Detailed Management Accounting Report: Systems, Techniques, Analysis

VerifiedAdded on 2020/07/22

|20

|6392

|42

Report

AI Summary

This report analyzes management accounting practices within the context of Unicorn Grocery, a company specializing in organic food and goods. It delves into various types of management accounting systems, including job-order costing and inventory management, and contrasts them with financial accounting. The report outlines essential management accounting techniques such as budget reports, accounts receivable aging, and job cost reports. Furthermore, it explores cost analysis methodologies and evaluates the advantages and disadvantages of different planning tools used in budgetary control. The assignment concludes by assessing how companies adapt different management accounting systems to enhance decision-making and achieve organizational goals. This report provides a comprehensive overview of management accounting principles and their practical application within a real-world business setting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1 ..........................................................................................................................................1

P1 Management accounting & different types of accounting system.........................................1

P2 Different techniques used for management accounting reporting........................................4

TASK 2............................................................................................................................................6

P3 Different techniques of cost analysis.....................................................................................6

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tool ......................................8

TASK 4..........................................................................................................................................11

P5 Evaluate how companies are adapting different management account system ..................11

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION ..........................................................................................................................1

TASK 1 ..........................................................................................................................................1

P1 Management accounting & different types of accounting system.........................................1

P2 Different techniques used for management accounting reporting........................................4

TASK 2............................................................................................................................................6

P3 Different techniques of cost analysis.....................................................................................6

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tool ......................................8

TASK 4..........................................................................................................................................11

P5 Evaluate how companies are adapting different management account system ..................11

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting refers to the process of examining business operations and costs

in order to make financial account, report and records to support the process of decision making

by managers of the firm so that goals of the business can attained. It is a process of determining,

measuring, examining, interpreting & communicating data and information in order to pursuit

objective of an organisation (Bennett and James, 2010). These accounting reports help managers

in making short term decisions by providing them accurate and timely information related to

finance and statistics. It is also known as managerial accounting. In the present assignment,

chosen company is Unicorn Grocery which is located in Chorlton, England. The firm sells

processed, fresh and dried organic food & drink with emphasize on fair trade and local sourcing.

Along with this, it also sells body care, household and general grocery goods. The report covers

various types of management accounting system and their essential requirements. It also includes

different methods used in management accounting reporting. By the use of suitable techniques of

cost analysis, various costs are calculated. Apart from this, merits and demerits of various

planning tools used in budgetary control are defined in the project.

TASK 1

P1 Management accounting & different types of accounting system

From: Management Accounting Officer Date: 21t February, 2018

To: General Manager of Unicorn Grocery

Subject: Management Accounting and Its Types

Management Accounting can be defined as an accounting activities which play an important

role in providing information to managers which helps in conducting company's operations. It

provides more detailed information as compare to financial accounting, for example if there is

any difference in revenue and expenditure in company products, then department will provide

comparative data that helps in analysing all the profitable and unprofitable activities.

This accounting provides faster information as compare to financial accounting in regards to

performance of company. It is a most important medium in providing future cost and revenue

rather than simply presenting past revenue expenditure. Further, it gives information more

quickly than financial accounting irrespective of giving annual report which is done financial

accounts it provides monthly, weekly or daily basis report that enable managers to consider all

1

Management Accounting refers to the process of examining business operations and costs

in order to make financial account, report and records to support the process of decision making

by managers of the firm so that goals of the business can attained. It is a process of determining,

measuring, examining, interpreting & communicating data and information in order to pursuit

objective of an organisation (Bennett and James, 2010). These accounting reports help managers

in making short term decisions by providing them accurate and timely information related to

finance and statistics. It is also known as managerial accounting. In the present assignment,

chosen company is Unicorn Grocery which is located in Chorlton, England. The firm sells

processed, fresh and dried organic food & drink with emphasize on fair trade and local sourcing.

Along with this, it also sells body care, household and general grocery goods. The report covers

various types of management accounting system and their essential requirements. It also includes

different methods used in management accounting reporting. By the use of suitable techniques of

cost analysis, various costs are calculated. Apart from this, merits and demerits of various

planning tools used in budgetary control are defined in the project.

TASK 1

P1 Management accounting & different types of accounting system

From: Management Accounting Officer Date: 21t February, 2018

To: General Manager of Unicorn Grocery

Subject: Management Accounting and Its Types

Management Accounting can be defined as an accounting activities which play an important

role in providing information to managers which helps in conducting company's operations. It

provides more detailed information as compare to financial accounting, for example if there is

any difference in revenue and expenditure in company products, then department will provide

comparative data that helps in analysing all the profitable and unprofitable activities.

This accounting provides faster information as compare to financial accounting in regards to

performance of company. It is a most important medium in providing future cost and revenue

rather than simply presenting past revenue expenditure. Further, it gives information more

quickly than financial accounting irrespective of giving annual report which is done financial

accounts it provides monthly, weekly or daily basis report that enable managers to consider all

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the feedback and shift it's concern towards management inefficiencies (Chenhall, 2012). It

enable in providing valuable management information for accurate estimates and tenders that

helps in negotiating prices.

Benefits of Management accounting:-

It helps in forecasting future trends of business.

Through management accounting insights must be developed that helps in decision

making both at operational and strategic levels.

It helps in analysing the difference between what was predicted and what is actually

achieved.

The cost control devices is management accounting enables the reduction in prices of

the product and good are supplied with quality at reasonable prices.

Management accounting selects only those information which are relevant and useful

for organisations.

It emphasis on those factors which helps in estimating future revenue and expenditure

like standard costing, budgetary control (Christ and Burritt, 2013).

Management takes the proper decisions and better planning on basis of financial

accounting information.

It select appropriate alternative from the available alternates which are normally more

attractive and profitable.

Types of management accounting -

Job-Order Costing Method: This method uses material cost flow document, overhead

cost flow document, labour cost flow document and job cost sheet so to track the

manufacturing expenses related with producing job lot. Manufactures produce various

products and each of them is produced with different production process. Each job lot is

having its own specific budget according to which activities related to it takes place.

For example: Account manager of Unicorn Grocery will first track raw material cost,

then they will track their labour cost and lastly they will figure out overhead expenses.

Further all of these three cost combine together on a job cost sheet. If the entire

production plan went as per the defined plan, then the total cost of job lot will be on

budget & comparatively less than selling price.

Inventory Management System: This type of management accounting system provides

2

enable in providing valuable management information for accurate estimates and tenders that

helps in negotiating prices.

Benefits of Management accounting:-

It helps in forecasting future trends of business.

Through management accounting insights must be developed that helps in decision

making both at operational and strategic levels.

It helps in analysing the difference between what was predicted and what is actually

achieved.

The cost control devices is management accounting enables the reduction in prices of

the product and good are supplied with quality at reasonable prices.

Management accounting selects only those information which are relevant and useful

for organisations.

It emphasis on those factors which helps in estimating future revenue and expenditure

like standard costing, budgetary control (Christ and Burritt, 2013).

Management takes the proper decisions and better planning on basis of financial

accounting information.

It select appropriate alternative from the available alternates which are normally more

attractive and profitable.

Types of management accounting -

Job-Order Costing Method: This method uses material cost flow document, overhead

cost flow document, labour cost flow document and job cost sheet so to track the

manufacturing expenses related with producing job lot. Manufactures produce various

products and each of them is produced with different production process. Each job lot is

having its own specific budget according to which activities related to it takes place.

For example: Account manager of Unicorn Grocery will first track raw material cost,

then they will track their labour cost and lastly they will figure out overhead expenses.

Further all of these three cost combine together on a job cost sheet. If the entire

production plan went as per the defined plan, then the total cost of job lot will be on

budget & comparatively less than selling price.

Inventory Management System: This type of management accounting system provides

2

beneficial information to manager of Unicorn Grocery concerned with inventory or

stock. It provides information related with raw material, finished goods, inventory

turnover. Usually companies manage their stock on daily basis. It is considered as an

essential aspect of doing business. In simple words, it refers to the remaining stock after

company has produced goods as per the customer demand and also after completing its

day to day operation. It covers each and every aspect starting from production, to

retailing to warehousing to shipping. It is component of operation management that

supervise the flow of stock from production department to warehouse in an effective and

efficient manner so to avoid overstock and stock-out.

Financial accounting – It presents the information in form of the financial statements

which is very crucial to the external parties such as stakeholders,creditors,lenders,banks

and other financial positions. These statements are based on the

rules,regulations,guidelines and directions of GAAP(generally accepted accounting

principles) which shows the past and current position. It includes the standards for the

financial information. Principles also contain the accounting

conventions,rules,regulations and other policies and accountant has to consider it before

creating balance sheet,operating statement. Reports are also created upon standards by

government bodies (Contrafatto and Burns, 2013). Company can also compare reports

and other information as they know their benchmarks. Through which they can also

improve their performance. Outside parties by evaluating these information take

decision to invest in the company.

Management accounting – It gives information regarding the management which is

important to internal users. Users include managers,CEO owners,employees and

internal stakeholders who evaluates information. Through this they can check past and

present performance of the company. They can check their progress and take corrective

actions if any deviations are there (Dillard and Roslender, 2011). Managers can make

short,long term plans , policies and other objectives. It also helps them in sales

forecasting,making budgets. Executives can create their reports and can take decisions

related to future. Owners can also do the cost comparison of present with that of past

year and try to reduce the cost. So it is beneficial to the company.

3

stock. It provides information related with raw material, finished goods, inventory

turnover. Usually companies manage their stock on daily basis. It is considered as an

essential aspect of doing business. In simple words, it refers to the remaining stock after

company has produced goods as per the customer demand and also after completing its

day to day operation. It covers each and every aspect starting from production, to

retailing to warehousing to shipping. It is component of operation management that

supervise the flow of stock from production department to warehouse in an effective and

efficient manner so to avoid overstock and stock-out.

Financial accounting – It presents the information in form of the financial statements

which is very crucial to the external parties such as stakeholders,creditors,lenders,banks

and other financial positions. These statements are based on the

rules,regulations,guidelines and directions of GAAP(generally accepted accounting

principles) which shows the past and current position. It includes the standards for the

financial information. Principles also contain the accounting

conventions,rules,regulations and other policies and accountant has to consider it before

creating balance sheet,operating statement. Reports are also created upon standards by

government bodies (Contrafatto and Burns, 2013). Company can also compare reports

and other information as they know their benchmarks. Through which they can also

improve their performance. Outside parties by evaluating these information take

decision to invest in the company.

Management accounting – It gives information regarding the management which is

important to internal users. Users include managers,CEO owners,employees and

internal stakeholders who evaluates information. Through this they can check past and

present performance of the company. They can check their progress and take corrective

actions if any deviations are there (Dillard and Roslender, 2011). Managers can make

short,long term plans , policies and other objectives. It also helps them in sales

forecasting,making budgets. Executives can create their reports and can take decisions

related to future. Owners can also do the cost comparison of present with that of past

year and try to reduce the cost. So it is beneficial to the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax accounting – GAAP includes the different guidelines ,directions through which

reports and other accounting statements can be prepared to modify provisions of

taxes .Concepts,principles and other rules are based on GAAP. Through this company

can make tax planning,implementation of tax rules and they can pay taxes timely .Firm

can create tax reports ,returns and give advice regarding it to other areas of business.

They can calculate profits through deducting the profits. Organization will not face any

problem as they pay taxes timely .Through it government can also make their reports

and take short and long term decisions.

Government accounting – It is referred to public accounting and this type of

accounting is used in public sector. Separate rules,regulations,concepts,principles are

there of this sector as compared to private sector. It checks past, present financial

performance of this sector and if deviations they take remedial actions to improve them.

They can make their reports,rules,policies, plans and objectives related to the budgets

and that of any other problems. Separate policies are created for their events and other

transactions.

Forensic Accounting – It means the techniques ,auditing and use of other tools in

solving the conflicts in the management. Accountants are witnesses of the criminal and

civil disputes. They helps in detecting the fraud. It includes different cases such as

insurance,personal injury and other different frauds and claims (DRURY, 2013).

Project accounting – It helps in checking the financial progress of the project. So they

are the standards. Managers can evaluate their performance and can take corrective

actions to improve them. It is beneficial for success of completing the project. It is used

as a competitive weapon for many companies.

Social accounting – It includes policies,rules which evaluates different activities related

to protection of social environment. Company can make different environmental reports

which helps in making yearly reports. It helps in public awareness and thus helps in

development of society (Dumitru and et. al. 2011).

4

reports and other accounting statements can be prepared to modify provisions of

taxes .Concepts,principles and other rules are based on GAAP. Through this company

can make tax planning,implementation of tax rules and they can pay taxes timely .Firm

can create tax reports ,returns and give advice regarding it to other areas of business.

They can calculate profits through deducting the profits. Organization will not face any

problem as they pay taxes timely .Through it government can also make their reports

and take short and long term decisions.

Government accounting – It is referred to public accounting and this type of

accounting is used in public sector. Separate rules,regulations,concepts,principles are

there of this sector as compared to private sector. It checks past, present financial

performance of this sector and if deviations they take remedial actions to improve them.

They can make their reports,rules,policies, plans and objectives related to the budgets

and that of any other problems. Separate policies are created for their events and other

transactions.

Forensic Accounting – It means the techniques ,auditing and use of other tools in

solving the conflicts in the management. Accountants are witnesses of the criminal and

civil disputes. They helps in detecting the fraud. It includes different cases such as

insurance,personal injury and other different frauds and claims (DRURY, 2013).

Project accounting – It helps in checking the financial progress of the project. So they

are the standards. Managers can evaluate their performance and can take corrective

actions to improve them. It is beneficial for success of completing the project. It is used

as a competitive weapon for many companies.

Social accounting – It includes policies,rules which evaluates different activities related

to protection of social environment. Company can make different environmental reports

which helps in making yearly reports. It helps in public awareness and thus helps in

development of society (Dumitru and et. al. 2011).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Different techniques used for management accounting reporting

From: Management Accounting Officer Date: 21t February, 2018

To: General Manager of Unicorn Grocery

Subject: Management Accounting Reporting

Management Accounting Reporting: Management accounts and reports are the sources by the

help of which goals and targets of the firm can be achieved. Managerial accounting emphasize

on information received by financial accounting and is used for decision making, planning and

controlling. Data and information are collected from various departments of the organisation

such as administration, production and operations, human resource, finance & accounts, sales

and marketing etc. Below described are some techniques used for management accounting

reporting which are as follows:

Budget Report: Under this method, future needs related to finance is forecasted and

arranged it on orderly basis accordingly. Budgetary control technique is used to monitor and

control financial performances of the firm. Through this, the operations of business are directed

in desirable direction. This technique is very useful for managers in order to control all the

operations and costs in given period of accounting.

Accounts Receivable Aging: It is a critical tool mainly used for handling cash flow for

business entities that extent credit to their consumers. This Aging report divides the balance of

customer by the amount they have owned. Most of the report maintains separate columns for

invoices that are usually 60 days late or 90 days late or 30 days late. Accounts manager use

these report so to figure out problem related with firm's collection process. However, if

significant number of customers fails to pay their balances then company are require to tighten

their credit policies. In addition to that, if account manager of Unicorn Grocery periodically

examine account receivable aging then they are ultimately reducing the chances of overlooking

old debts.

Job Cost Report: These reports are mainly prepare for specific project that shows all

the expenses related to that particular project. Thy are matched with estimated revenue which

enables firm to figure to out whether they earned significant profitability in this job or not.

Along with this, it aid in determining high-earning areas of the company so that they can laid

stress on those areas instead of wasting money and time on low profit margin jobs. Unicorn

Grocery is using these report so as to examine expenses during on-going project so that

5

From: Management Accounting Officer Date: 21t February, 2018

To: General Manager of Unicorn Grocery

Subject: Management Accounting Reporting

Management Accounting Reporting: Management accounts and reports are the sources by the

help of which goals and targets of the firm can be achieved. Managerial accounting emphasize

on information received by financial accounting and is used for decision making, planning and

controlling. Data and information are collected from various departments of the organisation

such as administration, production and operations, human resource, finance & accounts, sales

and marketing etc. Below described are some techniques used for management accounting

reporting which are as follows:

Budget Report: Under this method, future needs related to finance is forecasted and

arranged it on orderly basis accordingly. Budgetary control technique is used to monitor and

control financial performances of the firm. Through this, the operations of business are directed

in desirable direction. This technique is very useful for managers in order to control all the

operations and costs in given period of accounting.

Accounts Receivable Aging: It is a critical tool mainly used for handling cash flow for

business entities that extent credit to their consumers. This Aging report divides the balance of

customer by the amount they have owned. Most of the report maintains separate columns for

invoices that are usually 60 days late or 90 days late or 30 days late. Accounts manager use

these report so to figure out problem related with firm's collection process. However, if

significant number of customers fails to pay their balances then company are require to tighten

their credit policies. In addition to that, if account manager of Unicorn Grocery periodically

examine account receivable aging then they are ultimately reducing the chances of overlooking

old debts.

Job Cost Report: These reports are mainly prepare for specific project that shows all

the expenses related to that particular project. Thy are matched with estimated revenue which

enables firm to figure to out whether they earned significant profitability in this job or not.

Along with this, it aid in determining high-earning areas of the company so that they can laid

stress on those areas instead of wasting money and time on low profit margin jobs. Unicorn

Grocery is using these report so as to examine expenses during on-going project so that

5

managers can deal with wastage area in an effective manner and develop corrective action

before final costs increases or escalate.

Management Information System: For proper and effective functioning of business,

free flow communication is necessary within the organisation. Thus, management needs to

build the system by which every individual of the firm can assess information & data and used

it for discharging their responsibilities and taking decisions. Proper and clear communication of

information ensures attainment of set objectives and targets of the company in effective and

efficient manner.

Cost Accounting: Cost data is presented by this method of accounting in product,

process, department and branch wise. This method focuses to capture cost of manufacturing of

the company by assessing the cost of raw material at every production step and fixed cost. Data

is compared with predetermined cost data. This comparison enables the management to find out

the reasons that are responsible for variance among these costs. Various costs are considered in

this method of accounting.

Fund Flow Analysis: This is used to determine all inflows and outflows of cash in and

out of financial assets. It is useful for the management to ensure proper utilization of funds. The

data of present year is compared with previous one in order to know that whether capital is

properly utilized or not. By the assistance of fund flow analysis, funds from operations and

changes in working capital are also examined.

Marginal Costing: This method is use to set fix selling price, pick out best sales mix,

optimum utilization of scarce resources or raw materials, make decisions, rejection and

acceptance of bulk and foreign order etc. It is rely on fixed & variable cost as well as

contribution (Fullerton, Kennedy and Widener, 2013).

Decision Making Accounting: It is the method by which management choose most

profitable and best alternative to solve the issues related to business. Comparison of relevant

cost is done in order to select such alternative. Hence, accounting information and data are used

to resolve issues which arises due to increasing nature of complexity of business. This method

helps the managers of the company in making effective decisions which leads the firm towards

attainment of objectives on specific period of time.

Management Reporting: A report is prepared by management accountant on the basis

of balance sheet, profit & loss account content and submit them to top management (Granlund,

6

before final costs increases or escalate.

Management Information System: For proper and effective functioning of business,

free flow communication is necessary within the organisation. Thus, management needs to

build the system by which every individual of the firm can assess information & data and used

it for discharging their responsibilities and taking decisions. Proper and clear communication of

information ensures attainment of set objectives and targets of the company in effective and

efficient manner.

Cost Accounting: Cost data is presented by this method of accounting in product,

process, department and branch wise. This method focuses to capture cost of manufacturing of

the company by assessing the cost of raw material at every production step and fixed cost. Data

is compared with predetermined cost data. This comparison enables the management to find out

the reasons that are responsible for variance among these costs. Various costs are considered in

this method of accounting.

Fund Flow Analysis: This is used to determine all inflows and outflows of cash in and

out of financial assets. It is useful for the management to ensure proper utilization of funds. The

data of present year is compared with previous one in order to know that whether capital is

properly utilized or not. By the assistance of fund flow analysis, funds from operations and

changes in working capital are also examined.

Marginal Costing: This method is use to set fix selling price, pick out best sales mix,

optimum utilization of scarce resources or raw materials, make decisions, rejection and

acceptance of bulk and foreign order etc. It is rely on fixed & variable cost as well as

contribution (Fullerton, Kennedy and Widener, 2013).

Decision Making Accounting: It is the method by which management choose most

profitable and best alternative to solve the issues related to business. Comparison of relevant

cost is done in order to select such alternative. Hence, accounting information and data are used

to resolve issues which arises due to increasing nature of complexity of business. This method

helps the managers of the company in making effective decisions which leads the firm towards

attainment of objectives on specific period of time.

Management Reporting: A report is prepared by management accountant on the basis

of balance sheet, profit & loss account content and submit them to top management (Granlund,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2011). These reports reveal strengths and weaknesses in various areas of financial and operating

activities. These determination are very useful to manager in decision making and exercising

control.

Ratio Analysis: This method is useful to management in release of its general functions

of anticipating, planning, coordination, communicating and control. It coat the way of effective

control of firm's operations by undertaking appraisal of both monetary and physical targets. It is

used to analyse different aspects of financial and operating performance of the company such as

liquidity, profitability, efficiency and solvency of firm.

Financial Statement Analysis: Balance sheet and profit & loss account are crucial

financial statements. These are examined for different period. This analysis assist the

administration to know the growth rate of business entity. Financial statement analysis is done

by ratio analysis, comparative and common financial statements.

Revaluation Accounting: According to this technique, fixed assets are revalued so that

capital is clearly represented with the value of asset (Hopwood, Unerman and Fries, 2010). It

assists to determine fair return on the capital employed.

Cash Flow Analysis: Cash movement from one period to other can be determined by

this analysis. It is use to evaluate quality of firm's income. Positive cash flow shows increase in

liquid assets of company and negative indicates decrease in liquid assets.

Financial Planning: The main purpose of every business organisation is profit

maximization. This objective is attained by formulating appropriate and sound financial

planning. Thus, financial planning tool is considered as a best method for accomplishing

objectives and targets of business concern (Kotas, 2014).

Standard costing: It is defined as a predetermined cost. It acts as a yard stick to measure

actual performance. This method is used to find out the reasons for deviations. Standard

costing is used by the firms to determine the variances between actual cost of products that were

manufactured and the cost that must have incurred for those goods. It includes the cost of direct

labour & material and manufacturing overhead.

Above mentioned are the different techniques used for management accounting

reporting . The financial manager of Unicorn Grocery use some of these methods in order to

attain objectives of the organisation. These methods are assistive in making financial decisions

and monitoring and control of performance of the organisation.

7

activities. These determination are very useful to manager in decision making and exercising

control.

Ratio Analysis: This method is useful to management in release of its general functions

of anticipating, planning, coordination, communicating and control. It coat the way of effective

control of firm's operations by undertaking appraisal of both monetary and physical targets. It is

used to analyse different aspects of financial and operating performance of the company such as

liquidity, profitability, efficiency and solvency of firm.

Financial Statement Analysis: Balance sheet and profit & loss account are crucial

financial statements. These are examined for different period. This analysis assist the

administration to know the growth rate of business entity. Financial statement analysis is done

by ratio analysis, comparative and common financial statements.

Revaluation Accounting: According to this technique, fixed assets are revalued so that

capital is clearly represented with the value of asset (Hopwood, Unerman and Fries, 2010). It

assists to determine fair return on the capital employed.

Cash Flow Analysis: Cash movement from one period to other can be determined by

this analysis. It is use to evaluate quality of firm's income. Positive cash flow shows increase in

liquid assets of company and negative indicates decrease in liquid assets.

Financial Planning: The main purpose of every business organisation is profit

maximization. This objective is attained by formulating appropriate and sound financial

planning. Thus, financial planning tool is considered as a best method for accomplishing

objectives and targets of business concern (Kotas, 2014).

Standard costing: It is defined as a predetermined cost. It acts as a yard stick to measure

actual performance. This method is used to find out the reasons for deviations. Standard

costing is used by the firms to determine the variances between actual cost of products that were

manufactured and the cost that must have incurred for those goods. It includes the cost of direct

labour & material and manufacturing overhead.

Above mentioned are the different techniques used for management accounting

reporting . The financial manager of Unicorn Grocery use some of these methods in order to

attain objectives of the organisation. These methods are assistive in making financial decisions

and monitoring and control of performance of the organisation.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

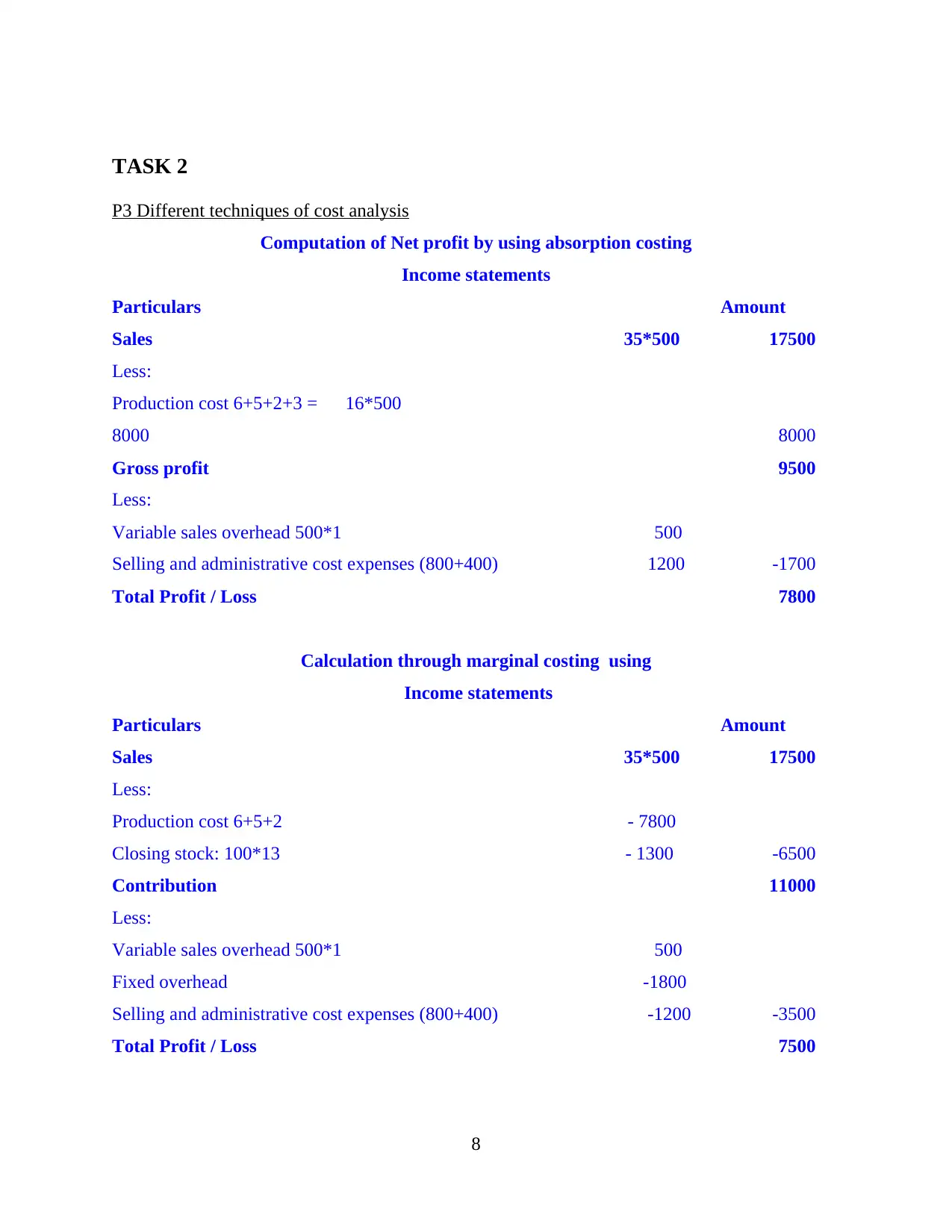

TASK 2

P3 Different techniques of cost analysis

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

8

P3 Different techniques of cost analysis

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

8

In above practical question, cost has been analysed via two techniques one is absorption and

other is marginal. In absorption costing, fixed cost and overheads are not taken into

consideration. Profit under marginal cost technique is £7500 and under absorption is £9500.

Difference between financial statement and financial planning:

Financial Statement Financial Planning

This statement is generally prepare on

the basis of financial statement or

records such as income statement,

balance sheet, profit and loss statement.

It shows the actual position of the

company in terms of numerical figures.

This technique also determine the

capacity of Unicorn Grocery in context

of paying all debt and liabilities on

time.

It anticipates financial needs, managing

different department and division and

identifies the needs in order to achieve

specific task.

It assist in creating financial

procedures which further help in

achieving goals and objectives of the

company.

With the help of financial planning,

Unicorn Grocery can identify the need

to capital requirement.

TASK 3

P4 Advantages and disadvantages of different types of planning tool

Budgetary Control refers to the process through which various business

enterprises prepare budget for future time period and match with actual performance in order to

detect any variances (Leitner, 2013). In simple words, budgeting means preparation of plans in

numerical figures for the specified future time-frame. Companies may develop the budget for

different divisions, departments, units or the entire organisation. The time period of budget is

usually for one year depending upon the firm whether they prefer accounting or financial year.

Organisations compare budgeted figures with the actual ones which is ultimately beneficial for

company as via this they can easily determine variances & take corrective measures without any

further delay. Budgets are the basis of control systems. They measure the performance of the

company in terms of financial figures and alleviate comparison among different levels or

divisions of Unicorn Grocery.

9

other is marginal. In absorption costing, fixed cost and overheads are not taken into

consideration. Profit under marginal cost technique is £7500 and under absorption is £9500.

Difference between financial statement and financial planning:

Financial Statement Financial Planning

This statement is generally prepare on

the basis of financial statement or

records such as income statement,

balance sheet, profit and loss statement.

It shows the actual position of the

company in terms of numerical figures.

This technique also determine the

capacity of Unicorn Grocery in context

of paying all debt and liabilities on

time.

It anticipates financial needs, managing

different department and division and

identifies the needs in order to achieve

specific task.

It assist in creating financial

procedures which further help in

achieving goals and objectives of the

company.

With the help of financial planning,

Unicorn Grocery can identify the need

to capital requirement.

TASK 3

P4 Advantages and disadvantages of different types of planning tool

Budgetary Control refers to the process through which various business

enterprises prepare budget for future time period and match with actual performance in order to

detect any variances (Leitner, 2013). In simple words, budgeting means preparation of plans in

numerical figures for the specified future time-frame. Companies may develop the budget for

different divisions, departments, units or the entire organisation. The time period of budget is

usually for one year depending upon the firm whether they prefer accounting or financial year.

Organisations compare budgeted figures with the actual ones which is ultimately beneficial for

company as via this they can easily determine variances & take corrective measures without any

further delay. Budgets are the basis of control systems. They measure the performance of the

company in terms of financial figures and alleviate comparison among different levels or

divisions of Unicorn Grocery.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.