UK Tax System History Assignment

6 Pages1395 Words168 Views

Added on 2019-10-16

UK Tax System History Assignment

Added on 2019-10-16

ShareRelated Documents

Running Head: UK TAX SYSTEM 1TitleAssignment: UK TAX SYSTEM1 | Page

UK TAX SYSTEM2Brief History on UK Tax SystemBefore we discuss the historical background of the UK taxation we can define taxes as acompulsory levy, enforced by the government, on income or expenditure.Income Tax was the first tax in British history to be levied directly on people's earnings. Itwas introduced in 1798 by the then Prime Minister William Pitt the Younger, as atemporary measure to cover the cost of the Napoleonic Wars. Pitt's income tax was leviedfrom 1799 to 1802, the income tax was reintroduced by Addington in 1803 but abolished in1816 & again But it was reintroduced in 1842 by Sir Robert Peel (Freedman and Vella,2017). Corporation tax, Finance Act 1965replaced this structure for companies and associationswith a single corporate tax, which took its basic structure and rules from the income taxsystem. These changes were consolidated by theIncome and Corporation Taxes Act 1970.Also the schedules under which tax is levied have changed (Gov.uk., 2017a). The tax year commences on 6 April and ends on the following 5 April in the UnitedKingdom. Statement of Income Tax liabilities that is filed with theHM Revenue &Customsdeclaring liability fortaxation. SA 100 is for individuals payingIncome Tax &CT600 for corporation (SimpleTax, 2017).Element in Statement of Income Tax Liabilities For Individuals (SA 100)Personal Details b) Income earned in Employment c) Income Earned from Self EmployedBusiness d) Income Earned as partner in Partnership Business e) Capital Gain f) IncomeEarned as trustee g) Foreign Income h) Interest and dividends from UK Banks, Buildingsocieties i) UK Pensions, annuities and other state benefits received j) Tax Reliefs k)Charitable giving l) Information about Student loan repayments (Gov.uk., 2017b).***Other Important Points1.Your Personal Allowance goes down by £1 for every £2 that youradjusted net incomeisabove £100,000. This means your allowance is zero if your income is £123,000 or above.2.There is no tax on saving Interest & Dividend Income.2 | Page

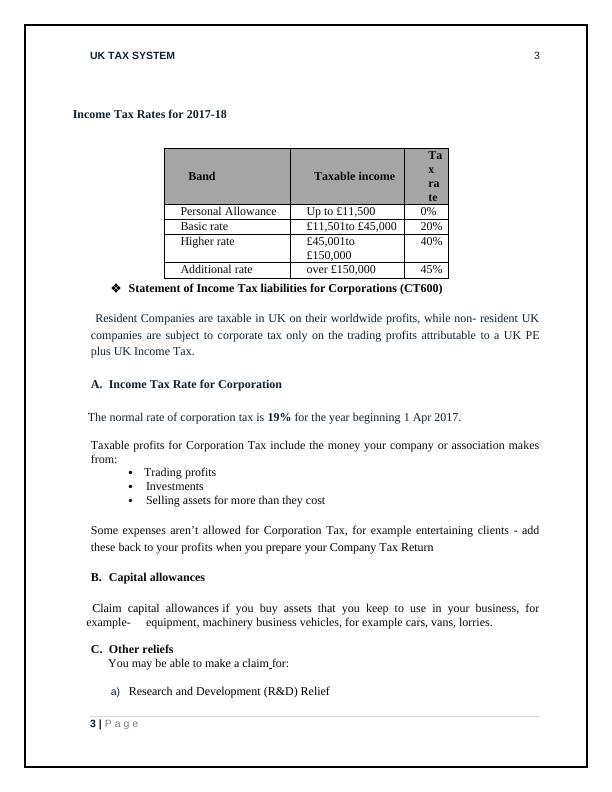

UK TAX SYSTEM3Income Tax Rates for 2017-18Statement of Income Tax liabilities for Corporations (CT600) Resident Companies are taxable in UK on their worldwide profits, while non- resident UKcompanies are subject to corporate tax only on the trading profits attributable to a UK PEplus UK Income Tax. A.Income Tax Rate for Corporation The normal rate of corporation tax is 19% for the year beginning 1 Apr 2017.Taxable profits for Corporation Tax include the money your company or association makesfrom:Trading profits InvestmentsSelling assetsfor more than they costSome expenses aren’t allowed for Corporation Tax, for example entertaining clients - addthese back to your profits when youprepare your Company Tax ReturnB.Capital allowancesClaim capital allowancesif you buy assets that you keep to use in your business, forexample- equipment, machinery business vehicles, for examplecars, vans, lorries.C.Other reliefs You may be able tomake a claimfor:a)Research and Development (R&D) Relief3 | PageBandTaxable incomeTaxratePersonal AllowanceUp to £11,5000%Basic rate£11,501to £45,00020%Higher rate£45,001to£150,00040%Additional rateover £150,00045%

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Brief History on UK Tax System | Assignmentlg...

|6

|1313

|258

Assignment UK Tax System Essaylg...

|4

|1347

|182

Essay on UK Tax System Assignmentlg...

|4

|1409

|134

Assignment on Taxation in UKlg...

|24

|5080

|35

(solved) Taxation Assignment PDFlg...

|10

|2368

|32

The UK Tax System and The Environment - PDFlg...

|19

|4226

|153