Phenomena of Cost Accounting and Management Accounting Systems

VerifiedAdded on 2023/01/19

|22

|5241

|66

AI Summary

This article discusses the phenomena of cost accounting and the essential necessities of diverse types of management accounting systems. It also explores the advantages of price optimization, job costing system, and cost accounting system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management Accounting can be explained as the procedure of accumulating, measuring,

preparing, identifying financial data and information within enterprise so that manager can

control, plan and evaluate to take better decision. Management accounting is used only for

internal purposes and within department’s performance such as project, processes and

departments. This is widely implemented in the small and big scale firm because it aids in

accomplishing group objectives (Abernethy and Wallis, 2018). Along with this it arranges and

organize resources, accumulate factors of production and integrates available resources in

effective manner to meet the desire set standards. The assignment is concerned with Ovation

Systems Ltd which is a client company who provide high quality video surveillance products

to police, military and other governmental agencies. In the year 2009 firm was awarded The

Queen's Award for innovation. The goods range includes rugged and small audio and video

recorders. This report includes phenomena of cost accounting and focus on essential

requirements of several types of management accounting systems. Moreover, calculate costs by

using appropriate tools and techniques. Along with this design income statement by using

marginal and absorption costs. Additionally, comparison is dome on executing management

accounting system in different company to handle financial problems (Agrawal and Cooper,

2017).

LO 1

P1) Discuss the phenomena of cost accounting along with this study the essential necessities of

diverse sort of management accounting systems.

According to American Accounting Association, management accounting refers to as

application of suitable methods in processing economic data of an enterprise in order to frame

plans to achieve deserving objectives (About Management Accounting, 2018).

Management accounting is also well known by other names like, cost accounting and

managerial accounting. Cost accounting is stated as involving all those activities which provide

financial information to the top level management to guide them to formulate tactics in order to

function business operations smoothly. Management uses gathered financial knowledge and

numerical data for ascertaining product and cost of various job. By effectively implementing

managerial accounting in Ovation Systems Ltd. they will be able to deliver fast and immediate

1

Management Accounting can be explained as the procedure of accumulating, measuring,

preparing, identifying financial data and information within enterprise so that manager can

control, plan and evaluate to take better decision. Management accounting is used only for

internal purposes and within department’s performance such as project, processes and

departments. This is widely implemented in the small and big scale firm because it aids in

accomplishing group objectives (Abernethy and Wallis, 2018). Along with this it arranges and

organize resources, accumulate factors of production and integrates available resources in

effective manner to meet the desire set standards. The assignment is concerned with Ovation

Systems Ltd which is a client company who provide high quality video surveillance products

to police, military and other governmental agencies. In the year 2009 firm was awarded The

Queen's Award for innovation. The goods range includes rugged and small audio and video

recorders. This report includes phenomena of cost accounting and focus on essential

requirements of several types of management accounting systems. Moreover, calculate costs by

using appropriate tools and techniques. Along with this design income statement by using

marginal and absorption costs. Additionally, comparison is dome on executing management

accounting system in different company to handle financial problems (Agrawal and Cooper,

2017).

LO 1

P1) Discuss the phenomena of cost accounting along with this study the essential necessities of

diverse sort of management accounting systems.

According to American Accounting Association, management accounting refers to as

application of suitable methods in processing economic data of an enterprise in order to frame

plans to achieve deserving objectives (About Management Accounting, 2018).

Management accounting is also well known by other names like, cost accounting and

managerial accounting. Cost accounting is stated as involving all those activities which provide

financial information to the top level management to guide them to formulate tactics in order to

function business operations smoothly. Management uses gathered financial knowledge and

numerical data for ascertaining product and cost of various job. By effectively implementing

managerial accounting in Ovation Systems Ltd. they will be able to deliver fast and immediate

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

information to the mangers regarding product and services and day to day budgeting assist firm

to take best decision in order to rise company’s operational effectiveness and efficiency.

There are distinguished kinds of management accounting system and are mandatory

needs for the administration. Price optimization, job costing system and cost accounting system

are types of accounting system in the global market (Agrawal, 2018).

Price optimization: Business associates by adopting this kind of management

accounting system in the working environment is able to measure the suitable prices for their

innovative product that is offered. It is a mathematical evaluation in order to examine how

targeted consumers will react to several prices for product and services through various channels.

Price optimizing helps administration to determine the best prices so that Ovation Systems Ltd is

able to maximize operating profit. By this act huge customer base can be raised for the high

quality video surveillance products designed for departments of police, military and other

governmental agencies. Price optimization helps business administration to meet the set goals

and objectives in the set time duration. This is more useful for business dealing in retail sector.

Advantages of price optimizing:

Price optimization in an organization provide consistency to the business (Ax and Greve,

2017).

It aids in gathering authentic and reliable data which reduces the chances of error in the

working premises.

Firm by effectively implementing this in business administration assist in automating the

entire process. That results in positive results.

Job costing system: Ovation Systems Ltd adopts job costing system effectively and

efficiently in their working environment as it assigns and collect manufacturing costs of a single

unit of output. It is used in any industry because it is usefull in checking cost of production

exceeds the overhead price. in order to gain profit for complete process (Weetman, 2019). This

aspect is more worthful when it is adopted to produce sufficiently varied goods and services

from one another and has significant cost. By systematically executing this in the business it

leads in accumulating huge revenue, management decisions, financial reporting and project

estimating. In order to get satisfactory results, it is very important to choose the most suitable

costing system as per their business type and product in the cut throat competitive world.

Advantages of Job costing system:

2

to take best decision in order to rise company’s operational effectiveness and efficiency.

There are distinguished kinds of management accounting system and are mandatory

needs for the administration. Price optimization, job costing system and cost accounting system

are types of accounting system in the global market (Agrawal, 2018).

Price optimization: Business associates by adopting this kind of management

accounting system in the working environment is able to measure the suitable prices for their

innovative product that is offered. It is a mathematical evaluation in order to examine how

targeted consumers will react to several prices for product and services through various channels.

Price optimizing helps administration to determine the best prices so that Ovation Systems Ltd is

able to maximize operating profit. By this act huge customer base can be raised for the high

quality video surveillance products designed for departments of police, military and other

governmental agencies. Price optimization helps business administration to meet the set goals

and objectives in the set time duration. This is more useful for business dealing in retail sector.

Advantages of price optimizing:

Price optimization in an organization provide consistency to the business (Ax and Greve,

2017).

It aids in gathering authentic and reliable data which reduces the chances of error in the

working premises.

Firm by effectively implementing this in business administration assist in automating the

entire process. That results in positive results.

Job costing system: Ovation Systems Ltd adopts job costing system effectively and

efficiently in their working environment as it assigns and collect manufacturing costs of a single

unit of output. It is used in any industry because it is usefull in checking cost of production

exceeds the overhead price. in order to gain profit for complete process (Weetman, 2019). This

aspect is more worthful when it is adopted to produce sufficiently varied goods and services

from one another and has significant cost. By systematically executing this in the business it

leads in accumulating huge revenue, management decisions, financial reporting and project

estimating. In order to get satisfactory results, it is very important to choose the most suitable

costing system as per their business type and product in the cut throat competitive world.

Advantages of Job costing system:

2

Job costing system assist the firm to calculate the revenue gained on single jobs.

This directly aid the company to better understand weather specific jobs are desirable to

pursue in the near future.

It prevents duplication of work as it aids in measuring of similar job. By doing so firm

quoting the price of a job always depends upon the previous job pricing.

Cost accounting system: This system is used by Ovation Systems Ltd because cost

accounting system assist in determining cost of the goods for profitability investigation, cost

control and inventory valuation (Azudin and Mansor, 2018). In the era of neck to neck

competitive world all medium and large scale businesses rely on cost accounting in order to

render data which financial accounting provides. By performing this system appropriately

business function will run smoothly in the global market. Along with this emerging needs of the

customers for video surveillance products and other rugged and small audio and video recorders

will be full-filled accordingly.

Advantages of cost accounting system:

Cost accounting system helps in fixation of prices for the goods and services.

In an organization this directly assist in expansion in production.

Firm is given proper information for planning and framing unique tactics to increase sales

volume.

It guides business administration how to reduce prices of the product and services in the

cut throat competitive world (Turner and Witteman, 2017).

Inventory management system:

P2) Discuss several methods used for management accounting reporting.

This is termed as process of providing information to distinguished stages of management

so that corrective measures can be taken for improvements. By effectively executing

management accounting reporting in the Ovation Systems Ltd distinguished benefits can be

garbed such as, it helps in setting price for the goods and services, guide in formation of budget,

aid in planning, assist in controlling business activities etc.

Budgeting report: Organization adopts this in the working premises as it helps them to

measure overall performance of enterprise (Beyer and Marinovic, 2018). By designing budgeting

report company manage cash amount of every single activity. It aids report to do comparison

between estimated and actual budget in order to keep proper control on various outcomes. Better

3

This directly aid the company to better understand weather specific jobs are desirable to

pursue in the near future.

It prevents duplication of work as it aids in measuring of similar job. By doing so firm

quoting the price of a job always depends upon the previous job pricing.

Cost accounting system: This system is used by Ovation Systems Ltd because cost

accounting system assist in determining cost of the goods for profitability investigation, cost

control and inventory valuation (Azudin and Mansor, 2018). In the era of neck to neck

competitive world all medium and large scale businesses rely on cost accounting in order to

render data which financial accounting provides. By performing this system appropriately

business function will run smoothly in the global market. Along with this emerging needs of the

customers for video surveillance products and other rugged and small audio and video recorders

will be full-filled accordingly.

Advantages of cost accounting system:

Cost accounting system helps in fixation of prices for the goods and services.

In an organization this directly assist in expansion in production.

Firm is given proper information for planning and framing unique tactics to increase sales

volume.

It guides business administration how to reduce prices of the product and services in the

cut throat competitive world (Turner and Witteman, 2017).

Inventory management system:

P2) Discuss several methods used for management accounting reporting.

This is termed as process of providing information to distinguished stages of management

so that corrective measures can be taken for improvements. By effectively executing

management accounting reporting in the Ovation Systems Ltd distinguished benefits can be

garbed such as, it helps in setting price for the goods and services, guide in formation of budget,

aid in planning, assist in controlling business activities etc.

Budgeting report: Organization adopts this in the working premises as it helps them to

measure overall performance of enterprise (Beyer and Marinovic, 2018). By designing budgeting

report company manage cash amount of every single activity. It aids report to do comparison

between estimated and actual budget in order to keep proper control on various outcomes. Better

3

incentives and benefits are given to the staff members in order to reduce the cost which provides

complete satisfaction to workers.

Performance reports: Ovation System Ltd is executing performance report so as to

examine the performance of the business administration and their staff members. This directly or

indirectly aid enterprise to take the quick and smart decisions in order to upgrade workforce

productivity and profitability ratio. By appropriately scanning this report Ovation Systems

determine the efficiency of their tactics towards stated aims and objectives. The effectiveness

motivates workers to work day and night in order to attain the companies set standards.

Job costs reports: Organization by taking job costs report within the enterprise is able to

investigate the cost of each individual project (Booth, 2018). It leads in providing benefit to

Ovation Systems Ltd as they are capable enough to find higher earning areas. Moreover, by

using this progression and succession of the project areas can be determined. This helps in

measuring and monitoring the wastage of precious time and money in the low margin areas in

the global market

Therefore, for Ovation Systems Ltd all the reports discussed above are beneficial for

them in the intense competitive world. All the reports discussed above has helped business

administration to operate the business function smoothly. As well as timely guide them to take

appropriate decisions for the betterment of employees and employer

LO 2

P3) Compute costs using appropriate techniques of cost analysis to prepare an income statement

Computation of costs by using appropriate techniques of cost analysis to design an

income statements are explained as follows:

Cost: It is considered as the backbone of Ovation Systems Ltd. Without sufficient

amount of funds business cannot be functioned properly in neck to neck competitive world.

Marginal costing and absorption costing are two methods that are studied so as to figure out the

approximation cost. By doing so accordingly the unique tactics are designed to over the

deficiency of funds in the global market. To create tough competition for rivalry in the

competitive market place business associates need to be financially stable in nature (Bui and De

Villiers, 2017). Here, the brief discussion about marginal and absorption cost are done as under:

4

complete satisfaction to workers.

Performance reports: Ovation System Ltd is executing performance report so as to

examine the performance of the business administration and their staff members. This directly or

indirectly aid enterprise to take the quick and smart decisions in order to upgrade workforce

productivity and profitability ratio. By appropriately scanning this report Ovation Systems

determine the efficiency of their tactics towards stated aims and objectives. The effectiveness

motivates workers to work day and night in order to attain the companies set standards.

Job costs reports: Organization by taking job costs report within the enterprise is able to

investigate the cost of each individual project (Booth, 2018). It leads in providing benefit to

Ovation Systems Ltd as they are capable enough to find higher earning areas. Moreover, by

using this progression and succession of the project areas can be determined. This helps in

measuring and monitoring the wastage of precious time and money in the low margin areas in

the global market

Therefore, for Ovation Systems Ltd all the reports discussed above are beneficial for

them in the intense competitive world. All the reports discussed above has helped business

administration to operate the business function smoothly. As well as timely guide them to take

appropriate decisions for the betterment of employees and employer

LO 2

P3) Compute costs using appropriate techniques of cost analysis to prepare an income statement

Computation of costs by using appropriate techniques of cost analysis to design an

income statements are explained as follows:

Cost: It is considered as the backbone of Ovation Systems Ltd. Without sufficient

amount of funds business cannot be functioned properly in neck to neck competitive world.

Marginal costing and absorption costing are two methods that are studied so as to figure out the

approximation cost. By doing so accordingly the unique tactics are designed to over the

deficiency of funds in the global market. To create tough competition for rivalry in the

competitive market place business associates need to be financially stable in nature (Bui and De

Villiers, 2017). Here, the brief discussion about marginal and absorption cost are done as under:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

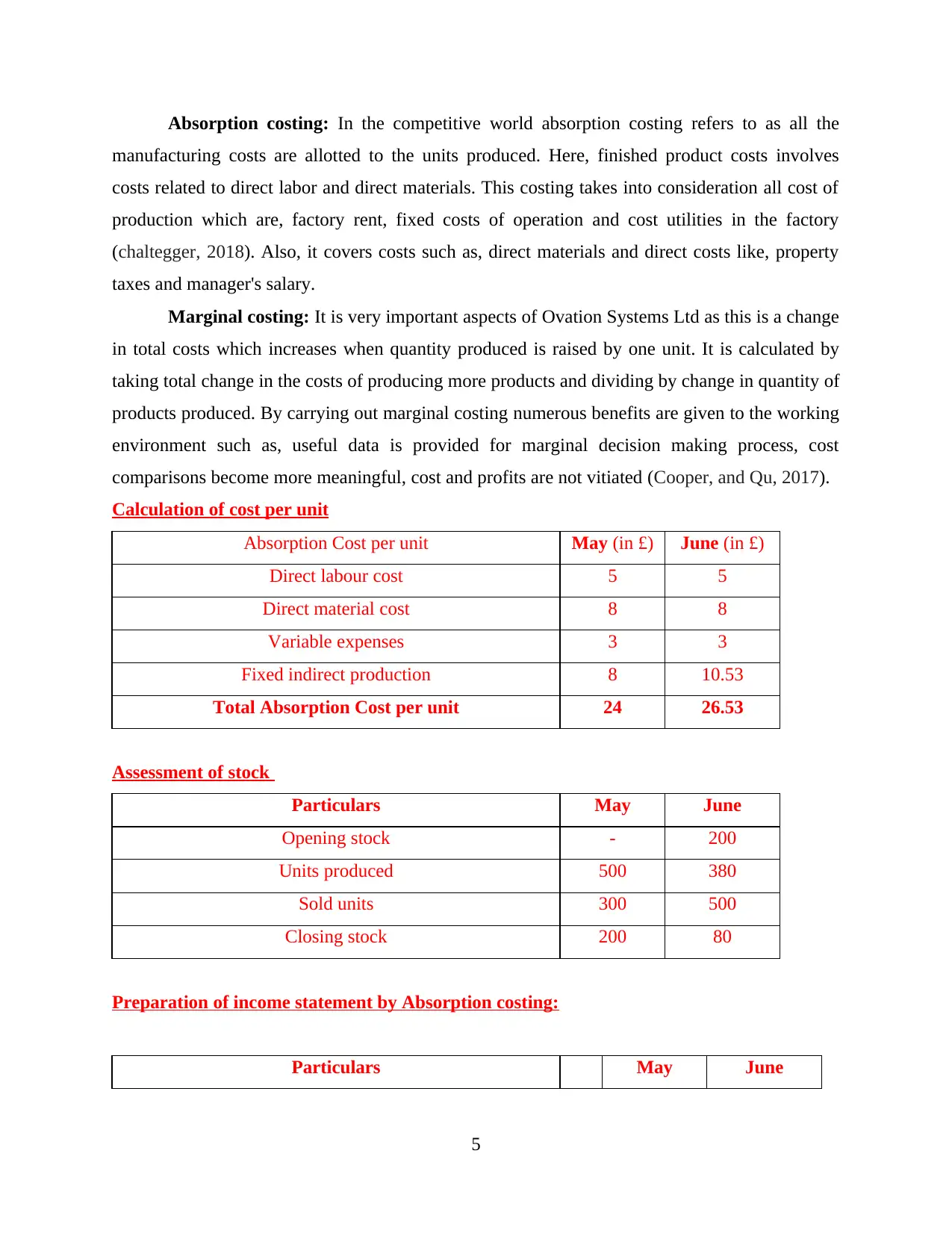

Absorption costing: In the competitive world absorption costing refers to as all the

manufacturing costs are allotted to the units produced. Here, finished product costs involves

costs related to direct labor and direct materials. This costing takes into consideration all cost of

production which are, factory rent, fixed costs of operation and cost utilities in the factory

(chaltegger, 2018). Also, it covers costs such as, direct materials and direct costs like, property

taxes and manager's salary.

Marginal costing: It is very important aspects of Ovation Systems Ltd as this is a change

in total costs which increases when quantity produced is raised by one unit. It is calculated by

taking total change in the costs of producing more products and dividing by change in quantity of

products produced. By carrying out marginal costing numerous benefits are given to the working

environment such as, useful data is provided for marginal decision making process, cost

comparisons become more meaningful, cost and profits are not vitiated (Cooper, and Qu, 2017).

Calculation of cost per unit

Absorption Cost per unit May (in £) June (in £)

Direct labour cost 5 5

Direct material cost 8 8

Variable expenses 3 3

Fixed indirect production 8 10.53

Total Absorption Cost per unit 24 26.53

Assessment of stock

Particulars May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Preparation of income statement by Absorption costing:

Particulars May June

5

manufacturing costs are allotted to the units produced. Here, finished product costs involves

costs related to direct labor and direct materials. This costing takes into consideration all cost of

production which are, factory rent, fixed costs of operation and cost utilities in the factory

(chaltegger, 2018). Also, it covers costs such as, direct materials and direct costs like, property

taxes and manager's salary.

Marginal costing: It is very important aspects of Ovation Systems Ltd as this is a change

in total costs which increases when quantity produced is raised by one unit. It is calculated by

taking total change in the costs of producing more products and dividing by change in quantity of

products produced. By carrying out marginal costing numerous benefits are given to the working

environment such as, useful data is provided for marginal decision making process, cost

comparisons become more meaningful, cost and profits are not vitiated (Cooper, and Qu, 2017).

Calculation of cost per unit

Absorption Cost per unit May (in £) June (in £)

Direct labour cost 5 5

Direct material cost 8 8

Variable expenses 3 3

Fixed indirect production 8 10.53

Total Absorption Cost per unit 24 26.53

Assessment of stock

Particulars May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Preparation of income statement by Absorption costing:

Particulars May June

5

(in £) (in £)

Sales 50 15000 25000

Less: Cost of Goods sold (COGS)

Opening inventory

Direct labour (DL) 5 2500 1900

Direct material (DM) 8 4000 3040

Variable cost of production 3 1500 1140

Fixed indirect expenditure related to production 4000 4000

Ending inventory -4800 2122.4

Total cost of goods sold 7200 7957.6

Gross profit (GP) 7800 17042.4

Selling & Distribution expenditure 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

Net profit (NP) 1050 9792.4

Per unit cost evaluation under marginal costing

Particulars May (in £) June (in £)

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

Inventory assessment

Particulars May June

Inventory at the beginning of period - 200

6

Sales 50 15000 25000

Less: Cost of Goods sold (COGS)

Opening inventory

Direct labour (DL) 5 2500 1900

Direct material (DM) 8 4000 3040

Variable cost of production 3 1500 1140

Fixed indirect expenditure related to production 4000 4000

Ending inventory -4800 2122.4

Total cost of goods sold 7200 7957.6

Gross profit (GP) 7800 17042.4

Selling & Distribution expenditure 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

Net profit (NP) 1050 9792.4

Per unit cost evaluation under marginal costing

Particulars May (in £) June (in £)

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

Inventory assessment

Particulars May June

Inventory at the beginning of period - 200

6

Production (in units) 500 380

Sales (in units) 300 500

Stock at the end of period 200 80

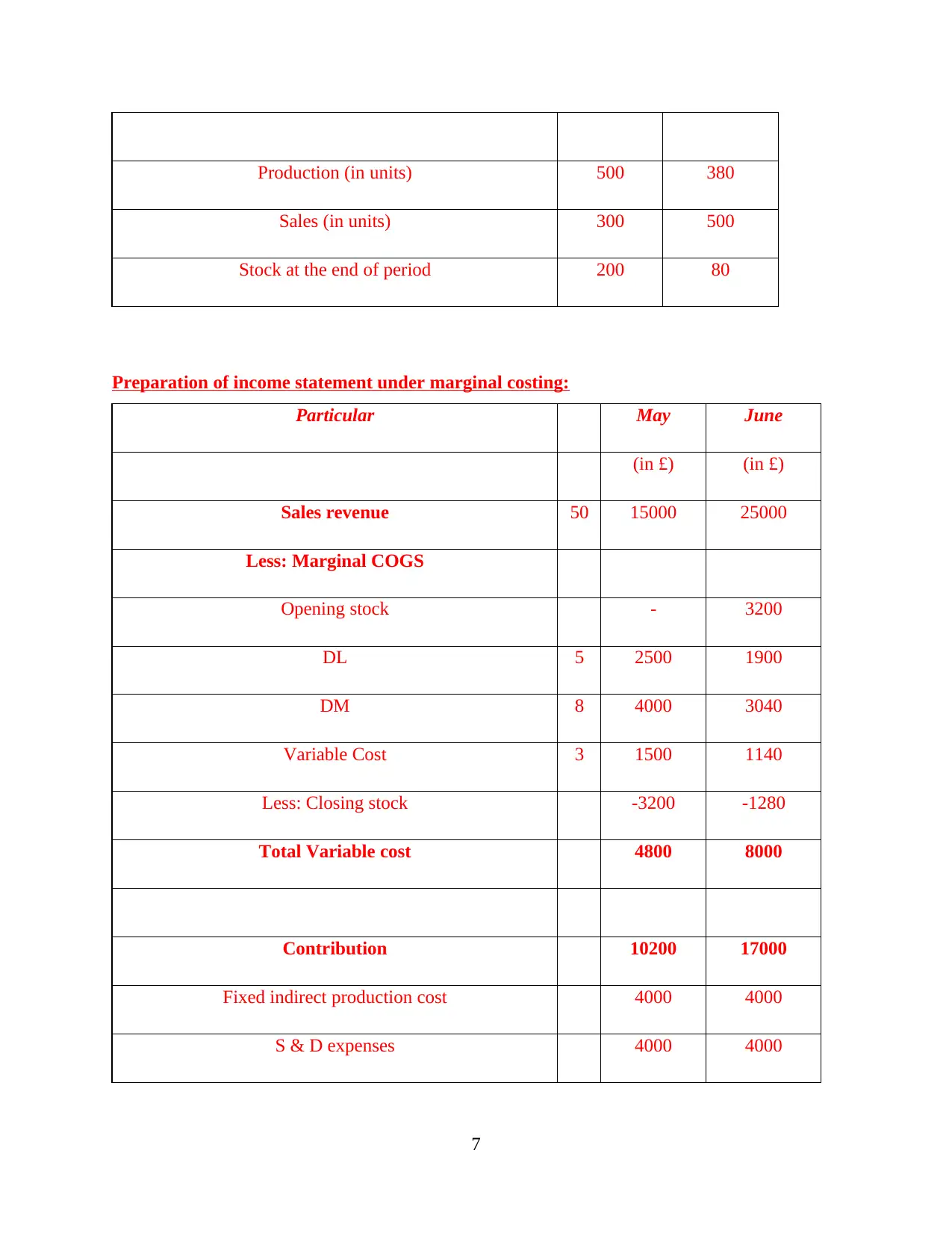

Preparation of income statement under marginal costing:

Particular May June

(in £) (in £)

Sales revenue 50 15000 25000

Less: Marginal COGS

Opening stock - 3200

DL 5 2500 1900

DM 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

S & D expenses 4000 4000

7

Sales (in units) 300 500

Stock at the end of period 200 80

Preparation of income statement under marginal costing:

Particular May June

(in £) (in £)

Sales revenue 50 15000 25000

Less: Marginal COGS

Opening stock - 3200

DL 5 2500 1900

DM 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

S & D expenses 4000 4000

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

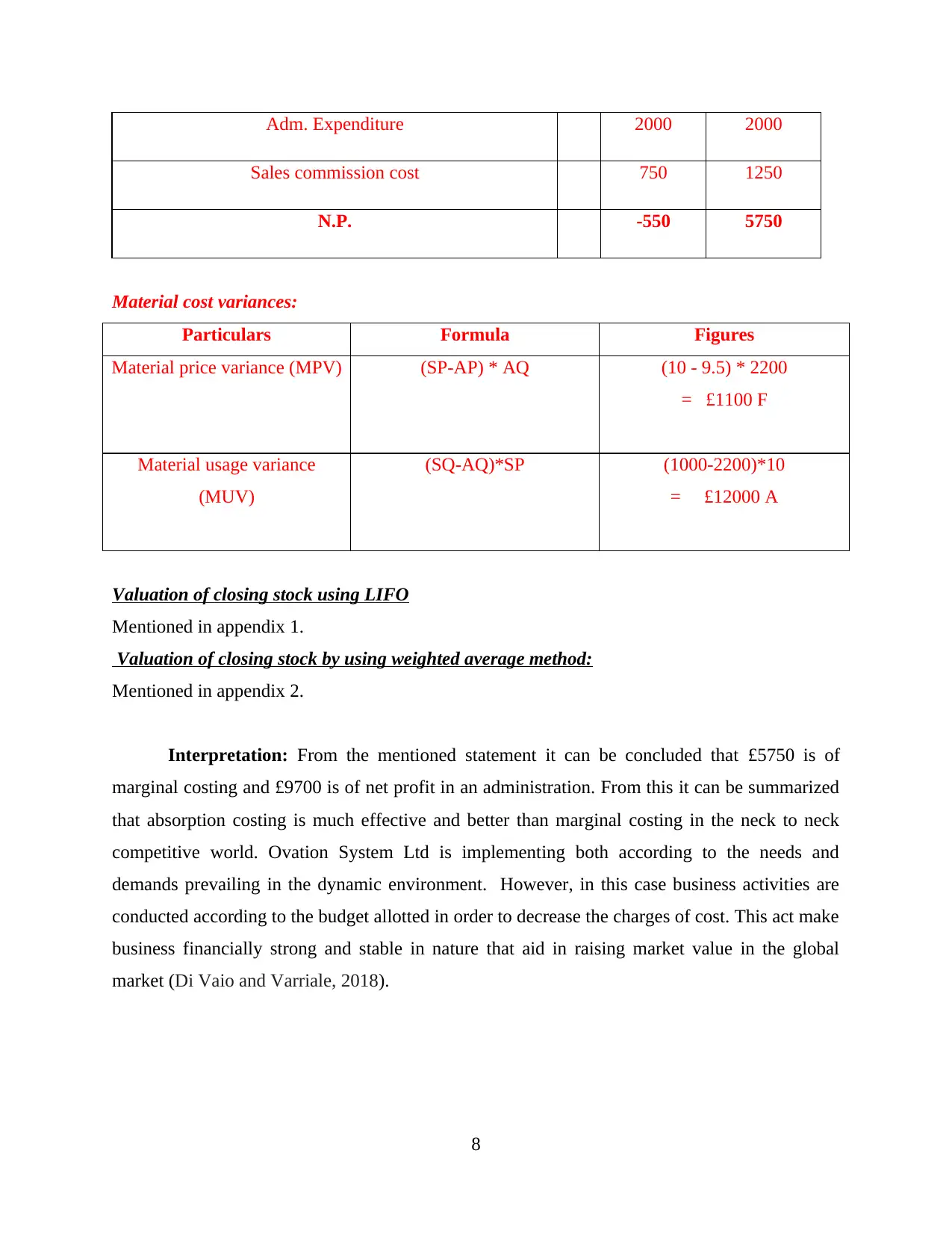

Adm. Expenditure 2000 2000

Sales commission cost 750 1250

N.P. -550 5750

Material cost variances:

Particulars Formula Figures

Material price variance (MPV) (SP-AP) * AQ (10 - 9.5) * 2200

= £1100 F

Material usage variance

(MUV)

(SQ-AQ)*SP (1000-2200)*10

= £12000 A

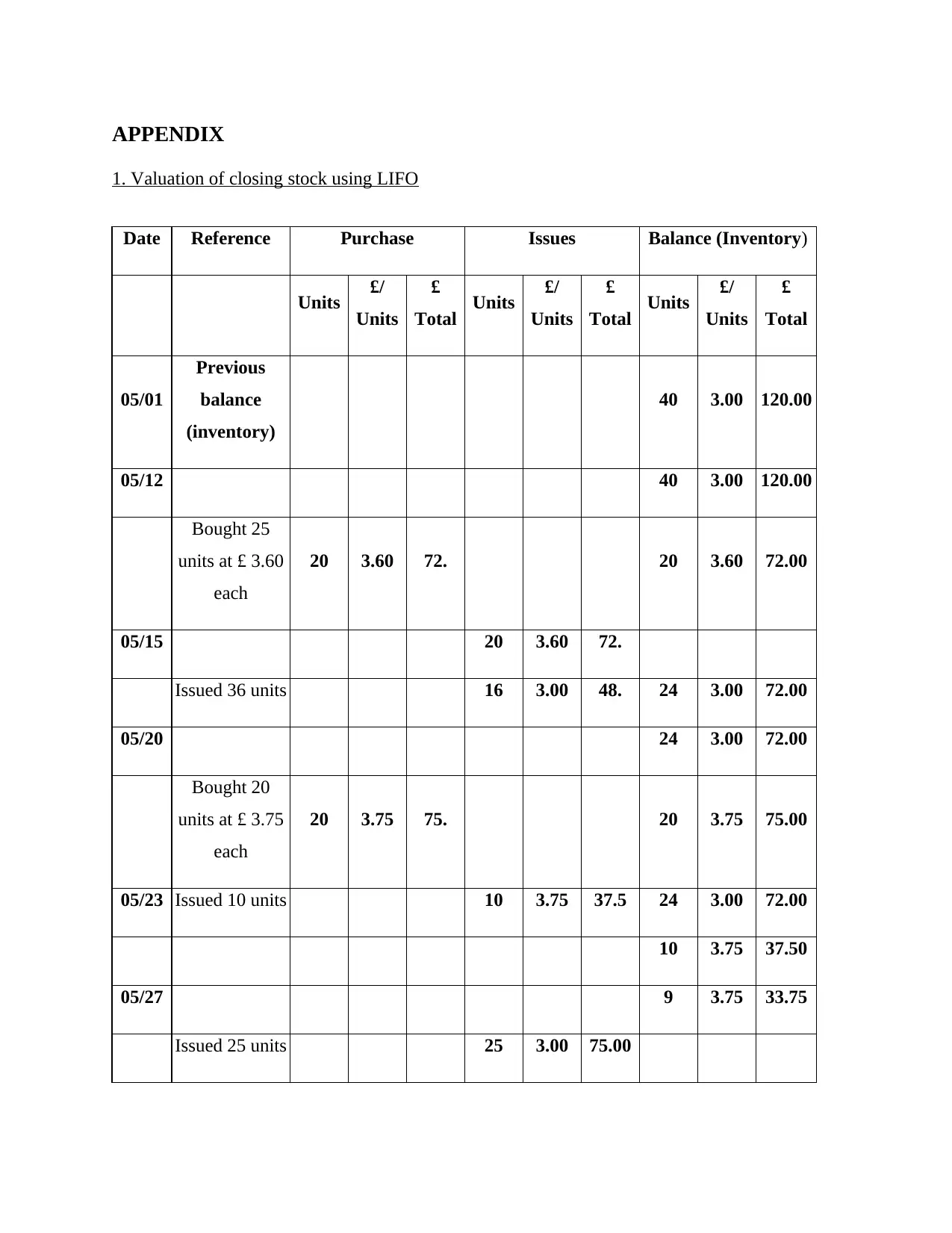

Valuation of closing stock using LIFO

Mentioned in appendix 1.

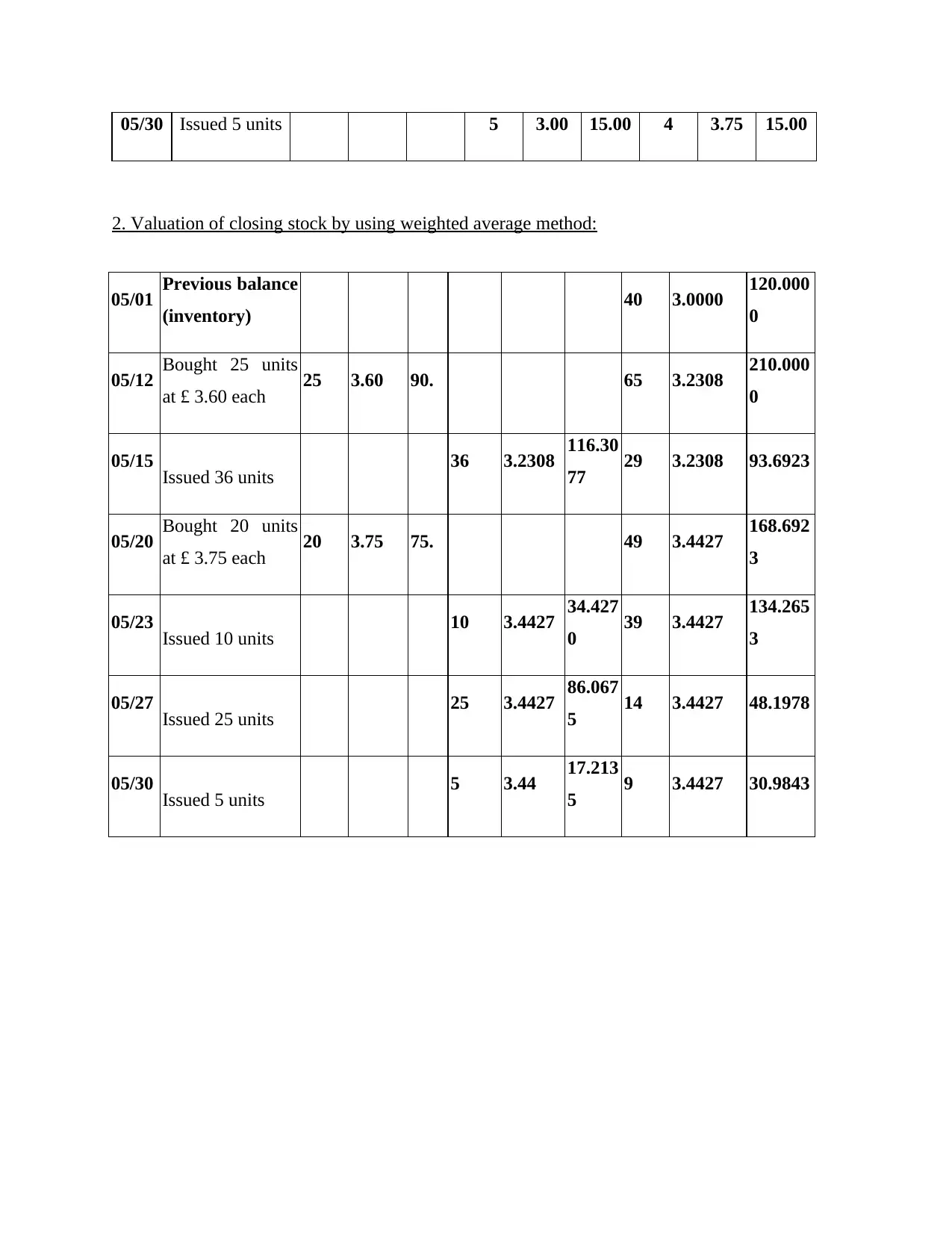

Valuation of closing stock by using weighted average method:

Mentioned in appendix 2.

Interpretation: From the mentioned statement it can be concluded that £5750 is of

marginal costing and £9700 is of net profit in an administration. From this it can be summarized

that absorption costing is much effective and better than marginal costing in the neck to neck

competitive world. Ovation System Ltd is implementing both according to the needs and

demands prevailing in the dynamic environment. However, in this case business activities are

conducted according to the budget allotted in order to decrease the charges of cost. This act make

business financially strong and stable in nature that aid in raising market value in the global

market (Di Vaio and Varriale, 2018).

8

Sales commission cost 750 1250

N.P. -550 5750

Material cost variances:

Particulars Formula Figures

Material price variance (MPV) (SP-AP) * AQ (10 - 9.5) * 2200

= £1100 F

Material usage variance

(MUV)

(SQ-AQ)*SP (1000-2200)*10

= £12000 A

Valuation of closing stock using LIFO

Mentioned in appendix 1.

Valuation of closing stock by using weighted average method:

Mentioned in appendix 2.

Interpretation: From the mentioned statement it can be concluded that £5750 is of

marginal costing and £9700 is of net profit in an administration. From this it can be summarized

that absorption costing is much effective and better than marginal costing in the neck to neck

competitive world. Ovation System Ltd is implementing both according to the needs and

demands prevailing in the dynamic environment. However, in this case business activities are

conducted according to the budget allotted in order to decrease the charges of cost. This act make

business financially strong and stable in nature that aid in raising market value in the global

market (Di Vaio and Varriale, 2018).

8

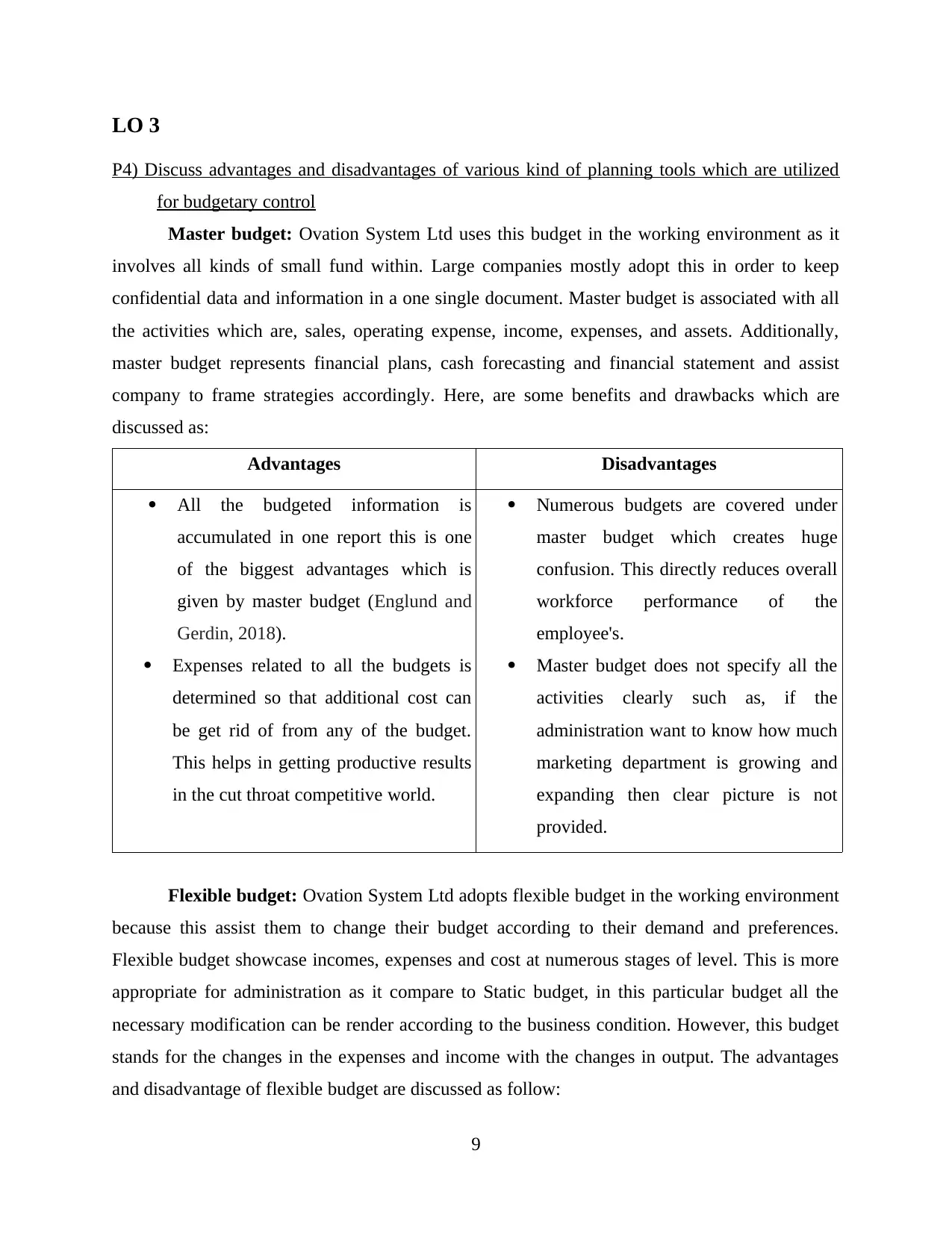

LO 3

P4) Discuss advantages and disadvantages of various kind of planning tools which are utilized

for budgetary control

Master budget: Ovation System Ltd uses this budget in the working environment as it

involves all kinds of small fund within. Large companies mostly adopt this in order to keep

confidential data and information in a one single document. Master budget is associated with all

the activities which are, sales, operating expense, income, expenses, and assets. Additionally,

master budget represents financial plans, cash forecasting and financial statement and assist

company to frame strategies accordingly. Here, are some benefits and drawbacks which are

discussed as:

Advantages Disadvantages

All the budgeted information is

accumulated in one report this is one

of the biggest advantages which is

given by master budget (Englund and

Gerdin, 2018).

Expenses related to all the budgets is

determined so that additional cost can

be get rid of from any of the budget.

This helps in getting productive results

in the cut throat competitive world.

Numerous budgets are covered under

master budget which creates huge

confusion. This directly reduces overall

workforce performance of the

employee's.

Master budget does not specify all the

activities clearly such as, if the

administration want to know how much

marketing department is growing and

expanding then clear picture is not

provided.

Flexible budget: Ovation System Ltd adopts flexible budget in the working environment

because this assist them to change their budget according to their demand and preferences.

Flexible budget showcase incomes, expenses and cost at numerous stages of level. This is more

appropriate for administration as it compare to Static budget, in this particular budget all the

necessary modification can be render according to the business condition. However, this budget

stands for the changes in the expenses and income with the changes in output. The advantages

and disadvantage of flexible budget are discussed as follow:

9

P4) Discuss advantages and disadvantages of various kind of planning tools which are utilized

for budgetary control

Master budget: Ovation System Ltd uses this budget in the working environment as it

involves all kinds of small fund within. Large companies mostly adopt this in order to keep

confidential data and information in a one single document. Master budget is associated with all

the activities which are, sales, operating expense, income, expenses, and assets. Additionally,

master budget represents financial plans, cash forecasting and financial statement and assist

company to frame strategies accordingly. Here, are some benefits and drawbacks which are

discussed as:

Advantages Disadvantages

All the budgeted information is

accumulated in one report this is one

of the biggest advantages which is

given by master budget (Englund and

Gerdin, 2018).

Expenses related to all the budgets is

determined so that additional cost can

be get rid of from any of the budget.

This helps in getting productive results

in the cut throat competitive world.

Numerous budgets are covered under

master budget which creates huge

confusion. This directly reduces overall

workforce performance of the

employee's.

Master budget does not specify all the

activities clearly such as, if the

administration want to know how much

marketing department is growing and

expanding then clear picture is not

provided.

Flexible budget: Ovation System Ltd adopts flexible budget in the working environment

because this assist them to change their budget according to their demand and preferences.

Flexible budget showcase incomes, expenses and cost at numerous stages of level. This is more

appropriate for administration as it compare to Static budget, in this particular budget all the

necessary modification can be render according to the business condition. However, this budget

stands for the changes in the expenses and income with the changes in output. The advantages

and disadvantage of flexible budget are discussed as follow:

9

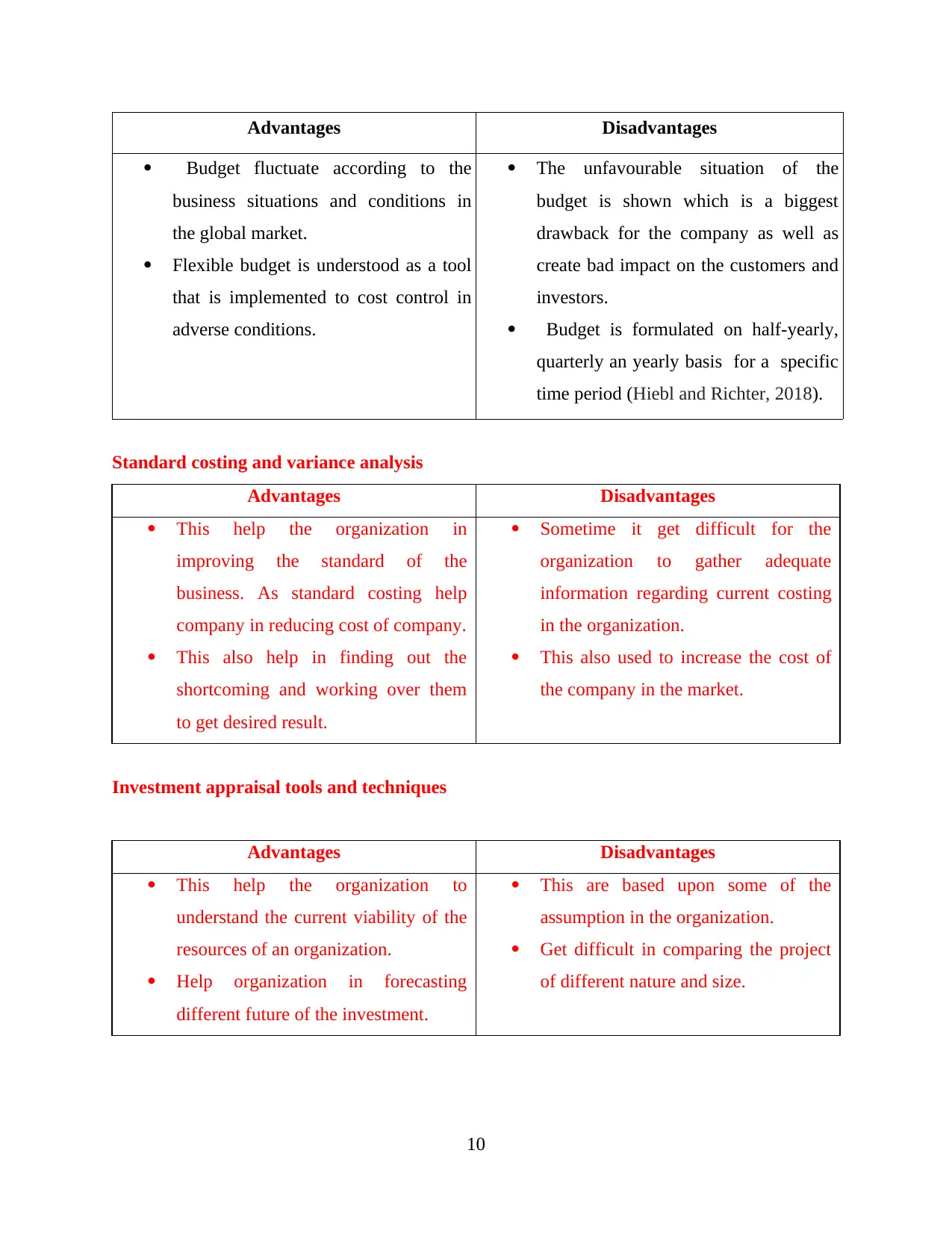

Advantages Disadvantages

Budget fluctuate according to the

business situations and conditions in

the global market.

Flexible budget is understood as a tool

that is implemented to cost control in

adverse conditions.

The unfavourable situation of the

budget is shown which is a biggest

drawback for the company as well as

create bad impact on the customers and

investors.

Budget is formulated on half-yearly,

quarterly an yearly basis for a specific

time period (Hiebl and Richter, 2018).

Standard costing and variance analysis

Advantages Disadvantages

This help the organization in

improving the standard of the

business. As standard costing help

company in reducing cost of company.

This also help in finding out the

shortcoming and working over them

to get desired result.

Sometime it get difficult for the

organization to gather adequate

information regarding current costing

in the organization.

This also used to increase the cost of

the company in the market.

Investment appraisal tools and techniques

Advantages Disadvantages

This help the organization to

understand the current viability of the

resources of an organization.

Help organization in forecasting

different future of the investment.

This are based upon some of the

assumption in the organization.

Get difficult in comparing the project

of different nature and size.

10

Budget fluctuate according to the

business situations and conditions in

the global market.

Flexible budget is understood as a tool

that is implemented to cost control in

adverse conditions.

The unfavourable situation of the

budget is shown which is a biggest

drawback for the company as well as

create bad impact on the customers and

investors.

Budget is formulated on half-yearly,

quarterly an yearly basis for a specific

time period (Hiebl and Richter, 2018).

Standard costing and variance analysis

Advantages Disadvantages

This help the organization in

improving the standard of the

business. As standard costing help

company in reducing cost of company.

This also help in finding out the

shortcoming and working over them

to get desired result.

Sometime it get difficult for the

organization to gather adequate

information regarding current costing

in the organization.

This also used to increase the cost of

the company in the market.

Investment appraisal tools and techniques

Advantages Disadvantages

This help the organization to

understand the current viability of the

resources of an organization.

Help organization in forecasting

different future of the investment.

This are based upon some of the

assumption in the organization.

Get difficult in comparing the project

of different nature and size.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

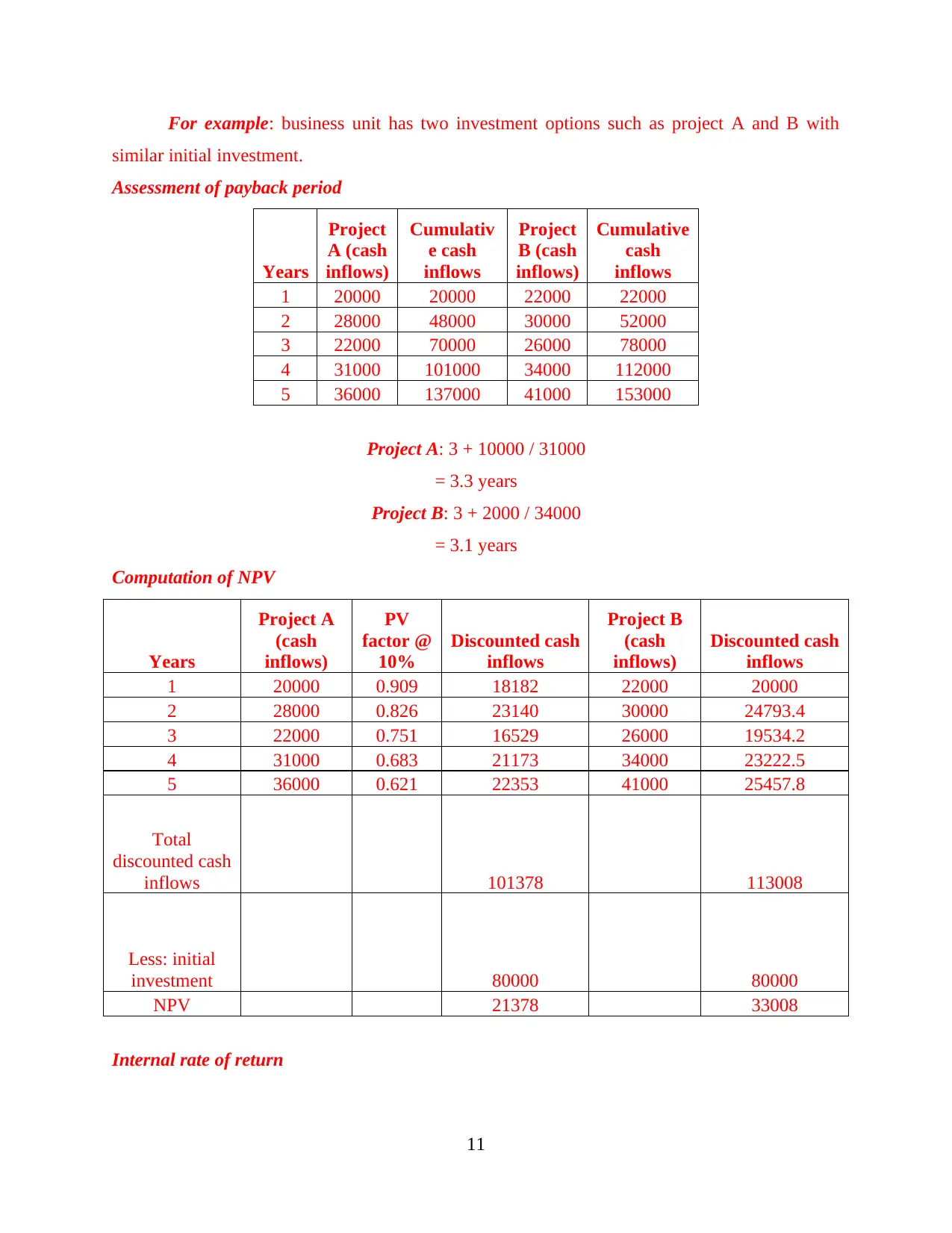

For example: business unit has two investment options such as project A and B with

similar initial investment.

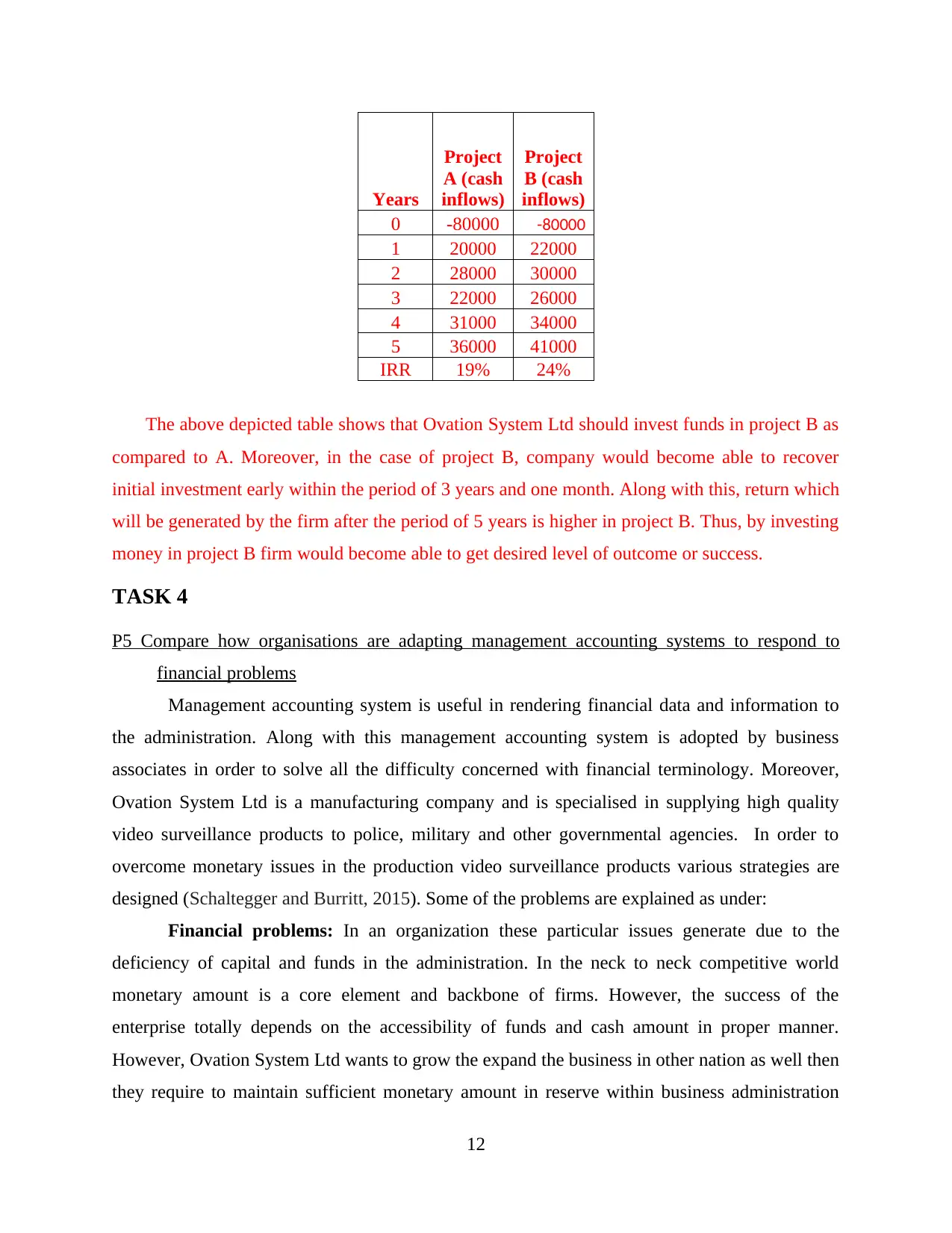

Assessment of payback period

Years

Project

A (cash

inflows)

Cumulativ

e cash

inflows

Project

B (cash

inflows)

Cumulative

cash

inflows

1 20000 20000 22000 22000

2 28000 48000 30000 52000

3 22000 70000 26000 78000

4 31000 101000 34000 112000

5 36000 137000 41000 153000

Project A: 3 + 10000 / 31000

= 3.3 years

Project B: 3 + 2000 / 34000

= 3.1 years

Computation of NPV

Years

Project A

(cash

inflows)

PV

factor @

10%

Discounted cash

inflows

Project B

(cash

inflows)

Discounted cash

inflows

1 20000 0.909 18182 22000 20000

2 28000 0.826 23140 30000 24793.4

3 22000 0.751 16529 26000 19534.2

4 31000 0.683 21173 34000 23222.5

5 36000 0.621 22353 41000 25457.8

Total

discounted cash

inflows 101378 113008

Less: initial

investment 80000 80000

NPV 21378 33008

Internal rate of return

11

similar initial investment.

Assessment of payback period

Years

Project

A (cash

inflows)

Cumulativ

e cash

inflows

Project

B (cash

inflows)

Cumulative

cash

inflows

1 20000 20000 22000 22000

2 28000 48000 30000 52000

3 22000 70000 26000 78000

4 31000 101000 34000 112000

5 36000 137000 41000 153000

Project A: 3 + 10000 / 31000

= 3.3 years

Project B: 3 + 2000 / 34000

= 3.1 years

Computation of NPV

Years

Project A

(cash

inflows)

PV

factor @

10%

Discounted cash

inflows

Project B

(cash

inflows)

Discounted cash

inflows

1 20000 0.909 18182 22000 20000

2 28000 0.826 23140 30000 24793.4

3 22000 0.751 16529 26000 19534.2

4 31000 0.683 21173 34000 23222.5

5 36000 0.621 22353 41000 25457.8

Total

discounted cash

inflows 101378 113008

Less: initial

investment 80000 80000

NPV 21378 33008

Internal rate of return

11

Years

Project

A (cash

inflows)

Project

B (cash

inflows)

0 -80000 -80000

1 20000 22000

2 28000 30000

3 22000 26000

4 31000 34000

5 36000 41000

IRR 19% 24%

The above depicted table shows that Ovation System Ltd should invest funds in project B as

compared to A. Moreover, in the case of project B, company would become able to recover

initial investment early within the period of 3 years and one month. Along with this, return which

will be generated by the firm after the period of 5 years is higher in project B. Thus, by investing

money in project B firm would become able to get desired level of outcome or success.

TASK 4

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Management accounting system is useful in rendering financial data and information to

the administration. Along with this management accounting system is adopted by business

associates in order to solve all the difficulty concerned with financial terminology. Moreover,

Ovation System Ltd is a manufacturing company and is specialised in supplying high quality

video surveillance products to police, military and other governmental agencies. In order to

overcome monetary issues in the production video surveillance products various strategies are

designed (Schaltegger and Burritt, 2015). Some of the problems are explained as under:

Financial problems: In an organization these particular issues generate due to the

deficiency of capital and funds in the administration. In the neck to neck competitive world

monetary amount is a core element and backbone of firms. However, the success of the

enterprise totally depends on the accessibility of funds and cash amount in proper manner.

However, Ovation System Ltd wants to grow the expand the business in other nation as well then

they require to maintain sufficient monetary amount in reserve within business administration

12

Project

A (cash

inflows)

Project

B (cash

inflows)

0 -80000 -80000

1 20000 22000

2 28000 30000

3 22000 26000

4 31000 34000

5 36000 41000

IRR 19% 24%

The above depicted table shows that Ovation System Ltd should invest funds in project B as

compared to A. Moreover, in the case of project B, company would become able to recover

initial investment early within the period of 3 years and one month. Along with this, return which

will be generated by the firm after the period of 5 years is higher in project B. Thus, by investing

money in project B firm would become able to get desired level of outcome or success.

TASK 4

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Management accounting system is useful in rendering financial data and information to

the administration. Along with this management accounting system is adopted by business

associates in order to solve all the difficulty concerned with financial terminology. Moreover,

Ovation System Ltd is a manufacturing company and is specialised in supplying high quality

video surveillance products to police, military and other governmental agencies. In order to

overcome monetary issues in the production video surveillance products various strategies are

designed (Schaltegger and Burritt, 2015). Some of the problems are explained as under:

Financial problems: In an organization these particular issues generate due to the

deficiency of capital and funds in the administration. In the neck to neck competitive world

monetary amount is a core element and backbone of firms. However, the success of the

enterprise totally depends on the accessibility of funds and cash amount in proper manner.

However, Ovation System Ltd wants to grow the expand the business in other nation as well then

they require to maintain sufficient monetary amount in reserve within business administration

12

(Hiebl, 2018). Below are mentioned some of the financial obstacles which are discussed as

under:

Deficiency of budget and money management skills: In cut throat competitive world

this issue occurs in the business because the top level management does not carry

sufficient and proper knowledge regarding budget implementation in productive way.

Along with this holding inappropriate money management skills is another issues which

results in unproductive outcomes for investments. This directly leads in mismanagement

of funds due to which company are able to ascertain where to invest and where not to. All

this aspect affects the set goals and objective of the administration.

Improper cash flow management: The difference between inflow and outflow of the

cash is one of the reason for financial crisis. Increasing the number of creditors,

unexpected changes occurring in the environment and so on are some of issues which is

faced by the administration (Hoque, 2018).

Therefore, the mentioned issues needed to be resolved by Ovation System Ltd so as to

operate and function their business smoothly in the global market. Additionally, there are

numerous techniques that is used by firm in order to solve financial issues. They are discussed as

follows:

Benchmarking: Administration adopts this tools and techniques to measure its

services, processes and products. It is directly beneficial for organization as it aids to find out

deviation among anticipated and actual results. Ovation System Ltd effectively implement this in

the working premises as it resolves the issue associated with improper cash flow. Benchmarking

is useful in the determining the internal opportunities prevailing in the administration. Along

with this ascertain the others successful firm's tactics so as to modify their strategies and

operations activities respectively. Benchmarking assist the organization to cut down problems

related to improper cash flow. By doing so set objectives can be achieved in the set time duration

(Qian and Schaltegger, 2018).

KPI (key performance indicator): In the modern world company adopts this

technique to refer the success and failure rate of the company. This is helpful for enterprise as it

aids to better understand the success level at each and every stage. By doing so organization is

running its activities in a correct path or not is measured in effective manner. Financial and non-

financial are two types of KPI tools which is studied by the firm. Moreover, Ovation System Ltd

13

under:

Deficiency of budget and money management skills: In cut throat competitive world

this issue occurs in the business because the top level management does not carry

sufficient and proper knowledge regarding budget implementation in productive way.

Along with this holding inappropriate money management skills is another issues which

results in unproductive outcomes for investments. This directly leads in mismanagement

of funds due to which company are able to ascertain where to invest and where not to. All

this aspect affects the set goals and objective of the administration.

Improper cash flow management: The difference between inflow and outflow of the

cash is one of the reason for financial crisis. Increasing the number of creditors,

unexpected changes occurring in the environment and so on are some of issues which is

faced by the administration (Hoque, 2018).

Therefore, the mentioned issues needed to be resolved by Ovation System Ltd so as to

operate and function their business smoothly in the global market. Additionally, there are

numerous techniques that is used by firm in order to solve financial issues. They are discussed as

follows:

Benchmarking: Administration adopts this tools and techniques to measure its

services, processes and products. It is directly beneficial for organization as it aids to find out

deviation among anticipated and actual results. Ovation System Ltd effectively implement this in

the working premises as it resolves the issue associated with improper cash flow. Benchmarking

is useful in the determining the internal opportunities prevailing in the administration. Along

with this ascertain the others successful firm's tactics so as to modify their strategies and

operations activities respectively. Benchmarking assist the organization to cut down problems

related to improper cash flow. By doing so set objectives can be achieved in the set time duration

(Qian and Schaltegger, 2018).

KPI (key performance indicator): In the modern world company adopts this

technique to refer the success and failure rate of the company. This is helpful for enterprise as it

aids to better understand the success level at each and every stage. By doing so organization is

running its activities in a correct path or not is measured in effective manner. Financial and non-

financial are two types of KPI tools which is studied by the firm. Moreover, Ovation System Ltd

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

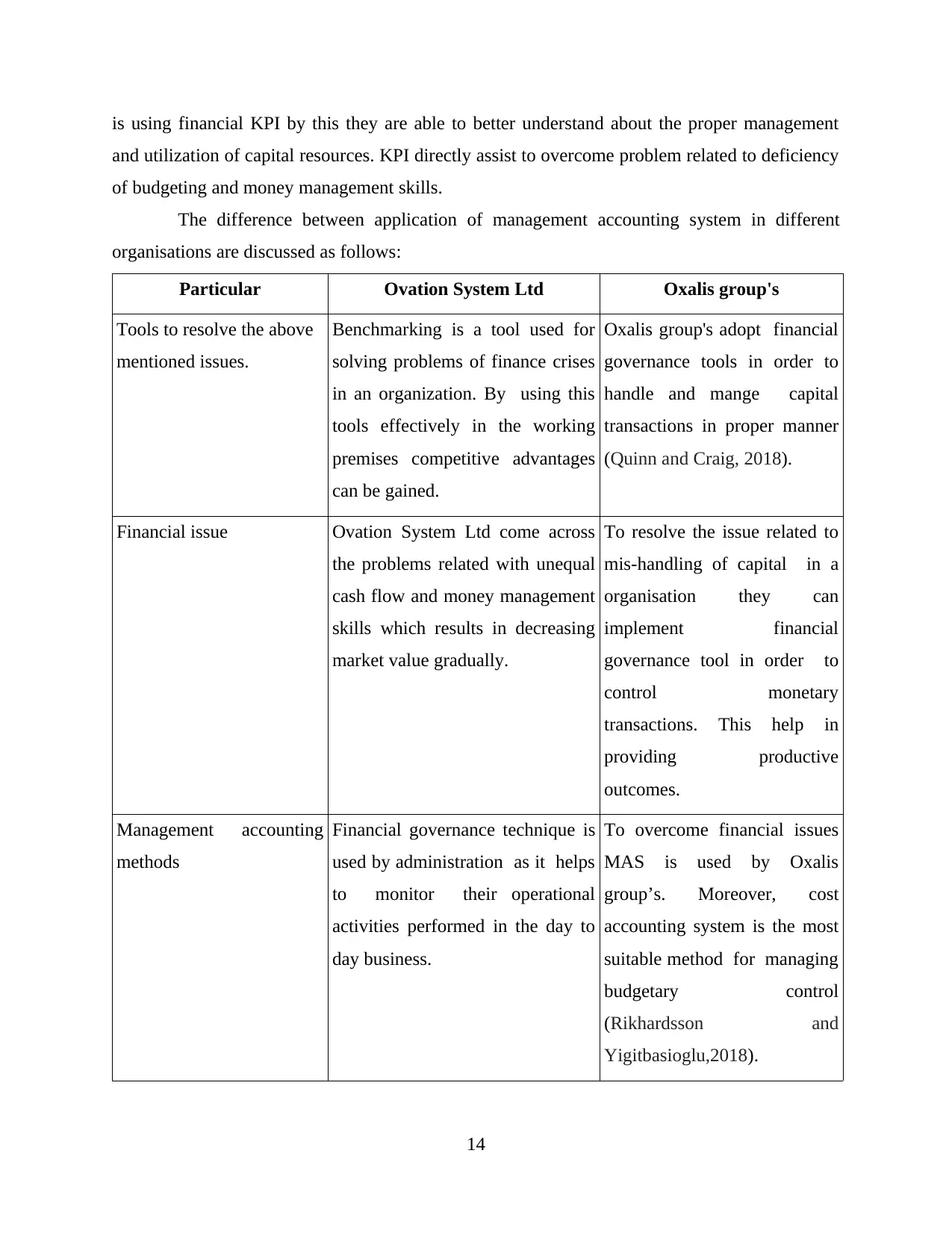

is using financial KPI by this they are able to better understand about the proper management

and utilization of capital resources. KPI directly assist to overcome problem related to deficiency

of budgeting and money management skills.

The difference between application of management accounting system in different

organisations are discussed as follows:

Particular Ovation System Ltd Oxalis group's

Tools to resolve the above

mentioned issues.

Benchmarking is a tool used for

solving problems of finance crises

in an organization. By using this

tools effectively in the working

premises competitive advantages

can be gained.

Oxalis group's adopt financial

governance tools in order to

handle and mange capital

transactions in proper manner

(Quinn and Craig, 2018).

Financial issue Ovation System Ltd come across

the problems related with unequal

cash flow and money management

skills which results in decreasing

market value gradually.

To resolve the issue related to

mis-handling of capital in a

organisation they can

implement financial

governance tool in order to

control monetary

transactions. This help in

providing productive

outcomes.

Management accounting

methods

Financial governance technique is

used by administration as it helps

to monitor their operational

activities performed in the day to

day business.

To overcome financial issues

MAS is used by Oxalis

group’s. Moreover, cost

accounting system is the most

suitable method for managing

budgetary control

(Rikhardsson and

Yigitbasioglu,2018).

14

and utilization of capital resources. KPI directly assist to overcome problem related to deficiency

of budgeting and money management skills.

The difference between application of management accounting system in different

organisations are discussed as follows:

Particular Ovation System Ltd Oxalis group's

Tools to resolve the above

mentioned issues.

Benchmarking is a tool used for

solving problems of finance crises

in an organization. By using this

tools effectively in the working

premises competitive advantages

can be gained.

Oxalis group's adopt financial

governance tools in order to

handle and mange capital

transactions in proper manner

(Quinn and Craig, 2018).

Financial issue Ovation System Ltd come across

the problems related with unequal

cash flow and money management

skills which results in decreasing

market value gradually.

To resolve the issue related to

mis-handling of capital in a

organisation they can

implement financial

governance tool in order to

control monetary

transactions. This help in

providing productive

outcomes.

Management accounting

methods

Financial governance technique is

used by administration as it helps

to monitor their operational

activities performed in the day to

day business.

To overcome financial issues

MAS is used by Oxalis

group’s. Moreover, cost

accounting system is the most

suitable method for managing

budgetary control

(Rikhardsson and

Yigitbasioglu,2018).

14

CONCLUSION

From the discussion it come to an end that cost accounting is the essential element which

need to be conducted in an organization. Functioning of inappropriate management accounting

gives unproductive results in the international market. Business concern need to frame strategies

by scanning the external environment so that set management can take best decision for the

betterment of the employees and employer both. This assist in meeting the deserving goals and

objectives in the specific time period. Distinguished administration ways of adopting

management accounting system is different in their working premises. Comparison is done

among several firm's on executing accounting systems so that further improvements can be done

accordingly. It directly or indirectly helps the business administration to work day and night to

full-fill the dynamic needs, demands and preferences of the consumers respectively. By

discussing numerous methods of management accounting reporting the best and the most

suitable is adopted in the company. The deeply scanning the organization methods related to

accounting reporting should be performed. By doing so employees can be motivated to increase

their workforce efficiency in the intense competitive world. Also, tough competition is

formulated for the business dealing in the same field in the open market place.

15

From the discussion it come to an end that cost accounting is the essential element which

need to be conducted in an organization. Functioning of inappropriate management accounting

gives unproductive results in the international market. Business concern need to frame strategies

by scanning the external environment so that set management can take best decision for the

betterment of the employees and employer both. This assist in meeting the deserving goals and

objectives in the specific time period. Distinguished administration ways of adopting

management accounting system is different in their working premises. Comparison is done

among several firm's on executing accounting systems so that further improvements can be done

accordingly. It directly or indirectly helps the business administration to work day and night to

full-fill the dynamic needs, demands and preferences of the consumers respectively. By

discussing numerous methods of management accounting reporting the best and the most

suitable is adopted in the company. The deeply scanning the organization methods related to

accounting reporting should be performed. By doing so employees can be motivated to increase

their workforce efficiency in the intense competitive world. Also, tough competition is

formulated for the business dealing in the same field in the open market place.

15

REFERENCES

Books and Journals

Abernethy, M. A. and Wallis, M.S., 2018. Critique on the'manager effects' research and

implications for management accounting research. Journal of Management Accounting

Research.

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

Agrawal, R. K., 2018. Principle of Management Accounting. Educreation Publishing.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review, 23(3), pp.222-226.

Beyer, A., Guttman, I. and Marinovic, I., 2018. Earnings management and earnings quality:

Theory and evidence. The Accounting Review. 94(4). pp.77-101.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting

Review. 49(1). pp.4-24.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Di Vaio, A. and Varriale, L., 2018. Management innovation for environmental sustainability in

seaports: Managerial accounting instruments and training for competitive green ports

beyond the regulations. Sustainability. 10(3). p.783.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Hiebl, M. R. and Richter, J. F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research. 30(2). pp.59-79.

Hiebl, M. R., 2018. Management accounting as a political resource for enabling embedded

agency. Management Accounting Research. 38. pp.22-38.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of cleaner production.

174. pp.1608-1619.

Quinn, M., Hiebl, M. R., Moores, K. and Craig, J. B., 2018. Future research on management

accounting and control in family firms: suggestions linked to architecture, governance,

entrepreneurship and stewardship. Journal of Management Control. 28(4). pp.529-546.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Books and Journals

Abernethy, M. A. and Wallis, M.S., 2018. Critique on the'manager effects' research and

implications for management accounting research. Journal of Management Accounting

Research.

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance. 7(01). p.1650014.

Agrawal, R. K., 2018. Principle of Management Accounting. Educreation Publishing.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review, 23(3), pp.222-226.

Beyer, A., Guttman, I. and Marinovic, I., 2018. Earnings management and earnings quality:

Theory and evidence. The Accounting Review. 94(4). pp.77-101.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting

Review. 49(1). pp.4-24.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Di Vaio, A. and Varriale, L., 2018. Management innovation for environmental sustainability in

seaports: Managerial accounting instruments and training for competitive green ports

beyond the regulations. Sustainability. 10(3). p.783.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Hiebl, M. R. and Richter, J. F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research. 30(2). pp.59-79.

Hiebl, M. R., 2018. Management accounting as a political resource for enabling embedded

agency. Management Accounting Research. 38. pp.22-38.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of cleaner production.

174. pp.1608-1619.

Quinn, M., Hiebl, M. R., Moores, K. and Craig, J. B., 2018. Future research on management

accounting and control in family firms: suggestions linked to architecture, governance,

entrepreneurship and stewardship. Journal of Management Control. 28(4). pp.529-546.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Schaltegger, S., 2018. Linking environmental management accounting: A reflection on (missing)

links to sustainability and planetary boundaries. Social and Environmental

Accountability Journal. 38(1). pp.19-29.

Turner, M. J., Way, S. A., Hodari, D. and Witteman, W., 2017. Hotel property performance: The

role of strategic management accounting. International Journal of Hospitality

Management. 63. pp.33-43.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online:

About Management Accounting. 2018. [Online]. Available

through:<http://www.accountingnotes.net/management-accounting/management-

accounting-meaning-limitations-and-scope/5859>.

and practice. Routledge.

Schaltegger, S., 2018. Linking environmental management accounting: A reflection on (missing)

links to sustainability and planetary boundaries. Social and Environmental

Accountability Journal. 38(1). pp.19-29.

Turner, M. J., Way, S. A., Hodari, D. and Witteman, W., 2017. Hotel property performance: The

role of strategic management accounting. International Journal of Hospitality

Management. 63. pp.33-43.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online:

About Management Accounting. 2018. [Online]. Available

through:<http://www.accountingnotes.net/management-accounting/management-

accounting-meaning-limitations-and-scope/5859>.

APPENDIX

1. Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

05/01

Previous

balance

(inventory)

40 3.00 120.00

05/12 40 3.00 120.00

Bought 25

units at £ 3.60

each

20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20

units at £ 3.75

each

20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

1. Valuation of closing stock using LIFO

Date Reference Purchase Issues Balance (Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

05/01

Previous

balance

(inventory)

40 3.00 120.00

05/12 40 3.00 120.00

Bought 25

units at £ 3.60

each

20 3.60 72. 20 3.60 72.00

05/15 20 3.60 72.

Issued 36 units 16 3.00 48. 24 3.00 72.00

05/20 24 3.00 72.00

Bought 20

units at £ 3.75

each

20 3.75 75. 20 3.75 75.00

05/23 Issued 10 units 10 3.75 37.5 24 3.00 72.00

10 3.75 37.50

05/27 9 3.75 33.75

Issued 25 units 25 3.00 75.00

05/30 Issued 5 units 5 3.00 15.00 4 3.75 15.00

2. Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.000

0

05/12 Bought 25 units

at £ 3.60 each 25 3.60 90. 65 3.2308 210.000

0

05/15 Issued 36 units 36 3.2308 116.30

77 29 3.2308 93.6923

05/20 Bought 20 units

at £ 3.75 each 20 3.75 75. 49 3.4427 168.692

3

05/23 Issued 10 units 10 3.4427 34.427

0 39 3.4427 134.265

3

05/27 Issued 25 units 25 3.4427 86.067

5 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.213

5 9 3.4427 30.9843

2. Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.000

0

05/12 Bought 25 units

at £ 3.60 each 25 3.60 90. 65 3.2308 210.000

0

05/15 Issued 36 units 36 3.2308 116.30

77 29 3.2308 93.6923

05/20 Bought 20 units

at £ 3.75 each 20 3.75 75. 49 3.4427 168.692

3

05/23 Issued 10 units 10 3.4427 34.427

0 39 3.4427 134.265

3

05/27 Issued 25 units 25 3.4427 86.067

5 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.213

5 9 3.4427 30.9843

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.