Analyzing FX Trading Profitability and Hedging Strategies for Risk

VerifiedAdded on 2023/04/21

|7

|837

|340

Report

AI Summary

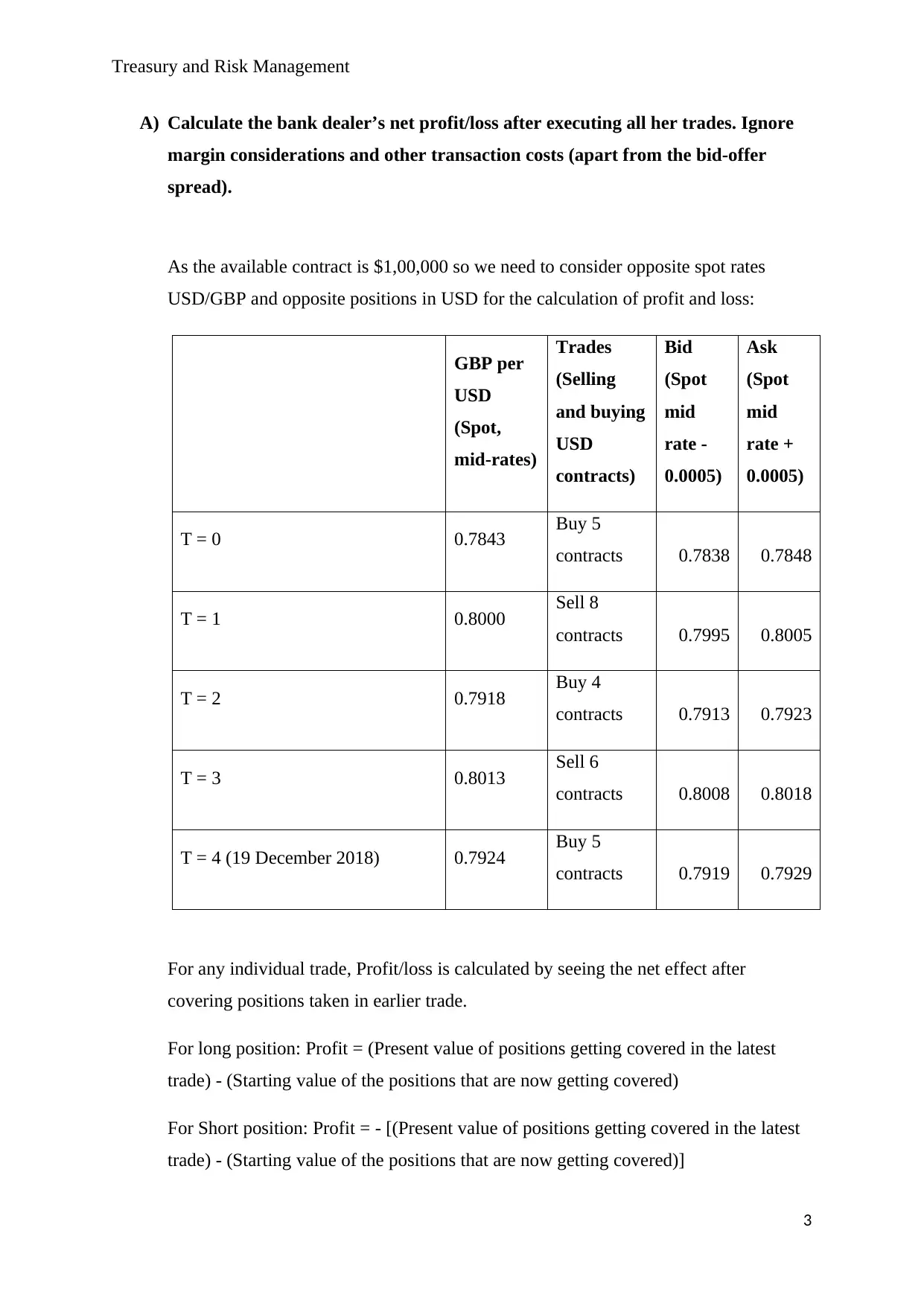

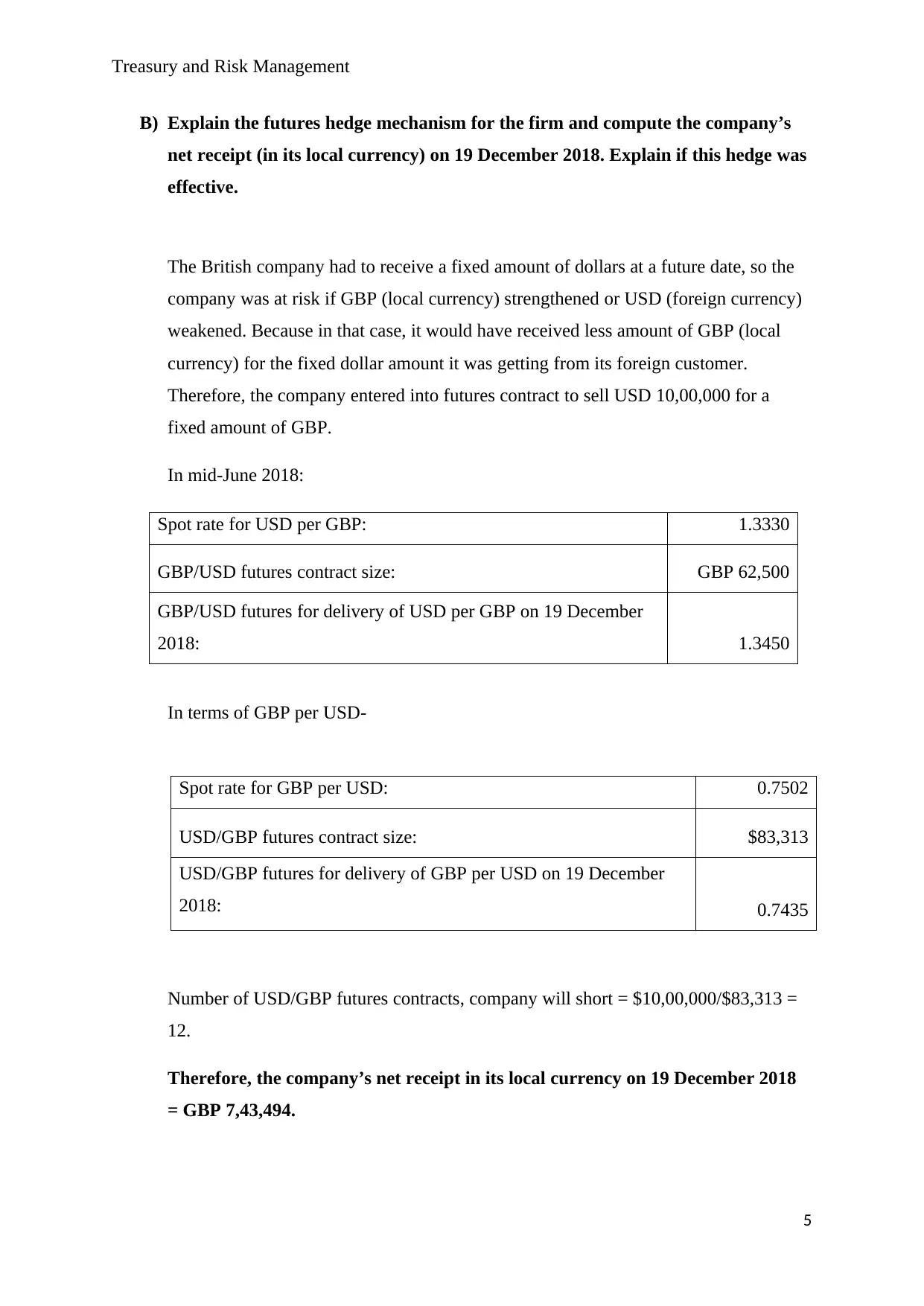

This report assesses a bank dealer's net profit/loss from foreign currency trades involving the British pound against the US dollar, considering bid-offer spreads. It then explains the futures hedge mechanism employed by a British company to mitigate currency risk associated with receiving a fixed amount of US dollars at a future date. The report calculates the company's net receipt in its local currency on December 19, 2018, and evaluates the effectiveness of the hedge by comparing the hedged outcome with an unhedged scenario. The analysis incorporates spot rates and futures contract details to determine whether the hedging strategy provided a beneficial outcome for the company, considering the fluctuations in currency values during the period. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.