Volatility Index (VIX): Construction, Importance, and Risk Management

VerifiedAdded on 2023/06/11

|21

|5556

|426

Report

AI Summary

This report provides a comprehensive analysis of the Volatility Index (VIX), beginning with its definition and construction, detailing the calculation steps involved in determining the VIX value. It highlights the VIX's importance for financial markets, noting its inverse relationship with market trends and its utility in interpreting market danger points. The report further explores how VIX and related products can be used for risk management, emphasizing strategies like reactive approaches, adjustments and allocations, scaling exposure, diversification, and maintaining a future perspective. It also discusses exchange-traded products linked to VIX and short volatility strategies, including how they generate returns and the associated risks, such as skewed risk-reward payoffs and opposite sentiments. The report concludes by outlining methods for managing these risks, including stock buy-sell derivative multi-strategies and fundamental analysis, making it a valuable resource for understanding and navigating the complexities of volatility trading. Desklib offers a wealth of resources for students seeking similar solved assignments and past papers.

Running Head: UNDERSTANDING THE VIX 0

Understanding the VIX

Understanding the VIX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UNDERSTANDING THE VIX 1

Table of Contents

Part 1..........................................................................................................................................3

Definition................................................................................................................................3

Construction of the VIX.........................................................................................................3

Calculation of the VIX...........................................................................................................4

Step1...................................................................................................................................5

Step 2..................................................................................................................................6

Importance of the VIX for financial markets.........................................................................6

Part 2..........................................................................................................................................7

Reactive rather than predictive...........................................................................................8

Adjustments and allocations...............................................................................................8

Scaling Exposure................................................................................................................8

Variety and diversification..................................................................................................8

Maintaining a future perspective........................................................................................9

Part 3..........................................................................................................................................9

Exchange traded products linked to VIX...............................................................................9

Part 4........................................................................................................................................11

Short volatility Strategies.....................................................................................................11

How are they used to create the returns for the investors?...................................................12

Short selling......................................................................................................................12

Stock buy sell derivative multi strategy............................................................................13

Movements in stock..........................................................................................................13

Risks.........................................................................................................................................14

Skewed risk and reward Payoff........................................................................................14

Opposite sentiments..........................................................................................................14

Fundamental analysis........................................................................................................14

Government or economic reform strategies changes........................................................15

Table of Contents

Part 1..........................................................................................................................................3

Definition................................................................................................................................3

Construction of the VIX.........................................................................................................3

Calculation of the VIX...........................................................................................................4

Step1...................................................................................................................................5

Step 2..................................................................................................................................6

Importance of the VIX for financial markets.........................................................................6

Part 2..........................................................................................................................................7

Reactive rather than predictive...........................................................................................8

Adjustments and allocations...............................................................................................8

Scaling Exposure................................................................................................................8

Variety and diversification..................................................................................................8

Maintaining a future perspective........................................................................................9

Part 3..........................................................................................................................................9

Exchange traded products linked to VIX...............................................................................9

Part 4........................................................................................................................................11

Short volatility Strategies.....................................................................................................11

How are they used to create the returns for the investors?...................................................12

Short selling......................................................................................................................12

Stock buy sell derivative multi strategy............................................................................13

Movements in stock..........................................................................................................13

Risks.........................................................................................................................................14

Skewed risk and reward Payoff........................................................................................14

Opposite sentiments..........................................................................................................14

Fundamental analysis........................................................................................................14

Government or economic reform strategies changes........................................................15

UNDERSTANDING THE VIX 2

How these risks are managed...................................................................................................15

References................................................................................................................................17

How these risks are managed...................................................................................................15

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UNDERSTANDING THE VIX 3

Part 1

Definition

According to the Franklin D. Roosevelt “the only thing we have to fear is fear itself”. The

volatility Index or VIX, is an index created by the Chicago board operations in the year 1993

by the professor of the duke university Robert F. Whaley to provide the benchmark of the

short term volatility. According to the CBOE the estimated volatility of the S/P 500 index is

measured by VIX for a cumulative period of the 30 day at the money OEX option. These

include hedge funds, professional managers with bundle of the money, and the individuals

that make investments which seeks to profit from the volatility of the market. VIX is an

implied volatility in the parlance of the industry of the securities. It is equally similar to the

bonds which provide the yield at the time of the maturity. The VIX is often referred to as the

“investor fear gauge” (Whaley, 2000). Generally when the stock prices are falling and

investors are having a fear the volatility and the index move up accordingly. Like a bond a

stock option has a model for its valuation and also the number of parameters are engaged

which are to be estimated with high level of accuracy. To find out the implied volatility the

market price of the index option is equated with model value. This implied volatility is

therefore the best benchmark of the expected volatility of the underlying stock over the

remaining life of the option. Since VIX is based on S&P 100 index option prices, VIX

represents a market consensus of the S&P 100 with expected volatility.

Construction of the VIX

When the transactions of the stock option began in the year 1973, Chicago Board Options

Exchange has made sure that the market volatility index can be constructed by the option

price which can reflect the expectation of the future. Since the initiation many methodologies

were proposed by different scholars. Then and there Whaley proposed a simple approach

which typically deals with the evolution of the market volatility index and making the same

Part 1

Definition

According to the Franklin D. Roosevelt “the only thing we have to fear is fear itself”. The

volatility Index or VIX, is an index created by the Chicago board operations in the year 1993

by the professor of the duke university Robert F. Whaley to provide the benchmark of the

short term volatility. According to the CBOE the estimated volatility of the S/P 500 index is

measured by VIX for a cumulative period of the 30 day at the money OEX option. These

include hedge funds, professional managers with bundle of the money, and the individuals

that make investments which seeks to profit from the volatility of the market. VIX is an

implied volatility in the parlance of the industry of the securities. It is equally similar to the

bonds which provide the yield at the time of the maturity. The VIX is often referred to as the

“investor fear gauge” (Whaley, 2000). Generally when the stock prices are falling and

investors are having a fear the volatility and the index move up accordingly. Like a bond a

stock option has a model for its valuation and also the number of parameters are engaged

which are to be estimated with high level of accuracy. To find out the implied volatility the

market price of the index option is equated with model value. This implied volatility is

therefore the best benchmark of the expected volatility of the underlying stock over the

remaining life of the option. Since VIX is based on S&P 100 index option prices, VIX

represents a market consensus of the S&P 100 with expected volatility.

Construction of the VIX

When the transactions of the stock option began in the year 1973, Chicago Board Options

Exchange has made sure that the market volatility index can be constructed by the option

price which can reflect the expectation of the future. Since the initiation many methodologies

were proposed by different scholars. Then and there Whaley proposed a simple approach

which typically deals with the evolution of the market volatility index and making the same

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UNDERSTANDING THE VIX 4

as the measure of the future stock market price. In the similar year, the Chicago Board Option

Exchange started to figure out the development of the CBOE volatility index also commonly

known as VIX. The VIX is based on the implied volatility of the S&P 100 index options.

After the ten years of its inception the VIX was accepted by the stock market. From thereafter

many indexes are calculated by the CBOE including the NASDAQ 100 index, in 2003 VIX

based on S&P 500 index, which is much nearer to the actual stock value. CBOE Russell

2000, CBOE DJIA volatility index and RVX in India the VIX came into existence in April

2008 by national stock exchange and is based on Nifty 50 index option prices (Stanton,

2011).

Calculation of the VIX

The original index was based on the option prices of S&P 100 index rather than the S&P 500

index. At the time, OEX options were widely traded options in the United States which was

covering about the 75% of the total volume of the index option in the year 1992 whereas in

case of the SPX option it was having a coverage of 16.1% of the volume. The implied

volatility index of the VIX is based on the prices from a deep and active index option

(Whaley, 2009).

The second feature of the original VIX was that only eight money index calls and puts. This

seems to be reasonable because of the option series available at the time and the money

options were traded actively. On the other hand the options which were having less exercise

prices were not traded that actively. Such quotations if have been included in the calculation

of the VIX it have reduced the timeliness and the accuracy. Since its evolution a change has

been observed fundamentally.

Normally there is a formula for VIX calculation given by CBOE to derive at the volatility.

Under this the average is calculated on the basis of the money puts and calls. A put is an

option contract which gives right to the owners to see the underlying asset at a specific price

as the measure of the future stock market price. In the similar year, the Chicago Board Option

Exchange started to figure out the development of the CBOE volatility index also commonly

known as VIX. The VIX is based on the implied volatility of the S&P 100 index options.

After the ten years of its inception the VIX was accepted by the stock market. From thereafter

many indexes are calculated by the CBOE including the NASDAQ 100 index, in 2003 VIX

based on S&P 500 index, which is much nearer to the actual stock value. CBOE Russell

2000, CBOE DJIA volatility index and RVX in India the VIX came into existence in April

2008 by national stock exchange and is based on Nifty 50 index option prices (Stanton,

2011).

Calculation of the VIX

The original index was based on the option prices of S&P 100 index rather than the S&P 500

index. At the time, OEX options were widely traded options in the United States which was

covering about the 75% of the total volume of the index option in the year 1992 whereas in

case of the SPX option it was having a coverage of 16.1% of the volume. The implied

volatility index of the VIX is based on the prices from a deep and active index option

(Whaley, 2009).

The second feature of the original VIX was that only eight money index calls and puts. This

seems to be reasonable because of the option series available at the time and the money

options were traded actively. On the other hand the options which were having less exercise

prices were not traded that actively. Such quotations if have been included in the calculation

of the VIX it have reduced the timeliness and the accuracy. Since its evolution a change has

been observed fundamentally.

Normally there is a formula for VIX calculation given by CBOE to derive at the volatility.

Under this the average is calculated on the basis of the money puts and calls. A put is an

option contract which gives right to the owners to see the underlying asset at a specific price

UNDERSTANDING THE VIX 5

and a specific time. There is a belief in the mind of the buyer that the price will fall below the

exercise price before the expiry date. On the other hand the call is an option contract which

gives the right to the owners, but not the entire obligation to purchase a particular amount of

the asset at a specified price within a specified time. A call auction can also be referred to as

the call market (Whaley, 2013).

There are following steps to calculate the VIX index calculation

Step1

The money calls from the SPX and money puts form the SPX are cumulatively centred

together at the strike price of the money, determined by the K0. Only those options are

included in the calculation of the VIX index calculation which is of non-zero nature. Here the

important note that is to be taken care of or shall be considered is that as the volatility

escalates and falls down there is an expansion of the non-zero bids tends to expand and

contract eventually. Therefore the frequency of the variation is high as the number of options

may vary either on monthly, daily or minute to minute basis. Henceforth, the right selection is

important (Cboe volatility index, 2018).

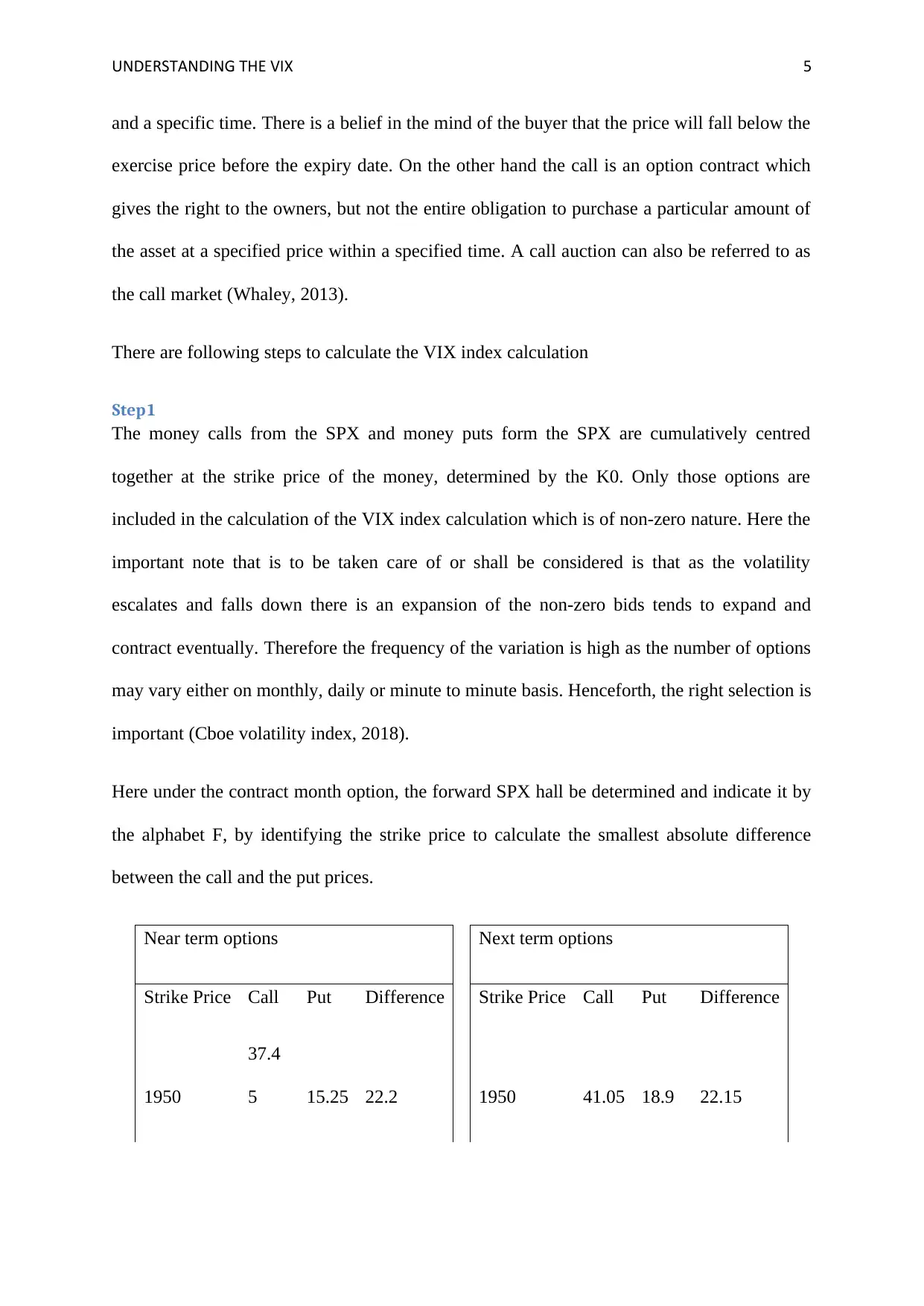

Here under the contract month option, the forward SPX hall be determined and indicate it by

the alphabet F, by identifying the strike price to calculate the smallest absolute difference

between the call and the put prices.

Near term options Next term options

Strike Price Call Put Difference Strike Price Call Put Difference

1950

37.4

5 15.25 22.2 1950 41.05 18.9 22.15

and a specific time. There is a belief in the mind of the buyer that the price will fall below the

exercise price before the expiry date. On the other hand the call is an option contract which

gives the right to the owners, but not the entire obligation to purchase a particular amount of

the asset at a specified price within a specified time. A call auction can also be referred to as

the call market (Whaley, 2013).

There are following steps to calculate the VIX index calculation

Step1

The money calls from the SPX and money puts form the SPX are cumulatively centred

together at the strike price of the money, determined by the K0. Only those options are

included in the calculation of the VIX index calculation which is of non-zero nature. Here the

important note that is to be taken care of or shall be considered is that as the volatility

escalates and falls down there is an expansion of the non-zero bids tends to expand and

contract eventually. Therefore the frequency of the variation is high as the number of options

may vary either on monthly, daily or minute to minute basis. Henceforth, the right selection is

important (Cboe volatility index, 2018).

Here under the contract month option, the forward SPX hall be determined and indicate it by

the alphabet F, by identifying the strike price to calculate the smallest absolute difference

between the call and the put prices.

Near term options Next term options

Strike Price Call Put Difference Strike Price Call Put Difference

1950

37.4

5 15.25 22.2 1950 41.05 18.9 22.15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UNDERSTANDING THE VIX 6

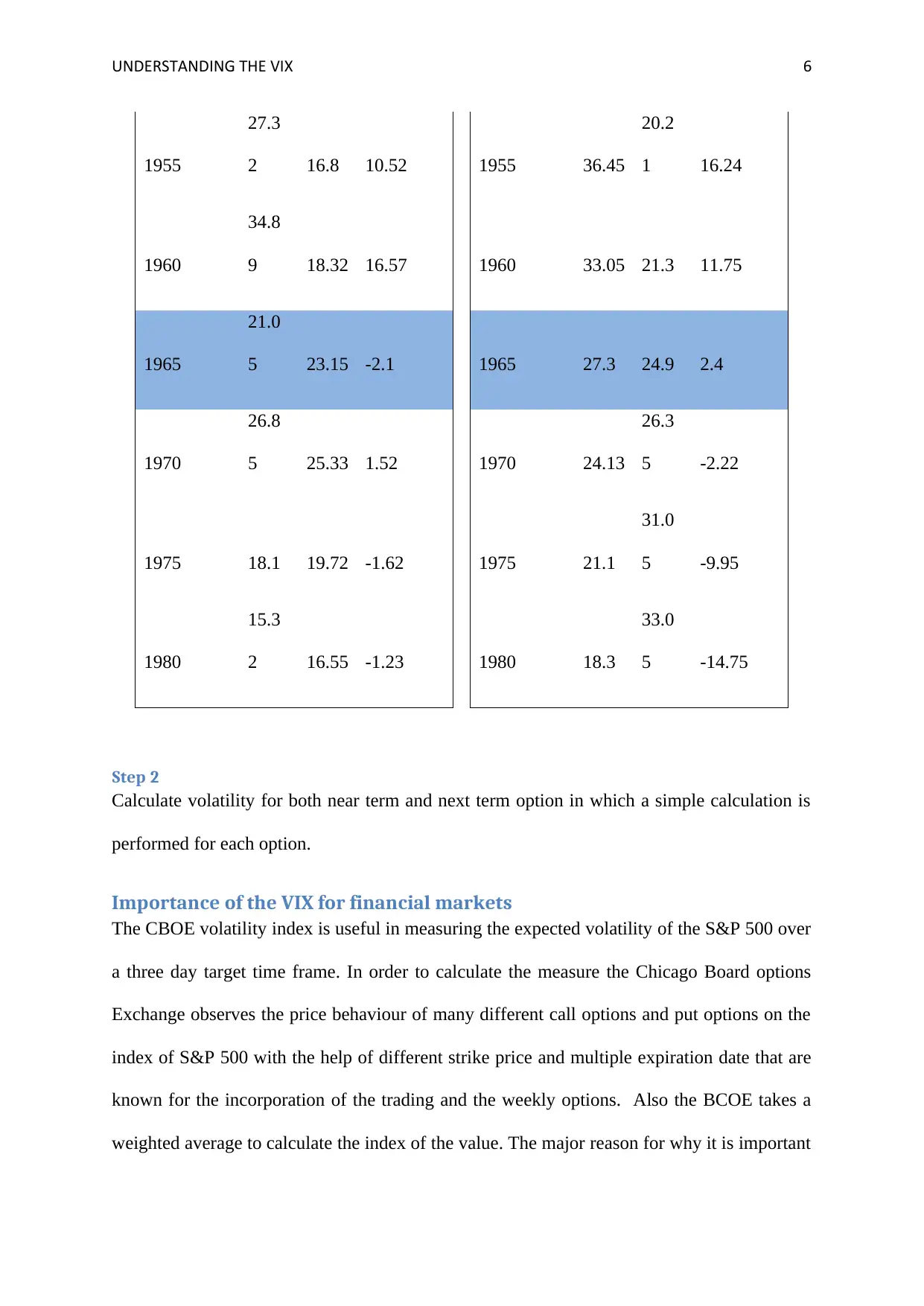

1955

27.3

2 16.8 10.52 1955 36.45

20.2

1 16.24

1960

34.8

9 18.32 16.57 1960 33.05 21.3 11.75

1965

21.0

5 23.15 -2.1 1965 27.3 24.9 2.4

1970

26.8

5 25.33 1.52 1970 24.13

26.3

5 -2.22

1975 18.1 19.72 -1.62 1975 21.1

31.0

5 -9.95

1980

15.3

2 16.55 -1.23 1980 18.3

33.0

5 -14.75

Step 2

Calculate volatility for both near term and next term option in which a simple calculation is

performed for each option.

Importance of the VIX for financial markets

The CBOE volatility index is useful in measuring the expected volatility of the S&P 500 over

a three day target time frame. In order to calculate the measure the Chicago Board options

Exchange observes the price behaviour of many different call options and put options on the

index of S&P 500 with the help of different strike price and multiple expiration date that are

known for the incorporation of the trading and the weekly options. Also the BCOE takes a

weighted average to calculate the index of the value. The major reason for why it is important

1955

27.3

2 16.8 10.52 1955 36.45

20.2

1 16.24

1960

34.8

9 18.32 16.57 1960 33.05 21.3 11.75

1965

21.0

5 23.15 -2.1 1965 27.3 24.9 2.4

1970

26.8

5 25.33 1.52 1970 24.13

26.3

5 -2.22

1975 18.1 19.72 -1.62 1975 21.1

31.0

5 -9.95

1980

15.3

2 16.55 -1.23 1980 18.3

33.0

5 -14.75

Step 2

Calculate volatility for both near term and next term option in which a simple calculation is

performed for each option.

Importance of the VIX for financial markets

The CBOE volatility index is useful in measuring the expected volatility of the S&P 500 over

a three day target time frame. In order to calculate the measure the Chicago Board options

Exchange observes the price behaviour of many different call options and put options on the

index of S&P 500 with the help of different strike price and multiple expiration date that are

known for the incorporation of the trading and the weekly options. Also the BCOE takes a

weighted average to calculate the index of the value. The major reason for why it is important

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UNDERSTANDING THE VIX 7

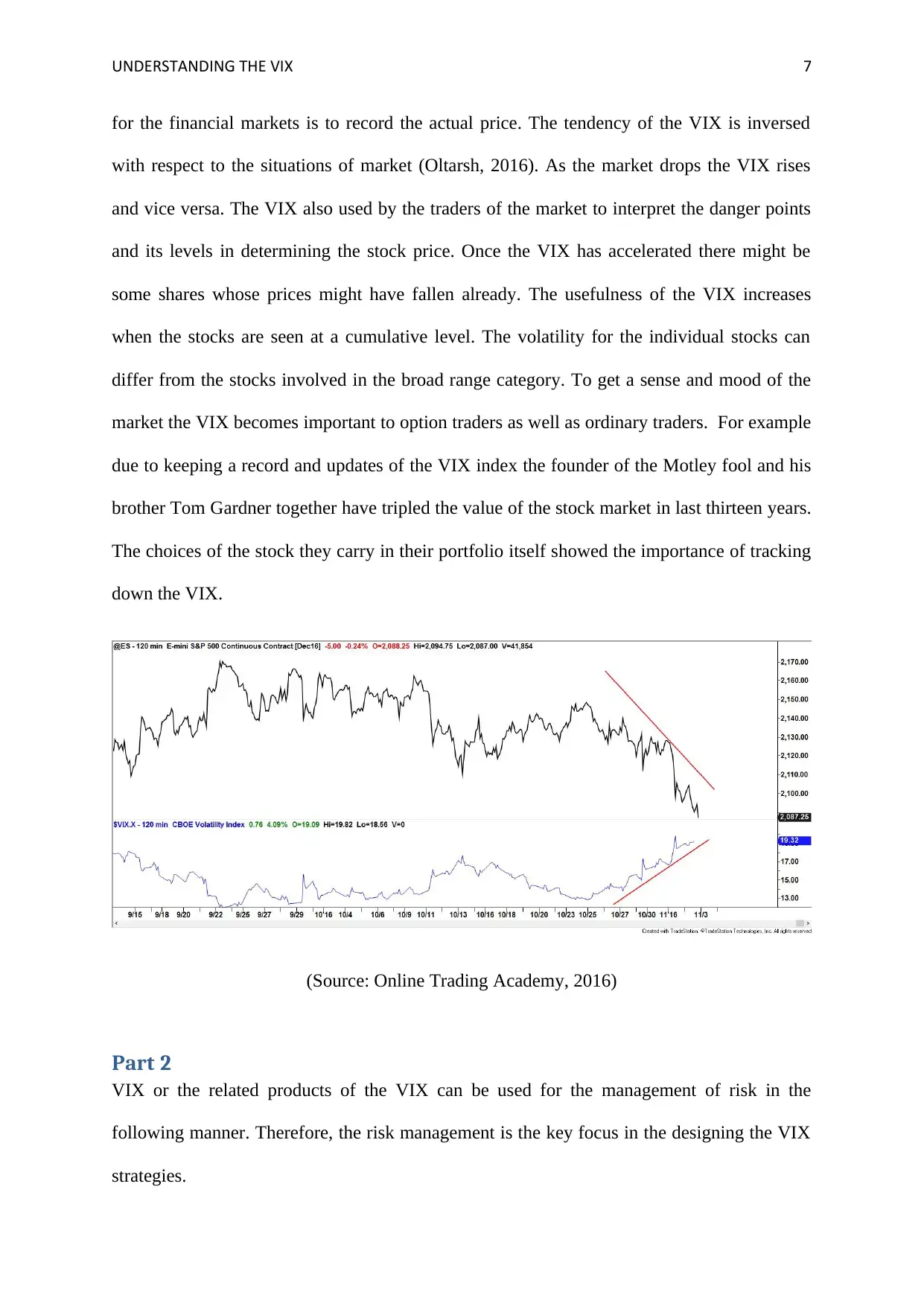

for the financial markets is to record the actual price. The tendency of the VIX is inversed

with respect to the situations of market (Oltarsh, 2016). As the market drops the VIX rises

and vice versa. The VIX also used by the traders of the market to interpret the danger points

and its levels in determining the stock price. Once the VIX has accelerated there might be

some shares whose prices might have fallen already. The usefulness of the VIX increases

when the stocks are seen at a cumulative level. The volatility for the individual stocks can

differ from the stocks involved in the broad range category. To get a sense and mood of the

market the VIX becomes important to option traders as well as ordinary traders. For example

due to keeping a record and updates of the VIX index the founder of the Motley fool and his

brother Tom Gardner together have tripled the value of the stock market in last thirteen years.

The choices of the stock they carry in their portfolio itself showed the importance of tracking

down the VIX.

(Source: Online Trading Academy, 2016)

Part 2

VIX or the related products of the VIX can be used for the management of risk in the

following manner. Therefore, the risk management is the key focus in the designing the VIX

strategies.

for the financial markets is to record the actual price. The tendency of the VIX is inversed

with respect to the situations of market (Oltarsh, 2016). As the market drops the VIX rises

and vice versa. The VIX also used by the traders of the market to interpret the danger points

and its levels in determining the stock price. Once the VIX has accelerated there might be

some shares whose prices might have fallen already. The usefulness of the VIX increases

when the stocks are seen at a cumulative level. The volatility for the individual stocks can

differ from the stocks involved in the broad range category. To get a sense and mood of the

market the VIX becomes important to option traders as well as ordinary traders. For example

due to keeping a record and updates of the VIX index the founder of the Motley fool and his

brother Tom Gardner together have tripled the value of the stock market in last thirteen years.

The choices of the stock they carry in their portfolio itself showed the importance of tracking

down the VIX.

(Source: Online Trading Academy, 2016)

Part 2

VIX or the related products of the VIX can be used for the management of risk in the

following manner. Therefore, the risk management is the key focus in the designing the VIX

strategies.

UNDERSTANDING THE VIX 8

Most of the strategies seek to harvest the volatility-risk-premium in the VIX futures which

ultimately provides the long term edge. At times, the VRP may vary and can be positive,

negative, or neutral. The performance is generally determined by the direction of the VRP

which provides some clues and hints. This way the volatility risk premiums is in the favour of

the investor and it can be used it mitigate the risk by keeping a track through the use of the

directions. The positions can be adjusted by determining the relationships between the VRP,

VIX futures, Spot VIX and the volatility of the S&P 500 to eliminate the risk and gain the

potential advantage in the long run (Anson and Ho, 2003).

Reactive rather than predictive

No one can predict the future, and it becomes cumbersome when the investors play the puzzle

to understand the direction of the volatility and usually risky one. Instead of trying to predict

the movements of the volatile nature and it is advised to take a reactive approach in which the

investors are supposed to react according to the volatility of the stock. A response can be

observed with regard to the changes in the VRP and this way it can help in minimising the

risk (Bhansali and Harris, 2018).

Adjustments and allocations

Conventionally a simple scaling in/out strategy is greatly outperforming the XIV drawdown

buy approach. This scaling strategy is not advisable for the investors who are thinking to

make the movement in the investments over the night. Therefore, one way to reduce the risk

is to stop the overnight exposures as it literally increases the trading costs and fails to capture

any favourable movements overnight (Lee, Liao and Tung, 2017).

Scaling Exposure

The volatility risk premium is important and equally valid in case of the size of the strategy

volatility exposure. If the VRP is large and if it seems to be in the favour of the investor, the

investor with the help of such strategy can increase the exposure and when the premium

Most of the strategies seek to harvest the volatility-risk-premium in the VIX futures which

ultimately provides the long term edge. At times, the VRP may vary and can be positive,

negative, or neutral. The performance is generally determined by the direction of the VRP

which provides some clues and hints. This way the volatility risk premiums is in the favour of

the investor and it can be used it mitigate the risk by keeping a track through the use of the

directions. The positions can be adjusted by determining the relationships between the VRP,

VIX futures, Spot VIX and the volatility of the S&P 500 to eliminate the risk and gain the

potential advantage in the long run (Anson and Ho, 2003).

Reactive rather than predictive

No one can predict the future, and it becomes cumbersome when the investors play the puzzle

to understand the direction of the volatility and usually risky one. Instead of trying to predict

the movements of the volatile nature and it is advised to take a reactive approach in which the

investors are supposed to react according to the volatility of the stock. A response can be

observed with regard to the changes in the VRP and this way it can help in minimising the

risk (Bhansali and Harris, 2018).

Adjustments and allocations

Conventionally a simple scaling in/out strategy is greatly outperforming the XIV drawdown

buy approach. This scaling strategy is not advisable for the investors who are thinking to

make the movement in the investments over the night. Therefore, one way to reduce the risk

is to stop the overnight exposures as it literally increases the trading costs and fails to capture

any favourable movements overnight (Lee, Liao and Tung, 2017).

Scaling Exposure

The volatility risk premium is important and equally valid in case of the size of the strategy

volatility exposure. If the VRP is large and if it seems to be in the favour of the investor, the

investor with the help of such strategy can increase the exposure and when the premium

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UNDERSTANDING THE VIX 9

skews the investor may reduce the exposure. This provides the risk adjusted exposure to the

VRP and most of the risk is taken when the probability of the event is positive.

Variety and diversification

Not every VIX strategies are exposed to the similar risks and each set of risk has its own

strength and weaknesses. Not all VIX procedures are presented to similar dangers, and every

set of the risks has its own strengths and weaknesses. These differences can significantly

traverse the performances due to market conditions. Diversifying the portfolio will reduce the

risks of the stock and will also give the opportunity to the investors to shift the risk from one

stock to another (Miao, Ramchander, Wang and Yang, 2017).

Maintaining a future perspective

Volatility trading strategies can generate the returns on timely basis. A strategy is designed to

get the benefits from the stock for long term purposes and to avoid any kind of risk that can

shake the drawdown scenario. While these strategies help in reducing the risk and the

magnitude of the duration of the drawdowns (Bekaert and Hoerova, 2014).

Part 3

Exchange traded products linked to VIX

The introduction of the Exchange traded volatility products also known as the ETP’s VIX

future contracts were launched in the year 2004, listed VIX option in the year 2006 and

volatility ETP’s in 2009 facilitates a lot of opportunities and enables the investors to access

the class of the assets and strategies that were out of reach earlier (Buehler and Cusatis,

2018). The facilitation of the short term volatility trading by traders at the short horizon end

gives a magnitude to the investors. One such example is the volatility space, which has been

changed from a hypothetical but however, a broadly followed measure of financial sentiment

of the investor. The VIX, which measures the suggested unpredictability of U.S. equity

markets over a period of 30 days and is computed on the basis of S&P 500 has been around

skews the investor may reduce the exposure. This provides the risk adjusted exposure to the

VRP and most of the risk is taken when the probability of the event is positive.

Variety and diversification

Not every VIX strategies are exposed to the similar risks and each set of risk has its own

strength and weaknesses. Not all VIX procedures are presented to similar dangers, and every

set of the risks has its own strengths and weaknesses. These differences can significantly

traverse the performances due to market conditions. Diversifying the portfolio will reduce the

risks of the stock and will also give the opportunity to the investors to shift the risk from one

stock to another (Miao, Ramchander, Wang and Yang, 2017).

Maintaining a future perspective

Volatility trading strategies can generate the returns on timely basis. A strategy is designed to

get the benefits from the stock for long term purposes and to avoid any kind of risk that can

shake the drawdown scenario. While these strategies help in reducing the risk and the

magnitude of the duration of the drawdowns (Bekaert and Hoerova, 2014).

Part 3

Exchange traded products linked to VIX

The introduction of the Exchange traded volatility products also known as the ETP’s VIX

future contracts were launched in the year 2004, listed VIX option in the year 2006 and

volatility ETP’s in 2009 facilitates a lot of opportunities and enables the investors to access

the class of the assets and strategies that were out of reach earlier (Buehler and Cusatis,

2018). The facilitation of the short term volatility trading by traders at the short horizon end

gives a magnitude to the investors. One such example is the volatility space, which has been

changed from a hypothetical but however, a broadly followed measure of financial sentiment

of the investor. The VIX, which measures the suggested unpredictability of U.S. equity

markets over a period of 30 days and is computed on the basis of S&P 500 has been around

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UNDERSTANDING THE VIX 10

for over two decades, yet by the difference of idea its estimation is not an investable resource

(Rhoads, 2018).

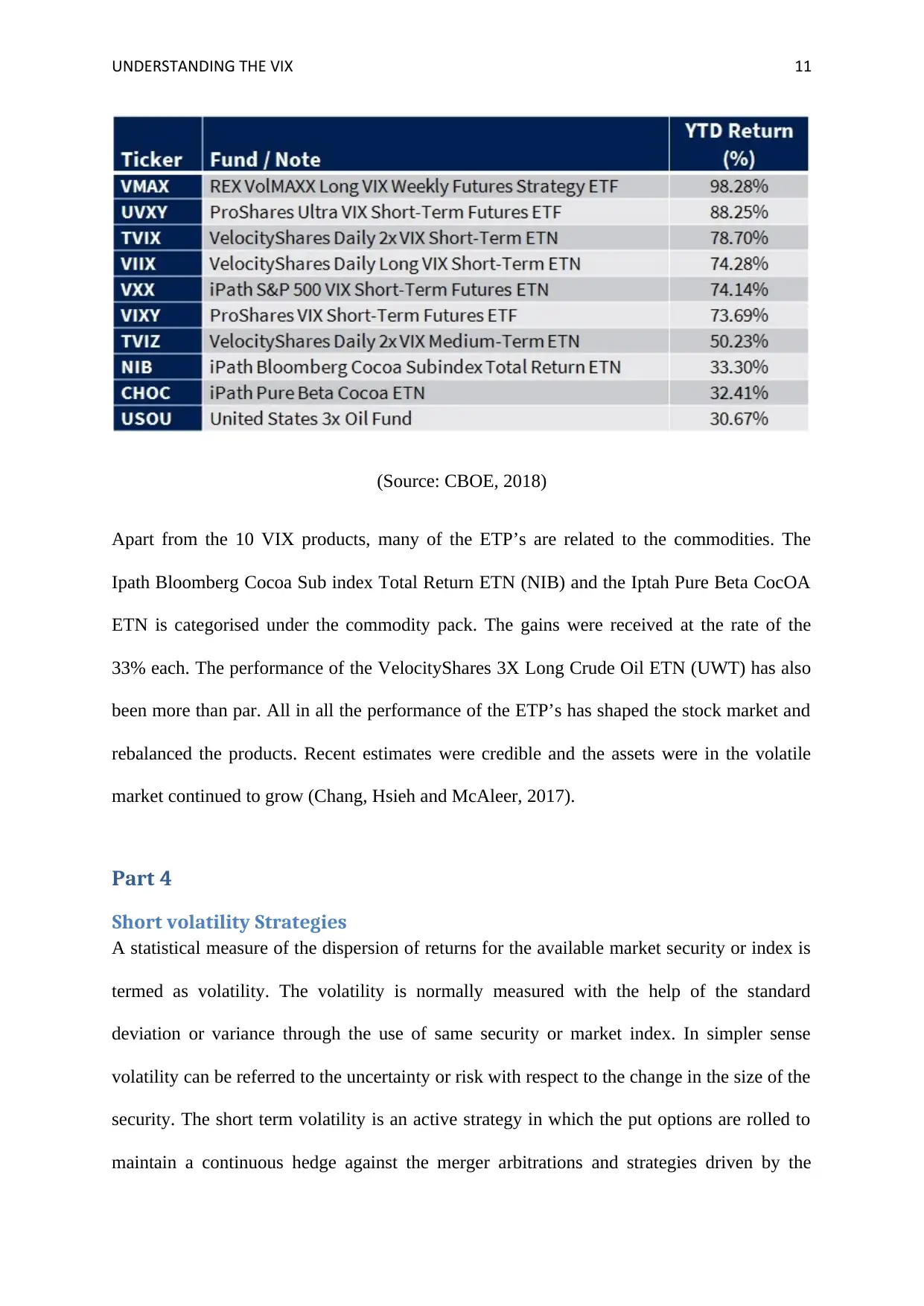

VIX ETP’s can be useful to hedge or cover the investments or to speculate on sell off of

potential nature. Generally VIX ETF’s are available for trading through the help of a range of

brokers. The largest and most popular volatility ETN is S&P 500 VIX Short-Term Futures

Exchange Traded Note. Generally VIX products and the related ETF’s are useful in

management of the risk. The first big accomplishment of the VIX ETPs was in the year 2010.

There are certain ETP’s such as SPDR S&P 500 ETF Trust, ishares Core U.S. Aggregate

Bond ETF iPath Pure Beta Cocoa ETN and Rex VoLMAXX long VIX futures Strategy ETF.

Keeping a view of the performance of these ETP’s in the financial market both the strategies

allow the traders to participate for the expected returns. During the year 2017, the

performance of the ETP’s was outperforming. The stellar performers in the bucket of the

ETF were SPY or AGG. Under the first list the returns ranged from almost 19% to 88%

(Roy, 2018). Half the ETP’s on the list are linked to volatility including Rex VoLMAXX

which was accelerated by 98.3%. The CBOE volatility index reached the summit of the stock

market as the U.S stock market faced a crash by 12%. In order to hedge their positions to

mitigate the future losses, investors bid up the prices.

The top performers are as follows.

for over two decades, yet by the difference of idea its estimation is not an investable resource

(Rhoads, 2018).

VIX ETP’s can be useful to hedge or cover the investments or to speculate on sell off of

potential nature. Generally VIX ETF’s are available for trading through the help of a range of

brokers. The largest and most popular volatility ETN is S&P 500 VIX Short-Term Futures

Exchange Traded Note. Generally VIX products and the related ETF’s are useful in

management of the risk. The first big accomplishment of the VIX ETPs was in the year 2010.

There are certain ETP’s such as SPDR S&P 500 ETF Trust, ishares Core U.S. Aggregate

Bond ETF iPath Pure Beta Cocoa ETN and Rex VoLMAXX long VIX futures Strategy ETF.

Keeping a view of the performance of these ETP’s in the financial market both the strategies

allow the traders to participate for the expected returns. During the year 2017, the

performance of the ETP’s was outperforming. The stellar performers in the bucket of the

ETF were SPY or AGG. Under the first list the returns ranged from almost 19% to 88%

(Roy, 2018). Half the ETP’s on the list are linked to volatility including Rex VoLMAXX

which was accelerated by 98.3%. The CBOE volatility index reached the summit of the stock

market as the U.S stock market faced a crash by 12%. In order to hedge their positions to

mitigate the future losses, investors bid up the prices.

The top performers are as follows.

UNDERSTANDING THE VIX 11

(Source: CBOE, 2018)

Apart from the 10 VIX products, many of the ETP’s are related to the commodities. The

Ipath Bloomberg Cocoa Sub index Total Return ETN (NIB) and the Iptah Pure Beta CocOA

ETN is categorised under the commodity pack. The gains were received at the rate of the

33% each. The performance of the VelocityShares 3X Long Crude Oil ETN (UWT) has also

been more than par. All in all the performance of the ETP’s has shaped the stock market and

rebalanced the products. Recent estimates were credible and the assets were in the volatile

market continued to grow (Chang, Hsieh and McAleer, 2017).

Part 4

Short volatility Strategies

A statistical measure of the dispersion of returns for the available market security or index is

termed as volatility. The volatility is normally measured with the help of the standard

deviation or variance through the use of same security or market index. In simpler sense

volatility can be referred to the uncertainty or risk with respect to the change in the size of the

security. The short term volatility is an active strategy in which the put options are rolled to

maintain a continuous hedge against the merger arbitrations and strategies driven by the

(Source: CBOE, 2018)

Apart from the 10 VIX products, many of the ETP’s are related to the commodities. The

Ipath Bloomberg Cocoa Sub index Total Return ETN (NIB) and the Iptah Pure Beta CocOA

ETN is categorised under the commodity pack. The gains were received at the rate of the

33% each. The performance of the VelocityShares 3X Long Crude Oil ETN (UWT) has also

been more than par. All in all the performance of the ETP’s has shaped the stock market and

rebalanced the products. Recent estimates were credible and the assets were in the volatile

market continued to grow (Chang, Hsieh and McAleer, 2017).

Part 4

Short volatility Strategies

A statistical measure of the dispersion of returns for the available market security or index is

termed as volatility. The volatility is normally measured with the help of the standard

deviation or variance through the use of same security or market index. In simpler sense

volatility can be referred to the uncertainty or risk with respect to the change in the size of the

security. The short term volatility is an active strategy in which the put options are rolled to

maintain a continuous hedge against the merger arbitrations and strategies driven by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.