Report on Management Accounting Systems for Agmet Company

VerifiedAdded on 2020/06/06

|19

|5147

|48

Report

AI Summary

This report analyzes the application of management accounting principles within Agmet Company, a chemical product manufacturer. It begins by defining management accounting and exploring its various types, including cost accounting, price optimization, job costing, batch costing, and inventory management, highlighting their importance in controlling costs and optimizing resources. The report then outlines different methods used for management accounting reporting, such as segmental reports, performance reports, inventory management reports, accounts receivables aging reports, and job cost reports, emphasizing their roles in internal efficiency and decision-making. The core of the report involves a comparative analysis of marginal and absorption costing methods, including income statements and discussions of their differences. Finally, the report discusses the merits and demerits of various planning tools and how Agmet is adapting its management accounting systems to respond to financial challenges, concluding with an overview of the benefits of management accounting systems in enhancing financial returns and operational efficiency.

UNIT 5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Define management accounting and discuss essential requirements of different types of

management accounting.........................................................................................................1

(P2) Outline methods used for management accounting reporting........................................3

TASK 2 ...........................................................................................................................................6

(P3) Computation of marginal and absorption costing and stating differences.....................6

..........................................................................................................................................................7

TASK 3 .........................................................................................................................................10

(P4) Discuss merits and demerits of different types of planning tools in the organisation..10

(P5) Outline how company is adapting management accounting systems to respond to

financial problems................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Define management accounting and discuss essential requirements of different types of

management accounting.........................................................................................................1

(P2) Outline methods used for management accounting reporting........................................3

TASK 2 ...........................................................................................................................................6

(P3) Computation of marginal and absorption costing and stating differences.....................6

..........................................................................................................................................................7

TASK 3 .........................................................................................................................................10

(P4) Discuss merits and demerits of different types of planning tools in the organisation..10

(P5) Outline how company is adapting management accounting systems to respond to

financial problems................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting provides ample of benefits to managers while taking decisions

for the betterment of the company. The enclosed report deals with Agmet company which is

engaged in production of chemical products and as such, management accounting is essential

requirement for it (Ward, 2012). It has several types which is helpful in analysing and controlling

the costs effectually. Marginal and absorption costing are important methods of management

accounting. The organisation may be benefited by preparing management accounting as it

controls cost of various overheads and as such, resources are fully optimised effectively.

TASK 1

To: General Manager

Agmet company

From: Management Accounting Officer

Subject: Writing a report to General Manager of Agmet company

Introduction:

In order to improve the internal efficiency of the organisation, the management accounting

techniques and tools are required by it. The management accounting will help Agmet to flourish

in its operations.

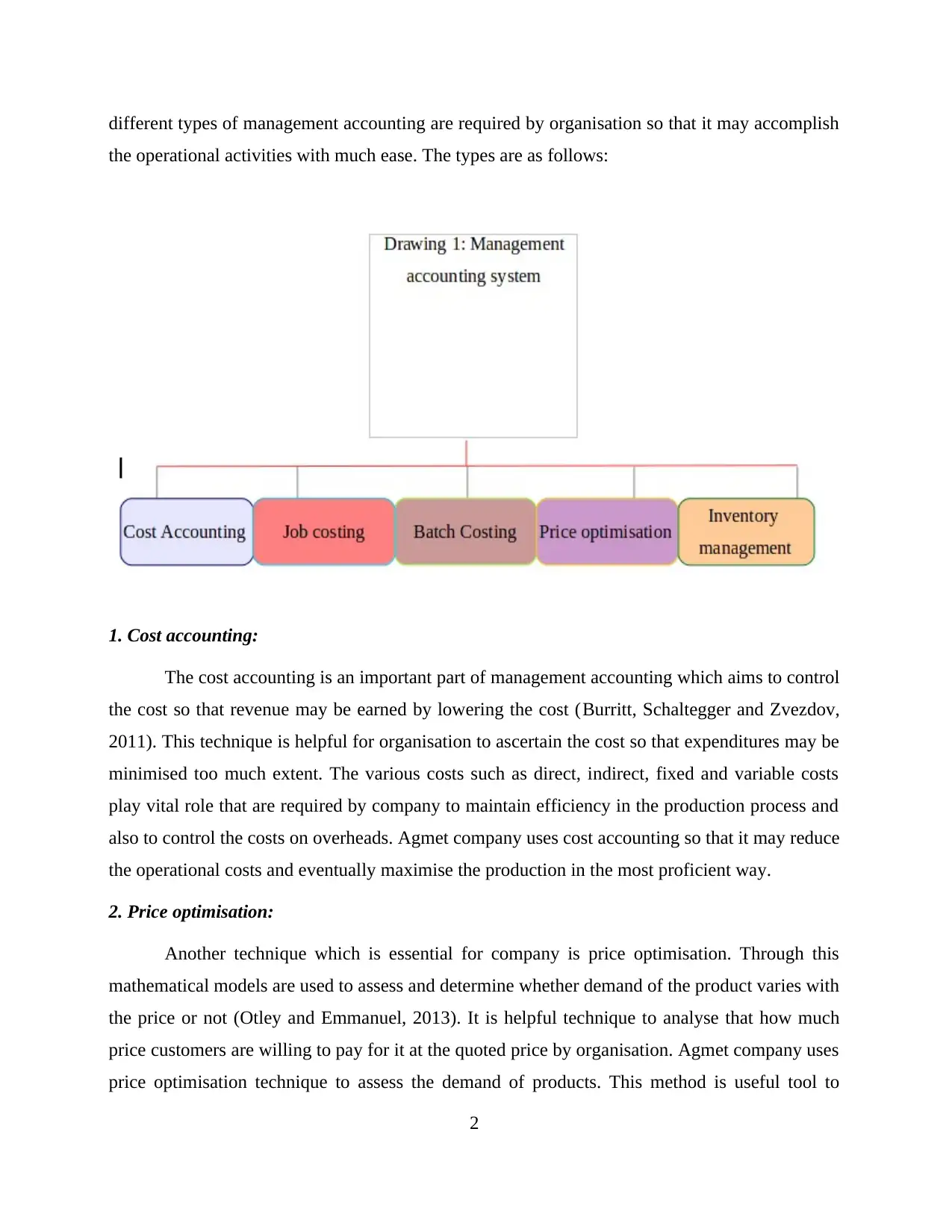

(P1) Define management accounting and discuss essential requirements of different types of

management accounting

Management accounting is useful accounting tool for managers to make effective

decisions for the betterment of the company. It is an amazing tool for management as through this

they are able to strengthen the internal position so that it may satisfy the demands of customers in

totality. Agmet company effectively uses management accounting information so that it may

manufacture chemical products with much ease (Parker, 2012). The cost accounting technique of

management accounting helps Agmet company to control the costs in effectual manner. It is

really helpful for organisation to meet its objectives by controlling the expenditures nicely. The

1

Management accounting provides ample of benefits to managers while taking decisions

for the betterment of the company. The enclosed report deals with Agmet company which is

engaged in production of chemical products and as such, management accounting is essential

requirement for it (Ward, 2012). It has several types which is helpful in analysing and controlling

the costs effectually. Marginal and absorption costing are important methods of management

accounting. The organisation may be benefited by preparing management accounting as it

controls cost of various overheads and as such, resources are fully optimised effectively.

TASK 1

To: General Manager

Agmet company

From: Management Accounting Officer

Subject: Writing a report to General Manager of Agmet company

Introduction:

In order to improve the internal efficiency of the organisation, the management accounting

techniques and tools are required by it. The management accounting will help Agmet to flourish

in its operations.

(P1) Define management accounting and discuss essential requirements of different types of

management accounting

Management accounting is useful accounting tool for managers to make effective

decisions for the betterment of the company. It is an amazing tool for management as through this

they are able to strengthen the internal position so that it may satisfy the demands of customers in

totality. Agmet company effectively uses management accounting information so that it may

manufacture chemical products with much ease (Parker, 2012). The cost accounting technique of

management accounting helps Agmet company to control the costs in effectual manner. It is

really helpful for organisation to meet its objectives by controlling the expenditures nicely. The

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

different types of management accounting are required by organisation so that it may accomplish

the operational activities with much ease. The types are as follows:

1. Cost accounting:

The cost accounting is an important part of management accounting which aims to control

the cost so that revenue may be earned by lowering the cost (Burritt, Schaltegger and Zvezdov,

2011). This technique is helpful for organisation to ascertain the cost so that expenditures may be

minimised too much extent. The various costs such as direct, indirect, fixed and variable costs

play vital role that are required by company to maintain efficiency in the production process and

also to control the costs on overheads. Agmet company uses cost accounting so that it may reduce

the operational costs and eventually maximise the production in the most proficient way.

2. Price optimisation:

Another technique which is essential for company is price optimisation. Through this

mathematical models are used to assess and determine whether demand of the product varies with

the price or not (Otley and Emmanuel, 2013). It is helpful technique to analyse that how much

price customers are willing to pay for it at the quoted price by organisation. Agmet company uses

price optimisation technique to assess the demand of products. This method is useful tool to

2

the operational activities with much ease. The types are as follows:

1. Cost accounting:

The cost accounting is an important part of management accounting which aims to control

the cost so that revenue may be earned by lowering the cost (Burritt, Schaltegger and Zvezdov,

2011). This technique is helpful for organisation to ascertain the cost so that expenditures may be

minimised too much extent. The various costs such as direct, indirect, fixed and variable costs

play vital role that are required by company to maintain efficiency in the production process and

also to control the costs on overheads. Agmet company uses cost accounting so that it may reduce

the operational costs and eventually maximise the production in the most proficient way.

2. Price optimisation:

Another technique which is essential for company is price optimisation. Through this

mathematical models are used to assess and determine whether demand of the product varies with

the price or not (Otley and Emmanuel, 2013). It is helpful technique to analyse that how much

price customers are willing to pay for it at the quoted price by organisation. Agmet company uses

price optimisation technique to assess the demand of products. This method is useful tool to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determine how demand fluctuates with the level of price of product which is being quoted by

company. As such, it imparts organisation clarity whether customers will pay for the quoted price

or not.

3. Job costing:

Job costing is another important method which is based on specific job which are

performed by various overheads (Weißenberger and Angelkort, 2011). It is useful tool to manage

the manufacturing cost such as cost of materials, of labour and overheads as well which are used

for production of chemical by Agmet company. Various jobs are analysed by management so that

costs incurred on each of it may be minimised so that more production may take place. The job

costing method is helpful to management as jobs which are incurring more expenditures may be

reduced so that production may be carried out in the most effective way. As a result, funds which

are saved may be utilised by firm for its effective functioning in the future.

4. Batch costing:

Every day in the production certain batches are being produced by organisation. As such,

batch costing is an effective method to control the expenditures which are incurred on several

batches and as a result, more production may be done with much ease. Agmet company

effectively uses batch costing method as expenses on batches of chemical products may be

minimised and more production may take place. Moreover, it estimates total labour, machinery

and quantity of materials which are being used to produce the chemical goods by Agmet in the

most proficient way.

5. Inventory management:

Inventory management is useful method to manage the inventory which is being required

for effective production. When stock is available in adequate manner, this reduces the wastage of

precious resources (Qian, Burritt and Monroe, 2011). Apart from this, more than required

inventories in the warehouse produces nothing but adds to additional cost which ultimately

deteriorates the revenue of Agmet company. As such, organisation needs managing inventories in

that way which yields it more profits by meeting the requirement of production.

(P2) Outline methods used for management accounting reporting

The various methods used for management accounting reporting are as listed below:

3

company. As such, it imparts organisation clarity whether customers will pay for the quoted price

or not.

3. Job costing:

Job costing is another important method which is based on specific job which are

performed by various overheads (Weißenberger and Angelkort, 2011). It is useful tool to manage

the manufacturing cost such as cost of materials, of labour and overheads as well which are used

for production of chemical by Agmet company. Various jobs are analysed by management so that

costs incurred on each of it may be minimised so that more production may take place. The job

costing method is helpful to management as jobs which are incurring more expenditures may be

reduced so that production may be carried out in the most effective way. As a result, funds which

are saved may be utilised by firm for its effective functioning in the future.

4. Batch costing:

Every day in the production certain batches are being produced by organisation. As such,

batch costing is an effective method to control the expenditures which are incurred on several

batches and as a result, more production may be done with much ease. Agmet company

effectively uses batch costing method as expenses on batches of chemical products may be

minimised and more production may take place. Moreover, it estimates total labour, machinery

and quantity of materials which are being used to produce the chemical goods by Agmet in the

most proficient way.

5. Inventory management:

Inventory management is useful method to manage the inventory which is being required

for effective production. When stock is available in adequate manner, this reduces the wastage of

precious resources (Qian, Burritt and Monroe, 2011). Apart from this, more than required

inventories in the warehouse produces nothing but adds to additional cost which ultimately

deteriorates the revenue of Agmet company. As such, organisation needs managing inventories in

that way which yields it more profits by meeting the requirement of production.

(P2) Outline methods used for management accounting reporting

The various methods used for management accounting reporting are as listed below:

3

1. Segmental report:

The segment reporting is quite useful to management as it helps them to analyse operating

segments by assessing the financial statements (Types of Managerial Accounting Reports). The

information produced by segmental report is useful to external stakeholders such as investors and

creditors as by analysing this they are able to make decisions of whether to invest or give funds to

company or not. It is the useful measuring tool which help them in gaining accounting

information of the organisation. Therefore, it is quite important tool of management. They assess

segmental reporting to make decisions. However, it is used by public firms and is not for the

private entities. This report includes revenue information and types of products which are sold by

organisation and this aids in decision making.

2. Performance report:

The performance report helps organisation to assess the performance of employees so that

their overall productivity may be increased in the best possible way. Performance report deals

with information of employee's performance so that organisation may come to know how they all

are working for the betterment of organisation (Van der Stede, 2011). Agmet company prepares

4

Source : (Granlund, 2011)

The segment reporting is quite useful to management as it helps them to analyse operating

segments by assessing the financial statements (Types of Managerial Accounting Reports). The

information produced by segmental report is useful to external stakeholders such as investors and

creditors as by analysing this they are able to make decisions of whether to invest or give funds to

company or not. It is the useful measuring tool which help them in gaining accounting

information of the organisation. Therefore, it is quite important tool of management. They assess

segmental reporting to make decisions. However, it is used by public firms and is not for the

private entities. This report includes revenue information and types of products which are sold by

organisation and this aids in decision making.

2. Performance report:

The performance report helps organisation to assess the performance of employees so that

their overall productivity may be increased in the best possible way. Performance report deals

with information of employee's performance so that organisation may come to know how they all

are working for the betterment of organisation (Van der Stede, 2011). Agmet company prepares

4

Source : (Granlund, 2011)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and analyses the performance of workers so that productivity may be increased to great extent.

This is important as by analysing the performance of workers, it is able to assess the actual

performance. Finally, the performance is matched with budgeted performance and if any

variances is found out, it can be resolved by taking corrective actions by Agmet company and in

this way efficiency of workers may be maximised by taking actions to regain the lost productivity

if any.

3. Inventory management report:

The inventory management report is another essential report which is prepared by

organisation. This helps to manage the stock in that way so that reduction in wastages may be

done. In this way Agmet company is able to produce according to the inventory which is

demanded by the production department. The excessive inventory in the warehouse certainly

increases the cost of handling and this deteriorates revenue and company should not do

unnecessary spoilage of stocks. The inventory management report aids Agmet to track the

inventory waste. By preparing this report, company analyses the inventory which is required by

production department and also helps to determine whether there is excessive inventory or not in

the warehouse. If excessive inventory is present, then it leads to additional costs which is not

good for organisation and as a result, this report helps to manage the inventory in the most

proficient manner.

4. Accounts receivables ageing report:

The firm needs funds for functioning properly to meet demands of daily activities. As

such, accounts receivables ageing report helps company to determine the customer invoices that

are become overdue for payment (Shah, Malik and Malik, 2011). It prepares list regarding unpaid

invoices and credit memos of customers so that payments should be done by them. If Agmet

company has liberal credit policies, then it should make strict polices so that timely payments

may be made by customers. It imparts clarity and transparency to managers regarding how much

outstanding payments are pending from the customers. As such, cash flows are managed

effectively by organisation. This helps managers to assess the payments which are pending from

customers. By analysing accounts receivables ageing report, managers implement strict credit

policies so that amount may be recovered timely.

5

This is important as by analysing the performance of workers, it is able to assess the actual

performance. Finally, the performance is matched with budgeted performance and if any

variances is found out, it can be resolved by taking corrective actions by Agmet company and in

this way efficiency of workers may be maximised by taking actions to regain the lost productivity

if any.

3. Inventory management report:

The inventory management report is another essential report which is prepared by

organisation. This helps to manage the stock in that way so that reduction in wastages may be

done. In this way Agmet company is able to produce according to the inventory which is

demanded by the production department. The excessive inventory in the warehouse certainly

increases the cost of handling and this deteriorates revenue and company should not do

unnecessary spoilage of stocks. The inventory management report aids Agmet to track the

inventory waste. By preparing this report, company analyses the inventory which is required by

production department and also helps to determine whether there is excessive inventory or not in

the warehouse. If excessive inventory is present, then it leads to additional costs which is not

good for organisation and as a result, this report helps to manage the inventory in the most

proficient manner.

4. Accounts receivables ageing report:

The firm needs funds for functioning properly to meet demands of daily activities. As

such, accounts receivables ageing report helps company to determine the customer invoices that

are become overdue for payment (Shah, Malik and Malik, 2011). It prepares list regarding unpaid

invoices and credit memos of customers so that payments should be done by them. If Agmet

company has liberal credit policies, then it should make strict polices so that timely payments

may be made by customers. It imparts clarity and transparency to managers regarding how much

outstanding payments are pending from the customers. As such, cash flows are managed

effectively by organisation. This helps managers to assess the payments which are pending from

customers. By analysing accounts receivables ageing report, managers implement strict credit

policies so that amount may be recovered timely.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Job cost report:

The job cost report deals with the cost which are incurred in carrying out various jobs in

the organisation (Chenhall and Smith, 2011). By carefully analysing job expenses, Agmet

company may be able to reduce expenditures which are deteriorating profit and as such, wastage

is minimised too much extent. The job cost report helps managers to asses specific job areas so

that profit may not get reduced. This ultimately helps company to effectively manage job's

profitability to those job areas which provide it results in the most proficient way. The job cost

report is quite helpful for organisation to manage costs on various jobs which carry out effective

production. Analysing various expenditures on jobs help Agmet to save funds and direct

expenses in maximising production in effectual manner.

The benefits of management accounting systems are

The management accounting systems have ample of benefits such as increasing financial

returns and managing and controlling costs in the most effectual way. Agmet carry out certain

activities and can review the economy and different operational functions in effectual manner.

Moreover, running costs in the firm may be analysed by it and this is quite helpful for

organisation. Apart from this, company may forecast customer's requirements which helps in

determining demand and as a result, profit may be maximised. These benefits of management

accounting systems help firm to increase profits by satisfying customer's needs effectually.

Management accounting reporting is integrated within organisational process :

Management accounting reporting helps company to improve its performance. This helps

company to create the value (DRURY, 2013). The management accounting reporting aids

organisation to effectively improve performance so that production may take place and in turn its

increase revenue of firm and as a result, competitive advantage is successfully gained. Moreover,

management accounting is related with planning and output which help to support operational

function in company. Expenditures are managed in the most proficient way and as a result,

management accounting reporting aids in accomplishing goals and objectives in effective

manner.

6

The job cost report deals with the cost which are incurred in carrying out various jobs in

the organisation (Chenhall and Smith, 2011). By carefully analysing job expenses, Agmet

company may be able to reduce expenditures which are deteriorating profit and as such, wastage

is minimised too much extent. The job cost report helps managers to asses specific job areas so

that profit may not get reduced. This ultimately helps company to effectively manage job's

profitability to those job areas which provide it results in the most proficient way. The job cost

report is quite helpful for organisation to manage costs on various jobs which carry out effective

production. Analysing various expenditures on jobs help Agmet to save funds and direct

expenses in maximising production in effectual manner.

The benefits of management accounting systems are

The management accounting systems have ample of benefits such as increasing financial

returns and managing and controlling costs in the most effectual way. Agmet carry out certain

activities and can review the economy and different operational functions in effectual manner.

Moreover, running costs in the firm may be analysed by it and this is quite helpful for

organisation. Apart from this, company may forecast customer's requirements which helps in

determining demand and as a result, profit may be maximised. These benefits of management

accounting systems help firm to increase profits by satisfying customer's needs effectually.

Management accounting reporting is integrated within organisational process :

Management accounting reporting helps company to improve its performance. This helps

company to create the value (DRURY, 2013). The management accounting reporting aids

organisation to effectively improve performance so that production may take place and in turn its

increase revenue of firm and as a result, competitive advantage is successfully gained. Moreover,

management accounting is related with planning and output which help to support operational

function in company. Expenditures are managed in the most proficient way and as a result,

management accounting reporting aids in accomplishing goals and objectives in effective

manner.

6

TASK 2

(P3) Computation of marginal and absorption costing and stating differences

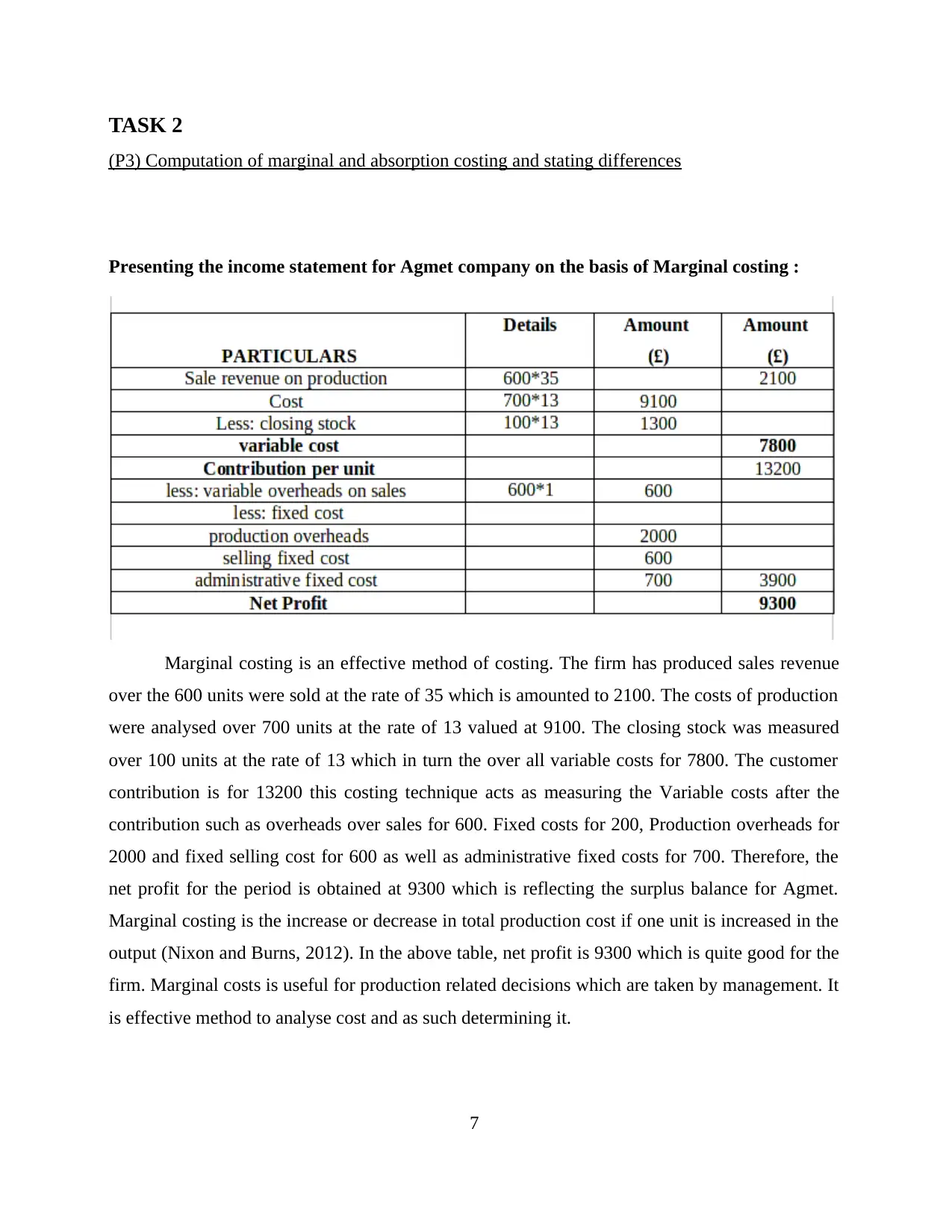

Presenting the income statement for Agmet company on the basis of Marginal costing :

Marginal costing is an effective method of costing. The firm has produced sales revenue

over the 600 units were sold at the rate of 35 which is amounted to 2100. The costs of production

were analysed over 700 units at the rate of 13 valued at 9100. The closing stock was measured

over 100 units at the rate of 13 which in turn the over all variable costs for 7800. The customer

contribution is for 13200 this costing technique acts as measuring the Variable costs after the

contribution such as overheads over sales for 600. Fixed costs for 200, Production overheads for

2000 and fixed selling cost for 600 as well as administrative fixed costs for 700. Therefore, the

net profit for the period is obtained at 9300 which is reflecting the surplus balance for Agmet.

Marginal costing is the increase or decrease in total production cost if one unit is increased in the

output (Nixon and Burns, 2012). In the above table, net profit is 9300 which is quite good for the

firm. Marginal costs is useful for production related decisions which are taken by management. It

is effective method to analyse cost and as such determining it.

7

(P3) Computation of marginal and absorption costing and stating differences

Presenting the income statement for Agmet company on the basis of Marginal costing :

Marginal costing is an effective method of costing. The firm has produced sales revenue

over the 600 units were sold at the rate of 35 which is amounted to 2100. The costs of production

were analysed over 700 units at the rate of 13 valued at 9100. The closing stock was measured

over 100 units at the rate of 13 which in turn the over all variable costs for 7800. The customer

contribution is for 13200 this costing technique acts as measuring the Variable costs after the

contribution such as overheads over sales for 600. Fixed costs for 200, Production overheads for

2000 and fixed selling cost for 600 as well as administrative fixed costs for 700. Therefore, the

net profit for the period is obtained at 9300 which is reflecting the surplus balance for Agmet.

Marginal costing is the increase or decrease in total production cost if one unit is increased in the

output (Nixon and Burns, 2012). In the above table, net profit is 9300 which is quite good for the

firm. Marginal costs is useful for production related decisions which are taken by management. It

is effective method to analyse cost and as such determining it.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

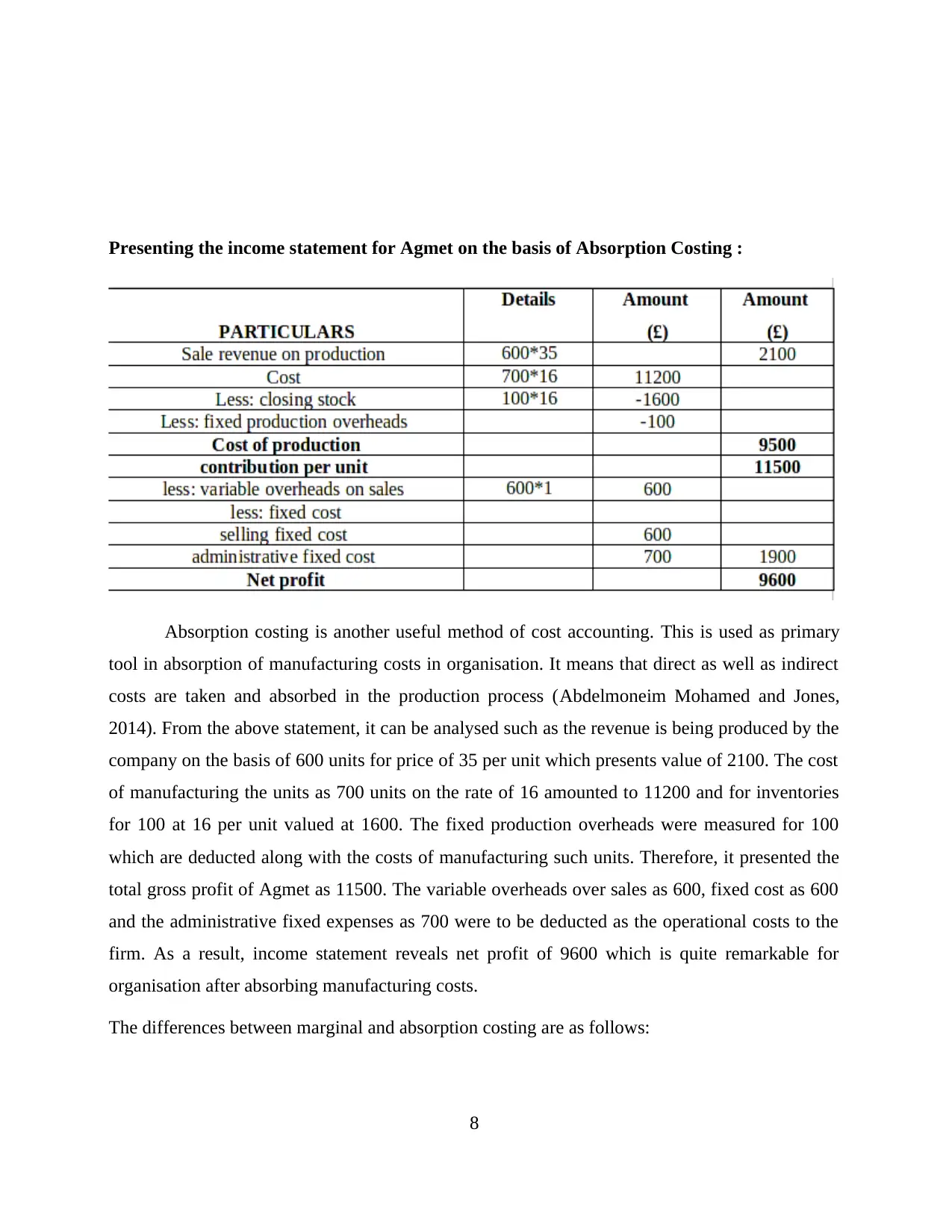

Presenting the income statement for Agmet on the basis of Absorption Costing :

Absorption costing is another useful method of cost accounting. This is used as primary

tool in absorption of manufacturing costs in organisation. It means that direct as well as indirect

costs are taken and absorbed in the production process (Abdelmoneim Mohamed and Jones,

2014). From the above statement, it can be analysed such as the revenue is being produced by the

company on the basis of 600 units for price of 35 per unit which presents value of 2100. The cost

of manufacturing the units as 700 units on the rate of 16 amounted to 11200 and for inventories

for 100 at 16 per unit valued at 1600. The fixed production overheads were measured for 100

which are deducted along with the costs of manufacturing such units. Therefore, it presented the

total gross profit of Agmet as 11500. The variable overheads over sales as 600, fixed cost as 600

and the administrative fixed expenses as 700 were to be deducted as the operational costs to the

firm. As a result, income statement reveals net profit of 9600 which is quite remarkable for

organisation after absorbing manufacturing costs.

The differences between marginal and absorption costing are as follows:

8

Absorption costing is another useful method of cost accounting. This is used as primary

tool in absorption of manufacturing costs in organisation. It means that direct as well as indirect

costs are taken and absorbed in the production process (Abdelmoneim Mohamed and Jones,

2014). From the above statement, it can be analysed such as the revenue is being produced by the

company on the basis of 600 units for price of 35 per unit which presents value of 2100. The cost

of manufacturing the units as 700 units on the rate of 16 amounted to 11200 and for inventories

for 100 at 16 per unit valued at 1600. The fixed production overheads were measured for 100

which are deducted along with the costs of manufacturing such units. Therefore, it presented the

total gross profit of Agmet as 11500. The variable overheads over sales as 600, fixed cost as 600

and the administrative fixed expenses as 700 were to be deducted as the operational costs to the

firm. As a result, income statement reveals net profit of 9600 which is quite remarkable for

organisation after absorbing manufacturing costs.

The differences between marginal and absorption costing are as follows:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Variable cost is only applied to inventory under marginal costing. However, under

absorption costing, fixed overheads costs are applied. As such, both of the costs are different

from each other (Cadez and Guilding, 2012).

2. Marginal costing is applied to inventory cost which was incurred when each unit was

produced of the product in the process by organisation. While, absorption costing is applied to all

the production costs to each of the units which were produced successfully by the production

department with much ease.

3. Another big difference is regarding profits. Marginal costing will yield much higher profit as

individual sale of goods are attained. However, absorption costing will impart lower profits to

organisation.

4. The profit is also measured differently in both the costing. Marginal costing uses contribution

margin which is deducted from overhead or it excludes overhead which was applied. On the other

hand, absorption costing assess profits by using gross margin which includes overhead and this is

how profit is being measured by each of the costing method.

5. Another difference is that overhead costs incurred during production are charged to expense in

the period which is under marginal costing. In contrary to this, overhead costs are applied or

charged to products under marginal costing method.

6. Last difference between marginal as well as absorption costing is that financial reporting is not

required under marginal method and whereas, it is required under absorption costing method of

management accounting. As a result, both costing method has their own importance in the

organisation to control and analyse cost in most productive way.

Management accounting techniques and financial reporting-

The techniques such as cost variance and revaluation accounting are useful method of

management accounting as it helps to improve performance of the company in effective manner

(Christ and Burritt, 2013). Cost variance is the difference between budgeted and actual costs. It is

helpful for generating financial reporting documents. Whereas, revaluation accounting is an

important accounting technique. It is an adjustment made to value of asset to analyse its current

market rate. These management accounting techniques are helpful for organisation and aids in

producing financial reporting.

9

absorption costing, fixed overheads costs are applied. As such, both of the costs are different

from each other (Cadez and Guilding, 2012).

2. Marginal costing is applied to inventory cost which was incurred when each unit was

produced of the product in the process by organisation. While, absorption costing is applied to all

the production costs to each of the units which were produced successfully by the production

department with much ease.

3. Another big difference is regarding profits. Marginal costing will yield much higher profit as

individual sale of goods are attained. However, absorption costing will impart lower profits to

organisation.

4. The profit is also measured differently in both the costing. Marginal costing uses contribution

margin which is deducted from overhead or it excludes overhead which was applied. On the other

hand, absorption costing assess profits by using gross margin which includes overhead and this is

how profit is being measured by each of the costing method.

5. Another difference is that overhead costs incurred during production are charged to expense in

the period which is under marginal costing. In contrary to this, overhead costs are applied or

charged to products under marginal costing method.

6. Last difference between marginal as well as absorption costing is that financial reporting is not

required under marginal method and whereas, it is required under absorption costing method of

management accounting. As a result, both costing method has their own importance in the

organisation to control and analyse cost in most productive way.

Management accounting techniques and financial reporting-

The techniques such as cost variance and revaluation accounting are useful method of

management accounting as it helps to improve performance of the company in effective manner

(Christ and Burritt, 2013). Cost variance is the difference between budgeted and actual costs. It is

helpful for generating financial reporting documents. Whereas, revaluation accounting is an

important accounting technique. It is an adjustment made to value of asset to analyse its current

market rate. These management accounting techniques are helpful for organisation and aids in

producing financial reporting.

9

Presenting the financial report of Agmet company

From: Management Accounting officer

To: General manager (Agmet company)

Subject: Facilitating the use of management accounting techniques in solving financial

problems

Sir,

The management accounting techniques are helpful for organisation so that financial

difficulties may be resolved with much ease. The budgets such as cash, sales, production, the

company will have efficient use of resources and as such, costs will be controlled. The

operational activities of the business will also be used to evaluate in the most productive

manner. It will also help in making better decisions by management.

TASK 3

(P4) Discuss merits and demerits of different types of planning tools in the organisation

Zero based budgeting:

This budgeting is prepared by management without using historical figures which means

that budget is prepared from completely scratch base and no reference is taken from past budget

(Sánchez-Rodríguez and Spraakman, 2012).

Advantages:

1. It ensures accuracy as completely new budget is prepared and no past figures are

included in it.

2. It is efficient as new budget is prepared by taking actual numbers and not from historic

figures.

Disadvantages:

10

From: Management Accounting officer

To: General manager (Agmet company)

Subject: Facilitating the use of management accounting techniques in solving financial

problems

Sir,

The management accounting techniques are helpful for organisation so that financial

difficulties may be resolved with much ease. The budgets such as cash, sales, production, the

company will have efficient use of resources and as such, costs will be controlled. The

operational activities of the business will also be used to evaluate in the most productive

manner. It will also help in making better decisions by management.

TASK 3

(P4) Discuss merits and demerits of different types of planning tools in the organisation

Zero based budgeting:

This budgeting is prepared by management without using historical figures which means

that budget is prepared from completely scratch base and no reference is taken from past budget

(Sánchez-Rodríguez and Spraakman, 2012).

Advantages:

1. It ensures accuracy as completely new budget is prepared and no past figures are

included in it.

2. It is efficient as new budget is prepared by taking actual numbers and not from historic

figures.

Disadvantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.