Finance Leases: Disclosures, AASB 16 and Journal Entries - Gali Ltd

VerifiedAdded on 2023/04/25

|9

|1498

|110

Report

AI Summary

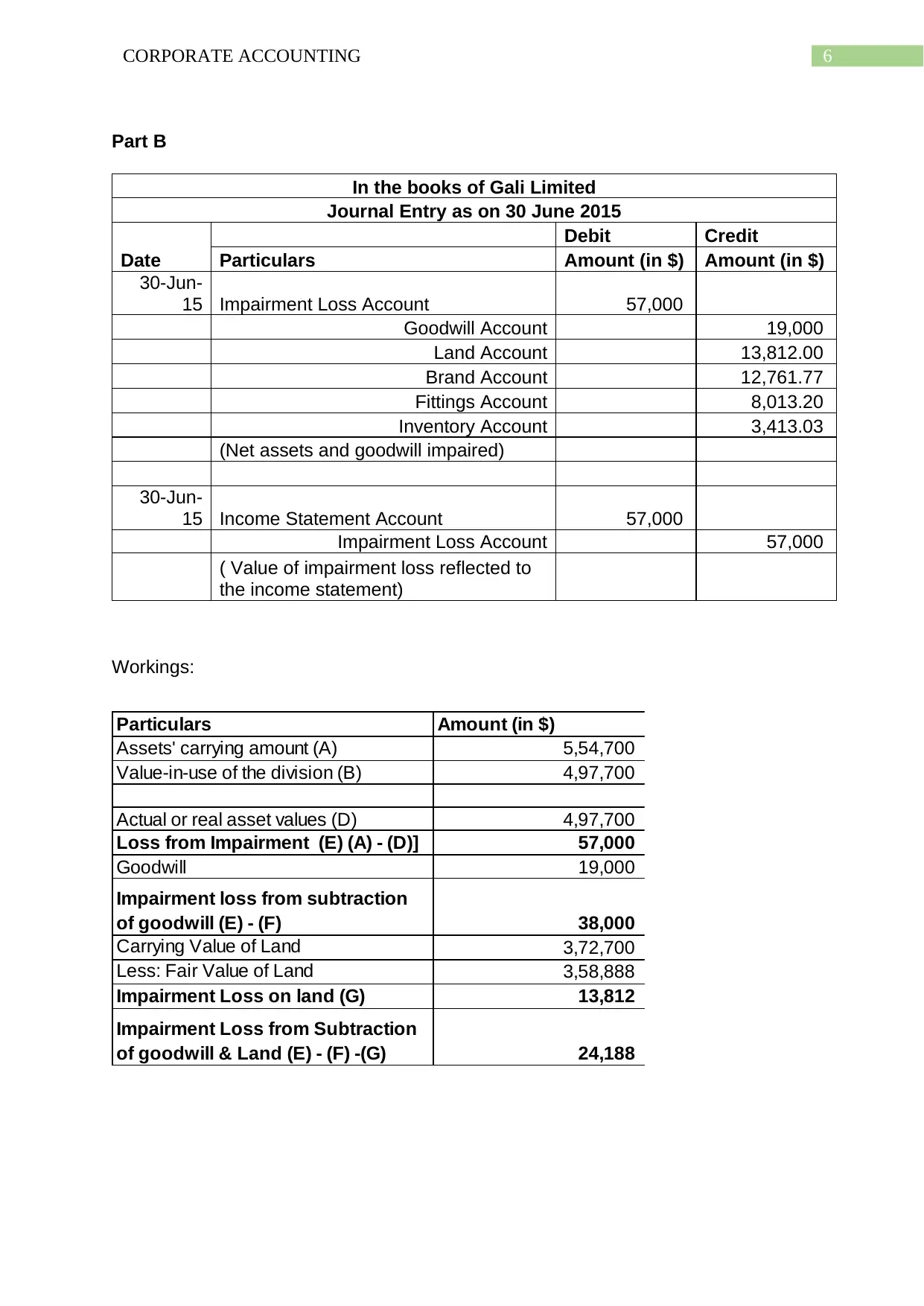

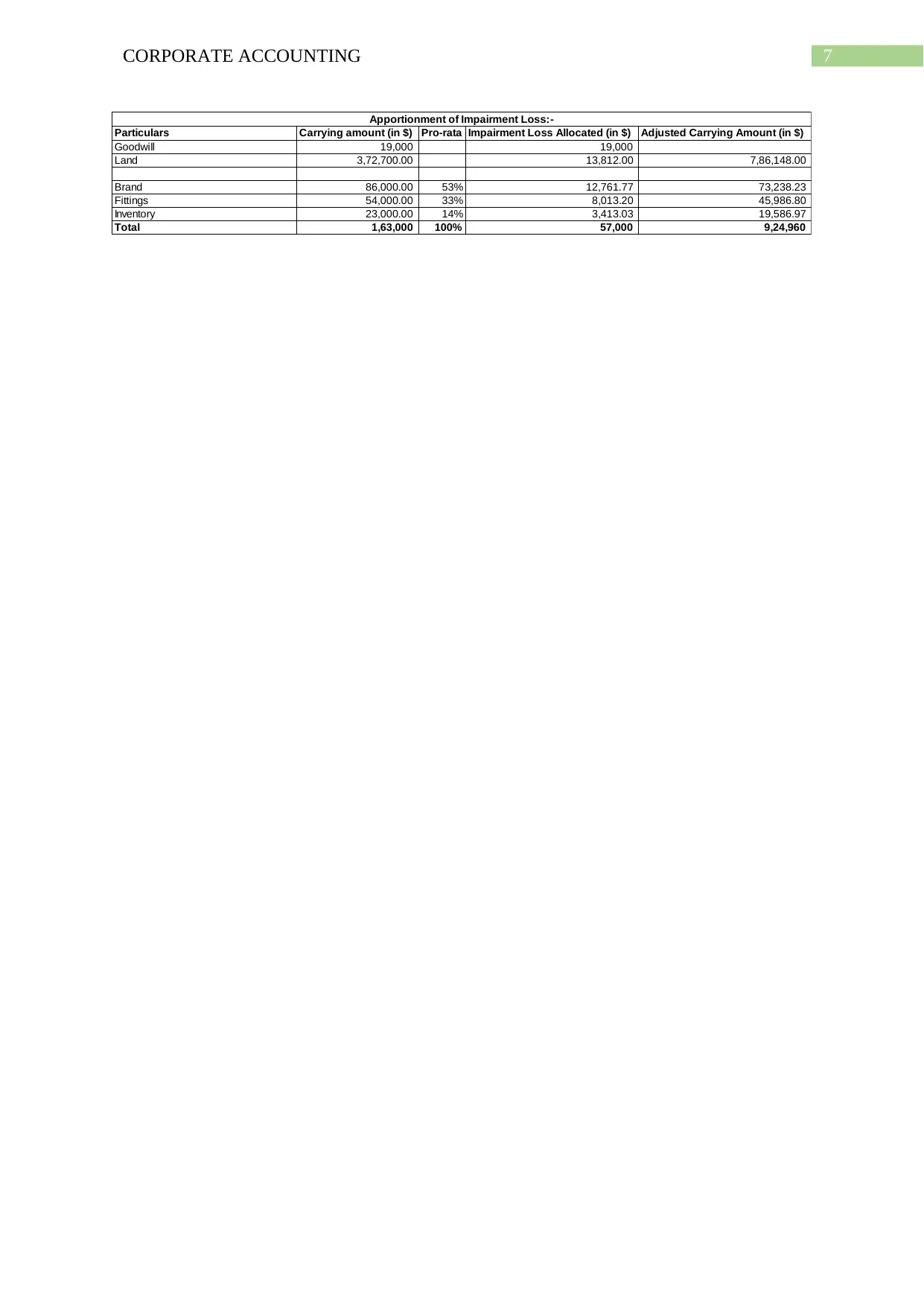

This report provides a comprehensive overview of disclosures for finance leases, referencing AASB 16 standards for lessees and lessors. It details the required disclosures in financial statements, including depreciation, interest expenditure, and lease liabilities. The report further includes a practical application in the form of journal entries for Gali Ltd, demonstrating the accounting treatment for impairment losses and asset revaluations. The analysis covers the calculation of impairment losses on various assets such as goodwill, land, brands, fittings, and inventory, providing a clear understanding of how to record these adjustments in the financial statements.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.