B9AC106 - Financial Analysis: Unilever plc Performance Review

VerifiedAdded on 2023/06/15

|29

|5833

|304

Report

AI Summary

This report provides a comprehensive financial analysis of Unilever plc, evaluating its financial performance and position through ratio analysis over the past five years. Profitability ratios, including return on shareholder's fund, operating profit margin, and gross profit margin, are assessed and compared with competitors like P&G and PepsiCo. Liquidity ratios, such as current and acid-test ratios, are examined to determine the company's short-term debt obligation capacity. Efficiency ratios, including receivable collection period, payable payment days, and inventory days, are calculated to assess working capital management. The report also covers gearing and investment ratios, including earnings per share and price-earnings ratio, and offers recommendations for enhancing the company’s performance, considering competitor stakes and investment opportunities. The analysis uses financial data from Unilever plc's annual reports and stock prices to provide a thorough evaluation of the company's financial health.

Running Head: Finance

1

Project Report: Finance

1

Project Report: Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

2

Contents

Introduction.......................................................................................................................4

Company overview...........................................................................................................4

Financial performance and financial position...................................................................4

Profitability ratio...........................................................................................................5

Return on shareholder’s fund....................................................................................5

Operating profit margin............................................................................................6

Gross profit margin...................................................................................................7

Liquidity ratio...............................................................................................................8

(Morningstar, 2018)..................................................................................................8

Current ratio..............................................................................................................8

Acid Test ratio..........................................................................................................9

Efficiency ratio...........................................................................................................11

Receivable collection period...................................................................................11

Payable payment days.............................................................................................12

Inventory days........................................................................................................13

Gearing ratio...............................................................................................................14

Investment ratio..........................................................................................................15

Earnings per share...................................................................................................16

Price earnings ratio.................................................................................................16

Initiative to enhance company’s performance................................................................17

Competitor’s stake in the company................................................................................18

Recommendation............................................................................................................19

References.......................................................................................................................21

Appendix.........................................................................................................................23

2

Contents

Introduction.......................................................................................................................4

Company overview...........................................................................................................4

Financial performance and financial position...................................................................4

Profitability ratio...........................................................................................................5

Return on shareholder’s fund....................................................................................5

Operating profit margin............................................................................................6

Gross profit margin...................................................................................................7

Liquidity ratio...............................................................................................................8

(Morningstar, 2018)..................................................................................................8

Current ratio..............................................................................................................8

Acid Test ratio..........................................................................................................9

Efficiency ratio...........................................................................................................11

Receivable collection period...................................................................................11

Payable payment days.............................................................................................12

Inventory days........................................................................................................13

Gearing ratio...............................................................................................................14

Investment ratio..........................................................................................................15

Earnings per share...................................................................................................16

Price earnings ratio.................................................................................................16

Initiative to enhance company’s performance................................................................17

Competitor’s stake in the company................................................................................18

Recommendation............................................................................................................19

References.......................................................................................................................21

Appendix.........................................................................................................................23

Finance

3

Figure 1: return on shareholders’ Fund............................................................................6

Figure 2: Operating profit margin.....................................................................................7

Figure 3: Gross Profit margin...........................................................................................8

Figure 4: Current ratio......................................................................................................9

Figure 5: Acid Test Ratio...............................................................................................10

Figure 6: Receivable collection period...........................................................................12

Figure 7: Payable collection period................................................................................13

Figure 8: Inventory days.................................................................................................14

Figure 9: Gearing ratio....................................................................................................15

Figure 10: Earnings per share.........................................................................................16

3

Figure 1: return on shareholders’ Fund............................................................................6

Figure 2: Operating profit margin.....................................................................................7

Figure 3: Gross Profit margin...........................................................................................8

Figure 4: Current ratio......................................................................................................9

Figure 5: Acid Test Ratio...............................................................................................10

Figure 6: Receivable collection period...........................................................................12

Figure 7: Payable collection period................................................................................13

Figure 8: Inventory days.................................................................................................14

Figure 9: Gearing ratio....................................................................................................15

Figure 10: Earnings per share.........................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

4

Introduction:

This report paper has been prepared to evaluate the financial position, financial

performance, competitor position and the investment opportunity of Unilever plc. Financial

evaluation over an organization is significant as it assists the company to make better

decision about the position and the performance of the company. This report explains that it

becomes easier for the company and the stakeholders of the company to evaluate the position

of the organization and make better conclusion about the position, investment opportunity

and performance of the company. Further, it explains that the financial performance of the

company could be analyzed on the basis of annual report, financial statements of the

company, stock price of the company, competitor position of the company and the worth of

the company.

For this report, financial data of Unilever plc of last 5 years have been analyzed and

the ratio study has been conducted. Further, the competitors financial performance has been

compare with the financial performance of Uniliver plc and lastly, the stock performance and

the investment opportunity of the company has been evaluated.

Company overview:

Unilever plc is one of the fastest growing organizations in consumer goods market.

This company operates its business through foods, home care, personal care refreshment

segment etc. The company has diversified its market among 112 countries and the market

share of the company is huge. Personal segment of the company provides hair care and

skincare products, oral care products and deodorants. Food segment provides sauces, soup,

mayonnaise, margarines, salad dressings, spreads etc. the company has been founded in 1885.

Headquarter of the company is in London, UK (Home, 2018). The financial performance and

the position expresses about various positive and impressive changes into the organization.

Financial performance and financial position:

Financial performance and financial position of an organization could be evaluated

and measured through the financial statement and the market worth of the company.

Basically, it is a process in which the results of an organization are measured through

identifying the policies and the activities of the company in monetary terms (Davies and

4

Introduction:

This report paper has been prepared to evaluate the financial position, financial

performance, competitor position and the investment opportunity of Unilever plc. Financial

evaluation over an organization is significant as it assists the company to make better

decision about the position and the performance of the company. This report explains that it

becomes easier for the company and the stakeholders of the company to evaluate the position

of the organization and make better conclusion about the position, investment opportunity

and performance of the company. Further, it explains that the financial performance of the

company could be analyzed on the basis of annual report, financial statements of the

company, stock price of the company, competitor position of the company and the worth of

the company.

For this report, financial data of Unilever plc of last 5 years have been analyzed and

the ratio study has been conducted. Further, the competitors financial performance has been

compare with the financial performance of Uniliver plc and lastly, the stock performance and

the investment opportunity of the company has been evaluated.

Company overview:

Unilever plc is one of the fastest growing organizations in consumer goods market.

This company operates its business through foods, home care, personal care refreshment

segment etc. The company has diversified its market among 112 countries and the market

share of the company is huge. Personal segment of the company provides hair care and

skincare products, oral care products and deodorants. Food segment provides sauces, soup,

mayonnaise, margarines, salad dressings, spreads etc. the company has been founded in 1885.

Headquarter of the company is in London, UK (Home, 2018). The financial performance and

the position expresses about various positive and impressive changes into the organization.

Financial performance and financial position:

Financial performance and financial position of an organization could be evaluated

and measured through the financial statement and the market worth of the company.

Basically, it is a process in which the results of an organization are measured through

identifying the policies and the activities of the company in monetary terms (Davies and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

5

Crawford, 2011). The study of financial performance and position of the Unilever plc is as

follows:

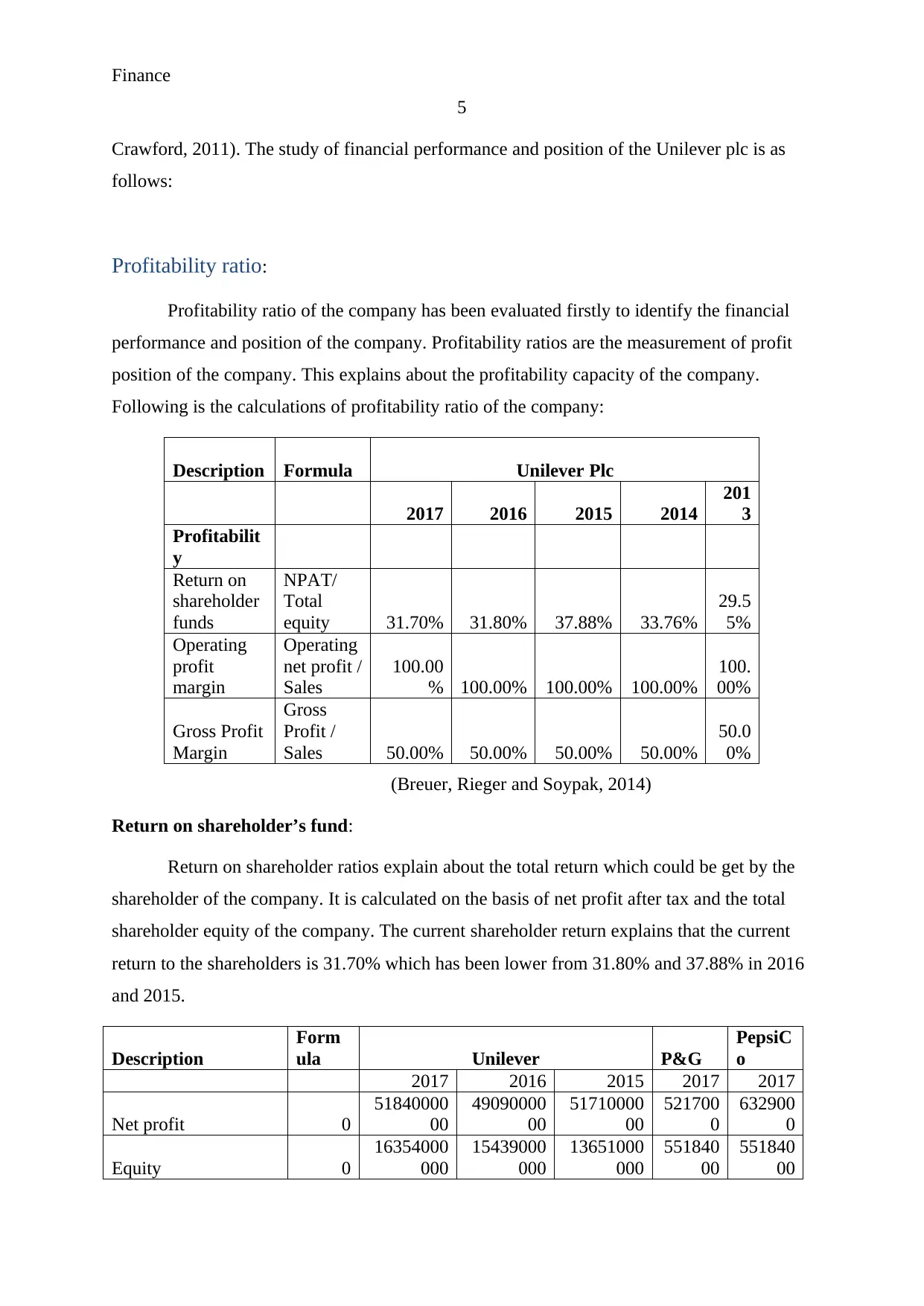

Profitability ratio:

Profitability ratio of the company has been evaluated firstly to identify the financial

performance and position of the company. Profitability ratios are the measurement of profit

position of the company. This explains about the profitability capacity of the company.

Following is the calculations of profitability ratio of the company:

Description Formula Unilever Plc

2017 2016 2015 2014

201

3

Profitabilit

y

Return on

shareholder

funds

NPAT/

Total

equity 31.70% 31.80% 37.88% 33.76%

29.5

5%

Operating

profit

margin

Operating

net profit /

Sales

100.00

% 100.00% 100.00% 100.00%

100.

00%

Gross Profit

Margin

Gross

Profit /

Sales 50.00% 50.00% 50.00% 50.00%

50.0

0%

(Breuer, Rieger and Soypak, 2014)

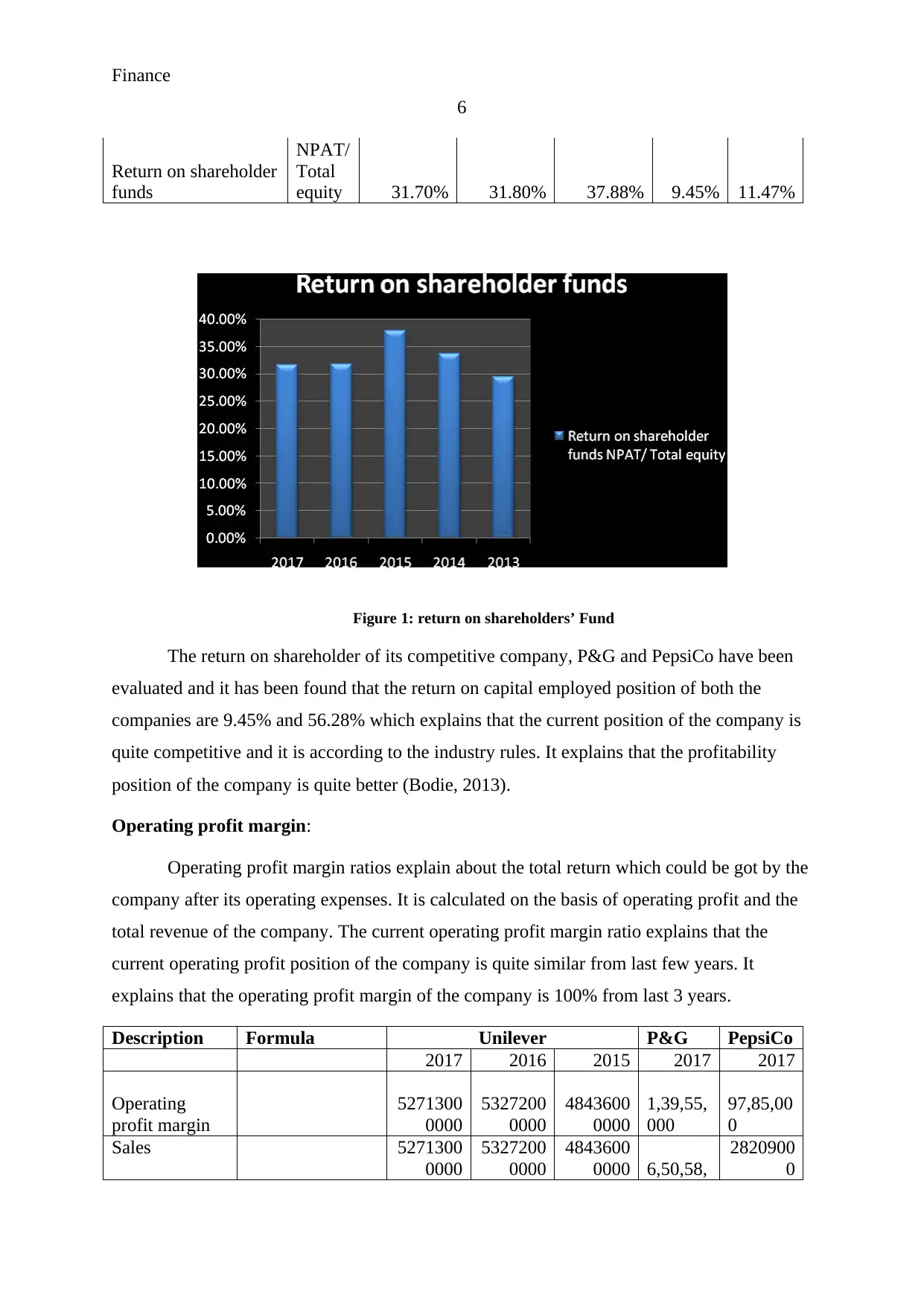

Return on shareholder’s fund:

Return on shareholder ratios explain about the total return which could be get by the

shareholder of the company. It is calculated on the basis of net profit after tax and the total

shareholder equity of the company. The current shareholder return explains that the current

return to the shareholders is 31.70% which has been lower from 31.80% and 37.88% in 2016

and 2015.

Description

Form

ula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Net profit 0

51840000

00

49090000

00

51710000

00

521700

0

632900

0

Equity 0

16354000

000

15439000

000

13651000

000

551840

00

551840

00

5

Crawford, 2011). The study of financial performance and position of the Unilever plc is as

follows:

Profitability ratio:

Profitability ratio of the company has been evaluated firstly to identify the financial

performance and position of the company. Profitability ratios are the measurement of profit

position of the company. This explains about the profitability capacity of the company.

Following is the calculations of profitability ratio of the company:

Description Formula Unilever Plc

2017 2016 2015 2014

201

3

Profitabilit

y

Return on

shareholder

funds

NPAT/

Total

equity 31.70% 31.80% 37.88% 33.76%

29.5

5%

Operating

profit

margin

Operating

net profit /

Sales

100.00

% 100.00% 100.00% 100.00%

100.

00%

Gross Profit

Margin

Gross

Profit /

Sales 50.00% 50.00% 50.00% 50.00%

50.0

0%

(Breuer, Rieger and Soypak, 2014)

Return on shareholder’s fund:

Return on shareholder ratios explain about the total return which could be get by the

shareholder of the company. It is calculated on the basis of net profit after tax and the total

shareholder equity of the company. The current shareholder return explains that the current

return to the shareholders is 31.70% which has been lower from 31.80% and 37.88% in 2016

and 2015.

Description

Form

ula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Net profit 0

51840000

00

49090000

00

51710000

00

521700

0

632900

0

Equity 0

16354000

000

15439000

000

13651000

000

551840

00

551840

00

Finance

6

Return on shareholder

funds

NPAT/

Total

equity 31.70% 31.80% 37.88% 9.45% 11.47%

Figure 1: return on shareholders’ Fund

The return on shareholder of its competitive company, P&G and PepsiCo have been

evaluated and it has been found that the return on capital employed position of both the

companies are 9.45% and 56.28% which explains that the current position of the company is

quite competitive and it is according to the industry rules. It explains that the profitability

position of the company is quite better (Bodie, 2013).

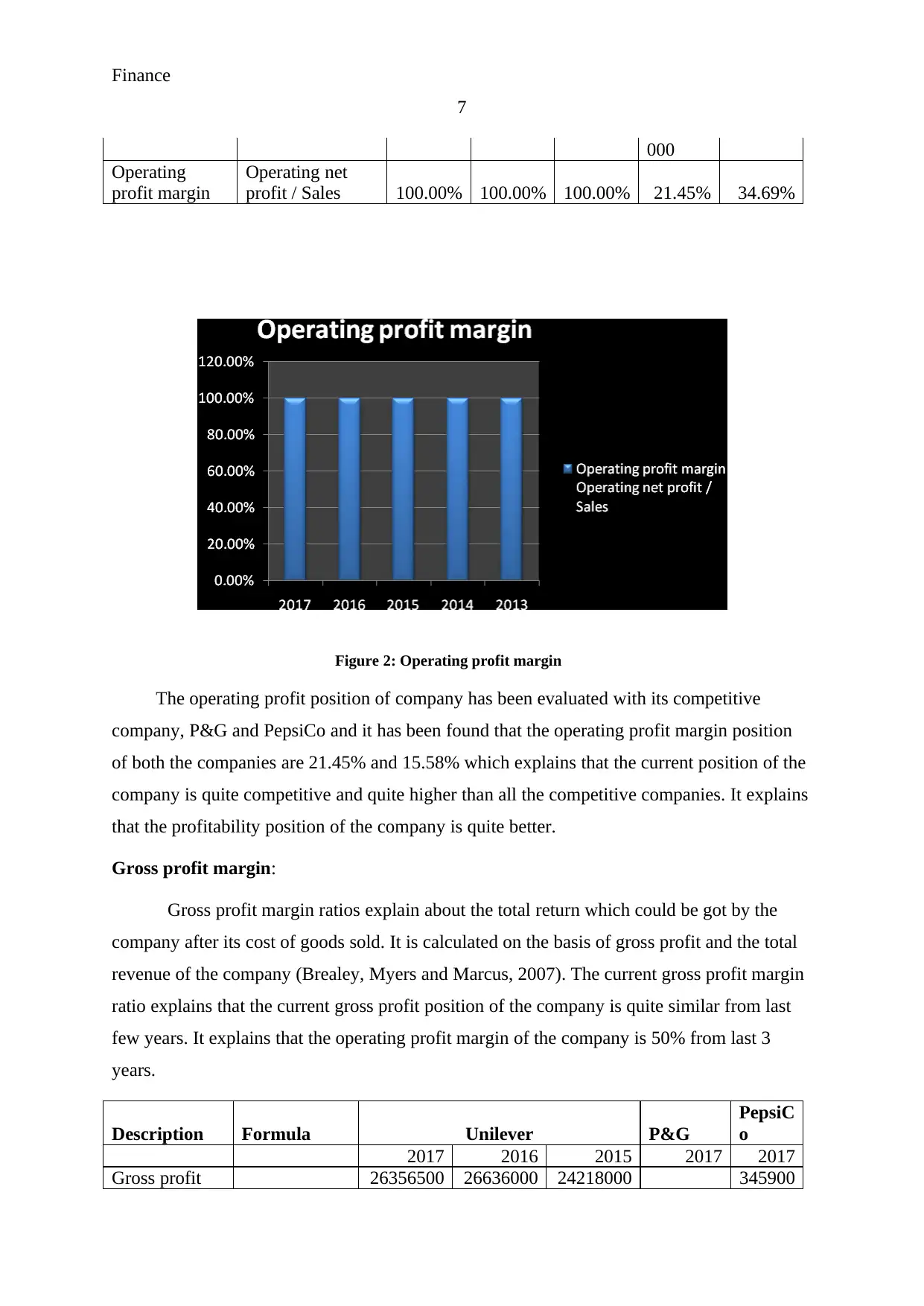

Operating profit margin:

Operating profit margin ratios explain about the total return which could be got by the

company after its operating expenses. It is calculated on the basis of operating profit and the

total revenue of the company. The current operating profit margin ratio explains that the

current operating profit position of the company is quite similar from last few years. It

explains that the operating profit margin of the company is 100% from last 3 years.

Description Formula Unilever P&G PepsiCo

2017 2016 2015 2017 2017

Operating

profit margin

5271300

0000

5327200

0000

4843600

0000

1,39,55,

000

97,85,00

0

Sales 5271300

0000

5327200

0000

4843600

0000 6,50,58,

2820900

0

6

Return on shareholder

funds

NPAT/

Total

equity 31.70% 31.80% 37.88% 9.45% 11.47%

Figure 1: return on shareholders’ Fund

The return on shareholder of its competitive company, P&G and PepsiCo have been

evaluated and it has been found that the return on capital employed position of both the

companies are 9.45% and 56.28% which explains that the current position of the company is

quite competitive and it is according to the industry rules. It explains that the profitability

position of the company is quite better (Bodie, 2013).

Operating profit margin:

Operating profit margin ratios explain about the total return which could be got by the

company after its operating expenses. It is calculated on the basis of operating profit and the

total revenue of the company. The current operating profit margin ratio explains that the

current operating profit position of the company is quite similar from last few years. It

explains that the operating profit margin of the company is 100% from last 3 years.

Description Formula Unilever P&G PepsiCo

2017 2016 2015 2017 2017

Operating

profit margin

5271300

0000

5327200

0000

4843600

0000

1,39,55,

000

97,85,00

0

Sales 5271300

0000

5327200

0000

4843600

0000 6,50,58,

2820900

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

7

000

Operating

profit margin

Operating net

profit / Sales 100.00% 100.00% 100.00% 21.45% 34.69%

Figure 2: Operating profit margin

The operating profit position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the operating profit margin position

of both the companies are 21.45% and 15.58% which explains that the current position of the

company is quite competitive and quite higher than all the competitive companies. It explains

that the profitability position of the company is quite better.

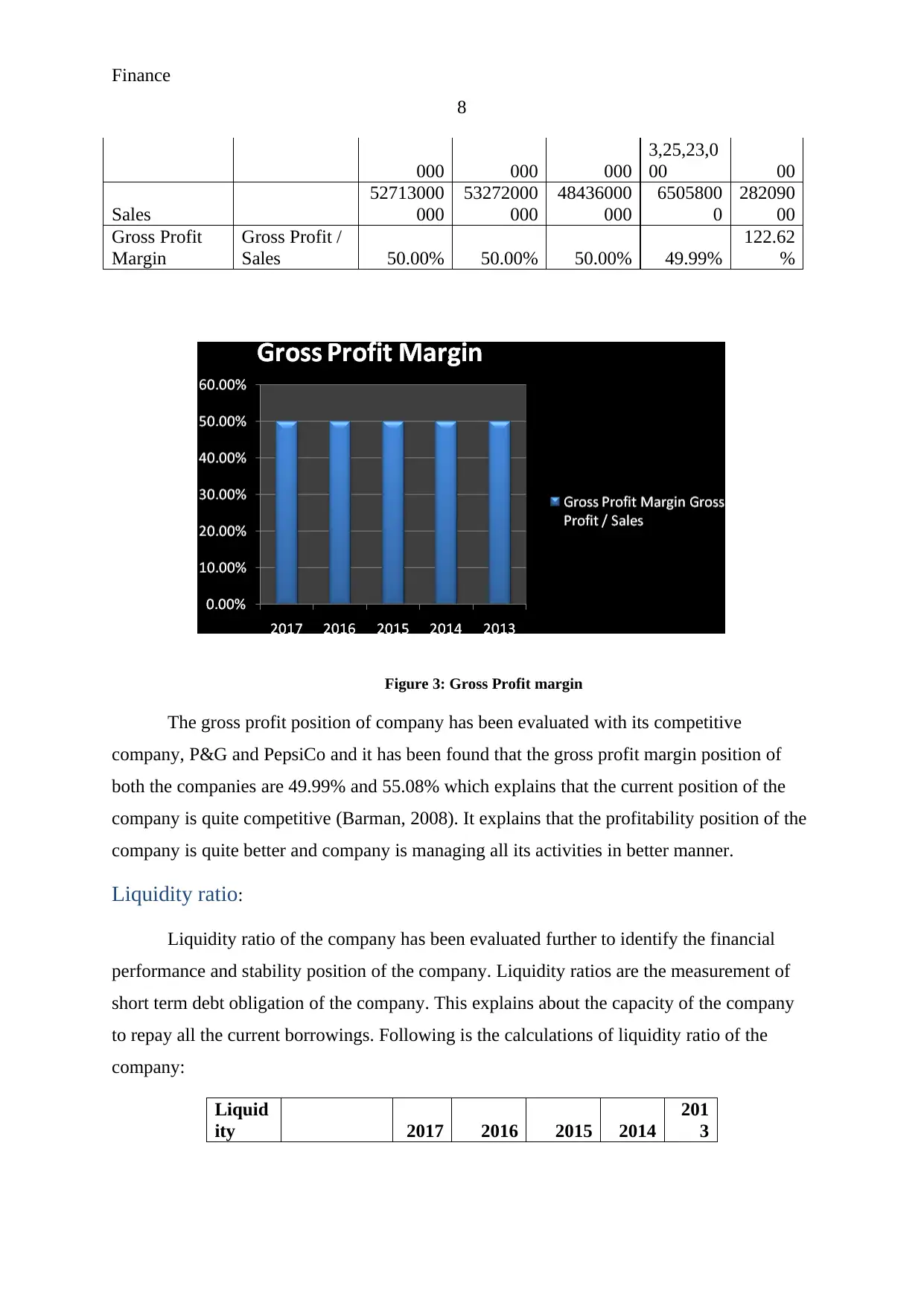

Gross profit margin:

Gross profit margin ratios explain about the total return which could be got by the

company after its cost of goods sold. It is calculated on the basis of gross profit and the total

revenue of the company (Brealey, Myers and Marcus, 2007). The current gross profit margin

ratio explains that the current gross profit position of the company is quite similar from last

few years. It explains that the operating profit margin of the company is 50% from last 3

years.

Description Formula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Gross profit 26356500 26636000 24218000 345900

7

000

Operating

profit margin

Operating net

profit / Sales 100.00% 100.00% 100.00% 21.45% 34.69%

Figure 2: Operating profit margin

The operating profit position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the operating profit margin position

of both the companies are 21.45% and 15.58% which explains that the current position of the

company is quite competitive and quite higher than all the competitive companies. It explains

that the profitability position of the company is quite better.

Gross profit margin:

Gross profit margin ratios explain about the total return which could be got by the

company after its cost of goods sold. It is calculated on the basis of gross profit and the total

revenue of the company (Brealey, Myers and Marcus, 2007). The current gross profit margin

ratio explains that the current gross profit position of the company is quite similar from last

few years. It explains that the operating profit margin of the company is 50% from last 3

years.

Description Formula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Gross profit 26356500 26636000 24218000 345900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

8

000 000 000

3,25,23,0

00 00

Sales

52713000

000

53272000

000

48436000

000

6505800

0

282090

00

Gross Profit

Margin

Gross Profit /

Sales 50.00% 50.00% 50.00% 49.99%

122.62

%

Figure 3: Gross Profit margin

The gross profit position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the gross profit margin position of

both the companies are 49.99% and 55.08% which explains that the current position of the

company is quite competitive (Barman, 2008). It explains that the profitability position of the

company is quite better and company is managing all its activities in better manner.

Liquidity ratio:

Liquidity ratio of the company has been evaluated further to identify the financial

performance and stability position of the company. Liquidity ratios are the measurement of

short term debt obligation of the company. This explains about the capacity of the company

to repay all the current borrowings. Following is the calculations of liquidity ratio of the

company:

Liquid

ity 2017 2016 2015 2014

201

3

8

000 000 000

3,25,23,0

00 00

Sales

52713000

000

53272000

000

48436000

000

6505800

0

282090

00

Gross Profit

Margin

Gross Profit /

Sales 50.00% 50.00% 50.00% 49.99%

122.62

%

Figure 3: Gross Profit margin

The gross profit position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the gross profit margin position of

both the companies are 49.99% and 55.08% which explains that the current position of the

company is quite competitive (Barman, 2008). It explains that the profitability position of the

company is quite better and company is managing all its activities in better manner.

Liquidity ratio:

Liquidity ratio of the company has been evaluated further to identify the financial

performance and stability position of the company. Liquidity ratios are the measurement of

short term debt obligation of the company. This explains about the capacity of the company

to repay all the current borrowings. Following is the calculations of liquidity ratio of the

company:

Liquid

ity 2017 2016 2015 2014

201

3

Finance

9

Current

ratio

Current

assets/curre

nt liabilities 0.68 0.63 0.63 0.70 0.77

Acid

test

ratios

Current

assets-

Inventory/cu

rrent

liabilities 0.47 0.63 0.63 0.47 0.49

(Morningstar, 2018)

Current ratio:

Current ratios explain about the total stability position and debt obligation position of

the company. It is calculated on the basis of current assets and the current liabilities of the

company. The current liquidity ratio explains that the current liquidity position of the

company is 0.68 which is higher than 0.63 and 0.63 in 2016 and 2015. It explains that the

assets level has been improved by the company.

Description Formula Unilever P&G

Pepsi

Co

2017 2016 2015 2017 2017

Current

Assets

1388400

0000

1268600

0000

1234700

0000

2,64,94,

000

27089

000

Current

Liabilities

2055600

0000

2001900

0000

1964200

0000

3,02,10,

000

21135

000

Current

ratio

Current

assets/current

liabilities 67.54% 63.37% 62.86% 87.70%

128.1

7%

(Bradford, Chen and Zhu, 2013)

9

Current

ratio

Current

assets/curre

nt liabilities 0.68 0.63 0.63 0.70 0.77

Acid

test

ratios

Current

assets-

Inventory/cu

rrent

liabilities 0.47 0.63 0.63 0.47 0.49

(Morningstar, 2018)

Current ratio:

Current ratios explain about the total stability position and debt obligation position of

the company. It is calculated on the basis of current assets and the current liabilities of the

company. The current liquidity ratio explains that the current liquidity position of the

company is 0.68 which is higher than 0.63 and 0.63 in 2016 and 2015. It explains that the

assets level has been improved by the company.

Description Formula Unilever P&G

Pepsi

Co

2017 2016 2015 2017 2017

Current

Assets

1388400

0000

1268600

0000

1234700

0000

2,64,94,

000

27089

000

Current

Liabilities

2055600

0000

2001900

0000

1964200

0000

3,02,10,

000

21135

000

Current

ratio

Current

assets/current

liabilities 67.54% 63.37% 62.86% 87.70%

128.1

7%

(Bradford, Chen and Zhu, 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

10

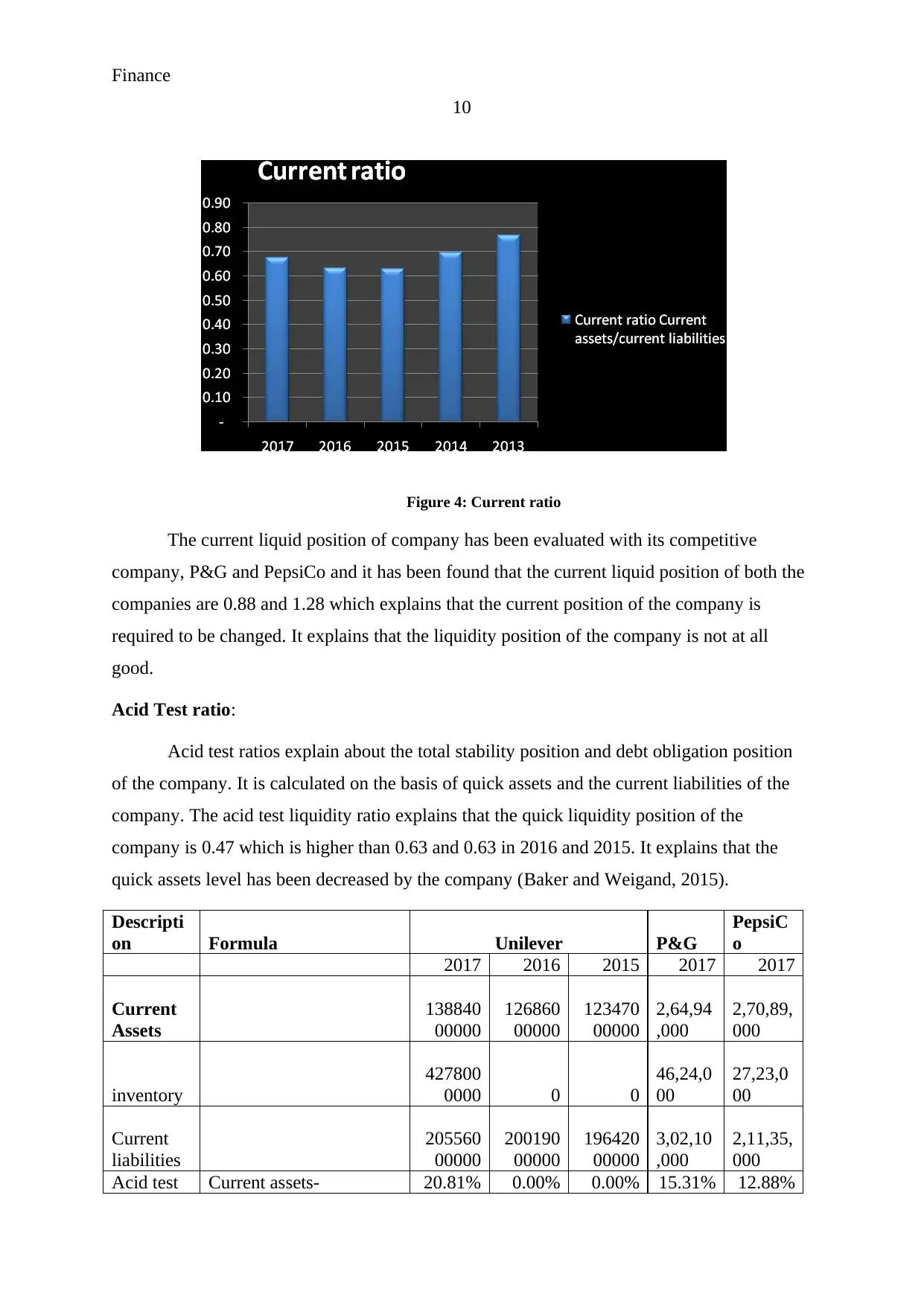

Figure 4: Current ratio

The current liquid position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the current liquid position of both the

companies are 0.88 and 1.28 which explains that the current position of the company is

required to be changed. It explains that the liquidity position of the company is not at all

good.

Acid Test ratio:

Acid test ratios explain about the total stability position and debt obligation position

of the company. It is calculated on the basis of quick assets and the current liabilities of the

company. The acid test liquidity ratio explains that the quick liquidity position of the

company is 0.47 which is higher than 0.63 and 0.63 in 2016 and 2015. It explains that the

quick assets level has been decreased by the company (Baker and Weigand, 2015).

Descripti

on Formula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Current

Assets

138840

00000

126860

00000

123470

00000

2,64,94

,000

2,70,89,

000

inventory

427800

0000 0 0

46,24,0

00

27,23,0

00

Current

liabilities

205560

00000

200190

00000

196420

00000

3,02,10

,000

2,11,35,

000

Acid test Current assets- 20.81% 0.00% 0.00% 15.31% 12.88%

10

Figure 4: Current ratio

The current liquid position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the current liquid position of both the

companies are 0.88 and 1.28 which explains that the current position of the company is

required to be changed. It explains that the liquidity position of the company is not at all

good.

Acid Test ratio:

Acid test ratios explain about the total stability position and debt obligation position

of the company. It is calculated on the basis of quick assets and the current liabilities of the

company. The acid test liquidity ratio explains that the quick liquidity position of the

company is 0.47 which is higher than 0.63 and 0.63 in 2016 and 2015. It explains that the

quick assets level has been decreased by the company (Baker and Weigand, 2015).

Descripti

on Formula Unilever P&G

PepsiC

o

2017 2016 2015 2017 2017

Current

Assets

138840

00000

126860

00000

123470

00000

2,64,94

,000

2,70,89,

000

inventory

427800

0000 0 0

46,24,0

00

27,23,0

00

Current

liabilities

205560

00000

200190

00000

196420

00000

3,02,10

,000

2,11,35,

000

Acid test Current assets- 20.81% 0.00% 0.00% 15.31% 12.88%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

11

ratios

Inventory/current

liabilities

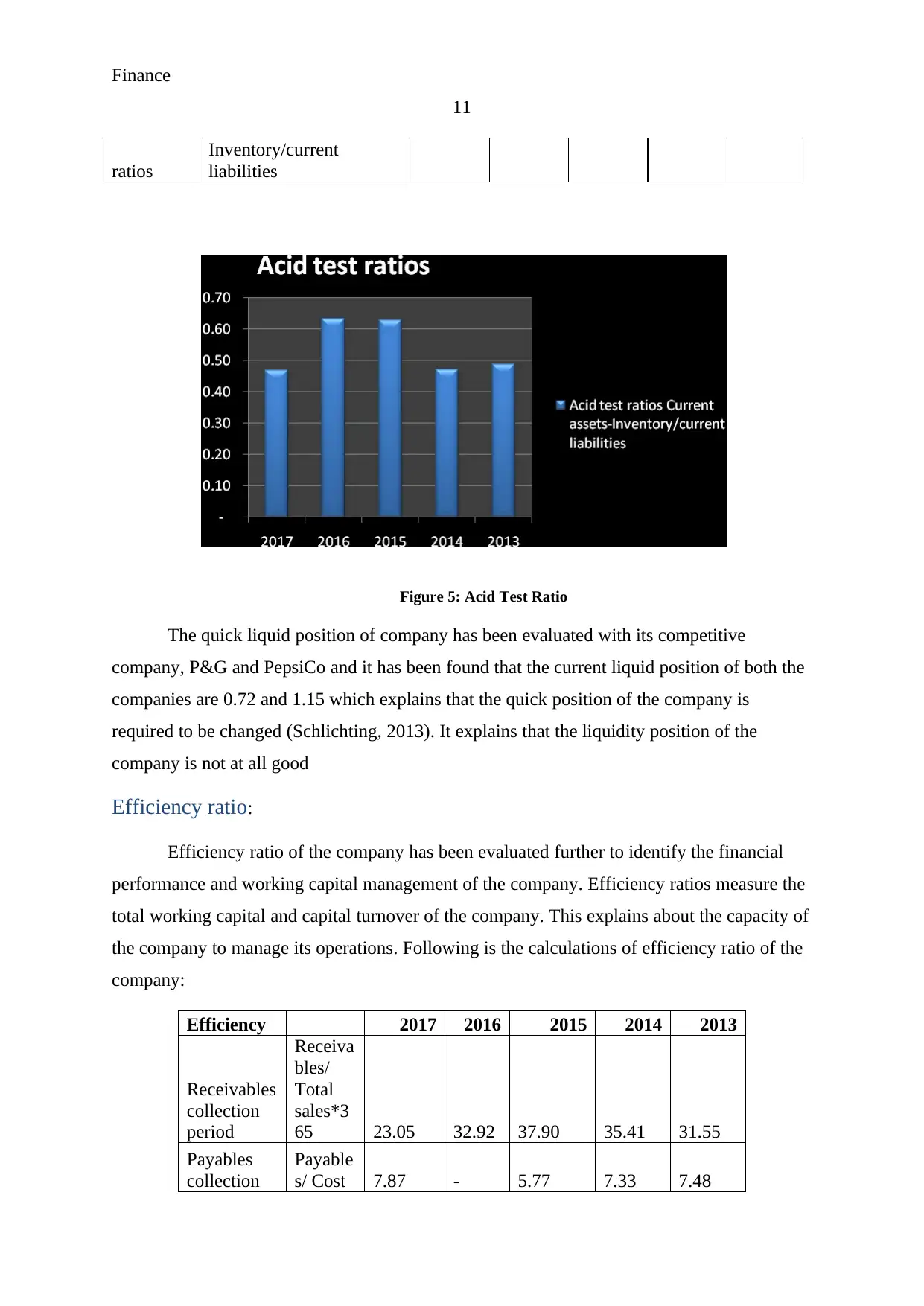

Figure 5: Acid Test Ratio

The quick liquid position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the current liquid position of both the

companies are 0.72 and 1.15 which explains that the quick position of the company is

required to be changed (Schlichting, 2013). It explains that the liquidity position of the

company is not at all good

Efficiency ratio:

Efficiency ratio of the company has been evaluated further to identify the financial

performance and working capital management of the company. Efficiency ratios measure the

total working capital and capital turnover of the company. This explains about the capacity of

the company to manage its operations. Following is the calculations of efficiency ratio of the

company:

Efficiency 2017 2016 2015 2014 2013

Receivables

collection

period

Receiva

bles/

Total

sales*3

65 23.05 32.92 37.90 35.41 31.55

Payables

collection

Payable

s/ Cost 7.87 - 5.77 7.33 7.48

11

ratios

Inventory/current

liabilities

Figure 5: Acid Test Ratio

The quick liquid position of company has been evaluated with its competitive

company, P&G and PepsiCo and it has been found that the current liquid position of both the

companies are 0.72 and 1.15 which explains that the quick position of the company is

required to be changed (Schlichting, 2013). It explains that the liquidity position of the

company is not at all good

Efficiency ratio:

Efficiency ratio of the company has been evaluated further to identify the financial

performance and working capital management of the company. Efficiency ratios measure the

total working capital and capital turnover of the company. This explains about the capacity of

the company to manage its operations. Following is the calculations of efficiency ratio of the

company:

Efficiency 2017 2016 2015 2014 2013

Receivables

collection

period

Receiva

bles/

Total

sales*3

65 23.05 32.92 37.90 35.41 31.55

Payables

collection

Payable

s/ Cost 7.87 - 5.77 7.33 7.48

Finance

12

period

of

sales*3

65

Inventory

days

Invento

ry/ cost

of

goods

sold

*365 59.24 - - 57.71 63.09

.

Receivable collection period:

Receivable collection period is calculated on the total accounting receivable and the

total sales of the company. The receivable collection period ratio explains that the collection

period of the company is 23.05 days which is lower than 32.92 days and 37.90 days in 2016

and 2015. Further, the collection period of P&G and PepsiCo is 25.77 days and 33.18 days. It

explains that cash turnover of the company is lower and explains that less cash is required for

the company to invest for daily activities (Phillips and Stawarski, 2016).

Description Formula Unilever P&G

Pepsi

Co

2017 2016 2015 2017 2017

Receivable

332900

0000

480400

0000

502900

0000

45,94,0

00

57090

00

Total Sales

527130

00000

532720

00000

484360

00000

650580

00

28209

000

Receivables

collection period

Receivables/

Total sales*365 23.05 32.92 37.90 25.77 33.18

12

period

of

sales*3

65

Inventory

days

Invento

ry/ cost

of

goods

sold

*365 59.24 - - 57.71 63.09

.

Receivable collection period:

Receivable collection period is calculated on the total accounting receivable and the

total sales of the company. The receivable collection period ratio explains that the collection

period of the company is 23.05 days which is lower than 32.92 days and 37.90 days in 2016

and 2015. Further, the collection period of P&G and PepsiCo is 25.77 days and 33.18 days. It

explains that cash turnover of the company is lower and explains that less cash is required for

the company to invest for daily activities (Phillips and Stawarski, 2016).

Description Formula Unilever P&G

Pepsi

Co

2017 2016 2015 2017 2017

Receivable

332900

0000

480400

0000

502900

0000

45,94,0

00

57090

00

Total Sales

527130

00000

532720

00000

484360

00000

650580

00

28209

000

Receivables

collection period

Receivables/

Total sales*365 23.05 32.92 37.90 25.77 33.18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.