Report on Hedging and Performance of Foreign Transaction Hedge

Analyzing futures markets and pricing, speculating with futures contracts, forecasting volatility, and introduction to risk management techniques in derivatives and risk management.

18 Pages4511 Words68 Views

Added on 2022-10-14

About This Document

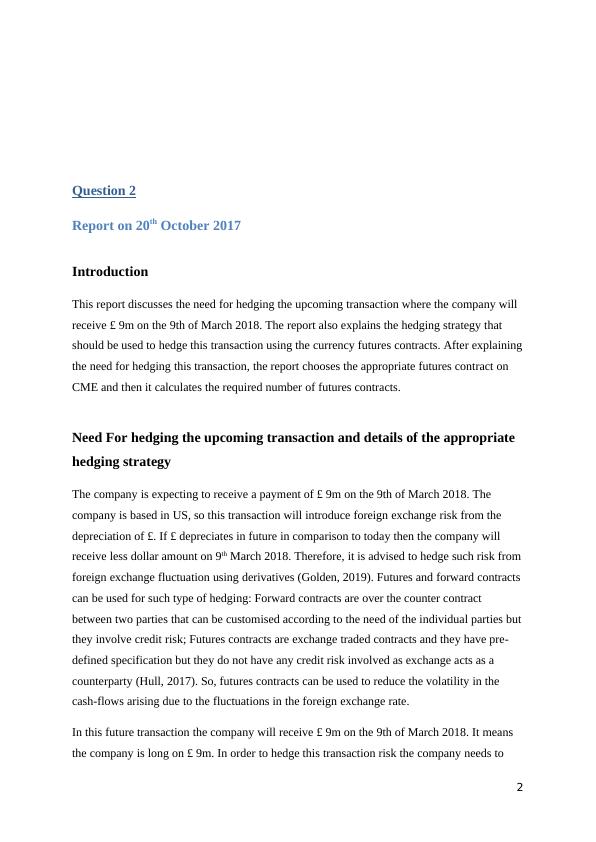

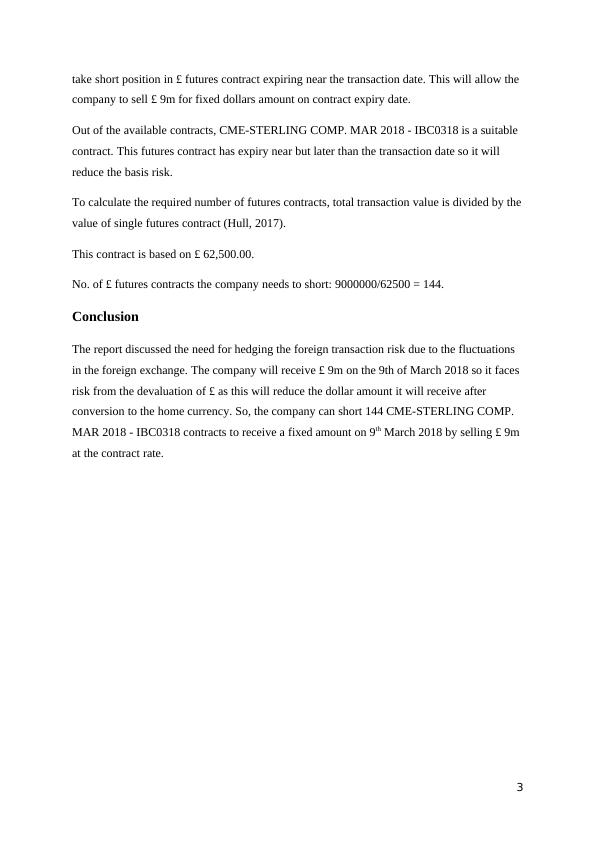

This report discusses the need for hedging the upcoming transaction where the company will receive £ 9m on the 9th of March 2018. The report also explains the hedging strategy that should be used to hedge this transaction using the currency futures contracts. It also discusses the performance of the foreign transaction hedge that the company entered on 20th October 2017. It also discusses about the margin account that is the initial margin, maintenance margin and variance margin.

Report on Hedging and Performance of Foreign Transaction Hedge

Analyzing futures markets and pricing, speculating with futures contracts, forecasting volatility, and introduction to risk management techniques in derivatives and risk management.

Added on 2022-10-14

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

FIN80018 Hedging Strategies - Assignment

|7

|1564

|334