Business Taxation Assignment - Analysis of Taxable Income and VAT

VerifiedAdded on 2022/12/27

|11

|2675

|37

Homework Assignment

AI Summary

This business taxation assignment solution provides a detailed analysis of various tax-related concepts. It begins with the calculation of taxable income, including adjustments for various expenses and income sources. The assignment then delves into the differences between employment and self-employment, exploring the advantages and disadvantages of each, and the impact of IR35 regulations. Further, it examines the "six badges of trade" used to determine if a transaction constitutes a trade for tax purposes and discusses different VAT schemes, including the flat-rate scheme. The solution also covers inheritance tax and provides a calculation of John's capital gains tax liability. Overall, the assignment offers a comprehensive overview of key business taxation topics and provides practical examples to illustrate the concepts.

Business Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

a) Employment vs. self-employment...........................................................................................5

b) Preference for self-employment..............................................................................................7

Question 3........................................................................................................................................9

a) Six badges of trade..................................................................................................................9

b) Different VAT schemes.........................................................................................................11

Question 4......................................................................................................................................12

a) Inheritance tax.......................................................................................................................12

b) John’s capital gains tax liability............................................................................................12

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

a) Employment vs. self-employment...........................................................................................5

b) Preference for self-employment..............................................................................................7

Question 3........................................................................................................................................9

a) Six badges of trade..................................................................................................................9

b) Different VAT schemes.........................................................................................................11

Question 4......................................................................................................................................12

a) Inheritance tax.......................................................................................................................12

b) John’s capital gains tax liability............................................................................................12

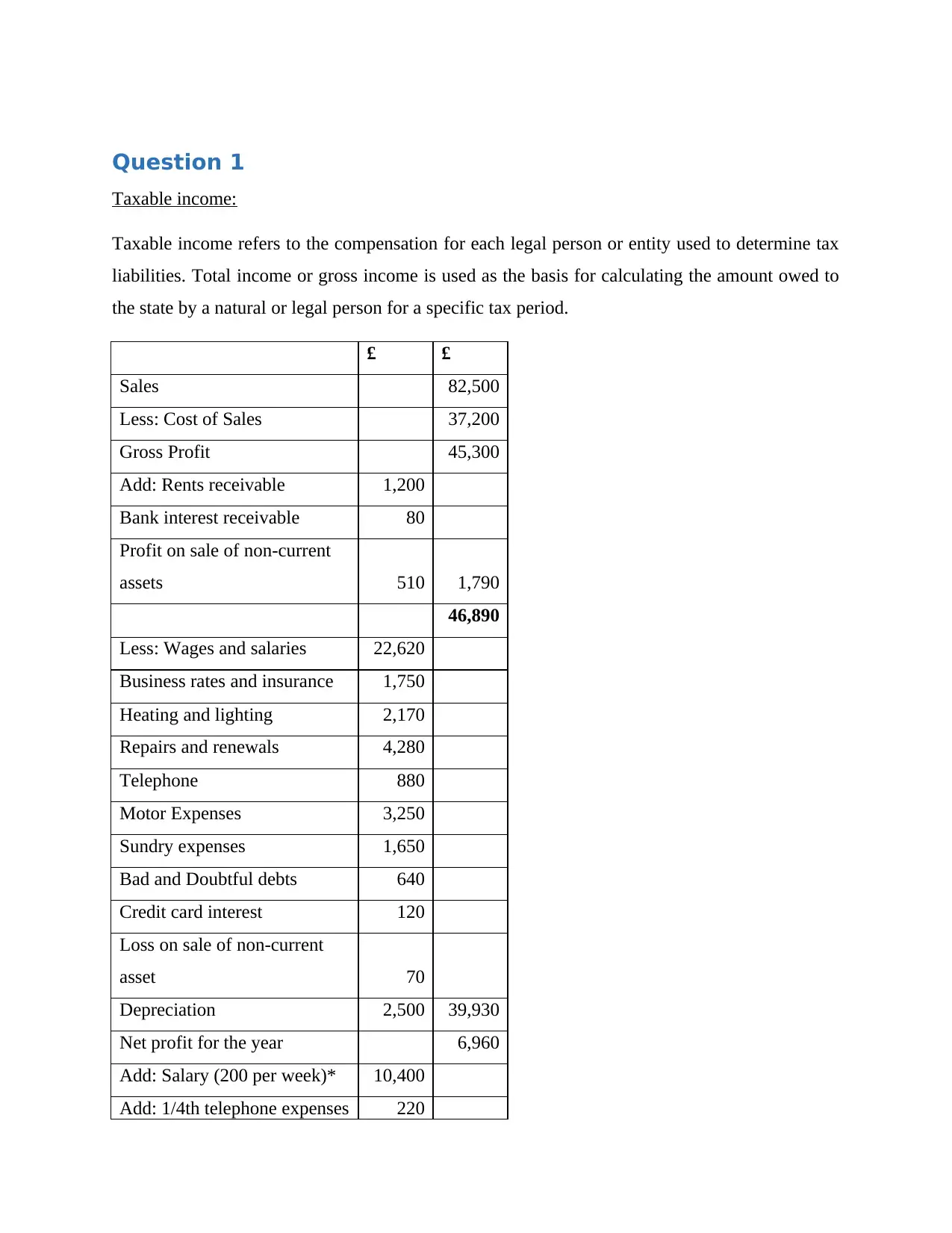

Question 1

Taxable income:

Taxable income refers to the compensation for each legal person or entity used to determine tax

liabilities. Total income or gross income is used as the basis for calculating the amount owed to

the state by a natural or legal person for a specific tax period.

£ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current

assets 510 1,790

46,890

Less: Wages and salaries 22,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 4,280

Telephone 880

Motor Expenses 3,250

Sundry expenses 1,650

Bad and Doubtful debts 640

Credit card interest 120

Loss on sale of non-current

asset 70

Depreciation 2,500 39,930

Net profit for the year 6,960

Add: Salary (200 per week)* 10,400

Add: 1/4th telephone expenses 220

Taxable income:

Taxable income refers to the compensation for each legal person or entity used to determine tax

liabilities. Total income or gross income is used as the basis for calculating the amount owed to

the state by a natural or legal person for a specific tax period.

£ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current

assets 510 1,790

46,890

Less: Wages and salaries 22,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 4,280

Telephone 880

Motor Expenses 3,250

Sundry expenses 1,650

Bad and Doubtful debts 640

Credit card interest 120

Loss on sale of non-current

asset 70

Depreciation 2,500 39,930

Net profit for the year 6,960

Add: Salary (200 per week)* 10,400

Add: 1/4th telephone expenses 220

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

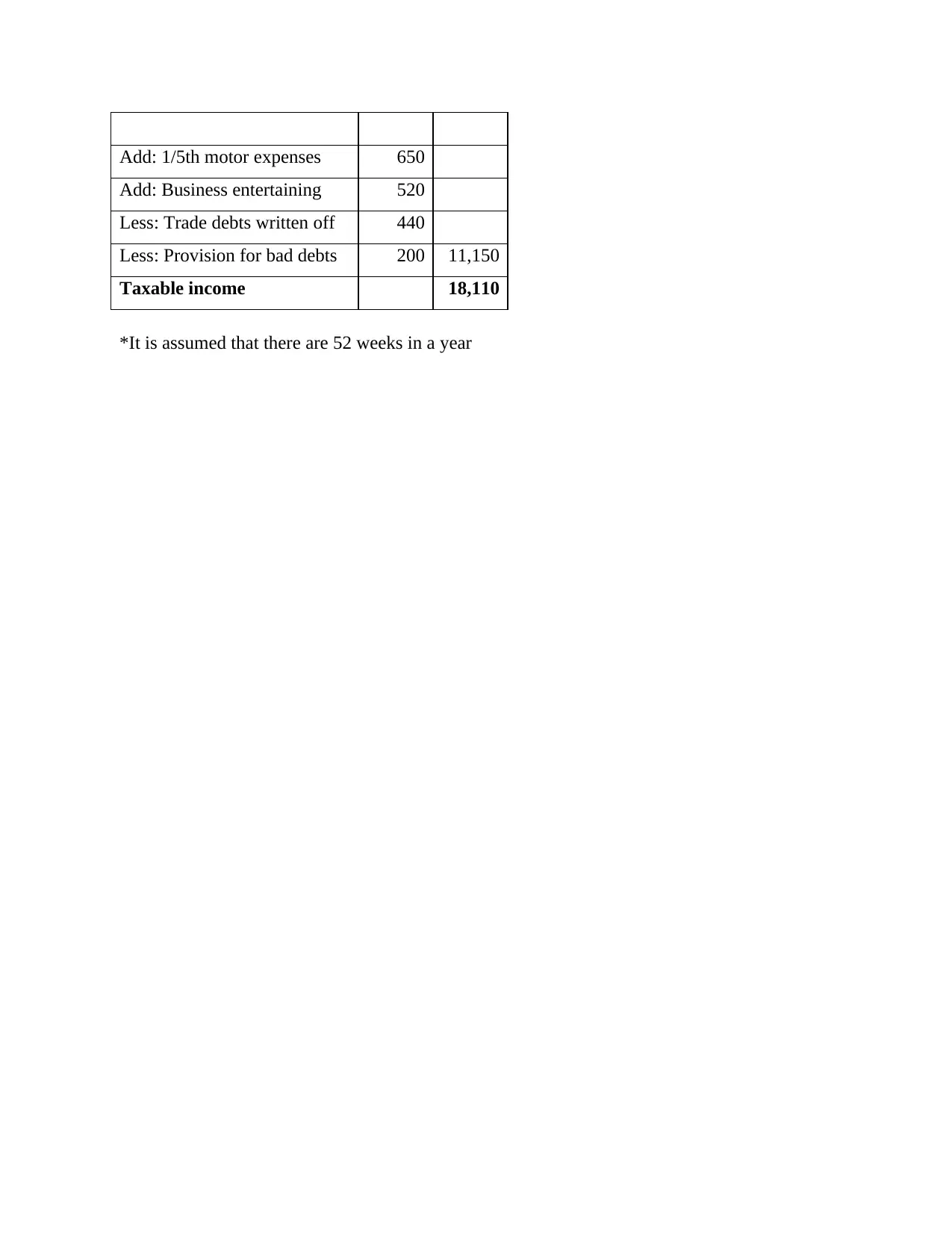

Add: 1/5th motor expenses 650

Add: Business entertaining 520

Less: Trade debts written off 440

Less: Provision for bad debts 200 11,150

Taxable income 18,110

*It is assumed that there are 52 weeks in a year

Add: Business entertaining 520

Less: Trade debts written off 440

Less: Provision for bad debts 200 11,150

Taxable income 18,110

*It is assumed that there are 52 weeks in a year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2

a) Employment vs. self-employment

Employees are involved in a wide range of industries. At each end of this spectrum, the

characteristics of employed and self-employed employees can be clearly identified. Self-

employed as well as running the company at their own expense, at risk of loss, capital investment

and independence from customers. In a fiscal context, it would be impossible, if not impossible,

to levy the withholding tax on someone's total income.

Anyone who is securely employed in long-term employment will receive a salary or salary. You

may be directly supervised in any form and integrated into the industry providing the service. It

would be practical and convenient to ask employers to withhold taxes on these employees, and

the PAYE cumulative system would work well. It does not fit these descriptions, but there are

personalities between the two ends of the spectrum. It can be said that they live in a "gray zone"

at the edge of the distribution gap. These employees can be classified in different ways according

to the legal purpose.

Even if employees are clearly and correctly categorized by both sides of the charge, some

differences in the rules can be unfair. For example, some employees have unparalleled real costs

that cannot be taken under current rules. However, for gray groups, wage inequality and the

plight of the self-employed are high.

For lawyers, the difference between an employee and a self-employed person can have serious

legal consequences. To assess an employee's rights and responsibilities, you need to know

clearly which side you are on. Subject to certain legal provisions, this is guaranteed by the

contractual rights and obligations between the employee and the person or organization

providing the service. This is not just about the label or the terms agreed by the parties. Under

UK law, the court will assess the situation on the basis of all the facts, but this is the true nature

of the report under the law.

a) Employment vs. self-employment

Employees are involved in a wide range of industries. At each end of this spectrum, the

characteristics of employed and self-employed employees can be clearly identified. Self-

employed as well as running the company at their own expense, at risk of loss, capital investment

and independence from customers. In a fiscal context, it would be impossible, if not impossible,

to levy the withholding tax on someone's total income.

Anyone who is securely employed in long-term employment will receive a salary or salary. You

may be directly supervised in any form and integrated into the industry providing the service. It

would be practical and convenient to ask employers to withhold taxes on these employees, and

the PAYE cumulative system would work well. It does not fit these descriptions, but there are

personalities between the two ends of the spectrum. It can be said that they live in a "gray zone"

at the edge of the distribution gap. These employees can be classified in different ways according

to the legal purpose.

Even if employees are clearly and correctly categorized by both sides of the charge, some

differences in the rules can be unfair. For example, some employees have unparalleled real costs

that cannot be taken under current rules. However, for gray groups, wage inequality and the

plight of the self-employed are high.

For lawyers, the difference between an employee and a self-employed person can have serious

legal consequences. To assess an employee's rights and responsibilities, you need to know

clearly which side you are on. Subject to certain legal provisions, this is guaranteed by the

contractual rights and obligations between the employee and the person or organization

providing the service. This is not just about the label or the terms agreed by the parties. Under

UK law, the court will assess the situation on the basis of all the facts, but this is the true nature

of the report under the law.

b) Preference for self-employment

In 1999, the British Domestic Finance Service introduced a new tax settlement measure that

limits the ability of entrepreneurs and small businesses to limit income tax and social security

through intermediaries or "personal services" company. Prior to the introduction of these

measures, the IR35 regulations, known as their own limited liability companies, often acted as

intermediaries for the taxes they levied on them. It really works.

Previously, one can limit your tax requirements in several ways by making use of intermediaries.

For example, by sharing small business ownership with a family member, to enter a low income

tax area or person’s salary comes in the form of: Benefits not eligible for benefits in Northern

Ireland. Another common way to reduce your tax debt is to work with a contract from Monday to

Friday, then work with a new contract but almost the same a week later, adding directly to your

Northern Ireland monthly limit. Replacing the monthly contribution is dependent on full time. A

secret employee is anyone who works the same way as a full-time company employee, but is

paid through a separate bankruptcy company, is governed by the IR35 rules, and is not self-

employed.

IR35 changed the previous stance of private data companies and entrepreneurs by introducing

rules requiring undercover employees to cover the same taxes and duties in Northern Ireland as

employees. This means that if you are found "in" and hidden in the IR35 rules, you can increase

the Irish rate and income tax to increase the tax credits you normally pay with direct employees

of the company. HMRC requires an investment to allow you to invest in "risk criteria" for a

person who can potentially connect.

Previously, it was up to the broker or sole proprietor of the contractor to assess whether the

broker was subject to the IR35 rule. In 2017, HMRC updated its approach to implementing IR35

in authorities in response to perceived increases in tax cuts.

Under the new rules, authorities such as the NHS or local authorities have a responsibility to

ensure that contractors or intermediaries are self-employed. These decisions for intermediaries

should be made individually rather than at a wider level for specific areas of staff. HMRC will

extend these rule changes to the private sector.

In 1999, the British Domestic Finance Service introduced a new tax settlement measure that

limits the ability of entrepreneurs and small businesses to limit income tax and social security

through intermediaries or "personal services" company. Prior to the introduction of these

measures, the IR35 regulations, known as their own limited liability companies, often acted as

intermediaries for the taxes they levied on them. It really works.

Previously, one can limit your tax requirements in several ways by making use of intermediaries.

For example, by sharing small business ownership with a family member, to enter a low income

tax area or person’s salary comes in the form of: Benefits not eligible for benefits in Northern

Ireland. Another common way to reduce your tax debt is to work with a contract from Monday to

Friday, then work with a new contract but almost the same a week later, adding directly to your

Northern Ireland monthly limit. Replacing the monthly contribution is dependent on full time. A

secret employee is anyone who works the same way as a full-time company employee, but is

paid through a separate bankruptcy company, is governed by the IR35 rules, and is not self-

employed.

IR35 changed the previous stance of private data companies and entrepreneurs by introducing

rules requiring undercover employees to cover the same taxes and duties in Northern Ireland as

employees. This means that if you are found "in" and hidden in the IR35 rules, you can increase

the Irish rate and income tax to increase the tax credits you normally pay with direct employees

of the company. HMRC requires an investment to allow you to invest in "risk criteria" for a

person who can potentially connect.

Previously, it was up to the broker or sole proprietor of the contractor to assess whether the

broker was subject to the IR35 rule. In 2017, HMRC updated its approach to implementing IR35

in authorities in response to perceived increases in tax cuts.

Under the new rules, authorities such as the NHS or local authorities have a responsibility to

ensure that contractors or intermediaries are self-employed. These decisions for intermediaries

should be made individually rather than at a wider level for specific areas of staff. HMRC will

extend these rule changes to the private sector.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From 2020, private companies have a responsibility to assess the condition of those who work

for them through intermediaries. Responsibility for non-compliance with IR35 regulation has

also passed to these private companies. These changes have had a significant impact on the work

of the NHS as organizations rely on professionals to work through intermediaries. A quarter of

NHS representatives responded to a survey by the contract calculator and decided to leave the

NHS altogether after an IR35 survey, with 60% of new samples saying they were "internally

recognized" with the IR35. "." After the NHS used general estimates illegal to limit increases in

administration costs. Small businesses should be exempt from these changes, and for IR35

purposes, small businesses are defined by at least two of the following three actions:

Less than 12 million pounds in sales

Less than £5.1 million on the balance sheet,

There are no more than 50 employees.

The new IR35 rule introduces the concept of state decision reporting (SDS). It is a complete

statement that the client must make after evaluating the IR35. It sets out the contractor's intended

employment status and the reasons for this decision. On April 6, 2020, a safety data sheet must

be completed for all new Personal Service Company (PSC) contracts and all existing PSC

contracts payable after that date.

Another change in the law is the introduction of a customer-driven legal process that allows

contractors to ask MSDS questions if they feel their decisions are wrong. Customers must

respond to the appeal within 45 days of receipt and keep the current status definition. When the

state of the art changes, the customer must withdraw the previous request and give the employee

a new safety data sheet containing the updated solution.

Another change to note is that IR35 entrepreneurs are now entitled to a 5% price to cover

running costs. As the responsibility for determining employment status for IR35 purposes is

transferred to the employer, this benefit is only available to intermediaries with small group

relationships.

The impact of these changes is huge for both companies that employ intermediaries and for

intermediaries themselves. 4.8 million Self-employed people, entrepreneurs and brokers cannot

be listed outside the IR35 rules, many of which could be interpreted as rules after a decision. .

for them through intermediaries. Responsibility for non-compliance with IR35 regulation has

also passed to these private companies. These changes have had a significant impact on the work

of the NHS as organizations rely on professionals to work through intermediaries. A quarter of

NHS representatives responded to a survey by the contract calculator and decided to leave the

NHS altogether after an IR35 survey, with 60% of new samples saying they were "internally

recognized" with the IR35. "." After the NHS used general estimates illegal to limit increases in

administration costs. Small businesses should be exempt from these changes, and for IR35

purposes, small businesses are defined by at least two of the following three actions:

Less than 12 million pounds in sales

Less than £5.1 million on the balance sheet,

There are no more than 50 employees.

The new IR35 rule introduces the concept of state decision reporting (SDS). It is a complete

statement that the client must make after evaluating the IR35. It sets out the contractor's intended

employment status and the reasons for this decision. On April 6, 2020, a safety data sheet must

be completed for all new Personal Service Company (PSC) contracts and all existing PSC

contracts payable after that date.

Another change in the law is the introduction of a customer-driven legal process that allows

contractors to ask MSDS questions if they feel their decisions are wrong. Customers must

respond to the appeal within 45 days of receipt and keep the current status definition. When the

state of the art changes, the customer must withdraw the previous request and give the employee

a new safety data sheet containing the updated solution.

Another change to note is that IR35 entrepreneurs are now entitled to a 5% price to cover

running costs. As the responsibility for determining employment status for IR35 purposes is

transferred to the employer, this benefit is only available to intermediaries with small group

relationships.

The impact of these changes is huge for both companies that employ intermediaries and for

intermediaries themselves. 4.8 million Self-employed people, entrepreneurs and brokers cannot

be listed outside the IR35 rules, many of which could be interpreted as rules after a decision. .

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

a) Six badges of trade

Moving to seek profit

When someone makes a contract, we have to decide if that person has a profit margin. What

matters is not the earning opportunity, but the motivation to get it. However, the revenue and

responsibilities to Her Majesty (Revenue Services) would be of great interest in this matter if the

profits were made. Taxpayers can claim that they are working to use the loss to reduce their

taxes. Taxpayers must show, not profit, to see if there is an exchange.

Frequency and number of such transactions

To recognize a transaction as a trade, it is necessary to repeat that transaction at repeated period

of time. On the other hand, doing a regular trade also indicates an action taken by a person. For

example, suppose a man sold a car he owned for 4 years. He bought another car for himself and

sold it two years later. HM Treasury & Customs is unlikely to accept a particular car dealer. But

if he buys and sells cars every month, they're more likely to try to tax the profits as trading

income. The most impressive example in this area is Pickford v. Quirk, where the taxpayer has

acquired a commercial structure. However, it was clear that the factory was in much worse shape

than expected, and the best thing a taxpayer could do was take everything out and sell it one by

one. In doing so, he made a huge profit and did it over and over again. A number of transactions

involved the taxation of profits from trading income.

Modification of the asset in order to make it more saleable

If someone buys something and sells it without doing anything, he is very likely to buy it. But if

someone buys a car, install a new engine, repair the body, and make it more attractive to buy, he

can be seen as seller.

The nature of the assets

The business label can be linked to one-time trading as it cannot be used as an excuse to

purchase a particular asset for any purpose other than resale. The most impressive example in

this area is Rutledge v. CIR. In this case, the taxpayer bought 1 million toilet papers in a single

transaction. They then sold it for profit in other stores. It was considered a career ("adventure" of

a) Six badges of trade

Moving to seek profit

When someone makes a contract, we have to decide if that person has a profit margin. What

matters is not the earning opportunity, but the motivation to get it. However, the revenue and

responsibilities to Her Majesty (Revenue Services) would be of great interest in this matter if the

profits were made. Taxpayers can claim that they are working to use the loss to reduce their

taxes. Taxpayers must show, not profit, to see if there is an exchange.

Frequency and number of such transactions

To recognize a transaction as a trade, it is necessary to repeat that transaction at repeated period

of time. On the other hand, doing a regular trade also indicates an action taken by a person. For

example, suppose a man sold a car he owned for 4 years. He bought another car for himself and

sold it two years later. HM Treasury & Customs is unlikely to accept a particular car dealer. But

if he buys and sells cars every month, they're more likely to try to tax the profits as trading

income. The most impressive example in this area is Pickford v. Quirk, where the taxpayer has

acquired a commercial structure. However, it was clear that the factory was in much worse shape

than expected, and the best thing a taxpayer could do was take everything out and sell it one by

one. In doing so, he made a huge profit and did it over and over again. A number of transactions

involved the taxation of profits from trading income.

Modification of the asset in order to make it more saleable

If someone buys something and sells it without doing anything, he is very likely to buy it. But if

someone buys a car, install a new engine, repair the body, and make it more attractive to buy, he

can be seen as seller.

The nature of the assets

The business label can be linked to one-time trading as it cannot be used as an excuse to

purchase a particular asset for any purpose other than resale. The most impressive example in

this area is Rutledge v. CIR. In this case, the taxpayer bought 1 million toilet papers in a single

transaction. They then sold it for profit in other stores. It was considered a career ("adventure" of

course) because there was no other reason to buy too much toilet paper. It could not be argued

that it was overcrowded.

Link to an existing trade

For example, an accountant sold a car. Because car sales are not linked to tax accountants, it is

unlikely that anyone will trade in cars. However, if someone has worked as a car sales mechanic,

HMRC is much more likely to successfully tax car income under the current contract, as car

repairs are directly linked to the cars they sell. Other signals should also be used, but HMRC

takes these references with caution.

Reasons to build / sell

The final signal is to explain the answer to how the fund was acquired. In other words, if

received by gift or bequest, and why did you sell the real estate? Consider an example of a mod

who received a coat from a deceased mother. He doesn't want them, so he posts ads in local

newspapers. This advertisement is displayed by HM Treasury and Customs and is intended to tax

Maud's income. Since Maud acquired the fur, the brand is unlikely to be associated with these

arrangements. However, if the mod bought a full-length wardrobe, advertised it, and then sold it

for a profit; it is far more likely to be seen as a trader. This is not just the beginning of selling

donations.

b) Different VAT schemes

Some of the different types of VAT schemes have been discussed below:

Flat rate VAT accounting scheme

The standard VAT accounting system simplifies VAT refunds. In this VAT reporting system,

only VAT due to HM Revenue and Customs (HMRC) is calculated as a percentage of sales. This

is in lieu of paying the difference between the VAT paid on the sale and the VAT paid on the

purchase. The only upstream VAT you can claim is to invest over £ 2000 including VAT. This

VAT is entered separately in the VAT return in box 4.

VAT cash accounting scheme

that it was overcrowded.

Link to an existing trade

For example, an accountant sold a car. Because car sales are not linked to tax accountants, it is

unlikely that anyone will trade in cars. However, if someone has worked as a car sales mechanic,

HMRC is much more likely to successfully tax car income under the current contract, as car

repairs are directly linked to the cars they sell. Other signals should also be used, but HMRC

takes these references with caution.

Reasons to build / sell

The final signal is to explain the answer to how the fund was acquired. In other words, if

received by gift or bequest, and why did you sell the real estate? Consider an example of a mod

who received a coat from a deceased mother. He doesn't want them, so he posts ads in local

newspapers. This advertisement is displayed by HM Treasury and Customs and is intended to tax

Maud's income. Since Maud acquired the fur, the brand is unlikely to be associated with these

arrangements. However, if the mod bought a full-length wardrobe, advertised it, and then sold it

for a profit; it is far more likely to be seen as a trader. This is not just the beginning of selling

donations.

b) Different VAT schemes

Some of the different types of VAT schemes have been discussed below:

Flat rate VAT accounting scheme

The standard VAT accounting system simplifies VAT refunds. In this VAT reporting system,

only VAT due to HM Revenue and Customs (HMRC) is calculated as a percentage of sales. This

is in lieu of paying the difference between the VAT paid on the sale and the VAT paid on the

purchase. The only upstream VAT you can claim is to invest over £ 2000 including VAT. This

VAT is entered separately in the VAT return in box 4.

VAT cash accounting scheme

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VAT refunds are usually based on the tax date (usually the same as the invoice date) for the sale

and purchase. This could mean that the buyer will have to pay HM Revenue & Customs VAT on

sales that have not yet been paid. Instead, the VAT accounting system is based on the date of

sale. You need to make sure that your VAT return shows the actual payment date.

Annual accounting scheme

The annual accounting system allows you to pay VAT within nine months or three quarters.

Then complete the annual VAT refund used to work out your balance or income and HM levels.

Again, this simplifies VAT practices. You can only qualify for the program if you can stay in

this system as long as your estimated tax version does not exceed £ 1.35 million and you live

below £ 1.6 million.

Retail and VAT margin schemes

There are several sales systems in place to enable VAT. The plan that's right for you depends on

whether your retail sales (excluding VAT) are under £ 1 million and from £ 1 million to over £

130 million. Small businesses can use sales planning with cash accounting and annual reports.

The sales system cannot be combined with the VAT model, but sellers can use standard amounts

instead. In addition, there is a VAT system for companies dealing in second-hand goods, art, etc.

and a special system for traveling group presentation.

Question 4

a) Inheritance tax

Total value of the estate = £880,000

Nil rate band = £325,000 (threshold free amount)

Tax chargeable amount = £880,000 - £325,000 = £555,000

According to the UK’s tax law, inheritance tax rate is 40% of chargeable amount.

Thus, the total inheritance tax that will be payable as a result of Peter’s death is:

40% of £555,000 = £222,200

and purchase. This could mean that the buyer will have to pay HM Revenue & Customs VAT on

sales that have not yet been paid. Instead, the VAT accounting system is based on the date of

sale. You need to make sure that your VAT return shows the actual payment date.

Annual accounting scheme

The annual accounting system allows you to pay VAT within nine months or three quarters.

Then complete the annual VAT refund used to work out your balance or income and HM levels.

Again, this simplifies VAT practices. You can only qualify for the program if you can stay in

this system as long as your estimated tax version does not exceed £ 1.35 million and you live

below £ 1.6 million.

Retail and VAT margin schemes

There are several sales systems in place to enable VAT. The plan that's right for you depends on

whether your retail sales (excluding VAT) are under £ 1 million and from £ 1 million to over £

130 million. Small businesses can use sales planning with cash accounting and annual reports.

The sales system cannot be combined with the VAT model, but sellers can use standard amounts

instead. In addition, there is a VAT system for companies dealing in second-hand goods, art, etc.

and a special system for traveling group presentation.

Question 4

a) Inheritance tax

Total value of the estate = £880,000

Nil rate band = £325,000 (threshold free amount)

Tax chargeable amount = £880,000 - £325,000 = £555,000

According to the UK’s tax law, inheritance tax rate is 40% of chargeable amount.

Thus, the total inheritance tax that will be payable as a result of Peter’s death is:

40% of £555,000 = £222,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) John’s capital gains tax liability

Value of the house gifted to John = £420,000

Profit from sale of house = (£496,400 - £5,200 - £2,800) - £420,000

= £68,000

Thus John’s capital gain tax liability = £68,000

Value of the house gifted to John = £420,000

Profit from sale of house = (£496,400 - £5,200 - £2,800) - £420,000

= £68,000

Thus John’s capital gain tax liability = £68,000

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.