Comprehensive UK Income Tax and Calculation Analysis Report

VerifiedAdded on 2023/01/05

|11

|2418

|2

Report

AI Summary

This report provides a comprehensive analysis of UK income tax calculations, focusing on various aspects such as taxable income, personal allowances, and tax payable. It delves into specific scenarios, including accommodation, company cars, and personal expenses, to determine tax implications. The report includes a detailed tax computation for an individual named Fiona, considering her annual salary, bonus, interest received, and other relevant financial details. Furthermore, it explores the impact of taxes and tax planning, covering topics like gardening leave, employee training, and payments related to salary, holidays, and redundancy. The report also examines overseas workday relief, explaining the tax implications for individuals with international income and earnings. The analysis incorporates relevant UK tax legislation and provides a practical understanding of tax obligations and planning strategies.

UK income tax and

calculations

calculations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................3

SECTION B.....................................................................................................................................6

Impact of Taxes and Tax Planning..................................................................................................6

Overseas Workday Relief................................................................................................................7

REFERENCES..............................................................................................................................10

Appendix........................................................................................................................................11

SECTION A.....................................................................................................................................3

SECTION B.....................................................................................................................................6

Impact of Taxes and Tax Planning..................................................................................................6

Overseas Workday Relief................................................................................................................7

REFERENCES..............................................................................................................................10

Appendix........................................................................................................................................11

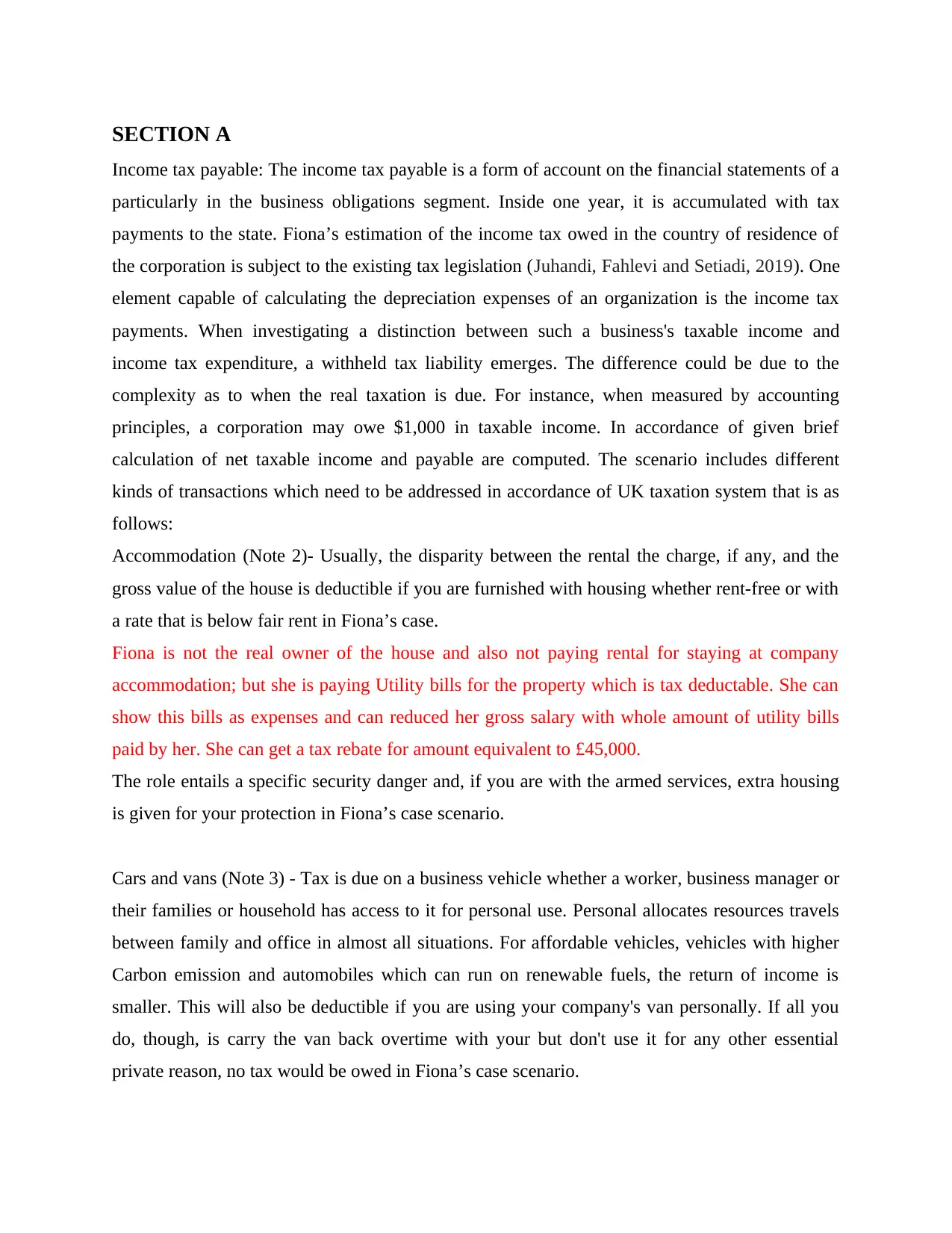

SECTION A

Income tax payable: The income tax payable is a form of account on the financial statements of a

particularly in the business obligations segment. Inside one year, it is accumulated with tax

payments to the state. Fiona’s estimation of the income tax owed in the country of residence of

the corporation is subject to the existing tax legislation (Juhandi, Fahlevi and Setiadi, 2019). One

element capable of calculating the depreciation expenses of an organization is the income tax

payments. When investigating a distinction between such a business's taxable income and

income tax expenditure, a withheld tax liability emerges. The difference could be due to the

complexity as to when the real taxation is due. For instance, when measured by accounting

principles, a corporation may owe $1,000 in taxable income. In accordance of given brief

calculation of net taxable income and payable are computed. The scenario includes different

kinds of transactions which need to be addressed in accordance of UK taxation system that is as

follows:

Accommodation (Note 2)- Usually, the disparity between the rental the charge, if any, and the

gross value of the house is deductible if you are furnished with housing whether rent-free or with

a rate that is below fair rent in Fiona’s case.

Fiona is not the real owner of the house and also not paying rental for staying at company

accommodation; but she is paying Utility bills for the property which is tax deductable. She can

show this bills as expenses and can reduced her gross salary with whole amount of utility bills

paid by her. She can get a tax rebate for amount equivalent to £45,000.

The role entails a specific security danger and, if you are with the armed services, extra housing

is given for your protection in Fiona’s case scenario.

Cars and vans (Note 3) - Tax is due on a business vehicle whether a worker, business manager or

their families or household has access to it for personal use. Personal allocates resources travels

between family and office in almost all situations. For affordable vehicles, vehicles with higher

Carbon emission and automobiles which can run on renewable fuels, the return of income is

smaller. This will also be deductible if you are using your company's van personally. If all you

do, though, is carry the van back overtime with your but don't use it for any other essential

private reason, no tax would be owed in Fiona’s case scenario.

Income tax payable: The income tax payable is a form of account on the financial statements of a

particularly in the business obligations segment. Inside one year, it is accumulated with tax

payments to the state. Fiona’s estimation of the income tax owed in the country of residence of

the corporation is subject to the existing tax legislation (Juhandi, Fahlevi and Setiadi, 2019). One

element capable of calculating the depreciation expenses of an organization is the income tax

payments. When investigating a distinction between such a business's taxable income and

income tax expenditure, a withheld tax liability emerges. The difference could be due to the

complexity as to when the real taxation is due. For instance, when measured by accounting

principles, a corporation may owe $1,000 in taxable income. In accordance of given brief

calculation of net taxable income and payable are computed. The scenario includes different

kinds of transactions which need to be addressed in accordance of UK taxation system that is as

follows:

Accommodation (Note 2)- Usually, the disparity between the rental the charge, if any, and the

gross value of the house is deductible if you are furnished with housing whether rent-free or with

a rate that is below fair rent in Fiona’s case.

Fiona is not the real owner of the house and also not paying rental for staying at company

accommodation; but she is paying Utility bills for the property which is tax deductable. She can

show this bills as expenses and can reduced her gross salary with whole amount of utility bills

paid by her. She can get a tax rebate for amount equivalent to £45,000.

The role entails a specific security danger and, if you are with the armed services, extra housing

is given for your protection in Fiona’s case scenario.

Cars and vans (Note 3) - Tax is due on a business vehicle whether a worker, business manager or

their families or household has access to it for personal use. Personal allocates resources travels

between family and office in almost all situations. For affordable vehicles, vehicles with higher

Carbon emission and automobiles which can run on renewable fuels, the return of income is

smaller. This will also be deductible if you are using your company's van personally. If all you

do, though, is carry the van back overtime with your but don't use it for any other essential

private reason, no tax would be owed in Fiona’s case scenario.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

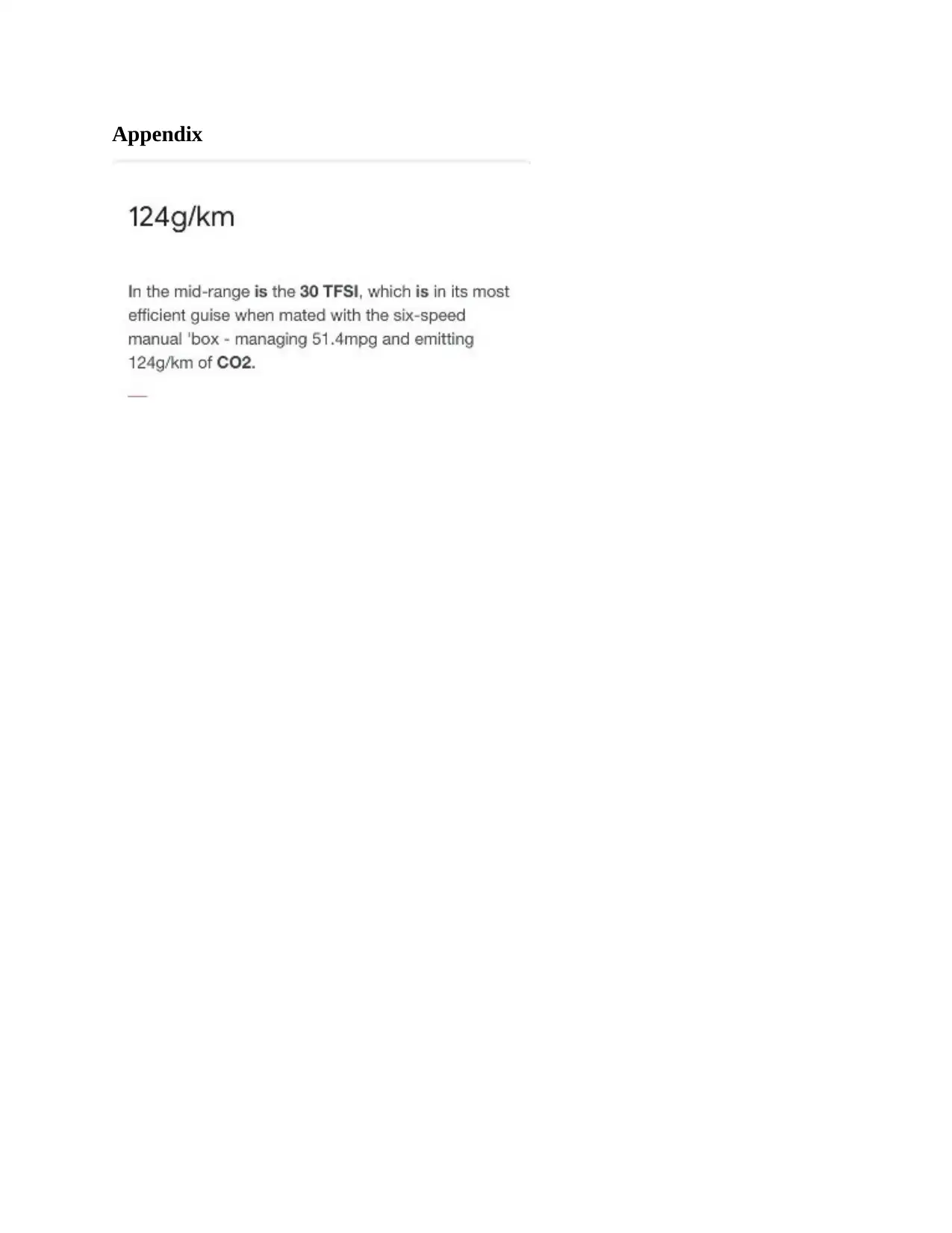

Car details:

Make – Hyundai Kona

Model – 2019 model; SUV, 5 seater, Hybrid Petrol

List Price - £25,000

Type of engine – Gear automatic, four cylinder Hybrid-Petrol engine with two horse power

pickup.

CO2 emission – Do not emit CO2; ecofriendly as it only emits hydrogen which is not harmful.

Often, vehicles are not taxable if:

They are issued for company also, and

They are not and will not be available for new use.

In reality, they are not commonly used.

Personal expenses (Note 4): if Fiona remain away from family and friends while for work to

spend funds for cash advances, such as magazines, confidential phone conversations to the sound

system or cleaning, even without charge being taxed, you will get a certain percentage of these

costs made back from the boss. For stops in the UK, the cap is £ 5 a week or £ 10 a month for

stops overseas (About tax on benefits, 2020).

Fiona is not using Music system to earn income; hence £2000 will be considered as expenses and

profit of £1000 as the basis of difference between market value and actual payment is not

recordable as profit because purchasing Music system is part of consumption not the earning

money from it.

Fiona

Annual Salary

DOB 01-06-1981

810601

810601/10

Annual Salary = 81060.1

Annual Salary = 81060

Bonus 15000

Make – Hyundai Kona

Model – 2019 model; SUV, 5 seater, Hybrid Petrol

List Price - £25,000

Type of engine – Gear automatic, four cylinder Hybrid-Petrol engine with two horse power

pickup.

CO2 emission – Do not emit CO2; ecofriendly as it only emits hydrogen which is not harmful.

Often, vehicles are not taxable if:

They are issued for company also, and

They are not and will not be available for new use.

In reality, they are not commonly used.

Personal expenses (Note 4): if Fiona remain away from family and friends while for work to

spend funds for cash advances, such as magazines, confidential phone conversations to the sound

system or cleaning, even without charge being taxed, you will get a certain percentage of these

costs made back from the boss. For stops in the UK, the cap is £ 5 a week or £ 10 a month for

stops overseas (About tax on benefits, 2020).

Fiona is not using Music system to earn income; hence £2000 will be considered as expenses and

profit of £1000 as the basis of difference between market value and actual payment is not

recordable as profit because purchasing Music system is part of consumption not the earning

money from it.

Fiona

Annual Salary

DOB 01-06-1981

810601

810601/10

Annual Salary = 81060.1

Annual Salary = 81060

Bonus 15000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

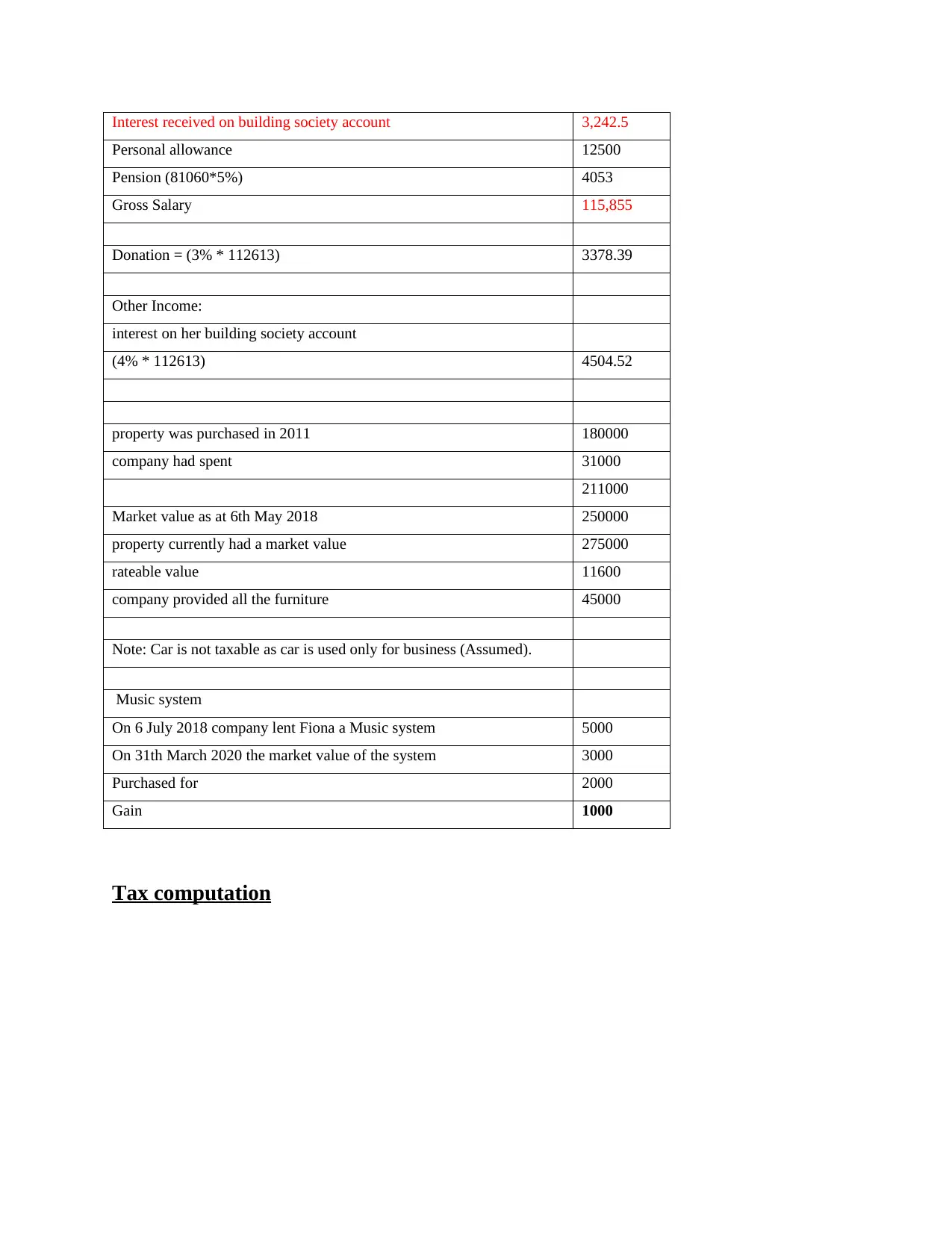

Interest received on building society account 3,242.5

Personal allowance 12500

Pension (81060*5%) 4053

Gross Salary 115,855

Donation = (3% * 112613) 3378.39

Other Income:

interest on her building society account

(4% * 112613) 4504.52

property was purchased in 2011 180000

company had spent 31000

211000

Market value as at 6th May 2018 250000

property currently had a market value 275000

rateable value 11600

company provided all the furniture 45000

Note: Car is not taxable as car is used only for business (Assumed).

Music system

On 6 July 2018 company lent Fiona a Music system 5000

On 31th March 2020 the market value of the system 3000

Purchased for 2000

Gain 1000

Tax computation

Personal allowance 12500

Pension (81060*5%) 4053

Gross Salary 115,855

Donation = (3% * 112613) 3378.39

Other Income:

interest on her building society account

(4% * 112613) 4504.52

property was purchased in 2011 180000

company had spent 31000

211000

Market value as at 6th May 2018 250000

property currently had a market value 275000

rateable value 11600

company provided all the furniture 45000

Note: Car is not taxable as car is used only for business (Assumed).

Music system

On 6 July 2018 company lent Fiona a Music system 5000

On 31th March 2020 the market value of the system 3000

Purchased for 2000

Gain 1000

Tax computation

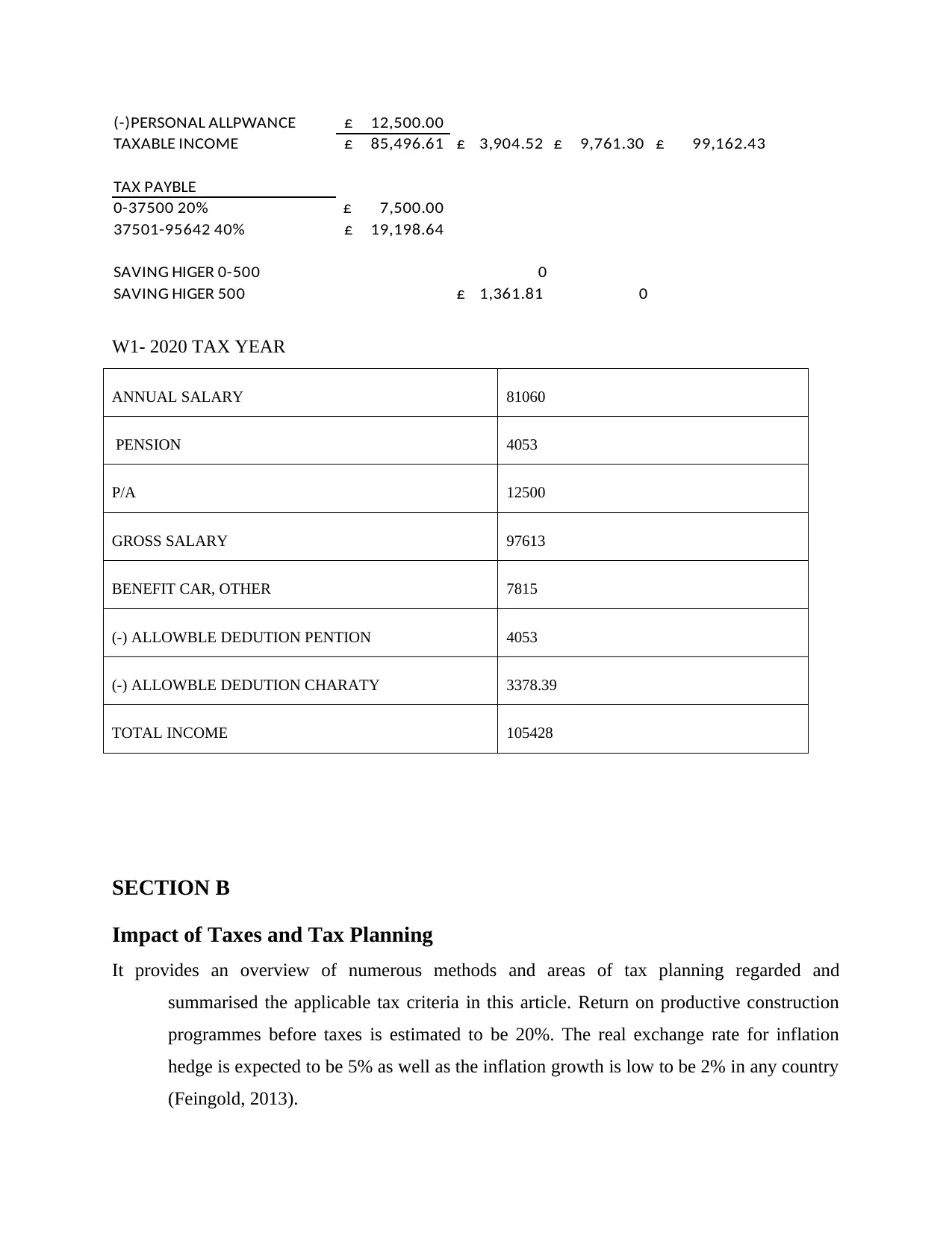

(-)PERSONAL ALLPWANCE £ 12,500.00

TAXABLE INCOME £ 85,496.61 £ 3,904.52 £ 9,761.30 £ 99,162.43

TAX PAYBLE

0-37500 20% £ 7,500.00

37501-95642 40% £ 19,198.64

SAVING HIGER 0-500 0

SAVING HIGER 500 £ 1,361.81 0

W1- 2020 TAX YEAR

ANNUAL SALARY 81060

PENSION 4053

P/A 12500

GROSS SALARY 97613

BENEFIT CAR, OTHER 7815

(-) ALLOWBLE DEDUTION PENTION 4053

(-) ALLOWBLE DEDUTION CHARATY 3378.39

TOTAL INCOME 105428

SECTION B

Impact of Taxes and Tax Planning

It provides an overview of numerous methods and areas of tax planning regarded and

summarised the applicable tax criteria in this article. Return on productive construction

programmes before taxes is estimated to be 20%. The real exchange rate for inflation

hedge is expected to be 5% as well as the inflation growth is low to be 2% in any country

(Feingold, 2013).

TAXABLE INCOME £ 85,496.61 £ 3,904.52 £ 9,761.30 £ 99,162.43

TAX PAYBLE

0-37500 20% £ 7,500.00

37501-95642 40% £ 19,198.64

SAVING HIGER 0-500 0

SAVING HIGER 500 £ 1,361.81 0

W1- 2020 TAX YEAR

ANNUAL SALARY 81060

PENSION 4053

P/A 12500

GROSS SALARY 97613

BENEFIT CAR, OTHER 7815

(-) ALLOWBLE DEDUTION PENTION 4053

(-) ALLOWBLE DEDUTION CHARATY 3378.39

TOTAL INCOME 105428

SECTION B

Impact of Taxes and Tax Planning

It provides an overview of numerous methods and areas of tax planning regarded and

summarised the applicable tax criteria in this article. Return on productive construction

programmes before taxes is estimated to be 20%. The real exchange rate for inflation

hedge is expected to be 5% as well as the inflation growth is low to be 2% in any country

(Feingold, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gardening leave: This is a concept that is common in the banking sector in the U.K.

administrative leave. An employees would normally spend time lobbying, for instance

gardening, the word extended leave. Pay levels and expenses extend until the conclusion

of the time of leave (Richards, 2018).

Payment for training and skill development of employee: The organisation seeks to provide

many avenues of improving and progressing its careers, acknowledging that some

avenues are more appealing to younger generations, whereby others are much more

appealing to mature workers. An instance, the strategy of BTD, which is outlined in the

introduction towards this series, is that employers should play a leading role in

developing a strong talent planning pipeline.

Past due salary & bonus: "salary or salary" implies all wages (other than compensation for over

time jobs) which, when they were met in stated or tacit conditions of jobs, would've

been applicable to a worker for his / her jobs or for jobs completed like this in a jobs and

will include the base pay (i.e., all payments made, by whichever name he / she is called;

"Salary or wage".

Pay in lieu of unutilised holidays: The Working Time Rules 1998 govern the time to relax. It

notes that between the Business and the worker / collective arrangement the value of the

yearly leaves are accepted as well as the legislation forbids the trading of annual lees for

cash. The legislative limit of 28 business days is assigned to a full-term employee which

is up to 8 bank holidays might well be protected by the boss.

Payment in lieu of notice (PILON): If the worker is forced to cancel an employment for certain

notice period, a 'paying instead of notice' shall mean instant remuneration equivalent to

that paying by the worker as salaries or wages, for serving the entire notification period,

rather as a month's salary. Instead, insurance for the vacation entitlements requires

reimbursement if the worker receives them (Fullagar and Francombe-Webb, 2015).

Statutory redundancy pay up to £30,000:The £30,000 exception refers only to benefits which are

not income cash payments following termination of work. Thus, in determining if the

benefit of £30,000 (and thus excluded from tax) is protected by a component in the

dismissal agreement, the very first step is to consider if this amount is a benefit amount.

Statutory redundancy pay above £30,000: Earnings contributions stay contributions of earnings

until completed and as such are entirely taxable. There is no value in the £30,000

administrative leave. An employees would normally spend time lobbying, for instance

gardening, the word extended leave. Pay levels and expenses extend until the conclusion

of the time of leave (Richards, 2018).

Payment for training and skill development of employee: The organisation seeks to provide

many avenues of improving and progressing its careers, acknowledging that some

avenues are more appealing to younger generations, whereby others are much more

appealing to mature workers. An instance, the strategy of BTD, which is outlined in the

introduction towards this series, is that employers should play a leading role in

developing a strong talent planning pipeline.

Past due salary & bonus: "salary or salary" implies all wages (other than compensation for over

time jobs) which, when they were met in stated or tacit conditions of jobs, would've

been applicable to a worker for his / her jobs or for jobs completed like this in a jobs and

will include the base pay (i.e., all payments made, by whichever name he / she is called;

"Salary or wage".

Pay in lieu of unutilised holidays: The Working Time Rules 1998 govern the time to relax. It

notes that between the Business and the worker / collective arrangement the value of the

yearly leaves are accepted as well as the legislation forbids the trading of annual lees for

cash. The legislative limit of 28 business days is assigned to a full-term employee which

is up to 8 bank holidays might well be protected by the boss.

Payment in lieu of notice (PILON): If the worker is forced to cancel an employment for certain

notice period, a 'paying instead of notice' shall mean instant remuneration equivalent to

that paying by the worker as salaries or wages, for serving the entire notification period,

rather as a month's salary. Instead, insurance for the vacation entitlements requires

reimbursement if the worker receives them (Fullagar and Francombe-Webb, 2015).

Statutory redundancy pay up to £30,000:The £30,000 exception refers only to benefits which are

not income cash payments following termination of work. Thus, in determining if the

benefit of £30,000 (and thus excluded from tax) is protected by a component in the

dismissal agreement, the very first step is to consider if this amount is a benefit amount.

Statutory redundancy pay above £30,000: Earnings contributions stay contributions of earnings

until completed and as such are entirely taxable. There is no value in the £30,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exception. However, for many other compensation received on termination, for instance

to reimburse the worker for loss of work or failing to provide a fair notice, the £30,000

exception applies. Such fees are not profits that will be paid outside of taxation in the

absence of the allowance of £ 30,000 (Hull and Donnelly, 2019).

Overseas Workday Relief

1. If one come to United Kingdom, became tax resident here as well as having international

income or earnings (i.e., incomes and earnings from outside United Kingdom) during his/her stay

in United Kingdom, one need to recognize more complicated tax laws. it is since the United

Kingdom tax scheme is attempting to tax someone resident in United Kingdom for their globally

incomes and earnings. If resident does not live in the United Kingdom, will be entitled to use the

tax justification for remittances if have international incomes or foreign earnings. Please notice

that, with effective from 6 Apr 2017, if satisfy such requirements, even if are resident and don't

live in the United Kingdom, HMRC will treat as resident as well as domiciled in United

Kingdom or deemed domiciled implying that cannot select tax basis for remittance.

Under remittance tax, one pay UK taxation in UK wages and earnings for tax year in whom they

occur, but one pay UK taxation regarding international incomes and foreign earnings only if they

are taken (or remitted) to United Kingdom. In fact, remittance basis may help discourage double

taxation. This is necessary to remember that if one have non-domiciled and have minimal sums

of unremitted overseas wages and profits (below £2,000 each tax year in United

Kingdom), remittance basis would automatically apply. In this scenario, unremitted international

wages and earnings will simply be beyond the jurisdiction of the United Kingdom tax

without need to make decision or argument. One will not forfeit tax-free personal exemption or

the annual tax-exempt sum of capital gains, neither will be responsible for the Remittance basis

(Kohlhase and Pierk, 2019

James, 2016).

2. The assignee would also require to recognize the revenue or dividends that will be needed to

be remitted to the United Kingdom within tax period. There are very detailed and complicated

rules for determining the sort of incomes and/or profits that an person has taken into the United

Kingdom when remitting sums to the United Kingdom from account that includes funds through

greater than one origin or for greater than one taxable year (Like account is recognized as "mixed

to reimburse the worker for loss of work or failing to provide a fair notice, the £30,000

exception applies. Such fees are not profits that will be paid outside of taxation in the

absence of the allowance of £ 30,000 (Hull and Donnelly, 2019).

Overseas Workday Relief

1. If one come to United Kingdom, became tax resident here as well as having international

income or earnings (i.e., incomes and earnings from outside United Kingdom) during his/her stay

in United Kingdom, one need to recognize more complicated tax laws. it is since the United

Kingdom tax scheme is attempting to tax someone resident in United Kingdom for their globally

incomes and earnings. If resident does not live in the United Kingdom, will be entitled to use the

tax justification for remittances if have international incomes or foreign earnings. Please notice

that, with effective from 6 Apr 2017, if satisfy such requirements, even if are resident and don't

live in the United Kingdom, HMRC will treat as resident as well as domiciled in United

Kingdom or deemed domiciled implying that cannot select tax basis for remittance.

Under remittance tax, one pay UK taxation in UK wages and earnings for tax year in whom they

occur, but one pay UK taxation regarding international incomes and foreign earnings only if they

are taken (or remitted) to United Kingdom. In fact, remittance basis may help discourage double

taxation. This is necessary to remember that if one have non-domiciled and have minimal sums

of unremitted overseas wages and profits (below £2,000 each tax year in United

Kingdom), remittance basis would automatically apply. In this scenario, unremitted international

wages and earnings will simply be beyond the jurisdiction of the United Kingdom tax

without need to make decision or argument. One will not forfeit tax-free personal exemption or

the annual tax-exempt sum of capital gains, neither will be responsible for the Remittance basis

(Kohlhase and Pierk, 2019

James, 2016).

2. The assignee would also require to recognize the revenue or dividends that will be needed to

be remitted to the United Kingdom within tax period. There are very detailed and complicated

rules for determining the sort of incomes and/or profits that an person has taken into the United

Kingdom when remitting sums to the United Kingdom from account that includes funds through

greater than one origin or for greater than one taxable year (Like account is recognized as "mixed

fund"). Such mixed fund laws can and often do give lead to major undesired tax consequences

for the unsuspecting. This is crucial that persons who are whether currently taxed on remittance

basis or have formerly been taxed on remittance basis obtain guidance prior remitting funds /

assets to United Kingdom This extends even if original source of funds was UK taxed earnings

and/or benefits.

3. If one non-UK citizen who come to live in the United Kingdom but haven't been citizen in the

United Kingdom for at least last three successive years of taxation in the United Kingdom,

one will be entitled to demand income tax exemption for overseas working days in first three

income taxes of UK residency. This exemption is applicable to individuals who claim tax base

for remittances and where wages for their international working days are compensated and held

international. Such profits are then payable in the United Kingdom and to the point that they are

repatriated to the United Kingdom (James, 2016).

for the unsuspecting. This is crucial that persons who are whether currently taxed on remittance

basis or have formerly been taxed on remittance basis obtain guidance prior remitting funds /

assets to United Kingdom This extends even if original source of funds was UK taxed earnings

and/or benefits.

3. If one non-UK citizen who come to live in the United Kingdom but haven't been citizen in the

United Kingdom for at least last three successive years of taxation in the United Kingdom,

one will be entitled to demand income tax exemption for overseas working days in first three

income taxes of UK residency. This exemption is applicable to individuals who claim tax base

for remittances and where wages for their international working days are compensated and held

international. Such profits are then payable in the United Kingdom and to the point that they are

repatriated to the United Kingdom (James, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Feingold, R. P., 2013. Every little girl can grow up to be queen: the coronation and The Virgin in

the Garden. Literature & History, 22(2), pp.73-90.

Fullagar, S. and Francombe-Webb, J., 2015. This Girl Can campaign is all about sex, not sport.

Hull, R. and Donnelly, R., 2019. THIS GIRL CAN FIGHT. Feminist Applied Sport Psychology:

From Theory to Practice.

Richards, L., 2018. Can girls play sport? Gender performativity in online responses to Sport

England’s This Girl Can campaign. In The Palgrave Handbook of Feminism and Sport,

Leisure and Physical Education (pp. 757-767). Palgrave Macmillan, London.

Kohlhase, S. and Pierk, J., 2019. The effect of a worldwide tax system on tax management of

foreign subsidiaries. Journal of International Business Studies, pp.1-19.

James, S., 2016. The complexity of tax simplification: the UK experience. In The Complexity of

Tax Simplification (pp. 229-246). Palgrave Macmillan, London.

Juhandi, N., Fahlevi, M. and Setiadi, S., 2019. Tax Policy and Fiscal Consolidation on Corporate

Income Tax. Journal of Business Management and Accounting, 1(1), p.322972

Online:

About tax on benefits, 2020 [online] available through :<https://www.citizensadvice.org.uk/debt-

and-money/tax/what-is-taxable-income/tax-on-benefits-in-kind/>.

Books and Journals

Feingold, R. P., 2013. Every little girl can grow up to be queen: the coronation and The Virgin in

the Garden. Literature & History, 22(2), pp.73-90.

Fullagar, S. and Francombe-Webb, J., 2015. This Girl Can campaign is all about sex, not sport.

Hull, R. and Donnelly, R., 2019. THIS GIRL CAN FIGHT. Feminist Applied Sport Psychology:

From Theory to Practice.

Richards, L., 2018. Can girls play sport? Gender performativity in online responses to Sport

England’s This Girl Can campaign. In The Palgrave Handbook of Feminism and Sport,

Leisure and Physical Education (pp. 757-767). Palgrave Macmillan, London.

Kohlhase, S. and Pierk, J., 2019. The effect of a worldwide tax system on tax management of

foreign subsidiaries. Journal of International Business Studies, pp.1-19.

James, S., 2016. The complexity of tax simplification: the UK experience. In The Complexity of

Tax Simplification (pp. 229-246). Palgrave Macmillan, London.

Juhandi, N., Fahlevi, M. and Setiadi, S., 2019. Tax Policy and Fiscal Consolidation on Corporate

Income Tax. Journal of Business Management and Accounting, 1(1), p.322972

Online:

About tax on benefits, 2020 [online] available through :<https://www.citizensadvice.org.uk/debt-

and-money/tax/what-is-taxable-income/tax-on-benefits-in-kind/>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.