Corporate Finance Report: Sun Pharma

VerifiedAdded on 2020/02/14

|14

|3506

|180

Report

AI Summary

This report provides a comprehensive analysis of Sun Pharma, a leading Indian pharmaceutical company. It evaluates the company's shareholder value, industry position, and investment summary. The core of the report focuses on equity valuation using multiple methods: Discounted Cash Flow (DCF), Price-to-Earnings (PE) ratio, Price-to-Book (PB) ratio, Enterprise Value to EBITDA (EV/EBITDA), and Net Present Value (NPV). Each method's results are detailed, along with a discussion of the assumptions made. The report concludes by recommending the PE ratio as the most suitable valuation method due to its simplicity and market understanding, while acknowledging the limitations of more complex methods. Economic Value Added (EVA) and Total Shareholder Return (TSR) analyses are also included, providing further insights into Sun Pharma's performance. Finally, potential investment risks are identified, such as market fluctuations and economic downturns.

CORPORATE FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Business description...............................................................................................................1

Value to shareholders in recent history..................................................................................2

Industry overview and competitive position..........................................................................2

Investment summary..............................................................................................................3

Valuation including explanation of assumptions...................................................................3

Investment risks......................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................9

INTRODUCTION...........................................................................................................................1

Business description...............................................................................................................1

Value to shareholders in recent history..................................................................................2

Industry overview and competitive position..........................................................................2

Investment summary..............................................................................................................3

Valuation including explanation of assumptions...................................................................3

Investment risks......................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................9

INDEX OF TABLES

Table 1: EVA analysis.....................................................................................................................9

Table 2: TSR analysis......................................................................................................................9

Table 3: Calculation of terminal value............................................................................................9

Table 4: Calculation of enterprise value........................................................................................10

Table 5: Calculation of intrinsic value of share.............................................................................10

Table 6: Ratio analysis...................................................................................................................10

Table 7: Comparison of firms on the basis of PE ratio..................................................................11

Table 8: Comparison of the firms on the basis of PB ratio...........................................................11

Table 9: Calculation of intrinsic value on the basis of EV/EBITDA method...............................12

Table 10: Computation of NPV.....................................................................................................12

Table 1: EVA analysis.....................................................................................................................9

Table 2: TSR analysis......................................................................................................................9

Table 3: Calculation of terminal value............................................................................................9

Table 4: Calculation of enterprise value........................................................................................10

Table 5: Calculation of intrinsic value of share.............................................................................10

Table 6: Ratio analysis...................................................................................................................10

Table 7: Comparison of firms on the basis of PE ratio..................................................................11

Table 8: Comparison of the firms on the basis of PB ratio...........................................................11

Table 9: Calculation of intrinsic value on the basis of EV/EBITDA method...............................12

Table 10: Computation of NPV.....................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Sun pharma is the India largest pharmaceutical company and in order to understand

concept of equity valuation, mentioned firm is taken in the report. In the report, EVA and TSR

analysis is done and their results are explained in detail. Along with this, valuation methods like

DCF, PE, PB, EV/EBITDA and net present value is also mentioned in the report. Out of these

methods best technique is identified for the share price valuation. Apart from this, assumptions

are used for conducting analysis in the report are also mentioned. At the end of the report,

investment risks are pointed out and global and domestic economic environment are considered.

Business description

Sun pharma is a leading pharmaceutical company of India and it is the world fifth largest

generic medicine manufacturer across the globe. Currently, it is operating in several nations and

supplying active pharmaceutical ingredients (API) to many large pharmaceutical corporations all

over the world. Its inception is focused on research & development, developing API and generic

medicine and launching medicines in major therapeutic areas. It also brings large strategic

change in its distribution strategy by following front end model in largest pharmaceutical market

in the world that is USA. Due to this reason, it rapidly grows its business in the mentioned

geographic region. Time to time it is also entering into strategic partnership with the leading

pharmaceutical firms that are headquartered in the USA, UK and Japan. This is the big reason

behind fast growth of the mentioned firm (Chaudhuri, 2005). Currently, it is producing

medicines related to various therapeutic areas like Oncology, respiratory and neurology etc.

Recently, it acquires Ranbaxy which was also giant firm of India. Due to some mistakes in its

operations, USFDA took strict action against the firm. After that, Ranbaxy was continuously

facing a lot of problems. In such a situation, Sun pharma decided to acquire Ranbaxy by

following a merger process. Regarding this, firm has completed all legal formalities and in FY

2015 it completely acquired a giant firm. After acquisition, firm distribution network got

increased and its product portfolio also enhanced (Kamath, 2008). After acquisition of Ranbaxy,

firm became number one company in the generic dermatology space and many projects of

Ranbaxy are in pipeline. Hence, it can be said that in future time period, firm will grow at a rapid

pace across the globe.

1 | P a g e

Sun pharma is the India largest pharmaceutical company and in order to understand

concept of equity valuation, mentioned firm is taken in the report. In the report, EVA and TSR

analysis is done and their results are explained in detail. Along with this, valuation methods like

DCF, PE, PB, EV/EBITDA and net present value is also mentioned in the report. Out of these

methods best technique is identified for the share price valuation. Apart from this, assumptions

are used for conducting analysis in the report are also mentioned. At the end of the report,

investment risks are pointed out and global and domestic economic environment are considered.

Business description

Sun pharma is a leading pharmaceutical company of India and it is the world fifth largest

generic medicine manufacturer across the globe. Currently, it is operating in several nations and

supplying active pharmaceutical ingredients (API) to many large pharmaceutical corporations all

over the world. Its inception is focused on research & development, developing API and generic

medicine and launching medicines in major therapeutic areas. It also brings large strategic

change in its distribution strategy by following front end model in largest pharmaceutical market

in the world that is USA. Due to this reason, it rapidly grows its business in the mentioned

geographic region. Time to time it is also entering into strategic partnership with the leading

pharmaceutical firms that are headquartered in the USA, UK and Japan. This is the big reason

behind fast growth of the mentioned firm (Chaudhuri, 2005). Currently, it is producing

medicines related to various therapeutic areas like Oncology, respiratory and neurology etc.

Recently, it acquires Ranbaxy which was also giant firm of India. Due to some mistakes in its

operations, USFDA took strict action against the firm. After that, Ranbaxy was continuously

facing a lot of problems. In such a situation, Sun pharma decided to acquire Ranbaxy by

following a merger process. Regarding this, firm has completed all legal formalities and in FY

2015 it completely acquired a giant firm. After acquisition, firm distribution network got

increased and its product portfolio also enhanced (Kamath, 2008). After acquisition of Ranbaxy,

firm became number one company in the generic dermatology space and many projects of

Ranbaxy are in pipeline. Hence, it can be said that in future time period, firm will grow at a rapid

pace across the globe.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Value to shareholders in recent history

Shareholder value is the sum of positive and negative impact of all strategic decisions on

the return that they earn on the invested amount. Making wise investment and good return on

investment are the major components of shareholder value. Sun pharma is a large pharmaceutical

company in India and across the globe. Since its inception it pays due attention on increasing its

business at a rapid rate. With the passage of time it also changes its strategy. Since FY 2011, it

gives good return to the shareholders. From FY 2011 to 2015 return percentage is 68.32%, which

is very huge in nature. Firm gives this return in the situation when economic health of the nations

was not well and people lose their confidence on the firm earning capability (Kale, and Little,

2007). During this period, Sun Pharma undertook and completed many projects that were related

to the development of the innovative medicines. It also carries out research projects in

collaboration with other well known pharmaceutical firms. Its main objective was to increase

presence in USA and Europe and in this regard it adopted front end model for distributing its

product. This model to large extent reduces firm dependency on other pharmaceutical firms to

distribute its product in the international market. This helps Sun pharma in running its business

smoothly and in proper manner. Continue approval of generic medicines from USFDA and

increase in demand for the company API in preparation of medicines by foreign companies in

international market increases confidence of investors in the company (Chittoor and et.al, 2009).

This is evident from the higher return percentage. Hence, it can be said that Sun pharma gives

good value to the shareholders.

Industry overview and competitive position

India pharmaceutical industry is one of the largest in the world. In mentioned industry,

there are many large companies like Cipla and Dr Datson etc. Indian companies have good

presence across the globe especially in USA. Preparation of generic medicines is one of the

unique selling prepositions of this industry. In USA, there is high demand for generic medicines

because medical operation cost is already high in the mentioned nation. Moreover, price of

newly developed medicines is already high in USA. Due to this reason, people mostly prefer to

consume generic medicines so as to reduce their treatment cost to some extent (Greene. 2007). In

USA, 80-85% prescriptions are based on generic drugs. Hence, in future also demand for generic

medicines will increase in the world’s largest pharmaceutical market. Other major USP or unique

selling proposition of Indian pharmaceutical industry is API or active pharmaceutical ingredient.

2 | P a g e

Shareholder value is the sum of positive and negative impact of all strategic decisions on

the return that they earn on the invested amount. Making wise investment and good return on

investment are the major components of shareholder value. Sun pharma is a large pharmaceutical

company in India and across the globe. Since its inception it pays due attention on increasing its

business at a rapid rate. With the passage of time it also changes its strategy. Since FY 2011, it

gives good return to the shareholders. From FY 2011 to 2015 return percentage is 68.32%, which

is very huge in nature. Firm gives this return in the situation when economic health of the nations

was not well and people lose their confidence on the firm earning capability (Kale, and Little,

2007). During this period, Sun Pharma undertook and completed many projects that were related

to the development of the innovative medicines. It also carries out research projects in

collaboration with other well known pharmaceutical firms. Its main objective was to increase

presence in USA and Europe and in this regard it adopted front end model for distributing its

product. This model to large extent reduces firm dependency on other pharmaceutical firms to

distribute its product in the international market. This helps Sun pharma in running its business

smoothly and in proper manner. Continue approval of generic medicines from USFDA and

increase in demand for the company API in preparation of medicines by foreign companies in

international market increases confidence of investors in the company (Chittoor and et.al, 2009).

This is evident from the higher return percentage. Hence, it can be said that Sun pharma gives

good value to the shareholders.

Industry overview and competitive position

India pharmaceutical industry is one of the largest in the world. In mentioned industry,

there are many large companies like Cipla and Dr Datson etc. Indian companies have good

presence across the globe especially in USA. Preparation of generic medicines is one of the

unique selling prepositions of this industry. In USA, there is high demand for generic medicines

because medical operation cost is already high in the mentioned nation. Moreover, price of

newly developed medicines is already high in USA. Due to this reason, people mostly prefer to

consume generic medicines so as to reduce their treatment cost to some extent (Greene. 2007). In

USA, 80-85% prescriptions are based on generic drugs. Hence, in future also demand for generic

medicines will increase in the world’s largest pharmaceutical market. Other major USP or unique

selling proposition of Indian pharmaceutical industry is API or active pharmaceutical ingredient.

2 | P a g e

It is a component of the tablet which plays a most important role in treatment of the patient who

is suffering from the specific disease. India is at second rank in API production after China

across the globe. There is a growing demand for API in the world. This is because cost of

preparing medicines API is very high in the large pharmaceutical markets like USA and Europe.

Due to this reason, companies that are headquartered in these continents are importing API from

countries like India and China. Indian companies are supplying API to companies like

Glaxosmitkline. This indicates that cost of API is small and quality of same supplied by the

Indian companies is of excellent quality (Chittoor and Ray, 2007). Thus, it can be said that

Indian pharmaceutical industry is highly competitive and companies operating in this industry

are giving stiff competition to the companies of USA and Europe etc.

Investment summary

In order to make investment in any company it is necessary to understand the same. By

creating a broad understanding it can be determined whether investment will be profitable or

unprofitable. In this report, Sun pharma is taken for valuation of equity. On the basis of valuation

of equity it can be determined that whether firm share is valued at its fair price in the stock

exchange. In this regard, techniques like discounted cash flow method and EV/EBITDA

technique is used in the report. But every time for earning profit an investor cannot entirely rely

of valuation of the company shares (Bhaumik, Driffield and Pal, 2010). With the change in time

shares gives profit or loss to an investor. If investment on 100 shares of the company is made

then it will be valued at 48,465 in the FY 2011. In FY 2015, the value of these 100 shares was

81,575. This clearly indicates that investment gives huge profit to the investor and even market

fluctuate sharply and investor gets a higher return on the invested amount.

Valuation including explanation of assumptions

In the report, valuation of the company shares is done by using several techniques. These

techniques are PE, PB, EV/EBITDA, DCF and net present value method. The results of these

techniques are explained below. PE ratio- This ratio indicates that firm share price is overvalued or undervalued in the

stock exchange. If firm PE ratio is below industry PE ratio then it is assumed that firm

share is undervalued and recommendation for investment is made (Hodder, Hopkins and

Wahlen, 2006). On other hand, if vice verse happen then it is assumed that share price is

overvalued and recommendation for investment is not made in this case by the

3 | P a g e

is suffering from the specific disease. India is at second rank in API production after China

across the globe. There is a growing demand for API in the world. This is because cost of

preparing medicines API is very high in the large pharmaceutical markets like USA and Europe.

Due to this reason, companies that are headquartered in these continents are importing API from

countries like India and China. Indian companies are supplying API to companies like

Glaxosmitkline. This indicates that cost of API is small and quality of same supplied by the

Indian companies is of excellent quality (Chittoor and Ray, 2007). Thus, it can be said that

Indian pharmaceutical industry is highly competitive and companies operating in this industry

are giving stiff competition to the companies of USA and Europe etc.

Investment summary

In order to make investment in any company it is necessary to understand the same. By

creating a broad understanding it can be determined whether investment will be profitable or

unprofitable. In this report, Sun pharma is taken for valuation of equity. On the basis of valuation

of equity it can be determined that whether firm share is valued at its fair price in the stock

exchange. In this regard, techniques like discounted cash flow method and EV/EBITDA

technique is used in the report. But every time for earning profit an investor cannot entirely rely

of valuation of the company shares (Bhaumik, Driffield and Pal, 2010). With the change in time

shares gives profit or loss to an investor. If investment on 100 shares of the company is made

then it will be valued at 48,465 in the FY 2011. In FY 2015, the value of these 100 shares was

81,575. This clearly indicates that investment gives huge profit to the investor and even market

fluctuate sharply and investor gets a higher return on the invested amount.

Valuation including explanation of assumptions

In the report, valuation of the company shares is done by using several techniques. These

techniques are PE, PB, EV/EBITDA, DCF and net present value method. The results of these

techniques are explained below. PE ratio- This ratio indicates that firm share price is overvalued or undervalued in the

stock exchange. If firm PE ratio is below industry PE ratio then it is assumed that firm

share is undervalued and recommendation for investment is made (Hodder, Hopkins and

Wahlen, 2006). On other hand, if vice verse happen then it is assumed that share price is

overvalued and recommendation for investment is not made in this case by the

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investment experts. PE ratio of the Sun pharma is below and on this basis it can be said

that firm shares valuation is proper. If we compare Sun pharma with other companies on

the basis of this ratio then it can be said that firm share is positively valued and at low PE

ratio. Thus, there is a high probability of growth in the firm share value in future. Hence,

it will be profitable to make investment in the company equity share. PB ratio- In this technique, valuation is done by comparing share value with the book

value of per share. By comparing with the same ratio of the other firms operating in the

industry it can be accessed whether firm shares are overvalued or undervalued (Roehling

and et.al, 2005). On comparison of value of ratio of Sun pharma with other companies it

can be seen that shares are overvalued so, on the basis of this technique it can be said that

investors must abstain from making investment in the firm. EV/EBITDA- In this ratio, enterprise value is calculated and divided by the EBITDA in

order to identify fair value the shares (EV/EBITDA ratio. 2016). By doing calculation, it

is identified that real value of the company share is 2332. Current share price is below

these values and this reflects that share price is undervalued and there is very high

probability of increase in the share price. DCF or discounted cash flow technique- In this method, share price is calculated by

using discounted cash flows. By using forecasting methodology, firm revenue is

projected and cost of the firm to earn that revenue is also computed (Fernández, 2007).

On the basis of this technique, fair value of per share is 1170. This is nearby the company

share price to some extent. Hence, it can be said that this technique is producing good

results. Net present value- In this method it is identified whether firm is earning profit on capital

expenditures (Net present value. 2013). For this, CAPEX for each year is computed and

future investment value if forecasted. NPV is positive and this reflects that firm is earning

good return on investment. Due to this reason, it can be said that investment in the firm

will be profitable for the investor.

Which technique is best?

PE ratio is best for the firm in comparison to other techniques. This is because market

players only understand pricing patterns and other large investor investing behavior. They have

deep knowledge of PE ratio. People do not understand DCF technique EV/EBITDA valuation

4 | P a g e

that firm shares valuation is proper. If we compare Sun pharma with other companies on

the basis of this ratio then it can be said that firm share is positively valued and at low PE

ratio. Thus, there is a high probability of growth in the firm share value in future. Hence,

it will be profitable to make investment in the company equity share. PB ratio- In this technique, valuation is done by comparing share value with the book

value of per share. By comparing with the same ratio of the other firms operating in the

industry it can be accessed whether firm shares are overvalued or undervalued (Roehling

and et.al, 2005). On comparison of value of ratio of Sun pharma with other companies it

can be seen that shares are overvalued so, on the basis of this technique it can be said that

investors must abstain from making investment in the firm. EV/EBITDA- In this ratio, enterprise value is calculated and divided by the EBITDA in

order to identify fair value the shares (EV/EBITDA ratio. 2016). By doing calculation, it

is identified that real value of the company share is 2332. Current share price is below

these values and this reflects that share price is undervalued and there is very high

probability of increase in the share price. DCF or discounted cash flow technique- In this method, share price is calculated by

using discounted cash flows. By using forecasting methodology, firm revenue is

projected and cost of the firm to earn that revenue is also computed (Fernández, 2007).

On the basis of this technique, fair value of per share is 1170. This is nearby the company

share price to some extent. Hence, it can be said that this technique is producing good

results. Net present value- In this method it is identified whether firm is earning profit on capital

expenditures (Net present value. 2013). For this, CAPEX for each year is computed and

future investment value if forecasted. NPV is positive and this reflects that firm is earning

good return on investment. Due to this reason, it can be said that investment in the firm

will be profitable for the investor.

Which technique is best?

PE ratio is best for the firm in comparison to other techniques. This is because market

players only understand pricing patterns and other large investor investing behavior. They have

deep knowledge of PE ratio. People do not understand DCF technique EV/EBITDA valuation

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

techniques for making investment decisions. PE ratio concept is also related to the price pattern

or technical analysis. Concept of PE ratio is simple and by comparing firm’s earning to shares

price is easily identified that company shares are fairly priced or not. This technique fairly valued

share price in comparison to other complicated techniques. DCF technique requires preparation

of assumptions and they may prove wrong in the future. Due to these reasons PE ratio is

considered better than other techniques.

Assumptions

In order to compute cost of equity, market returns are assumed by considering specific

time period of economic condition of India and relevant stock exchange performances.

Tax rate is assumed constant at 15%.

In past years, cost as a percentage of revenue does no change sharply. So, cost as a

percentage of revenue is taken same from FY 2016-2020 with reference to earlier year

cost percentages. Every year, revenue growth rate is increasing and on the basis of acquisition of Ranbaxy

in FY 2015 it is assumed that revenue will grow at a rapid rate. On the basis of hope of

approval from USFDA on several generic medicines whose production is in pipeline it is

assumed that revenue will increase at a rapid rate.

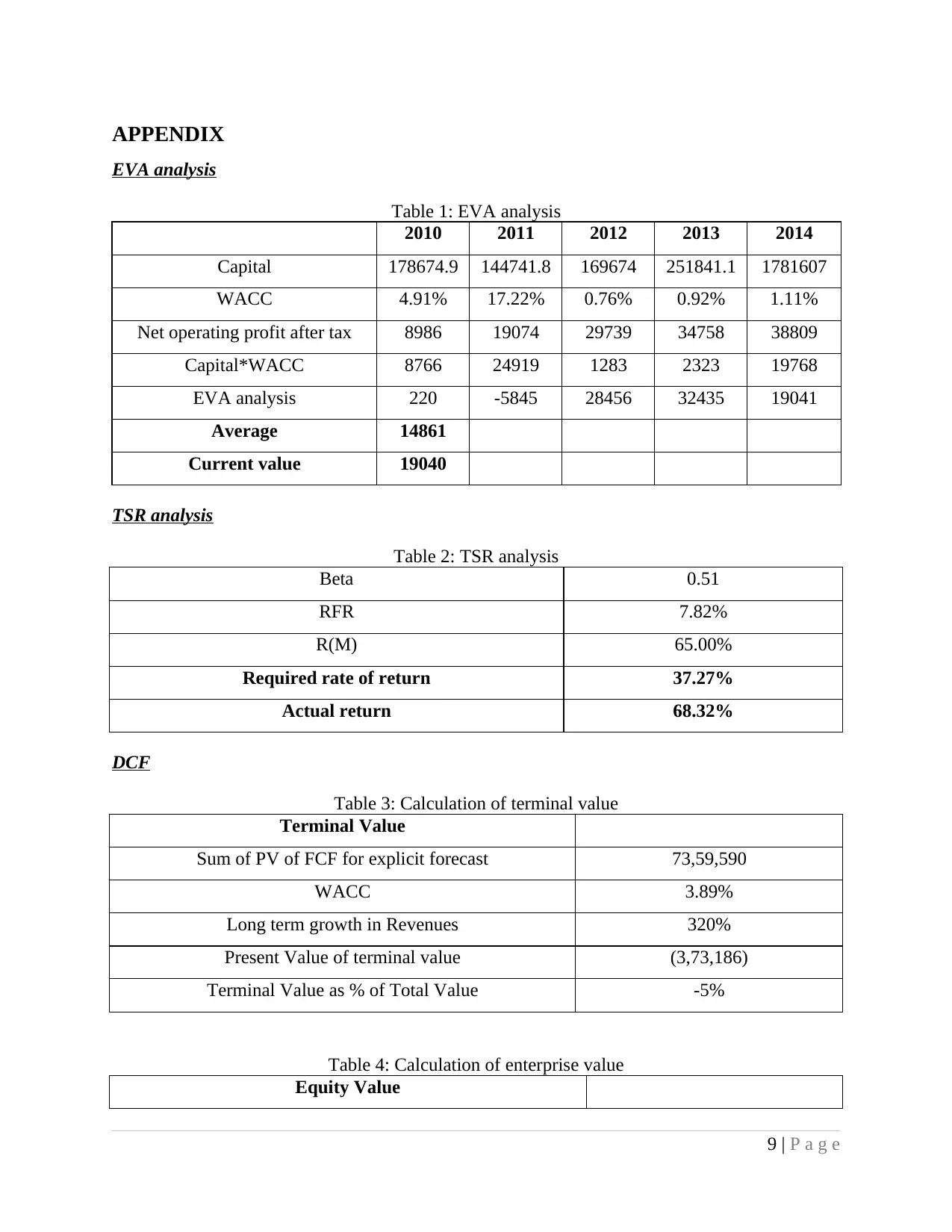

EVA and TSR analysis

Economic value added technique shows that Sun pharma EVA is above the average

EVA. Hence, it can be said that firm is giving elegant performance on this front. On other hand

TSR technique is also used in the report and it is identified that in last five years Sun pharma

shares gives return above the minimum return that investors must earn on the investment. Hence,

it can be said that investors earn good return on the Sun pharma shares.

Investment risks

Following are the investment risks.

If market becomes bearish then share price of Sun pharma will also fall. Hence,

investment needs to be made with full caution.

Frequent change in currency and interest rates in negative direction may lead to fall in

share price (Yang and Blyth, 2007).

5 | P a g e

or technical analysis. Concept of PE ratio is simple and by comparing firm’s earning to shares

price is easily identified that company shares are fairly priced or not. This technique fairly valued

share price in comparison to other complicated techniques. DCF technique requires preparation

of assumptions and they may prove wrong in the future. Due to these reasons PE ratio is

considered better than other techniques.

Assumptions

In order to compute cost of equity, market returns are assumed by considering specific

time period of economic condition of India and relevant stock exchange performances.

Tax rate is assumed constant at 15%.

In past years, cost as a percentage of revenue does no change sharply. So, cost as a

percentage of revenue is taken same from FY 2016-2020 with reference to earlier year

cost percentages. Every year, revenue growth rate is increasing and on the basis of acquisition of Ranbaxy

in FY 2015 it is assumed that revenue will grow at a rapid rate. On the basis of hope of

approval from USFDA on several generic medicines whose production is in pipeline it is

assumed that revenue will increase at a rapid rate.

EVA and TSR analysis

Economic value added technique shows that Sun pharma EVA is above the average

EVA. Hence, it can be said that firm is giving elegant performance on this front. On other hand

TSR technique is also used in the report and it is identified that in last five years Sun pharma

shares gives return above the minimum return that investors must earn on the investment. Hence,

it can be said that investors earn good return on the Sun pharma shares.

Investment risks

Following are the investment risks.

If market becomes bearish then share price of Sun pharma will also fall. Hence,

investment needs to be made with full caution.

Frequent change in currency and interest rates in negative direction may lead to fall in

share price (Yang and Blyth, 2007).

5 | P a g e

Downturn in China will negatively affect the global economy and pressure on economic

data of India can be observed. Thus, if this happens then share price of Sun pharma may

fall in future.

CONCLUSION

On the basis of above discussion it is concluded that there are many techniques of

valuation. But investor cannot use all techniques in order to make its investment decisions.

Hence, investors must abstain from using complicated methods for equity valuation. In DCF

techniques, assumptions are made and these may prove incorrect in the future. Hence, if

investment decisions are taken on the basis of this technique then investor may bear loss on the

investment. Hence, it is concluded that investors must use simple methods for equity valuation.

6 | P a g e

data of India can be observed. Thus, if this happens then share price of Sun pharma may

fall in future.

CONCLUSION

On the basis of above discussion it is concluded that there are many techniques of

valuation. But investor cannot use all techniques in order to make its investment decisions.

Hence, investors must abstain from using complicated methods for equity valuation. In DCF

techniques, assumptions are made and these may prove incorrect in the future. Hence, if

investment decisions are taken on the basis of this technique then investor may bear loss on the

investment. Hence, it is concluded that investors must use simple methods for equity valuation.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books & journals

Bhaumik, S.K., Driffield, N. and Pal, S., 2010. Does ownership structure of emerging-market

firms affect their outward FDI? The case of the Indian automotive and

pharmaceutical sectors. Journal of International Business Studies. 41(3). pp.437-450.

Chaudhuri, S., 2005. The WTO and India's pharmaceuticals industry: Patent protection, TRIPS,

and developing countries. New Delhi: Oxford University Press.

Chittoor, R. and Ray, S., 2007. Internationalization paths of Indian pharmaceutical firms—A

strategic group analysis. Journal of International Management. 13(3). pp.338-355.

Chittoor, R., et.al., 2009. Third-world copycats to emerging multinationals: Institutional changes

and organizational transformation in the Indian pharmaceutical industry. Organization

Science, 20(1). pp.187-205.

Fernández, P., 2007. Valuing companies by cash flow discounting: ten methods and nine

theories. Managerial Finance, 33(11), pp.853-876.

Greene, W., 2007. The emergence of India's pharmaceutical industry and implications for the

US generic drug market. US International Trade Commission, Office of Economics.

Hodder, L.D., Hopkins, P.E. and Wahlen, J.M., 2006. Risk-relevance of fair-value income

measures for commercial banks. The Accounting Review, 81(2), pp.337-375.

Kale, D. and Little, S., 2007. From imitation to innovation: The evolution of R&D capabilities

and learning processes in the Indian pharmaceutical industry. Technology Analysis &

Strategic Management. 19(5). pp.589-609.

Kamath, G., 2008. Intellectual capital and corporate performance in Indian pharmaceutical

industry. Journal of Intellectual Capital. 9(4). pp.684-704.

Roehling, M.V., et.al., 2005. The future of HR management: Research needs and directions.

Human Resource Management, 44(2), pp.207-216.

Yang, M. and Blyth, W., 2007. Modeling investment risks and uncertainties with real options

approach. International Energy Agency.

Online

EV/EBITDA ratio, 2016. [Online]. Available through: <

http://www.readyratios.com/reference/market/ev_ebitda_ratio.html>. [Accessed on 6th

January 2016].

7 | P a g e

Books & journals

Bhaumik, S.K., Driffield, N. and Pal, S., 2010. Does ownership structure of emerging-market

firms affect their outward FDI? The case of the Indian automotive and

pharmaceutical sectors. Journal of International Business Studies. 41(3). pp.437-450.

Chaudhuri, S., 2005. The WTO and India's pharmaceuticals industry: Patent protection, TRIPS,

and developing countries. New Delhi: Oxford University Press.

Chittoor, R. and Ray, S., 2007. Internationalization paths of Indian pharmaceutical firms—A

strategic group analysis. Journal of International Management. 13(3). pp.338-355.

Chittoor, R., et.al., 2009. Third-world copycats to emerging multinationals: Institutional changes

and organizational transformation in the Indian pharmaceutical industry. Organization

Science, 20(1). pp.187-205.

Fernández, P., 2007. Valuing companies by cash flow discounting: ten methods and nine

theories. Managerial Finance, 33(11), pp.853-876.

Greene, W., 2007. The emergence of India's pharmaceutical industry and implications for the

US generic drug market. US International Trade Commission, Office of Economics.

Hodder, L.D., Hopkins, P.E. and Wahlen, J.M., 2006. Risk-relevance of fair-value income

measures for commercial banks. The Accounting Review, 81(2), pp.337-375.

Kale, D. and Little, S., 2007. From imitation to innovation: The evolution of R&D capabilities

and learning processes in the Indian pharmaceutical industry. Technology Analysis &

Strategic Management. 19(5). pp.589-609.

Kamath, G., 2008. Intellectual capital and corporate performance in Indian pharmaceutical

industry. Journal of Intellectual Capital. 9(4). pp.684-704.

Roehling, M.V., et.al., 2005. The future of HR management: Research needs and directions.

Human Resource Management, 44(2), pp.207-216.

Yang, M. and Blyth, W., 2007. Modeling investment risks and uncertainties with real options

approach. International Energy Agency.

Online

EV/EBITDA ratio, 2016. [Online]. Available through: <

http://www.readyratios.com/reference/market/ev_ebitda_ratio.html>. [Accessed on 6th

January 2016].

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net present value, 2013. [Online], Available through: <

http://accountingexplained.com/managerial/capital-budgeting/npv>. [Accessed on 6th

January 2016].

8 | P a g e

http://accountingexplained.com/managerial/capital-budgeting/npv>. [Accessed on 6th

January 2016].

8 | P a g e

APPENDIX

EVA analysis

Table 1: EVA analysis

2010 2011 2012 2013 2014

Capital 178674.9 144741.8 169674 251841.1 1781607

WACC 4.91% 17.22% 0.76% 0.92% 1.11%

Net operating profit after tax 8986 19074 29739 34758 38809

Capital*WACC 8766 24919 1283 2323 19768

EVA analysis 220 -5845 28456 32435 19041

Average 14861

Current value 19040

TSR analysis

Table 2: TSR analysis

Beta 0.51

RFR 7.82%

R(M) 65.00%

Required rate of return 37.27%

Actual return 68.32%

DCF

Table 3: Calculation of terminal value

Terminal Value

Sum of PV of FCF for explicit forecast 73,59,590

WACC 3.89%

Long term growth in Revenues 320%

Present Value of terminal value (3,73,186)

Terminal Value as % of Total Value -5%

Table 4: Calculation of enterprise value

Equity Value

9 | P a g e

EVA analysis

Table 1: EVA analysis

2010 2011 2012 2013 2014

Capital 178674.9 144741.8 169674 251841.1 1781607

WACC 4.91% 17.22% 0.76% 0.92% 1.11%

Net operating profit after tax 8986 19074 29739 34758 38809

Capital*WACC 8766 24919 1283 2323 19768

EVA analysis 220 -5845 28456 32435 19041

Average 14861

Current value 19040

TSR analysis

Table 2: TSR analysis

Beta 0.51

RFR 7.82%

R(M) 65.00%

Required rate of return 37.27%

Actual return 68.32%

DCF

Table 3: Calculation of terminal value

Terminal Value

Sum of PV of FCF for explicit forecast 73,59,590

WACC 3.89%

Long term growth in Revenues 320%

Present Value of terminal value (3,73,186)

Terminal Value as % of Total Value -5%

Table 4: Calculation of enterprise value

Equity Value

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14