,000,000 - $55,000,000 = -$10,000,000

The unhedged strategy was unsuccessful.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

Profit: $52,500,000 - $55,000,000 = -$2,500,000

The unhedged strategy was unsuccessful.

Future spot rate: $1.13

€50,000,000 × $1.13 = $56,500,000

Profit: $56,500,000 - $55,000,000 = $1,500,000

Unhedged strategy was successful.

Future spot rate: $1.20

€50,000,000 × $1.20 = $60,000,000

Profit: $60,000,000 - $55,000,000 = $5,000,000

Unhedged strategy was successful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

Profit: $62,500,000 - $55,000,000 = $7,500,000

TREASURY AND RISK MANAGEMENT

6

Unhedged strategy was successful.

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

Profit: $65,000,000 - $55,000,000 = $10,000,000

Unhedged strategy was successful.

a.2) Forward hedge strategy for the payment of ABC:

1-year forward: $1.13

50,000,000 x 1.13 = 56,500,000

Future spot rate: $0.80

€50,000,000 × $0.80 = $40,000,000

The hedge worked.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

The hedge worked.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

The hedge worked.

Future spot rate: $1.20

6

Unhedged strategy was successful.

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

Profit: $65,000,000 - $55,000,000 = $10,000,000

Unhedged strategy was successful.

a.2) Forward hedge strategy for the payment of ABC:

1-year forward: $1.13

50,000,000 x 1.13 = 56,500,000

Future spot rate: $0.80

€50,000,000 × $0.80 = $40,000,000

The hedge worked.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

The hedge worked.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

The hedge worked.

Future spot rate: $1.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY AND RISK MANAGEMENT

7

€50,000,000 × $1.20 = $60,000,000

The hedge was unsuccessful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

The hedge was unsuccessful.

a.3) Money Market hedge strategy for the payment of ABC:

€50,000,000

Step 1: Borrow Euro

PV= FV/ (1+r) = €50,000,000 / (1.02)

= €49,019,607.84 €49,019,608

Step 2: spot. Sell €49,019,608

Buy USD =€49,019,608 × $1.10

= $53,921,568.8

= $53,921,569

Step 3: Lend/ Invest

$53,921,569 @1.055 = $56,887,255.3

= $56,887,255

Future spot rate: $0.80

7

€50,000,000 × $1.20 = $60,000,000

The hedge was unsuccessful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

The hedge was unsuccessful.

a.3) Money Market hedge strategy for the payment of ABC:

€50,000,000

Step 1: Borrow Euro

PV= FV/ (1+r) = €50,000,000 / (1.02)

= €49,019,607.84 €49,019,608

Step 2: spot. Sell €49,019,608

Buy USD =€49,019,608 × $1.10

= $53,921,568.8

= $53,921,569

Step 3: Lend/ Invest

$53,921,569 @1.055 = $56,887,255.3

= $56,887,255

Future spot rate: $0.80

TREASURY AND RISK MANAGEMENT

8

€50,000,000 × $0.80 = $40,000,000

The hedge worked.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

The hedge worked.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

The hedge worked.

Future spot rate: $1.13

€50,000,000 × $1.13 = $56,500,000

The hedge worked.

Future spot rate: $1.20

€50,000,000 × $1.20 = $60,000,000

The hedge was unsuccessful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

The hedge was unsuccessful.

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

8

€50,000,000 × $0.80 = $40,000,000

The hedge worked.

Future spot rate: $0.90

€50,000,000 × $0.90 = $45,000,000

The hedge worked.

Future spot rate: $1.05

€50,000,000 × $1.05 = $52,500,000

The hedge worked.

Future spot rate: $1.13

€50,000,000 × $1.13 = $56,500,000

The hedge worked.

Future spot rate: $1.20

€50,000,000 × $1.20 = $60,000,000

The hedge was unsuccessful.

Future spot rate: $1.25

€50,000,000 × $1.25 = $62,500,000

The hedge was unsuccessful.

Future spot rate: $1.30

€50,000,000 × $1.30 = $65,000,000

TREASURY AND RISK MANAGEMENT

9

The hedge was unsuccessful.

a.4) Option hedge strategy for the payment of ABC:

Put option

Exercise price: $1.11, premium: $0.06 per unit

If options are exercised

Receipt – premium

= (50 mil x 1.11) – 3,000,000

= 55,500,000 – 3,000,000

=52,500,000

Future spot rate: $0.80

= (50 mil x 0.80) – 3,000,000

=37,000,000

Do not exercise

Future spot rate: $0.90

= (50 mil x 0.90) – 3,000,000

=42,000,000

Do not exercise

Future spot rate: $1.05

= (50 mil x 1.05) – 3,000,000

=49,500,000

9

The hedge was unsuccessful.

a.4) Option hedge strategy for the payment of ABC:

Put option

Exercise price: $1.11, premium: $0.06 per unit

If options are exercised

Receipt – premium

= (50 mil x 1.11) – 3,000,000

= 55,500,000 – 3,000,000

=52,500,000

Future spot rate: $0.80

= (50 mil x 0.80) – 3,000,000

=37,000,000

Do not exercise

Future spot rate: $0.90

= (50 mil x 0.90) – 3,000,000

=42,000,000

Do not exercise

Future spot rate: $1.05

= (50 mil x 1.05) – 3,000,000

=49,500,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TREASURY AND RISK MANAGEMENT

10

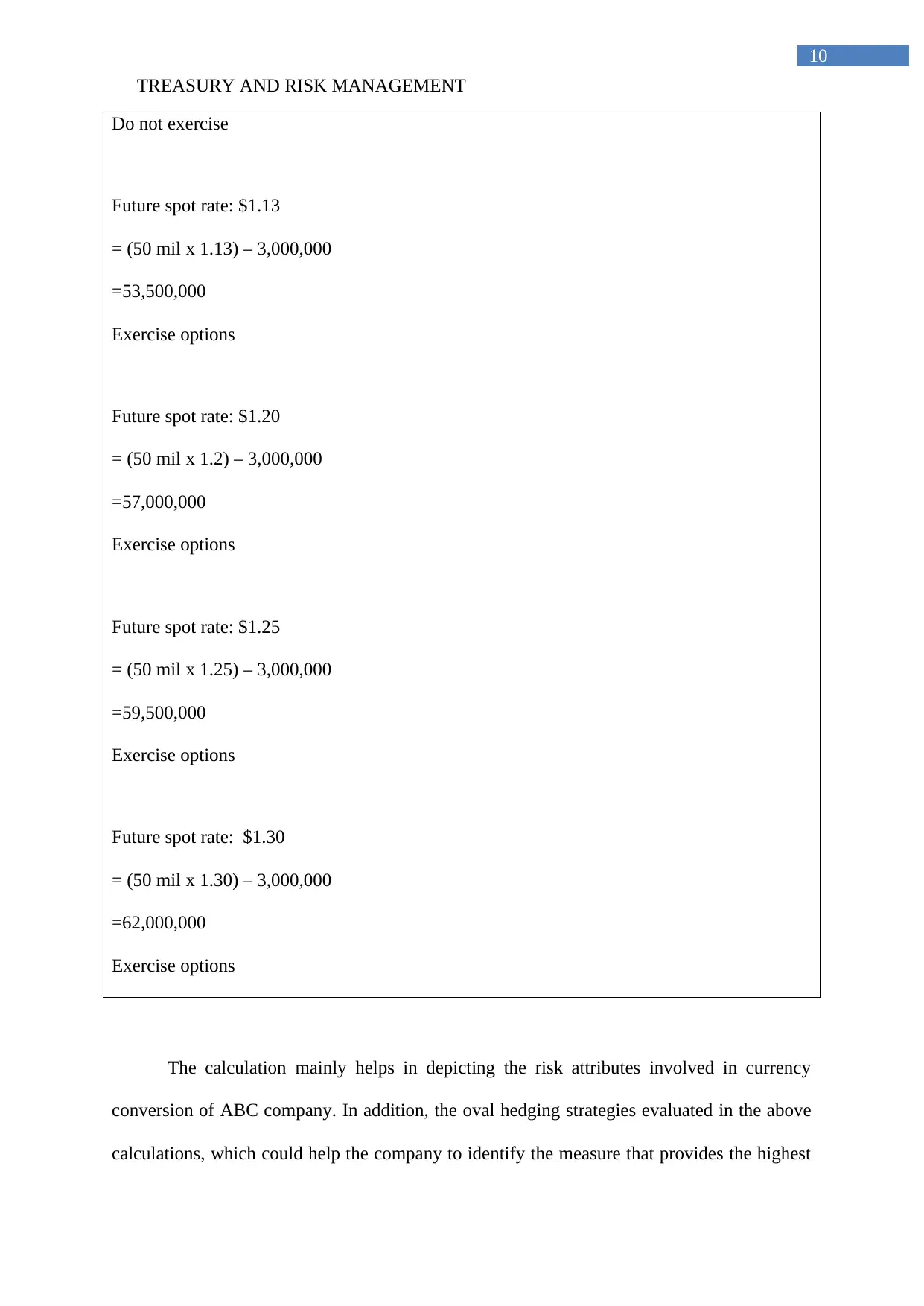

Do not exercise

Future spot rate: $1.13

= (50 mil x 1.13) – 3,000,000

=53,500,000

Exercise options

Future spot rate: $1.20

= (50 mil x 1.2) – 3,000,000

=57,000,000

Exercise options

Future spot rate: $1.25

= (50 mil x 1.25) – 3,000,000

=59,500,000

Exercise options

Future spot rate: $1.30

= (50 mil x 1.30) – 3,000,000

=62,000,000

Exercise options

The calculation mainly helps in depicting the risk attributes involved in currency

conversion of ABC company. In addition, the oval hedging strategies evaluated in the above

calculations, which could help the company to identify the measure that provides the highest

10

Do not exercise

Future spot rate: $1.13

= (50 mil x 1.13) – 3,000,000

=53,500,000

Exercise options

Future spot rate: $1.20

= (50 mil x 1.2) – 3,000,000

=57,000,000

Exercise options

Future spot rate: $1.25

= (50 mil x 1.25) – 3,000,000

=59,500,000

Exercise options

Future spot rate: $1.30

= (50 mil x 1.30) – 3,000,000

=62,000,000

Exercise options

The calculation mainly helps in depicting the risk attributes involved in currency

conversion of ABC company. In addition, the oval hedging strategies evaluated in the above

calculations, which could help the company to identify the measure that provides the highest

TREASURY AND RISK MANAGEMENT

11

conversion rate. Strategies such as forward contract, option contract, money market hedge

and unhedged is used to evaluate the relevant choices presented to the company. Currency

conversion relatively has high risk, which increases losses of the company over the period of

time due to problems faced by volatile currency market. and hedge strategy is a relatively and

adverse measure way no hedging is conducted by the company who is intended to convert the

currency in future. This relatively increases the risk of loss incurring from currency

conversion due to the volatile currency market. Moreover, forward contract is also an

adequate measure, which is only useful to fix the overall currency conversion rate. However,

any increment in the currency conversion rate was drastically hampered the actual profit

which could have been obtained by the company (Kim and Chance 2018).

b) Depicting the most optimal hedge for ABC:

The evaluation of the four different hedging strategies, which could be used by ABC

company the adequate and optimal strategy is chosen. From the overall assessment put option

is one of the most viable investment option for the company, which could relatively help in

increasing the conversion rate while reducing the risk. In addition, the use of optimal had

such as option hedging would eventually allow ABC company to generate higher conversion

rate in comparison to other options. Therefore, it could help in improving the actual revenues

of ABC company that is being generated in the international market. Cadman et al. (2017)

stated that with the help of adequate hedging measure, companies can reduce their exposure

in currency and capital market. This reduction in risk eventually allows the investor to

increase their exposure and return generation capacity by conducting adequate investment.

.

11

conversion rate. Strategies such as forward contract, option contract, money market hedge

and unhedged is used to evaluate the relevant choices presented to the company. Currency

conversion relatively has high risk, which increases losses of the company over the period of

time due to problems faced by volatile currency market. and hedge strategy is a relatively and

adverse measure way no hedging is conducted by the company who is intended to convert the

currency in future. This relatively increases the risk of loss incurring from currency

conversion due to the volatile currency market. Moreover, forward contract is also an

adequate measure, which is only useful to fix the overall currency conversion rate. However,

any increment in the currency conversion rate was drastically hampered the actual profit

which could have been obtained by the company (Kim and Chance 2018).

b) Depicting the most optimal hedge for ABC:

The evaluation of the four different hedging strategies, which could be used by ABC

company the adequate and optimal strategy is chosen. From the overall assessment put option

is one of the most viable investment option for the company, which could relatively help in

increasing the conversion rate while reducing the risk. In addition, the use of optimal had

such as option hedging would eventually allow ABC company to generate higher conversion

rate in comparison to other options. Therefore, it could help in improving the actual revenues

of ABC company that is being generated in the international market. Cadman et al. (2017)

stated that with the help of adequate hedging measure, companies can reduce their exposure

in currency and capital market. This reduction in risk eventually allows the investor to

increase their exposure and return generation capacity by conducting adequate investment.

.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.