Taxation of Business Income

VerifiedAdded on 2020/01/23

|16

|4720

|50

Essay

AI Summary

This assignment delves into the UK taxation system with a particular focus on business income. It examines various aspects, including income tax reliefs applicable to business owners, the roles and responsibilities of tax practitioners involved in this area, and fundamental concepts related to business taxation. The provided resources include academic journal articles and online publications from authoritative sources such as the UK government website, offering insights into the complexities of navigating the UK tax system for businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Taxation ...............................................................................................................................................1

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Describing the tax environment of UK......................................................................................3

1.2 Analyzing the roles and responsibilities of tax practitioner.......................................................4

1.3 Explaining the tax obligations of tax payers or their agents along with the implications of

non-compliance ...............................................................................................................................6

TASK 2.................................................................................................................................................7

2.1 Calculating relevant income, expense and allowances .............................................................7

2.2 Assessing the taxable amount for the employment at supermarket and calculating self

employment income ........................................................................................................................8

2.3 Completing relevant documentation and tax return for Susan .................................................9

TASK 3...............................................................................................................................................10

3.1 Calculating chargeable profit for the company .......................................................................10

3.2 Calculating the tax liability of the company............................................................................11

3.3 Explaining the ways through which one can deal with the income tax deductions ................12

TASK 4...............................................................................................................................................12

4.1 Identifying chargeable asset ....................................................................................................12

4.2 Calculating capital gain and losses .........................................................................................12

4.3 Calculating the tax payable capital gain .................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

2

Taxation ...............................................................................................................................................1

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Describing the tax environment of UK......................................................................................3

1.2 Analyzing the roles and responsibilities of tax practitioner.......................................................4

1.3 Explaining the tax obligations of tax payers or their agents along with the implications of

non-compliance ...............................................................................................................................6

TASK 2.................................................................................................................................................7

2.1 Calculating relevant income, expense and allowances .............................................................7

2.2 Assessing the taxable amount for the employment at supermarket and calculating self

employment income ........................................................................................................................8

2.3 Completing relevant documentation and tax return for Susan .................................................9

TASK 3...............................................................................................................................................10

3.1 Calculating chargeable profit for the company .......................................................................10

3.2 Calculating the tax liability of the company............................................................................11

3.3 Explaining the ways through which one can deal with the income tax deductions ................12

TASK 4...............................................................................................................................................12

4.1 Identifying chargeable asset ....................................................................................................12

4.2 Calculating capital gain and losses .........................................................................................12

4.3 Calculating the tax payable capital gain .................................................................................13

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................15

2

INTRODUCTION

Taxation is the source through which the government finance their expenses by levying tax

on the citizen and corporate entities. The main aim of the government behind taxation is to

encourage or discourage the certain economic decisions. For the purpose of taxation, UK

government has framed and introduced several rules and regulations in relation which tax

practitioners, corporate entities must follow while determining their obligation. In this way, by

charging suitable amount of tax, government can collect and employ fund in the productive

activities. The present is based on different case scenarios which will shed light on UK tax

environment. Further, it will develop understanding about the roles and responsibilities which tax

practitioner need to perform. This report will also describe the ways through which one can

calculate the taxable income, loss and capital gain.

TASK 1

1.1 Describing the tax environment of UK

In UK, each and every individual who are earning is obliged to pay tax to the government

through the means of tax department and the authority such as Her Majesty's Revenues and

Customs (HMRC). It is the responsibility of such authority to make available fund for the public

services and welfare by imposing tax on the citizens etc. HMRC is assigned with the responsibility

to gather tax from both individuals and corporate entities through the means of both direct as well

as indirect tax (Devereux, Liu and Loretz, 2014). Besides this, HMRC works with the treasury

system of UK for ensuring the smooth functioning of tax system. In accordance with the UK tax

framework, there are mainly two types of tax which are as follows:

Direct tax: Obligations which are determined on the basis of income, profit or gains in terms of

tax are termed as direct taxes. Such gains are either deducted or paid by the tax payer to the relevant

authorities when it becomes due. Examples of main direct taxes include income, corporation and

capital gain related obligations. All the direct tax related obligations are administered and controlled

by HMRC. Income tax: This type of tax is paid by the individual partnership companies and citizens

whose income level crosses the predetermined limit. Income tax is charged on the money

earned by the individual from employment, self-employment, and interest on saving, shares,

rental and pension gain (Tiley and Loutzenhiser, 2012). Besides this, at the time of

determining tax obligations of the individual HMRC segregates it into three types such as

saving, non-saving and dividend income. For the purpose of assessing suitable tax amount

3

Taxation is the source through which the government finance their expenses by levying tax

on the citizen and corporate entities. The main aim of the government behind taxation is to

encourage or discourage the certain economic decisions. For the purpose of taxation, UK

government has framed and introduced several rules and regulations in relation which tax

practitioners, corporate entities must follow while determining their obligation. In this way, by

charging suitable amount of tax, government can collect and employ fund in the productive

activities. The present is based on different case scenarios which will shed light on UK tax

environment. Further, it will develop understanding about the roles and responsibilities which tax

practitioner need to perform. This report will also describe the ways through which one can

calculate the taxable income, loss and capital gain.

TASK 1

1.1 Describing the tax environment of UK

In UK, each and every individual who are earning is obliged to pay tax to the government

through the means of tax department and the authority such as Her Majesty's Revenues and

Customs (HMRC). It is the responsibility of such authority to make available fund for the public

services and welfare by imposing tax on the citizens etc. HMRC is assigned with the responsibility

to gather tax from both individuals and corporate entities through the means of both direct as well

as indirect tax (Devereux, Liu and Loretz, 2014). Besides this, HMRC works with the treasury

system of UK for ensuring the smooth functioning of tax system. In accordance with the UK tax

framework, there are mainly two types of tax which are as follows:

Direct tax: Obligations which are determined on the basis of income, profit or gains in terms of

tax are termed as direct taxes. Such gains are either deducted or paid by the tax payer to the relevant

authorities when it becomes due. Examples of main direct taxes include income, corporation and

capital gain related obligations. All the direct tax related obligations are administered and controlled

by HMRC. Income tax: This type of tax is paid by the individual partnership companies and citizens

whose income level crosses the predetermined limit. Income tax is charged on the money

earned by the individual from employment, self-employment, and interest on saving, shares,

rental and pension gain (Tiley and Loutzenhiser, 2012). Besides this, at the time of

determining tax obligations of the individual HMRC segregates it into three types such as

saving, non-saving and dividend income. For the purpose of assessing suitable tax amount

3

IT Act 2003, Capital Allowance Act (CAA) 2001 is undertaken by HMRC. Corporation tax: Such kind of tax is paid by the business corporations in accordance with

the laws and legislation of IT Act 2003, Income and corporation Taxes Act (2001).

Capital gain tax: It occurs when investors receive higher money by selling the assets or

shares in comparison to the purchase price.

Indirect tax: It refers to those which are levied by the government on goods and services rather than

on income or profit aspect. Indirect taxes which are charged by UK government include sales tax,

VAT (value added tax) and GST.

VAT: In UK, VAT is charged by UK government on the good or services which are imported

by the business entities from outside the European Union (Mertens and Ravn, 2013). Rates

of VAT highly vary in accordance with the goods or services in the following manner:

Standard = 20%

Reduced = 5%

Zero = 0%

On the basis of the above mentioned table, goods which come into the category of reduced

rates are domestic fuel and power, installing energy saving material, sanitary hygiene products,

children car seats etc. Along with this, goods or services which are free from the VAT obligations

include food but not meals in restaurant, books and newspapers, children clothes as well as shoes,

public transport etc. Excise duty: This tax is charged by UK government on goods which are produced within the

country (Lecca and et.al, 2014). Hence, it is highly related to the production or sale of a

good. Examples of excise duty include alcohol and tobacco.

Custom duty: Such kind of duty is charged by the UK government on importation of goods

which are produced by other countries except EU.

1.2 Analyzing the roles and responsibilities of tax practitioner

Tax practitioner is the one who fulfils obligation of the third party in relation to SARS return

for reward or fee. Usually, tax payers take assistance of professionals for determining their financial

obligations because they have deeper insight about the rules and regulations which are related to it

(Brewer and et.al, 2013). In this way, tax practitioners provide high level of assistance to the payers

in filing the return according to HMRC. In this regard, there are several roles and responsibilities

which tax practitioner need to perform which are as follows:

Roles of tax practitioner

4

the laws and legislation of IT Act 2003, Income and corporation Taxes Act (2001).

Capital gain tax: It occurs when investors receive higher money by selling the assets or

shares in comparison to the purchase price.

Indirect tax: It refers to those which are levied by the government on goods and services rather than

on income or profit aspect. Indirect taxes which are charged by UK government include sales tax,

VAT (value added tax) and GST.

VAT: In UK, VAT is charged by UK government on the good or services which are imported

by the business entities from outside the European Union (Mertens and Ravn, 2013). Rates

of VAT highly vary in accordance with the goods or services in the following manner:

Standard = 20%

Reduced = 5%

Zero = 0%

On the basis of the above mentioned table, goods which come into the category of reduced

rates are domestic fuel and power, installing energy saving material, sanitary hygiene products,

children car seats etc. Along with this, goods or services which are free from the VAT obligations

include food but not meals in restaurant, books and newspapers, children clothes as well as shoes,

public transport etc. Excise duty: This tax is charged by UK government on goods which are produced within the

country (Lecca and et.al, 2014). Hence, it is highly related to the production or sale of a

good. Examples of excise duty include alcohol and tobacco.

Custom duty: Such kind of duty is charged by the UK government on importation of goods

which are produced by other countries except EU.

1.2 Analyzing the roles and responsibilities of tax practitioner

Tax practitioner is the one who fulfils obligation of the third party in relation to SARS return

for reward or fee. Usually, tax payers take assistance of professionals for determining their financial

obligations because they have deeper insight about the rules and regulations which are related to it

(Brewer and et.al, 2013). In this way, tax practitioners provide high level of assistance to the payers

in filing the return according to HMRC. In this regard, there are several roles and responsibilities

which tax practitioner need to perform which are as follows:

Roles of tax practitioner

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Tax practitioner plays a vital role in dealing with HMRC on behalf of clients. Further, such

professional authority provides high level of assistance to the payer by fulfilling all the tax

requirements according to HMRC on behalf of him. Tax practitioner also acts as an intermediary

between the tax collector and payer (Saez, Slemrod and Giertz, 2012). Moreover, professional

authority gives advice to the payer in relation to the laws and submits the return to HMRC on behalf

of him. Along with this, tax practitioner also helps in reducing effects of financial obligations of

payer to the large extent. The reason behind this is that such personnel have high level technical

knowledge about the tax laws and legislation (Wang, 2013). In this way, practitioner reduces the tax

liabilities of the payer to the great extent. Along with this, taxpayer role is to provide help to the

payer in paying income, corporation and capital gain tax. Hence, by taking into account all the

above mentioned aspects it can be said that tax practitioner plays an important role in advising and

persuading the payers about the tax laws. Moreover, tax practitioner clearly communicates to the

payers about the risk and opportunities which are available them.

Responsibilities of tax practitioner

Tax practitioner has the responsibility to comply with all the laws and legislation which are

introduced by UK government while giving advice to the clients.

Such professional authority is also accountable for preparing good tax returns for the client

honestly. Moreover, tax professionals have proper knowledge about the rules related to

taxation rather than others.

Further, tax practitioner also has the accountability to maintain confidentiality in relation to

the information which is served by the client (Reforms, Kleven and Schultz, 2014). On the

basis of this aspect, practitioner does not leak the information of the client without his prior

permission.

In addition to this, tax practitioner also needs to update with the changes take place in the

laws and legislation. Moreover, in the absence of updated information, tax practitioner

would not able to give suitable advice to client about the tax aspects (Roles and

responsibilities of tax practitioner, 2016). Thus, such personnel are required to follow the

updated laws and legislation while filing the return for their client.

In addition to this, tax practitioner is obliged to determine the suitable taxable income

which will not more than the law requires.

Hence, by performing all such roles and responsibilities tax practitioner can offer high

quality services to the clients.

5

professional authority provides high level of assistance to the payer by fulfilling all the tax

requirements according to HMRC on behalf of him. Tax practitioner also acts as an intermediary

between the tax collector and payer (Saez, Slemrod and Giertz, 2012). Moreover, professional

authority gives advice to the payer in relation to the laws and submits the return to HMRC on behalf

of him. Along with this, tax practitioner also helps in reducing effects of financial obligations of

payer to the large extent. The reason behind this is that such personnel have high level technical

knowledge about the tax laws and legislation (Wang, 2013). In this way, practitioner reduces the tax

liabilities of the payer to the great extent. Along with this, taxpayer role is to provide help to the

payer in paying income, corporation and capital gain tax. Hence, by taking into account all the

above mentioned aspects it can be said that tax practitioner plays an important role in advising and

persuading the payers about the tax laws. Moreover, tax practitioner clearly communicates to the

payers about the risk and opportunities which are available them.

Responsibilities of tax practitioner

Tax practitioner has the responsibility to comply with all the laws and legislation which are

introduced by UK government while giving advice to the clients.

Such professional authority is also accountable for preparing good tax returns for the client

honestly. Moreover, tax professionals have proper knowledge about the rules related to

taxation rather than others.

Further, tax practitioner also has the accountability to maintain confidentiality in relation to

the information which is served by the client (Reforms, Kleven and Schultz, 2014). On the

basis of this aspect, practitioner does not leak the information of the client without his prior

permission.

In addition to this, tax practitioner also needs to update with the changes take place in the

laws and legislation. Moreover, in the absence of updated information, tax practitioner

would not able to give suitable advice to client about the tax aspects (Roles and

responsibilities of tax practitioner, 2016). Thus, such personnel are required to follow the

updated laws and legislation while filing the return for their client.

In addition to this, tax practitioner is obliged to determine the suitable taxable income

which will not more than the law requires.

Hence, by performing all such roles and responsibilities tax practitioner can offer high

quality services to the clients.

5

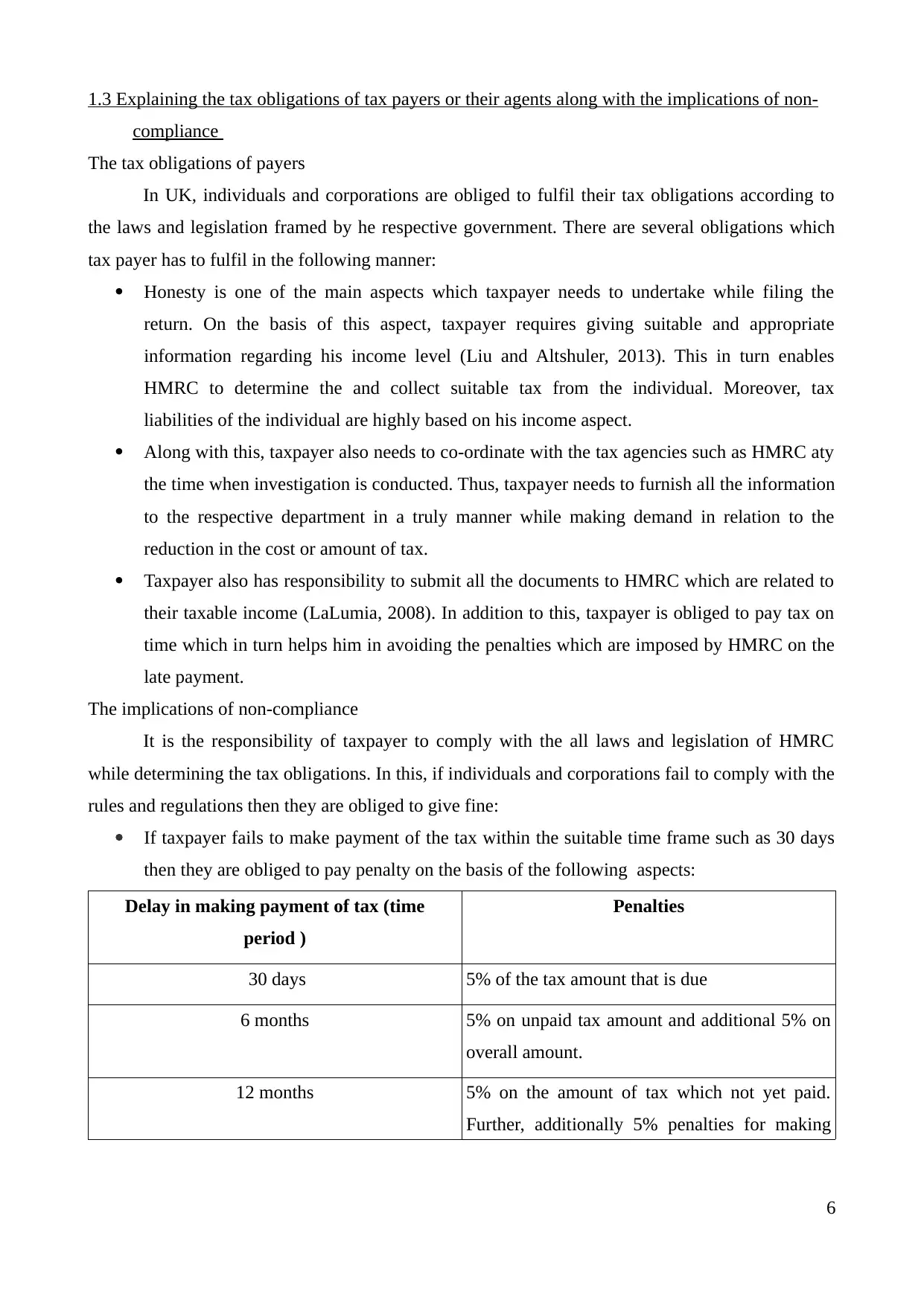

1.3 Explaining the tax obligations of tax payers or their agents along with the implications of non-

compliance

The tax obligations of payers

In UK, individuals and corporations are obliged to fulfil their tax obligations according to

the laws and legislation framed by he respective government. There are several obligations which

tax payer has to fulfil in the following manner:

Honesty is one of the main aspects which taxpayer needs to undertake while filing the

return. On the basis of this aspect, taxpayer requires giving suitable and appropriate

information regarding his income level (Liu and Altshuler, 2013). This in turn enables

HMRC to determine the and collect suitable tax from the individual. Moreover, tax

liabilities of the individual are highly based on his income aspect.

Along with this, taxpayer also needs to co-ordinate with the tax agencies such as HMRC aty

the time when investigation is conducted. Thus, taxpayer needs to furnish all the information

to the respective department in a truly manner while making demand in relation to the

reduction in the cost or amount of tax.

Taxpayer also has responsibility to submit all the documents to HMRC which are related to

their taxable income (LaLumia, 2008). In addition to this, taxpayer is obliged to pay tax on

time which in turn helps him in avoiding the penalties which are imposed by HMRC on the

late payment.

The implications of non-compliance

It is the responsibility of taxpayer to comply with the all laws and legislation of HMRC

while determining the tax obligations. In this, if individuals and corporations fail to comply with the

rules and regulations then they are obliged to give fine:

If taxpayer fails to make payment of the tax within the suitable time frame such as 30 days

then they are obliged to pay penalty on the basis of the following aspects:

Delay in making payment of tax (time

period )

Penalties

30 days 5% of the tax amount that is due

6 months 5% on unpaid tax amount and additional 5% on

overall amount.

12 months 5% on the amount of tax which not yet paid.

Further, additionally 5% penalties for making

6

compliance

The tax obligations of payers

In UK, individuals and corporations are obliged to fulfil their tax obligations according to

the laws and legislation framed by he respective government. There are several obligations which

tax payer has to fulfil in the following manner:

Honesty is one of the main aspects which taxpayer needs to undertake while filing the

return. On the basis of this aspect, taxpayer requires giving suitable and appropriate

information regarding his income level (Liu and Altshuler, 2013). This in turn enables

HMRC to determine the and collect suitable tax from the individual. Moreover, tax

liabilities of the individual are highly based on his income aspect.

Along with this, taxpayer also needs to co-ordinate with the tax agencies such as HMRC aty

the time when investigation is conducted. Thus, taxpayer needs to furnish all the information

to the respective department in a truly manner while making demand in relation to the

reduction in the cost or amount of tax.

Taxpayer also has responsibility to submit all the documents to HMRC which are related to

their taxable income (LaLumia, 2008). In addition to this, taxpayer is obliged to pay tax on

time which in turn helps him in avoiding the penalties which are imposed by HMRC on the

late payment.

The implications of non-compliance

It is the responsibility of taxpayer to comply with the all laws and legislation of HMRC

while determining the tax obligations. In this, if individuals and corporations fail to comply with the

rules and regulations then they are obliged to give fine:

If taxpayer fails to make payment of the tax within the suitable time frame such as 30 days

then they are obliged to pay penalty on the basis of the following aspects:

Delay in making payment of tax (time

period )

Penalties

30 days 5% of the tax amount that is due

6 months 5% on unpaid tax amount and additional 5% on

overall amount.

12 months 5% on the amount of tax which not yet paid.

Further, additionally 5% penalties for making

6

delay in the payment of tax by 12 months.

Along with this, taxpayer is obliged to submit the return to HMRC within the predetermined

time frame. If taxpayers make default in such performance then they are obliged to pay fine.

On the basis of this aspect, penalty of £100 will be charged by HMRC if individual delays 1

day in the submission of return (Freebairn and Quiggin, 2010). Whereas, in the case of 3

months delay maximum penalty of £900 will be charged by HMRC. In addition to this, in

the case of 6 months delay penalty of £300 or 5% of due amount will be imposed by HMRC

on individual.

TASK 2

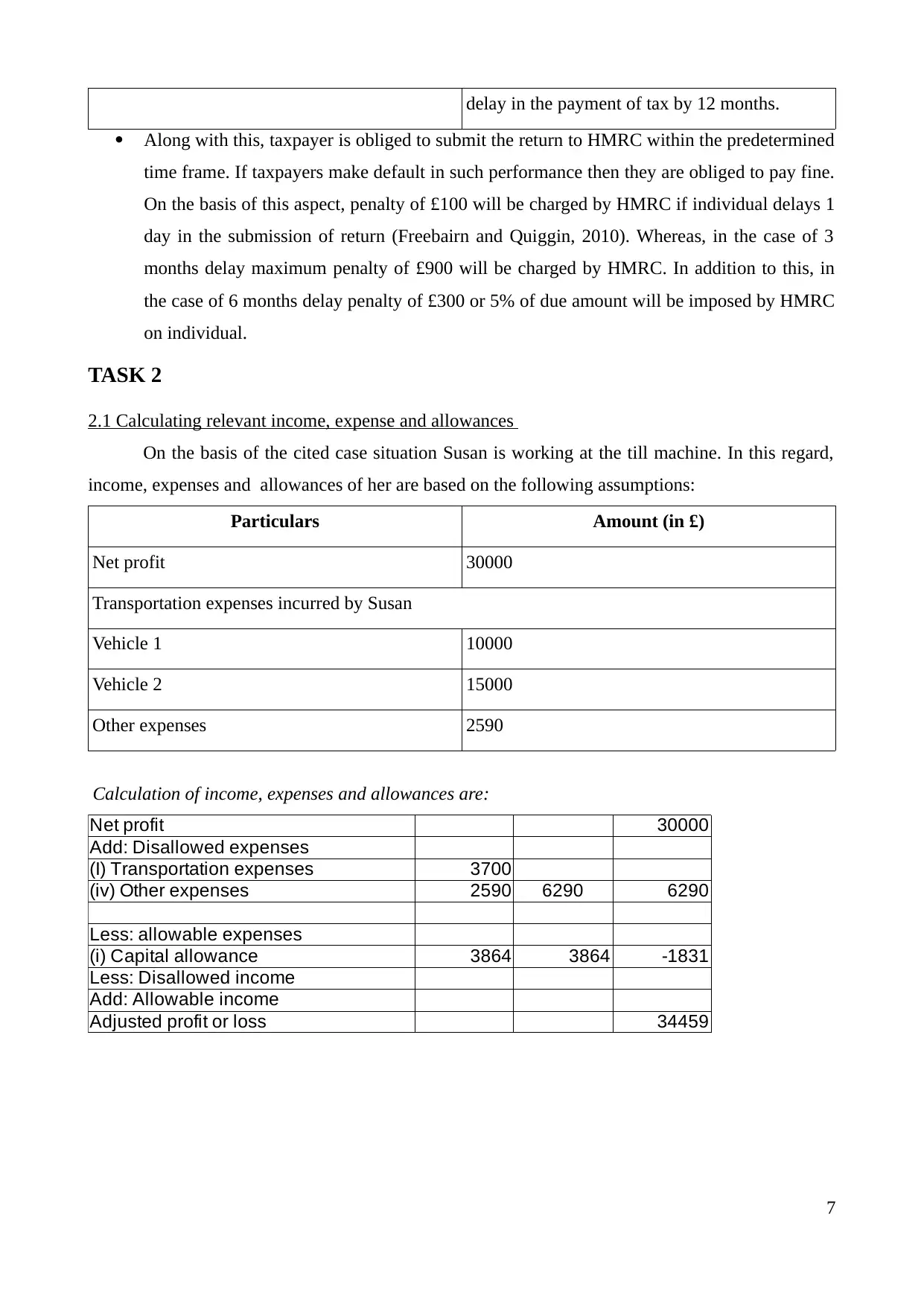

2.1 Calculating relevant income, expense and allowances

On the basis of the cited case situation Susan is working at the till machine. In this regard,

income, expenses and allowances of her are based on the following assumptions:

Particulars Amount (in £)

Net profit 30000

Transportation expenses incurred by Susan

Vehicle 1 10000

Vehicle 2 15000

Other expenses 2590

Calculation of income, expenses and allowances are:

Net profit 30000

Add: Disallowed expenses

(I) Transportation expenses 3700

(iv) Other expenses 2590 6290 6290

Less: allowable expenses

(i) Capital allowance 3864 3864 -1831

Less: Disallowed income

Add: Allowable income

Adjusted profit or loss 34459

7

Along with this, taxpayer is obliged to submit the return to HMRC within the predetermined

time frame. If taxpayers make default in such performance then they are obliged to pay fine.

On the basis of this aspect, penalty of £100 will be charged by HMRC if individual delays 1

day in the submission of return (Freebairn and Quiggin, 2010). Whereas, in the case of 3

months delay maximum penalty of £900 will be charged by HMRC. In addition to this, in

the case of 6 months delay penalty of £300 or 5% of due amount will be imposed by HMRC

on individual.

TASK 2

2.1 Calculating relevant income, expense and allowances

On the basis of the cited case situation Susan is working at the till machine. In this regard,

income, expenses and allowances of her are based on the following assumptions:

Particulars Amount (in £)

Net profit 30000

Transportation expenses incurred by Susan

Vehicle 1 10000

Vehicle 2 15000

Other expenses 2590

Calculation of income, expenses and allowances are:

Net profit 30000

Add: Disallowed expenses

(I) Transportation expenses 3700

(iv) Other expenses 2590 6290 6290

Less: allowable expenses

(i) Capital allowance 3864 3864 -1831

Less: Disallowed income

Add: Allowable income

Adjusted profit or loss 34459

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

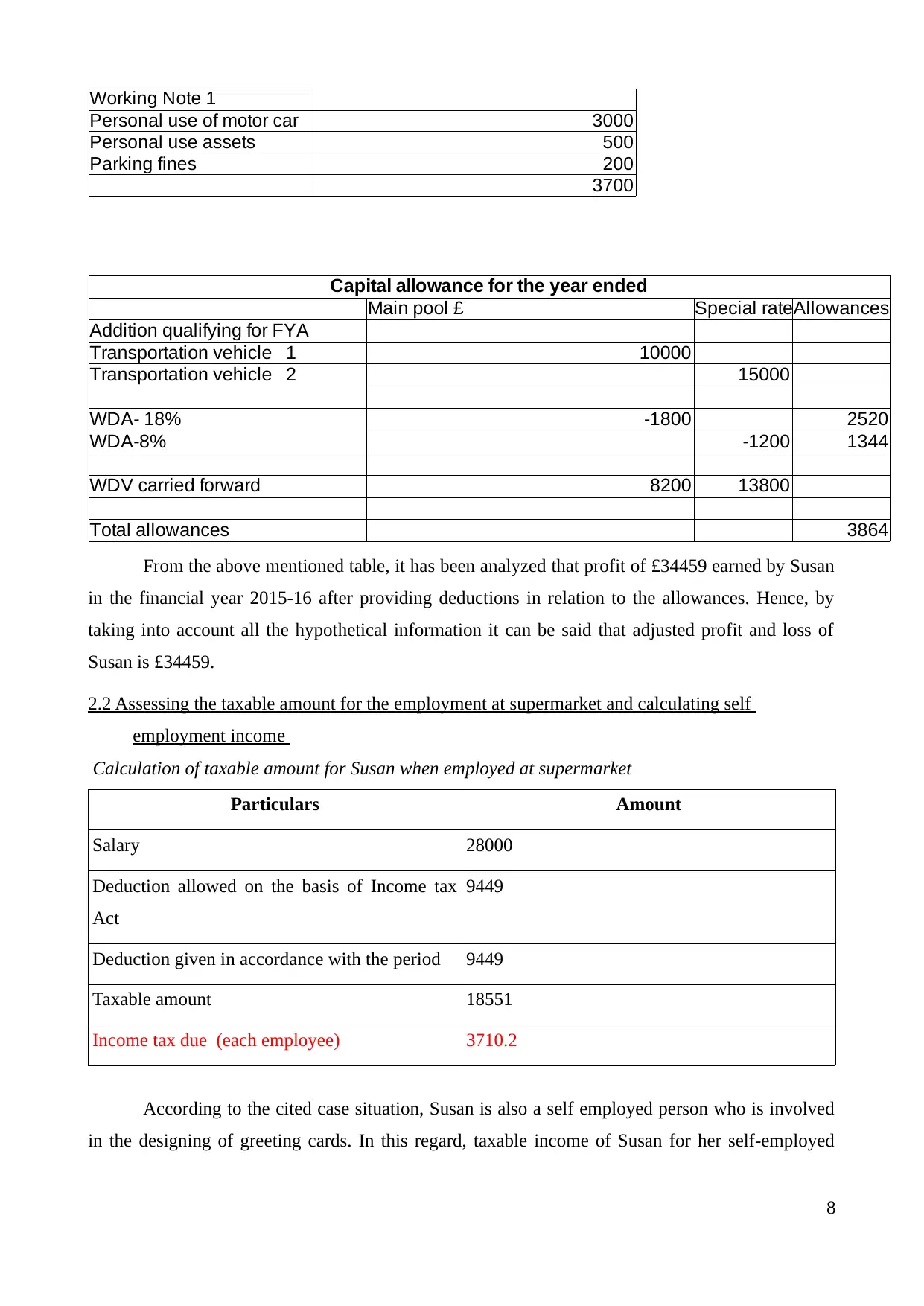

Working Note 1

Personal use of motor car 3000

Personal use assets 500

Parking fines 200

3700

Capital allowance for the year ended

Main pool £ Special rate pool £Allowances £

Addition qualifying for FYA

Transportation vehicle 1 10000

Transportation vehicle 2 15000

WDA- 18% -1800 2520

WDA-8% -1200 1344

WDV carried forward 8200 13800

Total allowances 3864

From the above mentioned table, it has been analyzed that profit of £34459 earned by Susan

in the financial year 2015-16 after providing deductions in relation to the allowances. Hence, by

taking into account all the hypothetical information it can be said that adjusted profit and loss of

Susan is £34459.

2.2 Assessing the taxable amount for the employment at supermarket and calculating self

employment income

Calculation of taxable amount for Susan when employed at supermarket

Particulars Amount

Salary 28000

Deduction allowed on the basis of Income tax

Act

9449

Deduction given in accordance with the period 9449

Taxable amount 18551

Income tax due (each employee) 3710.2

According to the cited case situation, Susan is also a self employed person who is involved

in the designing of greeting cards. In this regard, taxable income of Susan for her self-employed

8

Personal use of motor car 3000

Personal use assets 500

Parking fines 200

3700

Capital allowance for the year ended

Main pool £ Special rate pool £Allowances £

Addition qualifying for FYA

Transportation vehicle 1 10000

Transportation vehicle 2 15000

WDA- 18% -1800 2520

WDA-8% -1200 1344

WDV carried forward 8200 13800

Total allowances 3864

From the above mentioned table, it has been analyzed that profit of £34459 earned by Susan

in the financial year 2015-16 after providing deductions in relation to the allowances. Hence, by

taking into account all the hypothetical information it can be said that adjusted profit and loss of

Susan is £34459.

2.2 Assessing the taxable amount for the employment at supermarket and calculating self

employment income

Calculation of taxable amount for Susan when employed at supermarket

Particulars Amount

Salary 28000

Deduction allowed on the basis of Income tax

Act

9449

Deduction given in accordance with the period 9449

Taxable amount 18551

Income tax due (each employee) 3710.2

According to the cited case situation, Susan is also a self employed person who is involved

in the designing of greeting cards. In this regard, taxable income of Susan for her self-employed

8

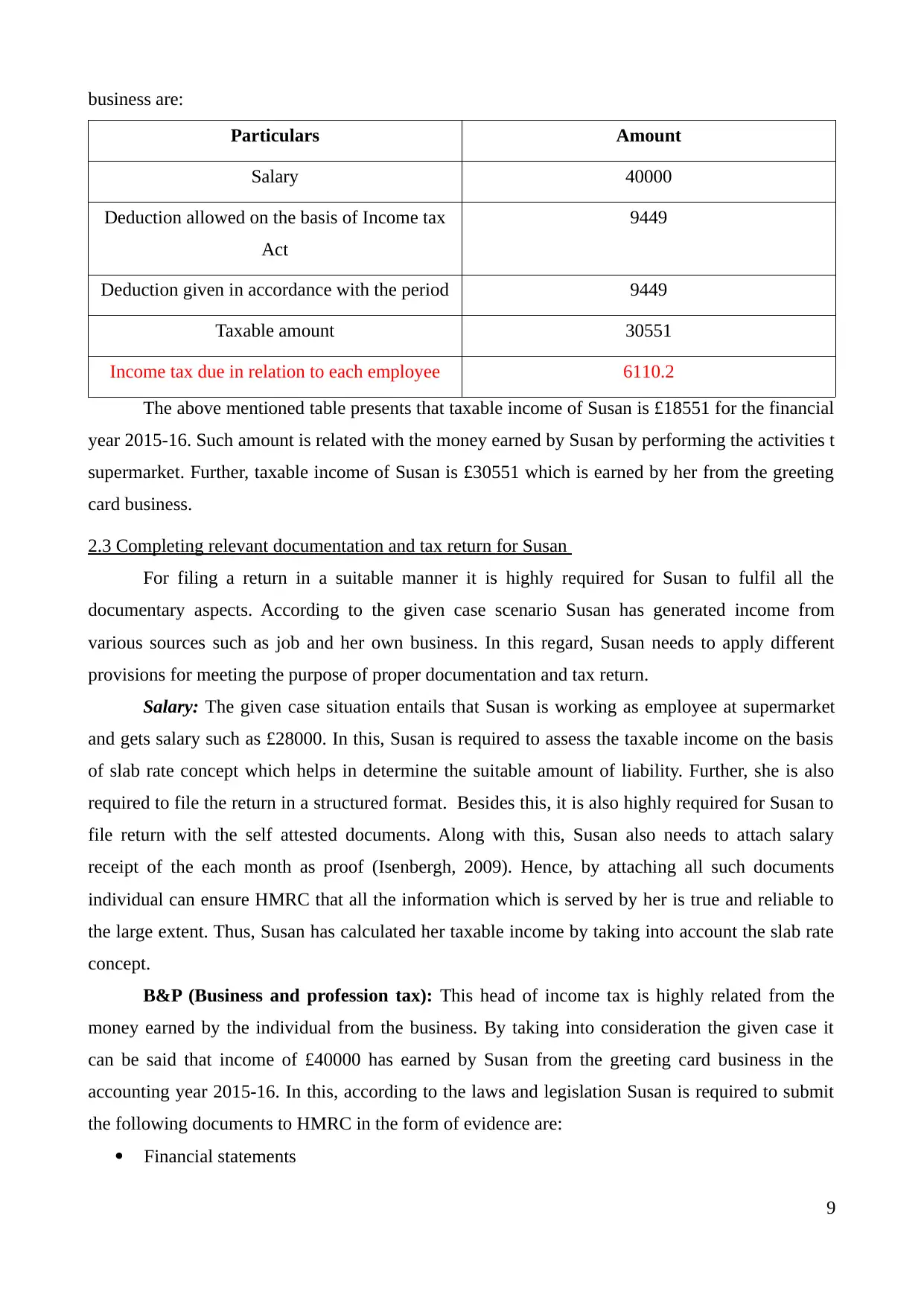

business are:

Particulars Amount

Salary 40000

Deduction allowed on the basis of Income tax

Act

9449

Deduction given in accordance with the period 9449

Taxable amount 30551

Income tax due in relation to each employee 6110.2

The above mentioned table presents that taxable income of Susan is £18551 for the financial

year 2015-16. Such amount is related with the money earned by Susan by performing the activities t

supermarket. Further, taxable income of Susan is £30551 which is earned by her from the greeting

card business.

2.3 Completing relevant documentation and tax return for Susan

For filing a return in a suitable manner it is highly required for Susan to fulfil all the

documentary aspects. According to the given case scenario Susan has generated income from

various sources such as job and her own business. In this regard, Susan needs to apply different

provisions for meeting the purpose of proper documentation and tax return.

Salary: The given case situation entails that Susan is working as employee at supermarket

and gets salary such as £28000. In this, Susan is required to assess the taxable income on the basis

of slab rate concept which helps in determine the suitable amount of liability. Further, she is also

required to file the return in a structured format. Besides this, it is also highly required for Susan to

file return with the self attested documents. Along with this, Susan also needs to attach salary

receipt of the each month as proof (Isenbergh, 2009). Hence, by attaching all such documents

individual can ensure HMRC that all the information which is served by her is true and reliable to

the large extent. Thus, Susan has calculated her taxable income by taking into account the slab rate

concept.

B&P (Business and profession tax): This head of income tax is highly related from the

money earned by the individual from the business. By taking into consideration the given case it

can be said that income of £40000 has earned by Susan from the greeting card business in the

accounting year 2015-16. In this, according to the laws and legislation Susan is required to submit

the following documents to HMRC in the form of evidence are:

Financial statements

9

Particulars Amount

Salary 40000

Deduction allowed on the basis of Income tax

Act

9449

Deduction given in accordance with the period 9449

Taxable amount 30551

Income tax due in relation to each employee 6110.2

The above mentioned table presents that taxable income of Susan is £18551 for the financial

year 2015-16. Such amount is related with the money earned by Susan by performing the activities t

supermarket. Further, taxable income of Susan is £30551 which is earned by her from the greeting

card business.

2.3 Completing relevant documentation and tax return for Susan

For filing a return in a suitable manner it is highly required for Susan to fulfil all the

documentary aspects. According to the given case scenario Susan has generated income from

various sources such as job and her own business. In this regard, Susan needs to apply different

provisions for meeting the purpose of proper documentation and tax return.

Salary: The given case situation entails that Susan is working as employee at supermarket

and gets salary such as £28000. In this, Susan is required to assess the taxable income on the basis

of slab rate concept which helps in determine the suitable amount of liability. Further, she is also

required to file the return in a structured format. Besides this, it is also highly required for Susan to

file return with the self attested documents. Along with this, Susan also needs to attach salary

receipt of the each month as proof (Isenbergh, 2009). Hence, by attaching all such documents

individual can ensure HMRC that all the information which is served by her is true and reliable to

the large extent. Thus, Susan has calculated her taxable income by taking into account the slab rate

concept.

B&P (Business and profession tax): This head of income tax is highly related from the

money earned by the individual from the business. By taking into consideration the given case it

can be said that income of £40000 has earned by Susan from the greeting card business in the

accounting year 2015-16. In this, according to the laws and legislation Susan is required to submit

the following documents to HMRC in the form of evidence are:

Financial statements

9

Audit report

Debit and credit note

Inventory report

Other supportive documents

Taxation forms:

1- Form 64-8: It is a significant form which requires involvement of tax practitioner and tax payer.

It is imperative that proper interaction and communication should be done with the financial agents,

tax advisors and accountant. Authorization for individual tax affairs is done under this form and and

it includes partnership, tax credits and trusts. Various types of business taxes are also included under

this method and it comprised of value added tax, corporation tax and PAYE.

2- Form SA102: It is considered as employment form and it has been mandatory for all the

individuals to completely fill this. All employees working on a part-time basis, regular basis and on

contractual basis needs to fill this employment form.

3- Form SA103S: The major purpose with which the form is used is for self- employment purpose.

Various objectives for which the form is used includes business details, allowable and disallowable

income, balance sheet and capital allowances (Kukk and Staehr, 2014). It is also used for

calculating taxable profit and loss CIS deductions and national contributions are also included under

this.

4- Form SA100: It is tax return form which is used by individuals for filing the tax return for

pensions, interest, annuities and capital gains. It is also considered for claiming tax reliefs and

allowances. Student loan repayments are also included under this option and it is mandatory to give

appropriate details under this form for claiming tax relaxations.

5- Form P11D: This form is completed by individuals for defining to HMRC about benefits given

by the employer during a particular tax year. All the information and data are send to the authorities

of HMRC. It is required that employees should record all the benefits given by the employer in an

appropriate manner and details needs to be verified before sending them at HMRC.

TASK 3

3.1 Calculating chargeable profit for the company

10

Debit and credit note

Inventory report

Other supportive documents

Taxation forms:

1- Form 64-8: It is a significant form which requires involvement of tax practitioner and tax payer.

It is imperative that proper interaction and communication should be done with the financial agents,

tax advisors and accountant. Authorization for individual tax affairs is done under this form and and

it includes partnership, tax credits and trusts. Various types of business taxes are also included under

this method and it comprised of value added tax, corporation tax and PAYE.

2- Form SA102: It is considered as employment form and it has been mandatory for all the

individuals to completely fill this. All employees working on a part-time basis, regular basis and on

contractual basis needs to fill this employment form.

3- Form SA103S: The major purpose with which the form is used is for self- employment purpose.

Various objectives for which the form is used includes business details, allowable and disallowable

income, balance sheet and capital allowances (Kukk and Staehr, 2014). It is also used for

calculating taxable profit and loss CIS deductions and national contributions are also included under

this.

4- Form SA100: It is tax return form which is used by individuals for filing the tax return for

pensions, interest, annuities and capital gains. It is also considered for claiming tax reliefs and

allowances. Student loan repayments are also included under this option and it is mandatory to give

appropriate details under this form for claiming tax relaxations.

5- Form P11D: This form is completed by individuals for defining to HMRC about benefits given

by the employer during a particular tax year. All the information and data are send to the authorities

of HMRC. It is required that employees should record all the benefits given by the employer in an

appropriate manner and details needs to be verified before sending them at HMRC.

TASK 3

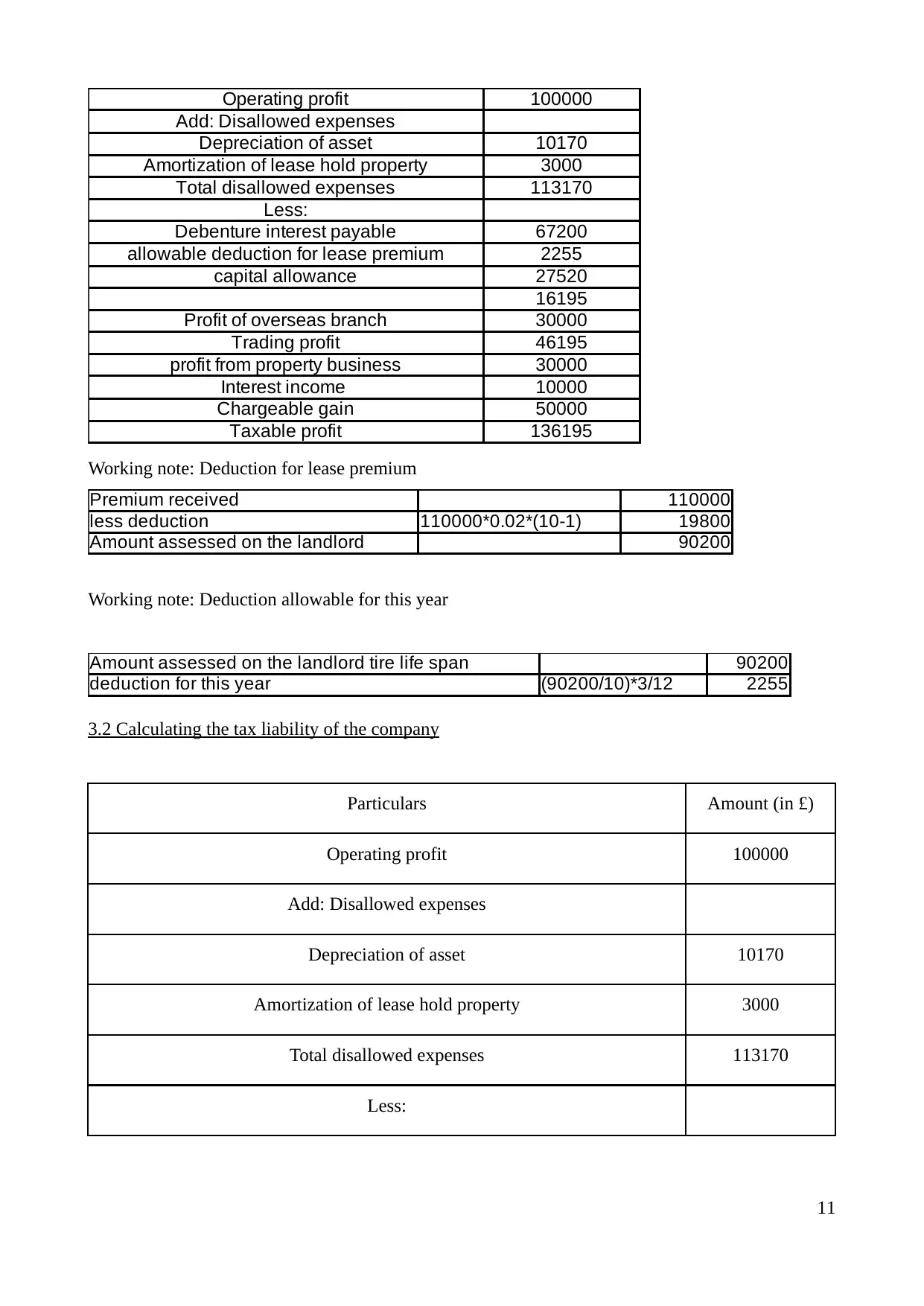

3.1 Calculating chargeable profit for the company

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Operating profit 100000

Add: Disallowed expenses

Depreciation of asset 10170

Amortization of lease hold property 3000

Total disallowed expenses 113170

Less:

Debenture interest payable 67200

allowable deduction for lease premium 2255

capital allowance 27520

16195

Profit of overseas branch 30000

Trading profit 46195

profit from property business 30000

Interest income 10000

Chargeable gain 50000

Taxable profit 136195

Working note: Deduction for lease premium

Premium received 110000

less deduction 110000*0.02*(10-1) 19800

Amount assessed on the landlord 90200

Working note: Deduction allowable for this year

Amount assessed on the landlord tire life span 90200

deduction for this year (90200/10)*3/12 2255

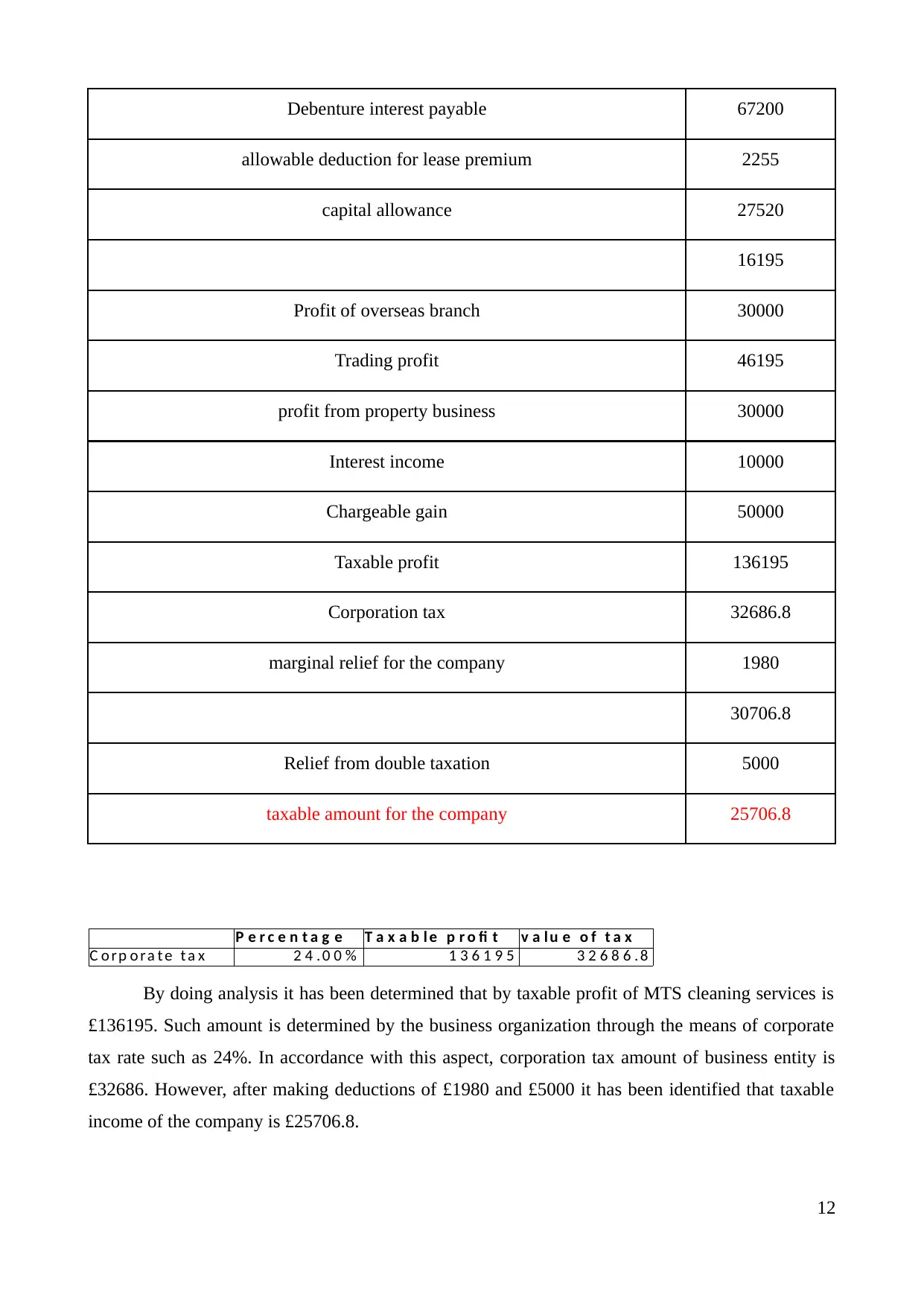

3.2 Calculating the tax liability of the company

Particulars Amount (in £)

Operating profit 100000

Add: Disallowed expenses

Depreciation of asset 10170

Amortization of lease hold property 3000

Total disallowed expenses 113170

Less:

11

Add: Disallowed expenses

Depreciation of asset 10170

Amortization of lease hold property 3000

Total disallowed expenses 113170

Less:

Debenture interest payable 67200

allowable deduction for lease premium 2255

capital allowance 27520

16195

Profit of overseas branch 30000

Trading profit 46195

profit from property business 30000

Interest income 10000

Chargeable gain 50000

Taxable profit 136195

Working note: Deduction for lease premium

Premium received 110000

less deduction 110000*0.02*(10-1) 19800

Amount assessed on the landlord 90200

Working note: Deduction allowable for this year

Amount assessed on the landlord tire life span 90200

deduction for this year (90200/10)*3/12 2255

3.2 Calculating the tax liability of the company

Particulars Amount (in £)

Operating profit 100000

Add: Disallowed expenses

Depreciation of asset 10170

Amortization of lease hold property 3000

Total disallowed expenses 113170

Less:

11

Debenture interest payable 67200

allowable deduction for lease premium 2255

capital allowance 27520

16195

Profit of overseas branch 30000

Trading profit 46195

profit from property business 30000

Interest income 10000

Chargeable gain 50000

Taxable profit 136195

Corporation tax 32686.8

marginal relief for the company 1980

30706.8

Relief from double taxation 5000

taxable amount for the company 25706.8

P e r c e n t a g e T a x a b l e p r o fi t v a l u e o f t a x

C o rp o ra t e t a x 2 4 . 0 0 % 1 3 6 1 9 5 3 2 6 8 6 . 8

By doing analysis it has been determined that by taxable profit of MTS cleaning services is

£136195. Such amount is determined by the business organization through the means of corporate

tax rate such as 24%. In accordance with this aspect, corporation tax amount of business entity is

£32686. However, after making deductions of £1980 and £5000 it has been identified that taxable

income of the company is £25706.8.

12

allowable deduction for lease premium 2255

capital allowance 27520

16195

Profit of overseas branch 30000

Trading profit 46195

profit from property business 30000

Interest income 10000

Chargeable gain 50000

Taxable profit 136195

Corporation tax 32686.8

marginal relief for the company 1980

30706.8

Relief from double taxation 5000

taxable amount for the company 25706.8

P e r c e n t a g e T a x a b l e p r o fi t v a l u e o f t a x

C o rp o ra t e t a x 2 4 . 0 0 % 1 3 6 1 9 5 3 2 6 8 6 . 8

By doing analysis it has been determined that by taxable profit of MTS cleaning services is

£136195. Such amount is determined by the business organization through the means of corporate

tax rate such as 24%. In accordance with this aspect, corporation tax amount of business entity is

£32686. However, after making deductions of £1980 and £5000 it has been identified that taxable

income of the company is £25706.8.

12

3.3 Explaining the ways through which one can deal with the income tax deductions

Income tax Act reveals several deductions which offers relief to the assessee from the tax

obligation. Such reliefs are applied on pension contribution, charity, donation, maintenance

payment etc. According to the laws, individual can claim for getting back the tax amount if donation

comes under the category of Gift Aid Scheme. Further, people who born before 6 April 1938 can

demand for the higher tax allowance (Claim Income Tax reliefs, 2016). Along with this, if employer

offers payroll giving scheme to the personnel then any contribution which is made by the employee

in this fund will free from tax. In addition to this, maintenance payment also reduces the tax liability

of individual to the large extent if such payment is made to an ex-spouse or civil partner. Hence, by

considering all such aspects tax deduction can be enjoyed by the payer or individual.

TASK 4

4.1 Identifying chargeable asset

Capital gain tax is the fourth head of income tax Act which imposes liabilities in front of the

individuals when they make sale of the chargeable asset. For assessing the tax liabilities in relation

to the capital gain aspect Taxation of Chargeable Gains Act (1992) introduced by UK government.

According to this act, when individual gets more than the invested price by selling the assets and

shares then it is considered as capital gain. Besides this, according to CGT Act there are also some

assets which are free from tax liability such as lotteries, prizes, government securities, life insurance

policies, movable properties etc. (Edgerton, 2010). On the other hand, income which is taxable on

the selling of asset include jewellery and ornaments, land, building and fixed assets, shares as well

as bonds etc.

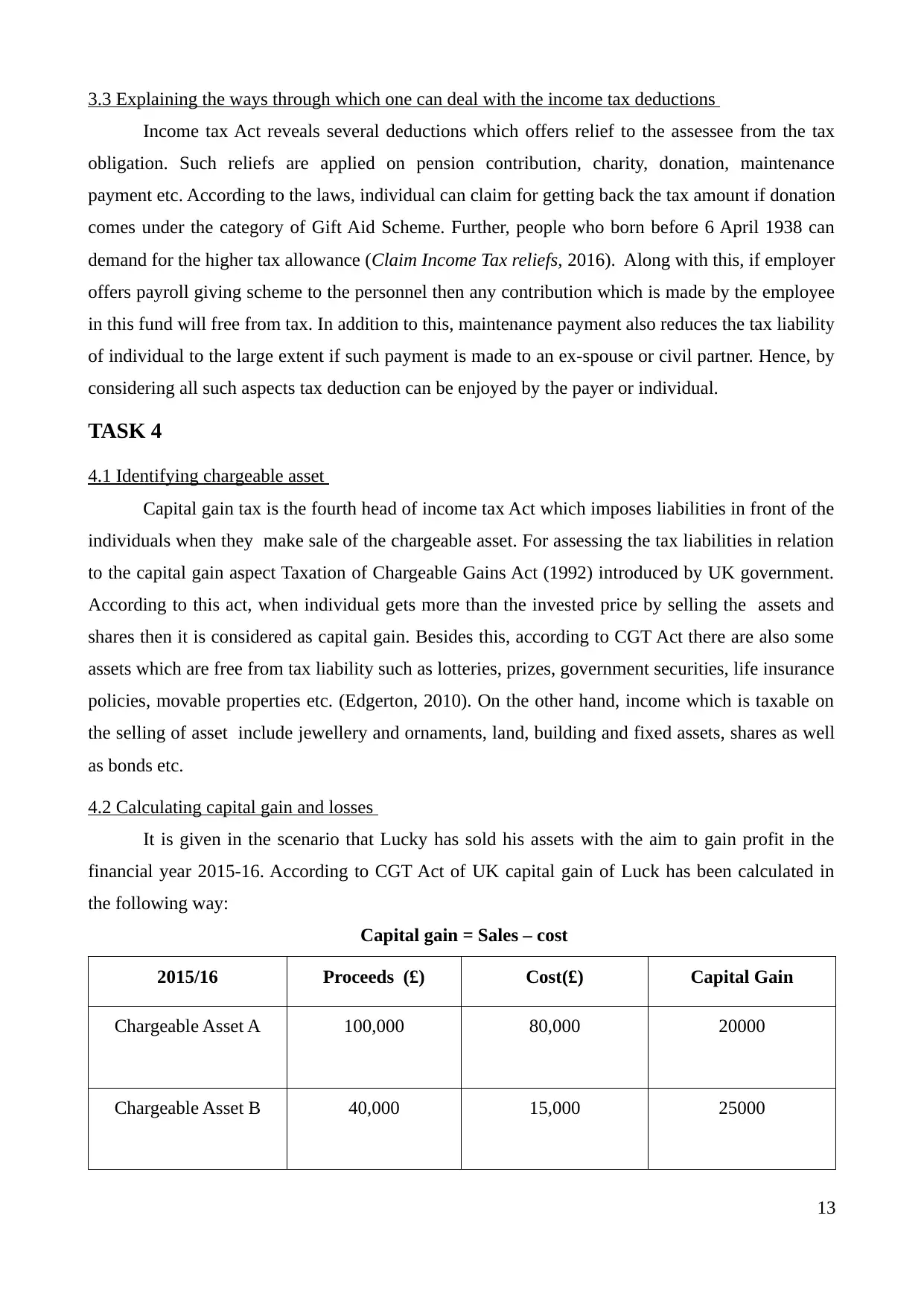

4.2 Calculating capital gain and losses

It is given in the scenario that Lucky has sold his assets with the aim to gain profit in the

financial year 2015-16. According to CGT Act of UK capital gain of Luck has been calculated in

the following way:

Capital gain = Sales – cost

2015/16 Proceeds (£) Cost(£) Capital Gain

Chargeable Asset A 100,000 80,000 20000

Chargeable Asset B 40,000 15,000 25000

13

Income tax Act reveals several deductions which offers relief to the assessee from the tax

obligation. Such reliefs are applied on pension contribution, charity, donation, maintenance

payment etc. According to the laws, individual can claim for getting back the tax amount if donation

comes under the category of Gift Aid Scheme. Further, people who born before 6 April 1938 can

demand for the higher tax allowance (Claim Income Tax reliefs, 2016). Along with this, if employer

offers payroll giving scheme to the personnel then any contribution which is made by the employee

in this fund will free from tax. In addition to this, maintenance payment also reduces the tax liability

of individual to the large extent if such payment is made to an ex-spouse or civil partner. Hence, by

considering all such aspects tax deduction can be enjoyed by the payer or individual.

TASK 4

4.1 Identifying chargeable asset

Capital gain tax is the fourth head of income tax Act which imposes liabilities in front of the

individuals when they make sale of the chargeable asset. For assessing the tax liabilities in relation

to the capital gain aspect Taxation of Chargeable Gains Act (1992) introduced by UK government.

According to this act, when individual gets more than the invested price by selling the assets and

shares then it is considered as capital gain. Besides this, according to CGT Act there are also some

assets which are free from tax liability such as lotteries, prizes, government securities, life insurance

policies, movable properties etc. (Edgerton, 2010). On the other hand, income which is taxable on

the selling of asset include jewellery and ornaments, land, building and fixed assets, shares as well

as bonds etc.

4.2 Calculating capital gain and losses

It is given in the scenario that Lucky has sold his assets with the aim to gain profit in the

financial year 2015-16. According to CGT Act of UK capital gain of Luck has been calculated in

the following way:

Capital gain = Sales – cost

2015/16 Proceeds (£) Cost(£) Capital Gain

Chargeable Asset A 100,000 80,000 20000

Chargeable Asset B 40,000 15,000 25000

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

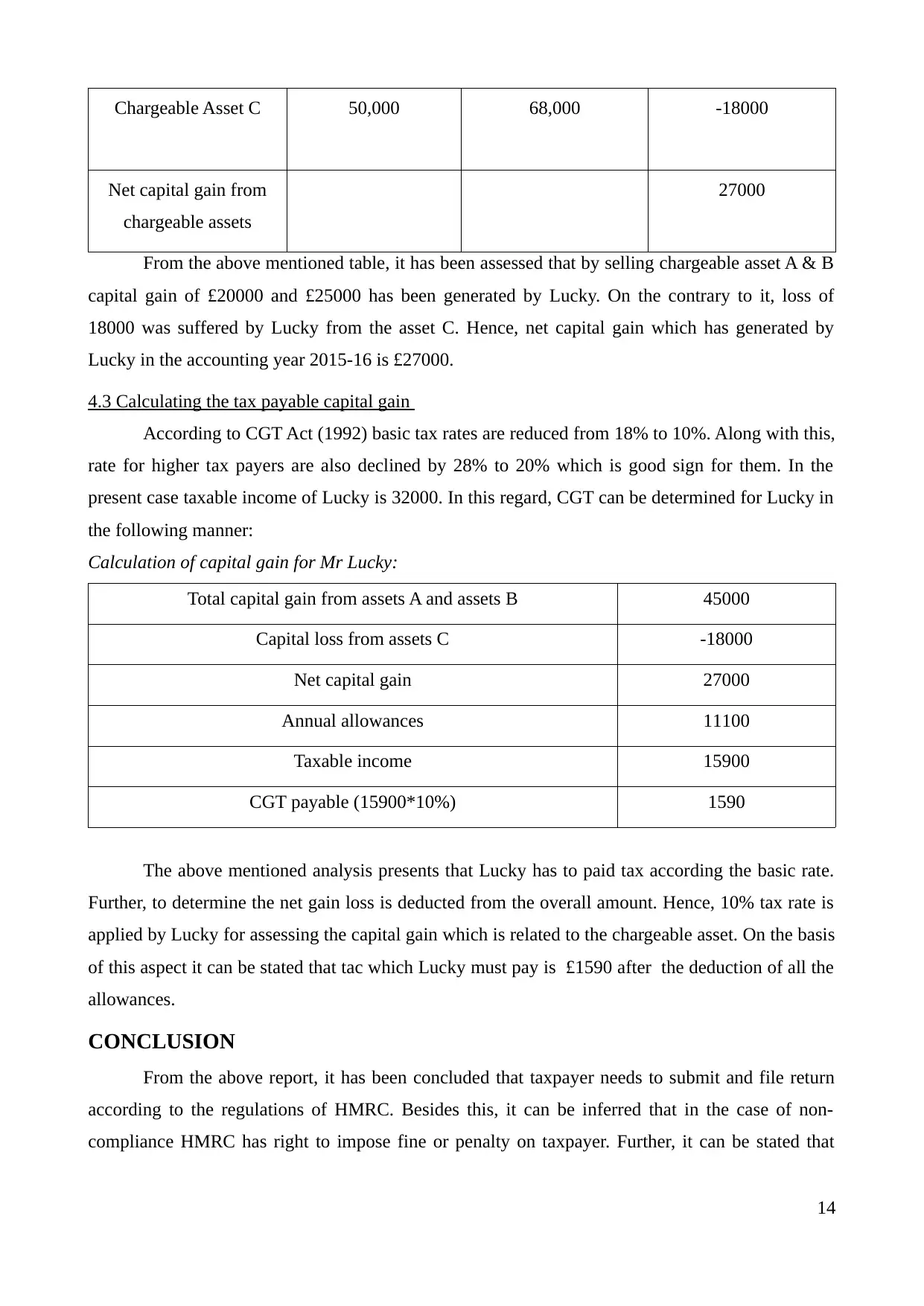

Chargeable Asset C 50,000 68,000 -18000

Net capital gain from

chargeable assets

27000

From the above mentioned table, it has been assessed that by selling chargeable asset A & B

capital gain of £20000 and £25000 has been generated by Lucky. On the contrary to it, loss of

18000 was suffered by Lucky from the asset C. Hence, net capital gain which has generated by

Lucky in the accounting year 2015-16 is £27000.

4.3 Calculating the tax payable capital gain

According to CGT Act (1992) basic tax rates are reduced from 18% to 10%. Along with this,

rate for higher tax payers are also declined by 28% to 20% which is good sign for them. In the

present case taxable income of Lucky is 32000. In this regard, CGT can be determined for Lucky in

the following manner:

Calculation of capital gain for Mr Lucky:

Total capital gain from assets A and assets B 45000

Capital loss from assets C -18000

Net capital gain 27000

Annual allowances 11100

Taxable income 15900

CGT payable (15900*10%) 1590

The above mentioned analysis presents that Lucky has to paid tax according the basic rate.

Further, to determine the net gain loss is deducted from the overall amount. Hence, 10% tax rate is

applied by Lucky for assessing the capital gain which is related to the chargeable asset. On the basis

of this aspect it can be stated that tac which Lucky must pay is £1590 after the deduction of all the

allowances.

CONCLUSION

From the above report, it has been concluded that taxpayer needs to submit and file return

according to the regulations of HMRC. Besides this, it can be inferred that in the case of non-

compliance HMRC has right to impose fine or penalty on taxpayer. Further, it can be stated that

14

Net capital gain from

chargeable assets

27000

From the above mentioned table, it has been assessed that by selling chargeable asset A & B

capital gain of £20000 and £25000 has been generated by Lucky. On the contrary to it, loss of

18000 was suffered by Lucky from the asset C. Hence, net capital gain which has generated by

Lucky in the accounting year 2015-16 is £27000.

4.3 Calculating the tax payable capital gain

According to CGT Act (1992) basic tax rates are reduced from 18% to 10%. Along with this,

rate for higher tax payers are also declined by 28% to 20% which is good sign for them. In the

present case taxable income of Lucky is 32000. In this regard, CGT can be determined for Lucky in

the following manner:

Calculation of capital gain for Mr Lucky:

Total capital gain from assets A and assets B 45000

Capital loss from assets C -18000

Net capital gain 27000

Annual allowances 11100

Taxable income 15900

CGT payable (15900*10%) 1590

The above mentioned analysis presents that Lucky has to paid tax according the basic rate.

Further, to determine the net gain loss is deducted from the overall amount. Hence, 10% tax rate is

applied by Lucky for assessing the capital gain which is related to the chargeable asset. On the basis

of this aspect it can be stated that tac which Lucky must pay is £1590 after the deduction of all the

allowances.

CONCLUSION

From the above report, it has been concluded that taxpayer needs to submit and file return

according to the regulations of HMRC. Besides this, it can be inferred that in the case of non-

compliance HMRC has right to impose fine or penalty on taxpayer. Further, it can be stated that

14

individual can make use of the services of tax practitioner for filing the suitable return in

compliance with HMRC. It also has been articulated that business entity or taxpayer must file the

return in a highly structured format with the proper documentation. In this way, by following all the

tax laws and legislation business unit or individual can determine his liability in the best possible

manner.

15

compliance with HMRC. It also has been articulated that business entity or taxpayer must file the

return in a highly structured format with the proper documentation. In this way, by following all the

tax laws and legislation business unit or individual can determine his liability in the best possible

manner.

15

REFERENCES

Books and Journals

Brewer, M. and et.al, 2013. The Short‐and Medium‐Term Impacts of the Recession on the UK

Income Distribution. Fiscal Studies. 34(2). pp.179-201.

Devereux, M. P., Liu, L. and Loretz, S., 2014. The elasticity of corporate taxable income: New

evidence from UK tax records. American Economic Journal: Economic Policy. 6(2). pp.19-

53.

Edgerton, J., 2010. Investment incentives and corporate tax asymmetries. Journal of Public

Economics. 94(11). pp.936-952.

Freebairn, J. and Quiggin, J., 2010. Special taxation of the mining industry. Economic Papers: A

journal of applied economics and policy. 29(4). pp.384-396.

Isenbergh, J., 2009. International Taxation, 3d (Concepts and Insights Series). West Academic.

Kukk, M. and Staehr, K., 2014. Income underreporting by households with business income:

evidence from Estonia. Post-communist economies. 26(2). pp.257-276.

LaLumia, S., 2008. The effects of joint taxation of married couples on labor supply and non-wage

income. Journal of Public Economics. 92(7). pp.1698-1719.

Lecca, P. and et.al, 2014. Balanced budget multipliers for small open regions within a federal

system: evidence from the Scottish variable rate of income tax. Journal of Regional Science.

54(3). pp.402-421.

Liu, L. and Altshuler, R., 2013. Measuring the burden of the corporate income tax under imperfect

competition. National Tax Journal. 66(1). pp.215-237.

Mertens, K. and Ravn, M. O., 2013. The dynamic effects of personal and corporate income tax

changes in the United States. The American Economic Review. 103(4). pp.1212-1247.

Reforms, U. D. T., Kleven, H. J. and Schultz, E. A., 2014. Estimating taxable income responses

using Danish tax reforms. American Economic Journal: Economic Policy. 6(4). pp.271-301.

Saez, E., Slemrod, J. and Giertz, S. H., 2012. The elasticity of taxable income with respect to

marginal tax rates: A critical review. Journal of economic literature. 50(1). pp.3-50.

Tiley, J. and Loutzenhiser, G., 2012. Revenue Law: Introduction to UK Tax Law; Income Tax;

Capital Gains Tax; Inheritance Tax. Bloomsbury Publishing.

Wang, J., 2013. The OTS Small Business Tax Review: a positive start to simplify the UK tax

system. The Company Lawyer. 34(3). pp.84-91.

Online

Claim Income Tax reliefs. 2016. [Online]. Available through: <https://www.gov.uk/income-tax-

16

Books and Journals

Brewer, M. and et.al, 2013. The Short‐and Medium‐Term Impacts of the Recession on the UK

Income Distribution. Fiscal Studies. 34(2). pp.179-201.

Devereux, M. P., Liu, L. and Loretz, S., 2014. The elasticity of corporate taxable income: New

evidence from UK tax records. American Economic Journal: Economic Policy. 6(2). pp.19-

53.

Edgerton, J., 2010. Investment incentives and corporate tax asymmetries. Journal of Public

Economics. 94(11). pp.936-952.

Freebairn, J. and Quiggin, J., 2010. Special taxation of the mining industry. Economic Papers: A

journal of applied economics and policy. 29(4). pp.384-396.

Isenbergh, J., 2009. International Taxation, 3d (Concepts and Insights Series). West Academic.

Kukk, M. and Staehr, K., 2014. Income underreporting by households with business income:

evidence from Estonia. Post-communist economies. 26(2). pp.257-276.

LaLumia, S., 2008. The effects of joint taxation of married couples on labor supply and non-wage

income. Journal of Public Economics. 92(7). pp.1698-1719.

Lecca, P. and et.al, 2014. Balanced budget multipliers for small open regions within a federal

system: evidence from the Scottish variable rate of income tax. Journal of Regional Science.

54(3). pp.402-421.

Liu, L. and Altshuler, R., 2013. Measuring the burden of the corporate income tax under imperfect

competition. National Tax Journal. 66(1). pp.215-237.

Mertens, K. and Ravn, M. O., 2013. The dynamic effects of personal and corporate income tax

changes in the United States. The American Economic Review. 103(4). pp.1212-1247.

Reforms, U. D. T., Kleven, H. J. and Schultz, E. A., 2014. Estimating taxable income responses

using Danish tax reforms. American Economic Journal: Economic Policy. 6(4). pp.271-301.

Saez, E., Slemrod, J. and Giertz, S. H., 2012. The elasticity of taxable income with respect to

marginal tax rates: A critical review. Journal of economic literature. 50(1). pp.3-50.

Tiley, J. and Loutzenhiser, G., 2012. Revenue Law: Introduction to UK Tax Law; Income Tax;

Capital Gains Tax; Inheritance Tax. Bloomsbury Publishing.

Wang, J., 2013. The OTS Small Business Tax Review: a positive start to simplify the UK tax

system. The Company Lawyer. 34(3). pp.84-91.

Online

Claim Income Tax reliefs. 2016. [Online]. Available through: <https://www.gov.uk/income-tax-

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.