Accounting and Finance Assessment for UGB 163 at Sunderland University

VerifiedAdded on 2023/01/05

|22

|3794

|58

Homework Assignment

AI Summary

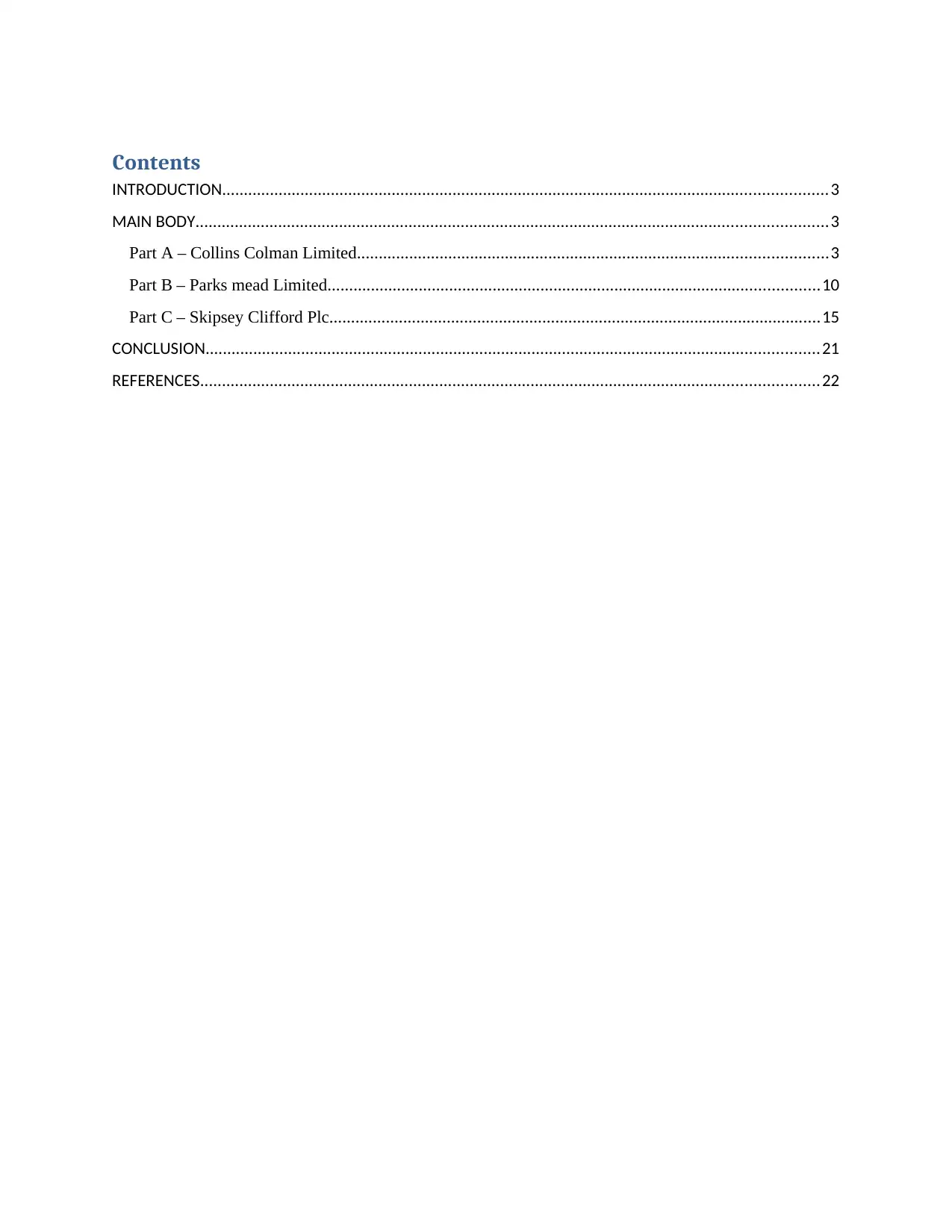

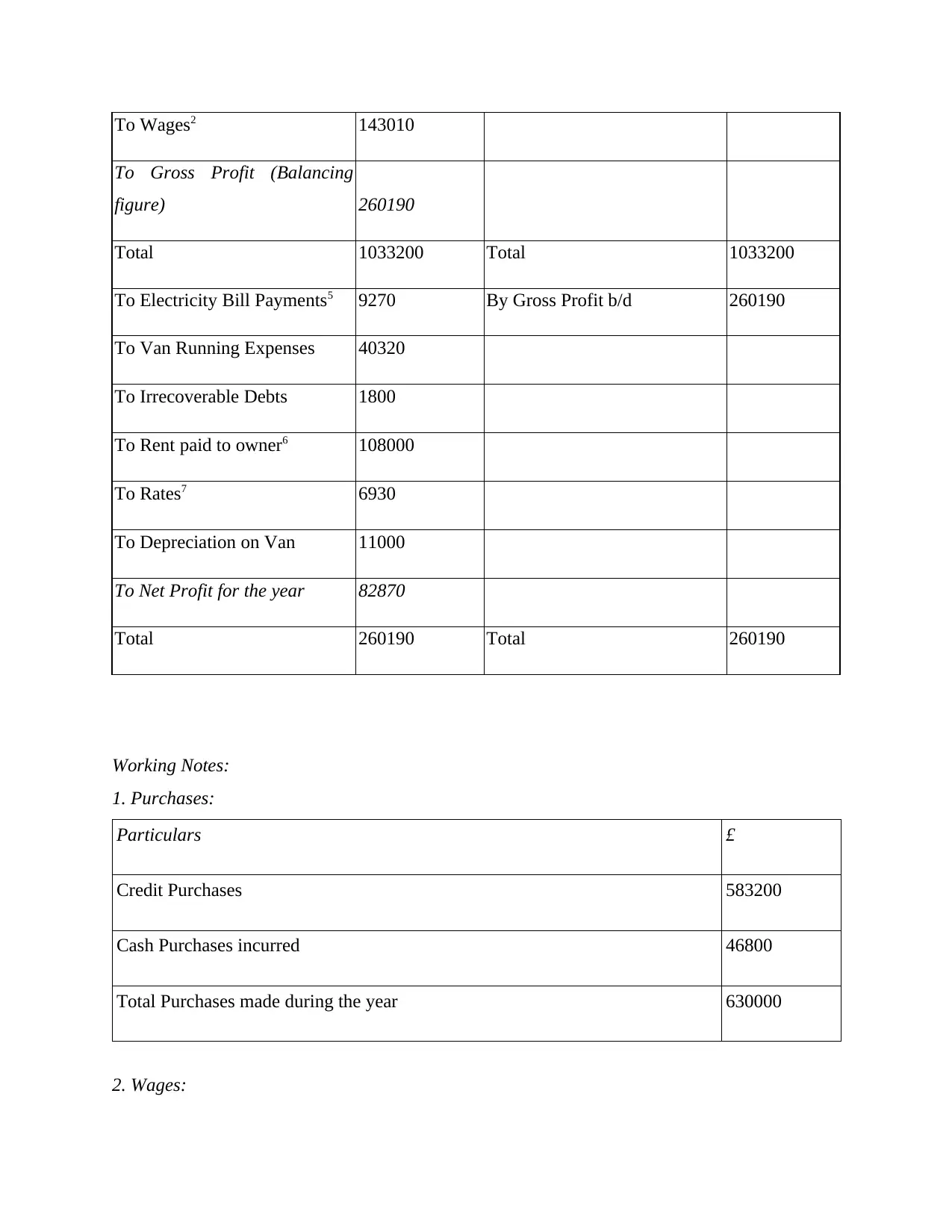

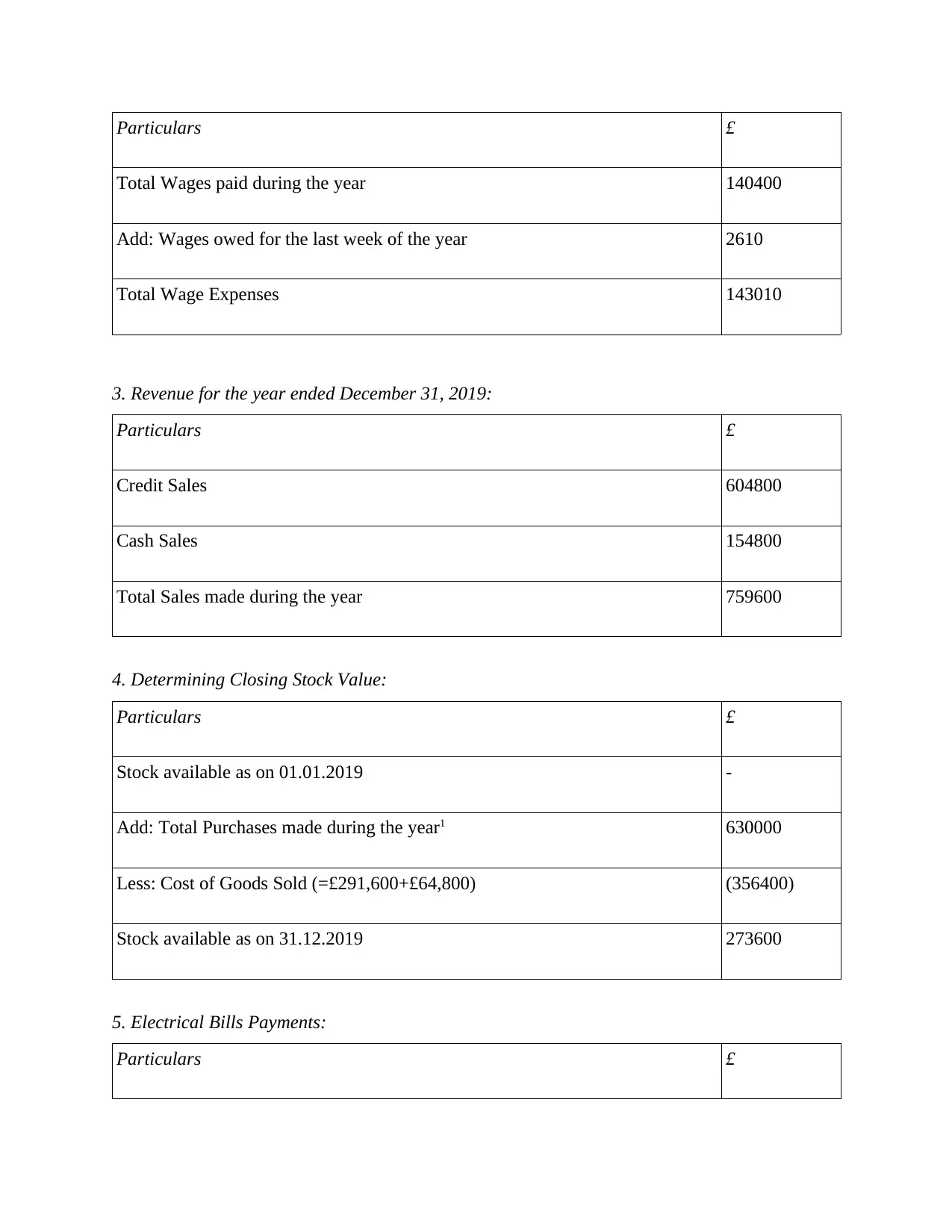

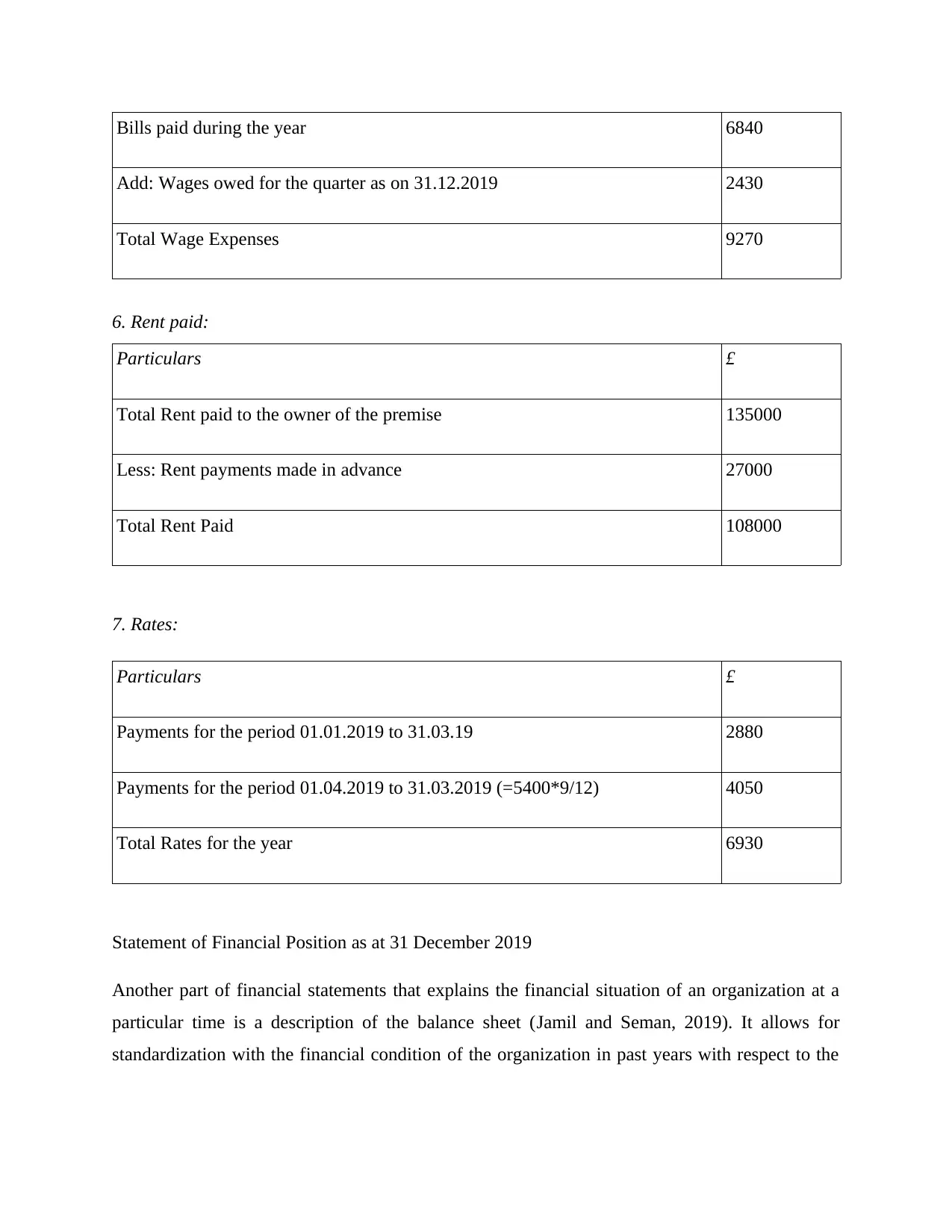

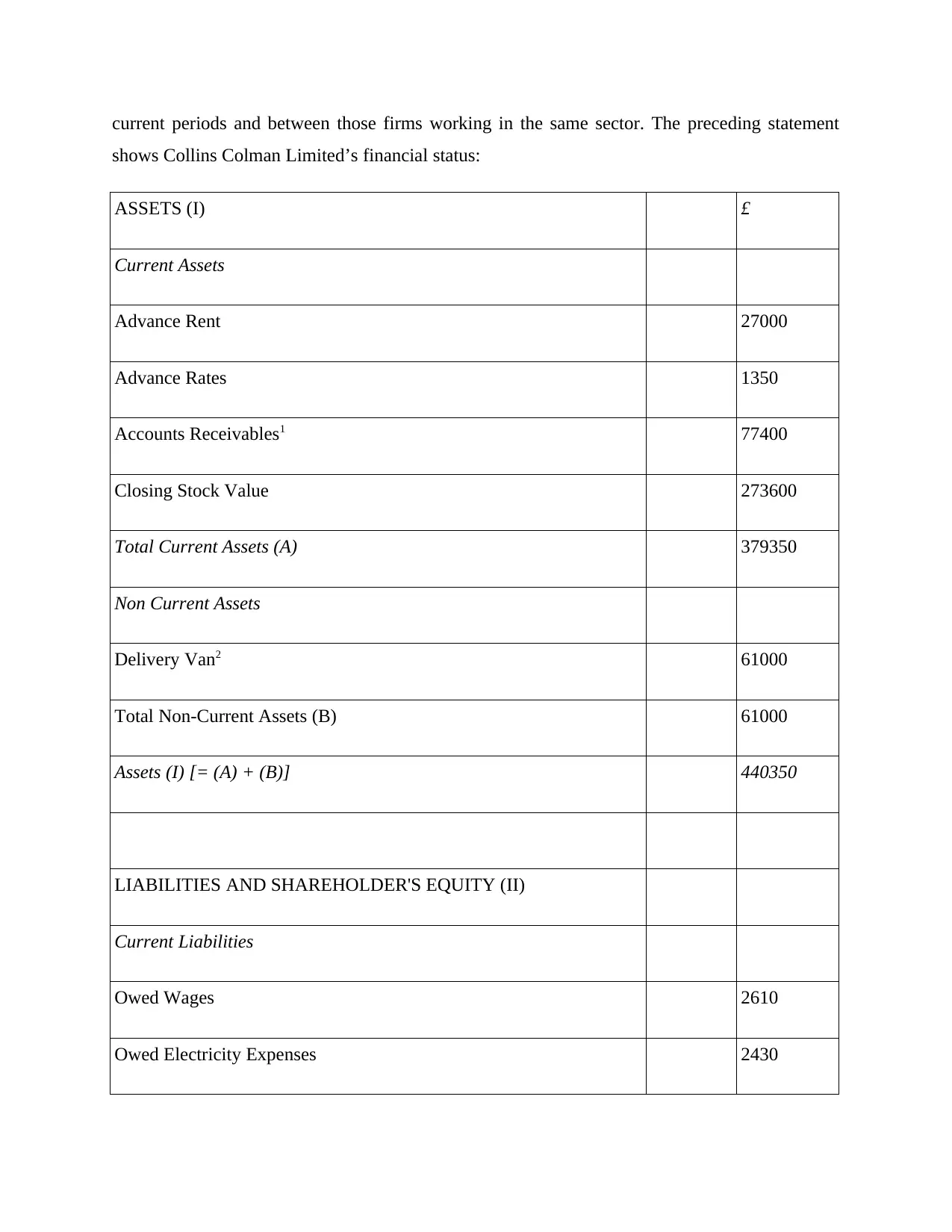

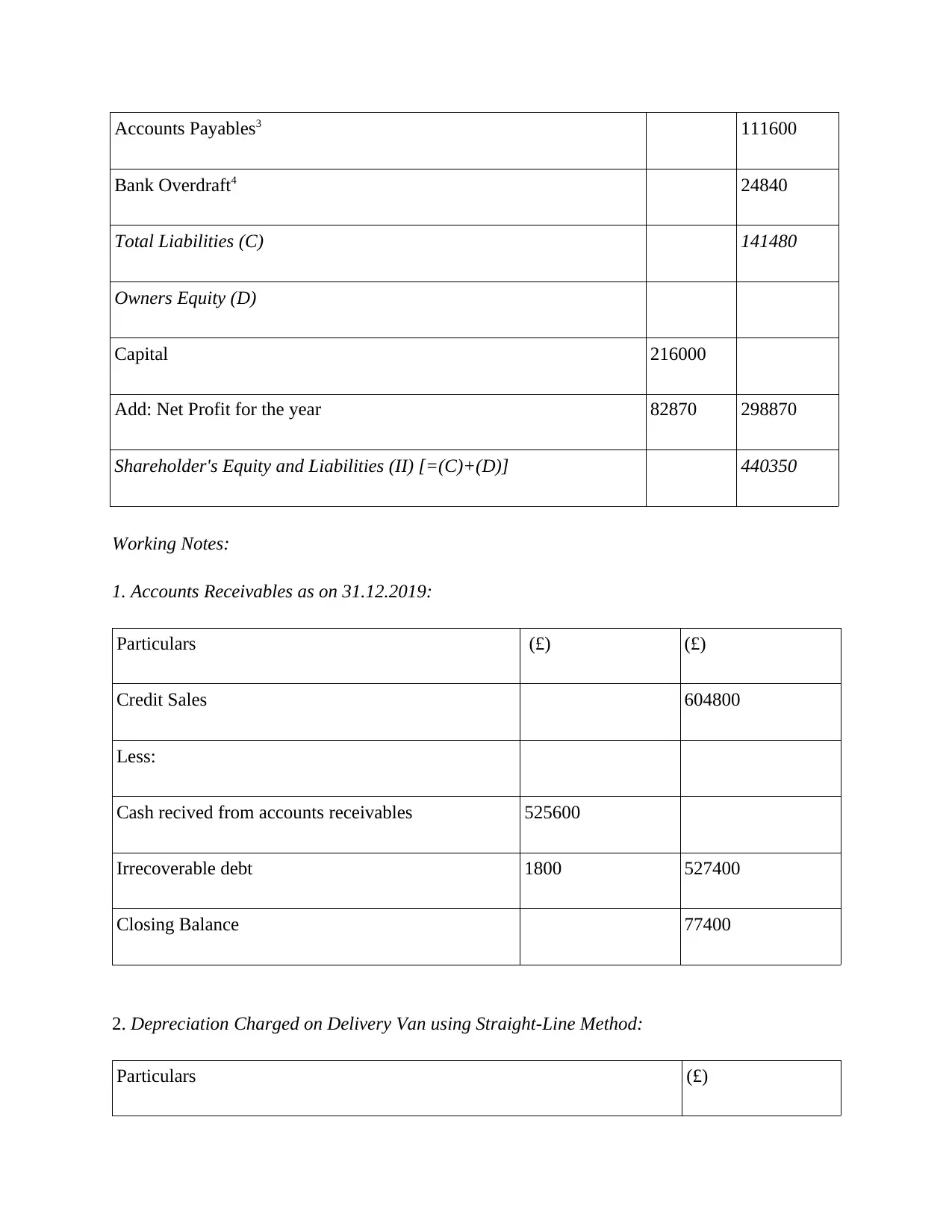

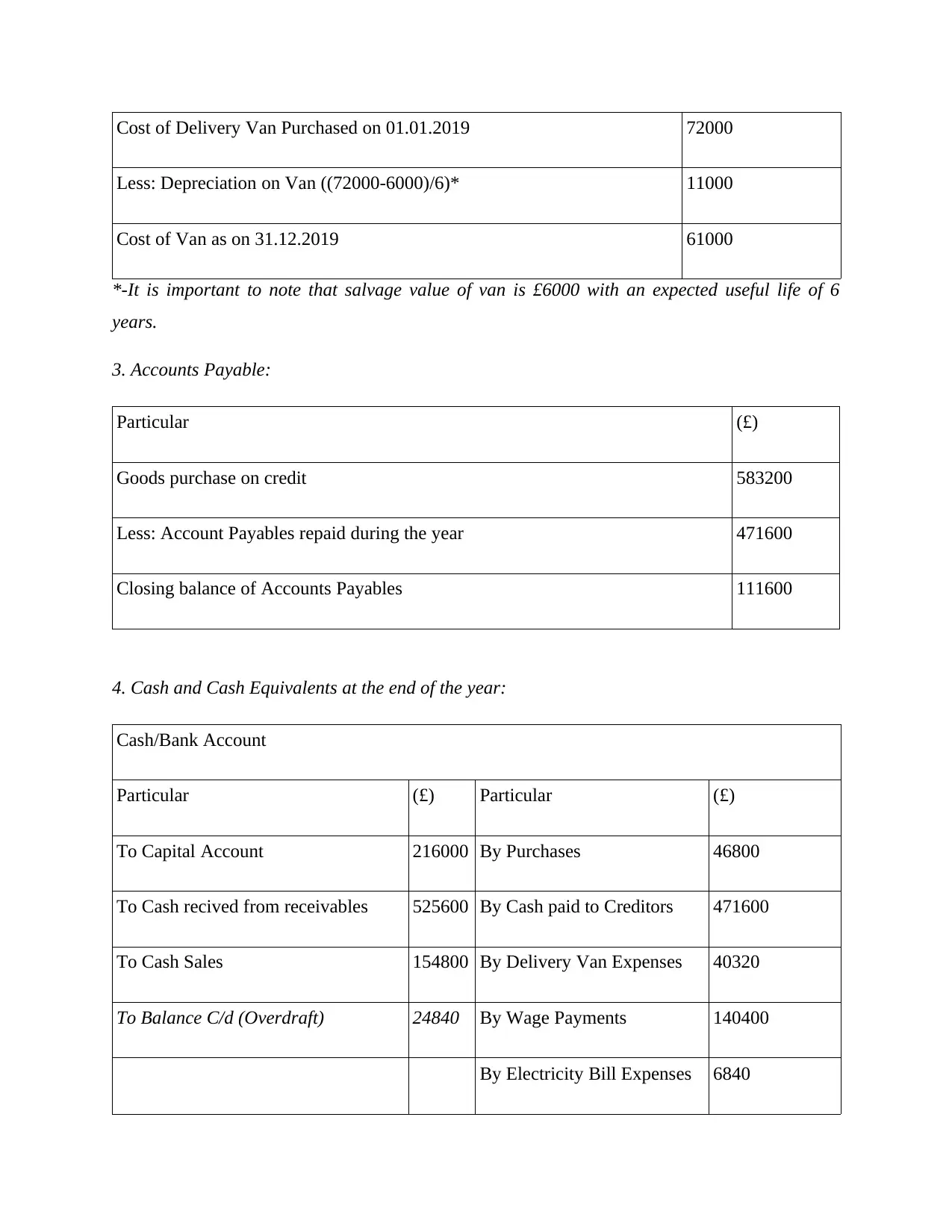

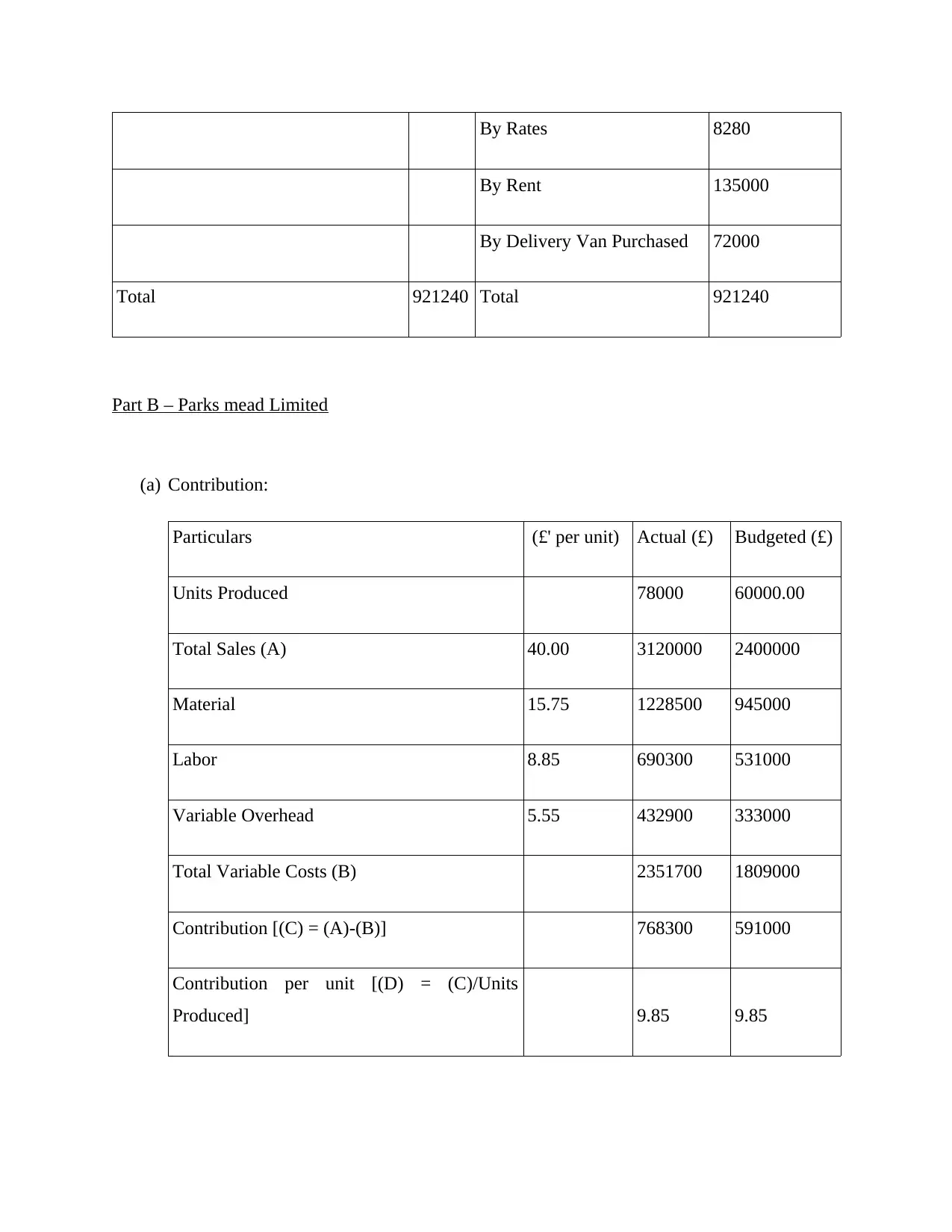

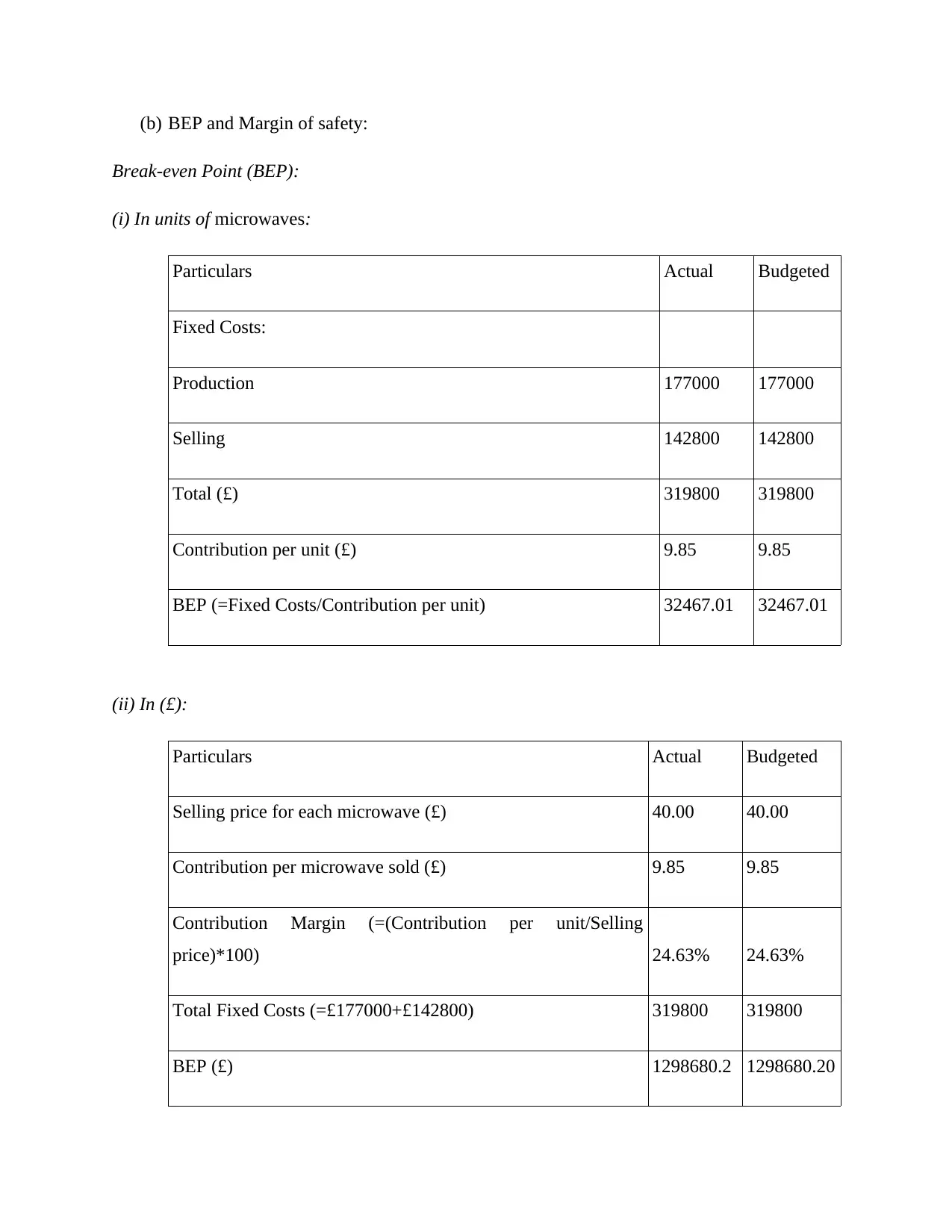

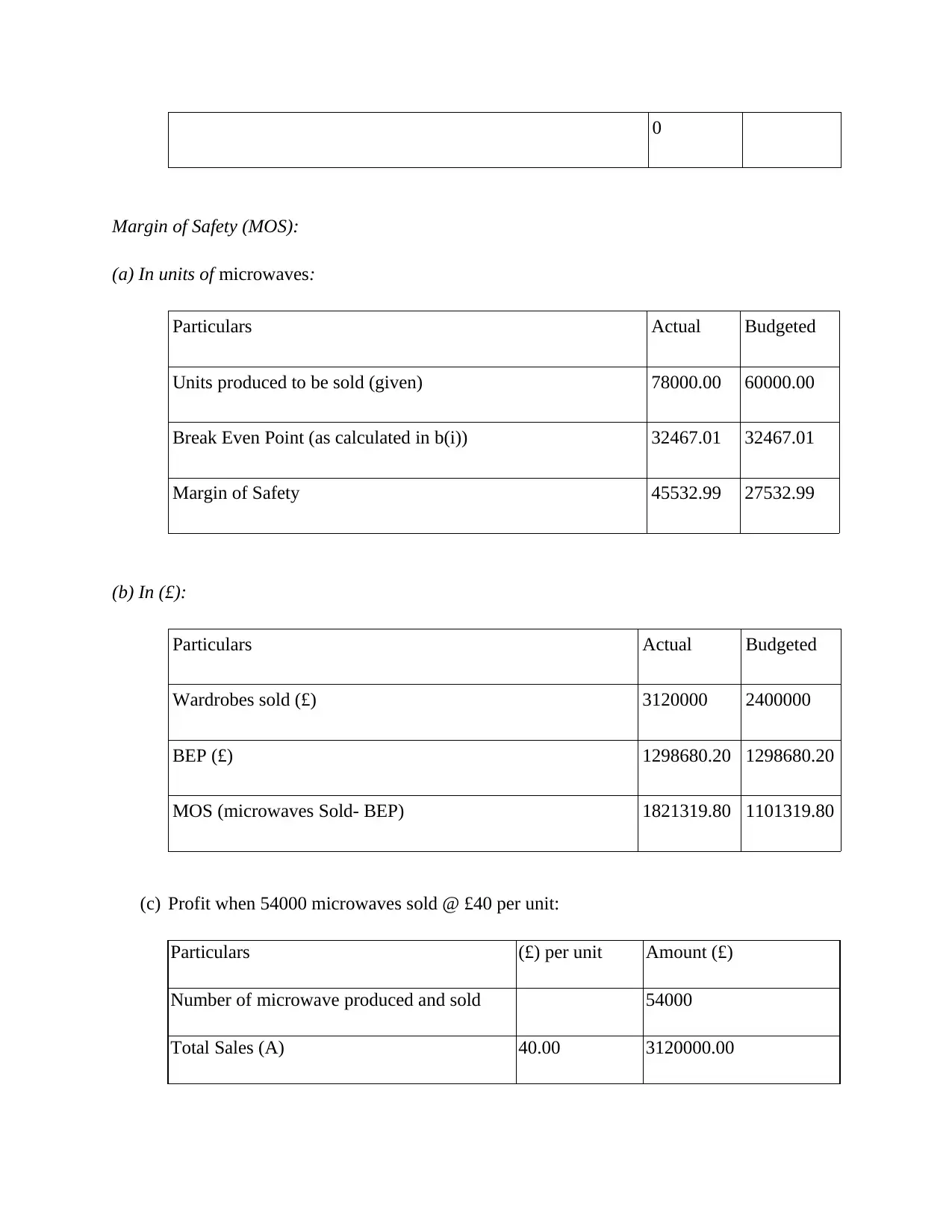

This document provides a complete solution to the UGB 163 Introduction to Accounting and Finance assessment, covering key aspects of financial and managerial accounting. The solution includes a detailed analysis of financial statements for Collins Colman Limited, encompassing the preparation of an income statement and a statement of financial position. Furthermore, it delves into cost accounting, including break-even analysis, margin of safety, and profit calculations for Parks Mead Limited. Finally, the document presents an investment appraisal for Skipsey Clifford Plc, calculating the payback period, accounting rate of return (ARR), and net present value (NPV), alongside a discussion of the merits and limitations of various investment appraisal techniques. The assignment addresses fundamental accounting principles and their practical applications, with a focus on financial statement analysis and investment decision-making.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.