Trust Accounts RPL

VerifiedAdded on 2023/01/06

|8

|1453

|33

AI Summary

This document provides a comprehensive study material on trust accounts, including gap assessment, checklist plan, reconciliation, expenses, and more. It covers legislative requirements, testing and tracking compliance, bank balance comparison, cash outflows, reconciliation process, property management, and fraud prevention.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Trust Accounts RPL

Gap Assessment

Gap Assessment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Question1.........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................4

Question 5........................................................................................................................................4

Question 6........................................................................................................................................5

Part 1............................................................................................................................................5

Part 2............................................................................................................................................5

Question 7........................................................................................................................................5

Question 8........................................................................................................................................6

Question 9........................................................................................................................................6

Question 10......................................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Question1.........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................4

Question 5........................................................................................................................................4

Question 6........................................................................................................................................5

Part 1............................................................................................................................................5

Part 2............................................................................................................................................5

Question 7........................................................................................................................................5

Question 8........................................................................................................................................6

Question 9........................................................................................................................................6

Question 10......................................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Question1

There are many trust accounting-software packages offered on the marketplace. Until buying one

of these, ensure that it has the potential to conform with the rule. At the behest of software

vendor, Department of trust accounts scrutinizes complying software programs for the purpose

of ensuring consistency with Uniform Law (NSW) as well as Uniform General Rules of

the Profession 2015 (Uniform Laws). There are certain legislative requirements for supervision

upon trust accounts system, as follows:

Obligatory copies of such classified papers to be printed on monthly basis;

file of trails audited for maintenance;

records and trails of exemption for generated debit balances;

the removal controls of the accounts of the ledger;

the criteria for page numbers and entry transmission;

criteria for mandatory input;

the specifications of the backup facility.

Question 2

Checklist plan which can be employed for testing and tracking compliance with trust

accounts transactions regularly:

Conformity of trust account requirements of Review agency trust accounts: Trust account criteria

in compliance with applicable legislation are specifically defined, correctly registered, and

constantly updated. Appropriate trust account maintenance policies and procedures that satisfy

trust account criteria, core fiscal and accounting standards, organisation protocol, and regulatory

requirements are established.

Establishing and maintaining trust accounts: In accordance with statutory provisions, origins of

trustworthy transaction records are defined and obtained. A trust register documents and

transfers are created to record correctly on behalf of consumers the transactions of the

organisation. Proper authorisations and paperwork endorse transactions and are compatible with

department protocol and regulatory standards. Entries and purchases should be entered timely

and correctly and can be submitted on request in compliance with applicable trust account needs

There are many trust accounting-software packages offered on the marketplace. Until buying one

of these, ensure that it has the potential to conform with the rule. At the behest of software

vendor, Department of trust accounts scrutinizes complying software programs for the purpose

of ensuring consistency with Uniform Law (NSW) as well as Uniform General Rules of

the Profession 2015 (Uniform Laws). There are certain legislative requirements for supervision

upon trust accounts system, as follows:

Obligatory copies of such classified papers to be printed on monthly basis;

file of trails audited for maintenance;

records and trails of exemption for generated debit balances;

the removal controls of the accounts of the ledger;

the criteria for page numbers and entry transmission;

criteria for mandatory input;

the specifications of the backup facility.

Question 2

Checklist plan which can be employed for testing and tracking compliance with trust

accounts transactions regularly:

Conformity of trust account requirements of Review agency trust accounts: Trust account criteria

in compliance with applicable legislation are specifically defined, correctly registered, and

constantly updated. Appropriate trust account maintenance policies and procedures that satisfy

trust account criteria, core fiscal and accounting standards, organisation protocol, and regulatory

requirements are established.

Establishing and maintaining trust accounts: In accordance with statutory provisions, origins of

trustworthy transaction records are defined and obtained. A trust register documents and

transfers are created to record correctly on behalf of consumers the transactions of the

organisation. Proper authorisations and paperwork endorse transactions and are compatible with

department protocol and regulatory standards. Entries and purchases should be entered timely

and correctly and can be submitted on request in compliance with applicable trust account needs

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and organisation specifications. Inconsistencies in entries or documents are immediately

monitored and submitted to the appropriate authority, if required, to ensure clarity or settlement.

Question 3

Start with bank balance and contrast cash inflows or withdrawals on trust accounting

records. Preferably, deposit entries in trust accounting records complement each transaction

on bank statement which should be labelled with washing. If you notice a transaction which does

not lead to any depositing entries in the reports on bank statement, trust-account records are also

incomplete. One must restore the missed entry to records, but must also analyses the accounts to

see if it may have been initially ignored. Please note that the aim is to ensure that all the

transactions that come through bank account represent trust account details so that have to deal

with any concerns if they occur.

Question 4

One will now have to do the same thing in case of cash outflows and disbursements,

after have cleared deposit records. Try comparing with disbursements reported in trust

accounts cheques and withdrawal transfers stated on bank statement. As for deposits, the

majority of withdrawals displayed on bank statement should follow certain details

of disbursement details of trust account. When you're not using disbursement details in

documents, a withdrawal reported in bank statement would need to amend file to fix the errors.

Question 5

When each month ends, one can take some time for completing a reconciliation of trust-

account. Two-way reconciliation matches internal accounts with their trust bank/cash account

operation in one of most critical reviews in trust account administration and helps one to ensure

that their records are reliable, full, and protected from unintentional misrepresentation. The

ultimate purpose of a trust reconciliation procedure is to compare, or transparent, transactions

in trust accounts by matching them to transactions reported on their bank statements to allow an

autonomous accounting of their bank account 's operation. The two documents must be in

complete balance with a balanced trust account.

monitored and submitted to the appropriate authority, if required, to ensure clarity or settlement.

Question 3

Start with bank balance and contrast cash inflows or withdrawals on trust accounting

records. Preferably, deposit entries in trust accounting records complement each transaction

on bank statement which should be labelled with washing. If you notice a transaction which does

not lead to any depositing entries in the reports on bank statement, trust-account records are also

incomplete. One must restore the missed entry to records, but must also analyses the accounts to

see if it may have been initially ignored. Please note that the aim is to ensure that all the

transactions that come through bank account represent trust account details so that have to deal

with any concerns if they occur.

Question 4

One will now have to do the same thing in case of cash outflows and disbursements,

after have cleared deposit records. Try comparing with disbursements reported in trust

accounts cheques and withdrawal transfers stated on bank statement. As for deposits, the

majority of withdrawals displayed on bank statement should follow certain details

of disbursement details of trust account. When you're not using disbursement details in

documents, a withdrawal reported in bank statement would need to amend file to fix the errors.

Question 5

When each month ends, one can take some time for completing a reconciliation of trust-

account. Two-way reconciliation matches internal accounts with their trust bank/cash account

operation in one of most critical reviews in trust account administration and helps one to ensure

that their records are reliable, full, and protected from unintentional misrepresentation. The

ultimate purpose of a trust reconciliation procedure is to compare, or transparent, transactions

in trust accounts by matching them to transactions reported on their bank statements to allow an

autonomous accounting of their bank account 's operation. The two documents must be in

complete balance with a balanced trust account.

For transfers, transfers which have not cleared bank are very normal to have been

reported in trust accounts. In the case of a bill for insurance, for instance, you can write and send

a cheque, but payer drops check or updates his address or misses to file this. All of that will lead

to a pause in cheque, which would be called a non-cleared charge if the cheque has not cleared

up bank at end of month. Any remaining checks must be taken out before disbursement occurs

on bank account and transaction could be cleared through any trust reconciliation. Till

then, monthly reconciliation would have to account with pending payments.

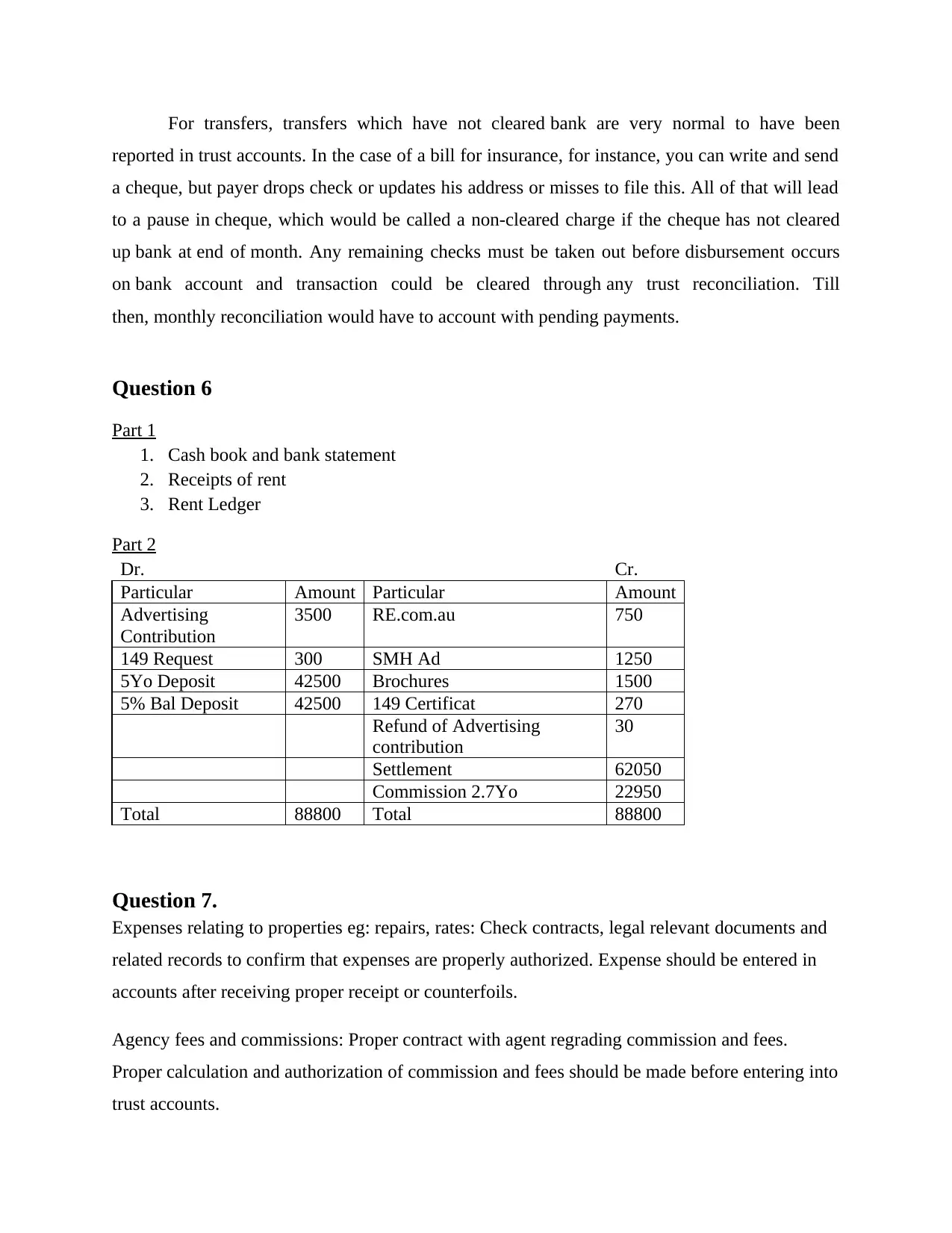

Question 6

Part 1

1. Cash book and bank statement

2. Receipts of rent

3. Rent Ledger

Part 2

Dr. Cr.

Particular Amount Particular Amount

Advertising

Contribution

3500 RE.com.au 750

149 Request 300 SMH Ad 1250

5Yo Deposit 42500 Brochures 1500

5% Bal Deposit 42500 149 Certificat 270

Refund of Advertising

contribution

30

Settlement 62050

Commission 2.7Yo 22950

Total 88800 Total 88800

Question 7.

Expenses relating to properties eg: repairs, rates: Check contracts, legal relevant documents and

related records to confirm that expenses are properly authorized. Expense should be entered in

accounts after receiving proper receipt or counterfoils.

Agency fees and commissions: Proper contract with agent regrading commission and fees.

Proper calculation and authorization of commission and fees should be made before entering into

trust accounts.

reported in trust accounts. In the case of a bill for insurance, for instance, you can write and send

a cheque, but payer drops check or updates his address or misses to file this. All of that will lead

to a pause in cheque, which would be called a non-cleared charge if the cheque has not cleared

up bank at end of month. Any remaining checks must be taken out before disbursement occurs

on bank account and transaction could be cleared through any trust reconciliation. Till

then, monthly reconciliation would have to account with pending payments.

Question 6

Part 1

1. Cash book and bank statement

2. Receipts of rent

3. Rent Ledger

Part 2

Dr. Cr.

Particular Amount Particular Amount

Advertising

Contribution

3500 RE.com.au 750

149 Request 300 SMH Ad 1250

5Yo Deposit 42500 Brochures 1500

5% Bal Deposit 42500 149 Certificat 270

Refund of Advertising

contribution

30

Settlement 62050

Commission 2.7Yo 22950

Total 88800 Total 88800

Question 7.

Expenses relating to properties eg: repairs, rates: Check contracts, legal relevant documents and

related records to confirm that expenses are properly authorized. Expense should be entered in

accounts after receiving proper receipt or counterfoils.

Agency fees and commissions: Proper contract with agent regrading commission and fees.

Proper calculation and authorization of commission and fees should be made before entering into

trust accounts.

Settlement of sale: Proper settlement procedure must be specified to determine settlement

account. Appropriate authorization of sales settlement should be made.

End of month process for property management: Periodic reconciliation shall, in accordance with

statutory provisions, be reviewed by the licensee in authority. Periodic financial accounts are

written with continuous consistency and shared with customers. Records are held to allow them

to be accurately and easily End of month process for property management. Specifications for

legal audit are satisfied.

Question 8

Transactions may be recorded in trust account, but must be redeemed at the end

of month. Banks require time to access deposits — about 1-3 working days — which means that

uncleared transactions generally happen on the final days of month when deposits made. While

these deposits may appear on next month's cash book, in reconciliation at end of month, do have

to take care of them, so please notice that they will be noted later. If one see deposit transaction

which constantly remains uncleared month after month, an mistake has been made and an

alteration is expected.

Question 9

A principal licensee may appoint one LIC for the whole undertaking, or a variety of licensees for

the various sections of the undertaking – provided that they are confident that no portion of the

undertaking can be left unattended. One LIC is responsible for different sector components but

not above one LIC are responsible for same company component. It's the key licensee 's duty to

evaluate its company components. For instance, they may intend to call a LIC with each position

of an entity or enterprise area. Conversely, principal licenses may chooses, as each business

location may have a separate licensee assigned to have been in control of such place of

business, retain the same oversight arrangements they used to have before 23 March 2020.

account. Appropriate authorization of sales settlement should be made.

End of month process for property management: Periodic reconciliation shall, in accordance with

statutory provisions, be reviewed by the licensee in authority. Periodic financial accounts are

written with continuous consistency and shared with customers. Records are held to allow them

to be accurately and easily End of month process for property management. Specifications for

legal audit are satisfied.

Question 8

Transactions may be recorded in trust account, but must be redeemed at the end

of month. Banks require time to access deposits — about 1-3 working days — which means that

uncleared transactions generally happen on the final days of month when deposits made. While

these deposits may appear on next month's cash book, in reconciliation at end of month, do have

to take care of them, so please notice that they will be noted later. If one see deposit transaction

which constantly remains uncleared month after month, an mistake has been made and an

alteration is expected.

Question 9

A principal licensee may appoint one LIC for the whole undertaking, or a variety of licensees for

the various sections of the undertaking – provided that they are confident that no portion of the

undertaking can be left unattended. One LIC is responsible for different sector components but

not above one LIC are responsible for same company component. It's the key licensee 's duty to

evaluate its company components. For instance, they may intend to call a LIC with each position

of an entity or enterprise area. Conversely, principal licenses may chooses, as each business

location may have a separate licensee assigned to have been in control of such place of

business, retain the same oversight arrangements they used to have before 23 March 2020.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 10

1.

Gives restricted access to accounts to employees – not every employee needs complete access to

capital, and only selected employees can manage trust accounts transaction.

Provide the required preparation of the Trust Account Management employees to detect device

anomalies, including regulatory enforcement awareness sessions and practices.

2.

Fraudulent activities occur adverse condition for business and in long run these can affect

business survival. These acts lead to loss of trust and confidence of customers on business as

well ass brand’s image in market. As most of customers are rely on company’s brand due to their

ethical practices thus fraudulent activities hurt their confidence and trust towards company and

its products.

1.

Gives restricted access to accounts to employees – not every employee needs complete access to

capital, and only selected employees can manage trust accounts transaction.

Provide the required preparation of the Trust Account Management employees to detect device

anomalies, including regulatory enforcement awareness sessions and practices.

2.

Fraudulent activities occur adverse condition for business and in long run these can affect

business survival. These acts lead to loss of trust and confidence of customers on business as

well ass brand’s image in market. As most of customers are rely on company’s brand due to their

ethical practices thus fraudulent activities hurt their confidence and trust towards company and

its products.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.