Business Management: Unit 5 Management Accounting Report

VerifiedAdded on 2022/12/28

|19

|5462

|44

Report

AI Summary

This report delves into the intricacies of management accounting, exploring its core principles, benefits, and various system types, such as cost accounting, inventory management, and price optimization. It examines different reporting methods, including cost, budget, and performance reports, and illustrates their practical application through a case study of Tesco Plc. The report critically evaluates the integration of management accounting systems and their impact on reporting efficiency, while also comparing absorption and marginal costing methods. Furthermore, it analyzes the advantages and disadvantages of planning tools used for budgetary control, assesses how management accounting aids in addressing financial challenges, and evaluates the role of these tools in achieving sustainable organizational success. The report provides a comprehensive overview of how management accounting principles and tools can be leveraged to enhance financial decision-making and improve overall business performance.

UNIT-5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Scenario 1.........................................................................................................................................3

Meaning of management accounting and principles & benefits of management accounting.....3

Types of management accounting systems and their requirements ............................................4

Methods of management accounting reporting............................................................................5

Application of management accounting systems in the Tesco Plc..............................................6

Critical evaluation of integration of management accounting system and management

accounting reporting....................................................................................................................7

Interpretation of income statement under absorption costing and marginal costing...................7

Scenario 2.......................................................................................................................................10

Advantages and disadvantages of types of planning tools used for budgetary control.............10

Critical evaluation of how management accounting helps to deal with financial problems.....11

Analysis of the use of planning tools in preparing and forecasting budget...............................11

Analyses of role of management accounting systems in solving financial problems and help in

decision making.........................................................................................................................13

Evaluation of how solving financial problems using planning tools lead organization to

sustainable success.....................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Scenario 1.........................................................................................................................................3

Meaning of management accounting and principles & benefits of management accounting.....3

Types of management accounting systems and their requirements ............................................4

Methods of management accounting reporting............................................................................5

Application of management accounting systems in the Tesco Plc..............................................6

Critical evaluation of integration of management accounting system and management

accounting reporting....................................................................................................................7

Interpretation of income statement under absorption costing and marginal costing...................7

Scenario 2.......................................................................................................................................10

Advantages and disadvantages of types of planning tools used for budgetary control.............10

Critical evaluation of how management accounting helps to deal with financial problems.....11

Analysis of the use of planning tools in preparing and forecasting budget...............................11

Analyses of role of management accounting systems in solving financial problems and help in

decision making.........................................................................................................................13

Evaluation of how solving financial problems using planning tools lead organization to

sustainable success.....................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION

The study of how managers create management accounting reports by following

accounting fundamentals. This report will help to understand the management accounting term

along with the requirements of types of management accounting systems to eliminate the extra

time, extra cost and enhancing the speed of the work. This report will also state the different

method used for management accounting reporting along with the financial statement report.

This report will also base on the study of the benefits of MA systems and their application on

Tesco plc of UK. These report will also critically evaluate the benefits of the integration of

management accounting systems in order to prepare reports. This report also includes the

comparison of income statement between absorption costing and marginal costing and also

interpret the best method to adopt by the company. This report also states the advantages,

disadvantages and uses of planning tools in order to control budgets. This report also compare

how company can use different accounting systems in order to achieve the goals and objectives

of the company.

MAIN BODY

Scenario 1

Meaning of management accounting and principles & benefits of management accounting

Management accounting uses the information provided by the financial accounting in

order to take decisions and help the company in achieving its goals. MA information is only

available to company's internal managements. MA systems are the systems with the help of

which the different processes of the company is get identified, measured, evaluated and

communicated (Zahid, and Vagif, 2020).

Principles of management accounting

The four management accounting principles that every organization must follow in order

to run the business in effective and efficient manner. It includes influence, relevance, value and

credibility.

Influence: Clear communication is important in every organization for proper decision-

making. In order to achieve the targets of the organization it is significant to

communicate the vision and mission of the organization with the all staffs of the

company from top to bottom.

The study of how managers create management accounting reports by following

accounting fundamentals. This report will help to understand the management accounting term

along with the requirements of types of management accounting systems to eliminate the extra

time, extra cost and enhancing the speed of the work. This report will also state the different

method used for management accounting reporting along with the financial statement report.

This report will also base on the study of the benefits of MA systems and their application on

Tesco plc of UK. These report will also critically evaluate the benefits of the integration of

management accounting systems in order to prepare reports. This report also includes the

comparison of income statement between absorption costing and marginal costing and also

interpret the best method to adopt by the company. This report also states the advantages,

disadvantages and uses of planning tools in order to control budgets. This report also compare

how company can use different accounting systems in order to achieve the goals and objectives

of the company.

MAIN BODY

Scenario 1

Meaning of management accounting and principles & benefits of management accounting

Management accounting uses the information provided by the financial accounting in

order to take decisions and help the company in achieving its goals. MA information is only

available to company's internal managements. MA systems are the systems with the help of

which the different processes of the company is get identified, measured, evaluated and

communicated (Zahid, and Vagif, 2020).

Principles of management accounting

The four management accounting principles that every organization must follow in order

to run the business in effective and efficient manner. It includes influence, relevance, value and

credibility.

Influence: Clear communication is important in every organization for proper decision-

making. In order to achieve the targets of the organization it is significant to

communicate the vision and mission of the organization with the all staffs of the

company from top to bottom.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relevance: It is the most significant principles of the management accounting which

indicate that managers have to analyse and use all the relevant information in their

decision-making. They have to make a proper balance between the past, present and

future, internal, external, financial and non-financial informations.

Value: It is a principle which enables the organization to know which value is required to

be produced by the organization to earn higher profitability and reduces the cost per

value. For this purpose, situation analysis is need to be implemented by the organization

to know the opportunities and challenges attach with each situation. It further helps in

decision-making.

Credibility: Being responsible and credible for their decisions help in making the

decisions more purposeful and relevant. For this purpose, organizations have to get

feedback from their customers and staffs and try to solve their queries to improve the

trust and reliability of the stakeholders.

Benefits of management accounting

Management accounting helps in creating and executing the plans for smooth operations

of the businesses.

It also helps in controlling and minimizing the gaps between actual and planned one by

use of variance analysis.

Management accounting helps in decision-making in order to serve the best and

improved services to the customer's.

Management accounting also helps in increasing coordination among the departments in

order to prepare budgets.

It also beneficial for improving the efficiency and productivity of the employees of the

organizations.

Types of management accounting systems and their requirements

The different types of management accounting systems are cost accounting, inventory

management, price optimization systems. Their requirements in the company are based on the

benefits they provide to the company. For example, Tesco Plc.

Cost accounting systems: It is a software which helps the company to know the cost of

its product and services. The requirement of cost accounting system is in the controlling

indicate that managers have to analyse and use all the relevant information in their

decision-making. They have to make a proper balance between the past, present and

future, internal, external, financial and non-financial informations.

Value: It is a principle which enables the organization to know which value is required to

be produced by the organization to earn higher profitability and reduces the cost per

value. For this purpose, situation analysis is need to be implemented by the organization

to know the opportunities and challenges attach with each situation. It further helps in

decision-making.

Credibility: Being responsible and credible for their decisions help in making the

decisions more purposeful and relevant. For this purpose, organizations have to get

feedback from their customers and staffs and try to solve their queries to improve the

trust and reliability of the stakeholders.

Benefits of management accounting

Management accounting helps in creating and executing the plans for smooth operations

of the businesses.

It also helps in controlling and minimizing the gaps between actual and planned one by

use of variance analysis.

Management accounting helps in decision-making in order to serve the best and

improved services to the customer's.

Management accounting also helps in increasing coordination among the departments in

order to prepare budgets.

It also beneficial for improving the efficiency and productivity of the employees of the

organizations.

Types of management accounting systems and their requirements

The different types of management accounting systems are cost accounting, inventory

management, price optimization systems. Their requirements in the company are based on the

benefits they provide to the company. For example, Tesco Plc.

Cost accounting systems: It is a software which helps the company to know the cost of

its product and services. The requirement of cost accounting system is in the controlling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of cost. It is also required to know the profitability of each product, service, jobs,

departments or operations. It also required in the valuation of inventory and setting

different prices in order to cover cost. For example, standard costing, process costing,

absorption costing etc.

Inventory management systems: It is a software which helps the company in

controlling and overseeing the stocks of raw material as well as finished goods. The

requirements of inventory management system is that it helps in placing order of raw

material and managing use and storage of raw material (Abdusalomova, 2019). It is also

required to make sales order, and managing the packaging and shipping of finished

goods. It also required to enhance the productivity of operations. For example perpetual

inventory and periodic inventory system.

Price-optimizing systems: It is a software in which company uses different

mathematical analysis in order to know the behaviour of the customer at different level of

prices set by company. It is required to make fast decisions based on the data it provided.

It is also required to understand the market and adopt different channel to increase sales.

It is also required to eliminate the manual work as it causes lots of human error. For

example, pricing analysis, leverage analysis, behavioural analysis etc.

Job costing systems: It is a system used by the organization in order to know the cost of

a specific job for example retail companies uses the job costing systems in order to know

how cost vary from product to product on the basis of the size of the job order. Job

costing system is required to know the direct material, direct labour and overhead cost of

the specific job in the organization. It is also required to know the profit of the particular

job or project and taking appropriate decision regarding the same.

Methods of management accounting reporting

The primary source of information for management accountant in order to make

decisions are financial information provided by financial accounting. But management

accountant does not depend only on the financial report (Schaltegger, Etxeberria, and Ortas,

2017). They also gathered information from different reports such as cost, budget and

performance reports.

departments or operations. It also required in the valuation of inventory and setting

different prices in order to cover cost. For example, standard costing, process costing,

absorption costing etc.

Inventory management systems: It is a software which helps the company in

controlling and overseeing the stocks of raw material as well as finished goods. The

requirements of inventory management system is that it helps in placing order of raw

material and managing use and storage of raw material (Abdusalomova, 2019). It is also

required to make sales order, and managing the packaging and shipping of finished

goods. It also required to enhance the productivity of operations. For example perpetual

inventory and periodic inventory system.

Price-optimizing systems: It is a software in which company uses different

mathematical analysis in order to know the behaviour of the customer at different level of

prices set by company. It is required to make fast decisions based on the data it provided.

It is also required to understand the market and adopt different channel to increase sales.

It is also required to eliminate the manual work as it causes lots of human error. For

example, pricing analysis, leverage analysis, behavioural analysis etc.

Job costing systems: It is a system used by the organization in order to know the cost of

a specific job for example retail companies uses the job costing systems in order to know

how cost vary from product to product on the basis of the size of the job order. Job

costing system is required to know the direct material, direct labour and overhead cost of

the specific job in the organization. It is also required to know the profit of the particular

job or project and taking appropriate decision regarding the same.

Methods of management accounting reporting

The primary source of information for management accountant in order to make

decisions are financial information provided by financial accounting. But management

accountant does not depend only on the financial report (Schaltegger, Etxeberria, and Ortas,

2017). They also gathered information from different reports such as cost, budget and

performance reports.

Cost reports: Cost report provides the information of all cost such as fixed cost, variable

cost, cost of production to produce a product, overheads or any other extra cost incurred

by the company. With the help of this information managers can analyse the total cost

with the selling price in order to know the profit margin. Managers also take decisions

regarding cost controlling and enhancing the sales to increase the profit margin.

Budget report: Budget report provides the information regarding the estimated list of

revenue and expense sources. With the help of information provide by budget report,

managers manages the money effectively and efficiently (GOVDYA, and KHROMOVA,

2018). It also helps the managers to identify the problems before it actually occurs. For

this purpose, managers have take appropriate decisions in order to bring down the level

of expenditures to budgeted expense in case if actual expenditures are high.

Performance report: Performance reports provides the information regarding the

performance gap in case if actual performance is different from planned performance of

the company. In that case, managers of the company try motivate the employees towards

companies goals to reduce performance gaps. With the help of PR, managers can plan

strategy to improve the performance of the company. In order to increase performance,

managers are always tries to take feedback from their employees regarding the

environment and culture of the company.

Application of management accounting systems in the Tesco Plc

MA systems such as price optimization helps the managers of the company such as Tesco

Plc to understand the market and demand of their products by organizing surveys. It also

helps the mangers in cost analysis, product analysis, profit analysis etc. It helps the

company in inventory valuations and controlling the cost of the product and service of the

company. By applying management accounting systems the Tesco company analyses the

employees and customer attitude towards their company. With the help of management

accounting systems, managers of the company can easily create and execute the plan in

response to the effective operations of the company. It also helps in controlling the

performance gap in case if any arises in the company. By applying process costing

techniques Tesco company are able to evaluate and monitor the different process

involved in making the product and the cost allocation (Africano, Rodrigues, and Santos,

2019). Tesco company apply activity based costing for proper allocation of resources

cost, cost of production to produce a product, overheads or any other extra cost incurred

by the company. With the help of this information managers can analyse the total cost

with the selling price in order to know the profit margin. Managers also take decisions

regarding cost controlling and enhancing the sales to increase the profit margin.

Budget report: Budget report provides the information regarding the estimated list of

revenue and expense sources. With the help of information provide by budget report,

managers manages the money effectively and efficiently (GOVDYA, and KHROMOVA,

2018). It also helps the managers to identify the problems before it actually occurs. For

this purpose, managers have take appropriate decisions in order to bring down the level

of expenditures to budgeted expense in case if actual expenditures are high.

Performance report: Performance reports provides the information regarding the

performance gap in case if actual performance is different from planned performance of

the company. In that case, managers of the company try motivate the employees towards

companies goals to reduce performance gaps. With the help of PR, managers can plan

strategy to improve the performance of the company. In order to increase performance,

managers are always tries to take feedback from their employees regarding the

environment and culture of the company.

Application of management accounting systems in the Tesco Plc

MA systems such as price optimization helps the managers of the company such as Tesco

Plc to understand the market and demand of their products by organizing surveys. It also

helps the mangers in cost analysis, product analysis, profit analysis etc. It helps the

company in inventory valuations and controlling the cost of the product and service of the

company. By applying management accounting systems the Tesco company analyses the

employees and customer attitude towards their company. With the help of management

accounting systems, managers of the company can easily create and execute the plan in

response to the effective operations of the company. It also helps in controlling the

performance gap in case if any arises in the company. By applying process costing

techniques Tesco company are able to evaluate and monitor the different process

involved in making the product and the cost allocation (Africano, Rodrigues, and Santos,

2019). Tesco company apply activity based costing for proper allocation of resources

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

among each activity of each department and proper inventory valuation. Tesco company

also apply job costing in order to know the cost related to each job order in their

company.

Critical evaluation of integration of management accounting system and management accounting

reporting

Adoption of MA systems such as ERP and CMS software help the company to prepare

management accounting report in less time because manual works are time eating. With the help

of adopting the cost accounting systems such as process, marginal, budgetary, activity based, job

and batch costing etc. the managers can easily and quickly allocate the resources between them.

The chances of error are less in case of allocating the manufacturing cost among the processes,

jobs, batches, departments etc. with the help of systems (Sledgianowski, Gomaa, and Tan, 2017).

Price-optimizing systems helps the managers to evaluate the demand of their product in the

market by setting different prices. Behaviour of the customers with different prices are analysed

in this system. It helps in enhancing the speed of the process of the company which directly

prepares the reports quickly. Because of handling all the work manually, the company has to

compromise with the speed of the work but MA systems helps in increasing the speed of the

work.

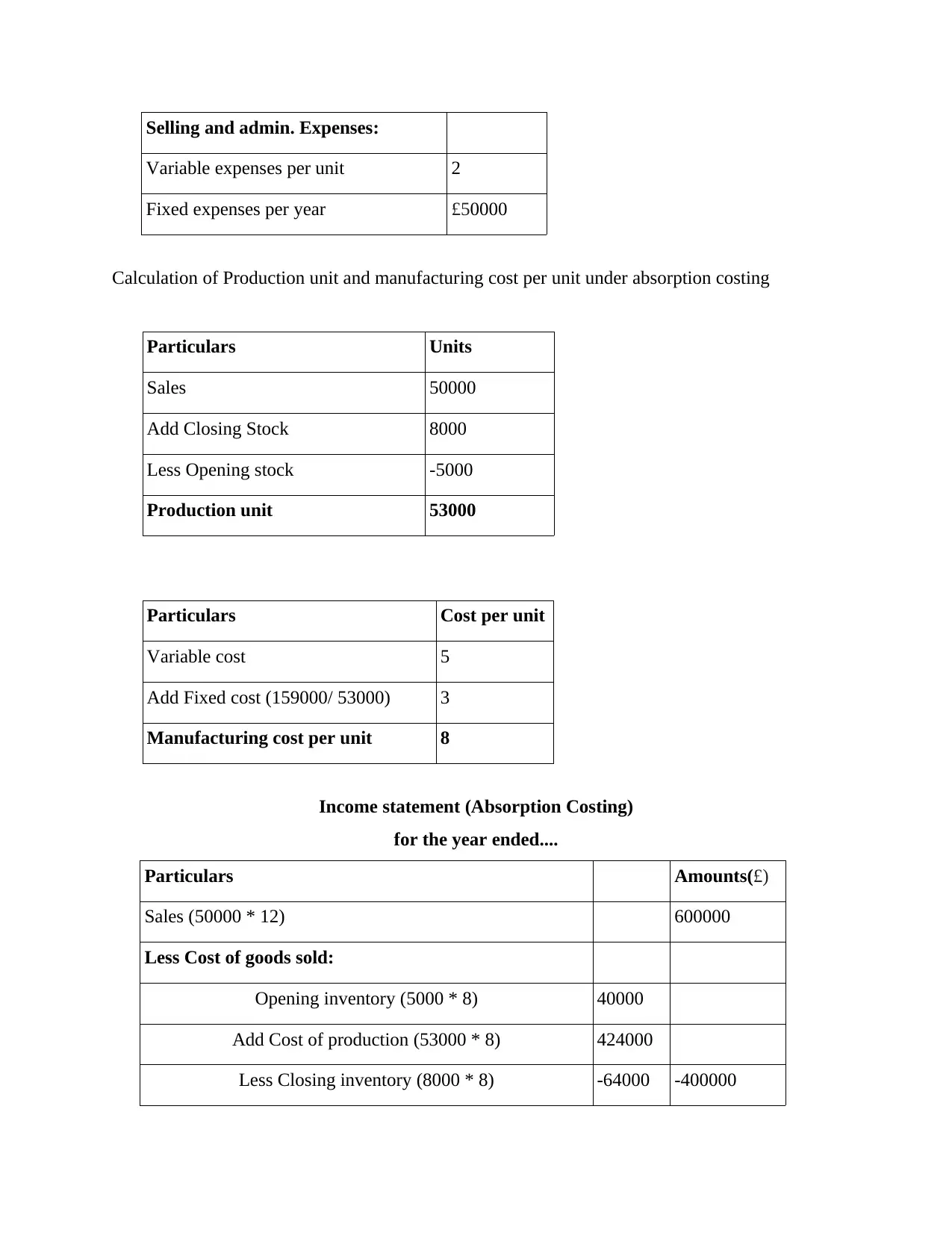

Interpretation of income statement under absorption costing and marginal costing

Sales (units) 50000

Selling price per unit 12

Opening stock of finished goods (units) 5000

Closing stock of finished goods (units) 8000

Production costs:

Variable cost per unit 5

Fixed production overheads per year £159000

also apply job costing in order to know the cost related to each job order in their

company.

Critical evaluation of integration of management accounting system and management accounting

reporting

Adoption of MA systems such as ERP and CMS software help the company to prepare

management accounting report in less time because manual works are time eating. With the help

of adopting the cost accounting systems such as process, marginal, budgetary, activity based, job

and batch costing etc. the managers can easily and quickly allocate the resources between them.

The chances of error are less in case of allocating the manufacturing cost among the processes,

jobs, batches, departments etc. with the help of systems (Sledgianowski, Gomaa, and Tan, 2017).

Price-optimizing systems helps the managers to evaluate the demand of their product in the

market by setting different prices. Behaviour of the customers with different prices are analysed

in this system. It helps in enhancing the speed of the process of the company which directly

prepares the reports quickly. Because of handling all the work manually, the company has to

compromise with the speed of the work but MA systems helps in increasing the speed of the

work.

Interpretation of income statement under absorption costing and marginal costing

Sales (units) 50000

Selling price per unit 12

Opening stock of finished goods (units) 5000

Closing stock of finished goods (units) 8000

Production costs:

Variable cost per unit 5

Fixed production overheads per year £159000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling and admin. Expenses:

Variable expenses per unit 2

Fixed expenses per year £50000

Calculation of Production unit and manufacturing cost per unit under absorption costing

Particulars Units

Sales 50000

Add Closing Stock 8000

Less Opening stock -5000

Production unit 53000

Particulars Cost per unit

Variable cost 5

Add Fixed cost (159000/ 53000) 3

Manufacturing cost per unit 8

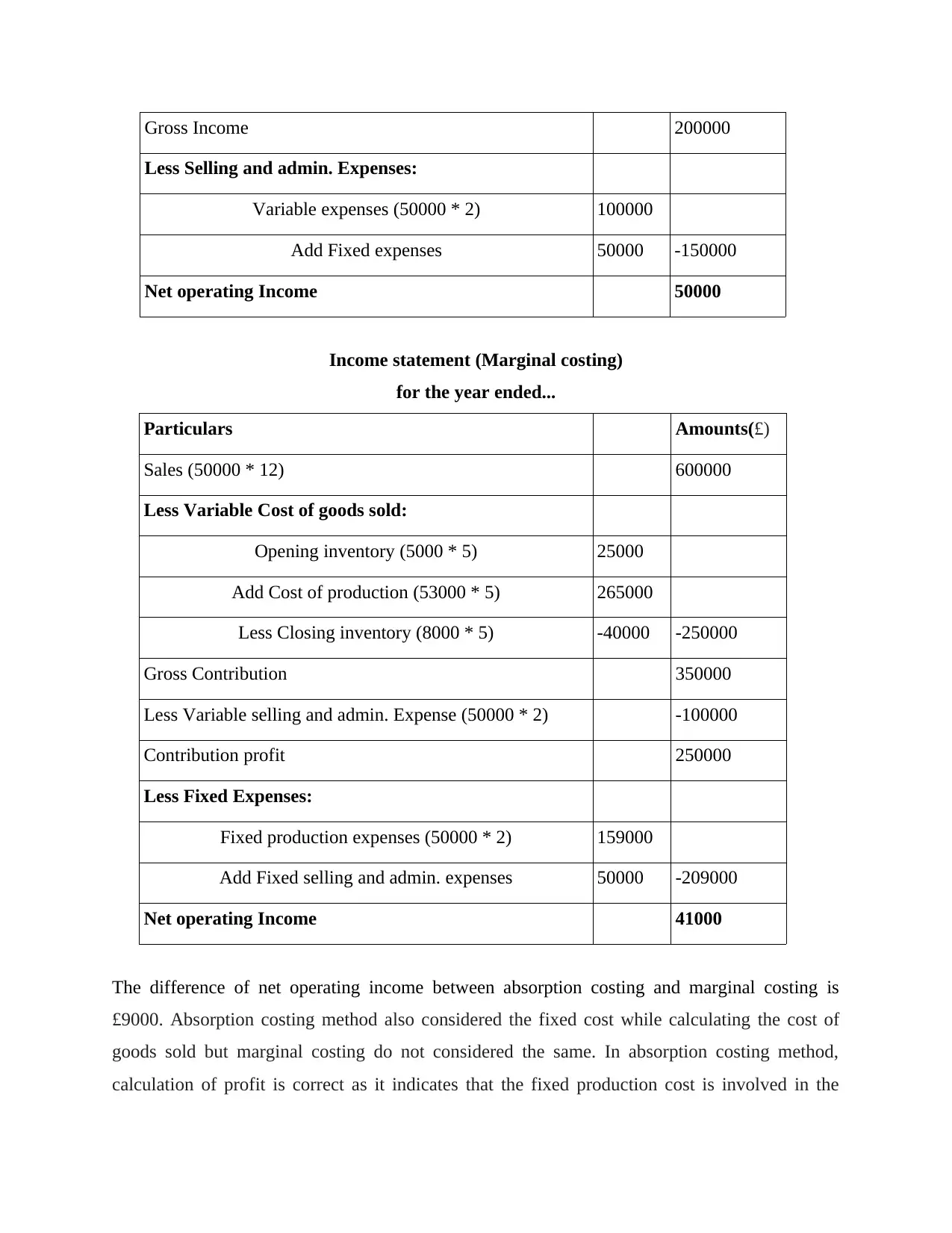

Income statement (Absorption Costing)

for the year ended....

Particulars Amounts(£)

Sales (50000 * 12) 600000

Less Cost of goods sold:

Opening inventory (5000 * 8) 40000

Add Cost of production (53000 * 8) 424000

Less Closing inventory (8000 * 8) -64000 -400000

Variable expenses per unit 2

Fixed expenses per year £50000

Calculation of Production unit and manufacturing cost per unit under absorption costing

Particulars Units

Sales 50000

Add Closing Stock 8000

Less Opening stock -5000

Production unit 53000

Particulars Cost per unit

Variable cost 5

Add Fixed cost (159000/ 53000) 3

Manufacturing cost per unit 8

Income statement (Absorption Costing)

for the year ended....

Particulars Amounts(£)

Sales (50000 * 12) 600000

Less Cost of goods sold:

Opening inventory (5000 * 8) 40000

Add Cost of production (53000 * 8) 424000

Less Closing inventory (8000 * 8) -64000 -400000

Gross Income 200000

Less Selling and admin. Expenses:

Variable expenses (50000 * 2) 100000

Add Fixed expenses 50000 -150000

Net operating Income 50000

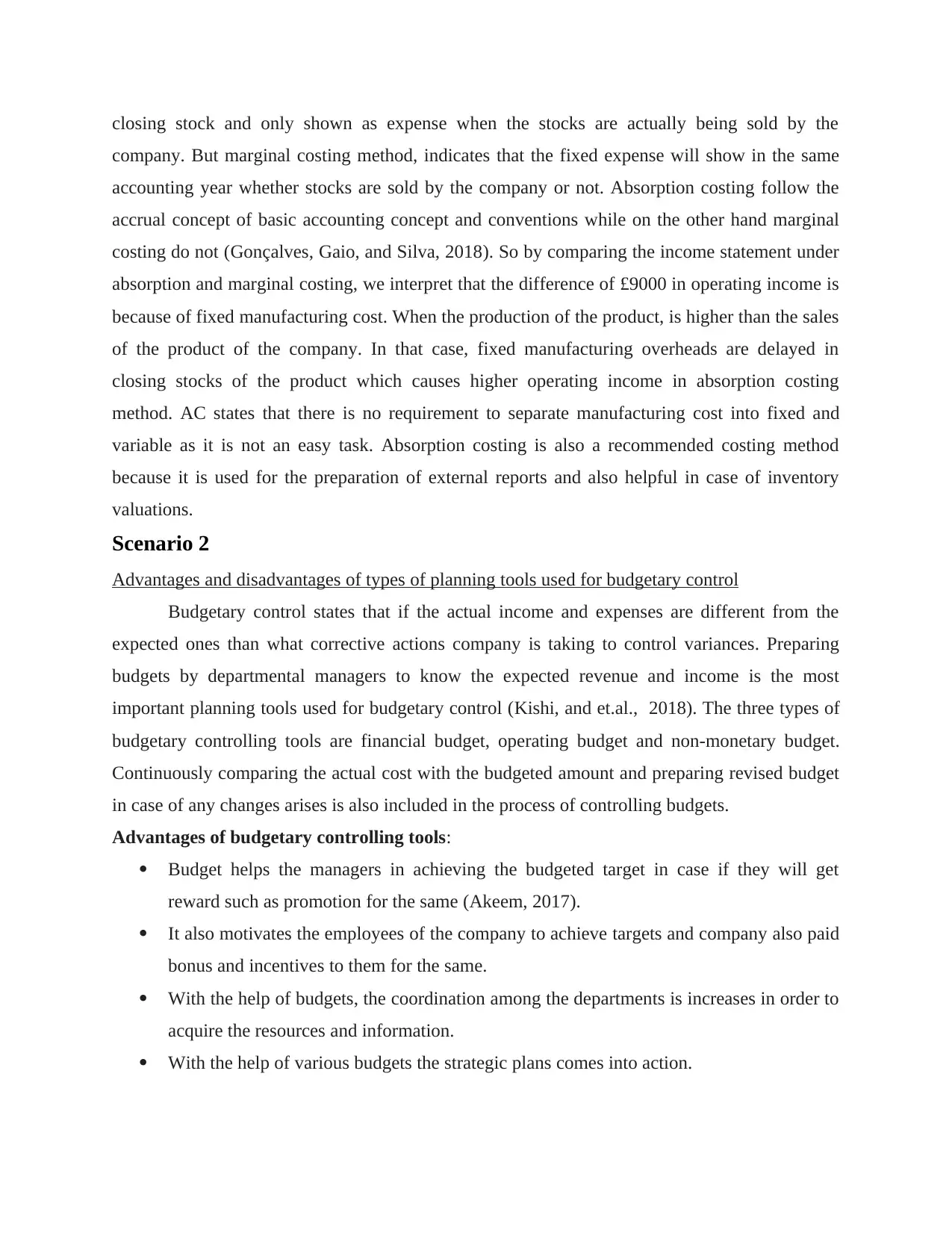

Income statement (Marginal costing)

for the year ended...

Particulars Amounts(£)

Sales (50000 * 12) 600000

Less Variable Cost of goods sold:

Opening inventory (5000 * 5) 25000

Add Cost of production (53000 * 5) 265000

Less Closing inventory (8000 * 5) -40000 -250000

Gross Contribution 350000

Less Variable selling and admin. Expense (50000 * 2) -100000

Contribution profit 250000

Less Fixed Expenses:

Fixed production expenses (50000 * 2) 159000

Add Fixed selling and admin. expenses 50000 -209000

Net operating Income 41000

The difference of net operating income between absorption costing and marginal costing is

£9000. Absorption costing method also considered the fixed cost while calculating the cost of

goods sold but marginal costing do not considered the same. In absorption costing method,

calculation of profit is correct as it indicates that the fixed production cost is involved in the

Less Selling and admin. Expenses:

Variable expenses (50000 * 2) 100000

Add Fixed expenses 50000 -150000

Net operating Income 50000

Income statement (Marginal costing)

for the year ended...

Particulars Amounts(£)

Sales (50000 * 12) 600000

Less Variable Cost of goods sold:

Opening inventory (5000 * 5) 25000

Add Cost of production (53000 * 5) 265000

Less Closing inventory (8000 * 5) -40000 -250000

Gross Contribution 350000

Less Variable selling and admin. Expense (50000 * 2) -100000

Contribution profit 250000

Less Fixed Expenses:

Fixed production expenses (50000 * 2) 159000

Add Fixed selling and admin. expenses 50000 -209000

Net operating Income 41000

The difference of net operating income between absorption costing and marginal costing is

£9000. Absorption costing method also considered the fixed cost while calculating the cost of

goods sold but marginal costing do not considered the same. In absorption costing method,

calculation of profit is correct as it indicates that the fixed production cost is involved in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

closing stock and only shown as expense when the stocks are actually being sold by the

company. But marginal costing method, indicates that the fixed expense will show in the same

accounting year whether stocks are sold by the company or not. Absorption costing follow the

accrual concept of basic accounting concept and conventions while on the other hand marginal

costing do not (Gonçalves, Gaio, and Silva, 2018). So by comparing the income statement under

absorption and marginal costing, we interpret that the difference of £9000 in operating income is

because of fixed manufacturing cost. When the production of the product, is higher than the sales

of the product of the company. In that case, fixed manufacturing overheads are delayed in

closing stocks of the product which causes higher operating income in absorption costing

method. AC states that there is no requirement to separate manufacturing cost into fixed and

variable as it is not an easy task. Absorption costing is also a recommended costing method

because it is used for the preparation of external reports and also helpful in case of inventory

valuations.

Scenario 2

Advantages and disadvantages of types of planning tools used for budgetary control

Budgetary control states that if the actual income and expenses are different from the

expected ones than what corrective actions company is taking to control variances. Preparing

budgets by departmental managers to know the expected revenue and income is the most

important planning tools used for budgetary control (Kishi, and et.al., 2018). The three types of

budgetary controlling tools are financial budget, operating budget and non-monetary budget.

Continuously comparing the actual cost with the budgeted amount and preparing revised budget

in case of any changes arises is also included in the process of controlling budgets.

Advantages of budgetary controlling tools:

Budget helps the managers in achieving the budgeted target in case if they will get

reward such as promotion for the same (Akeem, 2017).

It also motivates the employees of the company to achieve targets and company also paid

bonus and incentives to them for the same.

With the help of budgets, the coordination among the departments is increases in order to

acquire the resources and information.

With the help of various budgets the strategic plans comes into action.

company. But marginal costing method, indicates that the fixed expense will show in the same

accounting year whether stocks are sold by the company or not. Absorption costing follow the

accrual concept of basic accounting concept and conventions while on the other hand marginal

costing do not (Gonçalves, Gaio, and Silva, 2018). So by comparing the income statement under

absorption and marginal costing, we interpret that the difference of £9000 in operating income is

because of fixed manufacturing cost. When the production of the product, is higher than the sales

of the product of the company. In that case, fixed manufacturing overheads are delayed in

closing stocks of the product which causes higher operating income in absorption costing

method. AC states that there is no requirement to separate manufacturing cost into fixed and

variable as it is not an easy task. Absorption costing is also a recommended costing method

because it is used for the preparation of external reports and also helpful in case of inventory

valuations.

Scenario 2

Advantages and disadvantages of types of planning tools used for budgetary control

Budgetary control states that if the actual income and expenses are different from the

expected ones than what corrective actions company is taking to control variances. Preparing

budgets by departmental managers to know the expected revenue and income is the most

important planning tools used for budgetary control (Kishi, and et.al., 2018). The three types of

budgetary controlling tools are financial budget, operating budget and non-monetary budget.

Continuously comparing the actual cost with the budgeted amount and preparing revised budget

in case of any changes arises is also included in the process of controlling budgets.

Advantages of budgetary controlling tools:

Budget helps the managers in achieving the budgeted target in case if they will get

reward such as promotion for the same (Akeem, 2017).

It also motivates the employees of the company to achieve targets and company also paid

bonus and incentives to them for the same.

With the help of budgets, the coordination among the departments is increases in order to

acquire the resources and information.

With the help of various budgets the strategic plans comes into action.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As budgets shows all the activities and data of the company in organized manner, it

provides excellent reports in order to make decisions.

It also acts as a tool which help in planning, controlling and taking corrective actions in

case of difference between actuals and estimated figures.

It also helps in proper cost allocations between each product, departments, jobs etc.

Budgets also uses the informations provided by financial forecasting reports.

Disadvantage of budgetary controlling tools:

One of the disadvantage of budgets are that they required a lot of time to prepare and

compare the budgets.

In case of rigid budgets, it reduces the innovative ideas of the company at some level

which further reduces the sources of taking the money from the market for their new

ideas.

In case if managers do not involve employees in the tasks and imposed the budget in top

down structure then it may enhance the dissatisfaction attitude among the employees of

the company.

While preparing budgets of the company, all the members involved in the preparation of

budgets have their targets.

In order to achieve those targets it creates competitions of resources and informations

between staffs of the company.

Any budget prepared by the managers is based on the estimated figures which do not

have any relation with the actual figures shows inaccuracy of the company.

Because of rigid budgets, the decisions of the managers are also become rigid.

Critical evaluation of how management accounting helps to deal with financial problems

Management accounting systems such as job costing, batch costing, price-optimization

costing, inventory management costing helps the Sainsbury company in visualizing and

allocating the cost among each activity, process, job etc. By doing that Sainsbury company

improves the profitability and stability of the organization. It also helps the Sainsbury in

knowing the gaps between actual and planned one by variance analysis. On the other hand,

Tesco Plc because of not implementing management accounting systems causes lots difficulty in

decision-making. They are unable to allocate the cost among departments, job, process, activity

provides excellent reports in order to make decisions.

It also acts as a tool which help in planning, controlling and taking corrective actions in

case of difference between actuals and estimated figures.

It also helps in proper cost allocations between each product, departments, jobs etc.

Budgets also uses the informations provided by financial forecasting reports.

Disadvantage of budgetary controlling tools:

One of the disadvantage of budgets are that they required a lot of time to prepare and

compare the budgets.

In case of rigid budgets, it reduces the innovative ideas of the company at some level

which further reduces the sources of taking the money from the market for their new

ideas.

In case if managers do not involve employees in the tasks and imposed the budget in top

down structure then it may enhance the dissatisfaction attitude among the employees of

the company.

While preparing budgets of the company, all the members involved in the preparation of

budgets have their targets.

In order to achieve those targets it creates competitions of resources and informations

between staffs of the company.

Any budget prepared by the managers is based on the estimated figures which do not

have any relation with the actual figures shows inaccuracy of the company.

Because of rigid budgets, the decisions of the managers are also become rigid.

Critical evaluation of how management accounting helps to deal with financial problems

Management accounting systems such as job costing, batch costing, price-optimization

costing, inventory management costing helps the Sainsbury company in visualizing and

allocating the cost among each activity, process, job etc. By doing that Sainsbury company

improves the profitability and stability of the organization. It also helps the Sainsbury in

knowing the gaps between actual and planned one by variance analysis. On the other hand,

Tesco Plc because of not implementing management accounting systems causes lots difficulty in

decision-making. They are unable to allocate the cost among departments, job, process, activity

etc. which leads to increase in operation cost of the Tesco Plc and cause low profitability. So for

this purpose, they have to implement management accounting systems in their organizations.

Analysis of the use of planning tools in preparing and forecasting budget

The three planning tools involve in preparing, controlling and forecasting budgets are

financial budgets, operating budgets and non-monetary budgets. Financial budgets shows the

estimated cash flows, income & expenses and assets & liabilities of the company (Danzon, and

et.al., 2018). Operating budgets shows estimated sales revenue, cost of production, selling and

administrative expense and general expense. Non-monetary budgets shows the estimated figures

which are non financial in nature such as labour budget. These tools are playing vital role in

preparing the annual budgets.

1. Uses of Financial budgets:

Financial budgets such as cash budgets, capital expenditure budgets, balance sheet

budgets helps the company to know earnings and spending criteria of the business. It is

useful to know the cash inflow and cash outflow in the company after considering all the

cash income and expenses of the company.

It also provides the information of assets and liabilities of the company. It also helps

business to know whether the company is solvent or not.

Financial budgets will also disclose whether the profitability of the business is stable and

continuous or not (Cools, Stouthuysen, and Van den Abbeele, 2017). With right

estimations, financial budgets help the business to achieve its goals and targets.

In order to create annual report, monthly financial budgets play important role. It is also

useful in financial planning such as with the information provided by financial budgets

company can address the current liabilities before its debts become uncontrollable.

2. Uses of Operational budgets:

Operating budgets such as sales budget, production budget, selling and administrative

budgets helps the company to know the income and expenses from operations.

Company uses operational budgets in order to increase the efficiency level of the

company by analysing break even point. It also useful for tracking the entire business

activities and selecting the best level of activities.

this purpose, they have to implement management accounting systems in their organizations.

Analysis of the use of planning tools in preparing and forecasting budget

The three planning tools involve in preparing, controlling and forecasting budgets are

financial budgets, operating budgets and non-monetary budgets. Financial budgets shows the

estimated cash flows, income & expenses and assets & liabilities of the company (Danzon, and

et.al., 2018). Operating budgets shows estimated sales revenue, cost of production, selling and

administrative expense and general expense. Non-monetary budgets shows the estimated figures

which are non financial in nature such as labour budget. These tools are playing vital role in

preparing the annual budgets.

1. Uses of Financial budgets:

Financial budgets such as cash budgets, capital expenditure budgets, balance sheet

budgets helps the company to know earnings and spending criteria of the business. It is

useful to know the cash inflow and cash outflow in the company after considering all the

cash income and expenses of the company.

It also provides the information of assets and liabilities of the company. It also helps

business to know whether the company is solvent or not.

Financial budgets will also disclose whether the profitability of the business is stable and

continuous or not (Cools, Stouthuysen, and Van den Abbeele, 2017). With right

estimations, financial budgets help the business to achieve its goals and targets.

In order to create annual report, monthly financial budgets play important role. It is also

useful in financial planning such as with the information provided by financial budgets

company can address the current liabilities before its debts become uncontrollable.

2. Uses of Operational budgets:

Operating budgets such as sales budget, production budget, selling and administrative

budgets helps the company to know the income and expenses from operations.

Company uses operational budgets in order to increase the efficiency level of the

company by analysing break even point. It also useful for tracking the entire business

activities and selecting the best level of activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.