Different MA Systems and Methods of MA Reporting

VerifiedAdded on 2022/12/27

|14

|3744

|33

AI Summary

This study material provides a critical evaluation of different management accounting systems and methods of reporting. It covers topics such as cost accounting system, inventory management system, job costing system, and price optimization system. It also discusses the advantages and dis...

Read More

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

UNIT-5 MANAGEMENT

ACCOUNTI NG

ACCOUNTI NG

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P-1 Critically analysing different MA systems............................................................................1

P2 Different methods of MA reporting........................................................................................3

TASK-2............................................................................................................................................4

2a..................................................................................................................................................5

2 b.....................................................................................................................................................5

2 c.....................................................................................................................................................6

TASK-3............................................................................................................................................7

P-4: Advantages and disadvantages of various planning tools used in the budgetary control....7

M-3...............................................................................................................................................9

P-5: Adaptation of the management accounting systems to respond to the financial problems..9

M-4.............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P-1 Critically analysing different MA systems............................................................................1

P2 Different methods of MA reporting........................................................................................3

TASK-2............................................................................................................................................4

2a..................................................................................................................................................5

2 b.....................................................................................................................................................5

2 c.....................................................................................................................................................6

TASK-3............................................................................................................................................7

P-4: Advantages and disadvantages of various planning tools used in the budgetary control....7

M-3...............................................................................................................................................9

P-5: Adaptation of the management accounting systems to respond to the financial problems..9

M-4.............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting (MA) is the accounting system which deals with the managing

the business decision of an organization. Under this, the information is gathered from the

accounting team and is further analysed by the internal management team based upon which the

final decision is being made. In this report, Connect Catering services is taken as an organization

which is small and medium-sized business running in Oxfordshire. This report presents a critical

evaluation of the different management accounting system and the methods used for the purpose

of accounting reporting. Along with that it involves the making use of the MA techniques for

analysing the cost and determining the pros and cons of planning tools for the purpose of

budgetary control. It also covers comparing the ways the MA system being implemented by the

organizations.

TASK 1

P-1 Critically analysing different MA systems

Management accounting basically accounts for the application of the different types of

the professional skills and knowledge in regard to the preparation of the financial and accounting

information. This is needed to be done in such a way that it will assist the internal managerial

team in the formulation of the policies and the planning strategies of the firm.

Different types of MA system

Cost accounting system

The cost accounting system is the process or the framework through which the firms can

estimate their product related cost and expenses in order to carry out the profitability analysis

and in exercising the cost control techniques (Abdusalomova, 2019). By making use of this

system, Connect Catering services can effectively arrange the records and determine the suitable

investment allocation.

Benefits

It helps in eliminating the wastage of resources and inefficiencies by fixing the standards.

This system assist in carrying out the cost reduction process through the way of

implementing new and improved approaches of production.

It helps in determining the profitability related to the product so that remedial action can

be undertaken.

Essential requirements

1

Management accounting (MA) is the accounting system which deals with the managing

the business decision of an organization. Under this, the information is gathered from the

accounting team and is further analysed by the internal management team based upon which the

final decision is being made. In this report, Connect Catering services is taken as an organization

which is small and medium-sized business running in Oxfordshire. This report presents a critical

evaluation of the different management accounting system and the methods used for the purpose

of accounting reporting. Along with that it involves the making use of the MA techniques for

analysing the cost and determining the pros and cons of planning tools for the purpose of

budgetary control. It also covers comparing the ways the MA system being implemented by the

organizations.

TASK 1

P-1 Critically analysing different MA systems

Management accounting basically accounts for the application of the different types of

the professional skills and knowledge in regard to the preparation of the financial and accounting

information. This is needed to be done in such a way that it will assist the internal managerial

team in the formulation of the policies and the planning strategies of the firm.

Different types of MA system

Cost accounting system

The cost accounting system is the process or the framework through which the firms can

estimate their product related cost and expenses in order to carry out the profitability analysis

and in exercising the cost control techniques (Abdusalomova, 2019). By making use of this

system, Connect Catering services can effectively arrange the records and determine the suitable

investment allocation.

Benefits

It helps in eliminating the wastage of resources and inefficiencies by fixing the standards.

This system assist in carrying out the cost reduction process through the way of

implementing new and improved approaches of production.

It helps in determining the profitability related to the product so that remedial action can

be undertaken.

Essential requirements

1

This system requires highly competent personnels who are having knowledge and

relevant skills in carrying out cost accounting.

Applicability

This is mainly applicable to the organizations which are involved in the production or

manufacturing.

Inventory management system

This system is implemented with the purpose of effectively determining and managing

the inventory of the organization. It is the combination of the procedures and the processes which

helps in effectively handling the movement of the inventory and maintaining the required stock

level. It can be utilized by the Connect Catering services in order to manage its inventory

appropriately.

Benefits

It helps in reducing the risk of overselling through the way of synchronizing the

inventory.

This also supports in overcoming the situation of stock out or the excess stock.

Better understanding of demand and availability helps in meeting higher inventory

turnover.

Essential requirements

It requires effectively tracking of the inventory and interpreting the same which can be

met by the professional making knowledge pertaining to inventory management.

Applicability

This MA system is applicable for the organization which are needed to handling bulk of

products or material as inventory either for production or supply.

Job costing system

This accounts for accumulating all the relevant information pertaining to the specific

production or the job. This can be further used for submitting the information to the customer

under the contract. The information gathered can be used for assigning the inventoriable cost or

the manufacturing the goods (TRUHACHEV, KOSTYUKOVA and BOBRISHEV, 2017).

Therefore, if implemented by Connect Catering services then it can be able to effectively manage

the job pertaining to the specific product or services.

Benefits

2

relevant skills in carrying out cost accounting.

Applicability

This is mainly applicable to the organizations which are involved in the production or

manufacturing.

Inventory management system

This system is implemented with the purpose of effectively determining and managing

the inventory of the organization. It is the combination of the procedures and the processes which

helps in effectively handling the movement of the inventory and maintaining the required stock

level. It can be utilized by the Connect Catering services in order to manage its inventory

appropriately.

Benefits

It helps in reducing the risk of overselling through the way of synchronizing the

inventory.

This also supports in overcoming the situation of stock out or the excess stock.

Better understanding of demand and availability helps in meeting higher inventory

turnover.

Essential requirements

It requires effectively tracking of the inventory and interpreting the same which can be

met by the professional making knowledge pertaining to inventory management.

Applicability

This MA system is applicable for the organization which are needed to handling bulk of

products or material as inventory either for production or supply.

Job costing system

This accounts for accumulating all the relevant information pertaining to the specific

production or the job. This can be further used for submitting the information to the customer

under the contract. The information gathered can be used for assigning the inventoriable cost or

the manufacturing the goods (TRUHACHEV, KOSTYUKOVA and BOBRISHEV, 2017).

Therefore, if implemented by Connect Catering services then it can be able to effectively manage

the job pertaining to the specific product or services.

Benefits

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The costs are determined at the various stages of completion which provides scope of

cost control by undertaking suitable steps.

The management can determine the cost per job based on the past record.

It also helps in determining the overhead recovery rates based upon the budget prepared.

Essential requirements

The essential requirement of this system is in determining the cost at various stages of

completion so that it can undertake corrective actions at right time.

Applicability

It is applicable to the organizations where the products or the services are offered in

accordance with the customer's specification and preferences.

Price Optimization system

Under this, MA system, the price of the product or service is determined based on the

demand of that in the market. It is basically a mathematical program which helps in determining

how the demand changes with the change in the price at different levels (Cooper, Ezzamel and

Qu, 2017). The Connect Catering services can combine this data with the information on cost

and inventory level in order to determine the suitable price.

Benefits

It is entirely an automated process which reduces the manual work.

It also helps in undertaking better and quick decisions.

This provides chance to concentrate on various goals like margin of sales and make

financial benefits.

Essential requirements

The essential requirement of this is that it helps in regulating the and controlling the

pricing decisions of the company.

Applicability

It can be implemented by Connect Catering services in order to determine right price and

maximize its profitability.

P2 Different methods of MA reporting

There are various types of MA reporting which can be used by the organization for

purpose of undertaking better and informed decisions. A detailed evaluation is given below.

Account Receivable Aging Reports

3

cost control by undertaking suitable steps.

The management can determine the cost per job based on the past record.

It also helps in determining the overhead recovery rates based upon the budget prepared.

Essential requirements

The essential requirement of this system is in determining the cost at various stages of

completion so that it can undertake corrective actions at right time.

Applicability

It is applicable to the organizations where the products or the services are offered in

accordance with the customer's specification and preferences.

Price Optimization system

Under this, MA system, the price of the product or service is determined based on the

demand of that in the market. It is basically a mathematical program which helps in determining

how the demand changes with the change in the price at different levels (Cooper, Ezzamel and

Qu, 2017). The Connect Catering services can combine this data with the information on cost

and inventory level in order to determine the suitable price.

Benefits

It is entirely an automated process which reduces the manual work.

It also helps in undertaking better and quick decisions.

This provides chance to concentrate on various goals like margin of sales and make

financial benefits.

Essential requirements

The essential requirement of this is that it helps in regulating the and controlling the

pricing decisions of the company.

Applicability

It can be implemented by Connect Catering services in order to determine right price and

maximize its profitability.

P2 Different methods of MA reporting

There are various types of MA reporting which can be used by the organization for

purpose of undertaking better and informed decisions. A detailed evaluation is given below.

Account Receivable Aging Reports

3

This report is mainly useful for the organization's who are dependent heavily on the

credit being offered to the customers (Drury, 2018). Through this, the company can get an

insight into the account balances of each of its customer along with the due date and amount due.

It helps in determining any issue in its collection process. Also, it can identify the potential

customer who have become bad debts and required to be written off.

Budget Reports

This report is very important in measuring the performance of the company and in case of

big firms it is done department wise. This will helps Connect Catering services in making

estimation based on past experience and cater to the unforeseen circumstances and meeting with

goals and objectives within the amount budgeted.

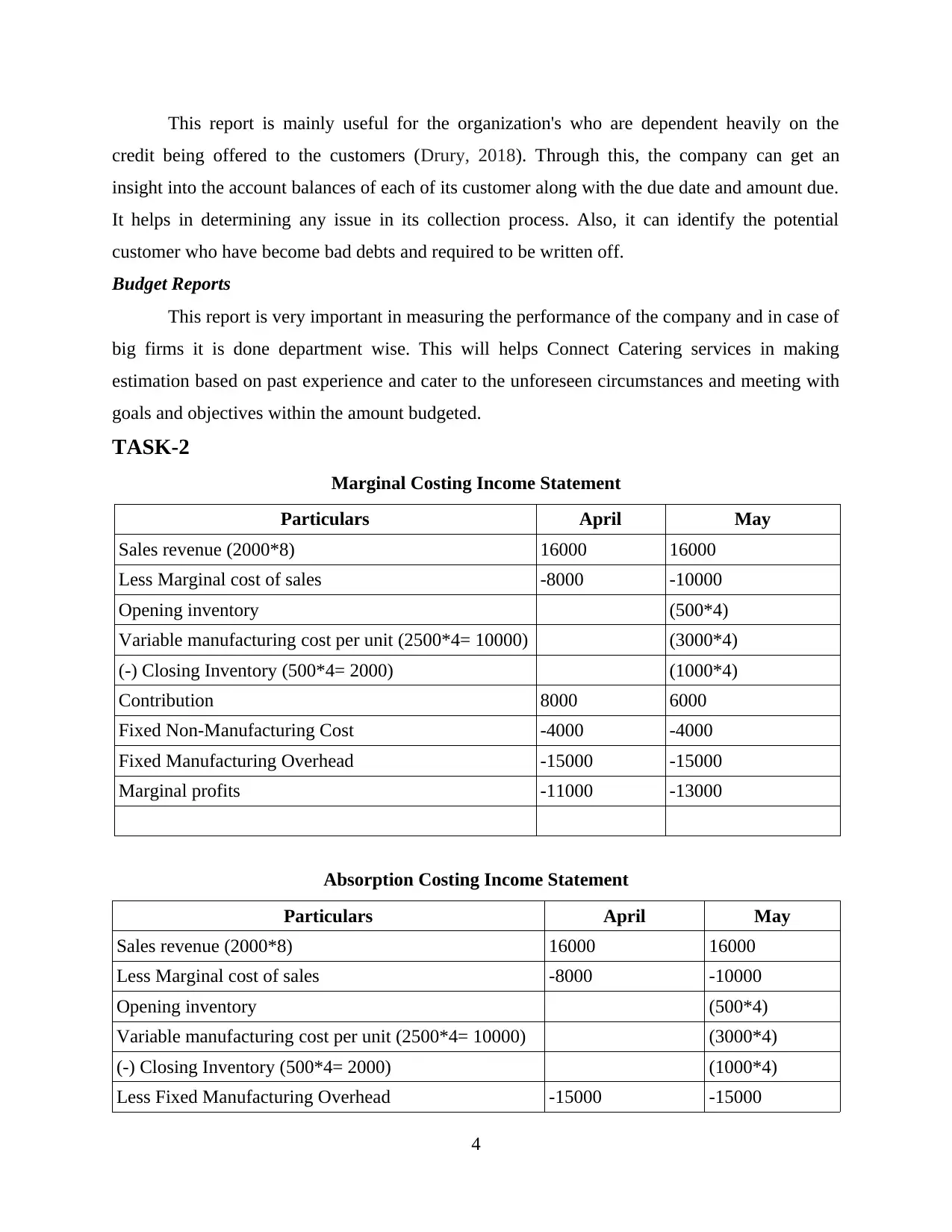

TASK-2

Marginal Costing Income Statement

Particulars April May

Sales revenue (2000*8) 16000 16000

Less Marginal cost of sales -8000 -10000

Opening inventory (500*4)

Variable manufacturing cost per unit (2500*4= 10000) (3000*4)

(-) Closing Inventory (500*4= 2000) (1000*4)

Contribution 8000 6000

Fixed Non-Manufacturing Cost -4000 -4000

Fixed Manufacturing Overhead -15000 -15000

Marginal profits -11000 -13000

Absorption Costing Income Statement

Particulars April May

Sales revenue (2000*8) 16000 16000

Less Marginal cost of sales -8000 -10000

Opening inventory (500*4)

Variable manufacturing cost per unit (2500*4= 10000) (3000*4)

(-) Closing Inventory (500*4= 2000) (1000*4)

Less Fixed Manufacturing Overhead -15000 -15000

4

credit being offered to the customers (Drury, 2018). Through this, the company can get an

insight into the account balances of each of its customer along with the due date and amount due.

It helps in determining any issue in its collection process. Also, it can identify the potential

customer who have become bad debts and required to be written off.

Budget Reports

This report is very important in measuring the performance of the company and in case of

big firms it is done department wise. This will helps Connect Catering services in making

estimation based on past experience and cater to the unforeseen circumstances and meeting with

goals and objectives within the amount budgeted.

TASK-2

Marginal Costing Income Statement

Particulars April May

Sales revenue (2000*8) 16000 16000

Less Marginal cost of sales -8000 -10000

Opening inventory (500*4)

Variable manufacturing cost per unit (2500*4= 10000) (3000*4)

(-) Closing Inventory (500*4= 2000) (1000*4)

Contribution 8000 6000

Fixed Non-Manufacturing Cost -4000 -4000

Fixed Manufacturing Overhead -15000 -15000

Marginal profits -11000 -13000

Absorption Costing Income Statement

Particulars April May

Sales revenue (2000*8) 16000 16000

Less Marginal cost of sales -8000 -10000

Opening inventory (500*4)

Variable manufacturing cost per unit (2500*4= 10000) (3000*4)

(-) Closing Inventory (500*4= 2000) (1000*4)

Less Fixed Manufacturing Overhead -15000 -15000

4

Gross Profit -7000

Less Fixed Non-Manufacturing Cost -4000 -4000

Absorption profits -11000 -13000

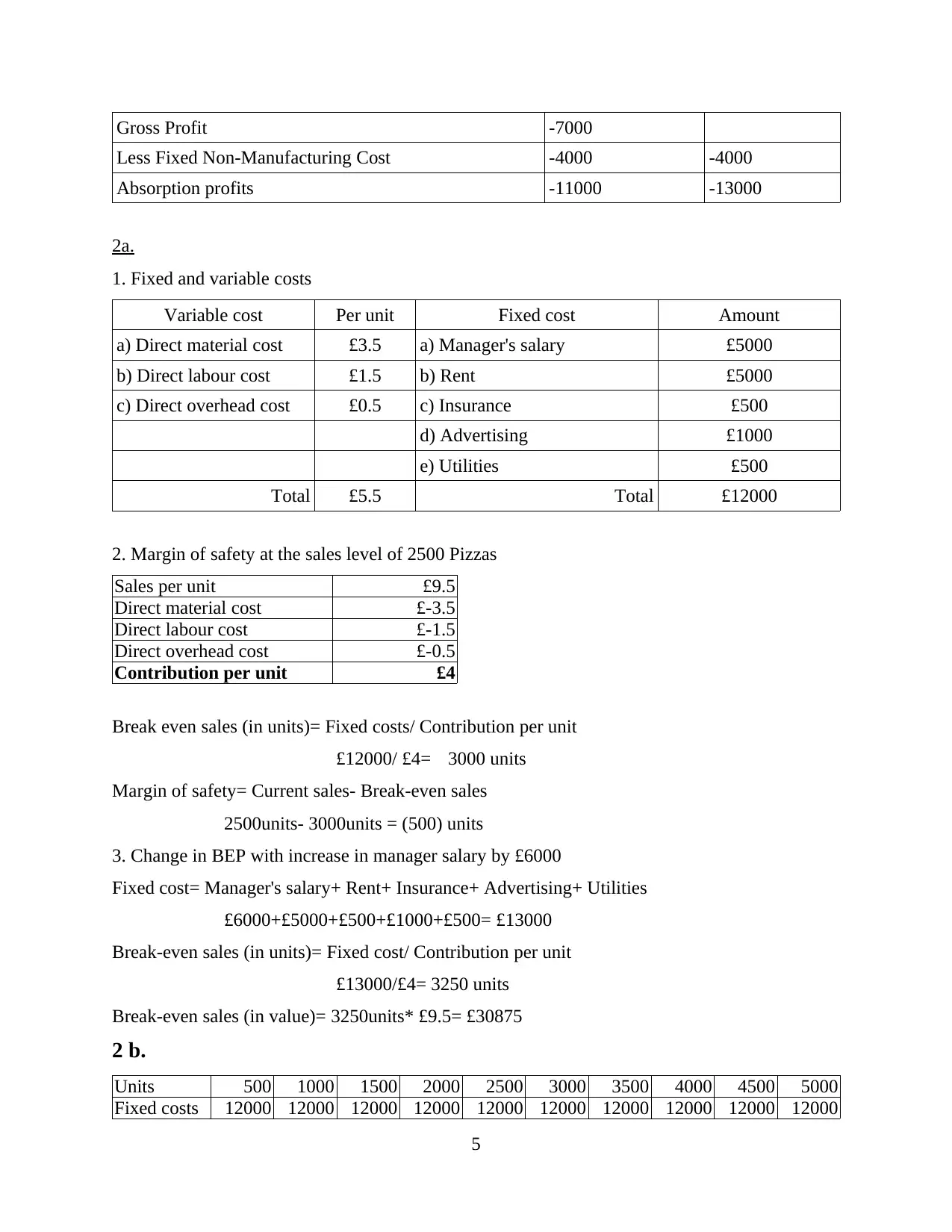

2a.

1. Fixed and variable costs

Variable cost Per unit Fixed cost Amount

a) Direct material cost £3.5 a) Manager's salary £5000

b) Direct labour cost £1.5 b) Rent £5000

c) Direct overhead cost £0.5 c) Insurance £500

d) Advertising £1000

e) Utilities £500

Total £5.5 Total £12000

2. Margin of safety at the sales level of 2500 Pizzas

Sales per unit £9.5

Direct material cost £-3.5

Direct labour cost £-1.5

Direct overhead cost £-0.5

Contribution per unit £4

Break even sales (in units)= Fixed costs/ Contribution per unit

£12000/ £4= 3000 units

Margin of safety= Current sales- Break-even sales

2500units- 3000units = (500) units

3. Change in BEP with increase in manager salary by £6000

Fixed cost= Manager's salary+ Rent+ Insurance+ Advertising+ Utilities

£6000+£5000+£500+£1000+£500= £13000

Break-even sales (in units)= Fixed cost/ Contribution per unit

£13000/£4= 3250 units

Break-even sales (in value)= 3250units* £9.5= £30875

2 b.

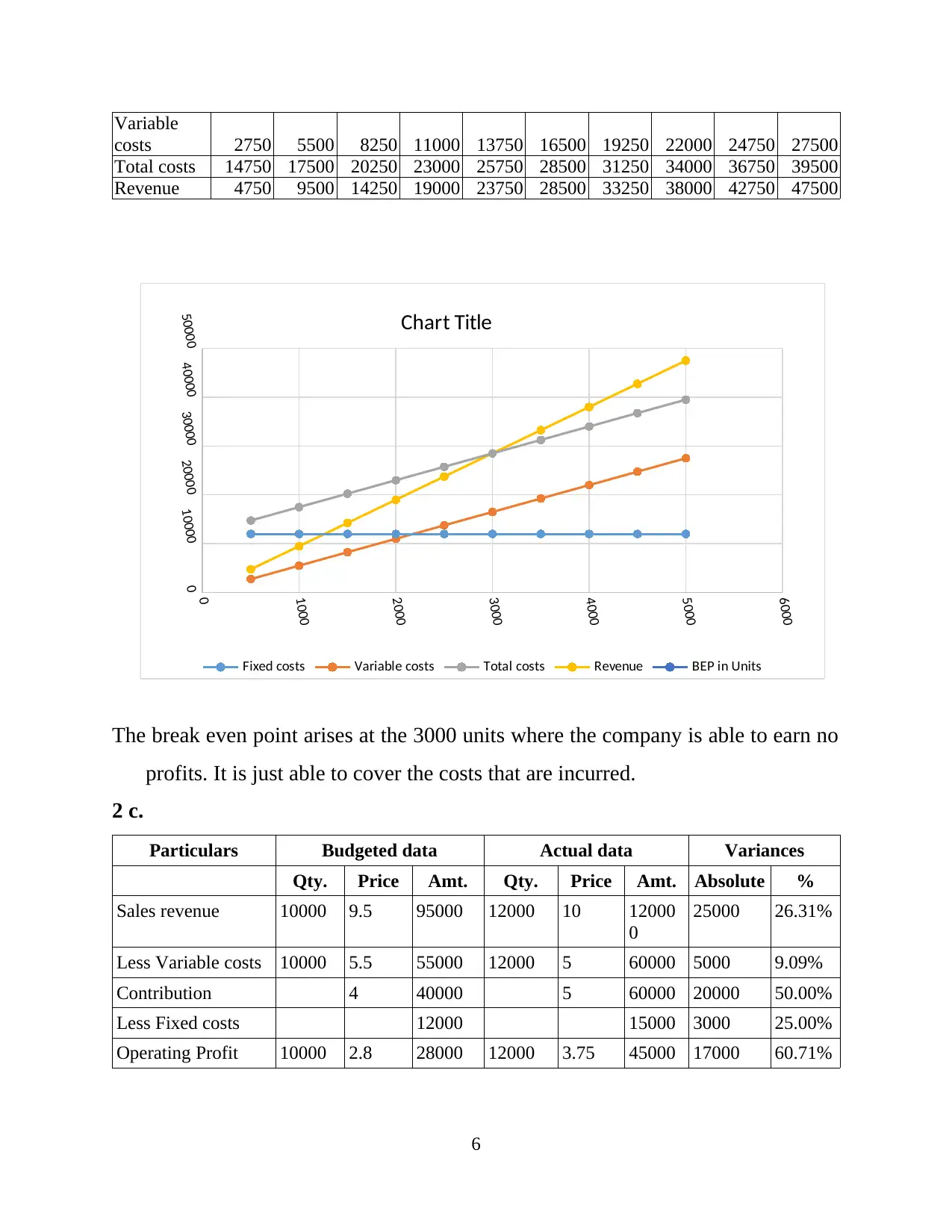

Units 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

Fixed costs 12000 12000 12000 12000 12000 12000 12000 12000 12000 12000

5

Less Fixed Non-Manufacturing Cost -4000 -4000

Absorption profits -11000 -13000

2a.

1. Fixed and variable costs

Variable cost Per unit Fixed cost Amount

a) Direct material cost £3.5 a) Manager's salary £5000

b) Direct labour cost £1.5 b) Rent £5000

c) Direct overhead cost £0.5 c) Insurance £500

d) Advertising £1000

e) Utilities £500

Total £5.5 Total £12000

2. Margin of safety at the sales level of 2500 Pizzas

Sales per unit £9.5

Direct material cost £-3.5

Direct labour cost £-1.5

Direct overhead cost £-0.5

Contribution per unit £4

Break even sales (in units)= Fixed costs/ Contribution per unit

£12000/ £4= 3000 units

Margin of safety= Current sales- Break-even sales

2500units- 3000units = (500) units

3. Change in BEP with increase in manager salary by £6000

Fixed cost= Manager's salary+ Rent+ Insurance+ Advertising+ Utilities

£6000+£5000+£500+£1000+£500= £13000

Break-even sales (in units)= Fixed cost/ Contribution per unit

£13000/£4= 3250 units

Break-even sales (in value)= 3250units* £9.5= £30875

2 b.

Units 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

Fixed costs 12000 12000 12000 12000 12000 12000 12000 12000 12000 12000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable

costs 2750 5500 8250 11000 13750 16500 19250 22000 24750 27500

Total costs 14750 17500 20250 23000 25750 28500 31250 34000 36750 39500

Revenue 4750 9500 14250 19000 23750 28500 33250 38000 42750 47500

The break even point arises at the 3000 units where the company is able to earn no

profits. It is just able to cover the costs that are incurred.

2 c.

Particulars Budgeted data Actual data Variances

Qty. Price Amt. Qty. Price Amt. Absolute %

Sales revenue 10000 9.5 95000 12000 10 12000

0

25000 26.31%

Less Variable costs 10000 5.5 55000 12000 5 60000 5000 9.09%

Contribution 4 40000 5 60000 20000 50.00%

Less Fixed costs 12000 15000 3000 25.00%

Operating Profit 10000 2.8 28000 12000 3.75 45000 17000 60.71%

6

0

1000

2000

3000

4000

5000

6000

0

10000

20000

30000

40000

50000

Chart Title

Fixed costs Variable costs Total costs Revenue BEP in Units

costs 2750 5500 8250 11000 13750 16500 19250 22000 24750 27500

Total costs 14750 17500 20250 23000 25750 28500 31250 34000 36750 39500

Revenue 4750 9500 14250 19000 23750 28500 33250 38000 42750 47500

The break even point arises at the 3000 units where the company is able to earn no

profits. It is just able to cover the costs that are incurred.

2 c.

Particulars Budgeted data Actual data Variances

Qty. Price Amt. Qty. Price Amt. Absolute %

Sales revenue 10000 9.5 95000 12000 10 12000

0

25000 26.31%

Less Variable costs 10000 5.5 55000 12000 5 60000 5000 9.09%

Contribution 4 40000 5 60000 20000 50.00%

Less Fixed costs 12000 15000 3000 25.00%

Operating Profit 10000 2.8 28000 12000 3.75 45000 17000 60.71%

6

0

1000

2000

3000

4000

5000

6000

0

10000

20000

30000

40000

50000

Chart Title

Fixed costs Variable costs Total costs Revenue BEP in Units

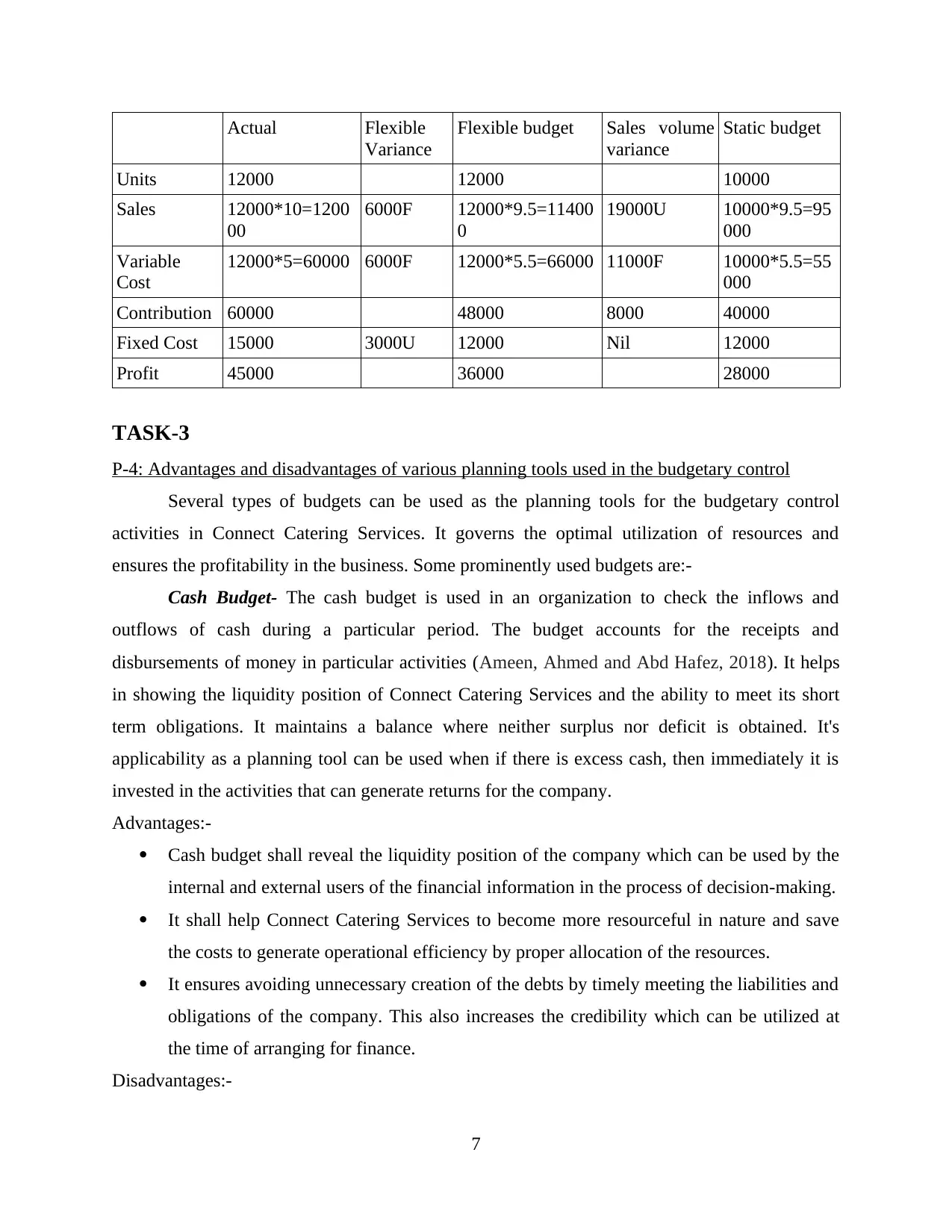

Actual Flexible

Variance

Flexible budget Sales volume

variance

Static budget

Units 12000 12000 10000

Sales 12000*10=1200

00

6000F 12000*9.5=11400

0

19000U 10000*9.5=95

000

Variable

Cost

12000*5=60000 6000F 12000*5.5=66000 11000F 10000*5.5=55

000

Contribution 60000 48000 8000 40000

Fixed Cost 15000 3000U 12000 Nil 12000

Profit 45000 36000 28000

TASK-3

P-4: Advantages and disadvantages of various planning tools used in the budgetary control

Several types of budgets can be used as the planning tools for the budgetary control

activities in Connect Catering Services. It governs the optimal utilization of resources and

ensures the profitability in the business. Some prominently used budgets are:-

Cash Budget- The cash budget is used in an organization to check the inflows and

outflows of cash during a particular period. The budget accounts for the receipts and

disbursements of money in particular activities (Ameen, Ahmed and Abd Hafez, 2018). It helps

in showing the liquidity position of Connect Catering Services and the ability to meet its short

term obligations. It maintains a balance where neither surplus nor deficit is obtained. It's

applicability as a planning tool can be used when if there is excess cash, then immediately it is

invested in the activities that can generate returns for the company.

Advantages:-

Cash budget shall reveal the liquidity position of the company which can be used by the

internal and external users of the financial information in the process of decision-making.

It shall help Connect Catering Services to become more resourceful in nature and save

the costs to generate operational efficiency by proper allocation of the resources.

It ensures avoiding unnecessary creation of the debts by timely meeting the liabilities and

obligations of the company. This also increases the credibility which can be utilized at

the time of arranging for finance.

Disadvantages:-

7

Variance

Flexible budget Sales volume

variance

Static budget

Units 12000 12000 10000

Sales 12000*10=1200

00

6000F 12000*9.5=11400

0

19000U 10000*9.5=95

000

Variable

Cost

12000*5=60000 6000F 12000*5.5=66000 11000F 10000*5.5=55

000

Contribution 60000 48000 8000 40000

Fixed Cost 15000 3000U 12000 Nil 12000

Profit 45000 36000 28000

TASK-3

P-4: Advantages and disadvantages of various planning tools used in the budgetary control

Several types of budgets can be used as the planning tools for the budgetary control

activities in Connect Catering Services. It governs the optimal utilization of resources and

ensures the profitability in the business. Some prominently used budgets are:-

Cash Budget- The cash budget is used in an organization to check the inflows and

outflows of cash during a particular period. The budget accounts for the receipts and

disbursements of money in particular activities (Ameen, Ahmed and Abd Hafez, 2018). It helps

in showing the liquidity position of Connect Catering Services and the ability to meet its short

term obligations. It maintains a balance where neither surplus nor deficit is obtained. It's

applicability as a planning tool can be used when if there is excess cash, then immediately it is

invested in the activities that can generate returns for the company.

Advantages:-

Cash budget shall reveal the liquidity position of the company which can be used by the

internal and external users of the financial information in the process of decision-making.

It shall help Connect Catering Services to become more resourceful in nature and save

the costs to generate operational efficiency by proper allocation of the resources.

It ensures avoiding unnecessary creation of the debts by timely meeting the liabilities and

obligations of the company. This also increases the credibility which can be utilized at

the time of arranging for finance.

Disadvantages:-

7

It reduces the flexibility in building the credit profile, spending power and initiating new

plans in Connect Catering Services (Van Helden and Uddin, 2016).

It is based on the estimates and assumptions that are made by the company. It neither

reflects the profitability nor the future growth prospects, which means it cannot be

utilized for the major decision-making.

Zero based budgeting:- It is a technique of budgeting wherein Connect Catering Services

starts the preparation of the budget from the scratch that is the zero level. This is undertaken by

not referring any of the past items rather assess the incomes and expenditures by taking the base

as zero. It involves justification of each and every expense that is being accounted for in the

budget. It ensures the highest degree of accuracy in its predictions regarding the future.

Advantages:-

It is more efficient and accurate as reduces the redundancy of activities in the

organization.

The major advantage is that all the expenses are being involved with proper justifications

so it avoids wastages of resources (Alborov and etal., 2017). It also maintains better

coordination and communication.

Disadvantages:-

It requires higher cost, time consumption which may delay the routine activities of the

business.

Higher degree of expertise and efficiency is required by the manpower of Connect

Catering Services.

Expenditure budget:- This budget shall consider all the expenditure that can arise in a

particular period. It is essential to plan for the expenditures and compare with the simultaneously

generated income in the business. This helps in avoiding the wasteful expenses and thereby

optimizing the financial resources of the company. Prior forecasting helps in creating reserves

for the future expenses which does not disturb the financial position of Connect Catering

Services.

Advantages:-

Facilitates effective coordination in the various departments of the business.

Ensures optimal utilization of the financial resources which ultimately helps in generating

better returns for the company.

8

plans in Connect Catering Services (Van Helden and Uddin, 2016).

It is based on the estimates and assumptions that are made by the company. It neither

reflects the profitability nor the future growth prospects, which means it cannot be

utilized for the major decision-making.

Zero based budgeting:- It is a technique of budgeting wherein Connect Catering Services

starts the preparation of the budget from the scratch that is the zero level. This is undertaken by

not referring any of the past items rather assess the incomes and expenditures by taking the base

as zero. It involves justification of each and every expense that is being accounted for in the

budget. It ensures the highest degree of accuracy in its predictions regarding the future.

Advantages:-

It is more efficient and accurate as reduces the redundancy of activities in the

organization.

The major advantage is that all the expenses are being involved with proper justifications

so it avoids wastages of resources (Alborov and etal., 2017). It also maintains better

coordination and communication.

Disadvantages:-

It requires higher cost, time consumption which may delay the routine activities of the

business.

Higher degree of expertise and efficiency is required by the manpower of Connect

Catering Services.

Expenditure budget:- This budget shall consider all the expenditure that can arise in a

particular period. It is essential to plan for the expenditures and compare with the simultaneously

generated income in the business. This helps in avoiding the wasteful expenses and thereby

optimizing the financial resources of the company. Prior forecasting helps in creating reserves

for the future expenses which does not disturb the financial position of Connect Catering

Services.

Advantages:-

Facilitates effective coordination in the various departments of the business.

Ensures optimal utilization of the financial resources which ultimately helps in generating

better returns for the company.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Disadvantages:-

Brings rigidity in the operations of employees where their initiative taking capacity

reduces.

It does not facilitate employee engagement and participation which lowers down the

morale of the workforce.

M-3

These planning tools can be used by Connect Catering Services, for the efficient and

effective budgeting and forecasting the future level of activities and operations that are to be

undertaken for ensuring profitability and future growth prospects. This optimizes the activities

and reduces the scope for wastages, miscommunication and conflicts.

P-5: Adaptation of the management accounting systems to respond to the financial problems

Management accounting systems can be used by Connect Catering Services for the

resolution of its financial problems like enhancement of profit-margin, planning expansion,

optimal utilization of the resources, maximize the wealth of shareholder and the achievement of

the organizational objectives.

Benchmarking:- It is an essential technique that is used for facilitating the comparison of the

business's performance with that of the leader in the industry. The comparison may be with the

performance of the competitor or internally within various departments. This helps in gaining

operational efficiency by establishing targets as per the one who is best in the business. The

standards in respect of production, sales, expenditure etc. are set which ensures the smooth and

efficient accomplishment of the goals of Connect Catering Services.

Applicability:- Benchmarking is most importantly used to handle the competition in the

business and for the survival of the company. The financial problems like wastages, idle money,

miscommunication and lack of operational efficiency can be tackled by the application of

benchmarking technique in the business.

Variance Analysis:- It is another technique that can be used for the resolution of the various

financial problems that are faced by the business (Quattrone, 2016). This is done by comparing

the actual performance of the company with the set standards that were prior established. This

comparison helps in finding out the deviations that are caused due to some inefficiencies in the

business. Further these variances shall be studied and the reasons behind its occurrence shall be

9

Brings rigidity in the operations of employees where their initiative taking capacity

reduces.

It does not facilitate employee engagement and participation which lowers down the

morale of the workforce.

M-3

These planning tools can be used by Connect Catering Services, for the efficient and

effective budgeting and forecasting the future level of activities and operations that are to be

undertaken for ensuring profitability and future growth prospects. This optimizes the activities

and reduces the scope for wastages, miscommunication and conflicts.

P-5: Adaptation of the management accounting systems to respond to the financial problems

Management accounting systems can be used by Connect Catering Services for the

resolution of its financial problems like enhancement of profit-margin, planning expansion,

optimal utilization of the resources, maximize the wealth of shareholder and the achievement of

the organizational objectives.

Benchmarking:- It is an essential technique that is used for facilitating the comparison of the

business's performance with that of the leader in the industry. The comparison may be with the

performance of the competitor or internally within various departments. This helps in gaining

operational efficiency by establishing targets as per the one who is best in the business. The

standards in respect of production, sales, expenditure etc. are set which ensures the smooth and

efficient accomplishment of the goals of Connect Catering Services.

Applicability:- Benchmarking is most importantly used to handle the competition in the

business and for the survival of the company. The financial problems like wastages, idle money,

miscommunication and lack of operational efficiency can be tackled by the application of

benchmarking technique in the business.

Variance Analysis:- It is another technique that can be used for the resolution of the various

financial problems that are faced by the business (Quattrone, 2016). This is done by comparing

the actual performance of the company with the set standards that were prior established. This

comparison helps in finding out the deviations that are caused due to some inefficiencies in the

business. Further these variances shall be studied and the reasons behind its occurrence shall be

9

found out. Improvisation in the shortcomings shall be undertaken such that the operational

efficiency can be boosted and better results can be generated for Connect Catering Services.

Applicability:- The variance analysis can be utilized to increase the production capacity,

attain economies of scale, reduce the cost per unit and optimize the financial utilization of

resources. All such financial incapabilities of the company can be solved and the growth

prospects can be effectively determined.

Key performance indicators:- The key performance indicators are used by the company to

measure their performance against the measurable values and find the deficiency of the business.

This shall help the company receive the desired level of outcome and will be able to develop the

competitive edge in the industry. The key performance indicators guide the employees in the

right path for the achievement of organizational objectives.

Applicability:- In Connect Catering Services it can be ensured that the staff is working as

per the provided performance indicators and accordingly the set targets are being accomplished

in the company. It ensures the maximum output in terms of profitability from the minimum input

that is the cost of productions (Kostyukova and etal., 2018). Optimization of all the processes can

be ensured by using this technique in the business.

Connect Catering Services Chefs on the move

The Connect Catering Services uses the

benchmarking technique to ensure the

resolution of the financial problems in the

business. They establish the targets of their

business as attained by the leading firm in the

industry. This helps them develop operational

efficiency, work at 100% capacity and reduce

the cost. It ascertains profitability and future

growth prospect for the business.

The Chefs on the move uses variance analysis

system to improvise its operations by resolving

the deviations by taking measures against the

same. These variances are discovered by

comparing the actual performance with that of

the standards.

M-4

The efficient and effective manner of handling the issues shall be leading to the growth

and development of the organization in a sustainable manner. The optimal utilization of the

10

efficiency can be boosted and better results can be generated for Connect Catering Services.

Applicability:- The variance analysis can be utilized to increase the production capacity,

attain economies of scale, reduce the cost per unit and optimize the financial utilization of

resources. All such financial incapabilities of the company can be solved and the growth

prospects can be effectively determined.

Key performance indicators:- The key performance indicators are used by the company to

measure their performance against the measurable values and find the deficiency of the business.

This shall help the company receive the desired level of outcome and will be able to develop the

competitive edge in the industry. The key performance indicators guide the employees in the

right path for the achievement of organizational objectives.

Applicability:- In Connect Catering Services it can be ensured that the staff is working as

per the provided performance indicators and accordingly the set targets are being accomplished

in the company. It ensures the maximum output in terms of profitability from the minimum input

that is the cost of productions (Kostyukova and etal., 2018). Optimization of all the processes can

be ensured by using this technique in the business.

Connect Catering Services Chefs on the move

The Connect Catering Services uses the

benchmarking technique to ensure the

resolution of the financial problems in the

business. They establish the targets of their

business as attained by the leading firm in the

industry. This helps them develop operational

efficiency, work at 100% capacity and reduce

the cost. It ascertains profitability and future

growth prospect for the business.

The Chefs on the move uses variance analysis

system to improvise its operations by resolving

the deviations by taking measures against the

same. These variances are discovered by

comparing the actual performance with that of

the standards.

M-4

The efficient and effective manner of handling the issues shall be leading to the growth

and development of the organization in a sustainable manner. The optimal utilization of the

10

scarce resources shall help in sustainable development of the business. It shall maintain long

growth and prosperity of the business.

CONCLUSION

It can be summarized from the above project report that management accounting is very

important for the company in a way that it facilitates the decision-making process and helps in

fulfilment of the organizational objectives. Management accounting systems are used by the

internal managers to make essential decisions regarding the future with the use of the available

financial reports. The major management accounting systems like the cost accounting, job

costing, inventory management are used by the company to optimize the operations of the

company in a way that profitability and future growth prospects of the business can be enhanced.

Apart from that profits can be analysed using the marginal as well as absorption costing methods.

The break-even point of the company shows the point where company earns zero level of profits.

The margin of safety shows the amounts of sales that are generated over and above the break-

even level. There are various planning tools that can be used by the company to forecast the

future level of activities of the company like the cash budget, operating budget and zero based

budget. Various management accounting systems are used in order to resolve the financial

problems that are arising in the business like wastages, high cost per unit, low capacity etc.

Benchmarking, key performance indicators and the variance analysis are some of the techniques

that can be used by the company for solving the financial problems of the business.

11

growth and prosperity of the business.

CONCLUSION

It can be summarized from the above project report that management accounting is very

important for the company in a way that it facilitates the decision-making process and helps in

fulfilment of the organizational objectives. Management accounting systems are used by the

internal managers to make essential decisions regarding the future with the use of the available

financial reports. The major management accounting systems like the cost accounting, job

costing, inventory management are used by the company to optimize the operations of the

company in a way that profitability and future growth prospects of the business can be enhanced.

Apart from that profits can be analysed using the marginal as well as absorption costing methods.

The break-even point of the company shows the point where company earns zero level of profits.

The margin of safety shows the amounts of sales that are generated over and above the break-

even level. There are various planning tools that can be used by the company to forecast the

future level of activities of the company like the cash budget, operating budget and zero based

budget. Various management accounting systems are used in order to resolve the financial

problems that are arising in the business like wastages, high cost per unit, low capacity etc.

Benchmarking, key performance indicators and the variance analysis are some of the techniques

that can be used by the company for solving the financial problems of the business.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3). p.2.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

TRUHACHEV, V. I., KOSTYUKOVA, E. I. and BOBRISHEV, A. N., 2017. Development of

management accounting in Russia. Revista Espacios. 38(27).

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2).

pp.991-1025.

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Van Helden, J. and Uddin, S., 2016. Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting. 41. pp.34-62.

Alborov, R. A. and etal., 2017. The development of management and strategic management

accounting in agriculture. Journal of engineering and applied sciences. 12(19).

pp.4979-4984.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Kostyukova, E. I. and etal., 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(2). pp.775-779.

Online

Management Accounting - Meaning, Advantages & Functions. 2021. [Online]. Available

through: <https://cleartax.in/s/management-accounting>

12

Books and Journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting. 2019(3). p.2.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

TRUHACHEV, V. I., KOSTYUKOVA, E. I. and BOBRISHEV, A. N., 2017. Development of

management accounting in Russia. Revista Espacios. 38(27).

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2).

pp.991-1025.

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Van Helden, J. and Uddin, S., 2016. Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting. 41. pp.34-62.

Alborov, R. A. and etal., 2017. The development of management and strategic management

accounting in agriculture. Journal of engineering and applied sciences. 12(19).

pp.4979-4984.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Kostyukova, E. I. and etal., 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(2). pp.775-779.

Online

Management Accounting - Meaning, Advantages & Functions. 2021. [Online]. Available

through: <https://cleartax.in/s/management-accounting>

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.