UNIT 5 Management Accounting Systems Sample Assignment

VerifiedAdded on 2021/02/20

|20

|5248

|32

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

UNIT 5 - MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................2

LO1..................................................................................................................................................2

P1 Management accounting and the essential requirements of different types of management

accounting systems......................................................................................................................2

P2 different methods used for management accounting reporting..............................................5

LO 2.................................................................................................................................................7

P3 preparation of income statements by using marginal cost and absorption cost......................7

LO 3...............................................................................................................................................11

P4 advantages and limitation of planning tools which are used for the budgetary control.......11

LO4................................................................................................................................................15

P5 Compare ways in which organisations are adapting management accounting systems to

respond to financial problems. ..................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

1

INTRODUCTION...........................................................................................................................2

LO1..................................................................................................................................................2

P1 Management accounting and the essential requirements of different types of management

accounting systems......................................................................................................................2

P2 different methods used for management accounting reporting..............................................5

LO 2.................................................................................................................................................7

P3 preparation of income statements by using marginal cost and absorption cost......................7

LO 3...............................................................................................................................................11

P4 advantages and limitation of planning tools which are used for the budgetary control.......11

LO4................................................................................................................................................15

P5 Compare ways in which organisations are adapting management accounting systems to

respond to financial problems. ..................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

1

INTRODUCTION

The process of Management accounting is providing an aid to internal management of an

organization in order to analyse the various financial statement to undertake necessary strategic

decisions for sustainability and growth of business (Peterson, Schmar - debeck, and Wilks,

2015). The management accounting is an effective process for presenting and analysing financial

information to the managers on interval for decision-making strategically. Super toughened glass

will be chosen for this report. The super toughened glass company is the best among the

construction industry, fire resistant, supply of shatter-proof and self-cleaning glass for the

building projects in UK. This company is a family firm and employs staff of 145 employees

working for their company.

The report will lay emphasis on management accounting and the essential requirements

of different types of system of management accounting. The report will also cover different

method for the management accounting. Along with it, the report will calculate the cost of

appropriate technique in order to analyse the cost and also income statement will be prepared for

further analysis of the company. The report will highlight the different types of planning tools

and their advantages and disadvantages for budgetary control. This report will lay study for a

brief comparison of organization for adapting management accounting system for responding in

financial problems.

LO1

P1 Management accounting and the essential requirements of different types of management

accounting systems

Management accounting

The management accounting is a process which provide aid to internal management of

organization in order to analyse financial statement for necessary decision-making for a long

period of sustainability in business (Abdel - Maksoud, Cheffi, and Ghoudi, 2016). This concept

of management accounting includes the planning in effective manner and to select the best

alternative action of an organization. Also, the control is executed by interpretation and

performance evaluation.

Financial accounting

The financial accounting is a specialized branch of accounting which tracks financial

transaction of a business (Davila, Foster, and Jia, 2015). The transactions in financial accounting

2

The process of Management accounting is providing an aid to internal management of an

organization in order to analyse the various financial statement to undertake necessary strategic

decisions for sustainability and growth of business (Peterson, Schmar - debeck, and Wilks,

2015). The management accounting is an effective process for presenting and analysing financial

information to the managers on interval for decision-making strategically. Super toughened glass

will be chosen for this report. The super toughened glass company is the best among the

construction industry, fire resistant, supply of shatter-proof and self-cleaning glass for the

building projects in UK. This company is a family firm and employs staff of 145 employees

working for their company.

The report will lay emphasis on management accounting and the essential requirements

of different types of system of management accounting. The report will also cover different

method for the management accounting. Along with it, the report will calculate the cost of

appropriate technique in order to analyse the cost and also income statement will be prepared for

further analysis of the company. The report will highlight the different types of planning tools

and their advantages and disadvantages for budgetary control. This report will lay study for a

brief comparison of organization for adapting management accounting system for responding in

financial problems.

LO1

P1 Management accounting and the essential requirements of different types of management

accounting systems

Management accounting

The management accounting is a process which provide aid to internal management of

organization in order to analyse financial statement for necessary decision-making for a long

period of sustainability in business (Abdel - Maksoud, Cheffi, and Ghoudi, 2016). This concept

of management accounting includes the planning in effective manner and to select the best

alternative action of an organization. Also, the control is executed by interpretation and

performance evaluation.

Financial accounting

The financial accounting is a specialized branch of accounting which tracks financial

transaction of a business (Davila, Foster, and Jia, 2015). The transactions in financial accounting

2

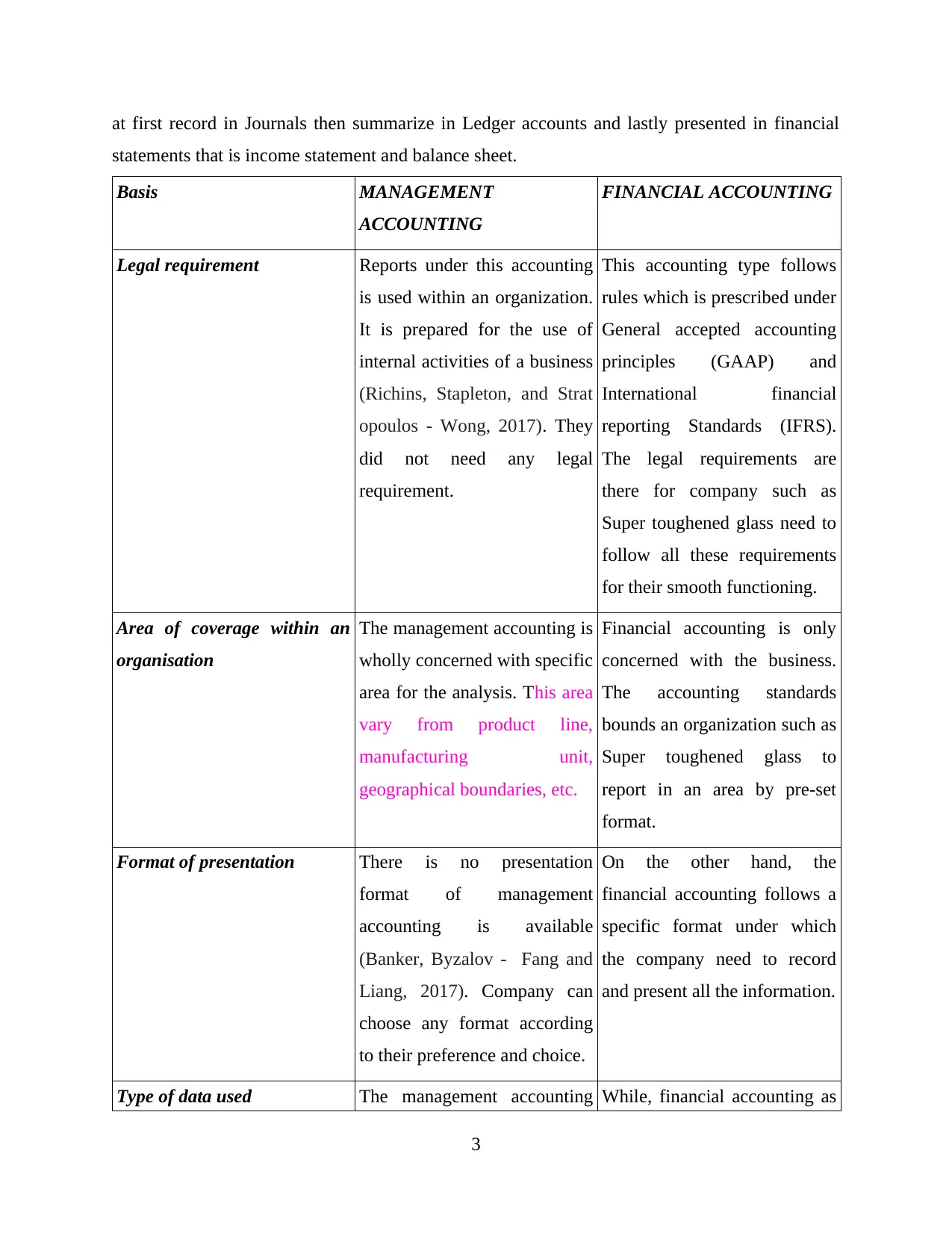

at first record in Journals then summarize in Ledger accounts and lastly presented in financial

statements that is income statement and balance sheet.

Basis MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Legal requirement Reports under this accounting

is used within an organization.

It is prepared for the use of

internal activities of a business

(Richins, Stapleton, and Strat

opoulos - Wong, 2017). They

did not need any legal

requirement.

This accounting type follows

rules which is prescribed under

General accepted accounting

principles (GAAP) and

International financial

reporting Standards (IFRS).

The legal requirements are

there for company such as

Super toughened glass need to

follow all these requirements

for their smooth functioning.

Area of coverage within an

organisation

The management accounting is

wholly concerned with specific

area for the analysis. This area

vary from product line,

manufacturing unit,

geographical boundaries, etc.

Financial accounting is only

concerned with the business.

The accounting standards

bounds an organization such as

Super toughened glass to

report in an area by pre-set

format.

Format of presentation There is no presentation

format of management

accounting is available

(Banker, Byzalov - Fang and

Liang, 2017). Company can

choose any format according

to their preference and choice.

On the other hand, the

financial accounting follows a

specific format under which

the company need to record

and present all the information.

Type of data used The management accounting While, financial accounting as

3

statements that is income statement and balance sheet.

Basis MANAGEMENT

ACCOUNTING

FINANCIAL ACCOUNTING

Legal requirement Reports under this accounting

is used within an organization.

It is prepared for the use of

internal activities of a business

(Richins, Stapleton, and Strat

opoulos - Wong, 2017). They

did not need any legal

requirement.

This accounting type follows

rules which is prescribed under

General accepted accounting

principles (GAAP) and

International financial

reporting Standards (IFRS).

The legal requirements are

there for company such as

Super toughened glass need to

follow all these requirements

for their smooth functioning.

Area of coverage within an

organisation

The management accounting is

wholly concerned with specific

area for the analysis. This area

vary from product line,

manufacturing unit,

geographical boundaries, etc.

Financial accounting is only

concerned with the business.

The accounting standards

bounds an organization such as

Super toughened glass to

report in an area by pre-set

format.

Format of presentation There is no presentation

format of management

accounting is available

(Banker, Byzalov - Fang and

Liang, 2017). Company can

choose any format according

to their preference and choice.

On the other hand, the

financial accounting follows a

specific format under which

the company need to record

and present all the information.

Type of data used The management accounting While, financial accounting as

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

uses both data that is

qualitative data and

quantitative data.

the name suggest uses only

quantitative data (Cassell,

Myers, and Seidel, 2015). The

company Super toughened

glass uses this accounting by

taking only quantitative data

into consideration.

Different types of management accounting systems are as follows :

Cost accounting system - This accounting system is used by various firms to estimate the

cost of product to analyse profitability, control and inventory valuation. The cost accounting

system work by tracking of raw material by passing through various stage of production and turn

into finish goods (Apostolou, Dorminey, and Hickey - Hassell, 2019). The accounting entry in

Super toughened glass company execute accounts when the raw material put into production. In

cost accounting, it is recorded immediately for the use of material by crediting account of raw

material and debit the account of goods in progress.

The direct cost is a type of cost which is related with production of good and services.

The distribution and labour cost are included as this is associated with products. On the other

hand, the production cost of material are used in direct expenses. The cost gets easily tracked by

project department (Peterson, Schmar - debeck, and Wilks, 2015). Also, derive value of

inventory is not allowed in International financial reporting standard (IFRS) and Generally

accepted accounting principles (GAAP). This did not provide view in which the cost is incurred

to create products and promoting activities of Super toughened glass.

The accounting standard is another cost which is occurred by evaluating difference

between budgeted and actual cost. The accounting executed a brief comparison between actual

expenditure of goods and estimating expenditure of goods used in production. The cost of goods

sold and ledger accounts contain standard one (Abdel - Maksoud, Cheffi, and Ghoudi, 2016).

The actual and estimated cost is identified by variance under the accounting standard cost which

uses the variance for generating outcomes.

Inventory management system – The system of inventory management tracks inventories

by supply chain or business portion in which they operate. The inventory management system

4

qualitative data and

quantitative data.

the name suggest uses only

quantitative data (Cassell,

Myers, and Seidel, 2015). The

company Super toughened

glass uses this accounting by

taking only quantitative data

into consideration.

Different types of management accounting systems are as follows :

Cost accounting system - This accounting system is used by various firms to estimate the

cost of product to analyse profitability, control and inventory valuation. The cost accounting

system work by tracking of raw material by passing through various stage of production and turn

into finish goods (Apostolou, Dorminey, and Hickey - Hassell, 2019). The accounting entry in

Super toughened glass company execute accounts when the raw material put into production. In

cost accounting, it is recorded immediately for the use of material by crediting account of raw

material and debit the account of goods in progress.

The direct cost is a type of cost which is related with production of good and services.

The distribution and labour cost are included as this is associated with products. On the other

hand, the production cost of material are used in direct expenses. The cost gets easily tracked by

project department (Peterson, Schmar - debeck, and Wilks, 2015). Also, derive value of

inventory is not allowed in International financial reporting standard (IFRS) and Generally

accepted accounting principles (GAAP). This did not provide view in which the cost is incurred

to create products and promoting activities of Super toughened glass.

The accounting standard is another cost which is occurred by evaluating difference

between budgeted and actual cost. The accounting executed a brief comparison between actual

expenditure of goods and estimating expenditure of goods used in production. The cost of goods

sold and ledger accounts contain standard one (Abdel - Maksoud, Cheffi, and Ghoudi, 2016).

The actual and estimated cost is identified by variance under the accounting standard cost which

uses the variance for generating outcomes.

Inventory management system – The system of inventory management tracks inventories

by supply chain or business portion in which they operate. The inventory management system

4

include shipping to warehousing, production to retail, etc. The inventory management includes

supervision of stock items and inventories.

The FIFO, LIFO and Weighted average are the different method of inventory

management. The First in first out (FIFO) is method of accounting which rely on cash flow

assumption in which cost of account of inventory is removed from the time it is purchased

(Davila, Foster, and Jia, 2015). The Last in first out method (LIFO) is utilization which is

matches with recent cost in income statement with the sales. While the Weighted average is

utilized under assignment of average cost of production. The inventory management assumes

selling all their inventories simultaneously.

Job costing systems – The job costing method involves process of accumulation of

information. This is associated with cost of production and service. There are three kinds of

information which is needed under this system (Richins, Stapleton, and Strat opoulos - Wong,

2017). They are direct material. Overhead and direct labour. The usefulness of this system is the

determination of accuracy in company's estimation system.

P2 different methods used for management accounting reporting.

The managerial reports are those report which provide aid to the internal users of the

company. This help enables effective decision-making in business. The reports generally

emphasizes on internal information that is received by financial accounting through auditors.

Also, this report is useful for effective planning, regulation, organizing, decision-making of the

company (Banker, Byzalov - Fang and Liang, 2017). This also helps in measuring performance

of internal staff of the business. This report is prepared under managerial accounting that is

focuses on providing information to all the internal users. The different types of managerial

report are prepared by businesses are as follows :

Budget reports - The budget reports are considered as very important report as it helps

the business in measuring performance and budgets of report which is generally prepared on

basis of different department to manage the operational activities and also the functions of

particular department effectively.

Budget report provides an aid to the organization in comparing actual performance with

projected. The corrective actions are taken in order to eliminate the deviation (Cassell, Myers,

and Seidel, 2015) . The income as well as expense are managed in according to budget. The

report informs internal users about inflow and outflow of cash and the performance deviations.

5

supervision of stock items and inventories.

The FIFO, LIFO and Weighted average are the different method of inventory

management. The First in first out (FIFO) is method of accounting which rely on cash flow

assumption in which cost of account of inventory is removed from the time it is purchased

(Davila, Foster, and Jia, 2015). The Last in first out method (LIFO) is utilization which is

matches with recent cost in income statement with the sales. While the Weighted average is

utilized under assignment of average cost of production. The inventory management assumes

selling all their inventories simultaneously.

Job costing systems – The job costing method involves process of accumulation of

information. This is associated with cost of production and service. There are three kinds of

information which is needed under this system (Richins, Stapleton, and Strat opoulos - Wong,

2017). They are direct material. Overhead and direct labour. The usefulness of this system is the

determination of accuracy in company's estimation system.

P2 different methods used for management accounting reporting.

The managerial reports are those report which provide aid to the internal users of the

company. This help enables effective decision-making in business. The reports generally

emphasizes on internal information that is received by financial accounting through auditors.

Also, this report is useful for effective planning, regulation, organizing, decision-making of the

company (Banker, Byzalov - Fang and Liang, 2017). This also helps in measuring performance

of internal staff of the business. This report is prepared under managerial accounting that is

focuses on providing information to all the internal users. The different types of managerial

report are prepared by businesses are as follows :

Budget reports - The budget reports are considered as very important report as it helps

the business in measuring performance and budgets of report which is generally prepared on

basis of different department to manage the operational activities and also the functions of

particular department effectively.

Budget report provides an aid to the organization in comparing actual performance with

projected. The corrective actions are taken in order to eliminate the deviation (Cassell, Myers,

and Seidel, 2015) . The income as well as expense are managed in according to budget. The

report informs internal users about inflow and outflow of cash and the performance deviations.

5

Advantages

The budget report is an effective tool to measure the performance.

Budget report provide help in taking corrective measures.

The budget report lead the organization and helps them in ascertaining the risk. It also helps investors in order to decide further investment based on the performance.

Account receivables Ageing reports - This report is made by company if there is any

involvement of extending to credit in their business. The amount in which the credit is given to

customer for specific time period. This helps the managers in identification of defaulters which

would not pay money and this also helps them in finding the issue in collection process

(Apostolou, Dorminey, and Hickey - Hassell, 2019). This report will help the businesses to

ascertain number of defaulters which they transfer to credit policies of the business. The

accounts receivable ageing report helps mangers for altering & changing their credit policies and

related strategies.

Advantages

This helps the managers of Super toughened glass in deciding the credit policies and also

restructuring of it.

The report leads an organization in ascertaining collection period of the Super toughened

glass (Peterson, Schmar - debeck, and Wilks, 2015). Also, the internal users make effective decisions in regarding extending the credit.

Performance Reports - The performance report is prepared for analysing and reviewing

performance of the business. The staff members take decisions regard to their appraisals and

other need of the organization. The different performance report is prepared under large

organization for each department to analyse their performance in the direction of the projected

performance and goal (Abdel - Maksoud, Cheffi, and Ghoudi, 2016). This will aid the

organization in executing right decision and taking different corrective measures for eliminating

difference between projected and actual performance.

Advantages

The performance reports helps in executing comparison between actual and budgeted

performance.

This also provide guidance for executing decision-making in the company regarding

promotion or termination of an employee.

6

The budget report is an effective tool to measure the performance.

Budget report provide help in taking corrective measures.

The budget report lead the organization and helps them in ascertaining the risk. It also helps investors in order to decide further investment based on the performance.

Account receivables Ageing reports - This report is made by company if there is any

involvement of extending to credit in their business. The amount in which the credit is given to

customer for specific time period. This helps the managers in identification of defaulters which

would not pay money and this also helps them in finding the issue in collection process

(Apostolou, Dorminey, and Hickey - Hassell, 2019). This report will help the businesses to

ascertain number of defaulters which they transfer to credit policies of the business. The

accounts receivable ageing report helps mangers for altering & changing their credit policies and

related strategies.

Advantages

This helps the managers of Super toughened glass in deciding the credit policies and also

restructuring of it.

The report leads an organization in ascertaining collection period of the Super toughened

glass (Peterson, Schmar - debeck, and Wilks, 2015). Also, the internal users make effective decisions in regarding extending the credit.

Performance Reports - The performance report is prepared for analysing and reviewing

performance of the business. The staff members take decisions regard to their appraisals and

other need of the organization. The different performance report is prepared under large

organization for each department to analyse their performance in the direction of the projected

performance and goal (Abdel - Maksoud, Cheffi, and Ghoudi, 2016). This will aid the

organization in executing right decision and taking different corrective measures for eliminating

difference between projected and actual performance.

Advantages

The performance reports helps in executing comparison between actual and budgeted

performance.

This also provide guidance for executing decision-making in the company regarding

promotion or termination of an employee.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

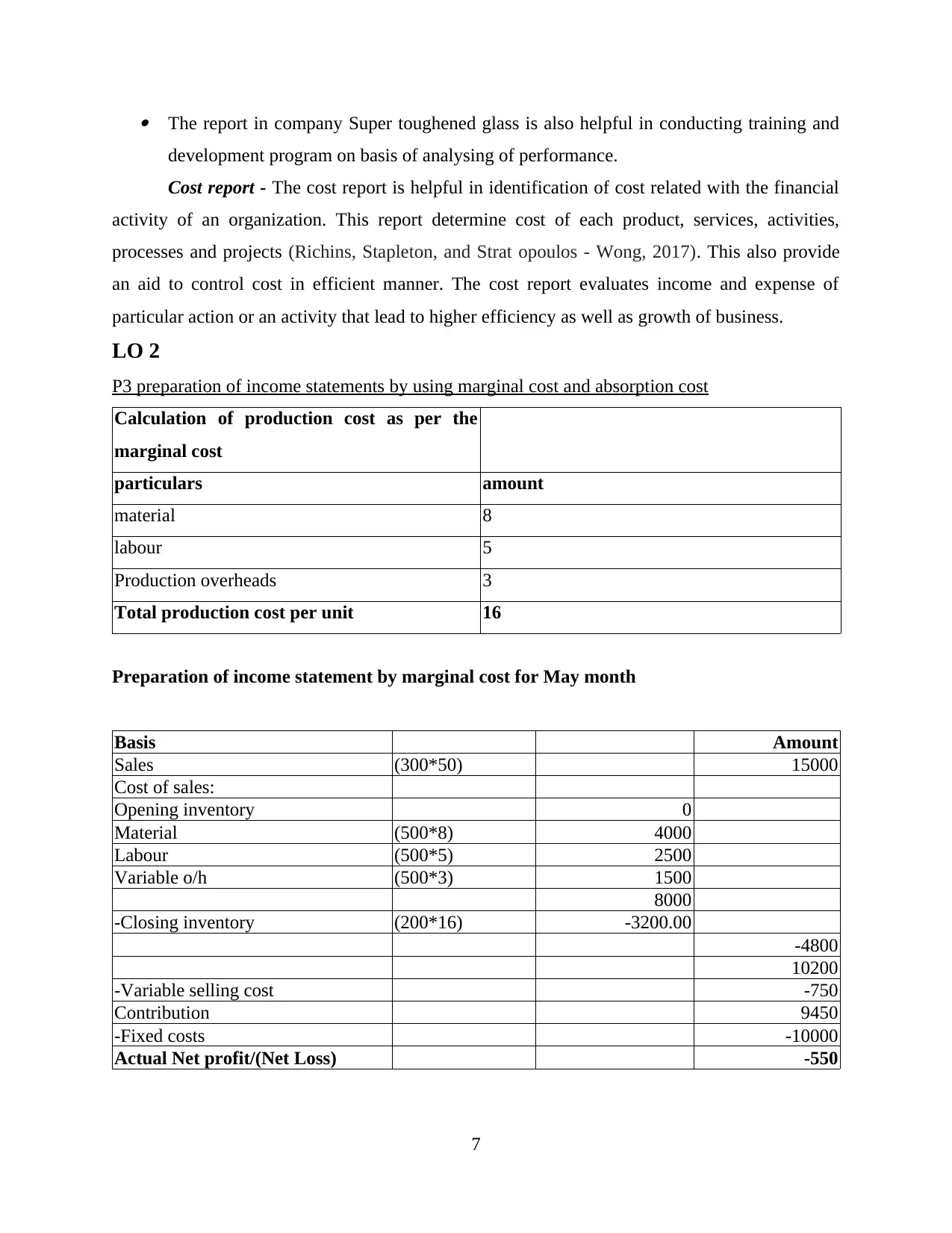

The report in company Super toughened glass is also helpful in conducting training and

development program on basis of analysing of performance.

Cost report - The cost report is helpful in identification of cost related with the financial

activity of an organization. This report determine cost of each product, services, activities,

processes and projects (Richins, Stapleton, and Strat opoulos - Wong, 2017). This also provide

an aid to control cost in efficient manner. The cost report evaluates income and expense of

particular action or an activity that lead to higher efficiency as well as growth of business.

LO 2

P3 preparation of income statements by using marginal cost and absorption cost

Calculation of production cost as per the

marginal cost

particulars amount

material 8

labour 5

Production overheads 3

Total production cost per unit 16

Preparation of income statement by marginal cost for May month

Basis Amount

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

7

development program on basis of analysing of performance.

Cost report - The cost report is helpful in identification of cost related with the financial

activity of an organization. This report determine cost of each product, services, activities,

processes and projects (Richins, Stapleton, and Strat opoulos - Wong, 2017). This also provide

an aid to control cost in efficient manner. The cost report evaluates income and expense of

particular action or an activity that lead to higher efficiency as well as growth of business.

LO 2

P3 preparation of income statements by using marginal cost and absorption cost

Calculation of production cost as per the

marginal cost

particulars amount

material 8

labour 5

Production overheads 3

Total production cost per unit 16

Preparation of income statement by marginal cost for May month

Basis Amount

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

7

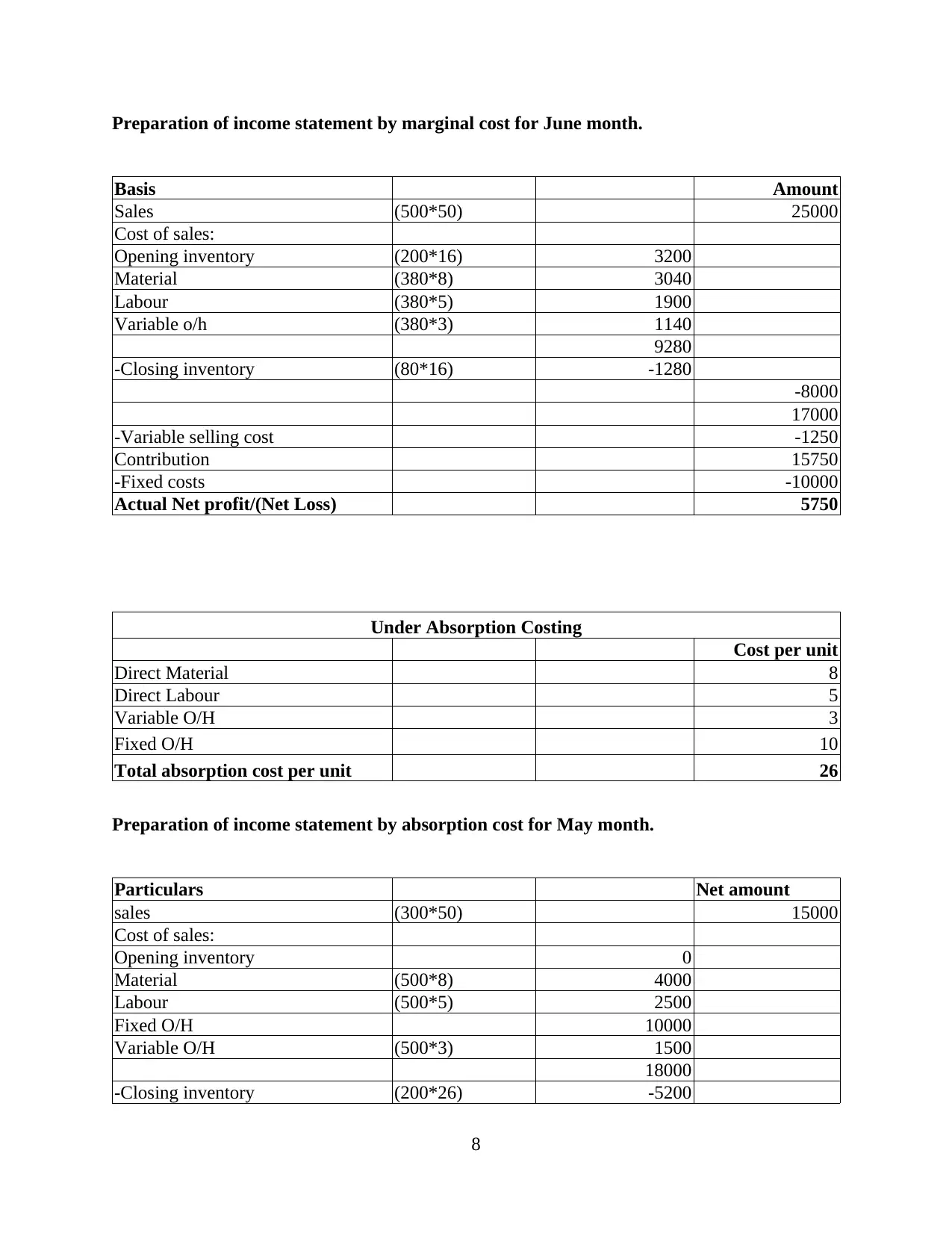

Preparation of income statement by marginal cost for June month.

Basis Amount

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed O/H 10

Total absorption cost per unit 26

Preparation of income statement by absorption cost for May month.

Particulars Net amount

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed O/H 10000

Variable O/H (500*3) 1500

18000

-Closing inventory (200*26) -5200

8

Basis Amount

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed O/H 10

Total absorption cost per unit 26

Preparation of income statement by absorption cost for May month.

Particulars Net amount

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed O/H 10000

Variable O/H (500*3) 1500

18000

-Closing inventory (200*26) -5200

8

-12800

Gross Profit/Loss 2200

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

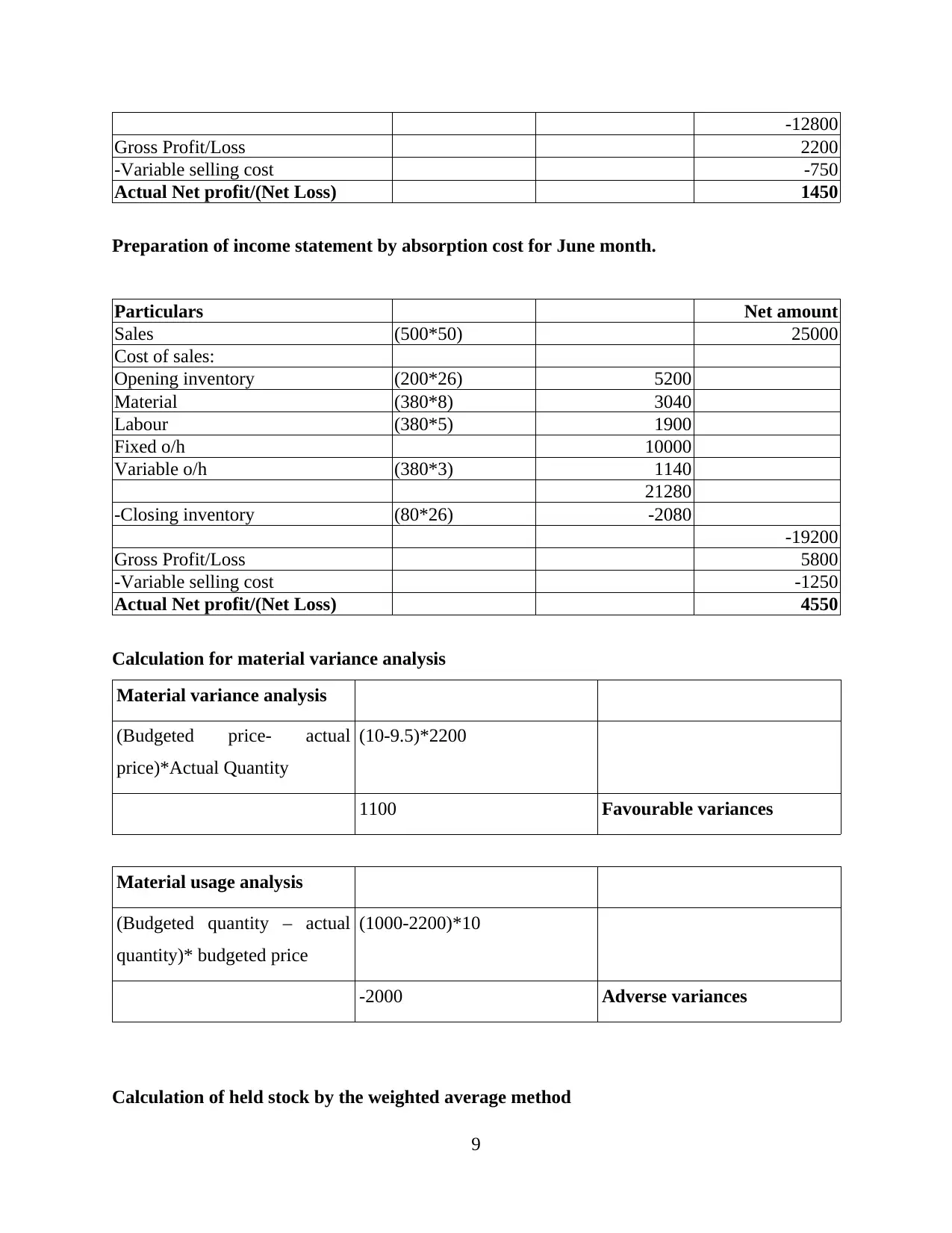

Preparation of income statement by absorption cost for June month.

Particulars Net amount

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Calculation for material variance analysis

Material variance analysis

(Budgeted price- actual

price)*Actual Quantity

(10-9.5)*2200

1100 Favourable variances

Material usage analysis

(Budgeted quantity – actual

quantity)* budgeted price

(1000-2200)*10

-2000 Adverse variances

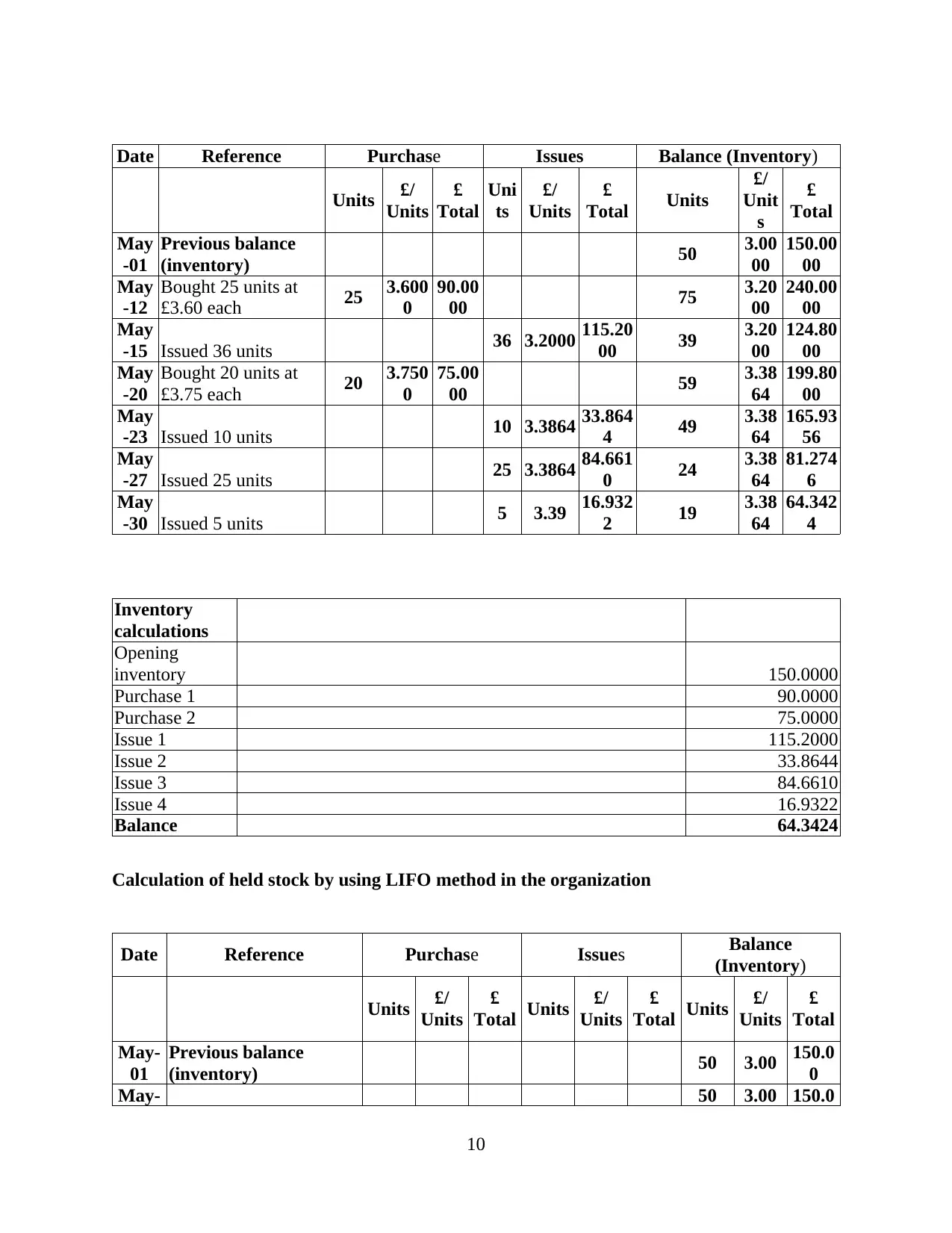

Calculation of held stock by the weighted average method

9

Gross Profit/Loss 2200

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

Preparation of income statement by absorption cost for June month.

Particulars Net amount

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Calculation for material variance analysis

Material variance analysis

(Budgeted price- actual

price)*Actual Quantity

(10-9.5)*2200

1100 Favourable variances

Material usage analysis

(Budgeted quantity – actual

quantity)* budgeted price

(1000-2200)*10

-2000 Adverse variances

Calculation of held stock by the weighted average method

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Date Reference Purchase Issues Balance (Inventory)

Units £/

Units

£

Total

Uni

ts

£/

Units

£

Total Units

£/

Unit

s

£

Total

May

-01

Previous balance

(inventory) 50 3.00

00

150.00

00

May

-12

Bought 25 units at

£3.60 each 25 3.600

0

90.00

00 75 3.20

00

240.00

00

May

-15 Issued 36 units 36 3.2000 115.20

00 39 3.20

00

124.80

00

May

-20

Bought 20 units at

£3.75 each 20 3.750

0

75.00

00 59 3.38

64

199.80

00

May

-23 Issued 10 units 10 3.3864 33.864

4 49 3.38

64

165.93

56

May

-27 Issued 25 units 25 3.3864 84.661

0 24 3.38

64

81.274

6

May

-30 Issued 5 units 5 3.39 16.932

2 19 3.38

64

64.342

4

Inventory

calculations

Opening

inventory 150.0000

Purchase 1 90.0000

Purchase 2 75.0000

Issue 1 115.2000

Issue 2 33.8644

Issue 3 84.6610

Issue 4 16.9322

Balance 64.3424

Calculation of held stock by using LIFO method in the organization

Date Reference Purchase Issues Balance

(Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

May-

01

Previous balance

(inventory) 50 3.00 150.0

0

May- 50 3.00 150.0

10

Units £/

Units

£

Total

Uni

ts

£/

Units

£

Total Units

£/

Unit

s

£

Total

May

-01

Previous balance

(inventory) 50 3.00

00

150.00

00

May

-12

Bought 25 units at

£3.60 each 25 3.600

0

90.00

00 75 3.20

00

240.00

00

May

-15 Issued 36 units 36 3.2000 115.20

00 39 3.20

00

124.80

00

May

-20

Bought 20 units at

£3.75 each 20 3.750

0

75.00

00 59 3.38

64

199.80

00

May

-23 Issued 10 units 10 3.3864 33.864

4 49 3.38

64

165.93

56

May

-27 Issued 25 units 25 3.3864 84.661

0 24 3.38

64

81.274

6

May

-30 Issued 5 units 5 3.39 16.932

2 19 3.38

64

64.342

4

Inventory

calculations

Opening

inventory 150.0000

Purchase 1 90.0000

Purchase 2 75.0000

Issue 1 115.2000

Issue 2 33.8644

Issue 3 84.6610

Issue 4 16.9322

Balance 64.3424

Calculation of held stock by using LIFO method in the organization

Date Reference Purchase Issues Balance

(Inventory)

Units £/

Units

£

Total Units £/

Units

£

Total Units £/

Units

£

Total

May-

01

Previous balance

(inventory) 50 3.00 150.0

0

May- 50 3.00 150.0

10

12 0

Bought 25 units at £3.60

each 25 3.60 90.00 25 3.60 90.00

May-

15 25 3.60 90.00

Issued 36 units 11 3.00 33.00 39 3.00 117.0

0

May-

20 39 3.00 117.0

0

Bought 20 units at £3.75

each 20 3.75 75.00 20 3.75 75.00

May-

23 Issued 10 units 10 3.75 37.50 39 3.00 117.0

0

10 3.75 37.50

May-

27 10 3.75 37.50 24 3.00 72.00

Issued 25 units 15 3.00 45.00

May-

30 Issued 5 units 5 3.00 15.00 19 3.00 57.00

Inventory

calculations

Opening

inventory 150.00

Purchase 1 90.00

Purchase 2 75.00

Issue 1 123.00

Issue 2 37.50

Issue 3 82.50

Issue 4 15.00

Balance 57.00

LO 3

P4 advantages and limitation of planning tools which are used for the budgetary control

Financial budget : Financial budget are prepared to get the information about the

upcoming cask inflow and outflow to manage the expenses and prepare the plan for the spending

the amount different organization activity such as purchasing the raw material, wages and salary,

operating expenses etc. in the business organization (Financial Budget Benefits in Business,

11

Bought 25 units at £3.60

each 25 3.60 90.00 25 3.60 90.00

May-

15 25 3.60 90.00

Issued 36 units 11 3.00 33.00 39 3.00 117.0

0

May-

20 39 3.00 117.0

0

Bought 20 units at £3.75

each 20 3.75 75.00 20 3.75 75.00

May-

23 Issued 10 units 10 3.75 37.50 39 3.00 117.0

0

10 3.75 37.50

May-

27 10 3.75 37.50 24 3.00 72.00

Issued 25 units 15 3.00 45.00

May-

30 Issued 5 units 5 3.00 15.00 19 3.00 57.00

Inventory

calculations

Opening

inventory 150.00

Purchase 1 90.00

Purchase 2 75.00

Issue 1 123.00

Issue 2 37.50

Issue 3 82.50

Issue 4 15.00

Balance 57.00

LO 3

P4 advantages and limitation of planning tools which are used for the budgetary control

Financial budget : Financial budget are prepared to get the information about the

upcoming cask inflow and outflow to manage the expenses and prepare the plan for the spending

the amount different organization activity such as purchasing the raw material, wages and salary,

operating expenses etc. in the business organization (Financial Budget Benefits in Business,

11

2017). There are different types of financial budget such as cash budget, balance sheet budget,

capital expenditure budget etc.

Cash budget are used to forecast the cash transaction such as inflow and outflow of the

cash in the company. Super toughened glass company used to prepare the cash budget to

determine there cash transaction for the particular period. Capital expenditure budget help the

organization to focus on the major assets like plant and machinery, land and building etc. of the

firm. Balance sheet budget is used to control the balance in the organization by evaluating the

total assets and liability and concentrates on the debtor and creditor of the Super toughened glass

company.

Advantages :

Cash budget provide the information to the management regarding the total cash of the

organization and manage the activity according the available cash.

Balance sheet budget help to get the total debt of the organization and provide different

measures to pay and collect the debt from the debtor.

It helps to control the cost of the organization by evaluating each activity, cash inflow

and total capital expenditure of the firm.

It manages and control the cash flow to maintain the cash in company and fulfil the day

to day requirement. It also helps top management for the financial planning and support

the decision of top management. Financial budget communicate the position of the organization to its stakeholders for

motivating them and involve them in business activity to get their full potential.

Disadvantages :

The manipulation of the data is quite common in financial budget preparation. Budgetary

slack increases the expenses of the organization and reduces the profit to earn for

themselves and gain the favourable variances to the budget.

The huge interference of stakeholders may create problem in taking the decisions for the

organization and delay the process which ultimately affect the growth of the business and

employee performance.

Operational budgeting : It represents the company's planned operation like the expected

sales for the accounting period (Pros & Cons of an Operational Budget, 2019). It includes the

various budget like revenue or sales budget, expenses budget and project budget.

12

capital expenditure budget etc.

Cash budget are used to forecast the cash transaction such as inflow and outflow of the

cash in the company. Super toughened glass company used to prepare the cash budget to

determine there cash transaction for the particular period. Capital expenditure budget help the

organization to focus on the major assets like plant and machinery, land and building etc. of the

firm. Balance sheet budget is used to control the balance in the organization by evaluating the

total assets and liability and concentrates on the debtor and creditor of the Super toughened glass

company.

Advantages :

Cash budget provide the information to the management regarding the total cash of the

organization and manage the activity according the available cash.

Balance sheet budget help to get the total debt of the organization and provide different

measures to pay and collect the debt from the debtor.

It helps to control the cost of the organization by evaluating each activity, cash inflow

and total capital expenditure of the firm.

It manages and control the cash flow to maintain the cash in company and fulfil the day

to day requirement. It also helps top management for the financial planning and support

the decision of top management. Financial budget communicate the position of the organization to its stakeholders for

motivating them and involve them in business activity to get their full potential.

Disadvantages :

The manipulation of the data is quite common in financial budget preparation. Budgetary

slack increases the expenses of the organization and reduces the profit to earn for

themselves and gain the favourable variances to the budget.

The huge interference of stakeholders may create problem in taking the decisions for the

organization and delay the process which ultimately affect the growth of the business and

employee performance.

Operational budgeting : It represents the company's planned operation like the expected

sales for the accounting period (Pros & Cons of an Operational Budget, 2019). It includes the

various budget like revenue or sales budget, expenses budget and project budget.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages :

It helps the manager to find and measure the financial position of Super toughened glass

company in future and prepare themselves according to the requirement by estimating the

expected expenses.

By estimating the expenses of the company they are able to control the activities to

minimize their expenses and increase the wealth of the organization.

It manages the current and future expenses by the sales budget and expenses budget. In

expenses budget they compare the actual expenses with the estimate expenses and find

the area in which they increase their expenses and control the activity to get the

favourable variances (Funderburg, 2019).

Operating budget increases the accountability of the manager and employees and force

them to provide the accurate data to understand the true position of Super toughened

glass company. The calculation of variances in the expected and actual expenses help them to control the

budget of the company.

Disadvantages :

In operational budget manager has to measure and control the slack in the data which

ultimately delay the process and increases the unnecessary cost for the Super toughened

glass company.

The adverse variances in the expense budget and project budget increases the cost of firm

and also affect the control of the managers.

Increment budget : Increment budget prepare on the basis of the actual performance or

previous year budget (Asogwa, and Etim, 2017). In the previous year budget the incremental

amount is added to prepare to new budget for the Super Toughened glass company.

Advantages :

The increment budget is easy to prepare and calculate the variances in the expected and

actual budget. Budget is based on the financial result which provide the effective base to

calculate the variances and manage them via proper methods.

It helps the organization to prepare the budget on time and evaluate the various

alternative to control the cost like the wages, raw material cost, production activity cost

etc.

13

It helps the manager to find and measure the financial position of Super toughened glass

company in future and prepare themselves according to the requirement by estimating the

expected expenses.

By estimating the expenses of the company they are able to control the activities to

minimize their expenses and increase the wealth of the organization.

It manages the current and future expenses by the sales budget and expenses budget. In

expenses budget they compare the actual expenses with the estimate expenses and find

the area in which they increase their expenses and control the activity to get the

favourable variances (Funderburg, 2019).

Operating budget increases the accountability of the manager and employees and force

them to provide the accurate data to understand the true position of Super toughened

glass company. The calculation of variances in the expected and actual expenses help them to control the

budget of the company.

Disadvantages :

In operational budget manager has to measure and control the slack in the data which

ultimately delay the process and increases the unnecessary cost for the Super toughened

glass company.

The adverse variances in the expense budget and project budget increases the cost of firm

and also affect the control of the managers.

Increment budget : Increment budget prepare on the basis of the actual performance or

previous year budget (Asogwa, and Etim, 2017). In the previous year budget the incremental

amount is added to prepare to new budget for the Super Toughened glass company.

Advantages :

The increment budget is easy to prepare and calculate the variances in the expected and

actual budget. Budget is based on the financial result which provide the effective base to

calculate the variances and manage them via proper methods.

It helps the organization to prepare the budget on time and evaluate the various

alternative to control the cost like the wages, raw material cost, production activity cost

etc.

13

Increment budget also help the company to compare the budget with the last year

performance and analysis the difference in their performance, so they can rectify them on

time and take effective decision to control the cost.

Disadvantages :

The estimate increment in the base year budget is not accurate or bases on some real fact

which increases the variances in the budget. The adverse variances increase the cost of

the Super toughened glass company (Godwin, 2018).

Manipulation of data is high in increment cost which increases the expenses to reduce the

profit. Interference of employees in decisions also sometime mismanaged the control

process.

It does not encourage the creativity and innovation of employees in setting the budget

because the budget is based on the previous year data so it restricts the creativity of the

employees.

Variance analysis: It is used to identify the variation or differences in the income and

expenses of budgeted cost to the actual cost. It can be calculated by subtracting the budgeted cost

from the actual cost. It helps the business organization to identify the fluctuation and reduce it by

taking effective measures.

Advantages:

It helps the company to identify the reason behind the variation in the actual and

budgeted cost.

Variance analysis is used to identify the methods of reducing adverse variances. It helps to achieve the goal and objectives of the organization by accomplishing the task

within the cost.

Disadvantages:

Variance analysis is mainly applicable in manufacturing and production industry. But in

service industry it is difficult to apply and find the variances in their performance.

The variance in the performance may be arisen due to different reasons. So, it's difficult

to set standard to measure the performance.

It is used for controlling the budget but delay in the presentation reduces it relevancy for

taking effective decisions.

Forecasting: It is the process of identifying the future trend and growth by analysing the

14

performance and analysis the difference in their performance, so they can rectify them on

time and take effective decision to control the cost.

Disadvantages :

The estimate increment in the base year budget is not accurate or bases on some real fact

which increases the variances in the budget. The adverse variances increase the cost of

the Super toughened glass company (Godwin, 2018).

Manipulation of data is high in increment cost which increases the expenses to reduce the

profit. Interference of employees in decisions also sometime mismanaged the control

process.

It does not encourage the creativity and innovation of employees in setting the budget

because the budget is based on the previous year data so it restricts the creativity of the

employees.

Variance analysis: It is used to identify the variation or differences in the income and

expenses of budgeted cost to the actual cost. It can be calculated by subtracting the budgeted cost

from the actual cost. It helps the business organization to identify the fluctuation and reduce it by

taking effective measures.

Advantages:

It helps the company to identify the reason behind the variation in the actual and

budgeted cost.

Variance analysis is used to identify the methods of reducing adverse variances. It helps to achieve the goal and objectives of the organization by accomplishing the task

within the cost.

Disadvantages:

Variance analysis is mainly applicable in manufacturing and production industry. But in

service industry it is difficult to apply and find the variances in their performance.

The variance in the performance may be arisen due to different reasons. So, it's difficult

to set standard to measure the performance.

It is used for controlling the budget but delay in the presentation reduces it relevancy for

taking effective decisions.

Forecasting: It is the process of identifying the future trend and growth by analysing the

14

past and present performance of the company. It is mainly used for planning and preparing

strategies to improve the performance of company in market.

Advantages:

It helps the manager to plan the strategies for the future growth and prepare to deal with

the unexpected circumstances or losses.

It helps to deal with upcoming environmental and market changes. It is used to identify the weaknesses of company and its employees. It helps to take

effective measures to minimize the weaknesses.

Disadvantages:

It is based on the estimation and assumptions. It did not provide accurate information

regarding the future changes.

To collect data and interpret the information consume lots of time that's why forecasting

is time and cost consuming activities.

LO4

P5 Compare ways in which organizations are adapting management accounting systems to

respond to financial problems.

There are different techniques of management accounting which different organization

use dealing with financial problems. This will be discussing below as :

Super toughed glass ABX construction company

The company Super toughened glass

applies benchmarking as well as KPI to

deal with their financial problems. It

helps them to identify the different

financial problem in the organization

such as decrease in demand, sales and

profit, increase in expenses supplier

demand etc.

ABX company use the variance

analysis and balance scorecard tool for

identifying the financial problems of

the company. It also helps to measure

the performance of the employees in

the organization.

Key performance indicator tool helps to

measure the performance of company

by comparing it to the pre setted

Variance analysis tool helps to identify

the difference in the actual and

budgeted performance of the company

15

strategies to improve the performance of company in market.

Advantages:

It helps the manager to plan the strategies for the future growth and prepare to deal with

the unexpected circumstances or losses.

It helps to deal with upcoming environmental and market changes. It is used to identify the weaknesses of company and its employees. It helps to take

effective measures to minimize the weaknesses.

Disadvantages:

It is based on the estimation and assumptions. It did not provide accurate information

regarding the future changes.

To collect data and interpret the information consume lots of time that's why forecasting

is time and cost consuming activities.

LO4

P5 Compare ways in which organizations are adapting management accounting systems to

respond to financial problems.

There are different techniques of management accounting which different organization

use dealing with financial problems. This will be discussing below as :

Super toughed glass ABX construction company

The company Super toughened glass

applies benchmarking as well as KPI to

deal with their financial problems. It

helps them to identify the different

financial problem in the organization

such as decrease in demand, sales and

profit, increase in expenses supplier

demand etc.

ABX company use the variance

analysis and balance scorecard tool for

identifying the financial problems of

the company. It also helps to measure

the performance of the employees in

the organization.

Key performance indicator tool helps to

measure the performance of company

by comparing it to the pre setted

Variance analysis tool helps to identify

the difference in the actual and

budgeted performance of the company

15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

standards. For example: The decrease in

sales may be because of the less

attention of sales department on quality

of product. KPI tool helps them to

measure the performance of employees.

but there are so many reasons of the

variances so its difficult for ABX to

identify the particular reason and take

effective measure to resolve them.

The benchmarking system helps the

Super toughed glass company to

evaluate and measure company

performance in terms of process,

employee, products, etc. (Davila,

Foster, and Jia, 2015).

Balance score card system helps the

ABX company to balance the

performance of employees via the

usage of score card But it only provides

non monetary benefits to the employees

so some time employees feel frustrated

because they want tangible benefits.

Key performance indicator and

benchmarking system helps to identify

bot financial and non financial

problems in the company. They also

provide the effective measures to

resolve the problems and get effective

results.

The balance scorecard and variance

analysis also helps to identify the

difference in their output and

performance of employees but at the

same time it does not give the clear

reason for the variances in performance

and decrease in the profit of company.

Therefore, the company Super toughened glass applies benchmarking as well as KPI to

deal with their financial problems. It has been found that Key performance indicators (KPI) and

benchmarking accounting technique is best to be followed by Super toughed glass in order to

measure and evaluate the performance by which the development of effective strategies can be

optimized. It can be suggested that ABX company has to adopt the additional management

accounting system to measure the performance of the employees and resolve the financial

problems such as decrease in profit, sales, increase in cost etc.

CONCLUSION

This report was all about management accounting. This report focuses on the company

Super toughened glass. This company is medium-sized company operating in UK. The report

16

sales may be because of the less

attention of sales department on quality

of product. KPI tool helps them to

measure the performance of employees.

but there are so many reasons of the

variances so its difficult for ABX to

identify the particular reason and take

effective measure to resolve them.

The benchmarking system helps the

Super toughed glass company to

evaluate and measure company

performance in terms of process,

employee, products, etc. (Davila,

Foster, and Jia, 2015).

Balance score card system helps the

ABX company to balance the

performance of employees via the

usage of score card But it only provides

non monetary benefits to the employees

so some time employees feel frustrated

because they want tangible benefits.

Key performance indicator and

benchmarking system helps to identify

bot financial and non financial

problems in the company. They also

provide the effective measures to

resolve the problems and get effective

results.

The balance scorecard and variance

analysis also helps to identify the

difference in their output and

performance of employees but at the

same time it does not give the clear

reason for the variances in performance

and decrease in the profit of company.

Therefore, the company Super toughened glass applies benchmarking as well as KPI to

deal with their financial problems. It has been found that Key performance indicators (KPI) and

benchmarking accounting technique is best to be followed by Super toughed glass in order to

measure and evaluate the performance by which the development of effective strategies can be

optimized. It can be suggested that ABX company has to adopt the additional management

accounting system to measure the performance of the employees and resolve the financial

problems such as decrease in profit, sales, increase in cost etc.

CONCLUSION

This report was all about management accounting. This report focuses on the company

Super toughened glass. This company is medium-sized company operating in UK. The report

16

was started with brief introduction of management accounting and their essential requirement of

various types of management accounting system. The report then highlighted about the different

method for management accounting. This includes Budget reports, Account receivables Ageing

reports and Performance Reports as different management accounting methods.

After this, the report then covers calculates the appropriate technique cost to analyse cost

and income statement were also prepared for the company Super toughened glass. Then comes

different types of tools of planning and their pros and cons for budgetary control. At last, the

report then lay focuses on comparison of organizational adaptation of management accounting

system for responding with financial problems by the company.

17

various types of management accounting system. The report then highlighted about the different

method for management accounting. This includes Budget reports, Account receivables Ageing

reports and Performance Reports as different management accounting methods.

After this, the report then covers calculates the appropriate technique cost to analyse cost

and income statement were also prepared for the company Super toughened glass. Then comes

different types of tools of planning and their pros and cons for budgetary control. At last, the

report then lay focuses on comparison of organizational adaptation of management accounting

system for responding with financial problems by the company.

17

REFERENCES

Books and Journals

Abdel - Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting Review. 48(2).

pp.169-184.

Apostolou, B., Dorminey, J. W., and Hickey - Hassell, A., 2019. Accounting education literature

review (2018). Journal of Accounting Education.

Asogwa, I.E. and Etim, O.E., 2017. Traditional Budgeting in Today's Business

Environment. Journal of Applied Finance and Banking, 7(3). p.111.

Banker, R. D., Byzalov - Fang D. and Liang, Y., 2017. Cost management research. Journal of

Management Accounting Research. 30(3). pp.187-209.

Cassell, C. A., Myers, L. A. and Seidel, T. A., 2015. Disclosure transparency about activity in

valuation allowance and reserve accounts and accruals-based earnings

management. Accounting, Organizations and Society. 46. pp.23-38.

Davila, A., Foster, G. and Jia, N., 2015. The valuation of management control systems in start-up

companies: international field-based evidence. European Accounting Review. 24(2).

pp.207-239.

Funderburg, R., 2019. Regional employment and housing impacts of tax increment financing

districts. Regional Studies, 53(6). pp.874-886.

Godwin, M. L., 2018. Studying Participatory Budgeting: Democratic Innovation or Budgeting

Tool?. State and Local Government Review, 50(2). pp.132-144.

Peterson, K., Schmardebeck, R. and Wilks, T. J., 2015. The earnings quality and information

processing effects of accounting consistency. The accounting review. 90(6). pp.2483-

2514.

Richins, G., Stapleton, A., and Stratopoulos - Wong, C., 2017. Big Data analytics: Opportunity

or threat for the accounting profession?. Journal of Information Systems. 31(3). pp.63-79.

Online

Financial Budget Benefits in Business. 2017. [Online]. Available through :

<https://bizfluent.com/info-8014791-financial-budget-benefits-business.html>.

18

Books and Journals

Abdel - Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting Review. 48(2).

pp.169-184.

Apostolou, B., Dorminey, J. W., and Hickey - Hassell, A., 2019. Accounting education literature

review (2018). Journal of Accounting Education.

Asogwa, I.E. and Etim, O.E., 2017. Traditional Budgeting in Today's Business

Environment. Journal of Applied Finance and Banking, 7(3). p.111.

Banker, R. D., Byzalov - Fang D. and Liang, Y., 2017. Cost management research. Journal of

Management Accounting Research. 30(3). pp.187-209.

Cassell, C. A., Myers, L. A. and Seidel, T. A., 2015. Disclosure transparency about activity in

valuation allowance and reserve accounts and accruals-based earnings

management. Accounting, Organizations and Society. 46. pp.23-38.

Davila, A., Foster, G. and Jia, N., 2015. The valuation of management control systems in start-up

companies: international field-based evidence. European Accounting Review. 24(2).

pp.207-239.

Funderburg, R., 2019. Regional employment and housing impacts of tax increment financing

districts. Regional Studies, 53(6). pp.874-886.

Godwin, M. L., 2018. Studying Participatory Budgeting: Democratic Innovation or Budgeting

Tool?. State and Local Government Review, 50(2). pp.132-144.

Peterson, K., Schmardebeck, R. and Wilks, T. J., 2015. The earnings quality and information

processing effects of accounting consistency. The accounting review. 90(6). pp.2483-

2514.

Richins, G., Stapleton, A., and Stratopoulos - Wong, C., 2017. Big Data analytics: Opportunity

or threat for the accounting profession?. Journal of Information Systems. 31(3). pp.63-79.

Online

Financial Budget Benefits in Business. 2017. [Online]. Available through :

<https://bizfluent.com/info-8014791-financial-budget-benefits-business.html>.

18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pros & Cons of an Operational Budget. 2019. [Online]. Available through :

<https://smallbusiness.chron.com/pros-cons-operational-budget-35123.html>.

19

<https://smallbusiness.chron.com/pros-cons-operational-budget-35123.html>.

19

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.