Presentation 10 Task 2: Report 11 Use of different planning tools use and advantages & disadvantages of budgets 12 Use and Advantages & Disadvantages of Variances 12 Use and Advantages & Disadvantages

VerifiedAdded on 2021/05/31

|23

|4241

|267

AI Summary

21 Unit 5: Budget Management Accounting NSAB530B5 Contents Budget Management Accounting NSAB530B5 Contents Task 1 3 Part A: Portfolio of Calculation and Comments 3 Comment and interpretation of above results 9 Part B: Presentation 10 Task 2: Report to Budget 11 Part A and B: 11 Use of different planning tools for the management to undertake the past budgeting methods 12 Use and Advantages & Disadvantages of Budgets 12 Use and Advantages & Disadvantages of Variances 13 Analysis of Adoption of Management Accounting

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Unit 5: Management Accounting NSAB530B5

Unit 5: Management Accounting NSAB530B5

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Contents

Task 1...............................................................................................................................................3

Part A: Portfolio of Calculation and Comments..............................................................................3

Comment and interpretation of above results..................................................................................9

Part B: Presentation.......................................................................................................................10

Task 2: Report................................................................................................................................11

Part A and B:.................................................................................................................................11

Use of different planning tools use budgetary tools with advantages and disadvantages of each

planning tools.................................................................................................................................12

Use and Advantages & Disadvantages of Budgets........................................................................12

Use and Advantages & Disadvantages of Variances.....................................................................13

Analysis of Adoption of Management Accounting Systems by Organizations in Responding to

Financial Problems........................................................................................................................13

Use of Management accounting for leading Organizations to Sustainable Success.....................15

Use of accounting planning tools to respond appropriately to solving financial problems of

organizations for sustainable success............................................................................................16

References......................................................................................................................................18

Contents

Task 1...............................................................................................................................................3

Part A: Portfolio of Calculation and Comments..............................................................................3

Comment and interpretation of above results..................................................................................9

Part B: Presentation.......................................................................................................................10

Task 2: Report................................................................................................................................11

Part A and B:.................................................................................................................................11

Use of different planning tools use budgetary tools with advantages and disadvantages of each

planning tools.................................................................................................................................12

Use and Advantages & Disadvantages of Budgets........................................................................12

Use and Advantages & Disadvantages of Variances.....................................................................13

Analysis of Adoption of Management Accounting Systems by Organizations in Responding to

Financial Problems........................................................................................................................13

Use of Management accounting for leading Organizations to Sustainable Success.....................15

Use of accounting planning tools to respond appropriately to solving financial problems of

organizations for sustainable success............................................................................................16

References......................................................................................................................................18

3

Task 1

Part A: Portfolio of Calculation and Comments

Summary of all the given information:

Year 3 3200

Sale Price per unit 85

Production

Year 1 3500

Year 2 3800

Year 3 3650

per unit

per unit

per unit

Task 1

Part A: Portfolio of Calculation and Comments

Summary of all the given information:

Year 3 3200

Sale Price per unit 85

Production

Year 1 3500

Year 2 3800

Year 3 3650

per unit

per unit

per unit

4

Distribution Expenses

Administrative Expenses

units

units Net loss before interest and taxes

units Less: Interest expenses

per unit Net Loss before tax

Add: Tax @ 19%

Net loss

units

units Income Statement Under Absorption Costing

units Year 2

Particulars

Sales (3500*85)

Less: Cost of Goods Sold

Opening Stock ( 900 units)

Production (3800 units * 30)

Less: Closing Stock (1200 units *30)

Less: Fixed Indirect manufacturing cost

Opening (900/3500) *92000

Production (2600/3800)*92000

Distribution Expenses

Administrative Expenses

units

units Net loss before interest and taxes

units Less: Interest expenses

per unit Net Loss before tax

Add: Tax @ 19%

Net loss

units

units Income Statement Under Absorption Costing

units Year 2

Particulars

Sales (3500*85)

Less: Cost of Goods Sold

Opening Stock ( 900 units)

Production (3800 units * 30)

Less: Closing Stock (1200 units *30)

Less: Fixed Indirect manufacturing cost

Opening (900/3500) *92000

Production (2600/3800)*92000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

Less: Closing Stock (1200 units *30)

Less: Fixed Indirect manufacturing cost

Opening (900/3500) *92000

Production (2600/3800)*92000

Total cost of good sold

Gross profit

Less: Other Overheads

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Absorption Costing

Year 3

Particulars

Sales (3200*85)

Less: Cost of Goods Sold

Opening Stock ( 1200 units *30)

Less: Closing Stock (1200 units *30)

Less: Fixed Indirect manufacturing cost

Opening (900/3500) *92000

Production (2600/3800)*92000

Total cost of good sold

Gross profit

Less: Other Overheads

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Absorption Costing

Year 3

Particulars

Sales (3200*85)

Less: Cost of Goods Sold

Opening Stock ( 1200 units *30)

6

Total cost of good sold

Gross profit

Less: Other Overheads

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net Loss

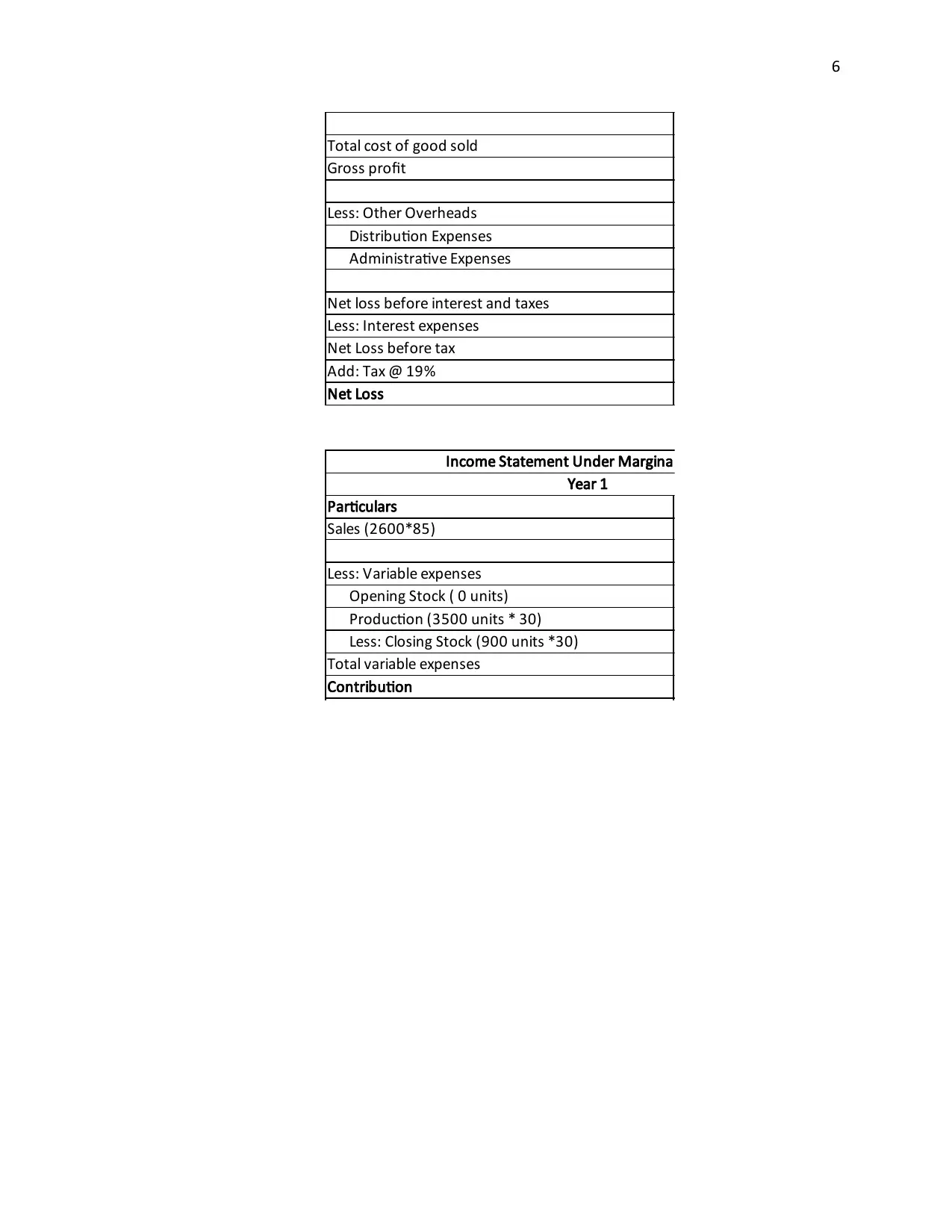

Income Statement Under Marginal Costing

Year 1

Particulars

Sales (2600*85)

Less: Variable expenses

Opening Stock ( 0 units)

Production (3500 units * 30)

Less: Closing Stock (900 units *30)

Total variable expenses

Contribution

Total cost of good sold

Gross profit

Less: Other Overheads

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net Loss

Income Statement Under Marginal Costing

Year 1

Particulars

Sales (2600*85)

Less: Variable expenses

Opening Stock ( 0 units)

Production (3500 units * 30)

Less: Closing Stock (900 units *30)

Total variable expenses

Contribution

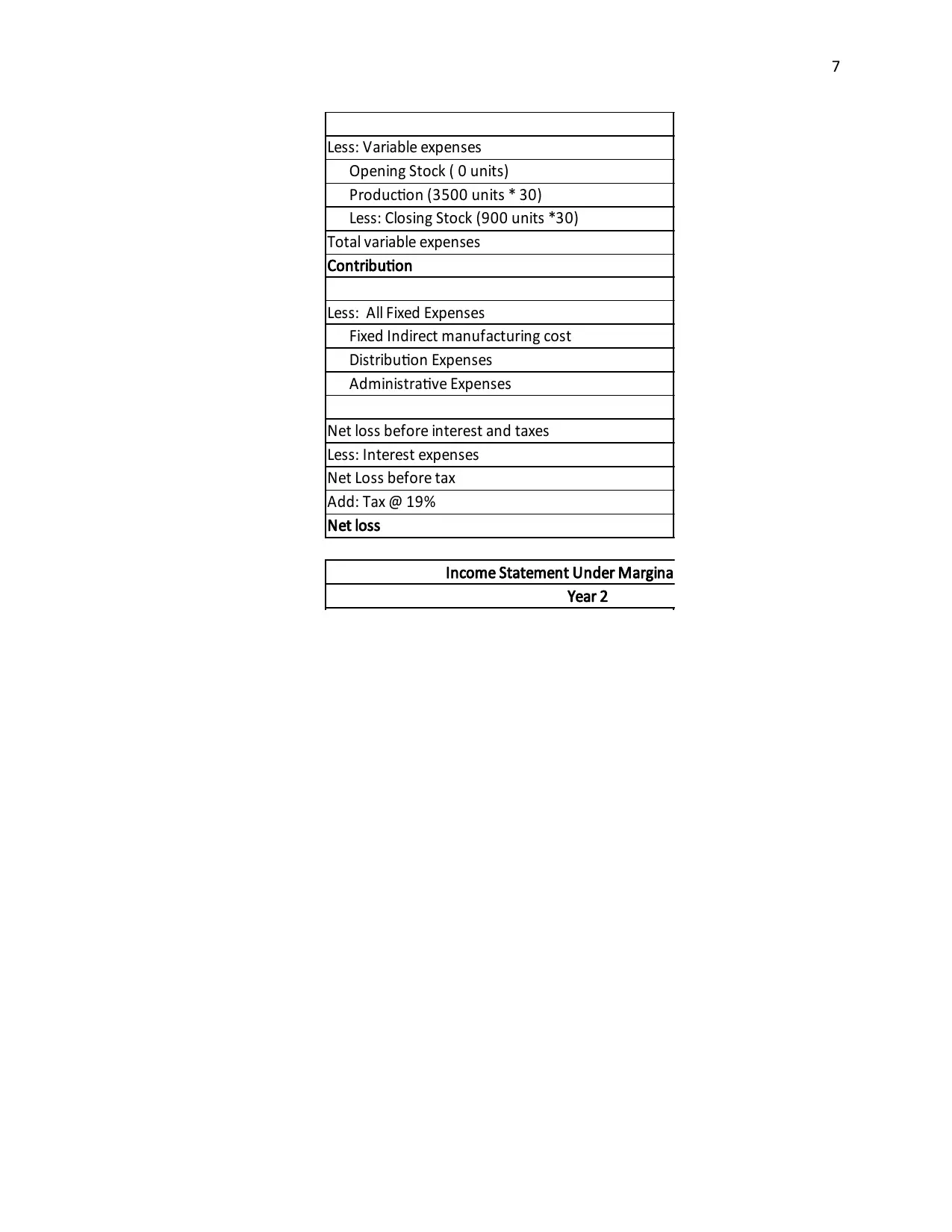

7

Less: Variable expenses

Opening Stock ( 0 units)

Production (3500 units * 30)

Less: Closing Stock (900 units *30)

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Marginal Costing

Year 2

Less: Variable expenses

Opening Stock ( 0 units)

Production (3500 units * 30)

Less: Closing Stock (900 units *30)

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Marginal Costing

Year 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

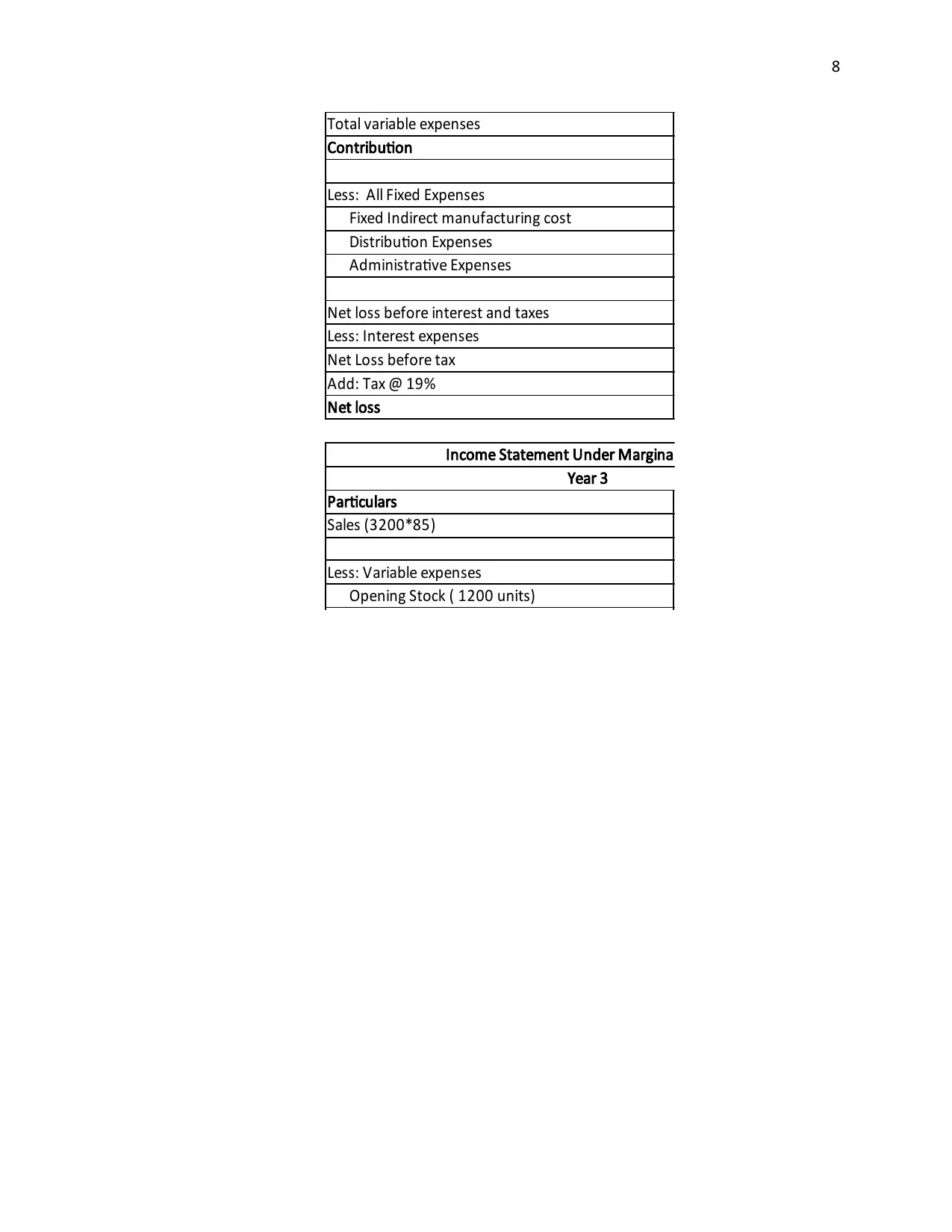

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Marginal Costing

Year 3

Particulars

Sales (3200*85)

Less: Variable expenses

Opening Stock ( 1200 units)

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Income Statement Under Marginal Costing

Year 3

Particulars

Sales (3200*85)

Less: Variable expenses

Opening Stock ( 1200 units)

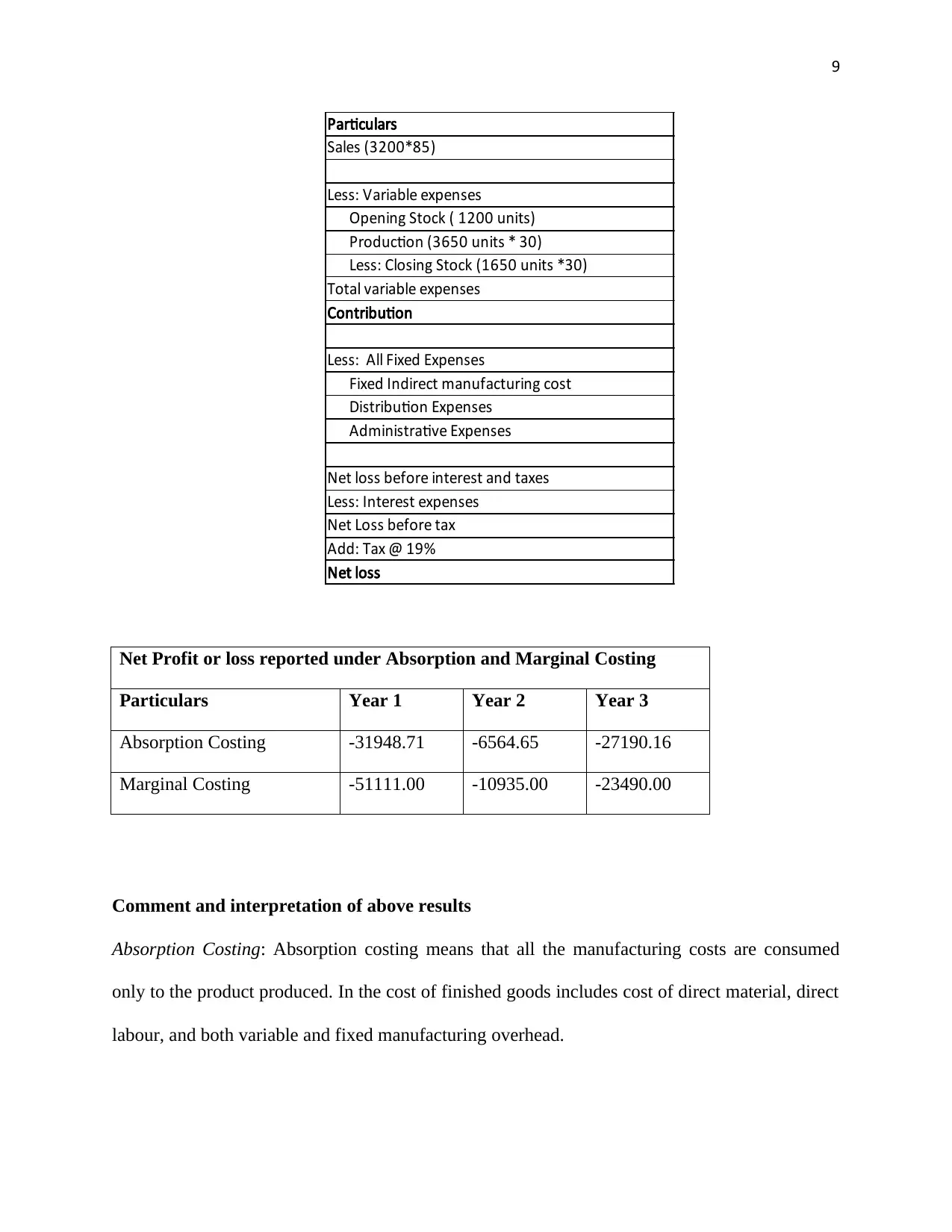

9

Particulars

Sales (3200*85)

Less: Variable expenses

Opening Stock ( 1200 units)

Production (3650 units * 30)

Less: Closing Stock (1650 units *30)

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Net Profit or loss reported under Absorption and Marginal Costing

Particulars Year 1 Year 2 Year 3

Absorption Costing -31948.71 -6564.65 -27190.16

Marginal Costing -51111.00 -10935.00 -23490.00

Comment and interpretation of above results

Absorption Costing: Absorption costing means that all the manufacturing costs are consumed

only to the product produced. In the cost of finished goods includes cost of direct material, direct

labour, and both variable and fixed manufacturing overhead.

Particulars

Sales (3200*85)

Less: Variable expenses

Opening Stock ( 1200 units)

Production (3650 units * 30)

Less: Closing Stock (1650 units *30)

Total variable expenses

Contribution

Less: All Fixed Expenses

Fixed Indirect manufacturing cost

Distribution Expenses

Administrative Expenses

Net loss before interest and taxes

Less: Interest expenses

Net Loss before tax

Add: Tax @ 19%

Net loss

Net Profit or loss reported under Absorption and Marginal Costing

Particulars Year 1 Year 2 Year 3

Absorption Costing -31948.71 -6564.65 -27190.16

Marginal Costing -51111.00 -10935.00 -23490.00

Comment and interpretation of above results

Absorption Costing: Absorption costing means that all the manufacturing costs are consumed

only to the product produced. In the cost of finished goods includes cost of direct material, direct

labour, and both variable and fixed manufacturing overhead.

10

Marginal Costing: In the marginal costing approach only variable cost are charged to the unit of

cost and all the fixed cost is written off against the contribution.

The main difference between the marginal and absorption costing is that fixed

manufacturing cost is included in the product cost in case in absorption costing while in case of

marginal costing all the fixed costs are charged to the contribution.

Comments: The above results a show that overall loss reported under the absorption costing

approach is less that the overall loss reported under the marginal costing approach. It is because

in absorption costing only those fixed manufacturing cost is charged to the cost of production

that is actually consumed by the unit sold while in case of marginal costing all the fixed

production cost are charged to the contribution and it is not based on number of units sold or

produced. In marginal costing fixed cost are charged on the basis of the period not on the basis of

the actual unit sold (Bromwich and Bhimani, 2005).

Task 2: Report

Part A and B:

Budget is refers to the financial tool that is used for preparing the projected financial

statements and also to make decisions. Budgets uses the past results and variances to prepare the

financial statements for future period. The main motive to prepare the budgets is to help the

management for making the future planning and to measure the future performance of the

company. It helps to evaluate the performance of the individual as it is compare the actual

performance with the budgeted performance of the individual. So in short it can be said that it is

used to make decision regarding the expenditures that has to be occurred for the fixed expenses,

Marginal Costing: In the marginal costing approach only variable cost are charged to the unit of

cost and all the fixed cost is written off against the contribution.

The main difference between the marginal and absorption costing is that fixed

manufacturing cost is included in the product cost in case in absorption costing while in case of

marginal costing all the fixed costs are charged to the contribution.

Comments: The above results a show that overall loss reported under the absorption costing

approach is less that the overall loss reported under the marginal costing approach. It is because

in absorption costing only those fixed manufacturing cost is charged to the cost of production

that is actually consumed by the unit sold while in case of marginal costing all the fixed

production cost are charged to the contribution and it is not based on number of units sold or

produced. In marginal costing fixed cost are charged on the basis of the period not on the basis of

the actual unit sold (Bromwich and Bhimani, 2005).

Task 2: Report

Part A and B:

Budget is refers to the financial tool that is used for preparing the projected financial

statements and also to make decisions. Budgets uses the past results and variances to prepare the

financial statements for future period. The main motive to prepare the budgets is to help the

management for making the future planning and to measure the future performance of the

company. It helps to evaluate the performance of the individual as it is compare the actual

performance with the budgeted performance of the individual. So in short it can be said that it is

used to make decision regarding the expenditures that has to be occurred for the fixed expenses,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

cash flow management, expansion plans and many other important managerial decisions (Lalli,

2011). Various planning tools are used to create the budgets such as ratio analysis, variance

analysis, and benchmarking. All these planning tools provide the base for preparing the budgets.

Planning tools uses historical data to make the analysis and provides information that is needed

to prepare the budgets. The important budgets that are produced using the past information are

sales budget, purchase budget, cash flow budget, budgeted income statement, budgeted balance

sheet and other flexible budgets (Davies and Crawford, 2011).

Budgets also include various process that need to be undertake in order to help the

managers to take managerial decisions. The preparation of budget involves proper use of proper

planning tools and use of budgetary controls methods. Budget can also be defined as the process

for statements of different management information is prepared for the future period and actual

results are compared with past results in order to find the variances. The variance helps the

management to make corrective actions for the future period and improve the financial and

performance (Malina, 2017).

Use of different planning tools use budgetary tools with advantages and disadvantages of

each planning tools

Use and Advantages & Disadvantages of Budgets

Budget is the most important planning tool that is used for the budgetary control

decisions. It is defined as the financial tool that helps the management in gaining an estimate of

the future financial performance. Budget performance is based on the past results that have been

derived using the trend analysis of the financial statements. Budgeted financial statement are

cash flow management, expansion plans and many other important managerial decisions (Lalli,

2011). Various planning tools are used to create the budgets such as ratio analysis, variance

analysis, and benchmarking. All these planning tools provide the base for preparing the budgets.

Planning tools uses historical data to make the analysis and provides information that is needed

to prepare the budgets. The important budgets that are produced using the past information are

sales budget, purchase budget, cash flow budget, budgeted income statement, budgeted balance

sheet and other flexible budgets (Davies and Crawford, 2011).

Budgets also include various process that need to be undertake in order to help the

managers to take managerial decisions. The preparation of budget involves proper use of proper

planning tools and use of budgetary controls methods. Budget can also be defined as the process

for statements of different management information is prepared for the future period and actual

results are compared with past results in order to find the variances. The variance helps the

management to make corrective actions for the future period and improve the financial and

performance (Malina, 2017).

Use of different planning tools use budgetary tools with advantages and disadvantages of

each planning tools

Use and Advantages & Disadvantages of Budgets

Budget is the most important planning tool that is used for the budgetary control

decisions. It is defined as the financial tool that helps the management in gaining an estimate of

the future financial performance. Budget performance is based on the past results that have been

derived using the trend analysis of the financial statements. Budgeted financial statement are

12

made using the financial statements of the company, while other financial budgets such cash

budget, sales budget, purchase and raw material purchase budget are prepared using the sales

growth rate, management expectation of closing inventory and other financial decisions for the

future period. Sales of the company can be estimated using various methods and using the sales

units for the future it is easy to estimate the budget performance of the company in future years

(Lumby and Jones, 2007).

The most important advantage of using the budget as the planning tool for the budgetary

controls is that it helps in controlling the overall cost and also helps the management for profit

maximization. It helps to define the business plans, objectives, policies for the future year based

on past performance of the company. It can be said that budget provides accurate information for

the future period as it based on the past results and use of estimation methods. It helps to prepare

to prepare the future activities and provide the performance standards for the entire managerial

person in the organization (Malina, 2017). Using the budget it is easy to allocate the specific

targets and goals for each business department and it is most important part of the budgetary

control process. So it can be said that process of budget helps in effective management of

different business activities and allow the proper coordination of between the various business

departments. The actual results of the business department have been compared with the

budgeted results and any unfavorable items are being sorted in order to know the possible cause

for the same. So it is easy for the managers for to identify the issues in each business department

and to develop the effective strategies to overcome the particular issue. Management can

determine the responsibilities and duties of managerial persons on the basis of budgetary targets

and objectives. In short it can be said that overall reduction in the production cost through using

made using the financial statements of the company, while other financial budgets such cash

budget, sales budget, purchase and raw material purchase budget are prepared using the sales

growth rate, management expectation of closing inventory and other financial decisions for the

future period. Sales of the company can be estimated using various methods and using the sales

units for the future it is easy to estimate the budget performance of the company in future years

(Lumby and Jones, 2007).

The most important advantage of using the budget as the planning tool for the budgetary

controls is that it helps in controlling the overall cost and also helps the management for profit

maximization. It helps to define the business plans, objectives, policies for the future year based

on past performance of the company. It can be said that budget provides accurate information for

the future period as it based on the past results and use of estimation methods. It helps to prepare

to prepare the future activities and provide the performance standards for the entire managerial

person in the organization (Malina, 2017). Using the budget it is easy to allocate the specific

targets and goals for each business department and it is most important part of the budgetary

control process. So it can be said that process of budget helps in effective management of

different business activities and allow the proper coordination of between the various business

departments. The actual results of the business department have been compared with the

budgeted results and any unfavorable items are being sorted in order to know the possible cause

for the same. So it is easy for the managers for to identify the issues in each business department

and to develop the effective strategies to overcome the particular issue. Management can

determine the responsibilities and duties of managerial persons on the basis of budgetary targets

and objectives. In short it can be said that overall reduction in the production cost through using

13

the proper budgetary control techniques helps the management to improve the overall economic

performance and efficiency of the company (Moles and Kidwekk, 2011).

Every budgetary control process has some drawbacks and it limits the use of planning

tools in the management process. Budgets are based on the past performance and future results

are estimated using the past trends but it is certain that future estimation can be fluctuated due to

inflation rate. So it can be said that budgets that are prepared using the past performance can

have some deviations and can provide unrealistic outcome only in few cases. Budgets are also

prepared using the help of top management, so it can be said that if top manager fails to provide

the help to the top management that there will problems in making the budgets (Rasmussen,

2003).

Use and Advantages & Disadvantages of Variances

The method of variance analysis is used for identifying the deviations in performance by

comparing the actual results with the budgeted results. This helps in development of strategies to

overcome the differences and taking corrective actions for future development and growth. It

helps in identification of the material variances, overhead variances and labor variances. Thus,

the accurate determination of the problem areas with the help of technique of variance analysis

enables the managers to plan and take actions to overcome the issues identified. The main aim of

the use of technique by accountants is to minimize the deviation in budgeted results and

achieving the long-term goal and objectives of the company (Warren, 2016).

The main advantage of variance analysis is that it assists the business managers in

performance measurement. The overall performance analyses will help the management in

gaining an understating of the root cause of the problems and then developing solutions so that

the proper budgetary control techniques helps the management to improve the overall economic

performance and efficiency of the company (Moles and Kidwekk, 2011).

Every budgetary control process has some drawbacks and it limits the use of planning

tools in the management process. Budgets are based on the past performance and future results

are estimated using the past trends but it is certain that future estimation can be fluctuated due to

inflation rate. So it can be said that budgets that are prepared using the past performance can

have some deviations and can provide unrealistic outcome only in few cases. Budgets are also

prepared using the help of top management, so it can be said that if top manager fails to provide

the help to the top management that there will problems in making the budgets (Rasmussen,

2003).

Use and Advantages & Disadvantages of Variances

The method of variance analysis is used for identifying the deviations in performance by

comparing the actual results with the budgeted results. This helps in development of strategies to

overcome the differences and taking corrective actions for future development and growth. It

helps in identification of the material variances, overhead variances and labor variances. Thus,

the accurate determination of the problem areas with the help of technique of variance analysis

enables the managers to plan and take actions to overcome the issues identified. The main aim of

the use of technique by accountants is to minimize the deviation in budgeted results and

achieving the long-term goal and objectives of the company (Warren, 2016).

The main advantage of variance analysis is that it assists the business managers in

performance measurement. The overall performance analyses will help the management in

gaining an understating of the root cause of the problems and then developing solutions so that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

the problematic areas can be completely removed. The analysis also helps in assigning the

responsibility to managers for improving the performance of the company to maximize the

operational efficiency. Also, it assists the manager in taking quantitative investigation of the

deviations in performance rather than only providing a theoretical estimation. Thus, the

quantitative investigation provides a more accurate estimation of the problematic areas which

help the manager in developing effective control measures for their resolution (Weygandt, 2015).

There are many disadvantages along with the numerous advantages that limits the use of

variance analysis in the applying the budgetary control techniques. Variance analysis is done for

two or more period and there is some time gap in each of period. So it can be said that variances

does not provide useful information because it does not consider the time vale of money concept

which is very important for making the managerial decisions. So it is important to pay attention

to various factors that can impact the overall results of the variances. Factors can be change in

material price, government regulations, technology changes and change in market conditions. So

it is important to incorporate all the external factors while applying the variance analysis method

in the budgetary control (Soyka, 2012).

Analysis of Adoption of Management Accounting Systems by Organizations in Responding

to Financial Problems

Management accounting can be regarded as the process of developing management

reports to extract accurate and timely financial and statistical information for decision-making.

The management reports prepared leads to analysis and interpreting of the relevant information

to enable an organization to achieve its goals and objectives. The field of management

accounting has considerably evolved over the past few years and has traditionally being changed

the problematic areas can be completely removed. The analysis also helps in assigning the

responsibility to managers for improving the performance of the company to maximize the

operational efficiency. Also, it assists the manager in taking quantitative investigation of the

deviations in performance rather than only providing a theoretical estimation. Thus, the

quantitative investigation provides a more accurate estimation of the problematic areas which

help the manager in developing effective control measures for their resolution (Weygandt, 2015).

There are many disadvantages along with the numerous advantages that limits the use of

variance analysis in the applying the budgetary control techniques. Variance analysis is done for

two or more period and there is some time gap in each of period. So it can be said that variances

does not provide useful information because it does not consider the time vale of money concept

which is very important for making the managerial decisions. So it is important to pay attention

to various factors that can impact the overall results of the variances. Factors can be change in

material price, government regulations, technology changes and change in market conditions. So

it is important to incorporate all the external factors while applying the variance analysis method

in the budgetary control (Soyka, 2012).

Analysis of Adoption of Management Accounting Systems by Organizations in Responding

to Financial Problems

Management accounting can be regarded as the process of developing management

reports to extract accurate and timely financial and statistical information for decision-making.

The management reports prepared leads to analysis and interpreting of the relevant information

to enable an organization to achieve its goals and objectives. The field of management

accounting has considerably evolved over the past few years and has traditionally being changed

15

from cost identification to facilitate decision-making. The considerable evolution of management

accounting over the past can be discussed as follows:

Prior to 1950: The major focus of management accounting before 1950’s was only

determination of cost and financial control. The management prepares financial reports

only for identification of costs involved in carrying out different business activities. This

facilitates the managers in achieving financial control through taking significant measures

for cost reduction and development of budgets. The business managers do not adopt the

use of management reports in strategy planning and execution. It was only used for

gaining an overview of the internal processes and cost accounting practices.

1950’s to 1970’s: The role of management accounting has been significantly changed

during this stage and involves extracting information for planning and controlling of

internal processes. The management activities during the period involves the use of

management controls in optimizing the production processes and seek to develop

effective ways for managing the resources to achieve the organizational objectives and

goals. Therefore, the role of management accounting has shifted from only cost allocating

to using the information for improving the operational efficiency during this phase. For

example, Nokia adopted the use of cost accounting for estimating the direct and indirect

cost involved in its operational functions. The company integrates the use of account

analysis method to classify various cost accounts as variable, fixed or mixed as per the

individual level of activity (Weygandt et al., 2015).

1970’s to 1990’s: The stages involve the use of information for managerial planning and

control by the use of information technologies and devices. This is largely been due to

increase in competition and technological development that has assisted the management

from cost identification to facilitate decision-making. The considerable evolution of management

accounting over the past can be discussed as follows:

Prior to 1950: The major focus of management accounting before 1950’s was only

determination of cost and financial control. The management prepares financial reports

only for identification of costs involved in carrying out different business activities. This

facilitates the managers in achieving financial control through taking significant measures

for cost reduction and development of budgets. The business managers do not adopt the

use of management reports in strategy planning and execution. It was only used for

gaining an overview of the internal processes and cost accounting practices.

1950’s to 1970’s: The role of management accounting has been significantly changed

during this stage and involves extracting information for planning and controlling of

internal processes. The management activities during the period involves the use of

management controls in optimizing the production processes and seek to develop

effective ways for managing the resources to achieve the organizational objectives and

goals. Therefore, the role of management accounting has shifted from only cost allocating

to using the information for improving the operational efficiency during this phase. For

example, Nokia adopted the use of cost accounting for estimating the direct and indirect

cost involved in its operational functions. The company integrates the use of account

analysis method to classify various cost accounts as variable, fixed or mixed as per the

individual level of activity (Weygandt et al., 2015).

1970’s to 1990’s: The stages involve the use of information for managerial planning and

control by the use of information technologies and devices. This is largely been due to

increase in competition and technological development that has assisted the management

16

in developing strategies for reduction of cost and reduction of waste to increase profit.

The management reports adopted the use of accounting techniques such as Activity based

costing for allocation of costs to each department activities and maximizing the

operational efficiency. For example, H&M adopts the use of activity based costing to

allocate cost as per the department activities and therefore accurate pricing of its products

and services (Warren et al., 2016).

1990’s onwards: This period has resulted in causing major changes in the management

accounting functions within organizations. The stage involves adoption of information

from the management reports to create value by better management of resources. The

information is used for strategic planning and decision-taking by the organizations. The

management reports involve the use of financial information for forecasting the future

growth potential in order to take strategic decisions regarding the investment in

equipment and other strategies adopted for promoting its financial growth. It aids the

management in taking decisions reading the procuring of materials either from outside or

manufacturing in-house (Warren, Reeve and Duchac, 2011). The insights developed by

the management personnel’s assists in taking effective decisions for maximizing the

operational effectiveness. It aids in budget planning and development by estimating the

future cash flows and as such assist the managers in allocating financial resources for

generating more revenue and promoting the growth of the company. Therefore, the role

of management accounting has shifted from only taking decisions regarding allocation of

resources to that becoming a strategic business partner. Thus, the changing role of

management accounting over the past few years has caused larger changes in financial

in developing strategies for reduction of cost and reduction of waste to increase profit.

The management reports adopted the use of accounting techniques such as Activity based

costing for allocation of costs to each department activities and maximizing the

operational efficiency. For example, H&M adopts the use of activity based costing to

allocate cost as per the department activities and therefore accurate pricing of its products

and services (Warren et al., 2016).

1990’s onwards: This period has resulted in causing major changes in the management

accounting functions within organizations. The stage involves adoption of information

from the management reports to create value by better management of resources. The

information is used for strategic planning and decision-taking by the organizations. The

management reports involve the use of financial information for forecasting the future

growth potential in order to take strategic decisions regarding the investment in

equipment and other strategies adopted for promoting its financial growth. It aids the

management in taking decisions reading the procuring of materials either from outside or

manufacturing in-house (Warren, Reeve and Duchac, 2011). The insights developed by

the management personnel’s assists in taking effective decisions for maximizing the

operational effectiveness. It aids in budget planning and development by estimating the

future cash flows and as such assist the managers in allocating financial resources for

generating more revenue and promoting the growth of the company. Therefore, the role

of management accounting has shifted from only taking decisions regarding allocation of

resources to that becoming a strategic business partner. Thus, the changing role of

management accounting over the past few years has caused larger changes in financial

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

reporting and development of effective cost management system to enable an

organization to attain competitive advantage (Moles and Kidwekk, 2011).

Use of Management accounting for leading Organizations to Sustainable Success

Business managers are adopting the use of information gained from the management

reports to promote sustainable growth and development of business entities. This is because the

financial and statistical information gained from the management reports will help in

identification of a financial risk in advance. The identification of a financial problem by the

development of budgets will helps the company to plan appropriate strategies for overcoming the

problem identified. Also, the analysis of the overall internal processes of a company with the

help of management report developed will lead to identification of Key Performance Indicators

(KPIS’s) to support its long-term business goals and objectives. The management on identifying

its KPIs’ can develop sustainable strategies incorporating the use to promote its growth and

development (Malina, 2017).

For example, IKEA have improved the competency of its value chain with the use of

management accounting systems. It adopted the use of two planning control systems that are,

budgets and business plans. The information extracted from the reports developed by the

management accountants is shared equally at all level. The management at higher level provides

guidance to lower level management team about the key focus area to improve the operational

efficiency. This can be price reduction, decrease in the waiting time or improving the production

processes.. The selection of the key problematic area is followed by determining target figure to

be achieved by the use of a management accounting system. This is followed by developing a

business plan for achieving the determine target and developing action plans for achieving them.

reporting and development of effective cost management system to enable an

organization to attain competitive advantage (Moles and Kidwekk, 2011).

Use of Management accounting for leading Organizations to Sustainable Success

Business managers are adopting the use of information gained from the management

reports to promote sustainable growth and development of business entities. This is because the

financial and statistical information gained from the management reports will help in

identification of a financial risk in advance. The identification of a financial problem by the

development of budgets will helps the company to plan appropriate strategies for overcoming the

problem identified. Also, the analysis of the overall internal processes of a company with the

help of management report developed will lead to identification of Key Performance Indicators

(KPIS’s) to support its long-term business goals and objectives. The management on identifying

its KPIs’ can develop sustainable strategies incorporating the use to promote its growth and

development (Malina, 2017).

For example, IKEA have improved the competency of its value chain with the use of

management accounting systems. It adopted the use of two planning control systems that are,

budgets and business plans. The information extracted from the reports developed by the

management accountants is shared equally at all level. The management at higher level provides

guidance to lower level management team about the key focus area to improve the operational

efficiency. This can be price reduction, decrease in the waiting time or improving the production

processes.. The selection of the key problematic area is followed by determining target figure to

be achieved by the use of a management accounting system. This is followed by developing a

business plan for achieving the determine target and developing action plans for achieving them.

18

The information provided by the management accounting reports is used to make forecast about

budgeted sales and them comparing it with actual sale figure to identify the deviations and taking

suitable actions for overcoming them. The reports are also used by stores manager to compare

the sale figures with the last year figures and budget figures to determine the percentage increase

or decrease in the financial growth. Therefore, it can be said that IKEA is using management

accounting system to identify its KPI’s that leads to its sustainable growth and success (Adler,

2013).

The identification of the operational and financial risk that a company can face I the

future context will enable in developing a risk management framework for mitigation of the

respective risks. The risk management framework will define the roles and responsibilities of

different management personnel in identifying, measuring and controlling the risks. The action

plan can be developed in advance against each of the identified risk so that it can be mitigated

properly. It also assists in developing an effective financial governance system to meet the

financial goals and objectives of the company. The presence of a financial governance system is

essential to prevent the occurrence of any fraudulent activities impacting the achievement of

financial goals of the company. The management reports will lead to easy identification of the

loopholes and also any unethical practice and procedures in advance by the company (Lumby

and Jones, 2007).

This will help in its early mitigation so that stakeholders are provided with only reliable

and accurate information. The error in the financial reporting process will also be identified

accurately by development of management reports. This assists the financial accountants to

disclose the information to the external stakeholders that is neutral, error-free and complete in all

aspects. The estimation of the costs involved in operational activities assist the management in

The information provided by the management accounting reports is used to make forecast about

budgeted sales and them comparing it with actual sale figure to identify the deviations and taking

suitable actions for overcoming them. The reports are also used by stores manager to compare

the sale figures with the last year figures and budget figures to determine the percentage increase

or decrease in the financial growth. Therefore, it can be said that IKEA is using management

accounting system to identify its KPI’s that leads to its sustainable growth and success (Adler,

2013).

The identification of the operational and financial risk that a company can face I the

future context will enable in developing a risk management framework for mitigation of the

respective risks. The risk management framework will define the roles and responsibilities of

different management personnel in identifying, measuring and controlling the risks. The action

plan can be developed in advance against each of the identified risk so that it can be mitigated

properly. It also assists in developing an effective financial governance system to meet the

financial goals and objectives of the company. The presence of a financial governance system is

essential to prevent the occurrence of any fraudulent activities impacting the achievement of

financial goals of the company. The management reports will lead to easy identification of the

loopholes and also any unethical practice and procedures in advance by the company (Lumby

and Jones, 2007).

This will help in its early mitigation so that stakeholders are provided with only reliable

and accurate information. The error in the financial reporting process will also be identified

accurately by development of management reports. This assists the financial accountants to

disclose the information to the external stakeholders that is neutral, error-free and complete in all

aspects. The estimation of the costs involved in operational activities assist the management in

19

taking accurate decisions reading the pricing of products and better inventory planning. The

identification of the wasteful activities will help in reducing the inventory costs and thus

improving the operational efficiency. This will enable the company to price its products at lower

price and achieve customer satisfaction that will promote its long-term growth and development

(Lalli, 2011). For example, Wal-Mart adopt the use of inventory forecasting for taking future

business decisions by estimating the amount of inventory required and therefore helpful in cost

assessment.

Use of accounting planning tools to respond appropriately to solving financial problems of

organizations for sustainable success

The different tools of accounting are used effectively by the management for resolving

the financial problems and promoting its sustainable success and growth as follows:

Budgetary Control: This is the most important and significant tool of management

accounting used planning and control of financial resources. The budgets are developed

with the use of past accounting data by keeping into account the future expectations of

growth and development of the company. The budgeted data is compared with actual data

in order to identify the deviation in the performance and planning strategies to overcome

the deviation.

Decision Accounting: Decision-making is also one of the most important tools of

management accounting. The development of financial reports assist the managers in

taking decision about the activities that need to be undertaken and that need to be

eliminated. The development of alternatives for improving the operational efficiency

helps in selection of the best possible methods to improve the productivity and

taking accurate decisions reading the pricing of products and better inventory planning. The

identification of the wasteful activities will help in reducing the inventory costs and thus

improving the operational efficiency. This will enable the company to price its products at lower

price and achieve customer satisfaction that will promote its long-term growth and development

(Lalli, 2011). For example, Wal-Mart adopt the use of inventory forecasting for taking future

business decisions by estimating the amount of inventory required and therefore helpful in cost

assessment.

Use of accounting planning tools to respond appropriately to solving financial problems of

organizations for sustainable success

The different tools of accounting are used effectively by the management for resolving

the financial problems and promoting its sustainable success and growth as follows:

Budgetary Control: This is the most important and significant tool of management

accounting used planning and control of financial resources. The budgets are developed

with the use of past accounting data by keeping into account the future expectations of

growth and development of the company. The budgeted data is compared with actual data

in order to identify the deviation in the performance and planning strategies to overcome

the deviation.

Decision Accounting: Decision-making is also one of the most important tools of

management accounting. The development of financial reports assist the managers in

taking decision about the activities that need to be undertaken and that need to be

eliminated. The development of alternatives for improving the operational efficiency

helps in selection of the best possible methods to improve the productivity and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

profitability of the organization. It also assists in accurately determining the product

prices by taking into account the overall operational costs (McWatters and Zimmerman,

2015).

Management Information system: MIS is an integrated tool used by the management in

order to record and stores the information accurately for use by the management. MIS

tools and device scan be sued by the management in collection, storing and retrieving the

information accurately so that it can be extracted easily at the time of its use (Davies and

Crawford, 2011). For example, Starbucks adopts the use of management information

system for maintaining communication flow across its different department in order to

take effective decisions. The company has developed a web portal that disseminates the

management accounting information to the people working in the organization. The tool

serves the function of providing different type of information to varying departments as

per their needs and requirements. This facilitates the department manager to plan the

consecutive strategies for driving its growth and development. The use of MIS enables

the management to gain timely information for strategic planning to promote the business

growth and development. The improved communication flow across different business

departments has improved its productivity. This has enhanced the supply chain capability

of the company and therefore optimizing the time involved in carrying out different

supply chain activities. It has having large number of stores and therefore the use of MIS

systems enables it to achieve success by effectively disseminating the information across

various departments. Therefore, it can be said that the use of accounting tool has largely

enabled Starbucks to resolve various financial problems (Marco, Te'eni, Albano and Za.,

2012).

profitability of the organization. It also assists in accurately determining the product

prices by taking into account the overall operational costs (McWatters and Zimmerman,

2015).

Management Information system: MIS is an integrated tool used by the management in

order to record and stores the information accurately for use by the management. MIS

tools and device scan be sued by the management in collection, storing and retrieving the

information accurately so that it can be extracted easily at the time of its use (Davies and

Crawford, 2011). For example, Starbucks adopts the use of management information

system for maintaining communication flow across its different department in order to

take effective decisions. The company has developed a web portal that disseminates the

management accounting information to the people working in the organization. The tool

serves the function of providing different type of information to varying departments as

per their needs and requirements. This facilitates the department manager to plan the

consecutive strategies for driving its growth and development. The use of MIS enables

the management to gain timely information for strategic planning to promote the business

growth and development. The improved communication flow across different business

departments has improved its productivity. This has enhanced the supply chain capability

of the company and therefore optimizing the time involved in carrying out different

supply chain activities. It has having large number of stores and therefore the use of MIS

systems enables it to achieve success by effectively disseminating the information across

various departments. Therefore, it can be said that the use of accounting tool has largely

enabled Starbucks to resolve various financial problems (Marco, Te'eni, Albano and Za.,

2012).

21

Capital Structuring: It is management accounting tool used by the business managers to

develop an appropriate capital structure consisting of balanced proportion of debt and

equity. This is possible by the use of management reports that provides a complete

overview regarding the financial resources and constraints possessed by the organization.

Thus, the business managers can accurately take the decision whether to incorporate the

use of equity of leverage financing for promoting the future growth and development of

the company. It also provides an analysis of the working capital management of the

company. Thus, it helps in determining the ability of a firm to effectively use is resource

to convert into cash to meet its financial obligations. Thus, the managers can plan of

strengthening its current asset base for meeting the liabilities in case the current assets are

comparatively less in amount to meet the financial obligations as they become due

(Bromwich and Bhimani, 2005) .

Variance Analysis: It is also regarded to be the most important tool of management

accounting for identifying and overcoming the deviations in the actual behavior as

compared o the forecasted behavior. This consists of two stages, that is, calculating ad

recording individual variances and gaining an adequate understanding of the cause of

each variance. The reasons for variances can be due to material deviations, labor changes

or overhead fluctuations. The material differences can be due to difference in the quantity

consumed and that allocated for production whereas labor variances can be due to

fluctuations in the actual wage paid to the workers and the standard wage specified.

Lastly, the overhead variances can be due to difference between standard overhead costs

budgeted in comparison to that incurred (Wickramasinghe and Alawattage, 2007).

Capital Structuring: It is management accounting tool used by the business managers to

develop an appropriate capital structure consisting of balanced proportion of debt and

equity. This is possible by the use of management reports that provides a complete

overview regarding the financial resources and constraints possessed by the organization.

Thus, the business managers can accurately take the decision whether to incorporate the

use of equity of leverage financing for promoting the future growth and development of

the company. It also provides an analysis of the working capital management of the

company. Thus, it helps in determining the ability of a firm to effectively use is resource

to convert into cash to meet its financial obligations. Thus, the managers can plan of

strengthening its current asset base for meeting the liabilities in case the current assets are

comparatively less in amount to meet the financial obligations as they become due

(Bromwich and Bhimani, 2005) .

Variance Analysis: It is also regarded to be the most important tool of management

accounting for identifying and overcoming the deviations in the actual behavior as

compared o the forecasted behavior. This consists of two stages, that is, calculating ad

recording individual variances and gaining an adequate understanding of the cause of

each variance. The reasons for variances can be due to material deviations, labor changes

or overhead fluctuations. The material differences can be due to difference in the quantity

consumed and that allocated for production whereas labor variances can be due to

fluctuations in the actual wage paid to the workers and the standard wage specified.

Lastly, the overhead variances can be due to difference between standard overhead costs

budgeted in comparison to that incurred (Wickramasinghe and Alawattage, 2007).

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23

References

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Lalli, W. 2011. Handbook of Budgeting. John Wiley & Sons.

Lumby,S and Jones,C. 2007. Corporate finance theory & practice. Thomson.

Malina, M. 2017. Advances in Management Accounting. Emerald Group Publishing.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Rasmussen, N. et al. 2003. Process Improvement for Effective Budgeting and Financial

Reporting. John Wiley & Sons.

Soyka, P. et al. 2012. Building Sustainability Into Your Organization (Collection). FT Press.

Warren, C. et al. 2016. Financial & Managerial Accounting. Cengage Learning.

Weygandt, J. et al. 2015. Financial & Managerial Accounting. John Wiley & Sons.

Wickramasinghe, D. and Alawattage, C. 2007. Management accounting change: approaches

and perspectives. London and New York: Routledge. Taylor & Francis Group.

Adler, R. 2013. Management Accounting. Routledge.

References

Bromwich, M. and Bhimani, A., 2005. Management accounting: Pathways to progress. Cima

publishing.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Lalli, W. 2011. Handbook of Budgeting. John Wiley & Sons.

Lumby,S and Jones,C. 2007. Corporate finance theory & practice. Thomson.

Malina, M. 2017. Advances in Management Accounting. Emerald Group Publishing.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Rasmussen, N. et al. 2003. Process Improvement for Effective Budgeting and Financial

Reporting. John Wiley & Sons.

Soyka, P. et al. 2012. Building Sustainability Into Your Organization (Collection). FT Press.

Warren, C. et al. 2016. Financial & Managerial Accounting. Cengage Learning.

Weygandt, J. et al. 2015. Financial & Managerial Accounting. John Wiley & Sons.

Wickramasinghe, D. and Alawattage, C. 2007. Management accounting change: approaches

and perspectives. London and New York: Routledge. Taylor & Francis Group.

Adler, R. 2013. Management Accounting. Routledge.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.