Financial Accounting and its Purposes

22 Pages3990 Words32 Views

Added on 2023-01-06

About This Document

This document provides an overview of financial accounting and its purposes. It explains the stakeholders of a large organization and provides insights into the journal entries and ledger accounts for a sole trader. The document also covers topics such as financial statements, double-entry bookkeeping, and underlying principles of financial accounting.

Financial Accounting and its Purposes

Added on 2023-01-06

ShareRelated Documents

Financial Accounting

1

1

Table of Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Financial Accounting and its purposes...................................................................................3

Stakeholders of a large organisation.......................................................................................6

Part B...............................................................................................................................................7

Client 1...................................................................................................................................7

Client 2.................................................................................................................................16

Client 3.................................................................................................................................17

Client 4.................................................................................................................................18

Client 5.................................................................................................................................19

Conclusion.....................................................................................................................................20

References......................................................................................................................................21

2

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Financial Accounting and its purposes...................................................................................3

Stakeholders of a large organisation.......................................................................................6

Part B...............................................................................................................................................7

Client 1...................................................................................................................................7

Client 2.................................................................................................................................16

Client 3.................................................................................................................................17

Client 4.................................................................................................................................18

Client 5.................................................................................................................................19

Conclusion.....................................................................................................................................20

References......................................................................................................................................21

2

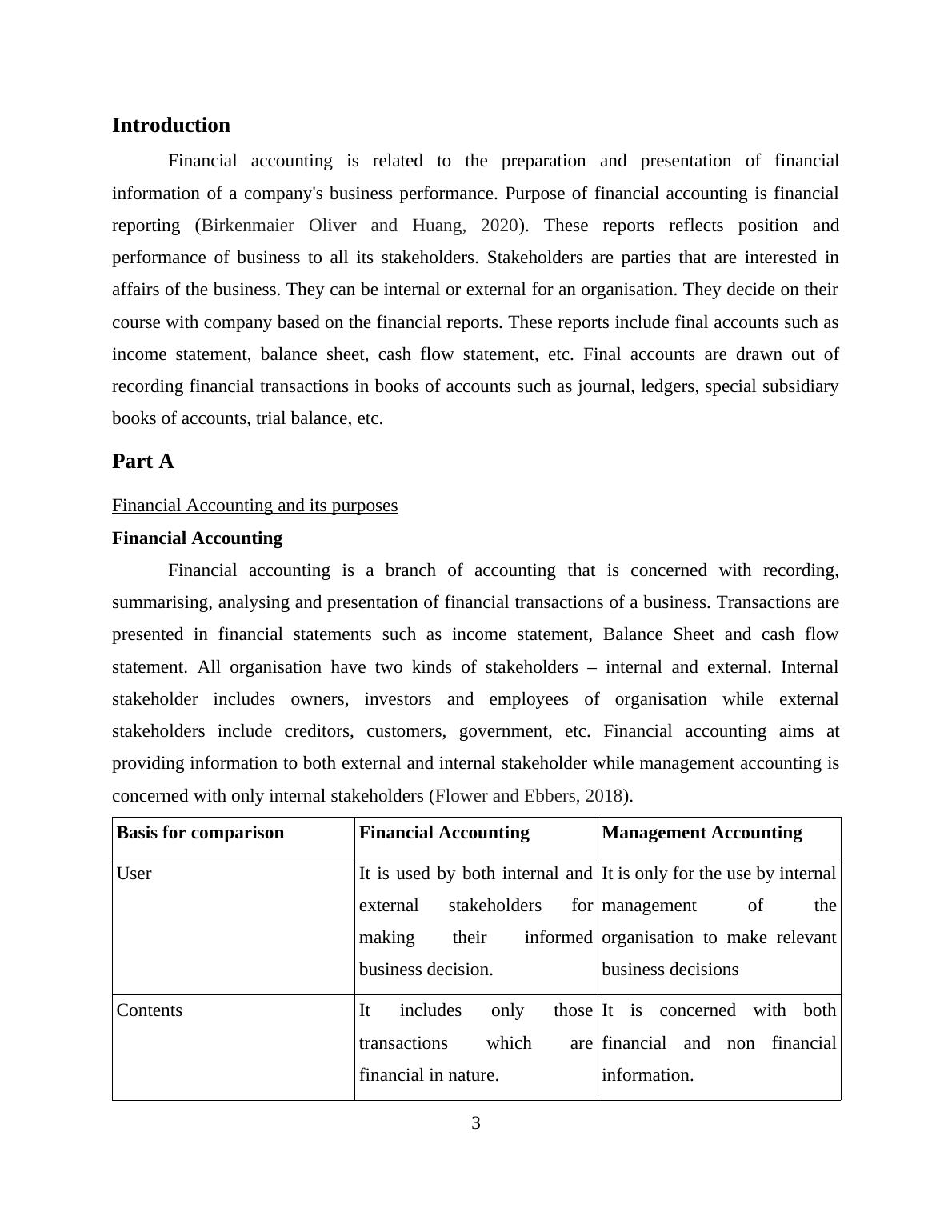

Introduction

Financial accounting is related to the preparation and presentation of financial

information of a company's business performance. Purpose of financial accounting is financial

reporting (Birkenmaier Oliver and Huang, 2020). These reports reflects position and

performance of business to all its stakeholders. Stakeholders are parties that are interested in

affairs of the business. They can be internal or external for an organisation. They decide on their

course with company based on the financial reports. These reports include final accounts such as

income statement, balance sheet, cash flow statement, etc. Final accounts are drawn out of

recording financial transactions in books of accounts such as journal, ledgers, special subsidiary

books of accounts, trial balance, etc.

Part A

Financial Accounting and its purposes

Financial Accounting

Financial accounting is a branch of accounting that is concerned with recording,

summarising, analysing and presentation of financial transactions of a business. Transactions are

presented in financial statements such as income statement, Balance Sheet and cash flow

statement. All organisation have two kinds of stakeholders – internal and external. Internal

stakeholder includes owners, investors and employees of organisation while external

stakeholders include creditors, customers, government, etc. Financial accounting aims at

providing information to both external and internal stakeholder while management accounting is

concerned with only internal stakeholders (Flower and Ebbers, 2018).

Basis for comparison Financial Accounting Management Accounting

User It is used by both internal and

external stakeholders for

making their informed

business decision.

It is only for the use by internal

management of the

organisation to make relevant

business decisions

Contents It includes only those

transactions which are

financial in nature.

It is concerned with both

financial and non financial

information.

3

Financial accounting is related to the preparation and presentation of financial

information of a company's business performance. Purpose of financial accounting is financial

reporting (Birkenmaier Oliver and Huang, 2020). These reports reflects position and

performance of business to all its stakeholders. Stakeholders are parties that are interested in

affairs of the business. They can be internal or external for an organisation. They decide on their

course with company based on the financial reports. These reports include final accounts such as

income statement, balance sheet, cash flow statement, etc. Final accounts are drawn out of

recording financial transactions in books of accounts such as journal, ledgers, special subsidiary

books of accounts, trial balance, etc.

Part A

Financial Accounting and its purposes

Financial Accounting

Financial accounting is a branch of accounting that is concerned with recording,

summarising, analysing and presentation of financial transactions of a business. Transactions are

presented in financial statements such as income statement, Balance Sheet and cash flow

statement. All organisation have two kinds of stakeholders – internal and external. Internal

stakeholder includes owners, investors and employees of organisation while external

stakeholders include creditors, customers, government, etc. Financial accounting aims at

providing information to both external and internal stakeholder while management accounting is

concerned with only internal stakeholders (Flower and Ebbers, 2018).

Basis for comparison Financial Accounting Management Accounting

User It is used by both internal and

external stakeholders for

making their informed

business decision.

It is only for the use by internal

management of the

organisation to make relevant

business decisions

Contents It includes only those

transactions which are

financial in nature.

It is concerned with both

financial and non financial

information.

3

Regulation It is subjected to multiple laws,

rules and regulations by

different authorities and are

prepared accordingly.

It it out of all legal purviews

and is prepared according to

management directions.

Purpose of financial accounting

Purpose of financial accounting is to prepare and present proper general purpose financial

statements (Foster, 2015). It helps management knowing whether company is incurring

profits or losses, what are the major sources of expenses, position of assets, investments

and liabilities, etc. Managerial accounting then takes over. Management analyses the

information extracted.

Financial statements provide necessary information to all stakeholders. This information

aids stakeholders in making their decisions regarding their association with company. For

example - it helps shareholders in deciding whether they should continue with their

investment in the company or withdraw it. Financial statements help management in

taking decisions regarding business operations and financial well being of the company.

Financial statements have quantified data. These statements serve as a base for

comparison between different products, departments, organisations and markets in

quantitative terms.

In order to maintain uniformity in all accounts of all business organisations, financial

accounting is performed according to some general standards, rules and guidelines. International

Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP)

have been prescribed that has to be followed by organisations all over.

Financial accounts are prepared on double entry book keeping system. It says that each

transaction affects at least two accounts and thus, for every debit in an account, there is

simultaneous and equal credit in some another account (Galariotis, Rong and Spyrou, 2015).

There are two different ways of recording financial transactions – Cash and accrual basis. Under

cash basis, incomes and expenses are only recorded as and when cash is received or paid

respectively. Under accrual basis, revenue and expenses are recognised as and when they

become due, irrespective of cash treatment being met or not.

4

rules and regulations by

different authorities and are

prepared accordingly.

It it out of all legal purviews

and is prepared according to

management directions.

Purpose of financial accounting

Purpose of financial accounting is to prepare and present proper general purpose financial

statements (Foster, 2015). It helps management knowing whether company is incurring

profits or losses, what are the major sources of expenses, position of assets, investments

and liabilities, etc. Managerial accounting then takes over. Management analyses the

information extracted.

Financial statements provide necessary information to all stakeholders. This information

aids stakeholders in making their decisions regarding their association with company. For

example - it helps shareholders in deciding whether they should continue with their

investment in the company or withdraw it. Financial statements help management in

taking decisions regarding business operations and financial well being of the company.

Financial statements have quantified data. These statements serve as a base for

comparison between different products, departments, organisations and markets in

quantitative terms.

In order to maintain uniformity in all accounts of all business organisations, financial

accounting is performed according to some general standards, rules and guidelines. International

Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP)

have been prescribed that has to be followed by organisations all over.

Financial accounts are prepared on double entry book keeping system. It says that each

transaction affects at least two accounts and thus, for every debit in an account, there is

simultaneous and equal credit in some another account (Galariotis, Rong and Spyrou, 2015).

There are two different ways of recording financial transactions – Cash and accrual basis. Under

cash basis, incomes and expenses are only recorded as and when cash is received or paid

respectively. Under accrual basis, revenue and expenses are recognised as and when they

become due, irrespective of cash treatment being met or not.

4

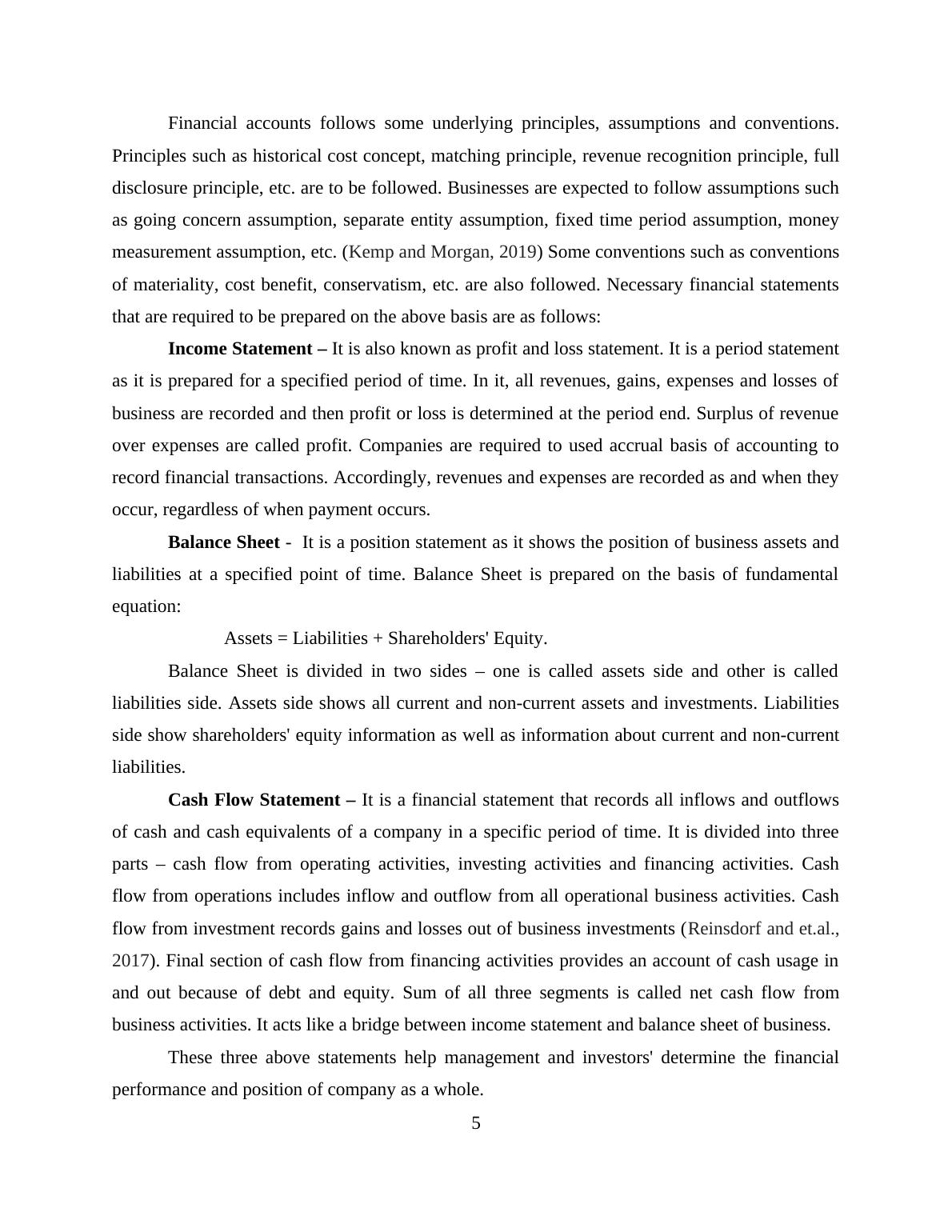

Financial accounts follows some underlying principles, assumptions and conventions.

Principles such as historical cost concept, matching principle, revenue recognition principle, full

disclosure principle, etc. are to be followed. Businesses are expected to follow assumptions such

as going concern assumption, separate entity assumption, fixed time period assumption, money

measurement assumption, etc. (Kemp and Morgan, 2019) Some conventions such as conventions

of materiality, cost benefit, conservatism, etc. are also followed. Necessary financial statements

that are required to be prepared on the above basis are as follows:

Income Statement – It is also known as profit and loss statement. It is a period statement

as it is prepared for a specified period of time. In it, all revenues, gains, expenses and losses of

business are recorded and then profit or loss is determined at the period end. Surplus of revenue

over expenses are called profit. Companies are required to used accrual basis of accounting to

record financial transactions. Accordingly, revenues and expenses are recorded as and when they

occur, regardless of when payment occurs.

Balance Sheet - It is a position statement as it shows the position of business assets and

liabilities at a specified point of time. Balance Sheet is prepared on the basis of fundamental

equation:

Assets = Liabilities + Shareholders' Equity.

Balance Sheet is divided in two sides – one is called assets side and other is called

liabilities side. Assets side shows all current and non-current assets and investments. Liabilities

side show shareholders' equity information as well as information about current and non-current

liabilities.

Cash Flow Statement – It is a financial statement that records all inflows and outflows

of cash and cash equivalents of a company in a specific period of time. It is divided into three

parts – cash flow from operating activities, investing activities and financing activities. Cash

flow from operations includes inflow and outflow from all operational business activities. Cash

flow from investment records gains and losses out of business investments (Reinsdorf and et.al.,

2017). Final section of cash flow from financing activities provides an account of cash usage in

and out because of debt and equity. Sum of all three segments is called net cash flow from

business activities. It acts like a bridge between income statement and balance sheet of business.

These three above statements help management and investors' determine the financial

performance and position of company as a whole.

5

Principles such as historical cost concept, matching principle, revenue recognition principle, full

disclosure principle, etc. are to be followed. Businesses are expected to follow assumptions such

as going concern assumption, separate entity assumption, fixed time period assumption, money

measurement assumption, etc. (Kemp and Morgan, 2019) Some conventions such as conventions

of materiality, cost benefit, conservatism, etc. are also followed. Necessary financial statements

that are required to be prepared on the above basis are as follows:

Income Statement – It is also known as profit and loss statement. It is a period statement

as it is prepared for a specified period of time. In it, all revenues, gains, expenses and losses of

business are recorded and then profit or loss is determined at the period end. Surplus of revenue

over expenses are called profit. Companies are required to used accrual basis of accounting to

record financial transactions. Accordingly, revenues and expenses are recorded as and when they

occur, regardless of when payment occurs.

Balance Sheet - It is a position statement as it shows the position of business assets and

liabilities at a specified point of time. Balance Sheet is prepared on the basis of fundamental

equation:

Assets = Liabilities + Shareholders' Equity.

Balance Sheet is divided in two sides – one is called assets side and other is called

liabilities side. Assets side shows all current and non-current assets and investments. Liabilities

side show shareholders' equity information as well as information about current and non-current

liabilities.

Cash Flow Statement – It is a financial statement that records all inflows and outflows

of cash and cash equivalents of a company in a specific period of time. It is divided into three

parts – cash flow from operating activities, investing activities and financing activities. Cash

flow from operations includes inflow and outflow from all operational business activities. Cash

flow from investment records gains and losses out of business investments (Reinsdorf and et.al.,

2017). Final section of cash flow from financing activities provides an account of cash usage in

and out because of debt and equity. Sum of all three segments is called net cash flow from

business activities. It acts like a bridge between income statement and balance sheet of business.

These three above statements help management and investors' determine the financial

performance and position of company as a whole.

5

Stakeholders of a large organisation

Stakeholder refers to any party that has a legitimate interest in the business of an

organisation. Some stakeholders have direct effect over organisation while some yield indirect

effect. Stakeholders are of two types – internal and external stakeholders.

Internal stakeholders- These are primary stakeholders which are directly involved in the

operations of a business (Shapiro and Hanouna, 2019). They get direct rewards on the success of

business. They primarily consists of employees, owners and managers of the organisation who

are directly involved in the operations of the business. Company's financial health and success is

directly co-related to primary stakeholders own personal benefits. Few internal stakeholder are

discussed below: Employees- Employees invest their time, energy and skills to run to operations of the

organisation. They also have financial stake in the company. Thus, it is important for

management to take into account employees opinions and expectations while forming

company's values, vision and mission statement.

Owners – Owners are shareholders of the organisation. All shareholders are stakeholder

of an organisation but not all stakeholders are shareholders. They have direct financial

stake in the organisation and thus are considered about every strategy and decision taken

for the organisation.

External stakeholders

These are varied sections of society that get impacted by the operations of organisation.

They need not have direct financial stake in the company but impacts business operations

indirectly (Tonkin and et.al., 2020). For example customers, creditors, government, suppliers,

etc. Management understands their responsibilities towards external stakeholders and keep in

mind to disclose necessary information relating to them when preparing and presenting financial

accounts. Few external stakeholders are discussed below: Customers – Customers are most important stakeholders of a business. They are

concerned with the price, quality and value of the product or service being provided to

them. Suppliers – Suppliers are the stakeholders that provide necessary supplies to the

organisation. Company is their customer and it relies on company for their revenue and

6

Stakeholder refers to any party that has a legitimate interest in the business of an

organisation. Some stakeholders have direct effect over organisation while some yield indirect

effect. Stakeholders are of two types – internal and external stakeholders.

Internal stakeholders- These are primary stakeholders which are directly involved in the

operations of a business (Shapiro and Hanouna, 2019). They get direct rewards on the success of

business. They primarily consists of employees, owners and managers of the organisation who

are directly involved in the operations of the business. Company's financial health and success is

directly co-related to primary stakeholders own personal benefits. Few internal stakeholder are

discussed below: Employees- Employees invest their time, energy and skills to run to operations of the

organisation. They also have financial stake in the company. Thus, it is important for

management to take into account employees opinions and expectations while forming

company's values, vision and mission statement.

Owners – Owners are shareholders of the organisation. All shareholders are stakeholder

of an organisation but not all stakeholders are shareholders. They have direct financial

stake in the organisation and thus are considered about every strategy and decision taken

for the organisation.

External stakeholders

These are varied sections of society that get impacted by the operations of organisation.

They need not have direct financial stake in the company but impacts business operations

indirectly (Tonkin and et.al., 2020). For example customers, creditors, government, suppliers,

etc. Management understands their responsibilities towards external stakeholders and keep in

mind to disclose necessary information relating to them when preparing and presenting financial

accounts. Few external stakeholders are discussed below: Customers – Customers are most important stakeholders of a business. They are

concerned with the price, quality and value of the product or service being provided to

them. Suppliers – Suppliers are the stakeholders that provide necessary supplies to the

organisation. Company is their customer and it relies on company for their revenue and

6

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting Principles Assignment Solutionlg...

|25

|4151

|240

Solved Financial Accounting : Assignmentlg...

|30

|4790

|26

Financial Accounting Principles Assignment - Airdri companylg...

|30

|6507

|439

Introduction to Financial Accounting (pdf)lg...

|25

|4847

|60

Purpose of Accounting Assignmentlg...

|18

|3334

|164

FINANCIAL ACCOUNTING PINCIPLES TABLE OF CONTENTS INTRODUCTION 4 1. Financial Accounting Principles of Munteanu Ltdlg...

|26

|5321

|460