Accounting Principles: Financial Analysis, Budgeting & Control

VerifiedAdded on 2023/06/05

|15

|4605

|260

Report

AI Summary

This report provides a comprehensive analysis of accounting principles in complex operational environments, focusing on meeting social requirements and stakeholder expectations. It includes a detailed evaluation of financial statements using various metrics and standards to assess corporate effect...

Unit 5 Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Analyzing critically the role of accountancy in complicated operational environments in meeting

social requirements and company stakeholders...............................................................................1

Utilizing a variety of metrics and standards, a comprehensive analysis of fiscal accounts is

conducted to evaluate corporate effectiveness and reach valid findings.........................................3

Preparation of financial statements for sole trader, partnership and not for profit organisation. 3

a) Calculation of financial ratios of Parcel Portal Ltd for the years 2020 and 2021...................4

b) Evaluation of financial statements of Parcel Portal Ltd and financial ratios to assess the

performance of the company.......................................................................................................5

Explanation of financial control measures and its influence on organisational decision-making...8

a) The benefits and limitations of budgets and budgetary planning and control for the company

.....................................................................................................................................................8

b) Duck café’s cash budget for the 3 months ended 30 June 2022..............................................9

c) Justifications of budgetary control solutions for Duck Café and their impact on the business

to ensure efficient and effective deployment of resources in the future....................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Analyzing critically the role of accountancy in complicated operational environments in meeting

social requirements and company stakeholders...............................................................................1

Utilizing a variety of metrics and standards, a comprehensive analysis of fiscal accounts is

conducted to evaluate corporate effectiveness and reach valid findings.........................................3

Preparation of financial statements for sole trader, partnership and not for profit organisation. 3

a) Calculation of financial ratios of Parcel Portal Ltd for the years 2020 and 2021...................4

b) Evaluation of financial statements of Parcel Portal Ltd and financial ratios to assess the

performance of the company.......................................................................................................5

Explanation of financial control measures and its influence on organisational decision-making...8

a) The benefits and limitations of budgets and budgetary planning and control for the company

.....................................................................................................................................................8

b) Duck café’s cash budget for the 3 months ended 30 June 2022..............................................9

c) Justifications of budgetary control solutions for Duck Café and their impact on the business

to ensure efficient and effective deployment of resources in the future....................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Accountancy standards seem to be the rules and regulations that businesses must adhere to

when disclosing fiscal data (Ahadiat, 2013). Such rules make it simpler to examine fiscal

information by specifying the language, circumstances, and methods which accounting

professionals should employ. Making sure that the corporation's fiscal reports are thorough, fair,

and accurate is the main goal of an accountancy set of regulations. Shareholders can more easily

analyse and derive meaningful information from fiscal accounts as a result. Comparing

accounting data between several organisations is much easier as a result. The paper covers a

comprehensive assessment of the function of accountancy in helping decision-makers satisfy

corporate and social demands in advanced working contexts, a scientific assessment of fiscal

reports to review effectiveness of the company using a variety of measurements and standards to

draw justifiable inferences, and an assessment of budgeting process methods and its influence on

corporate decision-making to assure quick and productive debt management. The paper also

discusses the advantages and disadvantages of budgeting, budgeting preparation, and total

spending management, as well as suggesting corrective measures for issues that the strategy

highlighted for institutional decision-making.

Analyzing critically the role of accountancy in complicated operational

environments in meeting social requirements and company stakeholders

The managerial conduct has always been crucial to the operations of contemporary civilizations.

The calibre of a corporation's administrative procedures determines how effective it is. High-

performance administration is required for this that denotes competence and sane decisions.

Decision-making and management procedures could benefit from accountancy. Delivering fiscal

data on the business undergoing examination is the goal of an accountancy data systems (Albu

and Albu, 2012). People uses this data to take judgments about the fiscal health of their

companies and the success of their businesses. To take managerial choices that will assist the

firm accomplish its goals, it is necessary to evaluate its condition to that of other businesses in

the similar industry or to earlier times. The business and culture both depend on accountants.

Accounting professionals promote strategies for reducing costs, increased revenues, and hazard

decrease to ensure efficient asset usage. The level of assistance provided to this industry's

customers determines how effective it is. The legislative environment in the financial sector

Accountancy standards seem to be the rules and regulations that businesses must adhere to

when disclosing fiscal data (Ahadiat, 2013). Such rules make it simpler to examine fiscal

information by specifying the language, circumstances, and methods which accounting

professionals should employ. Making sure that the corporation's fiscal reports are thorough, fair,

and accurate is the main goal of an accountancy set of regulations. Shareholders can more easily

analyse and derive meaningful information from fiscal accounts as a result. Comparing

accounting data between several organisations is much easier as a result. The paper covers a

comprehensive assessment of the function of accountancy in helping decision-makers satisfy

corporate and social demands in advanced working contexts, a scientific assessment of fiscal

reports to review effectiveness of the company using a variety of measurements and standards to

draw justifiable inferences, and an assessment of budgeting process methods and its influence on

corporate decision-making to assure quick and productive debt management. The paper also

discusses the advantages and disadvantages of budgeting, budgeting preparation, and total

spending management, as well as suggesting corrective measures for issues that the strategy

highlighted for institutional decision-making.

Analyzing critically the role of accountancy in complicated operational

environments in meeting social requirements and company stakeholders

The managerial conduct has always been crucial to the operations of contemporary civilizations.

The calibre of a corporation's administrative procedures determines how effective it is. High-

performance administration is required for this that denotes competence and sane decisions.

Decision-making and management procedures could benefit from accountancy. Delivering fiscal

data on the business undergoing examination is the goal of an accountancy data systems (Albu

and Albu, 2012). People uses this data to take judgments about the fiscal health of their

companies and the success of their businesses. To take managerial choices that will assist the

firm accomplish its goals, it is necessary to evaluate its condition to that of other businesses in

the similar industry or to earlier times. The business and culture both depend on accountants.

Accounting professionals promote strategies for reducing costs, increased revenues, and hazard

decrease to ensure efficient asset usage. The level of assistance provided to this industry's

customers determines how effective it is. The legislative environment in the financial sector

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

protects the quality and reliability of the operations. As a result, it follows that accounting

professionals need to uphold moral and technical norms. They should represent the objectives of

their customers and other secondary consumers, including lenders and shareholders.

Legal and moral limitations and the aim of accountancy features: Effective accountancy

not only allows the management, shareholders, and authorities to compare organisations side-by-

side but likewise assists supervisors in maintaining governance of their firms. In order to enable

immediate comparability of all accountancy methods across all organisations, widely recognized

accountancy standards were developed as the foundation for accountancy in the United States of

America. It is a collection of guidelines and accountancy rules used to present monetary

information (Alleyne and Weekes-Marshall, 2011). American widely recognised accountancy

standards is used by publically listed enterprises in the country. The majority of the globe uses

International Finance Accounting Rules. But the United States of America is likewise switching

from US widely recognised accountancy standards to International Finance Accounting Rules

norms as a result of the proximity. Synchronization aims to ensure that American widely

recognised accountancy standards truly describes International Finance Accounting

Rules requirements. The following are the essential guidelines for fiscal accounting which

businesses and their professionals should follow. The accounting professionals frequently face a

moral conundrum. They work to increase worth through expense cutting and income growth.

While maintaining the general concerns in mind, they strive to produce favourable outcomes for

the business or their customers. Fiscal data should be given honestly and correctly in order to

follow moral guidelines. However, although if companies don't, accounting professionals may

feel pressured to provide favourable outcomes for the company. By offering direction on how the

problem must be handled, ethical accountancy approaches could be used to help people take

wiser choices in both their interpersonal and professional lives. Accounting professionals should

follow the law. But not all circumstances have clear-cut regulations. This indicates that

accounting professionals should consistently behave in accordance with their expertise and

convictions (Bondar, Iershova and Chaika, 2019).

professionals need to uphold moral and technical norms. They should represent the objectives of

their customers and other secondary consumers, including lenders and shareholders.

Legal and moral limitations and the aim of accountancy features: Effective accountancy

not only allows the management, shareholders, and authorities to compare organisations side-by-

side but likewise assists supervisors in maintaining governance of their firms. In order to enable

immediate comparability of all accountancy methods across all organisations, widely recognized

accountancy standards were developed as the foundation for accountancy in the United States of

America. It is a collection of guidelines and accountancy rules used to present monetary

information (Alleyne and Weekes-Marshall, 2011). American widely recognised accountancy

standards is used by publically listed enterprises in the country. The majority of the globe uses

International Finance Accounting Rules. But the United States of America is likewise switching

from US widely recognised accountancy standards to International Finance Accounting Rules

norms as a result of the proximity. Synchronization aims to ensure that American widely

recognised accountancy standards truly describes International Finance Accounting

Rules requirements. The following are the essential guidelines for fiscal accounting which

businesses and their professionals should follow. The accounting professionals frequently face a

moral conundrum. They work to increase worth through expense cutting and income growth.

While maintaining the general concerns in mind, they strive to produce favourable outcomes for

the business or their customers. Fiscal data should be given honestly and correctly in order to

follow moral guidelines. However, although if companies don't, accounting professionals may

feel pressured to provide favourable outcomes for the company. By offering direction on how the

problem must be handled, ethical accountancy approaches could be used to help people take

wiser choices in both their interpersonal and professional lives. Accounting professionals should

follow the law. But not all circumstances have clear-cut regulations. This indicates that

accounting professionals should consistently behave in accordance with their expertise and

convictions (Bondar, Iershova and Chaika, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

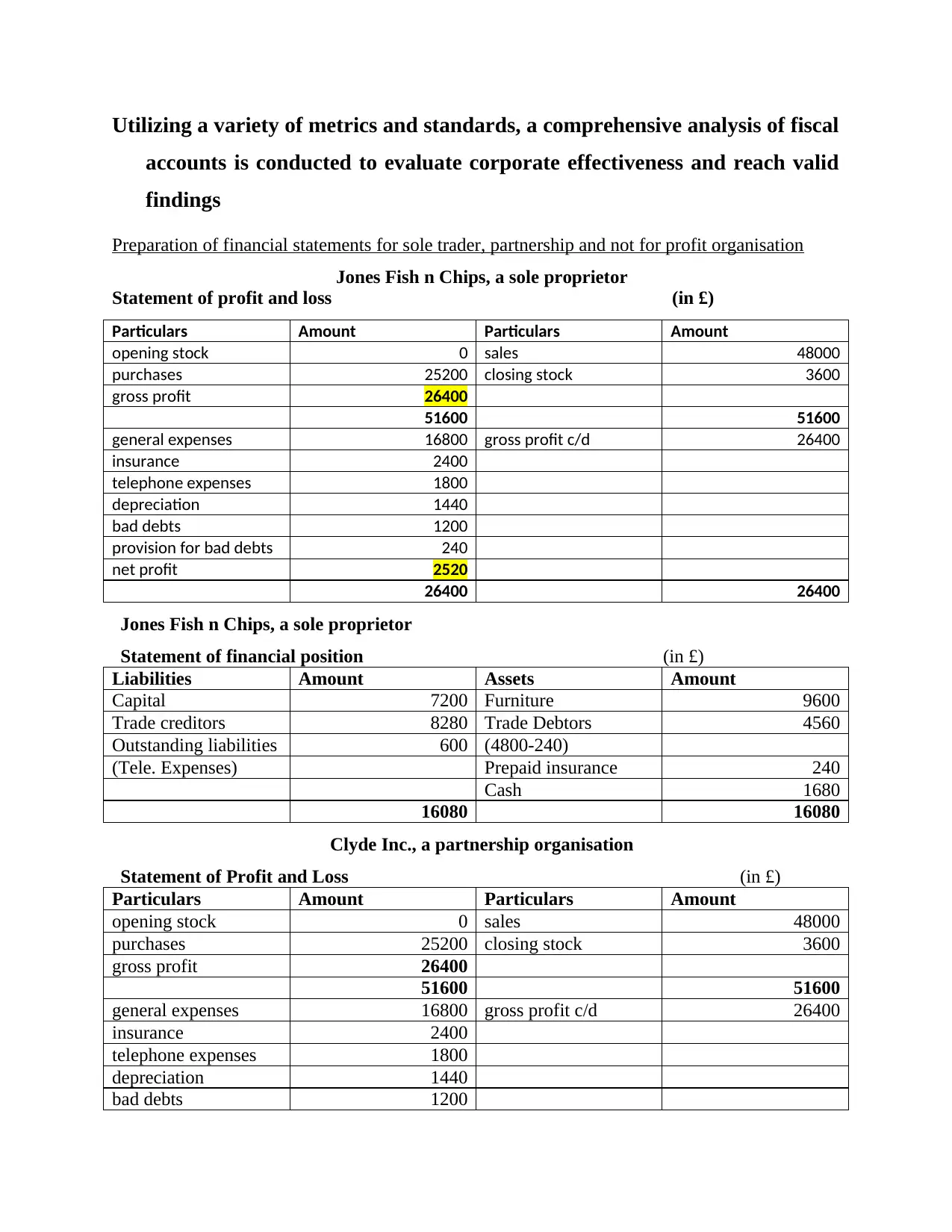

Utilizing a variety of metrics and standards, a comprehensive analysis of fiscal

accounts is conducted to evaluate corporate effectiveness and reach valid

findings

Preparation of financial statements for sole trader, partnership and not for profit organisation

Jones Fish n Chips, a sole proprietor

Statement of profit and loss (in £)

Particulars Amount Particulars Amount

opening stock 0 sales 48000

purchases 25200 closing stock 3600

gross profit 26400

51600 51600

general expenses 16800 gross profit c/d 26400

insurance 2400

telephone expenses 1800

depreciation 1440

bad debts 1200

provision for bad debts 240

net profit 2520

26400 26400

Jones Fish n Chips, a sole proprietor

Statement of financial position (in £)

Liabilities Amount Assets Amount

Capital 7200 Furniture 9600

Trade creditors 8280 Trade Debtors 4560

Outstanding liabilities 600 (4800-240)

(Tele. Expenses) Prepaid insurance 240

Cash 1680

16080 16080

Clyde Inc., a partnership organisation

Statement of Profit and Loss (in £)

Particulars Amount Particulars Amount

opening stock 0 sales 48000

purchases 25200 closing stock 3600

gross profit 26400

51600 51600

general expenses 16800 gross profit c/d 26400

insurance 2400

telephone expenses 1800

depreciation 1440

bad debts 1200

accounts is conducted to evaluate corporate effectiveness and reach valid

findings

Preparation of financial statements for sole trader, partnership and not for profit organisation

Jones Fish n Chips, a sole proprietor

Statement of profit and loss (in £)

Particulars Amount Particulars Amount

opening stock 0 sales 48000

purchases 25200 closing stock 3600

gross profit 26400

51600 51600

general expenses 16800 gross profit c/d 26400

insurance 2400

telephone expenses 1800

depreciation 1440

bad debts 1200

provision for bad debts 240

net profit 2520

26400 26400

Jones Fish n Chips, a sole proprietor

Statement of financial position (in £)

Liabilities Amount Assets Amount

Capital 7200 Furniture 9600

Trade creditors 8280 Trade Debtors 4560

Outstanding liabilities 600 (4800-240)

(Tele. Expenses) Prepaid insurance 240

Cash 1680

16080 16080

Clyde Inc., a partnership organisation

Statement of Profit and Loss (in £)

Particulars Amount Particulars Amount

opening stock 0 sales 48000

purchases 25200 closing stock 3600

gross profit 26400

51600 51600

general expenses 16800 gross profit c/d 26400

insurance 2400

telephone expenses 1800

depreciation 1440

bad debts 1200

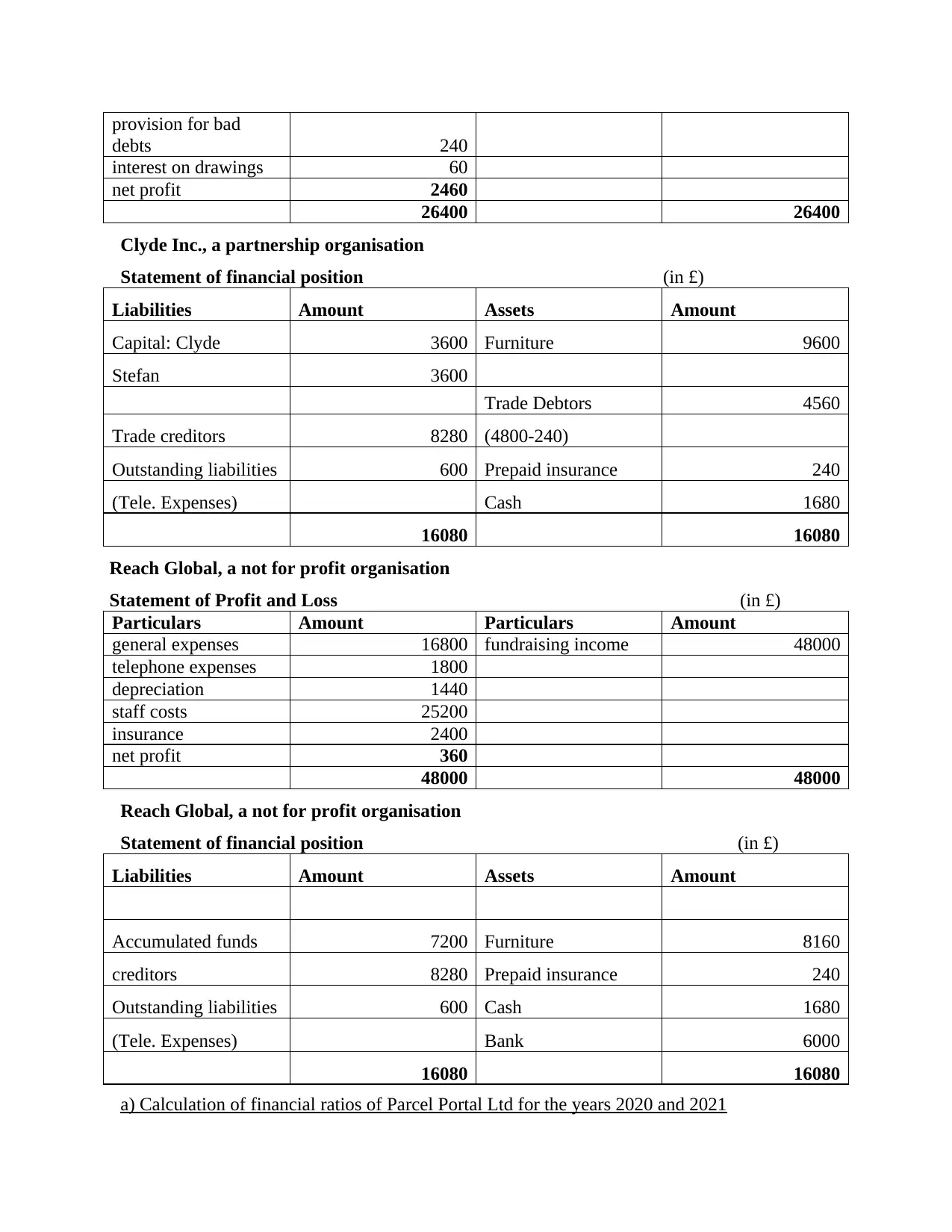

provision for bad

debts 240

interest on drawings 60

net profit 2460

26400 26400

Clyde Inc., a partnership organisation

Statement of financial position (in £)

Liabilities Amount Assets Amount

Capital: Clyde 3600 Furniture 9600

Stefan 3600

Trade Debtors 4560

Trade creditors 8280 (4800-240)

Outstanding liabilities 600 Prepaid insurance 240

(Tele. Expenses) Cash 1680

16080 16080

Reach Global, a not for profit organisation

Statement of Profit and Loss (in £)

Particulars Amount Particulars Amount

general expenses 16800 fundraising income 48000

telephone expenses 1800

depreciation 1440

staff costs 25200

insurance 2400

net profit 360

48000 48000

Reach Global, a not for profit organisation

Statement of financial position (in £)

Liabilities Amount Assets Amount

Accumulated funds 7200 Furniture 8160

creditors 8280 Prepaid insurance 240

Outstanding liabilities 600 Cash 1680

(Tele. Expenses) Bank 6000

16080 16080

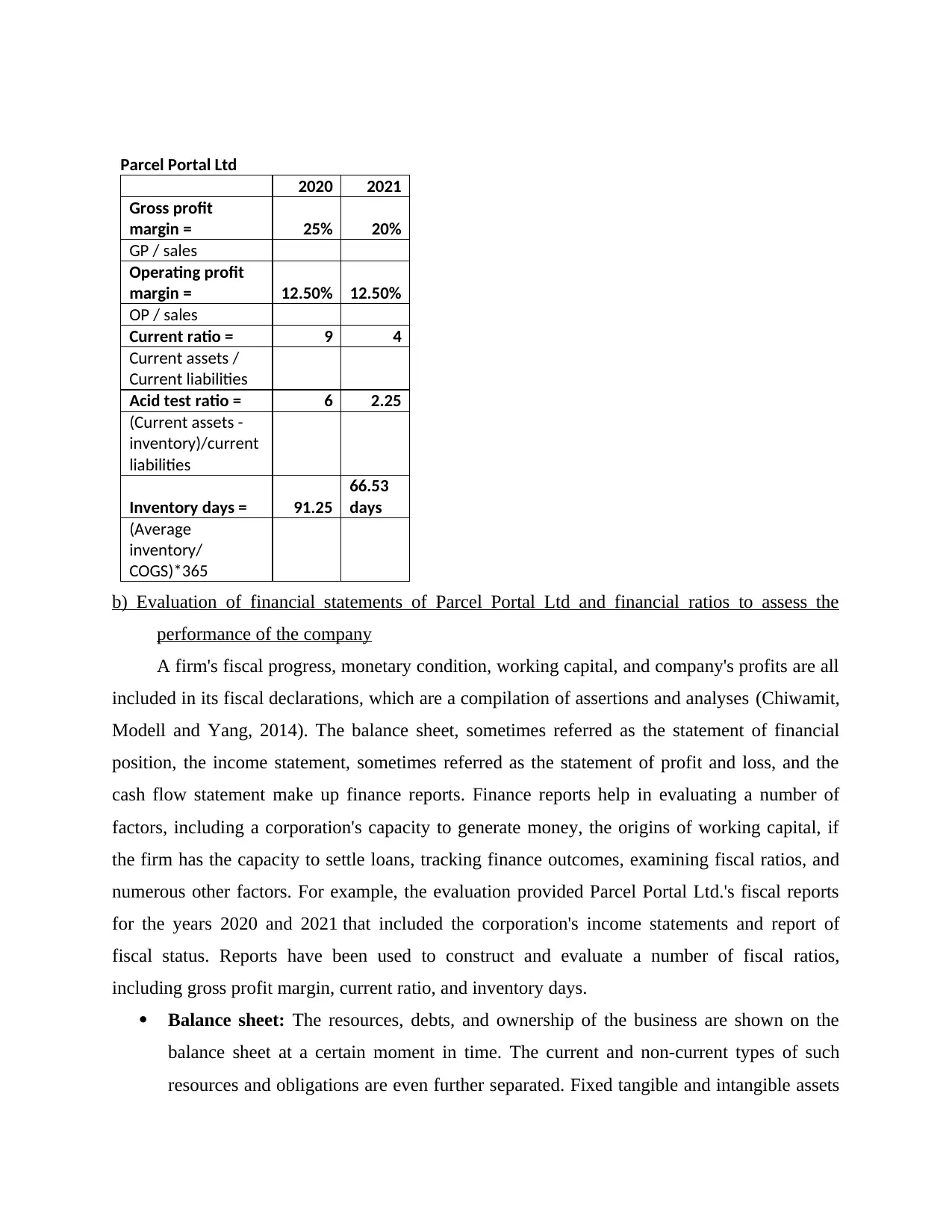

a) Calculation of financial ratios of Parcel Portal Ltd for the years 2020 and 2021

debts 240

interest on drawings 60

net profit 2460

26400 26400

Clyde Inc., a partnership organisation

Statement of financial position (in £)

Liabilities Amount Assets Amount

Capital: Clyde 3600 Furniture 9600

Stefan 3600

Trade Debtors 4560

Trade creditors 8280 (4800-240)

Outstanding liabilities 600 Prepaid insurance 240

(Tele. Expenses) Cash 1680

16080 16080

Reach Global, a not for profit organisation

Statement of Profit and Loss (in £)

Particulars Amount Particulars Amount

general expenses 16800 fundraising income 48000

telephone expenses 1800

depreciation 1440

staff costs 25200

insurance 2400

net profit 360

48000 48000

Reach Global, a not for profit organisation

Statement of financial position (in £)

Liabilities Amount Assets Amount

Accumulated funds 7200 Furniture 8160

creditors 8280 Prepaid insurance 240

Outstanding liabilities 600 Cash 1680

(Tele. Expenses) Bank 6000

16080 16080

a) Calculation of financial ratios of Parcel Portal Ltd for the years 2020 and 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Parcel Portal Ltd

2020 2021

Gross profit

margin = 25% 20%

GP / sales

Operating profit

margin = 12.50% 12.50%

OP / sales

Current ratio = 9 4

Current assets /

Current liabilities

Acid test ratio = 6 2.25

(Current assets -

inventory)/current

liabilities

Inventory days = 91.25

66.53

days

(Average

inventory/

COGS)*365

b) Evaluation of financial statements of Parcel Portal Ltd and financial ratios to assess the

performance of the company

A firm's fiscal progress, monetary condition, working capital, and company's profits are all

included in its fiscal declarations, which are a compilation of assertions and analyses (Chiwamit,

Modell and Yang, 2014). The balance sheet, sometimes referred as the statement of financial

position, the income statement, sometimes referred as the statement of profit and loss, and the

cash flow statement make up finance reports. Finance reports help in evaluating a number of

factors, including a corporation's capacity to generate money, the origins of working capital, if

the firm has the capacity to settle loans, tracking finance outcomes, examining fiscal ratios, and

numerous other factors. For example, the evaluation provided Parcel Portal Ltd.'s fiscal reports

for the years 2020 and 2021 that included the corporation's income statements and report of

fiscal status. Reports have been used to construct and evaluate a number of fiscal ratios,

including gross profit margin, current ratio, and inventory days.

Balance sheet: The resources, debts, and ownership of the business are shown on the

balance sheet at a certain moment in time. The current and non-current types of such

resources and obligations are even further separated. Fixed tangible and intangible assets

2020 2021

Gross profit

margin = 25% 20%

GP / sales

Operating profit

margin = 12.50% 12.50%

OP / sales

Current ratio = 9 4

Current assets /

Current liabilities

Acid test ratio = 6 2.25

(Current assets -

inventory)/current

liabilities

Inventory days = 91.25

66.53

days

(Average

inventory/

COGS)*365

b) Evaluation of financial statements of Parcel Portal Ltd and financial ratios to assess the

performance of the company

A firm's fiscal progress, monetary condition, working capital, and company's profits are all

included in its fiscal declarations, which are a compilation of assertions and analyses (Chiwamit,

Modell and Yang, 2014). The balance sheet, sometimes referred as the statement of financial

position, the income statement, sometimes referred as the statement of profit and loss, and the

cash flow statement make up finance reports. Finance reports help in evaluating a number of

factors, including a corporation's capacity to generate money, the origins of working capital, if

the firm has the capacity to settle loans, tracking finance outcomes, examining fiscal ratios, and

numerous other factors. For example, the evaluation provided Parcel Portal Ltd.'s fiscal reports

for the years 2020 and 2021 that included the corporation's income statements and report of

fiscal status. Reports have been used to construct and evaluate a number of fiscal ratios,

including gross profit margin, current ratio, and inventory days.

Balance sheet: The resources, debts, and ownership of the business are shown on the

balance sheet at a certain moment in time. The current and non-current types of such

resources and obligations are even further separated. Fixed tangible and intangible assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that may be used for a prolonged period of time are included in non-current assets. For

example, Parcel Portal Ltd.'s provided example analysis shows that in 2021, its non-

current assets will include equipments worth £16800. Current assets are those that could

be quickly turned into money, such as inside a year. In the practical example provided,

stocks, accounts receivable, and banks totalling £48000 are displayed underneath the

heading of current assets in 2021. The two sides of a balance sheet has to be equal. One is

for assets, while the other is for equities and obligations (Ejiogu and Ejiogu, 2018). Total

assets equals the sum of debts and equities. In 2021, Parcel Portal Ltd.'s balance sheet

shows a sum of £64800 on both parts. The sum on the balance sheet must match the sum

of cash and cash alternatives at the conclusion of the cash flow statement. The balance

sheet's provisions are adjusted to reflect net income from the report of profit and loss.

Income statement: Investment's initial consideration is the income statement. It displays

how the business has performed through time. The beginning of this section lists the sales

revenue, that according to the practical example provided is £96000 in 2020 and £144000

in 2021. After deducting the cost of sales, the gross profit amounts to £24000 in 2020 and

£28800 in 2021. The net profit for the company is then calculated by subtracting

operational revenue from operational expenditures. The net operational income in the

example is £12000 in 2020 and rises to £18000 in 2021. To depict quantities in this

report, accruing and matched accountancy rules are used. A monetary foundation is not

used to portray the quantities. This assertion is used to assess productivity. The firm's

increasing net income in the provided Parcel Portal Ltd. practical example is a positive

development (Fleischman, Johnson and Walker, 2017).

Finance ratios: To calculate monetary ratios and obtain useful information regarding

something like an operation of the corporation, numbers collected from the accounting

information are used. Numerical analytics is used to examine a corporation's viability, stability,

debt, profits, expansion, rates of return, and other factors using data derived from the fiscal

reports. The outcomes, operational effectiveness, and fiscal vulnerability of the business are

implied by several ratios. The finance ratios have 2 primary purposes: they help monitor

corporate success and help evaluate the profitability of the business in comparison to the sector

norm. Analyzing ratios for each interval makes it easier to monitor how numbers shift

throughout term and identify any recent developments (Gamage, 2016). It is possible to tell if a

example, Parcel Portal Ltd.'s provided example analysis shows that in 2021, its non-

current assets will include equipments worth £16800. Current assets are those that could

be quickly turned into money, such as inside a year. In the practical example provided,

stocks, accounts receivable, and banks totalling £48000 are displayed underneath the

heading of current assets in 2021. The two sides of a balance sheet has to be equal. One is

for assets, while the other is for equities and obligations (Ejiogu and Ejiogu, 2018). Total

assets equals the sum of debts and equities. In 2021, Parcel Portal Ltd.'s balance sheet

shows a sum of £64800 on both parts. The sum on the balance sheet must match the sum

of cash and cash alternatives at the conclusion of the cash flow statement. The balance

sheet's provisions are adjusted to reflect net income from the report of profit and loss.

Income statement: Investment's initial consideration is the income statement. It displays

how the business has performed through time. The beginning of this section lists the sales

revenue, that according to the practical example provided is £96000 in 2020 and £144000

in 2021. After deducting the cost of sales, the gross profit amounts to £24000 in 2020 and

£28800 in 2021. The net profit for the company is then calculated by subtracting

operational revenue from operational expenditures. The net operational income in the

example is £12000 in 2020 and rises to £18000 in 2021. To depict quantities in this

report, accruing and matched accountancy rules are used. A monetary foundation is not

used to portray the quantities. This assertion is used to assess productivity. The firm's

increasing net income in the provided Parcel Portal Ltd. practical example is a positive

development (Fleischman, Johnson and Walker, 2017).

Finance ratios: To calculate monetary ratios and obtain useful information regarding

something like an operation of the corporation, numbers collected from the accounting

information are used. Numerical analytics is used to examine a corporation's viability, stability,

debt, profits, expansion, rates of return, and other factors using data derived from the fiscal

reports. The outcomes, operational effectiveness, and fiscal vulnerability of the business are

implied by several ratios. The finance ratios have 2 primary purposes: they help monitor

corporate success and help evaluate the profitability of the business in comparison to the sector

norm. Analyzing ratios for each interval makes it easier to monitor how numbers shift

throughout term and identify any recent developments (Gamage, 2016). It is possible to tell if a

business is performing higher or less than the sector standard by analyzing its fiscal ratios to

those of its rivals. A shareholder could determine whether company is using its assets the most

effectively, for example, by evaluating the return on assets of the 2 firms. Both interior and

exterior consumers of the organisation might benefit from fiscal ratios. Interior viewers comprise

workers, the managerial group, and the proprietors. Exterior viewers comprise fiscal analysts,

lenders, shareholders, regulators, and others. For the 2020 and 2021 fiscal years, the accounting

calculations for the business Parcel Portal Ltd. must be evaluated and thus has been shown below

in a very precise and accurate manner:

Current ratio: A particular kind of liquidity ratio is the current ratio. Working capital

ratio or banker's ratio are some alternative terms for current ratio. It illustrates the

connection between current assets and liabilities. By dividing total current assets by total

current liabilities, it is determined. To determine if a firm's current ratio is excessive or

lower during the present time, compare the current ratio to its prior current ratio. One is

the optimal current ratio. Repaying the debts won't be a problem if the current ratio is 2.

However, if the current ratio is under 2, it may be difficult to discharge creditors, which

would have an effect on activities. The Parcel Portal Ltd. in the practical example does

have a current ratio of 9 in 2020. The corporation may not be handling its current assets

properly because of the substantially larger current ratio. It dropped to 4 that really is

positive news for the business, in 2021 (Hemmer and Labro, 2017). The corporation's

current ratio is higher compared to the sector standard that corresponds to a current ratio

of 3.

Acid test ratio: Another kind of liquidity ratio is the acid test ratio. This type of ratio is

also known as quick ratio and is typically used to assess a company's liquidity condition.

Additionally, it is often important to know a corporation's ability to repay off borrowing

more quickly than the current ratio suggests. Because of this, the most liquid assets are

used in the computation of this ratio. It is determined by dividing current liabilities by

current assets, omitting inventories. The acid test ratio must be greater than 1, like the

existing ratio. If this ratio is less than 1, it means that the company may not have enough

liquid assets to cover its present liabilities. In the example scenario provided, the acid test

ratio for Parcel Portal Ltd was 6 in 2020 before falling to 2.25 in 2021. The firm's acid

test ratio in 2021 is less than the 2.5 mean for the sector (Hrasky and Jones, 2016).

those of its rivals. A shareholder could determine whether company is using its assets the most

effectively, for example, by evaluating the return on assets of the 2 firms. Both interior and

exterior consumers of the organisation might benefit from fiscal ratios. Interior viewers comprise

workers, the managerial group, and the proprietors. Exterior viewers comprise fiscal analysts,

lenders, shareholders, regulators, and others. For the 2020 and 2021 fiscal years, the accounting

calculations for the business Parcel Portal Ltd. must be evaluated and thus has been shown below

in a very precise and accurate manner:

Current ratio: A particular kind of liquidity ratio is the current ratio. Working capital

ratio or banker's ratio are some alternative terms for current ratio. It illustrates the

connection between current assets and liabilities. By dividing total current assets by total

current liabilities, it is determined. To determine if a firm's current ratio is excessive or

lower during the present time, compare the current ratio to its prior current ratio. One is

the optimal current ratio. Repaying the debts won't be a problem if the current ratio is 2.

However, if the current ratio is under 2, it may be difficult to discharge creditors, which

would have an effect on activities. The Parcel Portal Ltd. in the practical example does

have a current ratio of 9 in 2020. The corporation may not be handling its current assets

properly because of the substantially larger current ratio. It dropped to 4 that really is

positive news for the business, in 2021 (Hemmer and Labro, 2017). The corporation's

current ratio is higher compared to the sector standard that corresponds to a current ratio

of 3.

Acid test ratio: Another kind of liquidity ratio is the acid test ratio. This type of ratio is

also known as quick ratio and is typically used to assess a company's liquidity condition.

Additionally, it is often important to know a corporation's ability to repay off borrowing

more quickly than the current ratio suggests. Because of this, the most liquid assets are

used in the computation of this ratio. It is determined by dividing current liabilities by

current assets, omitting inventories. The acid test ratio must be greater than 1, like the

existing ratio. If this ratio is less than 1, it means that the company may not have enough

liquid assets to cover its present liabilities. In the example scenario provided, the acid test

ratio for Parcel Portal Ltd was 6 in 2020 before falling to 2.25 in 2021. The firm's acid

test ratio in 2021 is less than the 2.5 mean for the sector (Hrasky and Jones, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory turnover days: This efficiency ratio determines how long an entity keeps

goods in warehouse prior to actually selling it. This ratio calculates the amount of days

that money is held in the inventories. It is computed by multiplying the duration of the

term that really is typically 365 days, by the costs of inventories divided by the costs of

selling. A lower inventory days ratio is preferable to a higher inventory days ratio since it

suggests that a company is effective at managing its inventories and performing well in

regards of selling. The Parcel Portal Ltd. in the practical example has 91.25 inventory

days in 2020, but that number drops to 66.53 days in 2021 that would be positive for the

business. The business has fewer inventory days than the sector norm.

Gross profitability margin: One class of profitability ratios is gross profitability margin.

Such ratios assess the firm's ability to generate revenue in relation to selling, balance

sheet resources, capital, and operational expenses. The firm's revenue after deducting the

costs of selling is known as the gross profitability margin (Isaac Roque and Cañizares

Roig, 2019). The gross profitability in relation to aggregate selling is compared. In the

example scenario provided, Parcel Portal Ltd. had a 25% gross profitability in 2020; by

2021, it had dropped to 20%. It is not encouraging for the business. Yet, it is not

significantly low when compared to the sector median that is also 20%. If, however, it

falls below the sector norm, the business must increase its effectiveness by lowering its

costs of selling.

Operational profitability margin: Estimated to assess operational effectiveness is the

operational profitability margin. It contrasts the firm's operational profit in relation to

aggregate selling. In the example scenario provided, Parcel Portal Ltd.'s 12.5% in 2020

and 2021 are identical. The effectiveness of its operations remains unchanged. Business

does have a higher operational profitability margin than the 10% market median.

Consequently, this is encouraging for the business in the long run as it can help the firm

to stand ahead of all its competitors in the market in which it is operational.

Explanation of financial control measures and its influence on organisational

decision-making

a) The benefits and limitations of budgets and budgetary planning and control for the company

Budget advantages:

goods in warehouse prior to actually selling it. This ratio calculates the amount of days

that money is held in the inventories. It is computed by multiplying the duration of the

term that really is typically 365 days, by the costs of inventories divided by the costs of

selling. A lower inventory days ratio is preferable to a higher inventory days ratio since it

suggests that a company is effective at managing its inventories and performing well in

regards of selling. The Parcel Portal Ltd. in the practical example has 91.25 inventory

days in 2020, but that number drops to 66.53 days in 2021 that would be positive for the

business. The business has fewer inventory days than the sector norm.

Gross profitability margin: One class of profitability ratios is gross profitability margin.

Such ratios assess the firm's ability to generate revenue in relation to selling, balance

sheet resources, capital, and operational expenses. The firm's revenue after deducting the

costs of selling is known as the gross profitability margin (Isaac Roque and Cañizares

Roig, 2019). The gross profitability in relation to aggregate selling is compared. In the

example scenario provided, Parcel Portal Ltd. had a 25% gross profitability in 2020; by

2021, it had dropped to 20%. It is not encouraging for the business. Yet, it is not

significantly low when compared to the sector median that is also 20%. If, however, it

falls below the sector norm, the business must increase its effectiveness by lowering its

costs of selling.

Operational profitability margin: Estimated to assess operational effectiveness is the

operational profitability margin. It contrasts the firm's operational profit in relation to

aggregate selling. In the example scenario provided, Parcel Portal Ltd.'s 12.5% in 2020

and 2021 are identical. The effectiveness of its operations remains unchanged. Business

does have a higher operational profitability margin than the 10% market median.

Consequently, this is encouraging for the business in the long run as it can help the firm

to stand ahead of all its competitors in the market in which it is operational.

Explanation of financial control measures and its influence on organisational

decision-making

a) The benefits and limitations of budgets and budgetary planning and control for the company

Budget advantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

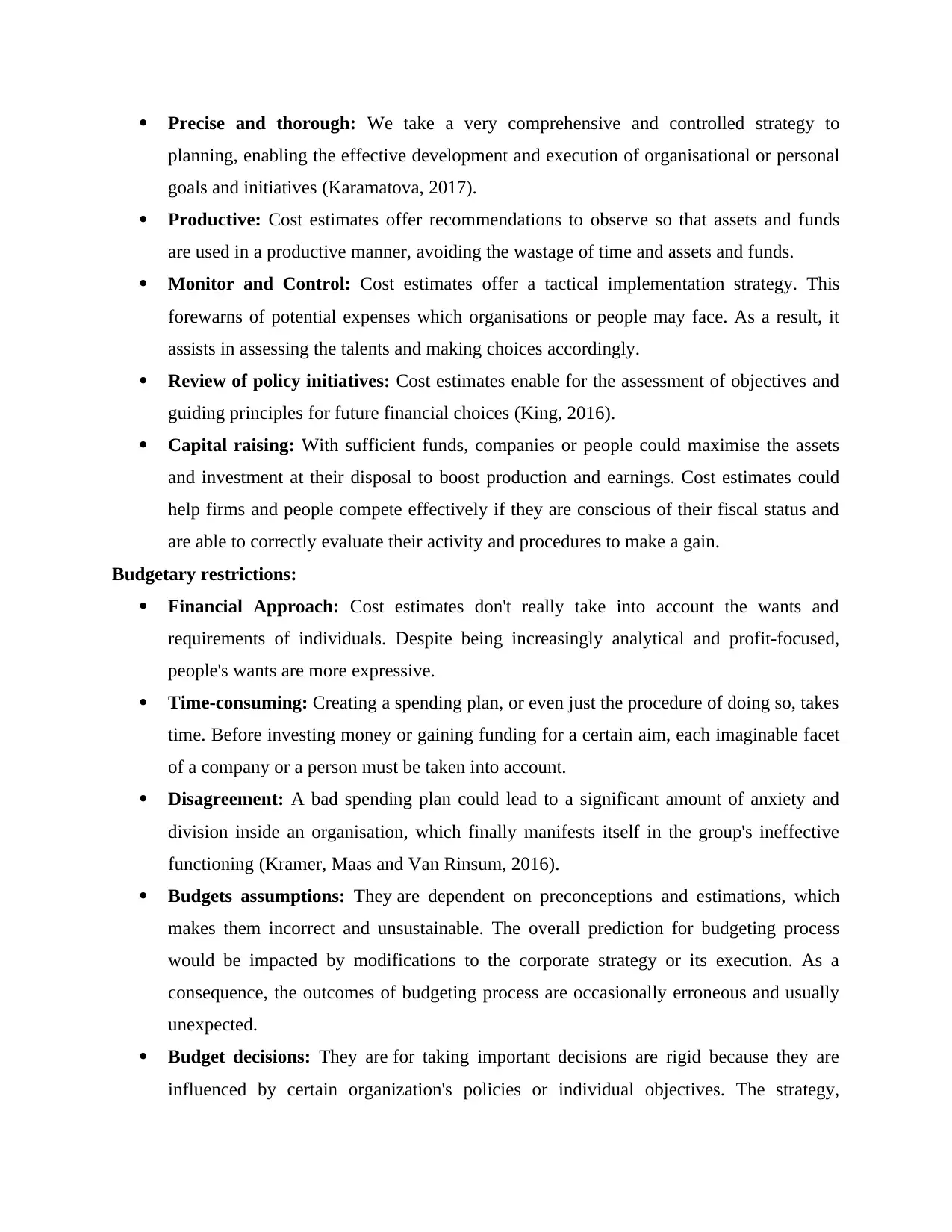

Precise and thorough: We take a very comprehensive and controlled strategy to

planning, enabling the effective development and execution of organisational or personal

goals and initiatives (Karamatova, 2017).

Productive: Cost estimates offer recommendations to observe so that assets and funds

are used in a productive manner, avoiding the wastage of time and assets and funds.

Monitor and Control: Cost estimates offer a tactical implementation strategy. This

forewarns of potential expenses which organisations or people may face. As a result, it

assists in assessing the talents and making choices accordingly.

Review of policy initiatives: Cost estimates enable for the assessment of objectives and

guiding principles for future financial choices (King, 2016).

Capital raising: With sufficient funds, companies or people could maximise the assets

and investment at their disposal to boost production and earnings. Cost estimates could

help firms and people compete effectively if they are conscious of their fiscal status and

are able to correctly evaluate their activity and procedures to make a gain.

Budgetary restrictions:

Financial Approach: Cost estimates don't really take into account the wants and

requirements of individuals. Despite being increasingly analytical and profit-focused,

people's wants are more expressive.

Time-consuming: Creating a spending plan, or even just the procedure of doing so, takes

time. Before investing money or gaining funding for a certain aim, each imaginable facet

of a company or a person must be taken into account.

Disagreement: A bad spending plan could lead to a significant amount of anxiety and

division inside an organisation, which finally manifests itself in the group's ineffective

functioning (Kramer, Maas and Van Rinsum, 2016).

Budgets assumptions: They are dependent on preconceptions and estimations, which

makes them incorrect and unsustainable. The overall prediction for budgeting process

would be impacted by modifications to the corporate strategy or its execution. As a

consequence, the outcomes of budgeting process are occasionally erroneous and usually

unexpected.

Budget decisions: They are for taking important decisions are rigid because they are

influenced by certain organization's policies or individual objectives. The strategy,

planning, enabling the effective development and execution of organisational or personal

goals and initiatives (Karamatova, 2017).

Productive: Cost estimates offer recommendations to observe so that assets and funds

are used in a productive manner, avoiding the wastage of time and assets and funds.

Monitor and Control: Cost estimates offer a tactical implementation strategy. This

forewarns of potential expenses which organisations or people may face. As a result, it

assists in assessing the talents and making choices accordingly.

Review of policy initiatives: Cost estimates enable for the assessment of objectives and

guiding principles for future financial choices (King, 2016).

Capital raising: With sufficient funds, companies or people could maximise the assets

and investment at their disposal to boost production and earnings. Cost estimates could

help firms and people compete effectively if they are conscious of their fiscal status and

are able to correctly evaluate their activity and procedures to make a gain.

Budgetary restrictions:

Financial Approach: Cost estimates don't really take into account the wants and

requirements of individuals. Despite being increasingly analytical and profit-focused,

people's wants are more expressive.

Time-consuming: Creating a spending plan, or even just the procedure of doing so, takes

time. Before investing money or gaining funding for a certain aim, each imaginable facet

of a company or a person must be taken into account.

Disagreement: A bad spending plan could lead to a significant amount of anxiety and

division inside an organisation, which finally manifests itself in the group's ineffective

functioning (Kramer, Maas and Van Rinsum, 2016).

Budgets assumptions: They are dependent on preconceptions and estimations, which

makes them incorrect and unsustainable. The overall prediction for budgeting process

would be impacted by modifications to the corporate strategy or its execution. As a

consequence, the outcomes of budgeting process are occasionally erroneous and usually

unexpected.

Budget decisions: They are for taking important decisions are rigid because they are

influenced by certain organization's policies or individual objectives. The strategy,

though, could not be altered under any circumstances if it becomes essential to evaluate

the fiscal condition in light of marketplace fluctuations.

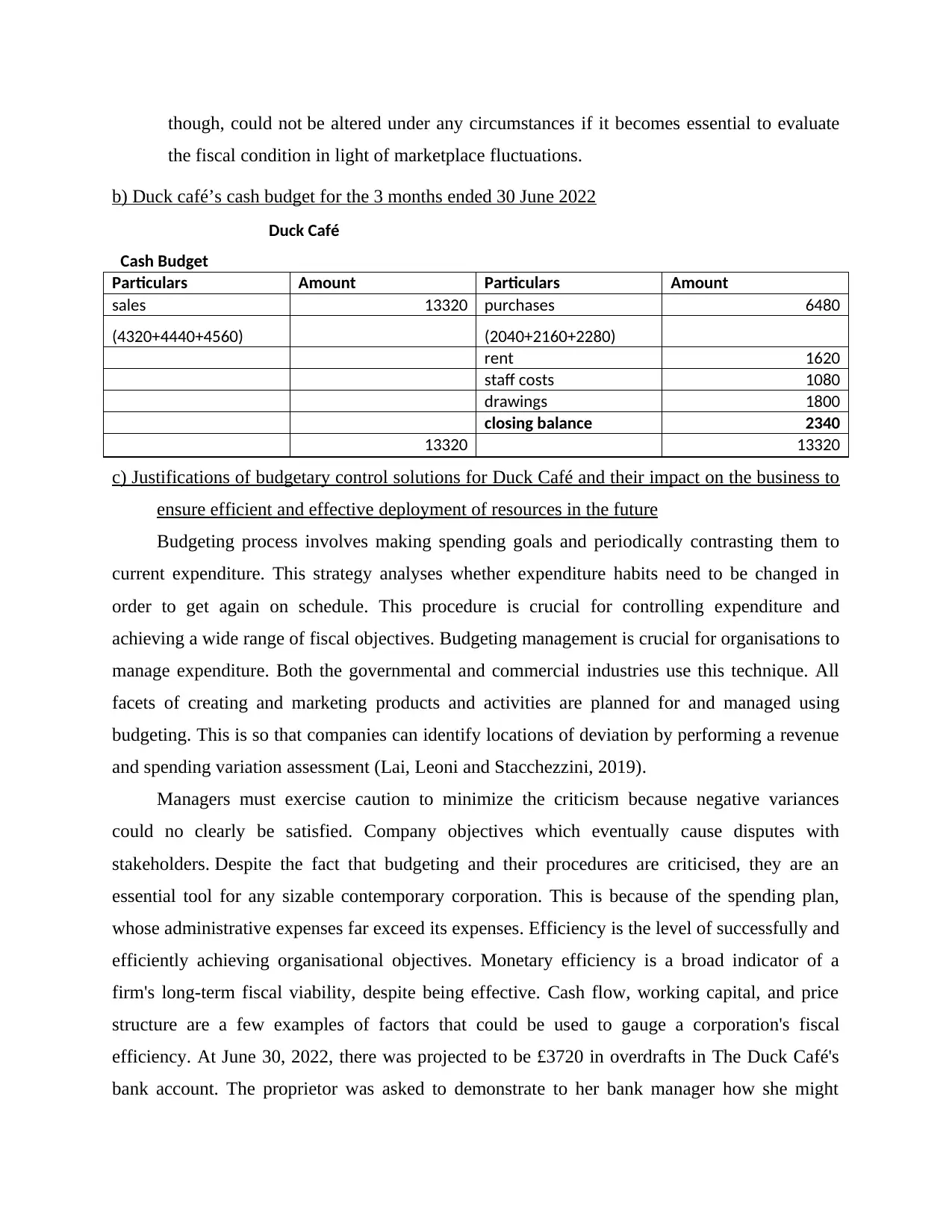

b) Duck café’s cash budget for the 3 months ended 30 June 2022

Duck Café

Cash Budget

Particulars Amount Particulars Amount

sales 13320 purchases 6480

(4320+4440+4560) (2040+2160+2280)

rent 1620

staff costs 1080

drawings 1800

closing balance 2340

13320 13320

c) Justifications of budgetary control solutions for Duck Café and their impact on the business to

ensure efficient and effective deployment of resources in the future

Budgeting process involves making spending goals and periodically contrasting them to

current expenditure. This strategy analyses whether expenditure habits need to be changed in

order to get again on schedule. This procedure is crucial for controlling expenditure and

achieving a wide range of fiscal objectives. Budgeting management is crucial for organisations to

manage expenditure. Both the governmental and commercial industries use this technique. All

facets of creating and marketing products and activities are planned for and managed using

budgeting. This is so that companies can identify locations of deviation by performing a revenue

and spending variation assessment (Lai, Leoni and Stacchezzini, 2019).

Managers must exercise caution to minimize the criticism because negative variances

could no clearly be satisfied. Company objectives which eventually cause disputes with

stakeholders. Despite the fact that budgeting and their procedures are criticised, they are an

essential tool for any sizable contemporary corporation. This is because of the spending plan,

whose administrative expenses far exceed its expenses. Efficiency is the level of successfully and

efficiently achieving organisational objectives. Monetary efficiency is a broad indicator of a

firm's long-term fiscal viability, despite being effective. Cash flow, working capital, and price

structure are a few examples of factors that could be used to gauge a corporation's fiscal

efficiency. At June 30, 2022, there was projected to be £3720 in overdrafts in The Duck Café's

bank account. The proprietor was asked to demonstrate to her bank manager how she might

the fiscal condition in light of marketplace fluctuations.

b) Duck café’s cash budget for the 3 months ended 30 June 2022

Duck Café

Cash Budget

Particulars Amount Particulars Amount

sales 13320 purchases 6480

(4320+4440+4560) (2040+2160+2280)

rent 1620

staff costs 1080

drawings 1800

closing balance 2340

13320 13320

c) Justifications of budgetary control solutions for Duck Café and their impact on the business to

ensure efficient and effective deployment of resources in the future

Budgeting process involves making spending goals and periodically contrasting them to

current expenditure. This strategy analyses whether expenditure habits need to be changed in

order to get again on schedule. This procedure is crucial for controlling expenditure and

achieving a wide range of fiscal objectives. Budgeting management is crucial for organisations to

manage expenditure. Both the governmental and commercial industries use this technique. All

facets of creating and marketing products and activities are planned for and managed using

budgeting. This is so that companies can identify locations of deviation by performing a revenue

and spending variation assessment (Lai, Leoni and Stacchezzini, 2019).

Managers must exercise caution to minimize the criticism because negative variances

could no clearly be satisfied. Company objectives which eventually cause disputes with

stakeholders. Despite the fact that budgeting and their procedures are criticised, they are an

essential tool for any sizable contemporary corporation. This is because of the spending plan,

whose administrative expenses far exceed its expenses. Efficiency is the level of successfully and

efficiently achieving organisational objectives. Monetary efficiency is a broad indicator of a

firm's long-term fiscal viability, despite being effective. Cash flow, working capital, and price

structure are a few examples of factors that could be used to gauge a corporation's fiscal

efficiency. At June 30, 2022, there was projected to be £3720 in overdrafts in The Duck Café's

bank account. The proprietor was asked to demonstrate to her bank manager how she might

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

lower this over the next three months. As could be observed from the previously created

financial budgeting, the proprietor was able to obtain the overdraft decrease. The price dropped

to £2340 (van Helden, 2016).

CONCLUSION

The pressure on businesses to operate profitably and productively while adhering to

ethically and ecologically responsible principles is growing. Although accountancy is about

monitoring, analyzing, and documenting, managerial accountancy's main purpose is to support

strategy, administration, and strategic planning. In the end, it is a collection of culturally

constructed activities wherein members of the company create and understand accountancy data

based on how they each engage with the managerial accountancy systems. All of the study

findings included in the evaluation were summarised in the aforementioned study. It simply

demonstrates the budgeting constraints, ratio assessment, and income reports. One could have a

basic comprehension of the key components of finance accounting by reading the

aforementioned paper.

financial budgeting, the proprietor was able to obtain the overdraft decrease. The price dropped

to £2340 (van Helden, 2016).

CONCLUSION

The pressure on businesses to operate profitably and productively while adhering to

ethically and ecologically responsible principles is growing. Although accountancy is about

monitoring, analyzing, and documenting, managerial accountancy's main purpose is to support

strategy, administration, and strategic planning. In the end, it is a collection of culturally

constructed activities wherein members of the company create and understand accountancy data

based on how they each engage with the managerial accountancy systems. All of the study

findings included in the evaluation were summarised in the aforementioned study. It simply

demonstrates the budgeting constraints, ratio assessment, and income reports. One could have a

basic comprehension of the key components of finance accounting by reading the

aforementioned paper.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Ahadiat, N., 2013. In search of practice-based topics for management accounting education.

Available at SSRN 2355853.

Albu, N. and Albu, C. N., 2012. Factors associated with the adoption and use of management

accounting techniques in developing countries: The case of Romania. Journal of

International Financial Management & Accounting. 23(3). pp.245-276.

Alleyne, P. and Weekes-Marshall, D., 2011. An exploratory study of management accounting

practices in manufacturing companies in Barbados. International Journal of Business

and Social Science. 2(10).

Bondar, M., Iershova, N. and Chaika, T., 2019. Strategic management accounting as an

information platform for measuring innovation of the enterprise. SHS Web of

Conferences.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Ejiogu, A. R. and Ejiogu, C., 2018. Translation in the “contact zone” between accounting and

human resource management. Accounting, Auditing & Accountability Journal.

Fleischman, G.M., Johnson, E.N. and Walker, K.B., 2017. An exploratory investigation of

management accounting service quality dimensions using servqual and servperf. In

Advances in Management Accounting. Emerald Publishing Limited.

Gamage, P., 2016. Big Data: are accounting educators ready?. Journal of Accounting and

Management Information Systems. 15(3). pp.588-604.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Hrasky, S. and Jones, M., 2016, December. Lake Pedder: Accounting, environmental decision-

making, nature and impression management. In Accounting forum (Vol. 40, No. 4, pp.

285-299). No longer published by Elsevier.

Isaac Roque, D. and Cañizares Roig, M., 2019. ¿ Cómo vincular la información que brinda la

contabilidad de gestión ambiental con los proyectos de inversión?(How to Link the

Information Provided by Environmental Management Accounting With Investment

Projects?). How to Link the Information Provided by Environmental Management

Accounting With Investment Projects.

Karamatova, L., 2017. Management Accounting and ERP Systems: Factors behind the choice of

information systems when exercising management accounting.

King, D., 2016. Management Accounting–Combining Blended Learning and Mobile Apps to

Enhance the Flipped Classroom Concept.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

Lai, A., Leoni, G. and Stacchezzini, R., 2019. Accounting and governance in diverse settings–an

introduction.

Books and journals

Ahadiat, N., 2013. In search of practice-based topics for management accounting education.

Available at SSRN 2355853.

Albu, N. and Albu, C. N., 2012. Factors associated with the adoption and use of management

accounting techniques in developing countries: The case of Romania. Journal of

International Financial Management & Accounting. 23(3). pp.245-276.

Alleyne, P. and Weekes-Marshall, D., 2011. An exploratory study of management accounting

practices in manufacturing companies in Barbados. International Journal of Business

and Social Science. 2(10).

Bondar, M., Iershova, N. and Chaika, T., 2019. Strategic management accounting as an

information platform for measuring innovation of the enterprise. SHS Web of

Conferences.

Chiwamit, P., Modell, S. and Yang, C. L., 2014. The societal relevance of management

accounting innovations: economic value added and institutional work in the fields of

Chinese and Thai state-owned enterprises. Accounting and Business Research. 44(2).

pp.144-180.

Ejiogu, A. R. and Ejiogu, C., 2018. Translation in the “contact zone” between accounting and

human resource management. Accounting, Auditing & Accountability Journal.

Fleischman, G.M., Johnson, E.N. and Walker, K.B., 2017. An exploratory investigation of

management accounting service quality dimensions using servqual and servperf. In

Advances in Management Accounting. Emerald Publishing Limited.

Gamage, P., 2016. Big Data: are accounting educators ready?. Journal of Accounting and

Management Information Systems. 15(3). pp.588-604.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Hrasky, S. and Jones, M., 2016, December. Lake Pedder: Accounting, environmental decision-

making, nature and impression management. In Accounting forum (Vol. 40, No. 4, pp.

285-299). No longer published by Elsevier.

Isaac Roque, D. and Cañizares Roig, M., 2019. ¿ Cómo vincular la información que brinda la

contabilidad de gestión ambiental con los proyectos de inversión?(How to Link the

Information Provided by Environmental Management Accounting With Investment

Projects?). How to Link the Information Provided by Environmental Management

Accounting With Investment Projects.

Karamatova, L., 2017. Management Accounting and ERP Systems: Factors behind the choice of

information systems when exercising management accounting.

King, D., 2016. Management Accounting–Combining Blended Learning and Mobile Apps to

Enhance the Flipped Classroom Concept.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

Lai, A., Leoni, G. and Stacchezzini, R., 2019. Accounting and governance in diverse settings–an

introduction.

van Helden, J., 2016. Literature review and challenging research agenda on politicians’ use of

accounting information. Public Money & Management. 36(7). pp.531-538.

accounting information. Public Money & Management. 36(7). pp.531-538.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.