Analysis of Management Accounting for Capital Joinery Ltd. (CJL)

VerifiedAdded on 2022/12/09

|22

|4481

|475

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Capital Joinery Ltd. (CJL). It begins by defining management accounting and exploring different types of systems such as job costing, cost accounting, price optimization, and inventory management. The report then delves into management accounting reporting (MAR), detailing various forms like account receivable aging reports, performance reports, budget reports, and cost accounting reports. Furthermore, it showcases the application of management accounting techniques, including income statements prepared using both absorption and marginal costing methods, along with a reconciliation of profit figures and variance analysis. The report also explains the advantages and disadvantages of planning tools of budgetary control and how management accounting systems can be adopted to respond to financial problems, culminating in a conclusion that highlights the importance of effective management accounting for organizational success. The report is structured around two scenarios, providing practical examples and calculations to illustrate key concepts.

UNIT 5 – MANAGEMENT

ACCOUNTING L-4

ACCOUNTING L-4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

P1 Explaining Management accounting and different types of its systems..............................................3

P2 Explaining different types of Management Accounting Reporting (MAR)........................................6

SCENARIO 2..............................................................................................................................................8

P3 Types of management accounting techniques....................................................................................8

P4. Explaining advantages and disadvantages types of planning tools of budgetary control................15

P5 Explaining How management accounting system adopted by organizations to respond financial

problems................................................................................................................................................18

CONCLUSION.........................................................................................................................................20

REFERENCES..........................................................................................................................................21

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

P1 Explaining Management accounting and different types of its systems..............................................3

P2 Explaining different types of Management Accounting Reporting (MAR)........................................6

SCENARIO 2..............................................................................................................................................8

P3 Types of management accounting techniques....................................................................................8

P4. Explaining advantages and disadvantages types of planning tools of budgetary control................15

P5 Explaining How management accounting system adopted by organizations to respond financial

problems................................................................................................................................................18

CONCLUSION.........................................................................................................................................20

REFERENCES..........................................................................................................................................21

INTRODUCTION

Management accounting is crucial component which S a systematic process of assessing,

allocating and managing monetary resources of organizations. It comprises various systems,

reports, techniques, etc to make the functioning of firm more effective. The current case is based

on Capital Joinery Ltd. which makes a wide variety of joinery, made-to-measure doors, windows

etc. The present report will give emphasis on management accounting system along with

benefits & applications in context of organization. Different types of management accounting

reports will be explained in present case study. Calculations of costs using appropriate

techniques of concerned analysis with marginal and absorption costing via preparing income

statements will shown in present case study. Case study will include advantages and

disadvantages of planning tools. It will comprise how organization responds to financial

problems for obtaining sustainability

MAIN BODY

SCENARIO 1

P1 Explaining Management accounting and different types of its systems

Management Accounting (MA) is procedure of utilization financial information for

taking strategic decisions in order to work effectively. Capital Joinery Ltd. (CJL) will be

benefited by having different types of Management Accounting System (MAS) in its business

practices (Abdusalomova, 2019). There are different types of MAS which can help CJL to derive

varying advantages for moving towards success.

Job Costing System

It is one of the management accounting system which helps organization to determine

cost of each task or project. Business comprises different functional areas that ahs its different

cost structuring which is responsible for some part of total profitability of organization. In

addition o this Capital Joinery Ltd. Will be benefited by having systematic job costing in its

business practices. These advantages can be understood by following points.

Management accounting is crucial component which S a systematic process of assessing,

allocating and managing monetary resources of organizations. It comprises various systems,

reports, techniques, etc to make the functioning of firm more effective. The current case is based

on Capital Joinery Ltd. which makes a wide variety of joinery, made-to-measure doors, windows

etc. The present report will give emphasis on management accounting system along with

benefits & applications in context of organization. Different types of management accounting

reports will be explained in present case study. Calculations of costs using appropriate

techniques of concerned analysis with marginal and absorption costing via preparing income

statements will shown in present case study. Case study will include advantages and

disadvantages of planning tools. It will comprise how organization responds to financial

problems for obtaining sustainability

MAIN BODY

SCENARIO 1

P1 Explaining Management accounting and different types of its systems

Management Accounting (MA) is procedure of utilization financial information for

taking strategic decisions in order to work effectively. Capital Joinery Ltd. (CJL) will be

benefited by having different types of Management Accounting System (MAS) in its business

practices (Abdusalomova, 2019). There are different types of MAS which can help CJL to derive

varying advantages for moving towards success.

Job Costing System

It is one of the management accounting system which helps organization to determine

cost of each task or project. Business comprises different functional areas that ahs its different

cost structuring which is responsible for some part of total profitability of organization. In

addition o this Capital Joinery Ltd. Will be benefited by having systematic job costing in its

business practices. These advantages can be understood by following points.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages

It helps in analyzing performance of each department of company which can be useful in

determining its efficiency. CJL will be able to derive performance of its functional areas

in turn its working as well operational efficiency can be evaluated to bring modification

in prevailing policies.

Accuracy, flexibility and Scalability in its way of conducting organizational activities can

be attained. Capital Joinery Ltd can identify profitability of each task through these

characteristics in organization.

Continuous monitory aids firm to make changes in required areas at in systematic

manner. This is the biggest advantage CJL will get through executing job costing system

in firm.

Cost accounting System

This is internally focused process which is developed to determine cost, inventory as well

profitability of organization. Capital Joinery Ltd will be benefited by having this system into

while making wide variety of joinery. With help of this, company can make comparison between

current and previous data for getting deep insights into enterprise’s effectiveness. Cost

accounting system is widely sued by all types of firm regardless of industry variation and scale

difference (Mahmoudian and et.al.,2021). It play crucial role in determining significant

components that are essential for having smooth functioning.

Benefits

This provides ability to view data in different ways so that all aspects can be covered to

make evaluation. Capital Joinery ltd can use this particulars system to determine cost of

operational practices.

Determination of prices become possible by having cost accountings system in business

as it provides all details of all related cost so that better profit margin can be decided.

It helps in analyzing performance of each department of company which can be useful in

determining its efficiency. CJL will be able to derive performance of its functional areas

in turn its working as well operational efficiency can be evaluated to bring modification

in prevailing policies.

Accuracy, flexibility and Scalability in its way of conducting organizational activities can

be attained. Capital Joinery Ltd can identify profitability of each task through these

characteristics in organization.

Continuous monitory aids firm to make changes in required areas at in systematic

manner. This is the biggest advantage CJL will get through executing job costing system

in firm.

Cost accounting System

This is internally focused process which is developed to determine cost, inventory as well

profitability of organization. Capital Joinery Ltd will be benefited by having this system into

while making wide variety of joinery. With help of this, company can make comparison between

current and previous data for getting deep insights into enterprise’s effectiveness. Cost

accounting system is widely sued by all types of firm regardless of industry variation and scale

difference (Mahmoudian and et.al.,2021). It play crucial role in determining significant

components that are essential for having smooth functioning.

Benefits

This provides ability to view data in different ways so that all aspects can be covered to

make evaluation. Capital Joinery ltd can use this particulars system to determine cost of

operational practices.

Determination of prices become possible by having cost accountings system in business

as it provides all details of all related cost so that better profit margin can be decided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reasons for losses can be identified by CJL through executing this management

accounting system. Controlling cost become possible through elimination of unnecessary

components that are result of losses.

Price Optimization system

It ensures firm is setting appropriate price to meet effectively market forces through

maintaining profitability. This is utilized by organization to assess reaction of customers on

varying prices of products in turn assistance can be derived for fixing prices of products (Latan

and et.al., 2018). In competitive scenario it provides various competitive advantages to firm so

adopting it would eb beneficial for Capital Joinery Limited.

Pros

Better profitability ensures longer scale of organizational practices as economies of scale

can be derived by having good amount of profit margins. CJL will be benefited by this

characteristic of price optimization system.

Immediate financial benefits can be attained by this management accounting system as it

will provide Capital Joinery Ltd opportunity to concentrate on different details of

company.

Prompt decision making in respect to this filed become becomes by having price

optimization in organization.

Inventory Management System

It ensures entire supply chain including inbound, operations, outbound are maintained

effectively. This helps in gaining efficient management process of inventory so that better

productivity can be obtained. Capital Joinery Ltd will get assistance in managing its stock so that

burden of over or under consumption of resources can be avoided. The firm will receive

following benefits through this particular system:

accounting system. Controlling cost become possible through elimination of unnecessary

components that are result of losses.

Price Optimization system

It ensures firm is setting appropriate price to meet effectively market forces through

maintaining profitability. This is utilized by organization to assess reaction of customers on

varying prices of products in turn assistance can be derived for fixing prices of products (Latan

and et.al., 2018). In competitive scenario it provides various competitive advantages to firm so

adopting it would eb beneficial for Capital Joinery Limited.

Pros

Better profitability ensures longer scale of organizational practices as economies of scale

can be derived by having good amount of profit margins. CJL will be benefited by this

characteristic of price optimization system.

Immediate financial benefits can be attained by this management accounting system as it

will provide Capital Joinery Ltd opportunity to concentrate on different details of

company.

Prompt decision making in respect to this filed become becomes by having price

optimization in organization.

Inventory Management System

It ensures entire supply chain including inbound, operations, outbound are maintained

effectively. This helps in gaining efficient management process of inventory so that better

productivity can be obtained. Capital Joinery Ltd will get assistance in managing its stock so that

burden of over or under consumption of resources can be avoided. The firm will receive

following benefits through this particular system:

Reduction of expenditure becomes possible by making production as well other related

processes more effective and efficient.

Significant relationship with suppliers and vendor can be built by Capital Joiner Ltd. In

addition to this, more insights into essential information can be obtained by firm through

this management accounting system. It is most important systems of MAS. Which need

to be y more consideration for having efficient functioning.

P2 Explaining different types of Management Accounting Reporting (MAR)

MAR helps organization to give focus on each aspects of operational activity so that

company can derive relevant information for attaining sustainability. Capital Joiner Ltd. Can

obtain required information which can enhances its productivity and profitability. MAR can be

prepared in following different forms:

Account Receivable Aging Report

Large or small organization makes sales in both cash and credit form to increase its

revenue. It becomes essential for concerned firm to give focus on certain factors that can increase

its liquidity. Capital Joiner Ltd would be benefited by having this specific report in its

management in order to get details regarding actual cash received and account receivables. This

particular report helps in identifying client’s remaining balances that need to be received with

limited time period. It also aids in finding efficiency of payment collection from debtors. The

steps can be taken by CJL to avoid bad debt and written off situations are prompt payment

making policies, immediate cash paying related offers like discount, etc. Capital Joiner Ltd can

improve its current credit policy to have smooth functioning.

Performance Report

At the end of the term every scale of firm pay attention on reviewing performance of

company as a whole. In addition to this, each employees potential can be identified by

formulating this specific report in firm. Capital Joiner Ltd can use this to encourage its

employees for sharing their full potential in order to achieve company’s growth. Variations can

also be found through comparing two periods performance report which will provide assistance

to CJL to get insights regarding low efficient areas that are the results of adverse outcome. In

addition to this, performance report will enable Capital Joiner Ltd to assess its current position

processes more effective and efficient.

Significant relationship with suppliers and vendor can be built by Capital Joiner Ltd. In

addition to this, more insights into essential information can be obtained by firm through

this management accounting system. It is most important systems of MAS. Which need

to be y more consideration for having efficient functioning.

P2 Explaining different types of Management Accounting Reporting (MAR)

MAR helps organization to give focus on each aspects of operational activity so that

company can derive relevant information for attaining sustainability. Capital Joiner Ltd. Can

obtain required information which can enhances its productivity and profitability. MAR can be

prepared in following different forms:

Account Receivable Aging Report

Large or small organization makes sales in both cash and credit form to increase its

revenue. It becomes essential for concerned firm to give focus on certain factors that can increase

its liquidity. Capital Joiner Ltd would be benefited by having this specific report in its

management in order to get details regarding actual cash received and account receivables. This

particular report helps in identifying client’s remaining balances that need to be received with

limited time period. It also aids in finding efficiency of payment collection from debtors. The

steps can be taken by CJL to avoid bad debt and written off situations are prompt payment

making policies, immediate cash paying related offers like discount, etc. Capital Joiner Ltd can

improve its current credit policy to have smooth functioning.

Performance Report

At the end of the term every scale of firm pay attention on reviewing performance of

company as a whole. In addition to this, each employees potential can be identified by

formulating this specific report in firm. Capital Joiner Ltd can use this to encourage its

employees for sharing their full potential in order to achieve company’s growth. Variations can

also be found through comparing two periods performance report which will provide assistance

to CJL to get insights regarding low efficient areas that are the results of adverse outcome. In

addition to this, performance report will enable Capital Joiner Ltd to assess its current position

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in present scenario and ability for adopting changing circumstances can also be evaluated to take

suitable course of actions.

Budget Report

This is very crucial report for all small, medium and large scale fro getting instructions in

doer to move forward. Budgetary reports are widely prepared by firm to accomplish its objective

through identifying available resources, appropriate pattern for allocating according to

requirements and controlling cost of unnecessary parts (Bhimani, 2020). CJL will be able to

obtain structure for preparing budget by referring previous statement for identification of

changing requirements of company. It aids in recognizing unforeseen situations which can

influence success of CJL so that corrective actions can be taken. Appropriate segregation

between expected income and expenditure can be known by CJL to have significant information

for taking important decisions. Budgets play important role in providing various types of

advantages to company so having this type of management accounting report would be

beneficial for Capital Joiner Ltd. Guidance from budget can help CJL to move in right direction

for achieving desirable profit.

Cost Accounting Reports

It helps in determining cost of articles that are created in company as this comprises all

raw materials, overheads, etc which are directly and indirectly linked with its volume of

manufacturing. Capital Joiner Ltd can attain summary of all expenses related with its

operational activities. This report helps in identifying cost prices versus selling value. Estimating

profit margins become possible by formulating cost accounting reports in company (Garbowski

and et.al., 2021). CJL will be able to ascertain inventory waste, hourly labor cost, overheads, etc.

information can be used by company for taking improvement actions. Having cost accounting

report would be beneficial os company should give emphasis on this.

Additional Managerial Accounting Reports

Project, order information, competitor, variance analysis, etc. are some other types of

management accounting reports for which is useful in having information regarding operational

activities (Kapiyangoda and Gooneratne, 2021). This can be internally prepared outsourced by

suitable course of actions.

Budget Report

This is very crucial report for all small, medium and large scale fro getting instructions in

doer to move forward. Budgetary reports are widely prepared by firm to accomplish its objective

through identifying available resources, appropriate pattern for allocating according to

requirements and controlling cost of unnecessary parts (Bhimani, 2020). CJL will be able to

obtain structure for preparing budget by referring previous statement for identification of

changing requirements of company. It aids in recognizing unforeseen situations which can

influence success of CJL so that corrective actions can be taken. Appropriate segregation

between expected income and expenditure can be known by CJL to have significant information

for taking important decisions. Budgets play important role in providing various types of

advantages to company so having this type of management accounting report would be

beneficial for Capital Joiner Ltd. Guidance from budget can help CJL to move in right direction

for achieving desirable profit.

Cost Accounting Reports

It helps in determining cost of articles that are created in company as this comprises all

raw materials, overheads, etc which are directly and indirectly linked with its volume of

manufacturing. Capital Joiner Ltd can attain summary of all expenses related with its

operational activities. This report helps in identifying cost prices versus selling value. Estimating

profit margins become possible by formulating cost accounting reports in company (Garbowski

and et.al., 2021). CJL will be able to ascertain inventory waste, hourly labor cost, overheads, etc.

information can be used by company for taking improvement actions. Having cost accounting

report would be beneficial os company should give emphasis on this.

Additional Managerial Accounting Reports

Project, order information, competitor, variance analysis, etc. are some other types of

management accounting reports for which is useful in having information regarding operational

activities (Kapiyangoda and Gooneratne, 2021). This can be internally prepared outsourced by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CJL. This will provide immense help in getting relevant information which can impact

company’s productivity and profitability. Greater amount of focus on managerial accounting

report help company to derive significant improvement for having better sustainability and

profitability. Having such process in firm can enable organization to have proper identification

of strengths and weakness for overcoming challenges and obtaining maximum profitability of

CJL.

SCENARIO 2

P3 Types of management accounting techniques

Applying management accounting techniques and producing appropriate financial

reporting documents

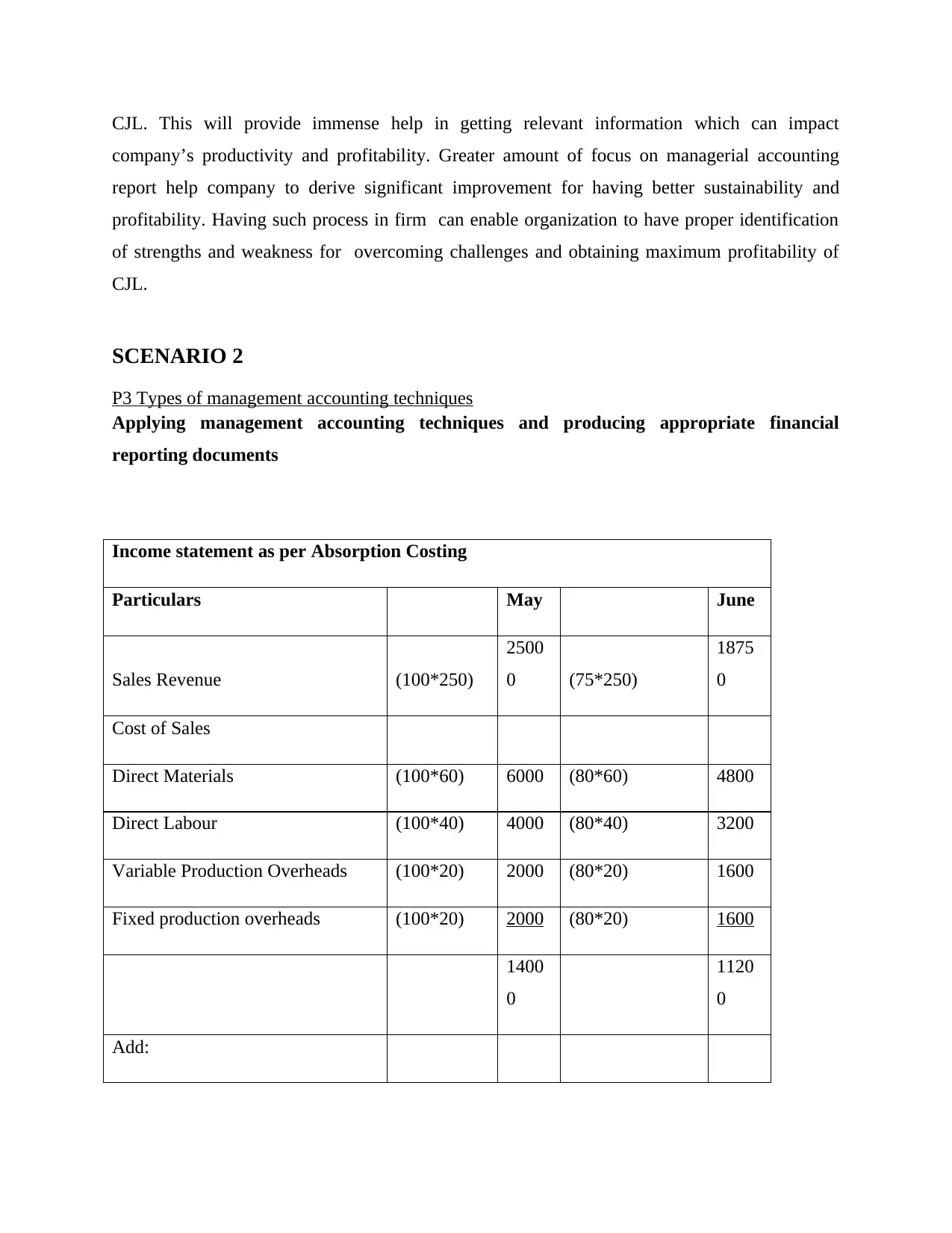

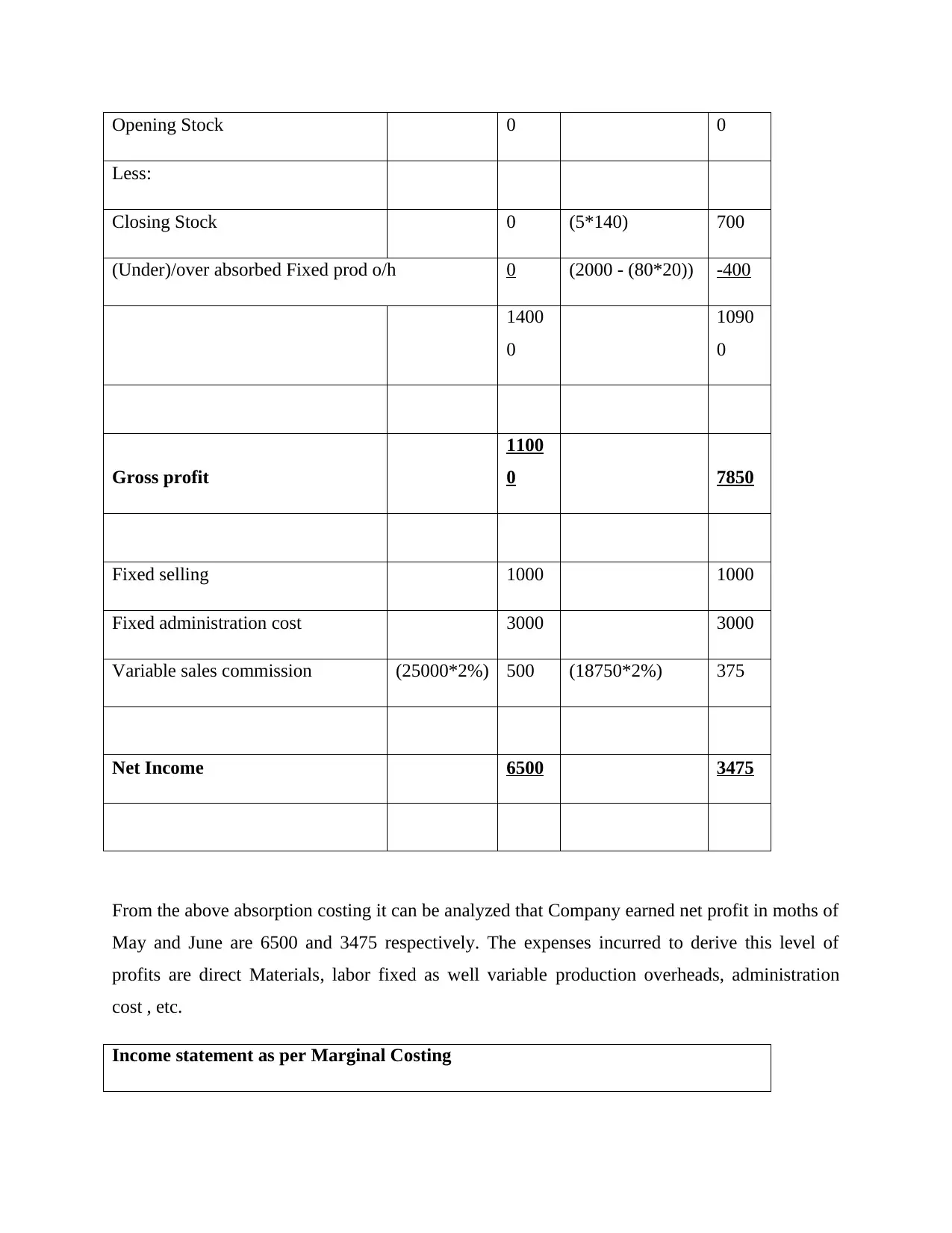

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250)

2500

0 (75*250)

1875

0

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (80*20) 1600

1400

0

1120

0

Add:

company’s productivity and profitability. Greater amount of focus on managerial accounting

report help company to derive significant improvement for having better sustainability and

profitability. Having such process in firm can enable organization to have proper identification

of strengths and weakness for overcoming challenges and obtaining maximum profitability of

CJL.

SCENARIO 2

P3 Types of management accounting techniques

Applying management accounting techniques and producing appropriate financial

reporting documents

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250)

2500

0 (75*250)

1875

0

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable Production Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (80*20) 1600

1400

0

1120

0

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*140) 700

(Under)/over absorbed Fixed prod o/h 0 (2000 - (80*20)) -400

1400

0

1090

0

Gross profit

1100

0 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3475

From the above absorption costing it can be analyzed that Company earned net profit in moths of

May and June are 6500 and 3475 respectively. The expenses incurred to derive this level of

profits are direct Materials, labor fixed as well variable production overheads, administration

cost , etc.

Income statement as per Marginal Costing

Less:

Closing Stock 0 (5*140) 700

(Under)/over absorbed Fixed prod o/h 0 (2000 - (80*20)) -400

1400

0

1090

0

Gross profit

1100

0 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3475

From the above absorption costing it can be analyzed that Company earned net profit in moths of

May and June are 6500 and 3475 respectively. The expenses incurred to derive this level of

profits are direct Materials, labor fixed as well variable production overheads, administration

cost , etc.

Income statement as per Marginal Costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

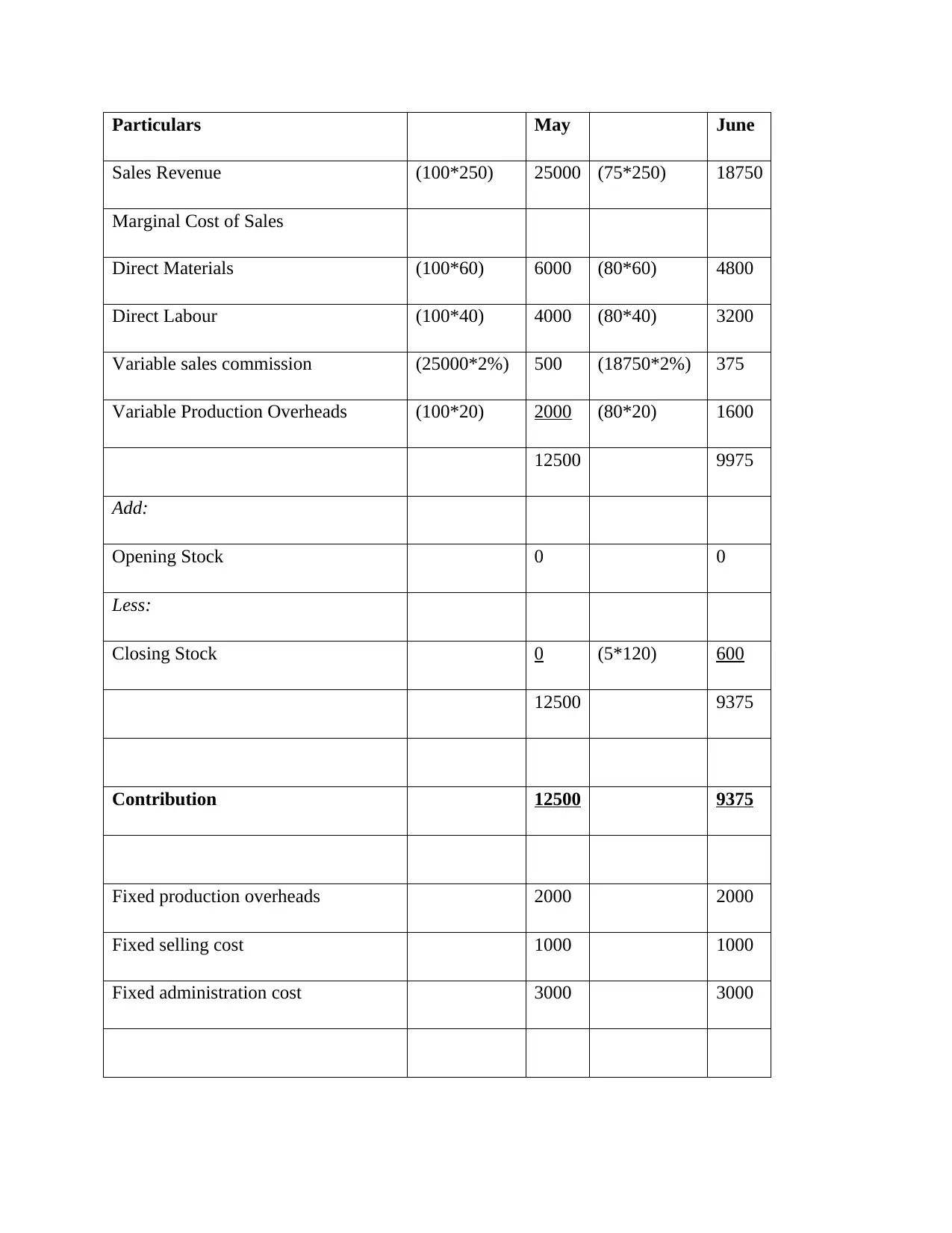

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

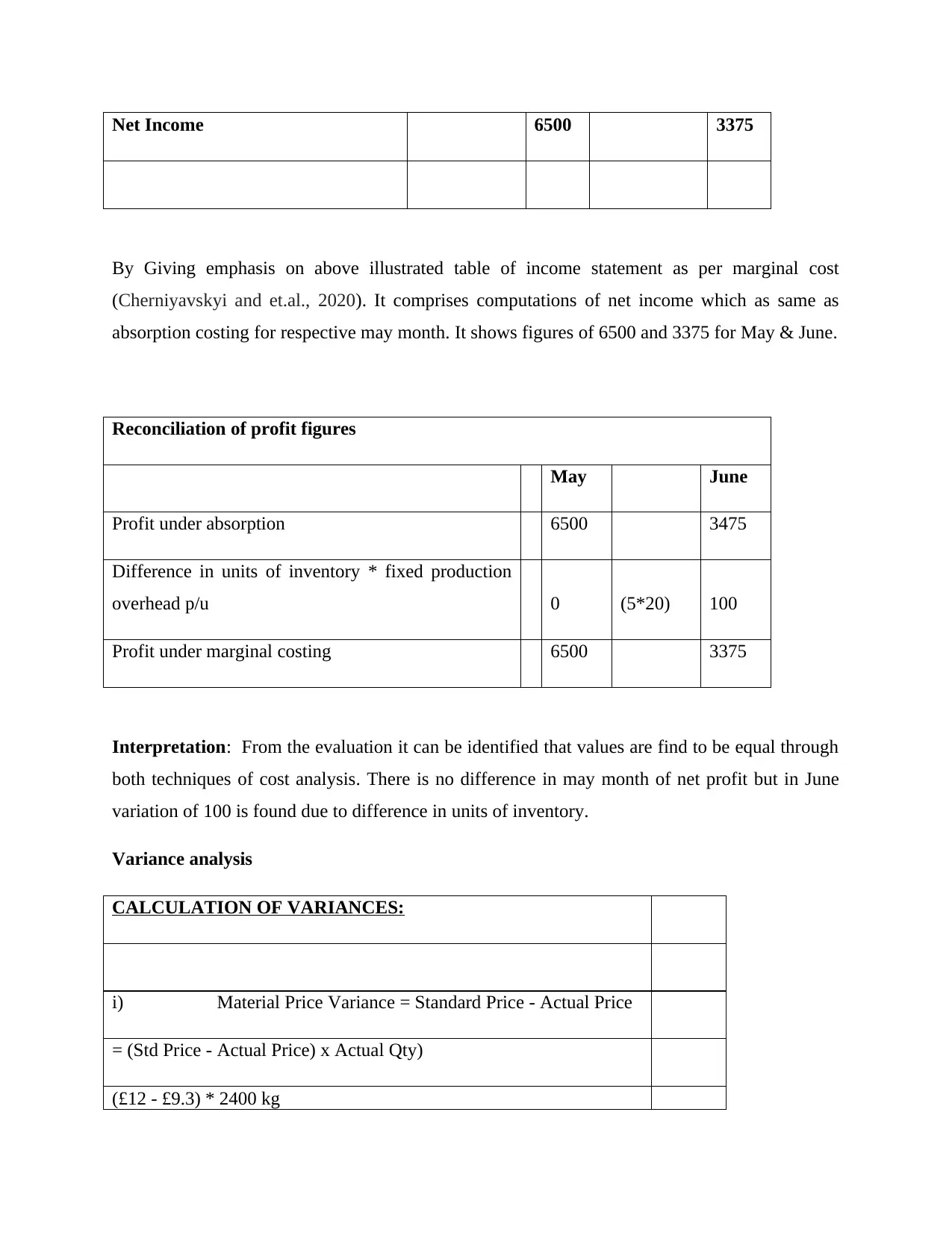

Net Income 6500 3375

By Giving emphasis on above illustrated table of income statement as per marginal cost

(Cherniyavskyi and et.al., 2020). It comprises computations of net income which as same as

absorption costing for respective may month. It shows figures of 6500 and 3375 for May & June.

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production

overhead p/u 0 (5*20) 100

Profit under marginal costing 6500 3375

Interpretation: From the evaluation it can be identified that values are find to be equal through

both techniques of cost analysis. There is no difference in may month of net profit but in June

variation of 100 is found due to difference in units of inventory.

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

By Giving emphasis on above illustrated table of income statement as per marginal cost

(Cherniyavskyi and et.al., 2020). It comprises computations of net income which as same as

absorption costing for respective may month. It shows figures of 6500 and 3375 for May & June.

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production

overhead p/u 0 (5*20) 100

Profit under marginal costing 6500 3375

Interpretation: From the evaluation it can be identified that values are find to be equal through

both techniques of cost analysis. There is no difference in may month of net profit but in June

variation of 100 is found due to difference in units of inventory.

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

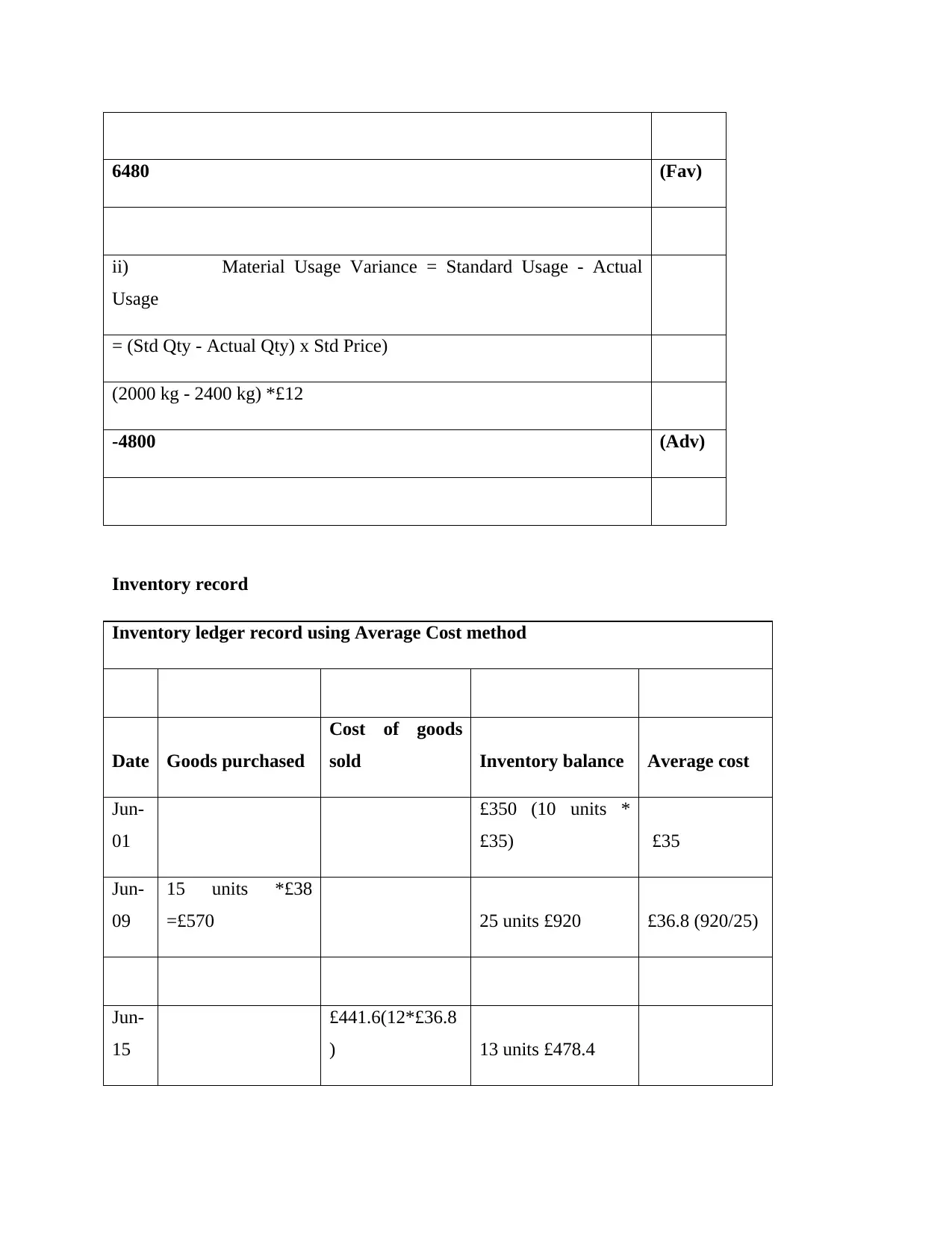

6480 (Fav)

ii) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

Inventory record

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun-

15

£441.6(12*£36.8

) 13 units £478.4

ii) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

Inventory record

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun-

15

£441.6(12*£36.8

) 13 units £478.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.