ACC5202 Semester 1 Assignment: Trial Balance and Financial Statements

VerifiedAdded on 2023/06/12

|15

|3630

|114

Homework Assignment

AI Summary

This accounting assignment solution addresses various aspects of financial accounting, including the importance of the trial balance, error identification and correction, application of the matching principle, and the preparation of journal entries and financial statements. It covers topics such as adjusting entries, qualitative characteristics of financial information as per IASB, and methods for calculating allowance for bad debts. The solution includes detailed explanations and calculations, providing a comprehensive understanding of the concepts and their practical application. Desklib offers a wide range of solved assignments and past papers to aid students in their studies.

Solution-1

Part-A

(i) It is true that trial balance is very important statement; this is so because trial balance gives a

bird’s eye view of the entire transactions posted in the books. In other words, it is the

summary of the entries posted in the general ledgers. With the help of trial balance, the other

financial statements like balance sheet, income statement, etc. are prepared, without trial

balance one cannot think of preparing these statements (Accounting-simplified.com, 2018).

(ii) No, this is not correct to assume that if the trial balance “balances”, then the books are

correct. Because the trial balance cannot highlight the compensating error like error of

omission or error of commission. The examples of such errors are if the amount required to

be posted to the fuel account is posted to the maintenance account, so this error will not be

reflected by trial balance, since it is an error of commission, similarly if an entry is omitted to

be posted in the books, then also it will not affect the trial balance (Accounting-

simplified.com, 2018).

Part-B

Would the error

cause the Trial

Balance not to

balance

Which

accounts

would be

affected and

how?

How would the

error be corrected

Effect on Trial

Balance totals

Yes No Debit Credit

Example A payment for wages of

$500 was credited to cash correctly

but debited to wages twice expense.

Yes Wages

expense

Debit side of Wages

Expense reduced by

500

$ (500)

1. The Accrued Wages account with

a balance of $500 was omitted from

the Trial Balance.

Yes Accrued

Wages

Credit side of

Accrued Wages to be

increased by 500

$ 500

2. A payment of $490 for Prepaid

Rent was only posted to the Cash at

Bank account and not to Prepaid

Rent

Yes Prepaid Rent

Debit side of Prepaid

rent account to be

increased by 490

$ 490

3. A debit of $458 to Cash at Bank

was posted as $485. The credit entry

was correct.

Yes Cash at bank

Debit side of cash at

bank account to be

reduced by $27

$ (27)

4. A credit of $600 to Accounts

Payable should have been made to

Fees Revenue

No

Accounts

Payable, Fees

revenue

Credit side of

accounts payable to

be reduced by $600,

and credit side of

fees revenue account

is increased by $600

$ -

5. A Dr for a cash receipt of $500

from customers in settlement of their

accounts was posted twice as a DR to

the Cash at Bank and a Dr to

Yes Cash at bank

Debit side of cash at

bank account to be

reduced by $500

$ (500)

Part-A

(i) It is true that trial balance is very important statement; this is so because trial balance gives a

bird’s eye view of the entire transactions posted in the books. In other words, it is the

summary of the entries posted in the general ledgers. With the help of trial balance, the other

financial statements like balance sheet, income statement, etc. are prepared, without trial

balance one cannot think of preparing these statements (Accounting-simplified.com, 2018).

(ii) No, this is not correct to assume that if the trial balance “balances”, then the books are

correct. Because the trial balance cannot highlight the compensating error like error of

omission or error of commission. The examples of such errors are if the amount required to

be posted to the fuel account is posted to the maintenance account, so this error will not be

reflected by trial balance, since it is an error of commission, similarly if an entry is omitted to

be posted in the books, then also it will not affect the trial balance (Accounting-

simplified.com, 2018).

Part-B

Would the error

cause the Trial

Balance not to

balance

Which

accounts

would be

affected and

how?

How would the

error be corrected

Effect on Trial

Balance totals

Yes No Debit Credit

Example A payment for wages of

$500 was credited to cash correctly

but debited to wages twice expense.

Yes Wages

expense

Debit side of Wages

Expense reduced by

500

$ (500)

1. The Accrued Wages account with

a balance of $500 was omitted from

the Trial Balance.

Yes Accrued

Wages

Credit side of

Accrued Wages to be

increased by 500

$ 500

2. A payment of $490 for Prepaid

Rent was only posted to the Cash at

Bank account and not to Prepaid

Rent

Yes Prepaid Rent

Debit side of Prepaid

rent account to be

increased by 490

$ 490

3. A debit of $458 to Cash at Bank

was posted as $485. The credit entry

was correct.

Yes Cash at bank

Debit side of cash at

bank account to be

reduced by $27

$ (27)

4. A credit of $600 to Accounts

Payable should have been made to

Fees Revenue

No

Accounts

Payable, Fees

revenue

Credit side of

accounts payable to

be reduced by $600,

and credit side of

fees revenue account

is increased by $600

$ -

5. A Dr for a cash receipt of $500

from customers in settlement of their

accounts was posted twice as a DR to

the Cash at Bank and a Dr to

Yes Cash at bank

Debit side of cash at

bank account to be

reduced by $500

$ (500)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

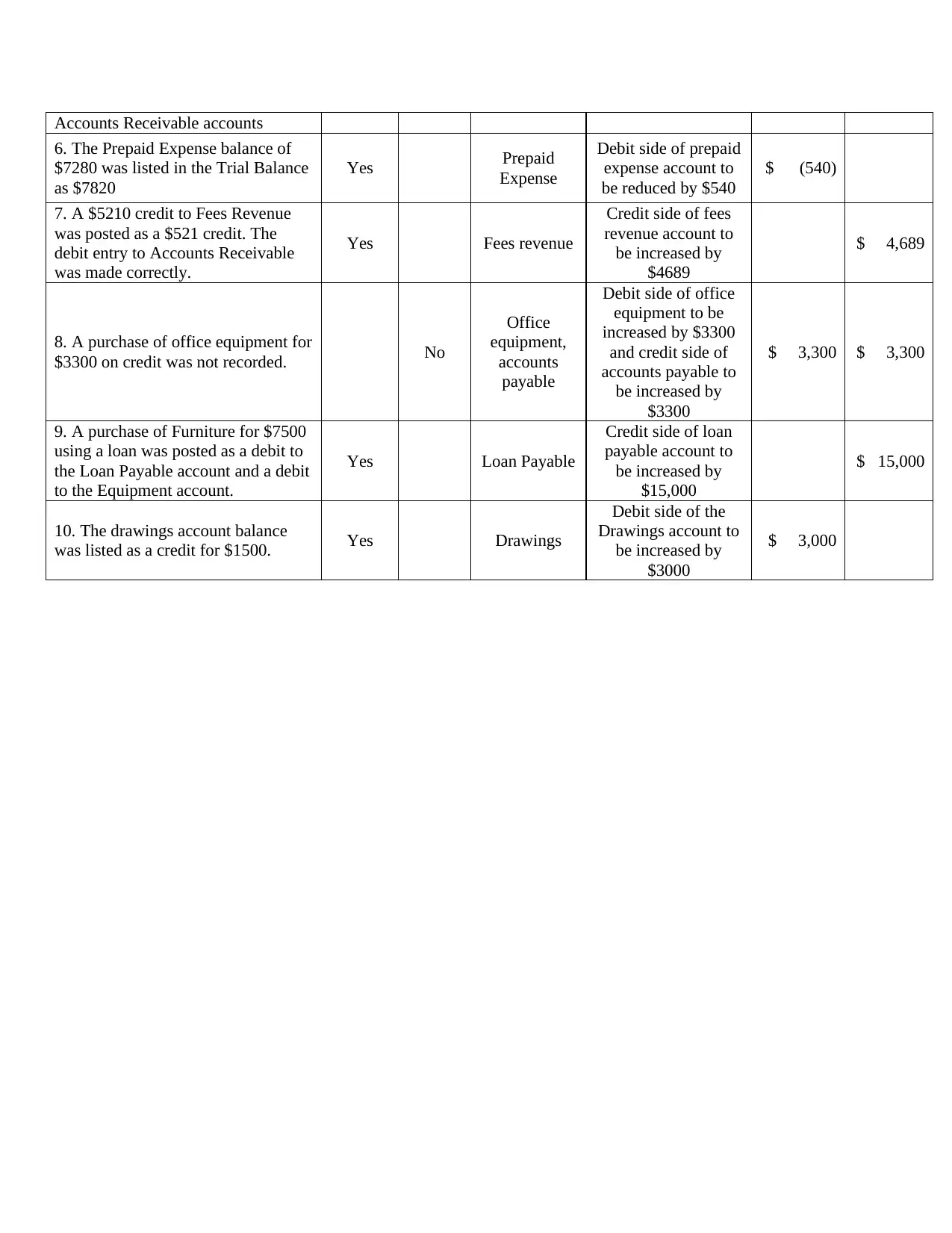

Accounts Receivable accounts

6. The Prepaid Expense balance of

$7280 was listed in the Trial Balance

as $7820

Yes Prepaid

Expense

Debit side of prepaid

expense account to

be reduced by $540

$ (540)

7. A $5210 credit to Fees Revenue

was posted as a $521 credit. The

debit entry to Accounts Receivable

was made correctly.

Yes Fees revenue

Credit side of fees

revenue account to

be increased by

$4689

$ 4,689

8. A purchase of office equipment for

$3300 on credit was not recorded. No

Office

equipment,

accounts

payable

Debit side of office

equipment to be

increased by $3300

and credit side of

accounts payable to

be increased by

$3300

$ 3,300 $ 3,300

9. A purchase of Furniture for $7500

using a loan was posted as a debit to

the Loan Payable account and a debit

to the Equipment account.

Yes Loan Payable

Credit side of loan

payable account to

be increased by

$15,000

$ 15,000

10. The drawings account balance

was listed as a credit for $1500. Yes Drawings

Debit side of the

Drawings account to

be increased by

$3000

$ 3,000

6. The Prepaid Expense balance of

$7280 was listed in the Trial Balance

as $7820

Yes Prepaid

Expense

Debit side of prepaid

expense account to

be reduced by $540

$ (540)

7. A $5210 credit to Fees Revenue

was posted as a $521 credit. The

debit entry to Accounts Receivable

was made correctly.

Yes Fees revenue

Credit side of fees

revenue account to

be increased by

$4689

$ 4,689

8. A purchase of office equipment for

$3300 on credit was not recorded. No

Office

equipment,

accounts

payable

Debit side of office

equipment to be

increased by $3300

and credit side of

accounts payable to

be increased by

$3300

$ 3,300 $ 3,300

9. A purchase of Furniture for $7500

using a loan was posted as a debit to

the Loan Payable account and a debit

to the Equipment account.

Yes Loan Payable

Credit side of loan

payable account to

be increased by

$15,000

$ 15,000

10. The drawings account balance

was listed as a credit for $1500. Yes Drawings

Debit side of the

Drawings account to

be increased by

$3000

$ 3,000

Solution-2

Part-A

Matching principle is the basic accounting principle, which states that the expenses should be booked in

the period in which associated income is booked. This principle works best with accrual method of

accounting, but is not in line with cash method of accounting. Under accrual method of accounting, the

expenses are booked on accrual basis, i.e. when they are incurred, irrespective of when their payment is

made, whereas under cash basis of accounting, expenses are booked when they are actually paid in cash.

So, if a company pays commission on its sales, which is required to be paid in the following month of

sale let’s say for December sales, the commission is payable in January. So, matching principle and

accrual method of accounting requires the company to account for commission payable in December only

whereas cash method of accounting requires the commission to be accounted for in January, i.e. when it is

paid (AccountingCoach.com, 2018).

Part-B

(i) Journal entries in the books of J. Jackson for the year ended 30th June, 2018

Sr. No. Particulars Debit ($) Credit ($)

(i) Wages expense (21000/5*2) 8,400

To Wages payable 8,400

(To record the wages payable for the 2 days in June, 18)

(ii) Commission fees receivable 1,520

To Commission fees 1,520

(To record income earned but not received)

(iii) Prepaid Rent (36000/12*7) 21,000

To Rent expense 21,000

(To record prepaid rent)

(iv) Interest receivable (25,000*6%*1/4) 375

To Interest income 375

(To record interest earned but not received)

(v) Unearned revenue (12000*30%) 3,600

To Revenue 3,600

(To record revenue earned)

(vi) Office furniture 6,000

To Office expenses 6,000

(To record the rectifying entry)

(vii) Supplies expense (800+5200-1500) 4,500

To Office supplies 4,500

(To record consumption of office supplies)

(viii) GST Collected 7,960

To GST Paid 7,960

(To record the settlement of amounts)

Part-A

Matching principle is the basic accounting principle, which states that the expenses should be booked in

the period in which associated income is booked. This principle works best with accrual method of

accounting, but is not in line with cash method of accounting. Under accrual method of accounting, the

expenses are booked on accrual basis, i.e. when they are incurred, irrespective of when their payment is

made, whereas under cash basis of accounting, expenses are booked when they are actually paid in cash.

So, if a company pays commission on its sales, which is required to be paid in the following month of

sale let’s say for December sales, the commission is payable in January. So, matching principle and

accrual method of accounting requires the company to account for commission payable in December only

whereas cash method of accounting requires the commission to be accounted for in January, i.e. when it is

paid (AccountingCoach.com, 2018).

Part-B

(i) Journal entries in the books of J. Jackson for the year ended 30th June, 2018

Sr. No. Particulars Debit ($) Credit ($)

(i) Wages expense (21000/5*2) 8,400

To Wages payable 8,400

(To record the wages payable for the 2 days in June, 18)

(ii) Commission fees receivable 1,520

To Commission fees 1,520

(To record income earned but not received)

(iii) Prepaid Rent (36000/12*7) 21,000

To Rent expense 21,000

(To record prepaid rent)

(iv) Interest receivable (25,000*6%*1/4) 375

To Interest income 375

(To record interest earned but not received)

(v) Unearned revenue (12000*30%) 3,600

To Revenue 3,600

(To record revenue earned)

(vi) Office furniture 6,000

To Office expenses 6,000

(To record the rectifying entry)

(vii) Supplies expense (800+5200-1500) 4,500

To Office supplies 4,500

(To record consumption of office supplies)

(viii) GST Collected 7,960

To GST Paid 7,960

(To record the settlement of amounts)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ii) Calculation of new profit figure

Particulars Amount ($)

Old Profit 3,281,001

Adjustments

(Increase) / decrease in expense

Wages expense (8,400)

Rent expense 21,000

Office furniture purchased 6,000

Supplies expenses (4,500) 14,100

Increase / (decrease) in income

Commission fees 1,520

Interest income 375

Unearned revenue 3,600 5,495

Revised Profit 3,300,596

The revised profit is $3,300,596.

Particulars Amount ($)

Old Profit 3,281,001

Adjustments

(Increase) / decrease in expense

Wages expense (8,400)

Rent expense 21,000

Office furniture purchased 6,000

Supplies expenses (4,500) 14,100

Increase / (decrease) in income

Commission fees 1,520

Interest income 375

Unearned revenue 3,600 5,495

Revised Profit 3,300,596

The revised profit is $3,300,596.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution-3

Part-A

The four qualitative characteristics as mentioned in IASB’s conceptual framework are (Jan, 2018):

(a) Relevance – Means the financial information should be relevant and useful to the users of the

financial statements.

(b) Materiality – All the possible information affecting the users of the financial statements should be

disclosed

(c) Faithful representation – The financial information should be free from errors and should reflect

true and fair view.

(d) Comparability – The financial information should be comparable with the financial information

of other companies or for previous years.

Part-B (i)

HARDYARDS ACCOUNTING SERVICES

Worksheet for period ended 30th June, 2018

Account Adjusted Trial Balance Income Statement Balance Sheet

Debit Credit Debit Credit Debit Credit

Cash at Bank 14,900 14,900

Accounts Receivable 25,825 25,825

Prepaid Expenses 2,200 2,200

Office Supplies 6,160 6,160

Accrued Revenue 2,540 2,540

GST Paid 26,000 26,000

Equipment 163,000 163,000

Accumulated Depreciation 28,000 28,000

Accounts Payable 6,320 6,320

Loan Payable 55,000 55,000

Salaries Payable 1,930 1,930

GST Collected 32,740 32,740

Unearned Revenue 2,750 2,750

B. Bright Capital 50,000 50,000

B. Bright Drawings 5,000 5,000

Painting Revenue 204,055 204,055

Wages Expenses 100,020 100,020

Rent Expense 6,550 6,550

Depreciation Expense 11,000 11,000

Marketing Expense 5,520 5,520

Office Supplies Expense 6,180 6,180

Interest on Loan Expense 5,900 5,900

380,795 380,795 135,170 204,055 245,625 176,740

Profit 68,885

Part-A

The four qualitative characteristics as mentioned in IASB’s conceptual framework are (Jan, 2018):

(a) Relevance – Means the financial information should be relevant and useful to the users of the

financial statements.

(b) Materiality – All the possible information affecting the users of the financial statements should be

disclosed

(c) Faithful representation – The financial information should be free from errors and should reflect

true and fair view.

(d) Comparability – The financial information should be comparable with the financial information

of other companies or for previous years.

Part-B (i)

HARDYARDS ACCOUNTING SERVICES

Worksheet for period ended 30th June, 2018

Account Adjusted Trial Balance Income Statement Balance Sheet

Debit Credit Debit Credit Debit Credit

Cash at Bank 14,900 14,900

Accounts Receivable 25,825 25,825

Prepaid Expenses 2,200 2,200

Office Supplies 6,160 6,160

Accrued Revenue 2,540 2,540

GST Paid 26,000 26,000

Equipment 163,000 163,000

Accumulated Depreciation 28,000 28,000

Accounts Payable 6,320 6,320

Loan Payable 55,000 55,000

Salaries Payable 1,930 1,930

GST Collected 32,740 32,740

Unearned Revenue 2,750 2,750

B. Bright Capital 50,000 50,000

B. Bright Drawings 5,000 5,000

Painting Revenue 204,055 204,055

Wages Expenses 100,020 100,020

Rent Expense 6,550 6,550

Depreciation Expense 11,000 11,000

Marketing Expense 5,520 5,520

Office Supplies Expense 6,180 6,180

Interest on Loan Expense 5,900 5,900

380,795 380,795 135,170 204,055 245,625 176,740

Profit 68,885

Total 245,625 245,625

(iii) Closing entries in the journal

Sr. No. Particulars Debit ($) Credit ($)

1 Painting Revenue 204,055

To Income Summary 204,055

2 Income Summary 135,170

To Wages expense 100,020

To Rent expense 6,550

To Depreciation expense 11,000

To Marketing expense 5,520

To Office supplies expense 6,180

To Interest on loan expense 5,900

3 Income summary 68,885

To Retained earnings 68,885

4 B. Bright Capital 5,000

To B. Bright Drawings 5,000

(iii) Closing entries in the journal

Sr. No. Particulars Debit ($) Credit ($)

1 Painting Revenue 204,055

To Income Summary 204,055

2 Income Summary 135,170

To Wages expense 100,020

To Rent expense 6,550

To Depreciation expense 11,000

To Marketing expense 5,520

To Office supplies expense 6,180

To Interest on loan expense 5,900

3 Income summary 68,885

To Retained earnings 68,885

4 B. Bright Capital 5,000

To B. Bright Drawings 5,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-4

Part-A

(a) No, the way the credit are offered will not change, however the process will change at the end of

the businesses as now instead of collecting the debts on their own, they will hire the factors who

will collect the debts on their behalf. They need to incur additional factoring costs for this.

(b) Yes, the firms will no longer be required to monitor their receivables. Factoring means

outsourcing the collections of debts to the third party.

(c) Not allowing the bad and doubtful debts will make the profit and loss account reflect the false

picture with overstated profits and overstated accounts receivable.

Part-B

(i) Journal Entries for June

Sr. No. Particulars Debit ($) Credit ($)

(i) Allowance for Doubtful Debts 11,510

To Accounts Receivable 11,510

(To record for bad debts written off)

(ii) Cash (99550*20%) 19,910

Accounts receivable (99550*80%) 79,640

To GST Collected (99550/110%*10%) 9,050

To Sales (99,550/110%) 90,500

(To record sales during the month)

(iii) Cash 121,600

To Accounts receivable 121,600

(To record cash collected from customers)

(iv) Accounts receivable 1,870

To Allowance for Doubtful Debts 1,870

(To record reversal of accounts receivable)

Cash 1,870

To Accounts receivable 1,870

(To record cash collected from customers)

(v) Accounts receivable 2,200

To Sales 2,200

(To record sale not recorded earlier)

(vi) Bad debts expense 13,075

To Allowance for Doubtful Debts 13,075

(To record bad debts expense)

Part-A

(a) No, the way the credit are offered will not change, however the process will change at the end of

the businesses as now instead of collecting the debts on their own, they will hire the factors who

will collect the debts on their behalf. They need to incur additional factoring costs for this.

(b) Yes, the firms will no longer be required to monitor their receivables. Factoring means

outsourcing the collections of debts to the third party.

(c) Not allowing the bad and doubtful debts will make the profit and loss account reflect the false

picture with overstated profits and overstated accounts receivable.

Part-B

(i) Journal Entries for June

Sr. No. Particulars Debit ($) Credit ($)

(i) Allowance for Doubtful Debts 11,510

To Accounts Receivable 11,510

(To record for bad debts written off)

(ii) Cash (99550*20%) 19,910

Accounts receivable (99550*80%) 79,640

To GST Collected (99550/110%*10%) 9,050

To Sales (99,550/110%) 90,500

(To record sales during the month)

(iii) Cash 121,600

To Accounts receivable 121,600

(To record cash collected from customers)

(iv) Accounts receivable 1,870

To Allowance for Doubtful Debts 1,870

(To record reversal of accounts receivable)

Cash 1,870

To Accounts receivable 1,870

(To record cash collected from customers)

(v) Accounts receivable 2,200

To Sales 2,200

(To record sale not recorded earlier)

(vi) Bad debts expense 13,075

To Allowance for Doubtful Debts 13,075

(To record bad debts expense)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(ii) Ledger Accounts

Accounts Receivable

Date Particulars Dr Cr Balance

01-Jun Opening balance $265,400 $ 265,400

30-June Allowance for doubtful debts $ 11,510 $ 253,890

30-June GST Collected $ 7,240 $ 261,130

30-June Sales $ 72,400 $ 333,530

30-June Cash $121,600 $ 211,930

30-June Allowance for doubtful debts $ 1,870 $ 213,800

30-June Cash $ 1,870 $ 211,930

30-June Sales $ 2,200 $ 214,130

Allowance for Doubtful Debts

Date Particulars Dr Cr Balance

01-Jun Opening balance $ 15,565 $ (15,565)

30-June Accounts receivable $ 11,510 $ (4,055)

30-June Accounts receivable $ 1,870 $ (5,925)

30-June Bad debts expense $ 13,075 $ (19,000)

Cash at Bank

Date Particulars Dr Cr Balance

01-Jun Opening balance $106,000 $ 106,000

30-June GST Collected $ 1,810 $ 107,810

30-June Sales $ 18,100 $ 125,910

30-June Accounts receivable $121,600 $ 247,510

30-June Accounts receivable $ 1,870 $ 249,380

Sales

Date Particulars Dr Cr Balance

01-Jun Opening balance $878,490 $(878,490)

30-June Cash $ 18,100 $(896,590)

30-June Accounts receivable $ 72,400 $(968,990)

30-June Accounts receivable $ 2,200 $(971,190)

GST Collected

Date Particulars Dr Cr Balance

Accounts Receivable

Date Particulars Dr Cr Balance

01-Jun Opening balance $265,400 $ 265,400

30-June Allowance for doubtful debts $ 11,510 $ 253,890

30-June GST Collected $ 7,240 $ 261,130

30-June Sales $ 72,400 $ 333,530

30-June Cash $121,600 $ 211,930

30-June Allowance for doubtful debts $ 1,870 $ 213,800

30-June Cash $ 1,870 $ 211,930

30-June Sales $ 2,200 $ 214,130

Allowance for Doubtful Debts

Date Particulars Dr Cr Balance

01-Jun Opening balance $ 15,565 $ (15,565)

30-June Accounts receivable $ 11,510 $ (4,055)

30-June Accounts receivable $ 1,870 $ (5,925)

30-June Bad debts expense $ 13,075 $ (19,000)

Cash at Bank

Date Particulars Dr Cr Balance

01-Jun Opening balance $106,000 $ 106,000

30-June GST Collected $ 1,810 $ 107,810

30-June Sales $ 18,100 $ 125,910

30-June Accounts receivable $121,600 $ 247,510

30-June Accounts receivable $ 1,870 $ 249,380

Sales

Date Particulars Dr Cr Balance

01-Jun Opening balance $878,490 $(878,490)

30-June Cash $ 18,100 $(896,590)

30-June Accounts receivable $ 72,400 $(968,990)

30-June Accounts receivable $ 2,200 $(971,190)

GST Collected

Date Particulars Dr Cr Balance

01-Jun Opening balance

30-June Cash $ 1,810 $ (1,810)

30-June Accounts receivable $ 7,240 $ (9,050)

Bad debt expense

Date Particulars Dr Cr Balance

01-Jun Opening balance

30-June Allowance for doubtful debts $ 13,075 $ 13,075

(iii) Classified Income Statement and Balance Sheet

Extract Income Statement in the books of Homewares Company Ltd

Particulars Amount ($)

Income

Sales $ 971,190

Expense

Bad debts expense $ 13,075

Extract Balance Sheet in the books of Homewares Company Ltd

Particulars Amount ($)

Assets

Current assets

Accounts receivables $ 214,130

Less: Allowance for doubtful debts $ (19,000) $ 195,130

Cash $ 249,380

Total Assets $ 444,510

Liabilities

Current liabilities

GST Collected $ 9,050 $ 9,050

Total Liabilities $ 9,050

(iv) The two methods that can be used to calculate allowance for bad debts are (Cliffsnotes.com,

2018):

a. Percentage of credit sales method – In this method, bad debts are taken at a percentage of

credit sales made during the year.

b. Ageing of debtors method – In this method, debtors outstanding beyond a specified

period say 1 year are taken for provisioning.

Solution-5

30-June Cash $ 1,810 $ (1,810)

30-June Accounts receivable $ 7,240 $ (9,050)

Bad debt expense

Date Particulars Dr Cr Balance

01-Jun Opening balance

30-June Allowance for doubtful debts $ 13,075 $ 13,075

(iii) Classified Income Statement and Balance Sheet

Extract Income Statement in the books of Homewares Company Ltd

Particulars Amount ($)

Income

Sales $ 971,190

Expense

Bad debts expense $ 13,075

Extract Balance Sheet in the books of Homewares Company Ltd

Particulars Amount ($)

Assets

Current assets

Accounts receivables $ 214,130

Less: Allowance for doubtful debts $ (19,000) $ 195,130

Cash $ 249,380

Total Assets $ 444,510

Liabilities

Current liabilities

GST Collected $ 9,050 $ 9,050

Total Liabilities $ 9,050

(iv) The two methods that can be used to calculate allowance for bad debts are (Cliffsnotes.com,

2018):

a. Percentage of credit sales method – In this method, bad debts are taken at a percentage of

credit sales made during the year.

b. Ageing of debtors method – In this method, debtors outstanding beyond a specified

period say 1 year are taken for provisioning.

Solution-5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part-A

(i) Calculation of the value of the machine for depreciation purposes

As per AASB 116, the cost of asset includes initial purchase price, any costs directly

attributable to bringing the asset to the location and condition necessary for it to be capable of

operating as per intended use. Hence, the following costs will become part of the asset cost.

Particulars

Is it a part of

asset? Remarks

Initial price paid to the supplier Yes

Purchase cost is part of asset cost as per

AASB 116

Cost to deliver the machine to the site Yes

Delivery costs are part of asset cost as per

AASB 116

Amount to paint the company name on the

machine No Not required for putting machine to use

Amount paid to an engineer to fit the

machine ready for work Yes

Installation costs are part of asset cost as

per AASB 116

Repairs to the factory door damaged when

bringing in the machine No

Since, it is not related to machine and

would come under repairs

Repairs made to replace bolts which had

dislodged during transit Yes

As it is mandatory for putting machine to

use

Particulars Amount ($)

Initial price paid to the supplier $65,000

Cost to deliver the machine to the site $3,500

Amount paid to an engineer to fit the machine ready for work $14,500

Repairs made to replace bolts which had dislodged during

transit $1,500

Total Machine Cost $84,500

(ii) The best method would be straight line depreciation method.

I. Depreciation under SLM using years as life (84,500-7,000)/10 = $7,750

II. Depreciation under SLM using hours as life (84,500-7,000)/100,000*10,000 = $7,750

Assuming 10,000 hours are used in each year

Hence, no change in depreciation under both of the methods, however the depreciation may change in the

2nd method, if the usage of machine hours changes.

(iii) When the fair value of assets differ significantly from its carrying value, then the revaluation

of assets is considered. It is necessary so that the assets reflect true and fair view in the books.

(i) Calculation of the value of the machine for depreciation purposes

As per AASB 116, the cost of asset includes initial purchase price, any costs directly

attributable to bringing the asset to the location and condition necessary for it to be capable of

operating as per intended use. Hence, the following costs will become part of the asset cost.

Particulars

Is it a part of

asset? Remarks

Initial price paid to the supplier Yes

Purchase cost is part of asset cost as per

AASB 116

Cost to deliver the machine to the site Yes

Delivery costs are part of asset cost as per

AASB 116

Amount to paint the company name on the

machine No Not required for putting machine to use

Amount paid to an engineer to fit the

machine ready for work Yes

Installation costs are part of asset cost as

per AASB 116

Repairs to the factory door damaged when

bringing in the machine No

Since, it is not related to machine and

would come under repairs

Repairs made to replace bolts which had

dislodged during transit Yes

As it is mandatory for putting machine to

use

Particulars Amount ($)

Initial price paid to the supplier $65,000

Cost to deliver the machine to the site $3,500

Amount paid to an engineer to fit the machine ready for work $14,500

Repairs made to replace bolts which had dislodged during

transit $1,500

Total Machine Cost $84,500

(ii) The best method would be straight line depreciation method.

I. Depreciation under SLM using years as life (84,500-7,000)/10 = $7,750

II. Depreciation under SLM using hours as life (84,500-7,000)/100,000*10,000 = $7,750

Assuming 10,000 hours are used in each year

Hence, no change in depreciation under both of the methods, however the depreciation may change in the

2nd method, if the usage of machine hours changes.

(iii) When the fair value of assets differ significantly from its carrying value, then the revaluation

of assets is considered. It is necessary so that the assets reflect true and fair view in the books.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part-B

(i) Journal Entries

Sr. No. Particulars Debit ($) Credit ($)

01-Mar-18 Truck 3 130,000

GST paid 13,000

To Cash 30,000

To Loan payable 113,000

(To record purchase of truck)

31-Mar-18 Depreciation 8,543

To Accumulated Depreciation 8,543

(To record depreciation till the date of sale)

31-Mar-18 Accumulated Depreciation 70,980

To Truck 2 70,980

(To record transfer of amount)

31-Mar-18 Cash 44,000

To Truck 2 37,020

To Profit on sale (refer WN-1) 2,980

To GST collected 4,000

(To record sale of truck)

30-Jun-18 Depreciation (130,000*9%/12*4) 3,900

To Accumulated Depreciation 3,900

(To record deprecation for the year end)

Note: GST to be assumed at 10%

WN-1 Calculation of Profit on sale of Truck -2

Given Information Truck 2 Truck 3

Date of purchase 1st July, 2014 1st March, 2018

Purchase cost 108,000 130000

Residual value 12,000 13000

Useful life (years) 8 10

Dep method WDV SLM

Dep rate 25% 9.00%

(i) Journal Entries

Sr. No. Particulars Debit ($) Credit ($)

01-Mar-18 Truck 3 130,000

GST paid 13,000

To Cash 30,000

To Loan payable 113,000

(To record purchase of truck)

31-Mar-18 Depreciation 8,543

To Accumulated Depreciation 8,543

(To record depreciation till the date of sale)

31-Mar-18 Accumulated Depreciation 70,980

To Truck 2 70,980

(To record transfer of amount)

31-Mar-18 Cash 44,000

To Truck 2 37,020

To Profit on sale (refer WN-1) 2,980

To GST collected 4,000

(To record sale of truck)

30-Jun-18 Depreciation (130,000*9%/12*4) 3,900

To Accumulated Depreciation 3,900

(To record deprecation for the year end)

Note: GST to be assumed at 10%

WN-1 Calculation of Profit on sale of Truck -2

Given Information Truck 2 Truck 3

Date of purchase 1st July, 2014 1st March, 2018

Purchase cost 108,000 130000

Residual value 12,000 13000

Useful life (years) 8 10

Dep method WDV SLM

Dep rate 25% 9.00%

Year

ended on Opening WDV Dep

Closing

WDV

30/06/2015 108,000 27,000 81,000

30/06/2016 81,000 20,250 60,750

30/06/2017 60,750 15,188 45,563

31/03/2018 45,563 8,543 37,020

70,980

WDV as on 31st March, 2018 37,020

Sale value (44,000/110%) 40,000

Profit on sale 2,980

(ii) Calculation of depreciation charges if the method of dep is change to SLM for Truck 2

Depreciation on Truck 2 as per WDV method

Year ended on Opening WDV Dep Closing WDV

30/06/2015 108,000 27,000 81,000

30/06/2016 81,000 20,250 60,750

30/06/2017 60,750 15,188 45,563

31/03/2018 45,563 8,542.97 37,020

70,980

Depreciation on Truck 2 as per SLM method

Depreciation rate ((108000-12000)/8)/108000 = 11.11%

Year ended on Opening WDV Dep Closing WDV

30/06/2015 108,000 12,000 96,000

30/06/2016 96,000 12,000 84,000

30/06/2017 84,000 12,000 72,000

31/03/2018 72,000 9,000 63,000

45,000

(iii) Effect on Profit under two methods of depreciation

ended on Opening WDV Dep

Closing

WDV

30/06/2015 108,000 27,000 81,000

30/06/2016 81,000 20,250 60,750

30/06/2017 60,750 15,188 45,563

31/03/2018 45,563 8,543 37,020

70,980

WDV as on 31st March, 2018 37,020

Sale value (44,000/110%) 40,000

Profit on sale 2,980

(ii) Calculation of depreciation charges if the method of dep is change to SLM for Truck 2

Depreciation on Truck 2 as per WDV method

Year ended on Opening WDV Dep Closing WDV

30/06/2015 108,000 27,000 81,000

30/06/2016 81,000 20,250 60,750

30/06/2017 60,750 15,188 45,563

31/03/2018 45,563 8,542.97 37,020

70,980

Depreciation on Truck 2 as per SLM method

Depreciation rate ((108000-12000)/8)/108000 = 11.11%

Year ended on Opening WDV Dep Closing WDV

30/06/2015 108,000 12,000 96,000

30/06/2016 96,000 12,000 84,000

30/06/2017 84,000 12,000 72,000

31/03/2018 72,000 9,000 63,000

45,000

(iii) Effect on Profit under two methods of depreciation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.