Optimal Hedging Strategy for ABC Company

VerifiedAdded on 2021/04/21

|9

|1788

|35

AI Summary

The provided assignment is a detailed evaluation of optimal hedging strategies for ABC company. The analysis compares various hedging techniques, such as forward hedge, money market hedge, and option hedge (put and call options), to determine the most suitable strategy. The results show that a money market hedge offers the lowest risk and highest potential gain, making it the recommended choice for ABC company. This assignment is relevant to finance and risk management, providing insights into effective hedging strategies for managing investment risks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TREASURY AND RISK MANAGEMENT

Treasury and Risk Management

Name of the Student:

Name of the University:

Authors Note:

Treasury and Risk Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TREASURY AND RISK MANAGEMENT

1

Table of Contents

Question 1: Identifying the reason for de-pegging of Franc and stating the hedging strategies

implemented by Swiss exporters................................................................................................2

Question 2:.................................................................................................................................4

a) Calculating the dollar cash flow from each strategy and detecting their risk:.......................4

b) Depicting the most optimal hedge for ABC:.........................................................................7

Reference and Bibliography:......................................................................................................8

1

Table of Contents

Question 1: Identifying the reason for de-pegging of Franc and stating the hedging strategies

implemented by Swiss exporters................................................................................................2

Question 2:.................................................................................................................................4

a) Calculating the dollar cash flow from each strategy and detecting their risk:.......................4

b) Depicting the most optimal hedge for ABC:.........................................................................7

Reference and Bibliography:......................................................................................................8

TREASURY AND RISK MANAGEMENT

2

Question 1: Identifying the reason for de-pegging of Franc and stating the hedging

strategies implemented by Swiss exporters

The main reason behind the unpegging of Swiss franc is due to the decisions made by

SNB is controlling the valuation of franc, which was rising due to continuous buying of the

currency. The franc was mainly pegged with Euro, where SNB increased the supply of franc,

which was used in buying the euro and reducing the actual valuation of franc. The pegging

was conducted for reducing the franc value against other currencies, as exporters were having

trouble selling their products internationally. The Swiss economy is mainly based on

exporters, where rising valuation of Swiss franc was hammering progress of the economy.

The SNB aimed in depreciating the Swiss franc by accumulating Euro and increasing the

flow of franc in the currency market. Bessis (2015) stated that with relevant measure

countries can control their currency valuation, which might help in improving the total GDP

value.

Moreover, the main problems started, when Euro value stated to depreciate against

major currencies, which in turn declined value of franc, due to high accumulation of Euro

currency by SNB. The value of Euro mainly depreciated by 10% to 12% against US dollar,

which devalued franc in the currency market (The Economist 2018). In addition, motive of

the SNB was fulfilled when euro stated to depreciate and they did not want any further

devaluation of their currency, which led to the de-pegging of Swiss Franc. Approximately

480 billion of Euro currency was accumulated by SNB, which relevantly declined the

valuation of Swiss Franc. This increment in foreign currency reserve is directly increasing the

chance of hyperinflation due to the increase in supply of domestic currency. On the other

hand, Chance and Brooks (2015) criticises that the control of currency was previously

conducted by Asian countries, which resulted in the occurrence of Asian financial crisis.

2

Question 1: Identifying the reason for de-pegging of Franc and stating the hedging

strategies implemented by Swiss exporters

The main reason behind the unpegging of Swiss franc is due to the decisions made by

SNB is controlling the valuation of franc, which was rising due to continuous buying of the

currency. The franc was mainly pegged with Euro, where SNB increased the supply of franc,

which was used in buying the euro and reducing the actual valuation of franc. The pegging

was conducted for reducing the franc value against other currencies, as exporters were having

trouble selling their products internationally. The Swiss economy is mainly based on

exporters, where rising valuation of Swiss franc was hammering progress of the economy.

The SNB aimed in depreciating the Swiss franc by accumulating Euro and increasing the

flow of franc in the currency market. Bessis (2015) stated that with relevant measure

countries can control their currency valuation, which might help in improving the total GDP

value.

Moreover, the main problems started, when Euro value stated to depreciate against

major currencies, which in turn declined value of franc, due to high accumulation of Euro

currency by SNB. The value of Euro mainly depreciated by 10% to 12% against US dollar,

which devalued franc in the currency market (The Economist 2018). In addition, motive of

the SNB was fulfilled when euro stated to depreciate and they did not want any further

devaluation of their currency, which led to the de-pegging of Swiss Franc. Approximately

480 billion of Euro currency was accumulated by SNB, which relevantly declined the

valuation of Swiss Franc. This increment in foreign currency reserve is directly increasing the

chance of hyperinflation due to the increase in supply of domestic currency. On the other

hand, Chance and Brooks (2015) criticises that the control of currency was previously

conducted by Asian countries, which resulted in the occurrence of Asian financial crisis.

TREASURY AND RISK MANAGEMENT

3

Moreover, the measure used by European central bank initiated a decline in euro,

which resulted in the devaluation of Swiss Franc. In addition, the overall measure used the

European bank resulted in printing more currency, which in turn increased the supply of

Swiss franc to continue with pegging. However, the motive of SNB was to reduce the

valuation Swiss Franc for supporting their exports, which was being fulfilled by the

continuous devaluation of Euro (The Economist 2018). Therefore, the increment in printing

of more France needs to be conducted by SNB for maintaining the pegging programs, which

was resulting in hyperinflation in their country. Hence, it became the main reason behind the

discontinuation of pegging, which was conducted by SNB for devaluating Swiss Franc. In

this context, Hopkin (2017) mentioned that countries and government cannot control the

impossible trinity, which lead to the augmentation of financial crisis. The above-mentioned

reasons are the longing point, which forced SNB to unpegged the franc that was continuously

being devaluated in comparison with other countries. The intervention of the government in

controlling the rising currency valuation made a drastic decline in Swiss Capital market after

the announcement of unpegging conducted by SNB. The swiss stock market collapsed, while

the currency value of Franc went from 1.2 to 0.8 in in comparison with USD (The Economist

2018).

The Swiss exporters seeing the devaluation of Franc could hedge their exposure in the

international market for controlling their loss incurred from current exchange. In addition, the

exporters of Switzerland could effectively use option hedging strategy for controlling their

losses incurred from devaluation of their currency. In addition, the use of call option could

allow exporters in Switzerland to curb the devaluation of franc in comparison to other

currencies. In this context, DeAngelo and Stulz (2015) mentioned that the use of hedging

process allows investor to reduce the risk from volatile currency and capital market. The sue

of call option might help in curbing the exposure of rising currency value. Moreover, the

3

Moreover, the measure used by European central bank initiated a decline in euro,

which resulted in the devaluation of Swiss Franc. In addition, the overall measure used the

European bank resulted in printing more currency, which in turn increased the supply of

Swiss franc to continue with pegging. However, the motive of SNB was to reduce the

valuation Swiss Franc for supporting their exports, which was being fulfilled by the

continuous devaluation of Euro (The Economist 2018). Therefore, the increment in printing

of more France needs to be conducted by SNB for maintaining the pegging programs, which

was resulting in hyperinflation in their country. Hence, it became the main reason behind the

discontinuation of pegging, which was conducted by SNB for devaluating Swiss Franc. In

this context, Hopkin (2017) mentioned that countries and government cannot control the

impossible trinity, which lead to the augmentation of financial crisis. The above-mentioned

reasons are the longing point, which forced SNB to unpegged the franc that was continuously

being devaluated in comparison with other countries. The intervention of the government in

controlling the rising currency valuation made a drastic decline in Swiss Capital market after

the announcement of unpegging conducted by SNB. The swiss stock market collapsed, while

the currency value of Franc went from 1.2 to 0.8 in in comparison with USD (The Economist

2018).

The Swiss exporters seeing the devaluation of Franc could hedge their exposure in the

international market for controlling their loss incurred from current exchange. In addition, the

exporters of Switzerland could effectively use option hedging strategy for controlling their

losses incurred from devaluation of their currency. In addition, the use of call option could

allow exporters in Switzerland to curb the devaluation of franc in comparison to other

currencies. In this context, DeAngelo and Stulz (2015) mentioned that the use of hedging

process allows investor to reduce the risk from volatile currency and capital market. The sue

of call option might help in curbing the exposure of rising currency value. Moreover, the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TREASURY AND RISK MANAGEMENT

4

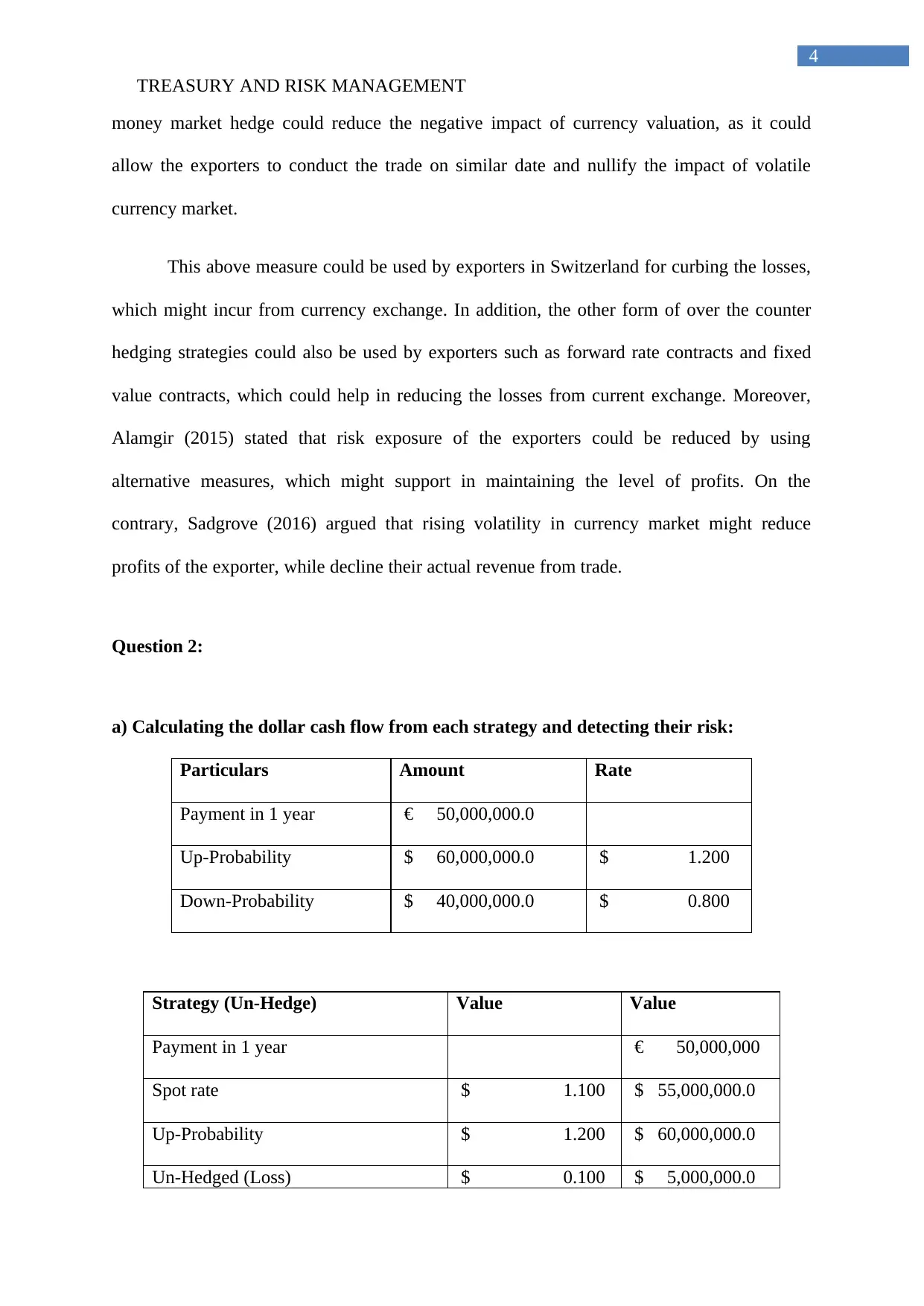

money market hedge could reduce the negative impact of currency valuation, as it could

allow the exporters to conduct the trade on similar date and nullify the impact of volatile

currency market.

This above measure could be used by exporters in Switzerland for curbing the losses,

which might incur from currency exchange. In addition, the other form of over the counter

hedging strategies could also be used by exporters such as forward rate contracts and fixed

value contracts, which could help in reducing the losses from current exchange. Moreover,

Alamgir (2015) stated that risk exposure of the exporters could be reduced by using

alternative measures, which might support in maintaining the level of profits. On the

contrary, Sadgrove (2016) argued that rising volatility in currency market might reduce

profits of the exporter, while decline their actual revenue from trade.

Question 2:

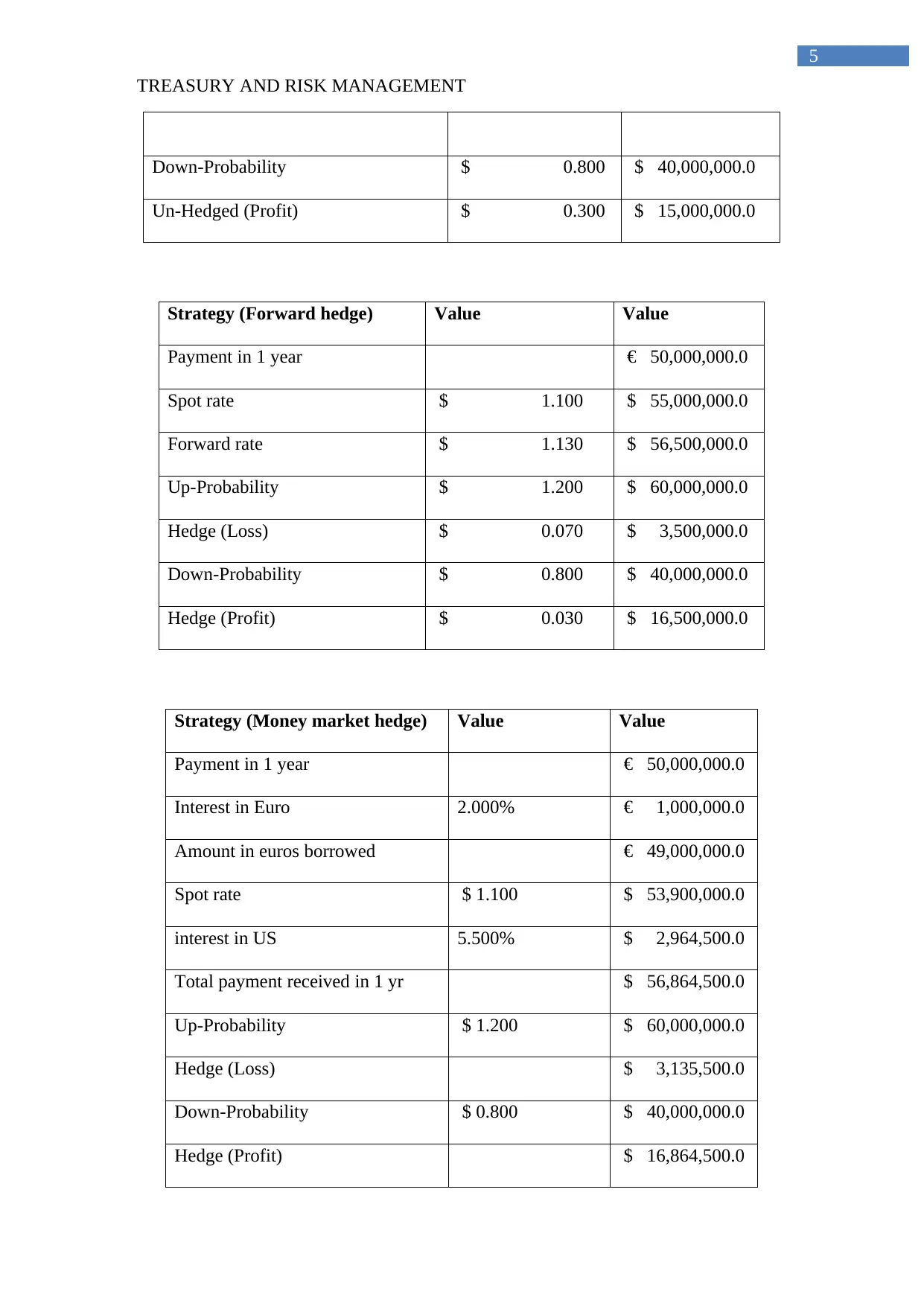

a) Calculating the dollar cash flow from each strategy and detecting their risk:

Particulars Amount Rate

Payment in 1 year € 50,000,000.0

Up-Probability $ 60,000,000.0 $ 1.200

Down-Probability $ 40,000,000.0 $ 0.800

Strategy (Un-Hedge) Value Value

Payment in 1 year € 50,000,000

Spot rate $ 1.100 $ 55,000,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Un-Hedged (Loss) $ 0.100 $ 5,000,000.0

4

money market hedge could reduce the negative impact of currency valuation, as it could

allow the exporters to conduct the trade on similar date and nullify the impact of volatile

currency market.

This above measure could be used by exporters in Switzerland for curbing the losses,

which might incur from currency exchange. In addition, the other form of over the counter

hedging strategies could also be used by exporters such as forward rate contracts and fixed

value contracts, which could help in reducing the losses from current exchange. Moreover,

Alamgir (2015) stated that risk exposure of the exporters could be reduced by using

alternative measures, which might support in maintaining the level of profits. On the

contrary, Sadgrove (2016) argued that rising volatility in currency market might reduce

profits of the exporter, while decline their actual revenue from trade.

Question 2:

a) Calculating the dollar cash flow from each strategy and detecting their risk:

Particulars Amount Rate

Payment in 1 year € 50,000,000.0

Up-Probability $ 60,000,000.0 $ 1.200

Down-Probability $ 40,000,000.0 $ 0.800

Strategy (Un-Hedge) Value Value

Payment in 1 year € 50,000,000

Spot rate $ 1.100 $ 55,000,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Un-Hedged (Loss) $ 0.100 $ 5,000,000.0

TREASURY AND RISK MANAGEMENT

5

Down-Probability $ 0.800 $ 40,000,000.0

Un-Hedged (Profit) $ 0.300 $ 15,000,000.0

Strategy (Forward hedge) Value Value

Payment in 1 year € 50,000,000.0

Spot rate $ 1.100 $ 55,000,000.0

Forward rate $ 1.130 $ 56,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.070 $ 3,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.030 $ 16,500,000.0

Strategy (Money market hedge) Value Value

Payment in 1 year € 50,000,000.0

Interest in Euro 2.000% € 1,000,000.0

Amount in euros borrowed € 49,000,000.0

Spot rate $ 1.100 $ 53,900,000.0

interest in US 5.500% $ 2,964,500.0

Total payment received in 1 yr $ 56,864,500.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 3,135,500.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 16,864,500.0

5

Down-Probability $ 0.800 $ 40,000,000.0

Un-Hedged (Profit) $ 0.300 $ 15,000,000.0

Strategy (Forward hedge) Value Value

Payment in 1 year € 50,000,000.0

Spot rate $ 1.100 $ 55,000,000.0

Forward rate $ 1.130 $ 56,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.070 $ 3,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.030 $ 16,500,000.0

Strategy (Money market hedge) Value Value

Payment in 1 year € 50,000,000.0

Interest in Euro 2.000% € 1,000,000.0

Amount in euros borrowed € 49,000,000.0

Spot rate $ 1.100 $ 53,900,000.0

interest in US 5.500% $ 2,964,500.0

Total payment received in 1 yr $ 56,864,500.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 3,135,500.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 16,864,500.0

TREASURY AND RISK MANAGEMENT

6

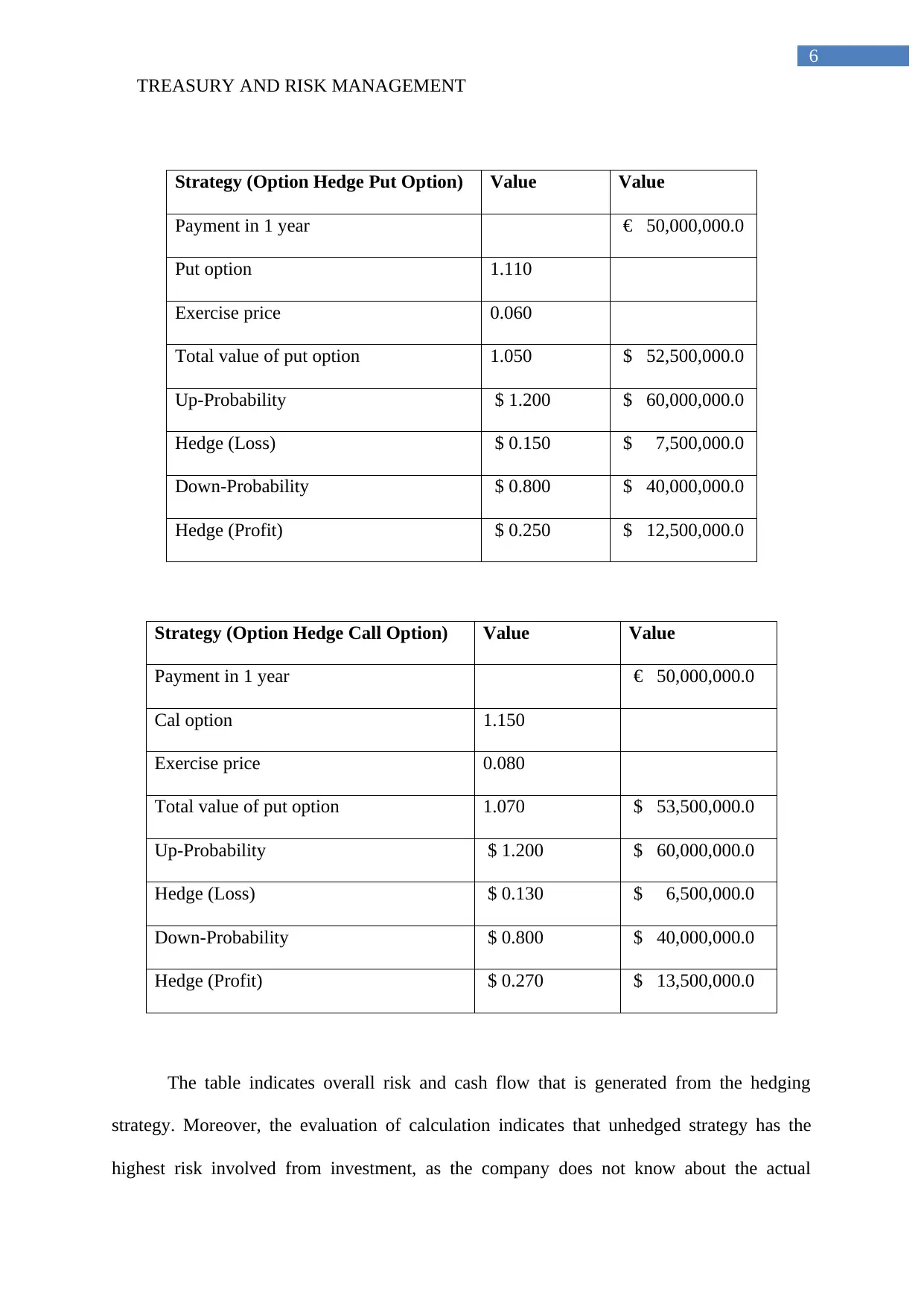

Strategy (Option Hedge Put Option) Value Value

Payment in 1 year € 50,000,000.0

Put option 1.110

Exercise price 0.060

Total value of put option 1.050 $ 52,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.150 $ 7,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.250 $ 12,500,000.0

Strategy (Option Hedge Call Option) Value Value

Payment in 1 year € 50,000,000.0

Cal option 1.150

Exercise price 0.080

Total value of put option 1.070 $ 53,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.130 $ 6,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.270 $ 13,500,000.0

The table indicates overall risk and cash flow that is generated from the hedging

strategy. Moreover, the evaluation of calculation indicates that unhedged strategy has the

highest risk involved from investment, as the company does not know about the actual

6

Strategy (Option Hedge Put Option) Value Value

Payment in 1 year € 50,000,000.0

Put option 1.110

Exercise price 0.060

Total value of put option 1.050 $ 52,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.150 $ 7,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.250 $ 12,500,000.0

Strategy (Option Hedge Call Option) Value Value

Payment in 1 year € 50,000,000.0

Cal option 1.150

Exercise price 0.080

Total value of put option 1.070 $ 53,500,000.0

Up-Probability $ 1.200 $ 60,000,000.0

Hedge (Loss) $ 0.130 $ 6,500,000.0

Down-Probability $ 0.800 $ 40,000,000.0

Hedge (Profit) $ 0.270 $ 13,500,000.0

The table indicates overall risk and cash flow that is generated from the hedging

strategy. Moreover, the evaluation of calculation indicates that unhedged strategy has the

highest risk involved from investment, as the company does not know about the actual

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TREASURY AND RISK MANAGEMENT

7

payment, which will be reduced over the period of one year. Furthermore, the risk reduction

is conducted by reducing adequate hedging strategies, such as forward strategy, money

market strategy and option strategy (Brooks 2015).

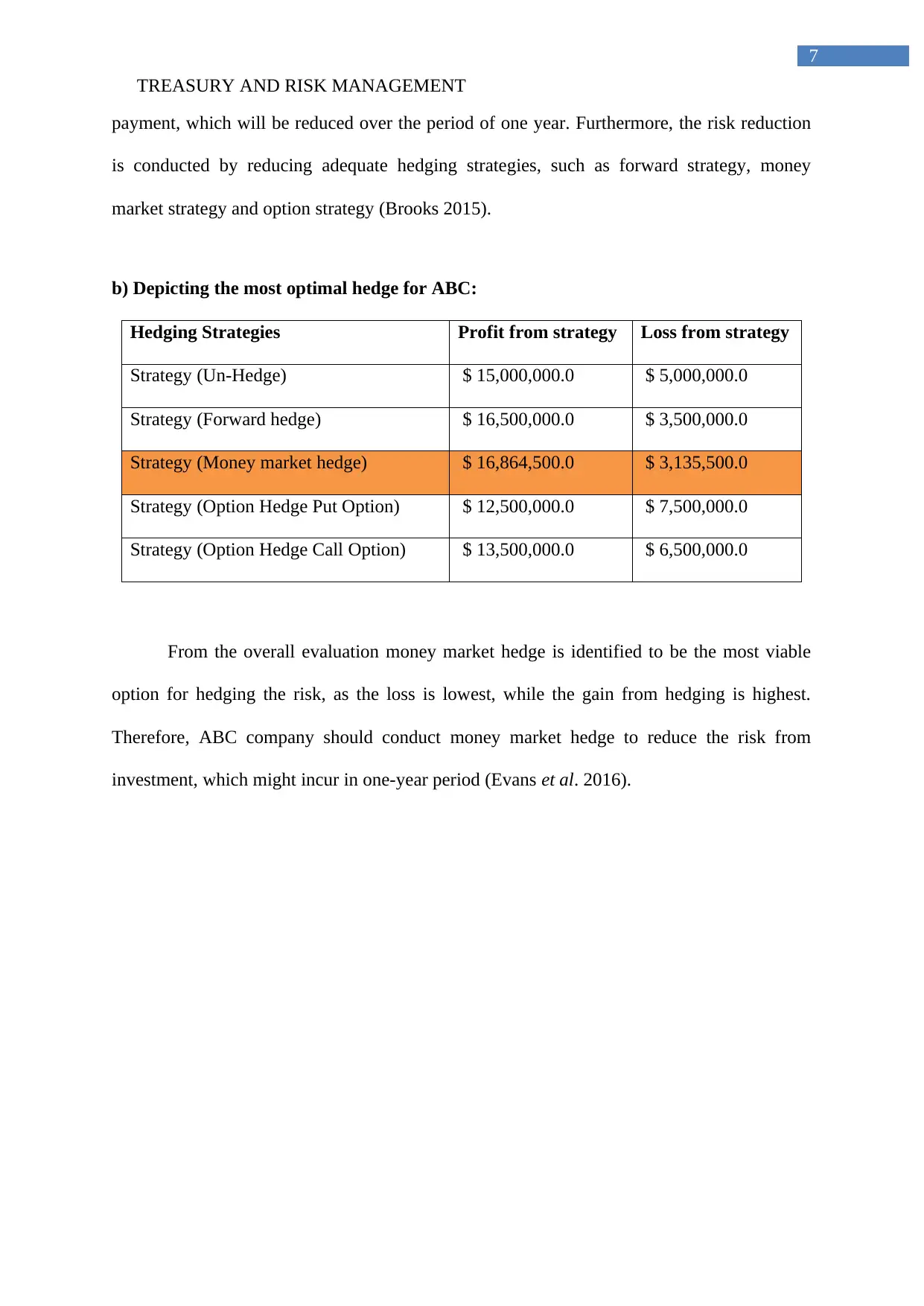

b) Depicting the most optimal hedge for ABC:

Hedging Strategies Profit from strategy Loss from strategy

Strategy (Un-Hedge) $ 15,000,000.0 $ 5,000,000.0

Strategy (Forward hedge) $ 16,500,000.0 $ 3,500,000.0

Strategy (Money market hedge) $ 16,864,500.0 $ 3,135,500.0

Strategy (Option Hedge Put Option) $ 12,500,000.0 $ 7,500,000.0

Strategy (Option Hedge Call Option) $ 13,500,000.0 $ 6,500,000.0

From the overall evaluation money market hedge is identified to be the most viable

option for hedging the risk, as the loss is lowest, while the gain from hedging is highest.

Therefore, ABC company should conduct money market hedge to reduce the risk from

investment, which might incur in one-year period (Evans et al. 2016).

7

payment, which will be reduced over the period of one year. Furthermore, the risk reduction

is conducted by reducing adequate hedging strategies, such as forward strategy, money

market strategy and option strategy (Brooks 2015).

b) Depicting the most optimal hedge for ABC:

Hedging Strategies Profit from strategy Loss from strategy

Strategy (Un-Hedge) $ 15,000,000.0 $ 5,000,000.0

Strategy (Forward hedge) $ 16,500,000.0 $ 3,500,000.0

Strategy (Money market hedge) $ 16,864,500.0 $ 3,135,500.0

Strategy (Option Hedge Put Option) $ 12,500,000.0 $ 7,500,000.0

Strategy (Option Hedge Call Option) $ 13,500,000.0 $ 6,500,000.0

From the overall evaluation money market hedge is identified to be the most viable

option for hedging the risk, as the loss is lowest, while the gain from hedging is highest.

Therefore, ABC company should conduct money market hedge to reduce the risk from

investment, which might incur in one-year period (Evans et al. 2016).

TREASURY AND RISK MANAGEMENT

8

Reference and Bibliography:

Alamgir, M., 2015. Treasury Operations of Banks in Bangladesh: Issues and

Challenges. MERC Global’s International Journal of Social Science & Management, 2(2),

pp.96-118.

Bakke, T.E., Mahmudi, H., Fernando, C.S. and Salas, J.M., 2016. The causal effect of option

pay on corporate risk management. Journal of Financial Economics, 120(3), pp.623-643.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management.

Cengage Learning.

DeAngelo, H. and Stulz, R.M., 2015. Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), pp.219-236.

Evans, C., Fisher, J., Gourio, F. and Krane, S., 2016. Risk management for monetary policy

near the zero lower bound. Brookings Papers on Economic Activity, 2015(1), pp.141-219.

Hopkin, P., 2017. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

The Economist. (2018). Why the Swiss unpegged the franc. [online] Available at:

https://www.economist.com/blogs/economist-explains/2015/01/economist-explains-13

[Accessed 23 Mar. 2018].

8

Reference and Bibliography:

Alamgir, M., 2015. Treasury Operations of Banks in Bangladesh: Issues and

Challenges. MERC Global’s International Journal of Social Science & Management, 2(2),

pp.96-118.

Bakke, T.E., Mahmudi, H., Fernando, C.S. and Salas, J.M., 2016. The causal effect of option

pay on corporate risk management. Journal of Financial Economics, 120(3), pp.623-643.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management.

Cengage Learning.

DeAngelo, H. and Stulz, R.M., 2015. Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), pp.219-236.

Evans, C., Fisher, J., Gourio, F. and Krane, S., 2016. Risk management for monetary policy

near the zero lower bound. Brookings Papers on Economic Activity, 2015(1), pp.141-219.

Hopkin, P., 2017. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

The Economist. (2018). Why the Swiss unpegged the franc. [online] Available at:

https://www.economist.com/blogs/economist-explains/2015/01/economist-explains-13

[Accessed 23 Mar. 2018].

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.