Taxation Systems and Implications in National and International Context

VerifiedAdded on 2022/12/30

|17

|3723

|84

AI Summary

This document provides an in-depth analysis of tax systems and their implications in both national and international contexts. It discusses the taxation system of the UK, including direct and indirect taxes, as well as the tax liabilities for individuals and unincorporated organizations. It also explores the key ethical and legal constraints in tax legislations. The document offers valuable insights into the subject of taxation and its impact on various entities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

TASK 1............................................................................................................................................1

Analysing tax systems and implications in national and the international context.........................1

Taxation System of UK.............................................................................................................1

Impact of the taxation legislations............................................................................................4

Taxation liabilities for the individuals.....................................................................................4

UK self employment tax and the corporation tax...................................................................5

Comparison of the income tax of UK with Spain, France, USA and Canada......................6

TASK 2............................................................................................................................................9

Taxation Liabilities for Unincorporated organisations....................................................................9

Unincorporated Organisations.................................................................................................9

Taxation Legislations for the Unincorporated Organisations.............................................10

TASK 3..........................................................................................................................................11

Key ethical and the legal constraints in the tax legislations..........................................................11

Tax evasion and avoidance.....................................................................................................11

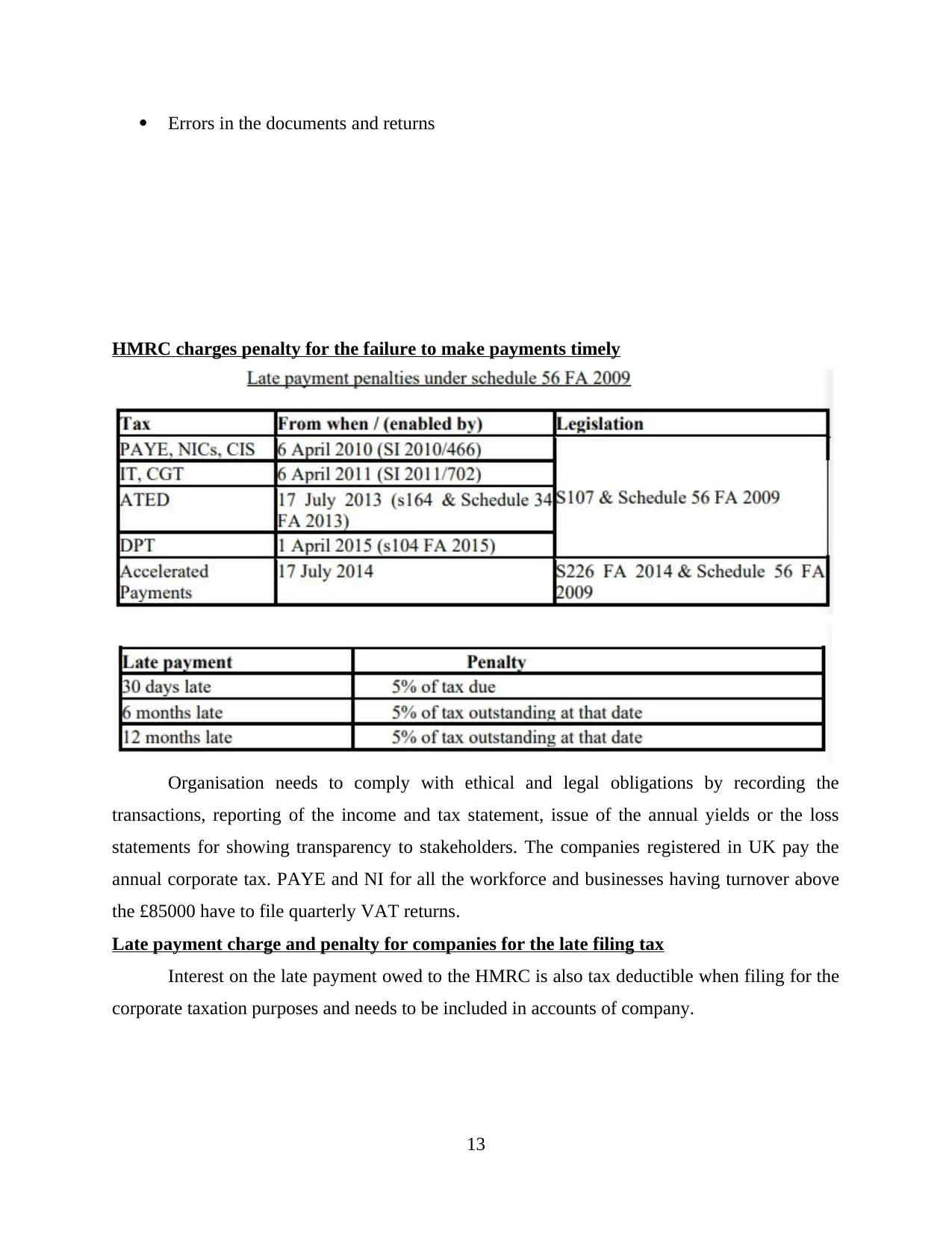

Self Assessment and the Late payment charges....................................................................12

HMRC charges penalty for the failure to make payments timely......................................13

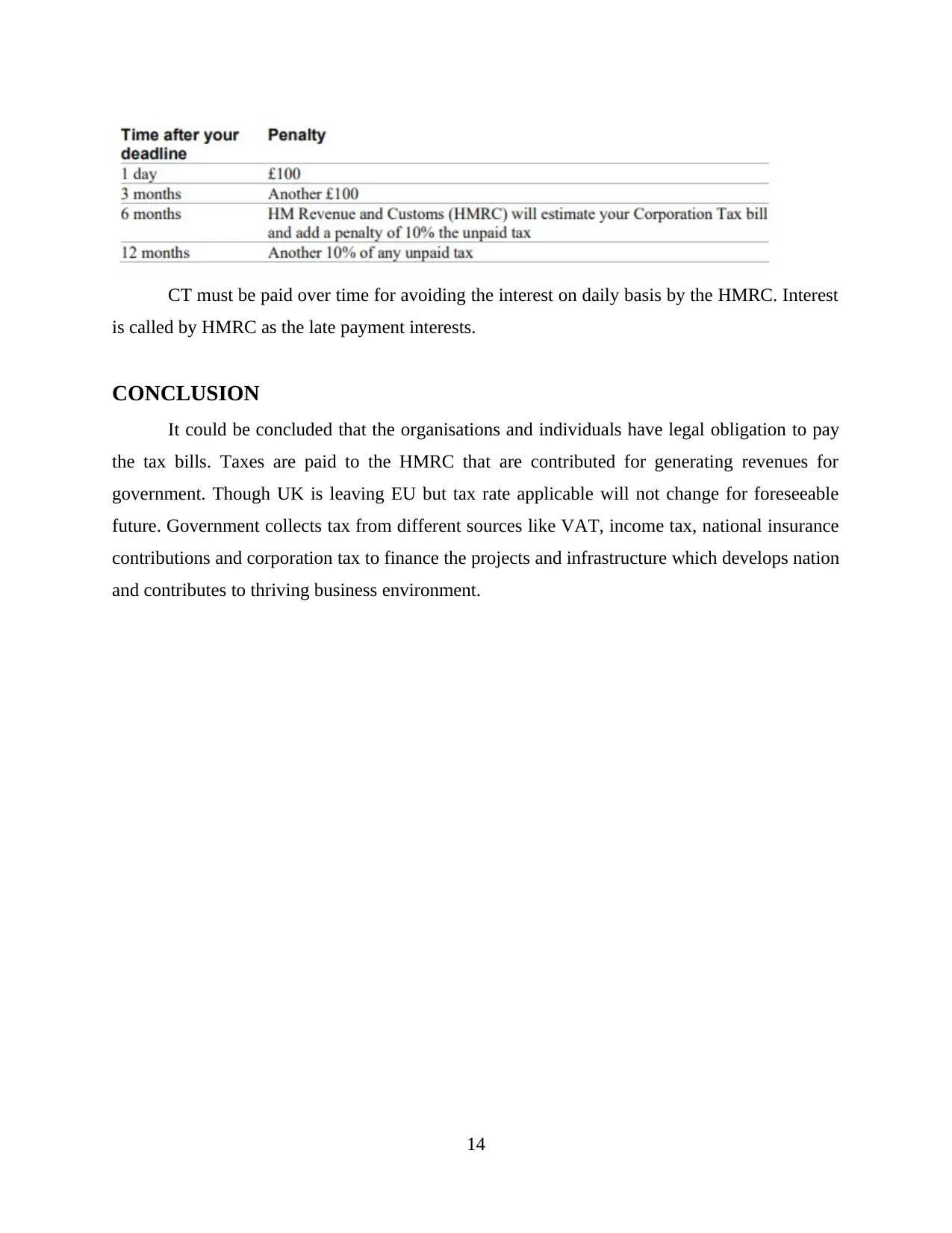

Late payment charge and penalty for companies for the late filing tax.............................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

TASK 1............................................................................................................................................1

Analysing tax systems and implications in national and the international context.........................1

Taxation System of UK.............................................................................................................1

Impact of the taxation legislations............................................................................................4

Taxation liabilities for the individuals.....................................................................................4

UK self employment tax and the corporation tax...................................................................5

Comparison of the income tax of UK with Spain, France, USA and Canada......................6

TASK 2............................................................................................................................................9

Taxation Liabilities for Unincorporated organisations....................................................................9

Unincorporated Organisations.................................................................................................9

Taxation Legislations for the Unincorporated Organisations.............................................10

TASK 3..........................................................................................................................................11

Key ethical and the legal constraints in the tax legislations..........................................................11

Tax evasion and avoidance.....................................................................................................11

Self Assessment and the Late payment charges....................................................................12

HMRC charges penalty for the failure to make payments timely......................................13

Late payment charge and penalty for companies for the late filing tax.............................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUTION

Taxation could be defined as means through which government or taxing authority levies

or imposes taxes on the citizens and the business entities of country. Taxes are levied in every of

the country of world mainly for purpose of raising revenues. It is also described as charged at a

fixed percentage over income of individual and businesses, on transactions and profits that

support government in the expenses and its revenues. In the modern economics taxation is an

important source for the government to earn revenues. Taxation differs from sources of the

revenues in which they are levied compulsorily and also unrequited which means not paid for

exchange of specific things like particular public services, sale of the public services, sale of the

public property or issue of public debt. Taxes are collected primarily for welfare of the taxpayers

as whole. Tax liability is independent of specific benefits received. Revenues raised are used for

meeting budgetary demands (Liu, 2018). It includes financing the public and government

projects and making business environment in country conducive for the economic growth. The

government projects are taken for increasing the standard of living, creation of jobs and to

increase the consumption levels. A effective taxation system helps in overall growth of country

with equal distribution of income and providing standardised public services.

Charles and Charles Strategy consultants is tax consultant and advisory firm offering

services to small and medium sized businesses. The report will reveal the national and

international taxation systems, individual and business taxation liabilities for the private and

public organisations and the unincorporated organisations. It will also discuss the legal and

ethical issues related to the taxation responsibilities at the national and international levels.

TASK 1

Analysing tax systems and implications in national and the international

context

Taxation System of UK

UK has tax system that is ruled by the taxation legislations acting over three levels of

government. It includes central, regional and local level.

The tax structure of UK is classified in two categories; Direct and Indirect tax.

Direct tax is defined as tax which is imposed directly over taxpayers and is paid to

government. An individual is not allowed to assign or pass another person for the taxes on behalf

1

Taxation could be defined as means through which government or taxing authority levies

or imposes taxes on the citizens and the business entities of country. Taxes are levied in every of

the country of world mainly for purpose of raising revenues. It is also described as charged at a

fixed percentage over income of individual and businesses, on transactions and profits that

support government in the expenses and its revenues. In the modern economics taxation is an

important source for the government to earn revenues. Taxation differs from sources of the

revenues in which they are levied compulsorily and also unrequited which means not paid for

exchange of specific things like particular public services, sale of the public services, sale of the

public property or issue of public debt. Taxes are collected primarily for welfare of the taxpayers

as whole. Tax liability is independent of specific benefits received. Revenues raised are used for

meeting budgetary demands (Liu, 2018). It includes financing the public and government

projects and making business environment in country conducive for the economic growth. The

government projects are taken for increasing the standard of living, creation of jobs and to

increase the consumption levels. A effective taxation system helps in overall growth of country

with equal distribution of income and providing standardised public services.

Charles and Charles Strategy consultants is tax consultant and advisory firm offering

services to small and medium sized businesses. The report will reveal the national and

international taxation systems, individual and business taxation liabilities for the private and

public organisations and the unincorporated organisations. It will also discuss the legal and

ethical issues related to the taxation responsibilities at the national and international levels.

TASK 1

Analysing tax systems and implications in national and the international

context

Taxation System of UK

UK has tax system that is ruled by the taxation legislations acting over three levels of

government. It includes central, regional and local level.

The tax structure of UK is classified in two categories; Direct and Indirect tax.

Direct tax is defined as tax which is imposed directly over taxpayers and is paid to

government. An individual is not allowed to assign or pass another person for the taxes on behalf

1

of individual. Direct taxes imposed mainly are Income tax which is applicable over income

earned by taxpayer or individuals. Corporate tax is applicable over profits which are earned by

the companies from business.

Indirect tax is referred as tax levied over profits, income or revenues but goods and the

services rendered by taxpayers. Indirect taxes could be shifted from one person to other. The

indirect taxes include VAT, landfill taxes, custom duties and the excise duties.

The legislations also provisions that exempt some individuals from payment of taxes when

the income is below threshold limits prescribed (Budak and James, 2018). Individuals are

exempt from tax of household income is below £11850 and corporation tax of 19% on the

earnings up to £300000.

Central Government Level

Main source of revenues for central government is Income tax, Value added tax, National

Insurance Contribution and Corporate tax.

Income tax

The individuals are required to pay income tax every year on all the earnings made

throughout the year from national and international sources. However the non residents are

charged only for their UK based income. Individual tax rate applicable is determined on the basis

of below mentioned income levels.

Tax Band Income levels Applicable tax rate

Personal Allowances 0 - £12,500 Nil

Basic tax rate £12,501 - £50,000 20%

Higher tax rate £50,001 - £150,000 40%

Additional tax rate Above £150,001 45%

National Insurance Contribution

It is the fundamental component of welfare state of UK. It is considered as social security as

payment of the contribution establishes entitlement to the certain benefits from state to the

workers and families like Maternity allowance and State Pension. In UK individuals start paying

NIC from age of sixteen when income earned reaches certain level. Self employed individual has

to make contributions on profits above £6475 in a year. An employee has to pay NIC class 1 on

2

earned by taxpayer or individuals. Corporate tax is applicable over profits which are earned by

the companies from business.

Indirect tax is referred as tax levied over profits, income or revenues but goods and the

services rendered by taxpayers. Indirect taxes could be shifted from one person to other. The

indirect taxes include VAT, landfill taxes, custom duties and the excise duties.

The legislations also provisions that exempt some individuals from payment of taxes when

the income is below threshold limits prescribed (Budak and James, 2018). Individuals are

exempt from tax of household income is below £11850 and corporation tax of 19% on the

earnings up to £300000.

Central Government Level

Main source of revenues for central government is Income tax, Value added tax, National

Insurance Contribution and Corporate tax.

Income tax

The individuals are required to pay income tax every year on all the earnings made

throughout the year from national and international sources. However the non residents are

charged only for their UK based income. Individual tax rate applicable is determined on the basis

of below mentioned income levels.

Tax Band Income levels Applicable tax rate

Personal Allowances 0 - £12,500 Nil

Basic tax rate £12,501 - £50,000 20%

Higher tax rate £50,001 - £150,000 40%

Additional tax rate Above £150,001 45%

National Insurance Contribution

It is the fundamental component of welfare state of UK. It is considered as social security as

payment of the contribution establishes entitlement to the certain benefits from state to the

workers and families like Maternity allowance and State Pension. In UK individuals start paying

NIC from age of sixteen when income earned reaches certain level. Self employed individual has

to make contributions on profits above £6475 in a year. An employee has to pay NIC class 1 on

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the earnings. Employer is required to make the secondary contributions for 13.8% of the earning

over £166 per week. An employee has to pay:

National Insurance contributions for earning above £183 per week for the year 2020-21

12% of earnings over the limit specified and up-to £962 per week for the year 2020-21

Rate falls to 2% of earnings above £962 per week.

Value Added Tax

It is levied over sales of goods & services in UK. It is considered as consumption tax as

charged over goods bought by the people and is indirect tax collected by the businesses for

government. Standard VAT rate is 20% charged over most of the purchases (Izawa, 2018).

Reduced rate is 5% and least rate is 0%. Business having turnover above £85000 has to register

and pay VAT over goods & services which they sell and buy.

Corporation Tax

It is levied over profits made by the resident companies and over profits of the non

resident entities having permanent establishments in UK. All the limited companies are levied

for corporation tax which aligned to financial year. Tax rate could change every year and has to

be aware of rate applicable. Normal corporation tax rate is 19% for the businesses for year 2020-

21 for limited companies, foreign companies, cooperatives and unincorporated associations. All

the partners as well as executives are required to file the income tax return of their own. Business

has to register with HMRC to pay CT. It has to be done within 3 months of incorporation with

Company House. Tax has to be paid within 9 months from end of financial year and is paid in

instalments if earnings are above £ 1.5 million.

The taxes imposed as per above legislations are paid by the businesses and individuals

who files and pay tax directly where the taxes of employees are deducted at source (Ghodsi and

Webster, 2018). The government require taxes for functioning, for building good infrastructure,

maintaining competitive and god education system, providing well funded and well- staffed

health organisations and to support the citizens having lower income.

Regional Government Level

The main source of revenue for regional government is property tax and road & car tax.

Property Tax

UK has 2nd highest rates of property taxes after US. Tax revenues account for around

1/10th of the total taxes from transfer, use and ownership of property in UK. There are 2 forms of

3

over £166 per week. An employee has to pay:

National Insurance contributions for earning above £183 per week for the year 2020-21

12% of earnings over the limit specified and up-to £962 per week for the year 2020-21

Rate falls to 2% of earnings above £962 per week.

Value Added Tax

It is levied over sales of goods & services in UK. It is considered as consumption tax as

charged over goods bought by the people and is indirect tax collected by the businesses for

government. Standard VAT rate is 20% charged over most of the purchases (Izawa, 2018).

Reduced rate is 5% and least rate is 0%. Business having turnover above £85000 has to register

and pay VAT over goods & services which they sell and buy.

Corporation Tax

It is levied over profits made by the resident companies and over profits of the non

resident entities having permanent establishments in UK. All the limited companies are levied

for corporation tax which aligned to financial year. Tax rate could change every year and has to

be aware of rate applicable. Normal corporation tax rate is 19% for the businesses for year 2020-

21 for limited companies, foreign companies, cooperatives and unincorporated associations. All

the partners as well as executives are required to file the income tax return of their own. Business

has to register with HMRC to pay CT. It has to be done within 3 months of incorporation with

Company House. Tax has to be paid within 9 months from end of financial year and is paid in

instalments if earnings are above £ 1.5 million.

The taxes imposed as per above legislations are paid by the businesses and individuals

who files and pay tax directly where the taxes of employees are deducted at source (Ghodsi and

Webster, 2018). The government require taxes for functioning, for building good infrastructure,

maintaining competitive and god education system, providing well funded and well- staffed

health organisations and to support the citizens having lower income.

Regional Government Level

The main source of revenue for regional government is property tax and road & car tax.

Property Tax

UK has 2nd highest rates of property taxes after US. Tax revenues account for around

1/10th of the total taxes from transfer, use and ownership of property in UK. There are 2 forms of

3

the property tax which are Stamp Duty and Council tax. SDLT is applicable to the residential

property valued above £125000 and non residential properties purchased above £150000. Other

tax is Council Tax which is municipality tax banded like income tax. Rate is determined on

assessable value of property.

Car & Road Tax

People using roads in UK have to pay the road tax. UK. Annual flat rate for the road tax

is £150 for 2020-21. There are annual discounts alternatively for the fuelled vehicles, so owners

have to pay £140 per year (Almunia and et.al., 2020). The tax rate depends on official Co2

emission of car and type of fuel used. The payments could be broken down for managing the

costs. The tax rates increases with Co2 emissions of car.

The taxes are compulsory for avoiding the penalties and to allow the regional

governments for functioning and for providing good social services.

Local Government Level

The primary source of revenues of local authority are council tax, which are paid by the

households in the local council, and from the fines and penalties charged for the street parking,

speeding etc.

Impact of the taxation legislations

UK tax systems aim at maximising the economic revenues of country and the HMRC has

collected £627.9 billion in financial year 2018-19. Legislations make it mandatory for the

payment of taxes and the penalties are attached for late payment or non payment. Tax liabilities

describes amount owed by the individuals and organisations to HMRC, these have to be paid by

the self employed individuals, employees and businesses.

Taxation liabilities for the individuals

Individuals file own taxes to the HMRC and filing needs to comprise of income tax,

property tax, capital gain tax and the inheritance tax and also accounts for the exemptions and

deductions to individuals are entitled to.

Capital Gain Tax

It is charged over the gains on sale of capital assets. Tax is charged when the value of

asset is increased (Jones, 2016). It is not separate tax from income tax and is charged in the

annual return of income of individual. CGT is charged at following rates

Higher Rate 20% on the personal gains 28% on the residential

4

property valued above £125000 and non residential properties purchased above £150000. Other

tax is Council Tax which is municipality tax banded like income tax. Rate is determined on

assessable value of property.

Car & Road Tax

People using roads in UK have to pay the road tax. UK. Annual flat rate for the road tax

is £150 for 2020-21. There are annual discounts alternatively for the fuelled vehicles, so owners

have to pay £140 per year (Almunia and et.al., 2020). The tax rate depends on official Co2

emission of car and type of fuel used. The payments could be broken down for managing the

costs. The tax rates increases with Co2 emissions of car.

The taxes are compulsory for avoiding the penalties and to allow the regional

governments for functioning and for providing good social services.

Local Government Level

The primary source of revenues of local authority are council tax, which are paid by the

households in the local council, and from the fines and penalties charged for the street parking,

speeding etc.

Impact of the taxation legislations

UK tax systems aim at maximising the economic revenues of country and the HMRC has

collected £627.9 billion in financial year 2018-19. Legislations make it mandatory for the

payment of taxes and the penalties are attached for late payment or non payment. Tax liabilities

describes amount owed by the individuals and organisations to HMRC, these have to be paid by

the self employed individuals, employees and businesses.

Taxation liabilities for the individuals

Individuals file own taxes to the HMRC and filing needs to comprise of income tax,

property tax, capital gain tax and the inheritance tax and also accounts for the exemptions and

deductions to individuals are entitled to.

Capital Gain Tax

It is charged over the gains on sale of capital assets. Tax is charged when the value of

asset is increased (Jones, 2016). It is not separate tax from income tax and is charged in the

annual return of income of individual. CGT is charged at following rates

Higher Rate 20% on the personal gains 28% on the residential

4

property

Normal Rate 10% on the personal gains 18% on the residential

property

Property tax is charged on value of property inclusive of land and is collected after the

annual appraisal of property value.

Inheritance Tax

It is collected after the individuals inherit estate from deceased person and also known as

transfer tax. It is not applicable if value of the estate is under nil rate band of £325000 or left

everything over threshold to the spouse or the civil partner or leaves everything over threshold to

the exempt beneficiary like charity (Habu, 2017). If value of estate is over nil rate band

(£325000), then part of estate may be liable to tax at 40%

UK self employment tax and the corporation tax

Tax rate band is same for the self employed individuals as the employees but they have

responsibility to file their taxes to the HMRC and corporation tax of company. They do not have

same rate.

Similarly the Corporation tax rules and rates are same for the resident and non resident

companies in UK. The resident companies have to pay tax over income earned from anywhere in

the world.

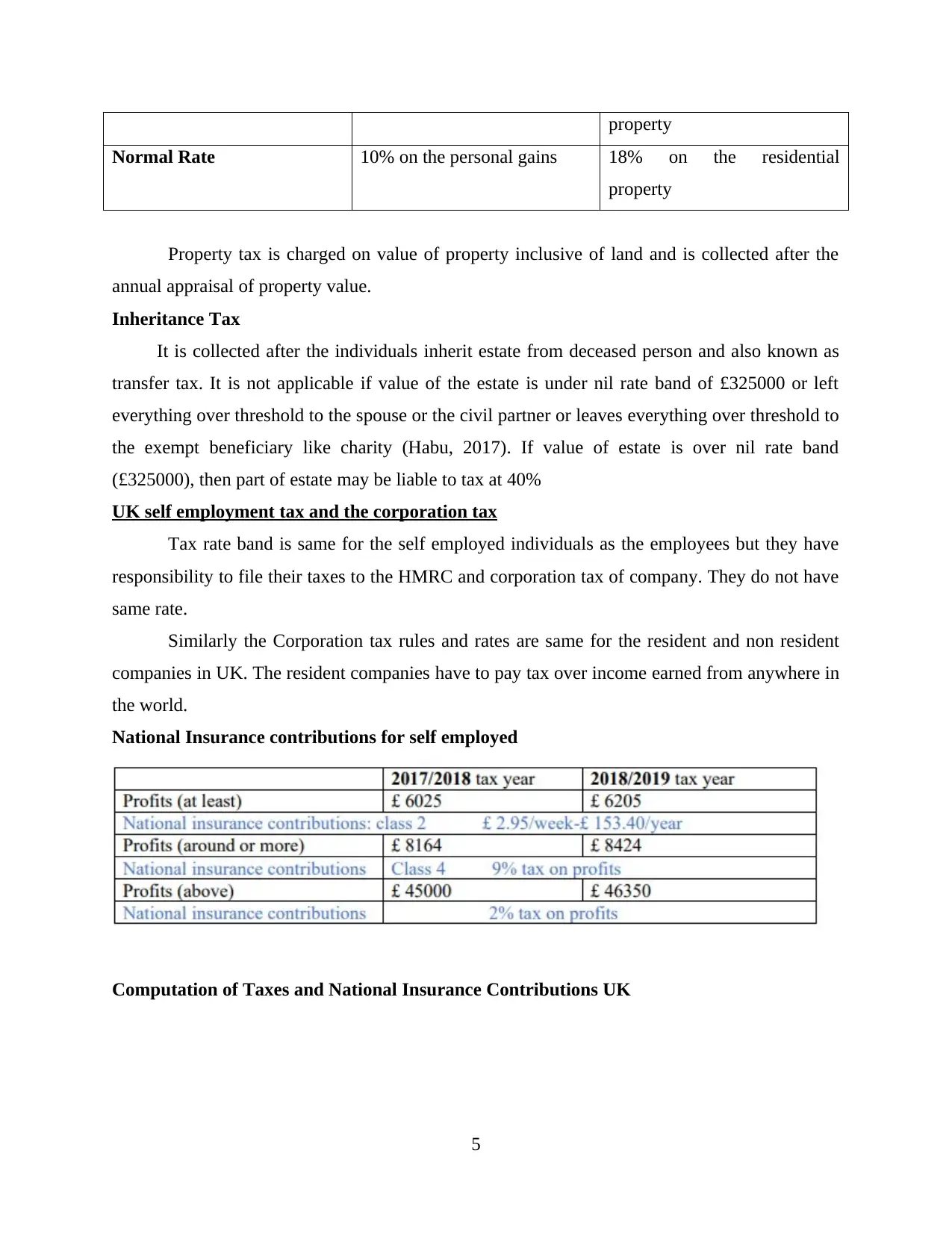

National Insurance contributions for self employed

Computation of Taxes and National Insurance Contributions UK

5

Normal Rate 10% on the personal gains 18% on the residential

property

Property tax is charged on value of property inclusive of land and is collected after the

annual appraisal of property value.

Inheritance Tax

It is collected after the individuals inherit estate from deceased person and also known as

transfer tax. It is not applicable if value of the estate is under nil rate band of £325000 or left

everything over threshold to the spouse or the civil partner or leaves everything over threshold to

the exempt beneficiary like charity (Habu, 2017). If value of estate is over nil rate band

(£325000), then part of estate may be liable to tax at 40%

UK self employment tax and the corporation tax

Tax rate band is same for the self employed individuals as the employees but they have

responsibility to file their taxes to the HMRC and corporation tax of company. They do not have

same rate.

Similarly the Corporation tax rules and rates are same for the resident and non resident

companies in UK. The resident companies have to pay tax over income earned from anywhere in

the world.

National Insurance contributions for self employed

Computation of Taxes and National Insurance Contributions UK

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Legislations in UK highly influence the tax system as there are business friendly rules and

laws that lead to booming business environment that thrives start- ups, small businesses and

funds for the big corporate.

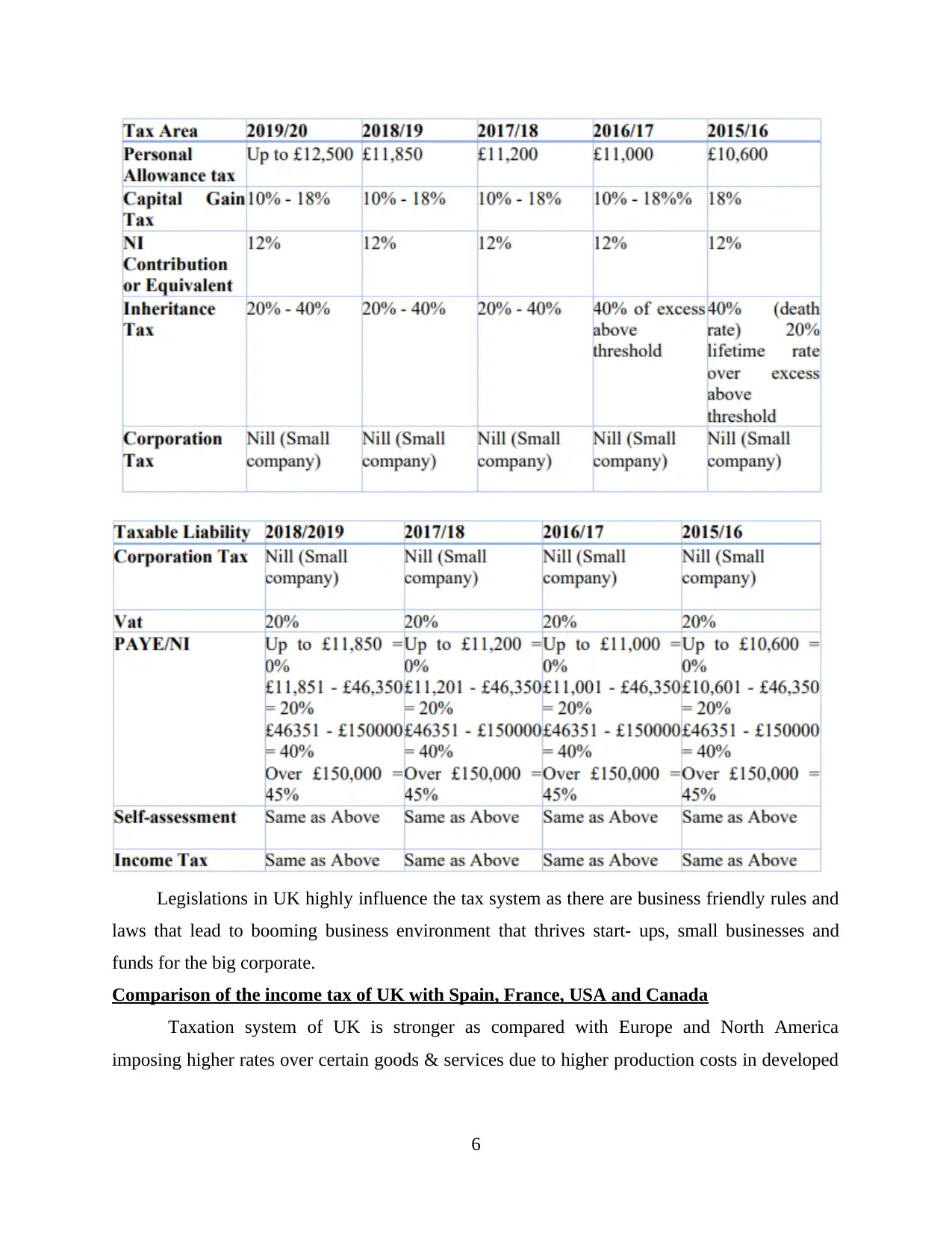

Comparison of the income tax of UK with Spain, France, USA and Canada

Taxation system of UK is stronger as compared with Europe and North America

imposing higher rates over certain goods & services due to higher production costs in developed

6

laws that lead to booming business environment that thrives start- ups, small businesses and

funds for the big corporate.

Comparison of the income tax of UK with Spain, France, USA and Canada

Taxation system of UK is stronger as compared with Europe and North America

imposing higher rates over certain goods & services due to higher production costs in developed

6

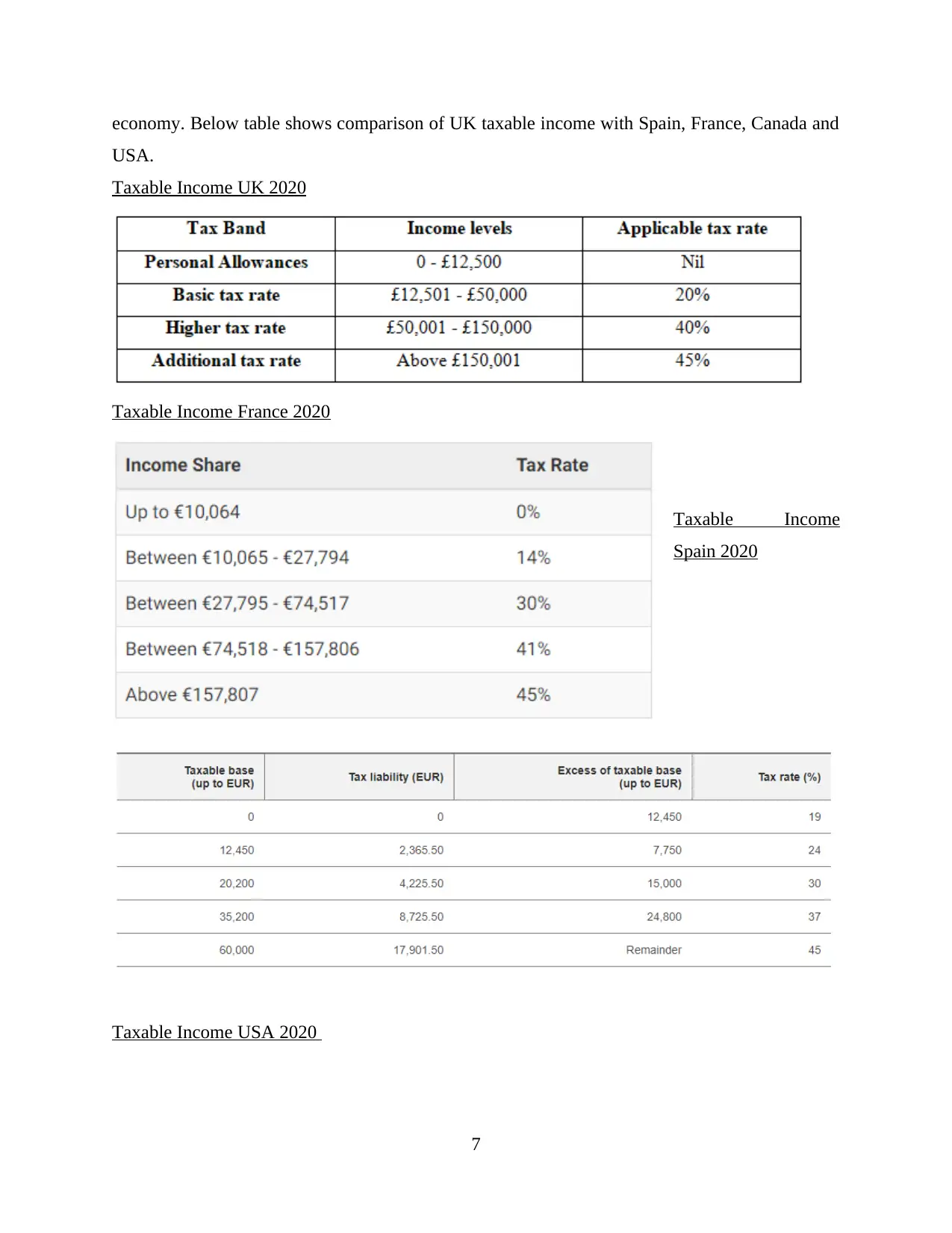

economy. Below table shows comparison of UK taxable income with Spain, France, Canada and

USA.

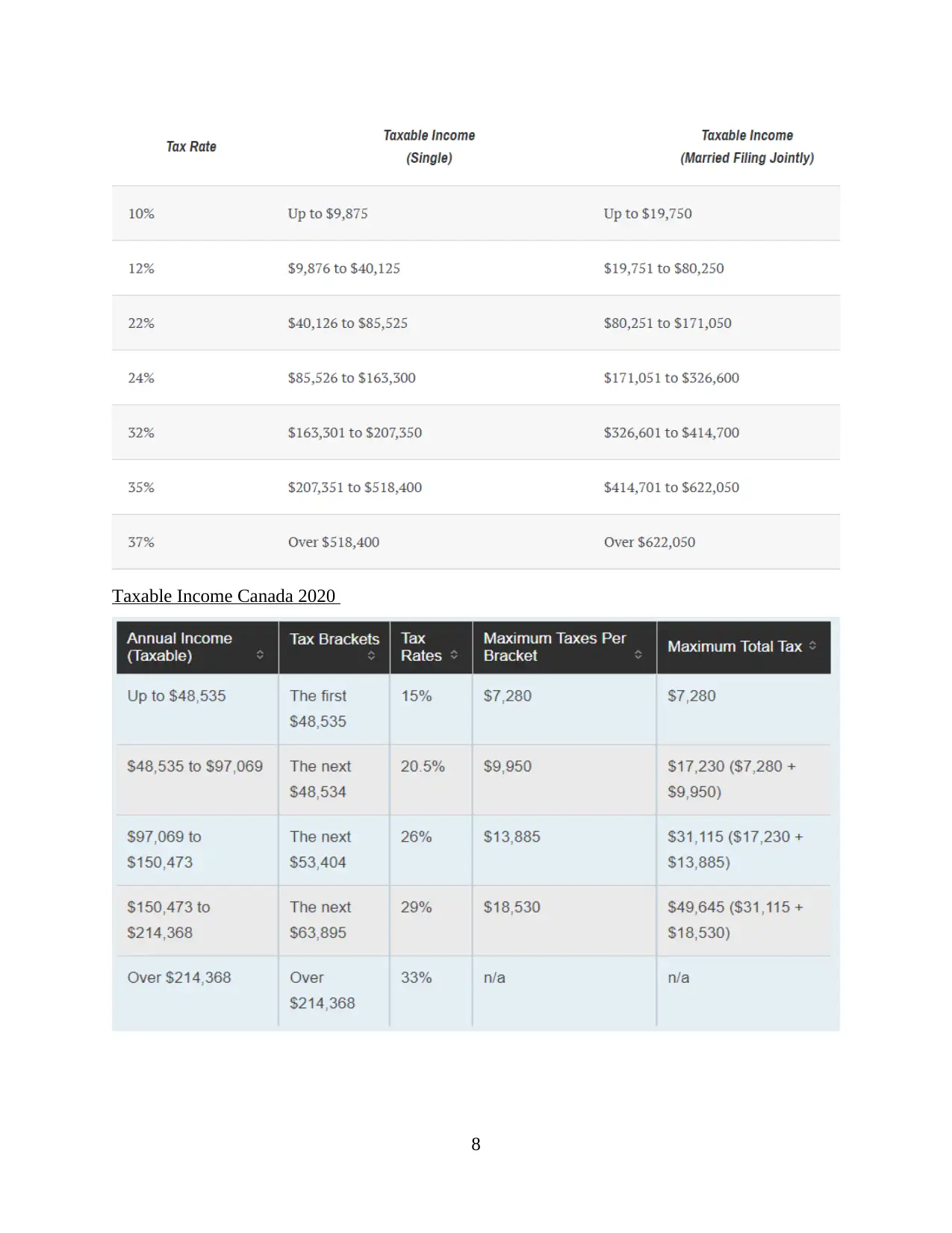

Taxable Income UK 2020

Taxable Income France 2020

Taxable Income

Spain 2020

Taxable Income USA 2020

7

USA.

Taxable Income UK 2020

Taxable Income France 2020

Taxable Income

Spain 2020

Taxable Income USA 2020

7

Taxable Income Canada 2020

8

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TASK 2

Taxation Liabilities for Unincorporated organisations

Unincorporated Organisations

They are the non profit organisations that are usually small and formed when group of

people agree over shared goals or interests to carry out the small activities for generating

revenues by selling the goods and services. These are easy to establish with limited income and

funded mainly from donations and grants. Requirements are small but members are required to

abide by the rules agreed over informal non- written constitution.

Incorporated Organisations

Private Company: Business is run and owned privately with the shareholders and stocks

but stocks could be traded over public exchange and could not be issued in IPO. Due to

this companies do not have to comply with rules and regulations of Security & Exchange

Commission. It includes: Limited liability companies, Sole proprietorship and

corporations.

Public Company: These are operated and owned by public. Shares of these companies are

freely tradable over stock exchange without restrictions (Schiavone 2020). Value of

shares is determined by daily trading in market. Examples of Public companies are GE,

HSBC Group etc.

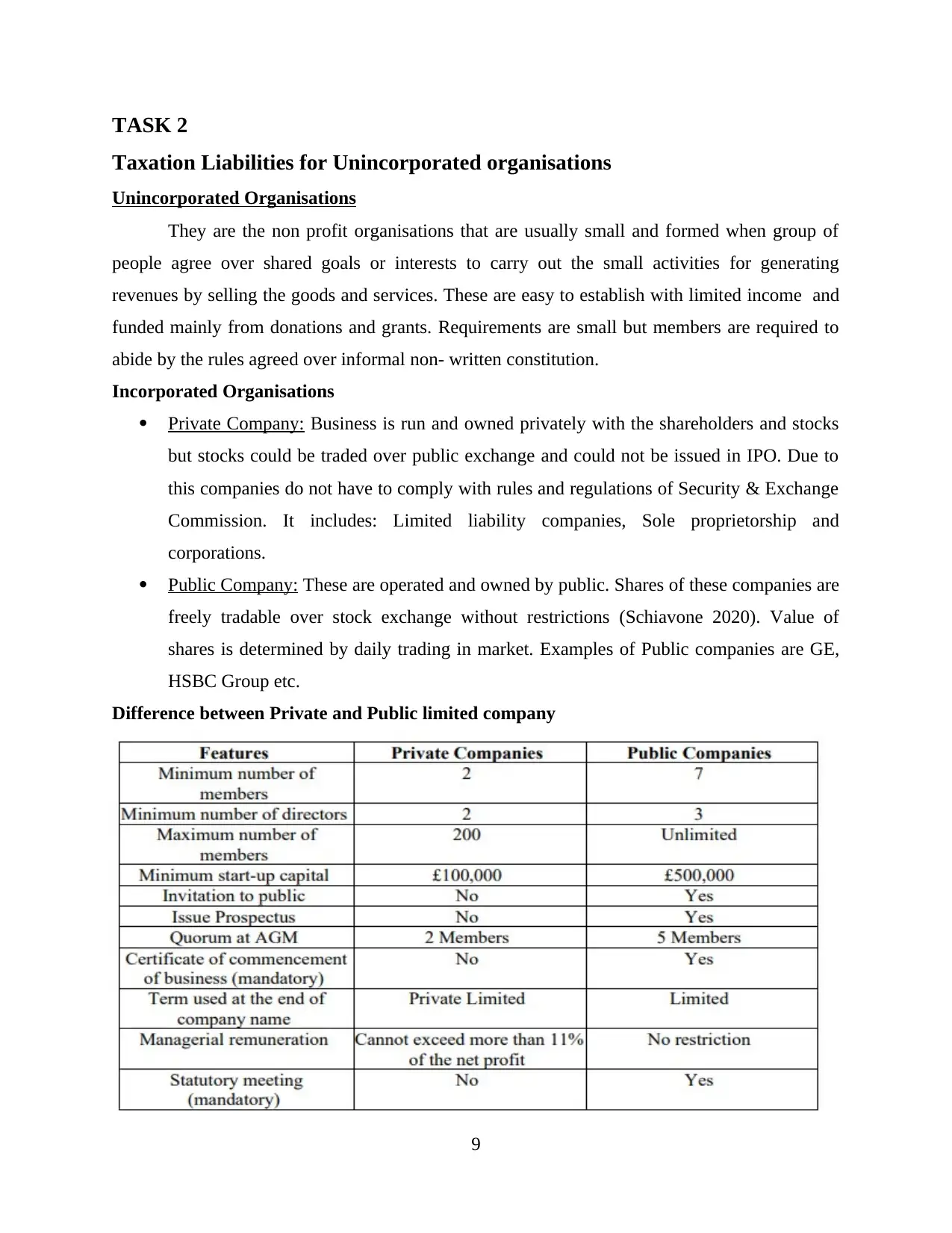

Difference between Private and Public limited company

9

Taxation Liabilities for Unincorporated organisations

Unincorporated Organisations

They are the non profit organisations that are usually small and formed when group of

people agree over shared goals or interests to carry out the small activities for generating

revenues by selling the goods and services. These are easy to establish with limited income and

funded mainly from donations and grants. Requirements are small but members are required to

abide by the rules agreed over informal non- written constitution.

Incorporated Organisations

Private Company: Business is run and owned privately with the shareholders and stocks

but stocks could be traded over public exchange and could not be issued in IPO. Due to

this companies do not have to comply with rules and regulations of Security & Exchange

Commission. It includes: Limited liability companies, Sole proprietorship and

corporations.

Public Company: These are operated and owned by public. Shares of these companies are

freely tradable over stock exchange without restrictions (Schiavone 2020). Value of

shares is determined by daily trading in market. Examples of Public companies are GE,

HSBC Group etc.

Difference between Private and Public limited company

9

Taxation Legislations for the Unincorporated Organisations

These organisations are generally exempt from the tax liabilities and are required to get

exemption certificate. They are required to pay the corporation tax on trading profits, sale of the

assets and investments sold at price higher than the cost and also Tax return to government.

Incorporated organisations are the legal entities that needs to register with the HMRC and to pay

corporation tax at 20% on annual profits, all the liabilities has to be paid in 9 months. Company

incorporated in UK has to pay taxes over all the profits earned outside and within borders of UK.

Taxation liabilities for the incorporated organisations

The incorporated companies benefits from the lower tax than the unincorporated organisations. It

has flexibility to defer the payment of corporation taxes and could also qualify for the deduction

for small businesses (Schiavone, 2020). The incorporated organisations have to file separate

corporation tax return with personal tax return and owners of unincorporated companies could

pay only one corporation return.

The public companies have legal obligations for payment of taxes accrued on annual

profits of company at 20% rate. Company has to register itself with HMRC and has to pay within

9 months and 1 day of accounting year end. They have to pay VAT charged over goods &

services. Standard rate 20%, reduced rate 5% and 0% on some goods & services is applicable.

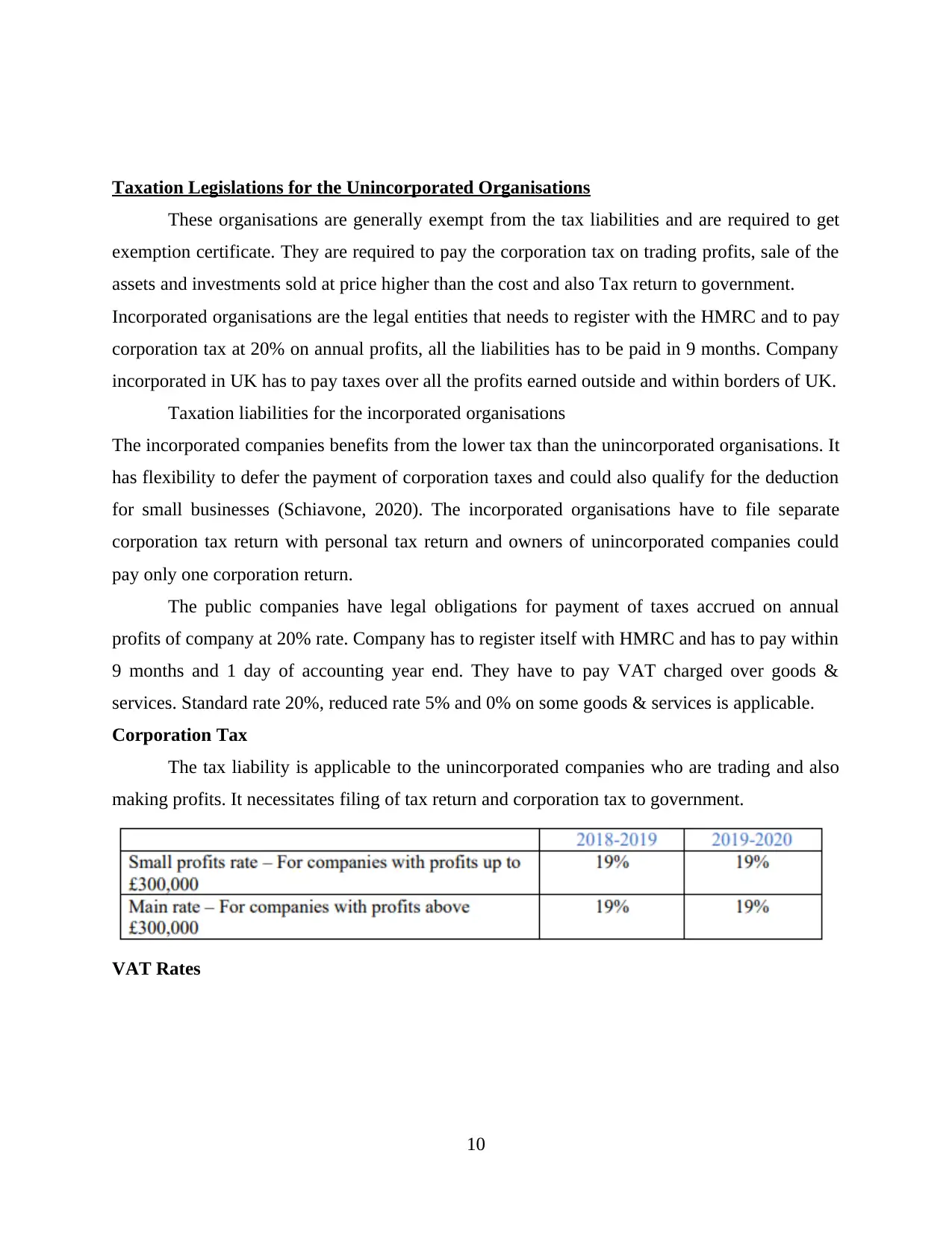

Corporation Tax

The tax liability is applicable to the unincorporated companies who are trading and also

making profits. It necessitates filing of tax return and corporation tax to government.

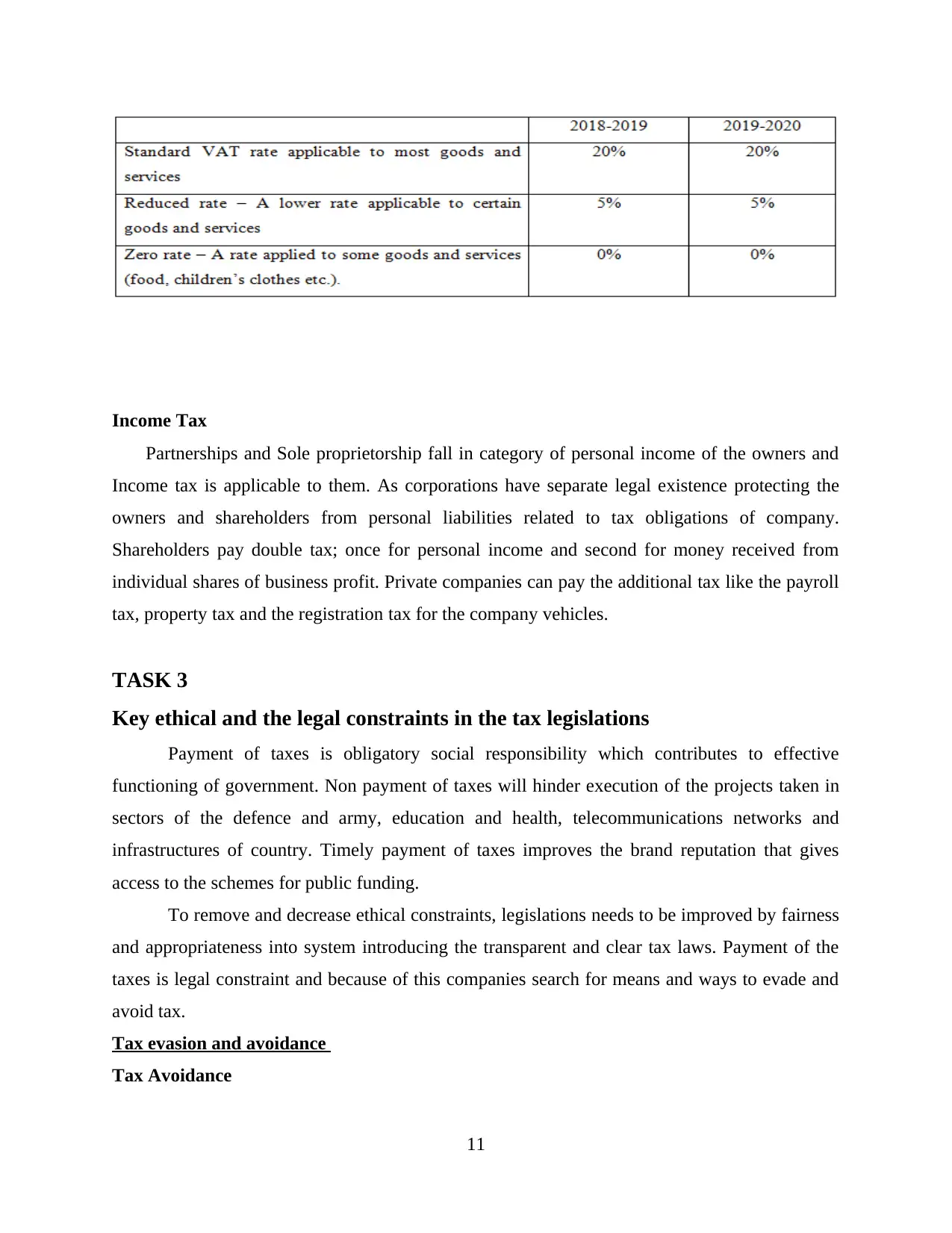

VAT Rates

10

These organisations are generally exempt from the tax liabilities and are required to get

exemption certificate. They are required to pay the corporation tax on trading profits, sale of the

assets and investments sold at price higher than the cost and also Tax return to government.

Incorporated organisations are the legal entities that needs to register with the HMRC and to pay

corporation tax at 20% on annual profits, all the liabilities has to be paid in 9 months. Company

incorporated in UK has to pay taxes over all the profits earned outside and within borders of UK.

Taxation liabilities for the incorporated organisations

The incorporated companies benefits from the lower tax than the unincorporated organisations. It

has flexibility to defer the payment of corporation taxes and could also qualify for the deduction

for small businesses (Schiavone, 2020). The incorporated organisations have to file separate

corporation tax return with personal tax return and owners of unincorporated companies could

pay only one corporation return.

The public companies have legal obligations for payment of taxes accrued on annual

profits of company at 20% rate. Company has to register itself with HMRC and has to pay within

9 months and 1 day of accounting year end. They have to pay VAT charged over goods &

services. Standard rate 20%, reduced rate 5% and 0% on some goods & services is applicable.

Corporation Tax

The tax liability is applicable to the unincorporated companies who are trading and also

making profits. It necessitates filing of tax return and corporation tax to government.

VAT Rates

10

Income Tax

Partnerships and Sole proprietorship fall in category of personal income of the owners and

Income tax is applicable to them. As corporations have separate legal existence protecting the

owners and shareholders from personal liabilities related to tax obligations of company.

Shareholders pay double tax; once for personal income and second for money received from

individual shares of business profit. Private companies can pay the additional tax like the payroll

tax, property tax and the registration tax for the company vehicles.

TASK 3

Key ethical and the legal constraints in the tax legislations

Payment of taxes is obligatory social responsibility which contributes to effective

functioning of government. Non payment of taxes will hinder execution of the projects taken in

sectors of the defence and army, education and health, telecommunications networks and

infrastructures of country. Timely payment of taxes improves the brand reputation that gives

access to the schemes for public funding.

To remove and decrease ethical constraints, legislations needs to be improved by fairness

and appropriateness into system introducing the transparent and clear tax laws. Payment of the

taxes is legal constraint and because of this companies search for means and ways to evade and

avoid tax.

Tax evasion and avoidance

Tax Avoidance

11

Partnerships and Sole proprietorship fall in category of personal income of the owners and

Income tax is applicable to them. As corporations have separate legal existence protecting the

owners and shareholders from personal liabilities related to tax obligations of company.

Shareholders pay double tax; once for personal income and second for money received from

individual shares of business profit. Private companies can pay the additional tax like the payroll

tax, property tax and the registration tax for the company vehicles.

TASK 3

Key ethical and the legal constraints in the tax legislations

Payment of taxes is obligatory social responsibility which contributes to effective

functioning of government. Non payment of taxes will hinder execution of the projects taken in

sectors of the defence and army, education and health, telecommunications networks and

infrastructures of country. Timely payment of taxes improves the brand reputation that gives

access to the schemes for public funding.

To remove and decrease ethical constraints, legislations needs to be improved by fairness

and appropriateness into system introducing the transparent and clear tax laws. Payment of the

taxes is legal constraint and because of this companies search for means and ways to evade and

avoid tax.

Tax evasion and avoidance

Tax Avoidance

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It involves use of the loopholes in tax legislations for gaining tax advantage and for

bending the rules. This is not illegal and therefore engaging in such acts is also not illegal.

Individuals could have saving accounts as means for reducing the income tax as all the savings in

ISA are not taxable. Self employed and organisations could reduce the tax bills by claiming the

expenses, using the tax deductions, by changing business structures by establishing or

incorporating headquarters in the tax heaven (Ruane and Byrne, 2020). Use of schemes resulting

in tax avoidance could lead to the penalties when found.

Tax evasion

It includes use of the illegal practices that results in avoidance of tax payment. Not

reporting all the income through hiding the taxable assets from the HMRC not filing the tax

returns or making use of offshore fake accounts. It is criminal offence which leads to the prison

sentences and being shamed and named by HMRC for avoidance of tax over 25000 that puts

stain on reputation and affects the sales.

The individuals and organisations have to comply with tax legislations in order to place

for governments for generating new functions and revenues. Effectiveness of the tax legislations

moulds business environment by the payment of taxes, businesses could be benefitted from the

public funding and the developed infrastructures helps to create trade opportunities providing

incomplete and wrong information leading to the organisational performance sufferings and risks

of prosecution for tax evasion or misreporting. Legal constraint faced by the corporations

relating to taxation includes payment of taxes over time and also reporting the profits and

incomes accurately through keeping the records of trade transactions.

Self employed individual are also required to pay the annual income tax returns and to

file return on internet before January 31st of following year (Liu and et.al., 2017). Legal

constraint forces the business to act responsibly and professionally for maintaining the cash

flows, payment of taxes, staff and the suppliers.

Self Assessment and the Late payment charges

Taxation system in UK often appears complicated relating to record keeping and correct

reporting of income, expenses and the transaction and the self assessment is responsibility of the

individual. Penalties for late filing are related to

Late payment

Failure to notify

12

bending the rules. This is not illegal and therefore engaging in such acts is also not illegal.

Individuals could have saving accounts as means for reducing the income tax as all the savings in

ISA are not taxable. Self employed and organisations could reduce the tax bills by claiming the

expenses, using the tax deductions, by changing business structures by establishing or

incorporating headquarters in the tax heaven (Ruane and Byrne, 2020). Use of schemes resulting

in tax avoidance could lead to the penalties when found.

Tax evasion

It includes use of the illegal practices that results in avoidance of tax payment. Not

reporting all the income through hiding the taxable assets from the HMRC not filing the tax

returns or making use of offshore fake accounts. It is criminal offence which leads to the prison

sentences and being shamed and named by HMRC for avoidance of tax over 25000 that puts

stain on reputation and affects the sales.

The individuals and organisations have to comply with tax legislations in order to place

for governments for generating new functions and revenues. Effectiveness of the tax legislations

moulds business environment by the payment of taxes, businesses could be benefitted from the

public funding and the developed infrastructures helps to create trade opportunities providing

incomplete and wrong information leading to the organisational performance sufferings and risks

of prosecution for tax evasion or misreporting. Legal constraint faced by the corporations

relating to taxation includes payment of taxes over time and also reporting the profits and

incomes accurately through keeping the records of trade transactions.

Self employed individual are also required to pay the annual income tax returns and to

file return on internet before January 31st of following year (Liu and et.al., 2017). Legal

constraint forces the business to act responsibly and professionally for maintaining the cash

flows, payment of taxes, staff and the suppliers.

Self Assessment and the Late payment charges

Taxation system in UK often appears complicated relating to record keeping and correct

reporting of income, expenses and the transaction and the self assessment is responsibility of the

individual. Penalties for late filing are related to

Late payment

Failure to notify

12

Errors in the documents and returns

HMRC charges penalty for the failure to make payments timely

Organisation needs to comply with ethical and legal obligations by recording the

transactions, reporting of the income and tax statement, issue of the annual yields or the loss

statements for showing transparency to stakeholders. The companies registered in UK pay the

annual corporate tax. PAYE and NI for all the workforce and businesses having turnover above

the £85000 have to file quarterly VAT returns.

Late payment charge and penalty for companies for the late filing tax

Interest on the late payment owed to the HMRC is also tax deductible when filing for the

corporate taxation purposes and needs to be included in accounts of company.

13

HMRC charges penalty for the failure to make payments timely

Organisation needs to comply with ethical and legal obligations by recording the

transactions, reporting of the income and tax statement, issue of the annual yields or the loss

statements for showing transparency to stakeholders. The companies registered in UK pay the

annual corporate tax. PAYE and NI for all the workforce and businesses having turnover above

the £85000 have to file quarterly VAT returns.

Late payment charge and penalty for companies for the late filing tax

Interest on the late payment owed to the HMRC is also tax deductible when filing for the

corporate taxation purposes and needs to be included in accounts of company.

13

CT must be paid over time for avoiding the interest on daily basis by the HMRC. Interest

is called by HMRC as the late payment interests.

CONCLUSION

It could be concluded that the organisations and individuals have legal obligation to pay

the tax bills. Taxes are paid to the HMRC that are contributed for generating revenues for

government. Though UK is leaving EU but tax rate applicable will not change for foreseeable

future. Government collects tax from different sources like VAT, income tax, national insurance

contributions and corporation tax to finance the projects and infrastructure which develops nation

and contributes to thriving business environment.

14

is called by HMRC as the late payment interests.

CONCLUSION

It could be concluded that the organisations and individuals have legal obligation to pay

the tax bills. Taxes are paid to the HMRC that are contributed for generating revenues for

government. Though UK is leaving EU but tax rate applicable will not change for foreseeable

future. Government collects tax from different sources like VAT, income tax, national insurance

contributions and corporation tax to finance the projects and infrastructure which develops nation

and contributes to thriving business environment.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Liu, L., 2018. Where does multinational investment go with territorial taxation? Evidence from

the UK.

Budak, T. and James, S.R., 2018. The level of tax complexity: A comparative analysis between

the UK and Turkey based on the OTS Index.

Izawa, R., 2018. International Double Taxation and British Investment in the United States from

the First World War to the 1945 UK-US Tax Treaty. Japanese Research in Business

History. 35. pp.125-141.

Almunia, M., and et.al., 2020. More giving or more givers? The effects of tax incentives on

charitable donations in the UK. Journal of Public Economics. 183. p.104114.

Ghodsi, Z. and Webster, A., 2018. UK Taxes and Tax Revenues: Composition and

Trends. Intech Open. 74380. pp.83-96.

Habu, K., 2017. How much tax do companies pay in the UK?.

Jones, C.M., 2016. The UK sugar tax–a healthy start?. British dental journal. 221(2). pp.59-60.

Schiavone, G., 2020. Tax aspects of UK debt financing. Novità fiscali. 2020(11). pp.721-725.

Ruane, S. and Byrne, D., 2020. Paying for the welfare state and taxation in the UK. Routledge.

Liu, L., and et.al., 2017. International Transfer Pricing and Tax Avoidance: Evidence from the

Linked Tax-Trade Statistics in the UK. Available at SSRN 3009883.

15

Books and Journals

Liu, L., 2018. Where does multinational investment go with territorial taxation? Evidence from

the UK.

Budak, T. and James, S.R., 2018. The level of tax complexity: A comparative analysis between

the UK and Turkey based on the OTS Index.

Izawa, R., 2018. International Double Taxation and British Investment in the United States from

the First World War to the 1945 UK-US Tax Treaty. Japanese Research in Business

History. 35. pp.125-141.

Almunia, M., and et.al., 2020. More giving or more givers? The effects of tax incentives on

charitable donations in the UK. Journal of Public Economics. 183. p.104114.

Ghodsi, Z. and Webster, A., 2018. UK Taxes and Tax Revenues: Composition and

Trends. Intech Open. 74380. pp.83-96.

Habu, K., 2017. How much tax do companies pay in the UK?.

Jones, C.M., 2016. The UK sugar tax–a healthy start?. British dental journal. 221(2). pp.59-60.

Schiavone, G., 2020. Tax aspects of UK debt financing. Novità fiscali. 2020(11). pp.721-725.

Ruane, S. and Byrne, D., 2020. Paying for the welfare state and taxation in the UK. Routledge.

Liu, L., and et.al., 2017. International Transfer Pricing and Tax Avoidance: Evidence from the

Linked Tax-Trade Statistics in the UK. Available at SSRN 3009883.

15

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.