Role of Management Accounting in Businesses

VerifiedAdded on 2023/01/17

|20

|5138

|92

AI Summary

This article discusses the role of management accounting in businesses, including its different types such as cost accounting system, inventory management system, price optimization system, and job order costing system. It also explains the difference between management accounting and financial accounting. The article further explores the different methods of management accounting reports, the benefits of management accounting systems, and the integration of MAS and MA reports with business processes. Additionally, it covers the preparation of income statements using absorption and marginal costing techniques.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of content

INTRODUCTION

Accounting is a key aspect for business entities for recording the financial transactions in

an effective manner. The MA is one of the main part of accounting (Siverbo, 2014). It is related

to process of collecting monetary and non monetary information with an aim of preparing

internal reports when needed by managers. These reports are presented only to the internal

stakeholders. The objective of project report is to analysing role of this accounting in context of

businesses. In the report Alpha limited company has been chosen that is located in United

Kingdom and operates in manufacturing of Pizzas. The report covers detailed information about

different MAS, MA reports and planning tools etc. In addition, role of different MAS in the

aspect of sorting financial issue is also mentioned in report.

MAIN BODY

TASK 1

P1. MA and its types.

MA- It is defined as a type of accounting which operates in the process of collecting quantitative

and qualitative information so that accountant can prepare internal reports. These reports provide

a detailed framework to the managers in order to take crucial internal decisions. Below some

types of MA are demonstrated such as:

Cost accounting system- It is integrated to finance department of businesses with an aim

of making projection of futuristic expenses (Granlund and Lukka, 2017). By help of

making projection of further cost, it becomes easier for managers to take suitable action

in order to allocate funds as accordance of need so that cost can be minimised. It is

essential for businesses to track the usage of funds and total cost occurred in process of

operating different operations. In Alpha limited company, they are using this accounting

system for keeping cost lower from the estimations.

Inventory management system – It is associated to process of tracking daily consumption

of stock value in order to produce new items. It is completely based on the stock

valuation methods such as Last and first method, First in first out method and many

more. It is essential for companies for reducing cost of storage lower as well as for

gathering information about usage of stock in completing activities regards to production.

Accounting is a key aspect for business entities for recording the financial transactions in

an effective manner. The MA is one of the main part of accounting (Siverbo, 2014). It is related

to process of collecting monetary and non monetary information with an aim of preparing

internal reports when needed by managers. These reports are presented only to the internal

stakeholders. The objective of project report is to analysing role of this accounting in context of

businesses. In the report Alpha limited company has been chosen that is located in United

Kingdom and operates in manufacturing of Pizzas. The report covers detailed information about

different MAS, MA reports and planning tools etc. In addition, role of different MAS in the

aspect of sorting financial issue is also mentioned in report.

MAIN BODY

TASK 1

P1. MA and its types.

MA- It is defined as a type of accounting which operates in the process of collecting quantitative

and qualitative information so that accountant can prepare internal reports. These reports provide

a detailed framework to the managers in order to take crucial internal decisions. Below some

types of MA are demonstrated such as:

Cost accounting system- It is integrated to finance department of businesses with an aim

of making projection of futuristic expenses (Granlund and Lukka, 2017). By help of

making projection of further cost, it becomes easier for managers to take suitable action

in order to allocate funds as accordance of need so that cost can be minimised. It is

essential for businesses to track the usage of funds and total cost occurred in process of

operating different operations. In Alpha limited company, they are using this accounting

system for keeping cost lower from the estimations.

Inventory management system – It is associated to process of tracking daily consumption

of stock value in order to produce new items. It is completely based on the stock

valuation methods such as Last and first method, First in first out method and many

more. It is essential for companies for reducing cost of storage lower as well as for

gathering information about usage of stock in completing activities regards to production.

In the aspect of above Alpha limited company, they are using this accounting system that

is helping them in order to assessing consumption of raw material, finished goods and

many more.

Price optimisation system – This is defined as a type of accounting system which is

linked to process of setting price of products and services in an effective manner. This

becomes possible because in this sales department utilise key information regards to

customers' perception, feedback as well as market demand. On the basis of it, they set

prices of various products in relation to different market and customer segments. It is

essential for companies in order to setting prices of products in accordance of market

analysis. In Alpha limited company, their sales department set the prices of Pizzas as per

the market position and customers need.

Job order costing system – This is a type of costing system which computes cost of each

activity in accordance of assigned number of jobs (Kastberg and Siverbo, 2016). It is

essential for companies in order to analyse and keep cost job lower as much as possible.

In Alpha limited company, they are using this costing system to provide important

information to their finance department about cost of each activity and job assigned in

completing different volume of operations.

Difference between MA and financial accounting:

Basis MA Financial accounting

Purpose This applied with an aim of internal

management of companies

This accounting is applied for

assessing monetary performance and

for publishing reports for external

stakeholders.

Information Under it, quantitative and qualitative

information is included.

While in this only monetary

information is included.

Essential This is not compulsory to apply in

organizational context.

It is essential for those companies

which are listed to prepare financial

statements.

is helping them in order to assessing consumption of raw material, finished goods and

many more.

Price optimisation system – This is defined as a type of accounting system which is

linked to process of setting price of products and services in an effective manner. This

becomes possible because in this sales department utilise key information regards to

customers' perception, feedback as well as market demand. On the basis of it, they set

prices of various products in relation to different market and customer segments. It is

essential for companies in order to setting prices of products in accordance of market

analysis. In Alpha limited company, their sales department set the prices of Pizzas as per

the market position and customers need.

Job order costing system – This is a type of costing system which computes cost of each

activity in accordance of assigned number of jobs (Kastberg and Siverbo, 2016). It is

essential for companies in order to analyse and keep cost job lower as much as possible.

In Alpha limited company, they are using this costing system to provide important

information to their finance department about cost of each activity and job assigned in

completing different volume of operations.

Difference between MA and financial accounting:

Basis MA Financial accounting

Purpose This applied with an aim of internal

management of companies

This accounting is applied for

assessing monetary performance and

for publishing reports for external

stakeholders.

Information Under it, quantitative and qualitative

information is included.

While in this only monetary

information is included.

Essential This is not compulsory to apply in

organizational context.

It is essential for those companies

which are listed to prepare financial

statements.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P2. Different methods of MA reports.

MA reports- The term MA reports can be defined as those documents which contains key

information related to each and every monetary and anti monetary aspects. In the context of

above Alpha limited company, they are preparing different types of reports that are mentioned

such as:

Inventory reports- It is a report that consists key information related to opening and

closing balance of various forms of stock including raw material, finished goods and

many more. Under it, all types of information is included as accordance of evaluating

quantity of stock under LIFO, FIFO and weighted average method. In the above Alpha

limited company, they are using this report with an aim of keep in touch about how much

quantity of material they have in the end of a particular day.

Performance report- It is a report that includes key information related to performance of

each and every aspect in a detailed manner (Hirsch, Seubert and Sohn, 2015). It is being

used by managers of companies in order to take critical decision about progress of

employees. In the absence of this report, the actual performance of employees can be

hide. Apart from the information related to performance of employees, it includes other

information such as performance of different performed operations and activities etc. In

Alpha limited company, they are preparing this report in order to assure sustainable

growth of various aspects.

Budget report- Under it, information about project output and actual output is included.

By help of this report, finance department becomes able to assess the variance between

actual and estimated output. In the context of above Alpha limited company, they

produce this report in order to track variances and for keeping an extra sheet of eye on

overall performance.

Accounts receivable ageing report –It is a report which includes detailed information

about total debt amount that is required to be collect in upcoming time period. As

accordance of it, finance manager make further plans regards to need of fund to complete

different operations and activities. One of the key feature of this report is that under it,

information is recorded in a systematic manner so that managers can track easily about

debt amount. In regards to above Alpha limited company, they are using this report for

focusing on those customers whose amount is not received yet.

MA reports- The term MA reports can be defined as those documents which contains key

information related to each and every monetary and anti monetary aspects. In the context of

above Alpha limited company, they are preparing different types of reports that are mentioned

such as:

Inventory reports- It is a report that consists key information related to opening and

closing balance of various forms of stock including raw material, finished goods and

many more. Under it, all types of information is included as accordance of evaluating

quantity of stock under LIFO, FIFO and weighted average method. In the above Alpha

limited company, they are using this report with an aim of keep in touch about how much

quantity of material they have in the end of a particular day.

Performance report- It is a report that includes key information related to performance of

each and every aspect in a detailed manner (Hirsch, Seubert and Sohn, 2015). It is being

used by managers of companies in order to take critical decision about progress of

employees. In the absence of this report, the actual performance of employees can be

hide. Apart from the information related to performance of employees, it includes other

information such as performance of different performed operations and activities etc. In

Alpha limited company, they are preparing this report in order to assure sustainable

growth of various aspects.

Budget report- Under it, information about project output and actual output is included.

By help of this report, finance department becomes able to assess the variance between

actual and estimated output. In the context of above Alpha limited company, they

produce this report in order to track variances and for keeping an extra sheet of eye on

overall performance.

Accounts receivable ageing report –It is a report which includes detailed information

about total debt amount that is required to be collect in upcoming time period. As

accordance of it, finance manager make further plans regards to need of fund to complete

different operations and activities. One of the key feature of this report is that under it,

information is recorded in a systematic manner so that managers can track easily about

debt amount. In regards to above Alpha limited company, they are using this report for

focusing on those customers whose amount is not received yet.

M1. Benefits of MAS.

Herein, below key role of MAS for businesses is mentioned that is as follows:

Benefit of cost accounting system- In accordance of above description, this accounting

system is linked to process of controlling and minimising cost of different operations. In

Alpha limited company, they get benefit from this by managing overall expenses and

costs.

Benefit of inventory management system- It is helpful for sales and production

department of companies in order to track consumption of goods and for calculating

opening & closing balance (Chandar, Collier and Miranti, 2012). Such as in Alpha

limited company, they get benefit from this by keeping cost of storage low.

Benefit of price optimisation system- It is linked with sales department of companies and

for setting prices of products at an effective level. In the Alpha limited company, they

revise their pricing strategies in accordance of market situation.

Benefit of job costing system- This is based on computing cost of various activities

separately. In the Alpha limited company, they are getting benefited from this accounting

system by tracking cost of job effectively.

D1. Integration of MAS and MA reports with business process.

It may become difficult for companies to operate different operations and activities

effectively if they fail to integrate their departments with accounting systems (Horton and de

Araujo Wanderley, 2018). Like in the Alpha limited company, their sales department is

integrated with price optimisation system and stock management system. In addition, their

production department utilise important information from stock management report and their

finance department also assess key information from account receivable ageing report.

Herein, below key role of MAS for businesses is mentioned that is as follows:

Benefit of cost accounting system- In accordance of above description, this accounting

system is linked to process of controlling and minimising cost of different operations. In

Alpha limited company, they get benefit from this by managing overall expenses and

costs.

Benefit of inventory management system- It is helpful for sales and production

department of companies in order to track consumption of goods and for calculating

opening & closing balance (Chandar, Collier and Miranti, 2012). Such as in Alpha

limited company, they get benefit from this by keeping cost of storage low.

Benefit of price optimisation system- It is linked with sales department of companies and

for setting prices of products at an effective level. In the Alpha limited company, they

revise their pricing strategies in accordance of market situation.

Benefit of job costing system- This is based on computing cost of various activities

separately. In the Alpha limited company, they are getting benefited from this accounting

system by tracking cost of job effectively.

D1. Integration of MAS and MA reports with business process.

It may become difficult for companies to operate different operations and activities

effectively if they fail to integrate their departments with accounting systems (Horton and de

Araujo Wanderley, 2018). Like in the Alpha limited company, their sales department is

integrated with price optimisation system and stock management system. In addition, their

production department utilise important information from stock management report and their

finance department also assess key information from account receivable ageing report.

TASK 2

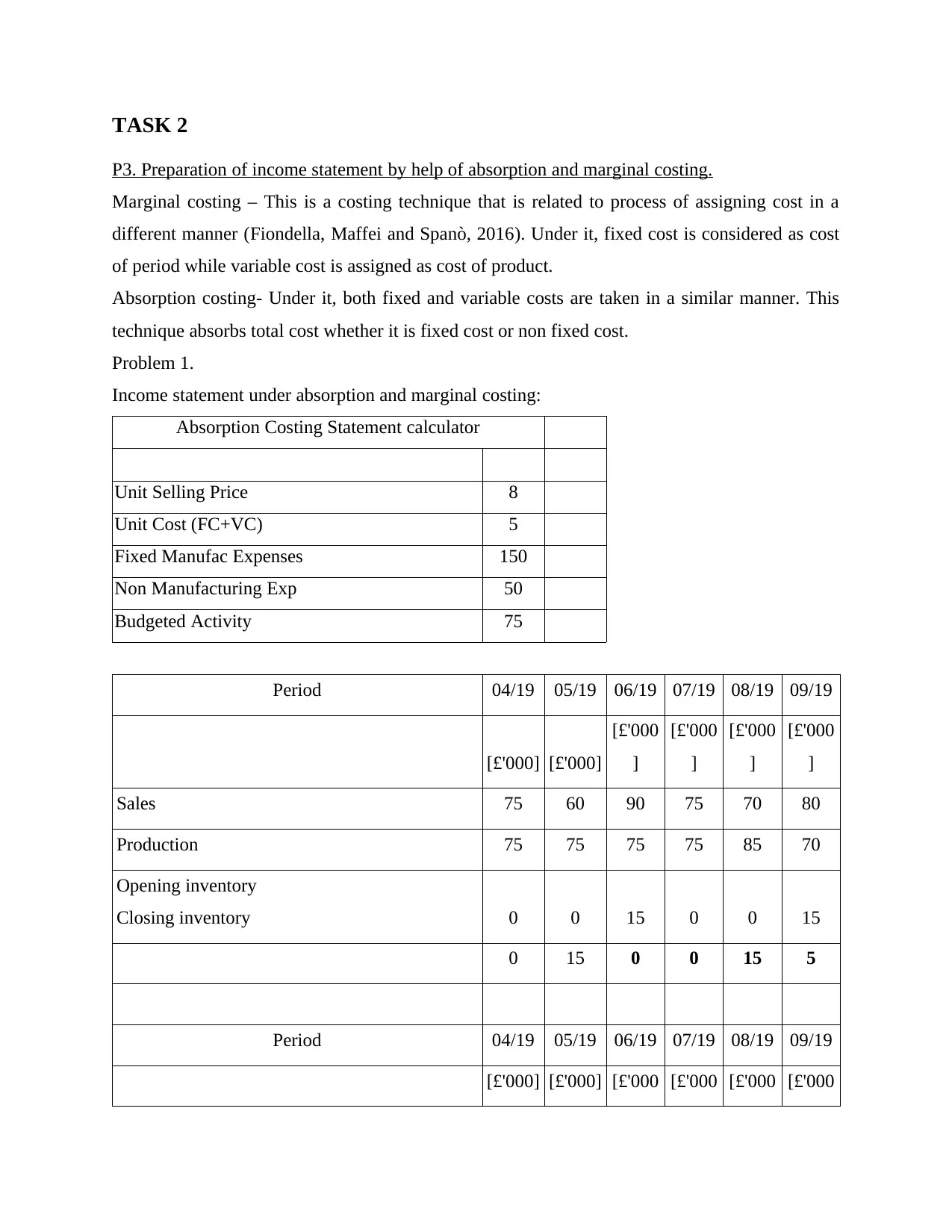

P3. Preparation of income statement by help of absorption and marginal costing.

Marginal costing – This is a costing technique that is related to process of assigning cost in a

different manner (Fiondella, Maffei and Spanò, 2016). Under it, fixed cost is considered as cost

of period while variable cost is assigned as cost of product.

Absorption costing- Under it, both fixed and variable costs are taken in a similar manner. This

technique absorbs total cost whether it is fixed cost or non fixed cost.

Problem 1.

Income statement under absorption and marginal costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000] [£'000 [£'000 [£'000 [£'000

P3. Preparation of income statement by help of absorption and marginal costing.

Marginal costing – This is a costing technique that is related to process of assigning cost in a

different manner (Fiondella, Maffei and Spanò, 2016). Under it, fixed cost is considered as cost

of period while variable cost is assigned as cost of product.

Absorption costing- Under it, both fixed and variable costs are taken in a similar manner. This

technique absorbs total cost whether it is fixed cost or non fixed cost.

Problem 1.

Income statement under absorption and marginal costing:

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000] [£'000 [£'000 [£'000 [£'000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

] ] ] ]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Prod.] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Prod.] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal costing:

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Prodn.] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufac Cost 150 150 150 150 150 150

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Prodn.] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufac Cost 150 150 150 150 150 150

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

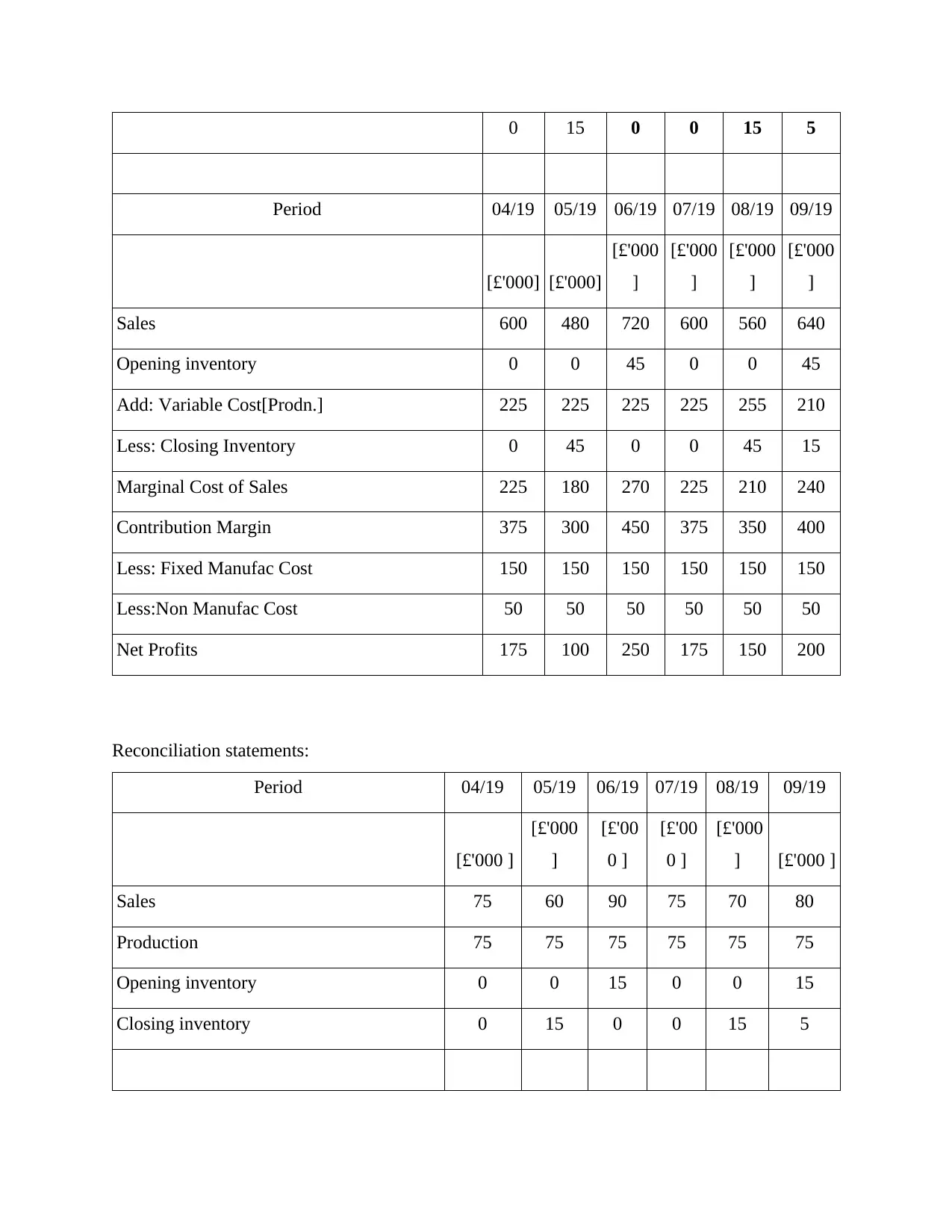

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

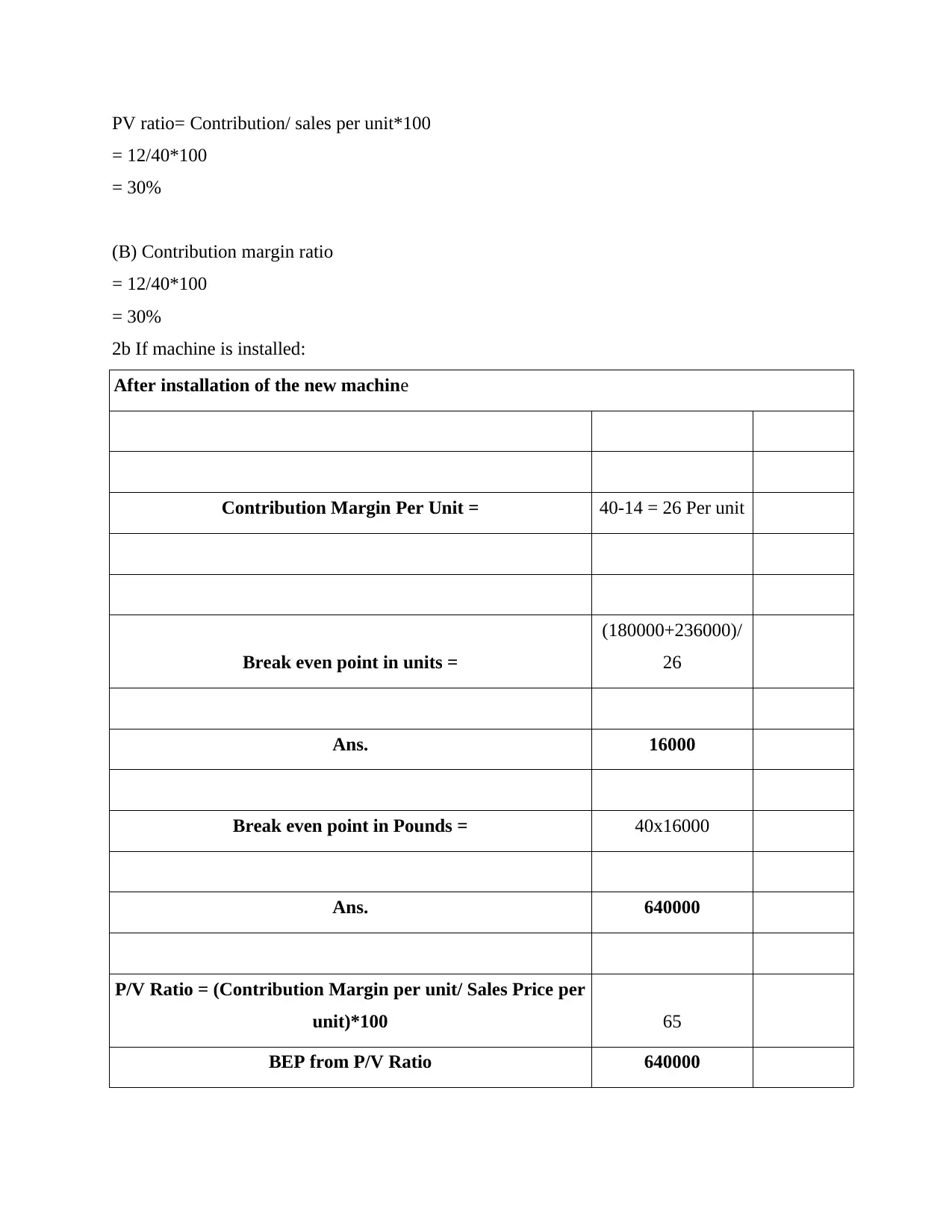

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

After installation of the new machine

Contribution Margin Per Unit = 40-14 = 26 Per unit

Break even point in units =

(180000+236000)/

26

Ans. 16000

Break even point in Pounds = 40x16000

Ans. 640000

P/V Ratio = (Contribution Margin per unit/ Sales Price per

unit)*100 65

BEP from P/V Ratio 640000

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

After installation of the new machine

Contribution Margin Per Unit = 40-14 = 26 Per unit

Break even point in units =

(180000+236000)/

26

Ans. 16000

Break even point in Pounds = 40x16000

Ans. 640000

P/V Ratio = (Contribution Margin per unit/ Sales Price per

unit)*100 65

BEP from P/V Ratio 640000

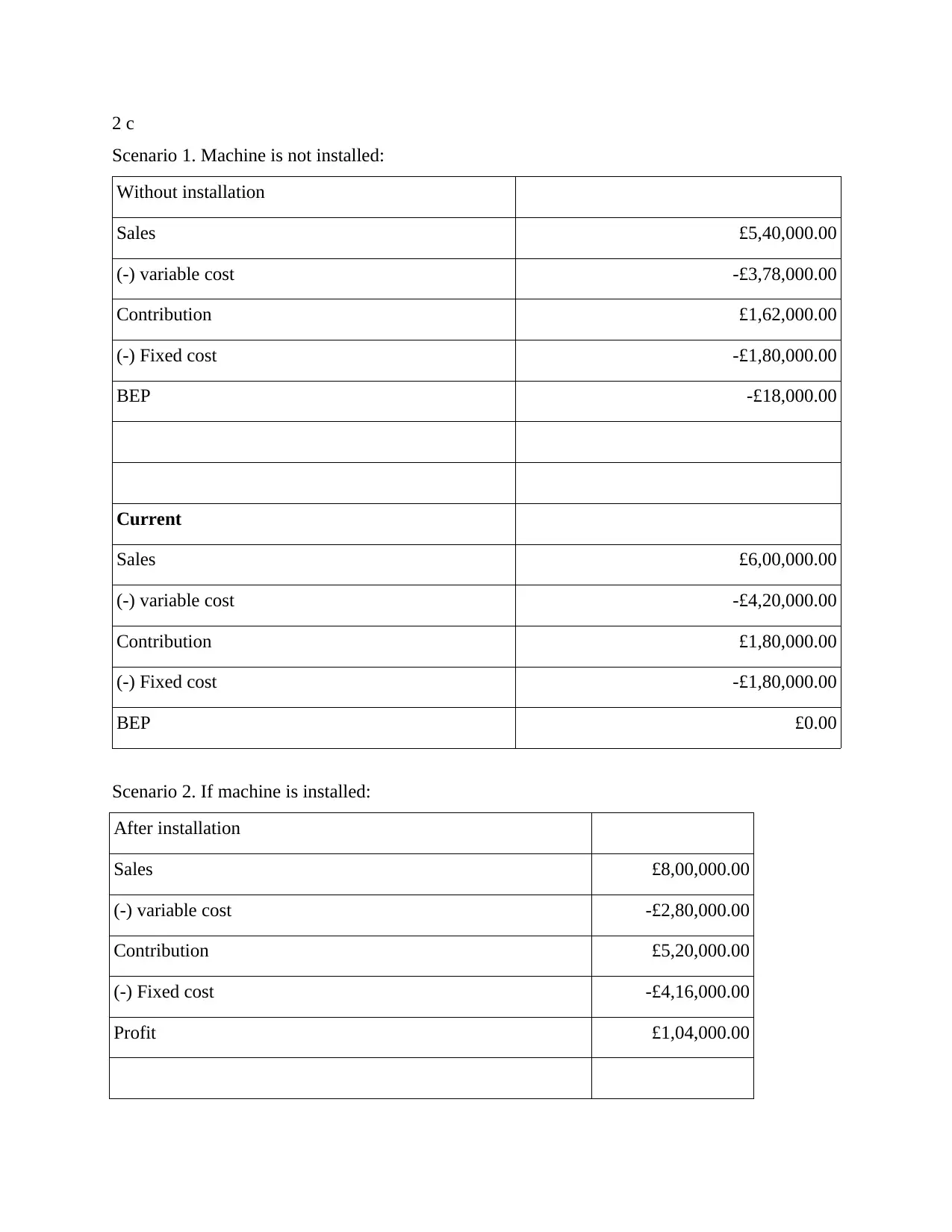

2 c

Scenario 1. Machine is not installed:

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2. If machine is installed:

After installation

Sales £8,00,000.00

(-) variable cost -£2,80,000.00

Contribution £5,20,000.00

(-) Fixed cost -£4,16,000.00

Profit £1,04,000.00

Scenario 1. Machine is not installed:

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2. If machine is installed:

After installation

Sales £8,00,000.00

(-) variable cost -£2,80,000.00

Contribution £5,20,000.00

(-) Fixed cost -£4,16,000.00

Profit £1,04,000.00

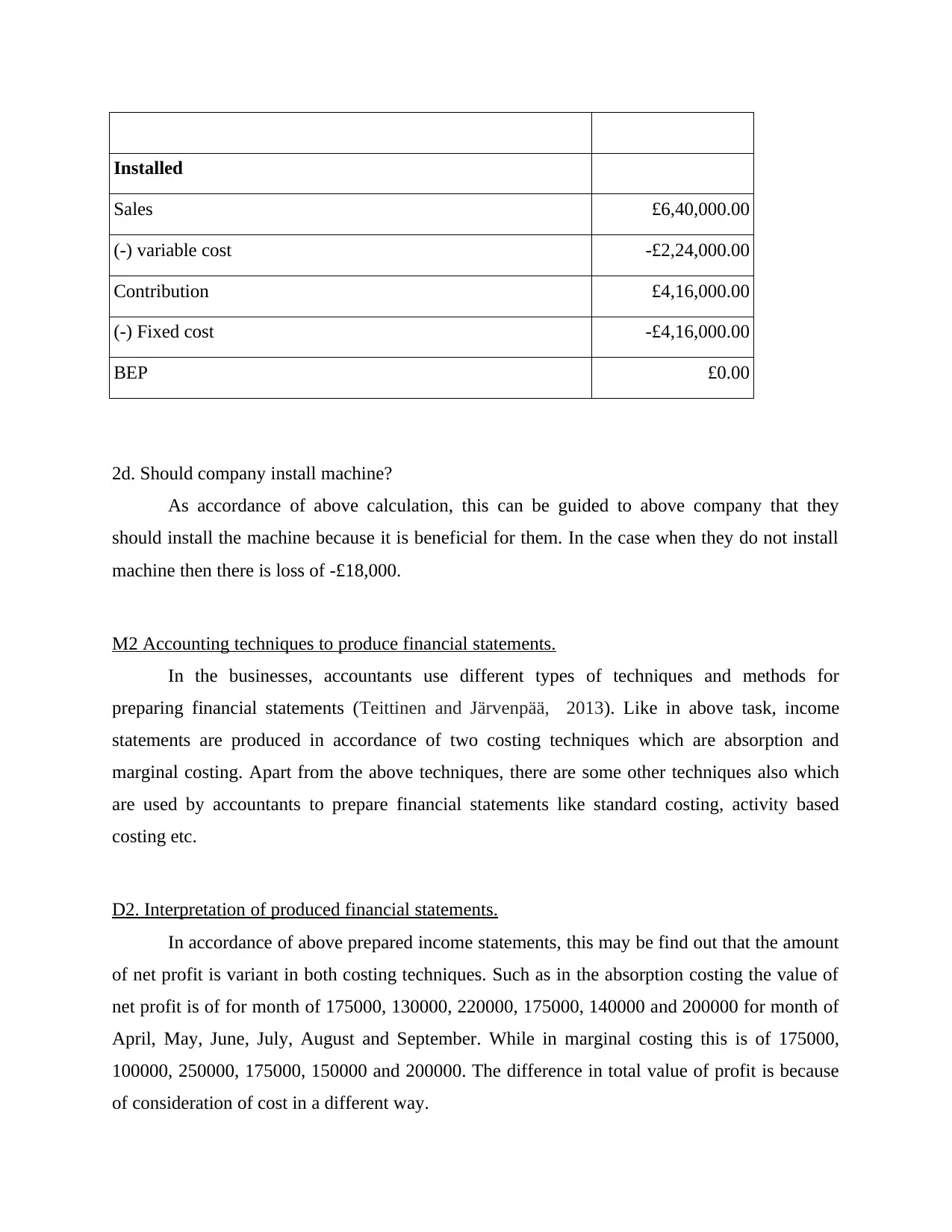

Installed

Sales £6,40,000.00

(-) variable cost -£2,24,000.00

Contribution £4,16,000.00

(-) Fixed cost -£4,16,000.00

BEP £0.00

2d. Should company install machine?

As accordance of above calculation, this can be guided to above company that they

should install the machine because it is beneficial for them. In the case when they do not install

machine then there is loss of -£18,000.

M2 Accounting techniques to produce financial statements.

In the businesses, accountants use different types of techniques and methods for

preparing financial statements (Teittinen and Järvenpää, 2013). Like in above task, income

statements are produced in accordance of two costing techniques which are absorption and

marginal costing. Apart from the above techniques, there are some other techniques also which

are used by accountants to prepare financial statements like standard costing, activity based

costing etc.

D2. Interpretation of produced financial statements.

In accordance of above prepared income statements, this may be find out that the amount

of net profit is variant in both costing techniques. Such as in the absorption costing the value of

net profit is of for month of 175000, 130000, 220000, 175000, 140000 and 200000 for month of

April, May, June, July, August and September. While in marginal costing this is of 175000,

100000, 250000, 175000, 150000 and 200000. The difference in total value of profit is because

of consideration of cost in a different way.

Sales £6,40,000.00

(-) variable cost -£2,24,000.00

Contribution £4,16,000.00

(-) Fixed cost -£4,16,000.00

BEP £0.00

2d. Should company install machine?

As accordance of above calculation, this can be guided to above company that they

should install the machine because it is beneficial for them. In the case when they do not install

machine then there is loss of -£18,000.

M2 Accounting techniques to produce financial statements.

In the businesses, accountants use different types of techniques and methods for

preparing financial statements (Teittinen and Järvenpää, 2013). Like in above task, income

statements are produced in accordance of two costing techniques which are absorption and

marginal costing. Apart from the above techniques, there are some other techniques also which

are used by accountants to prepare financial statements like standard costing, activity based

costing etc.

D2. Interpretation of produced financial statements.

In accordance of above prepared income statements, this may be find out that the amount

of net profit is variant in both costing techniques. Such as in the absorption costing the value of

net profit is of for month of 175000, 130000, 220000, 175000, 140000 and 200000 for month of

April, May, June, July, August and September. While in marginal costing this is of 175000,

100000, 250000, 175000, 150000 and 200000. The difference in total value of profit is because

of consideration of cost in a different way.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4. Advantages and disadvantages of different planning tools of budgetary control.

Budgetary control – This is a technique which is related to process of determining financial and

non financial objectives by different kinds of budgets. The key objective of this approach is to

track and manage overall performance of different aspects in an effective manner.

Zero Base Budgeting - In a financial year, this budget is planned by the company that

does not include past data that helps to run a successful business. This budget begins at zero,

which implies that it does not have a core year, that enables to understand the earnings of the

current year. Alpha Limited 's manager can arrange a zero base budget by preserving the expense

to know the actual year's profits or costs.

Benefits- This budget allows Alpha Ltd to better distribute the budget and assets that will keep

the profits running. It is flexible and can be changed over the course of the year. By preparing

this spending plan, that also provides better coordination with the department, specific

information can be obtained.

Drawbacks- Large manpower attrition or number of staff is needed to plan this budget. It is high

time for an optimistic budget because the preparation of this plan is becoming difficult for the

company. Here is an inexperience that Alpha Limited 's director can find it hard to plan zero

budget.

Master budget -It is one of the centralized planning that is designed for all the

company's divisions (Prencipe and Dekker, 2014). It is a one-year strategy report which is used

as a development tool to define specific targets and organize resources to meet them. In Alpha

limited company, they prepare this budget for managing overall number of operations.

Benefits - The goals and priorities of the organizations are identified via the master budget

summary. It enables to provide information about a business organization's income and

expenses.

Drawback - This budget is compelled for the organization as a whole no department-specific

information is available. Because of it, performance of different types of departments can not be

tracked in an effective manner.

P4. Advantages and disadvantages of different planning tools of budgetary control.

Budgetary control – This is a technique which is related to process of determining financial and

non financial objectives by different kinds of budgets. The key objective of this approach is to

track and manage overall performance of different aspects in an effective manner.

Zero Base Budgeting - In a financial year, this budget is planned by the company that

does not include past data that helps to run a successful business. This budget begins at zero,

which implies that it does not have a core year, that enables to understand the earnings of the

current year. Alpha Limited 's manager can arrange a zero base budget by preserving the expense

to know the actual year's profits or costs.

Benefits- This budget allows Alpha Ltd to better distribute the budget and assets that will keep

the profits running. It is flexible and can be changed over the course of the year. By preparing

this spending plan, that also provides better coordination with the department, specific

information can be obtained.

Drawbacks- Large manpower attrition or number of staff is needed to plan this budget. It is high

time for an optimistic budget because the preparation of this plan is becoming difficult for the

company. Here is an inexperience that Alpha Limited 's director can find it hard to plan zero

budget.

Master budget -It is one of the centralized planning that is designed for all the

company's divisions (Prencipe and Dekker, 2014). It is a one-year strategy report which is used

as a development tool to define specific targets and organize resources to meet them. In Alpha

limited company, they prepare this budget for managing overall number of operations.

Benefits - The goals and priorities of the organizations are identified via the master budget

summary. It enables to provide information about a business organization's income and

expenses.

Drawback - This budget is compelled for the organization as a whole no department-specific

information is available. Because of it, performance of different types of departments can not be

tracked in an effective manner.

Cash budget - An projection of cash flows over a specific time period is a money

budget. Cash budget enables an organization recognise adequate cash accessibility to meet

current needs. If cash preparation for company is effective, all sources will be used efficiently to

meet cash requirement. Such as above Alpha limited company, they are preparing this budget in

order to make proper estimation of cash for upcoming time period.

Benefits- This budget is useful for companies in order to track the need of cash during a

particular time period.

Drawback- Apart from the above mentioned benefits, this budget has some limitations such as it

restricts spending limit of companies.

SWOT analysis of budgets:

Strength-

ZBB- Its strength is accuracy and accountability in financial projection.

Master budget- This budget can keep focus on overall aspects of businesses.

Cash budget- It is too crucial for better management of in and out flow of cash.

Weakness-

ZBB- Higher consumption of cost and time is the key weakness of this budget.

Master budget- Lack of specificity is the main weakness of this budget.

Cash budget- Inaccuracy is the main issue of this budget.

Opportunity-

Opportunity of all three types of budgets is the implementation of new and advanced techniques

so that usefulness may increase.

Threat-

The main threat for above mentioned budgets is the inaccuracy regards to making projection of

financial activities.

budget. Cash budget enables an organization recognise adequate cash accessibility to meet

current needs. If cash preparation for company is effective, all sources will be used efficiently to

meet cash requirement. Such as above Alpha limited company, they are preparing this budget in

order to make proper estimation of cash for upcoming time period.

Benefits- This budget is useful for companies in order to track the need of cash during a

particular time period.

Drawback- Apart from the above mentioned benefits, this budget has some limitations such as it

restricts spending limit of companies.

SWOT analysis of budgets:

Strength-

ZBB- Its strength is accuracy and accountability in financial projection.

Master budget- This budget can keep focus on overall aspects of businesses.

Cash budget- It is too crucial for better management of in and out flow of cash.

Weakness-

ZBB- Higher consumption of cost and time is the key weakness of this budget.

Master budget- Lack of specificity is the main weakness of this budget.

Cash budget- Inaccuracy is the main issue of this budget.

Opportunity-

Opportunity of all three types of budgets is the implementation of new and advanced techniques

so that usefulness may increase.

Threat-

The main threat for above mentioned budgets is the inaccuracy regards to making projection of

financial activities.

M3 Different planning tools for preparing budgets.

The term is a projection of monetary aspects for a particular time period. In this context

different planning tools play a key role in order to make an effective estimation of further time

period's income and expenditures (Serena Chiucchi, 2013). There are various kinds of planning

tools like capital budgeting, flexible budgeting and many more. For example in Alpha limited

company, their accountants are using multiple planning tools named as cash budgeting, zero

based budgeting etc. All these tools are benefiting them to forecasting futuristic budgets. It

becomes possible because under these planning tools a detailed information regards to possible

activities which occur in upcoming time frame.

TASK 4

P5. Role of management accounting in solving financial issues.

Monetary issue- In the aspect of business entities, there are different number of issues which

hamper their profitability and progress (Leotta, Rizza and Ruggeri, 2017). Basically, it is

essential to them to sort out monetary issue in less time period so that loss of funds can be

prevent. In simple term, the financial issues arise in companies because of ineffective

management of monetary resources. As a result, it becomes difficult for companies to satisfy

need of funds to accomplish goals.

Decreasing in efficiency of generating revenue- It is a type of financial issue that is

occurs in companies because of decreasing in value of total sales revenues. Due to this

financial issue, it becomes difficult for companies to manage overall funds in order to

make payment of various expenses. Like in the context of above Tesco plc they face this

financial issue because their total sales revenues has been decreased in a significant

manner.

Increasing in total expenditures- This can be defined as an issue which is faced by

companies because of ineffective control over total number of expenses (Schaltegger,

Viere and Zvezdov, 2012). It mainly impacts to business entities' profitability and

progress in a negative manner. In the Sainsburry's plc they face issue of higher

operational cost.

Methods to identify financial issues:

The term is a projection of monetary aspects for a particular time period. In this context

different planning tools play a key role in order to make an effective estimation of further time

period's income and expenditures (Serena Chiucchi, 2013). There are various kinds of planning

tools like capital budgeting, flexible budgeting and many more. For example in Alpha limited

company, their accountants are using multiple planning tools named as cash budgeting, zero

based budgeting etc. All these tools are benefiting them to forecasting futuristic budgets. It

becomes possible because under these planning tools a detailed information regards to possible

activities which occur in upcoming time frame.

TASK 4

P5. Role of management accounting in solving financial issues.

Monetary issue- In the aspect of business entities, there are different number of issues which

hamper their profitability and progress (Leotta, Rizza and Ruggeri, 2017). Basically, it is

essential to them to sort out monetary issue in less time period so that loss of funds can be

prevent. In simple term, the financial issues arise in companies because of ineffective

management of monetary resources. As a result, it becomes difficult for companies to satisfy

need of funds to accomplish goals.

Decreasing in efficiency of generating revenue- It is a type of financial issue that is

occurs in companies because of decreasing in value of total sales revenues. Due to this

financial issue, it becomes difficult for companies to manage overall funds in order to

make payment of various expenses. Like in the context of above Tesco plc they face this

financial issue because their total sales revenues has been decreased in a significant

manner.

Increasing in total expenditures- This can be defined as an issue which is faced by

companies because of ineffective control over total number of expenses (Schaltegger,

Viere and Zvezdov, 2012). It mainly impacts to business entities' profitability and

progress in a negative manner. In the Sainsburry's plc they face issue of higher

operational cost.

Methods to identify financial issues:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Key performance indicator – This is an approach in that those aspects whose performance

is below standard or higher then standard are focused. Due to this, it becomes easier to

managers to find out actual level of deficit. Under it both financial and non financial

indicators are included. Such as the financial key financial indicator consists information

regards to cost, revenues etc. While non financial indicators include information about

employees relation, suppliers relationship and customers perception. All these

information help to companies to keep focus on monetary issues in an effective manner.

In the context of above Tesco plc, this system is being used in order to find out actual

level of issue.

Benchmarking – This is an approach in which two business entities are compared with

each other in terms of financial aspects (Novas, 2017). The objective of making

comparison is to find out those aspects in which company's performance is weaker and

needed to improve. Like in the Sainsburry's plc they apply this approach for finding

actual financial issue. As accordance of it, they find alternatives to sort issues.

Financial governance – This is a type of technique which is related to focusing on recording

financial transaction in a systematic manner. The objective of this technique is to keep focus on

those aspects which are causing as monetary issue in companies. In the aspect of solving

monetary issues, it contributes in an effective manner because by help of this companies can

track financial deficiencies. According to this, they can become able to overcome issues.

Comparison of companies:

Basis Tesco plc Sainsburry plc

Financial issue The company is facing issue of

decreasing in efficiency of

generating sales revenues. As a

result, they are getting the problem

of having lack of funds in order to

complete different operations and

activities.

Their monetary issue is of increasing

total expenditures. As a result they do

not have sufficient amount of funds to

fulfil working capital requirement. In

addition, their efficiency of making

payment to external parties is also

decreasing in a significant manner.

MAS This company is applying price Their managers have implemented

is below standard or higher then standard are focused. Due to this, it becomes easier to

managers to find out actual level of deficit. Under it both financial and non financial

indicators are included. Such as the financial key financial indicator consists information

regards to cost, revenues etc. While non financial indicators include information about

employees relation, suppliers relationship and customers perception. All these

information help to companies to keep focus on monetary issues in an effective manner.

In the context of above Tesco plc, this system is being used in order to find out actual

level of issue.

Benchmarking – This is an approach in which two business entities are compared with

each other in terms of financial aspects (Novas, 2017). The objective of making

comparison is to find out those aspects in which company's performance is weaker and

needed to improve. Like in the Sainsburry's plc they apply this approach for finding

actual financial issue. As accordance of it, they find alternatives to sort issues.

Financial governance – This is a type of technique which is related to focusing on recording

financial transaction in a systematic manner. The objective of this technique is to keep focus on

those aspects which are causing as monetary issue in companies. In the aspect of solving

monetary issues, it contributes in an effective manner because by help of this companies can

track financial deficiencies. According to this, they can become able to overcome issues.

Comparison of companies:

Basis Tesco plc Sainsburry plc

Financial issue The company is facing issue of

decreasing in efficiency of

generating sales revenues. As a

result, they are getting the problem

of having lack of funds in order to

complete different operations and

activities.

Their monetary issue is of increasing

total expenditures. As a result they do

not have sufficient amount of funds to

fulfil working capital requirement. In

addition, their efficiency of making

payment to external parties is also

decreasing in a significant manner.

MAS This company is applying price Their managers have implemented

optimisation system with an aim of

sorting their financial issue. They

have revised their pricing strategies

as accordance of different customer

segments. As a result more number

of customers made purchase after

changing the price by help of this

accounting system. Hence, the issue

of lower sales resolved as after

increasing total sales revenue.

cost accounting system in order to

keep cost of operations lower. Due to

this, total number of expenditures

have been reduced in an effective

manner. It became possible because

this accounting system track

expenditures on a regular basis. Thus,

implementation of this accounting

helped them in solving financial issue

of higher volume of expenditures.

M4. Role of MAS in order to sort monetary issues.

In this competitive environment companies who resolve their financial issue in less time

period are gaining higher revenue. In this aspect role of accounting systems is too crucial. It is so

because by implementing these systems the managers are companies become able in order to

allocate funds in an effective manner (Kober, Subraamanniam and Watson, 2012). As well as

these accounting systems guide to companies regards to finding actual level of issue and

alternatives to sort the problem in less time & cost. In Alpha limited company, they are applying

different accounting systems like cost accounting system, price optimisation system, job costing

system and many more. By help of these accounting system their various departments are

integrated with each other. In addition, above stated stores like Tesco plc and Sainsburry plc are

applying cost and price optimisation system that helped them in sorting monetary issues in an

effective manner.

D3. Planning tools to solve financial problems.

In the above part of report various types of planning tools are mentioned which can

contribute in a better way to solve financial issue. It becomes possible because different types of

planning tools consists detailed information regards to estimation of further time period's income

and expenditures. As well as these planning tools provide a framework to business entities in

order to identify monetary issues and implementing effective alternatives in order to overcome

sorting their financial issue. They

have revised their pricing strategies

as accordance of different customer

segments. As a result more number

of customers made purchase after

changing the price by help of this

accounting system. Hence, the issue

of lower sales resolved as after

increasing total sales revenue.

cost accounting system in order to

keep cost of operations lower. Due to

this, total number of expenditures

have been reduced in an effective

manner. It became possible because

this accounting system track

expenditures on a regular basis. Thus,

implementation of this accounting

helped them in solving financial issue

of higher volume of expenditures.

M4. Role of MAS in order to sort monetary issues.

In this competitive environment companies who resolve their financial issue in less time

period are gaining higher revenue. In this aspect role of accounting systems is too crucial. It is so

because by implementing these systems the managers are companies become able in order to

allocate funds in an effective manner (Kober, Subraamanniam and Watson, 2012). As well as

these accounting systems guide to companies regards to finding actual level of issue and

alternatives to sort the problem in less time & cost. In Alpha limited company, they are applying

different accounting systems like cost accounting system, price optimisation system, job costing

system and many more. By help of these accounting system their various departments are

integrated with each other. In addition, above stated stores like Tesco plc and Sainsburry plc are

applying cost and price optimisation system that helped them in sorting monetary issues in an

effective manner.

D3. Planning tools to solve financial problems.

In the above part of report various types of planning tools are mentioned which can

contribute in a better way to solve financial issue. It becomes possible because different types of

planning tools consists detailed information regards to estimation of further time period's income

and expenditures. As well as these planning tools provide a framework to business entities in

order to identify monetary issues and implementing effective alternatives in order to overcome

from financial issues (Hoque, Gooneratne, 2013). Like in above Alpha limited company, this

can be find out that they are using various types of planning tools such as cash budgeting, zero

based budgeting and many more which may help in sorting financial issues.

CONCLUSION

As accordance of report this can be concluded that role of MA can not be ignored by

companies in current time period. The report concludes about multiple accounting systems such

as cost accounting system, stock management system etc. along with their role in business

entities. In addition, integration of MA reports with business process is also mentioned in report.

Further, part of report concludes about various calculations are done such as income statement,

break even analysis etc. As well as different planning tools are also covered in report for instance

cash budget, zero based budget are concluded. In end part of report, comparison is done in order

to understand role of MAS to solve monetary issues.

can be find out that they are using various types of planning tools such as cash budgeting, zero

based budgeting and many more which may help in sorting financial issues.

CONCLUSION

As accordance of report this can be concluded that role of MA can not be ignored by

companies in current time period. The report concludes about multiple accounting systems such

as cost accounting system, stock management system etc. along with their role in business

entities. In addition, integration of MA reports with business process is also mentioned in report.

Further, part of report concludes about various calculations are done such as income statement,

break even analysis etc. As well as different planning tools are also covered in report for instance

cash budget, zero based budget are concluded. In end part of report, comparison is done in order

to understand role of MAS to solve monetary issues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Siverbo, S., 2014. The implementation and use of benchmarking in local government: a case

study of the translation of a management accounting innovation. Financial

Accountability & Management. 30(2). pp.121-149.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Kastberg, G. and Siverbo, S., 2016. The role of management accounting and control in making

professional organizations horizontal. Accounting, Auditing & Accountability Journal.

29(3). pp.428-451.

Hirsch, B., Seubert, A. and Sohn, M., 2015. Visualisation of data in management accounting

reports: How supplementary graphs improve every-day management

judgments. Journal of Applied Accounting Research. 16(2). pp.221-239.

Chandar, N., Collier, D. and Miranti, P., 2012. Graph standardization and management

accounting at AT&T during the 1920s. Accounting History. 17(1). pp.35-62.

Horton, K. E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research. 38. pp.39-50.

Fiondella, C., Macchioni, R., Maffei, M. and Spanò, R., 2016, September. Successful changes in

management accounting systems: A healthcare case study. In Accounting Forum (Vol.

40, No. 3, pp. 186-204). Taylor & Francis.

Teittinen, H., Pellinen, J. and Järvenpää, M., 2013. ERP in action—Challenges and benefits for

management control in SME context. International Journal of Accounting Information

Systems. 14(4). pp.278-296.

Prencipe, A., Bar-Yosef, S. and Dekker, H .C., 2014. Accounting research in family firms:

Theoretical and empirical challenges. European Accounting Review. 23(3). pp.361-385.

Serena Chiucchi, M., 2013. Intellectual capital accounting in action: enhancing learning through

interventionist research. Journal of Intellectual Capital. 14(1). pp.48-68.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Schaltegger, S., Viere, T. and Zvezdov, D., 2012. Tapping environmental accounting potentials

of beer brewing: Information needs for successful cleaner production. Journal of

Cleaner Production. 29. pp.1-10.

Novas, J. C., Alves, M. D. C. G. and Sousa, A., 2017. The role of management accounting

systems in the development of intellectual capital. Journal of Intellectual Capital. 18(2).

pp.286-315.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Hoque, Z., A. Covaleski, M. and N. Gooneratne, T., 2013. Theoretical triangulation and

pluralism in research methods in organizational and accounting research. Accounting,

Auditing & Accountability Journal. 26(7). pp.1170-1198.

Books and journals:

Siverbo, S., 2014. The implementation and use of benchmarking in local government: a case

study of the translation of a management accounting innovation. Financial

Accountability & Management. 30(2). pp.121-149.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting

research. Critical Perspectives on Accounting. 45. pp.63-80.

Kastberg, G. and Siverbo, S., 2016. The role of management accounting and control in making

professional organizations horizontal. Accounting, Auditing & Accountability Journal.

29(3). pp.428-451.

Hirsch, B., Seubert, A. and Sohn, M., 2015. Visualisation of data in management accounting

reports: How supplementary graphs improve every-day management

judgments. Journal of Applied Accounting Research. 16(2). pp.221-239.

Chandar, N., Collier, D. and Miranti, P., 2012. Graph standardization and management

accounting at AT&T during the 1920s. Accounting History. 17(1). pp.35-62.

Horton, K. E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research. 38. pp.39-50.

Fiondella, C., Macchioni, R., Maffei, M. and Spanò, R., 2016, September. Successful changes in

management accounting systems: A healthcare case study. In Accounting Forum (Vol.

40, No. 3, pp. 186-204). Taylor & Francis.

Teittinen, H., Pellinen, J. and Järvenpää, M., 2013. ERP in action—Challenges and benefits for

management control in SME context. International Journal of Accounting Information

Systems. 14(4). pp.278-296.

Prencipe, A., Bar-Yosef, S. and Dekker, H .C., 2014. Accounting research in family firms:

Theoretical and empirical challenges. European Accounting Review. 23(3). pp.361-385.

Serena Chiucchi, M., 2013. Intellectual capital accounting in action: enhancing learning through

interventionist research. Journal of Intellectual Capital. 14(1). pp.48-68.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Schaltegger, S., Viere, T. and Zvezdov, D., 2012. Tapping environmental accounting potentials

of beer brewing: Information needs for successful cleaner production. Journal of

Cleaner Production. 29. pp.1-10.

Novas, J. C., Alves, M. D. C. G. and Sousa, A., 2017. The role of management accounting

systems in the development of intellectual capital. Journal of Intellectual Capital. 18(2).

pp.286-315.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Hoque, Z., A. Covaleski, M. and N. Gooneratne, T., 2013. Theoretical triangulation and

pluralism in research methods in organizational and accounting research. Accounting,

Auditing & Accountability Journal. 26(7). pp.1170-1198.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.