Unit 5: Management Accounting

VerifiedAdded on 2023/01/17

|19

|5401

|23

AI Summary

2800 word

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Unit 5

Management Accounting

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and its system............................................................................3

P2 Management Accounting Reporting:................................................................................4

M1 Benefits of Management Accounting Systems:...............................................................5

D1 Integration of management accounting system and management accounting reporting in

organizational processes:........................................................................................................6

TASK 2............................................................................................................................................6

P3 Calculation of cost using management accounting techniques:........................................6

D2 Interpretation of the data:.................................................................................................9

TASK 3............................................................................................................................................9

P4 Different types of planning tools used for budgetary control:..........................................9

M3 Use of planning tools and their application in forecasting budgets:..............................13

TASK 4..........................................................................................................................................13

P5 Management accounting techniques used to identify financial problems:.....................13

M4 Analysis of how management accounting can lead an organisation to sustainable success:

..............................................................................................................................................15

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:..............................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and its system............................................................................3

P2 Management Accounting Reporting:................................................................................4

M1 Benefits of Management Accounting Systems:...............................................................5

D1 Integration of management accounting system and management accounting reporting in

organizational processes:........................................................................................................6

TASK 2............................................................................................................................................6

P3 Calculation of cost using management accounting techniques:........................................6

D2 Interpretation of the data:.................................................................................................9

TASK 3............................................................................................................................................9

P4 Different types of planning tools used for budgetary control:..........................................9

M3 Use of planning tools and their application in forecasting budgets:..............................13

TASK 4..........................................................................................................................................13

P5 Management accounting techniques used to identify financial problems:.....................13

M4 Analysis of how management accounting can lead an organisation to sustainable success:

..............................................................................................................................................15

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:..............................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

In today's economically changing world, the organizations have financial management

system that only provides the information and assistance of external organizational factors hence

the entrepreneurs are feeling the need of a system that can avail the information and manage the

internal activities and factors of an organization. For this purpose, the method which is evolved

is known as management or managerial accounting. Management accounting process was

followed at the beginning of 19th century and it differs from financial accounting in so many

aspects such as users of information and statements, format, legal aspects and others.

For the optimistic knowledge of management accounting process and its utilization, a

trainee management accountant of KEF LTD., which is the medium sized enterprise in the

manufacture sector. The company is preparing a report which explains the management

accounting, its systems, reporting process and various financial problems and their solutions with

the help of management accounting techniques. The report also includes some costing data and

information which help the management to better understanding of these managerial accounting

techniques.

TASK 1

P1 Management accounting and its system.

Management Accounting: The term management accounting can be defined as a

complete cycle that includes the process of collecting, recording, classifying, summarising,

preparing, presenting, reporting and controlling the financial and non-financial data in such a

manner so that it can help the management of the organization in order to measure the efficiency

and performance of the personnel as well as the operations and activities, planning the strategies

for achieving the objectives and making effective decisions to increase the profitability of the

company (Cuzzocrea and et.al, 2018).

Management Accounting System:

The management of KEF LTD follows various managerial accounting systems so that it

can impressively manage an effective business strategy. Some of them are elaborated below: Price Optimisation System: Price optimisation system is a mathematical analysis

technique that provides the information and material data about how the demand of a

product or service vary by the variation in price. It also analyse the behaviour and

reaction of the customers toward different price set for the same products in different

In today's economically changing world, the organizations have financial management

system that only provides the information and assistance of external organizational factors hence

the entrepreneurs are feeling the need of a system that can avail the information and manage the

internal activities and factors of an organization. For this purpose, the method which is evolved

is known as management or managerial accounting. Management accounting process was

followed at the beginning of 19th century and it differs from financial accounting in so many

aspects such as users of information and statements, format, legal aspects and others.

For the optimistic knowledge of management accounting process and its utilization, a

trainee management accountant of KEF LTD., which is the medium sized enterprise in the

manufacture sector. The company is preparing a report which explains the management

accounting, its systems, reporting process and various financial problems and their solutions with

the help of management accounting techniques. The report also includes some costing data and

information which help the management to better understanding of these managerial accounting

techniques.

TASK 1

P1 Management accounting and its system.

Management Accounting: The term management accounting can be defined as a

complete cycle that includes the process of collecting, recording, classifying, summarising,

preparing, presenting, reporting and controlling the financial and non-financial data in such a

manner so that it can help the management of the organization in order to measure the efficiency

and performance of the personnel as well as the operations and activities, planning the strategies

for achieving the objectives and making effective decisions to increase the profitability of the

company (Cuzzocrea and et.al, 2018).

Management Accounting System:

The management of KEF LTD follows various managerial accounting systems so that it

can impressively manage an effective business strategy. Some of them are elaborated below: Price Optimisation System: Price optimisation system is a mathematical analysis

technique that provides the information and material data about how the demand of a

product or service vary by the variation in price. It also analyse the behaviour and

reaction of the customers toward different price set for the same products in different

situations (Eckardt, Selen and Wynder, 2015). It records and classifies the information

and then apply it on cost of production of inventory to help the administration in opting

out the best price that improves the profit and customer satisfaction as well. For

collecting the information and observing costumer behaviour on different pricing, various

channels are used by KEF LTD. The company proposed different sets of prices to its all

age brackets' consumers and decide optimistic price according to them.

Inventory Management System: Inventory management system is a framework that

includes the structure and process of maintaining and supervising the inventory of the

organization. Inventory is an essential asset for the company and it is necessary to

maintain record of it (Fullerton, Kennedy and Widener, 2014). It is crucial for an

establishment to manage and keep a proper record of the inventory whether it is raw

material, work in progress, finished stock in warehouse and showrooms, goods sent on

consignment or goods dispatched for delivery to vendors or customers. For tracking its

inventory, KEF LTD uses software which helps the company to solve the queries of the

customers on time and also guides to maintain the quality of the juice products.

P2 Management Accounting Reporting:

Management Accounting Reports: These reports are basically the result statements

which contain the variances between estimations, forecasts and actual outcomes related to

different activities and operations and are prepared and presented by management accountants to

help the management in controlling and planning appropriate guidelines and strategies for

betterment of the employees as well as the procedures. Performance Report: Performance report can be defined as a report card which is

provided to any person, activity or process so that the effectiveness of their efforts and

efficiency of performance can be measured in order to achieve their objectives. An

establishment uses this kind of reports to analyse the potential of its employees, strategies

and management as well (Giannarakis, Konteos and Sariannidis, 2014). This report

reveals the variance between the efforts done by the employees and efforts they supposed

to do. The receiver of this report is liable to perform the remedial activities to improve

the performance if required. KEF LTD. management prepares performance reports for

employees and activities so that they may be rewarded, trained or change accordingly.

and then apply it on cost of production of inventory to help the administration in opting

out the best price that improves the profit and customer satisfaction as well. For

collecting the information and observing costumer behaviour on different pricing, various

channels are used by KEF LTD. The company proposed different sets of prices to its all

age brackets' consumers and decide optimistic price according to them.

Inventory Management System: Inventory management system is a framework that

includes the structure and process of maintaining and supervising the inventory of the

organization. Inventory is an essential asset for the company and it is necessary to

maintain record of it (Fullerton, Kennedy and Widener, 2014). It is crucial for an

establishment to manage and keep a proper record of the inventory whether it is raw

material, work in progress, finished stock in warehouse and showrooms, goods sent on

consignment or goods dispatched for delivery to vendors or customers. For tracking its

inventory, KEF LTD uses software which helps the company to solve the queries of the

customers on time and also guides to maintain the quality of the juice products.

P2 Management Accounting Reporting:

Management Accounting Reports: These reports are basically the result statements

which contain the variances between estimations, forecasts and actual outcomes related to

different activities and operations and are prepared and presented by management accountants to

help the management in controlling and planning appropriate guidelines and strategies for

betterment of the employees as well as the procedures. Performance Report: Performance report can be defined as a report card which is

provided to any person, activity or process so that the effectiveness of their efforts and

efficiency of performance can be measured in order to achieve their objectives. An

establishment uses this kind of reports to analyse the potential of its employees, strategies

and management as well (Giannarakis, Konteos and Sariannidis, 2014). This report

reveals the variance between the efforts done by the employees and efforts they supposed

to do. The receiver of this report is liable to perform the remedial activities to improve

the performance if required. KEF LTD. management prepares performance reports for

employees and activities so that they may be rewarded, trained or change accordingly.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

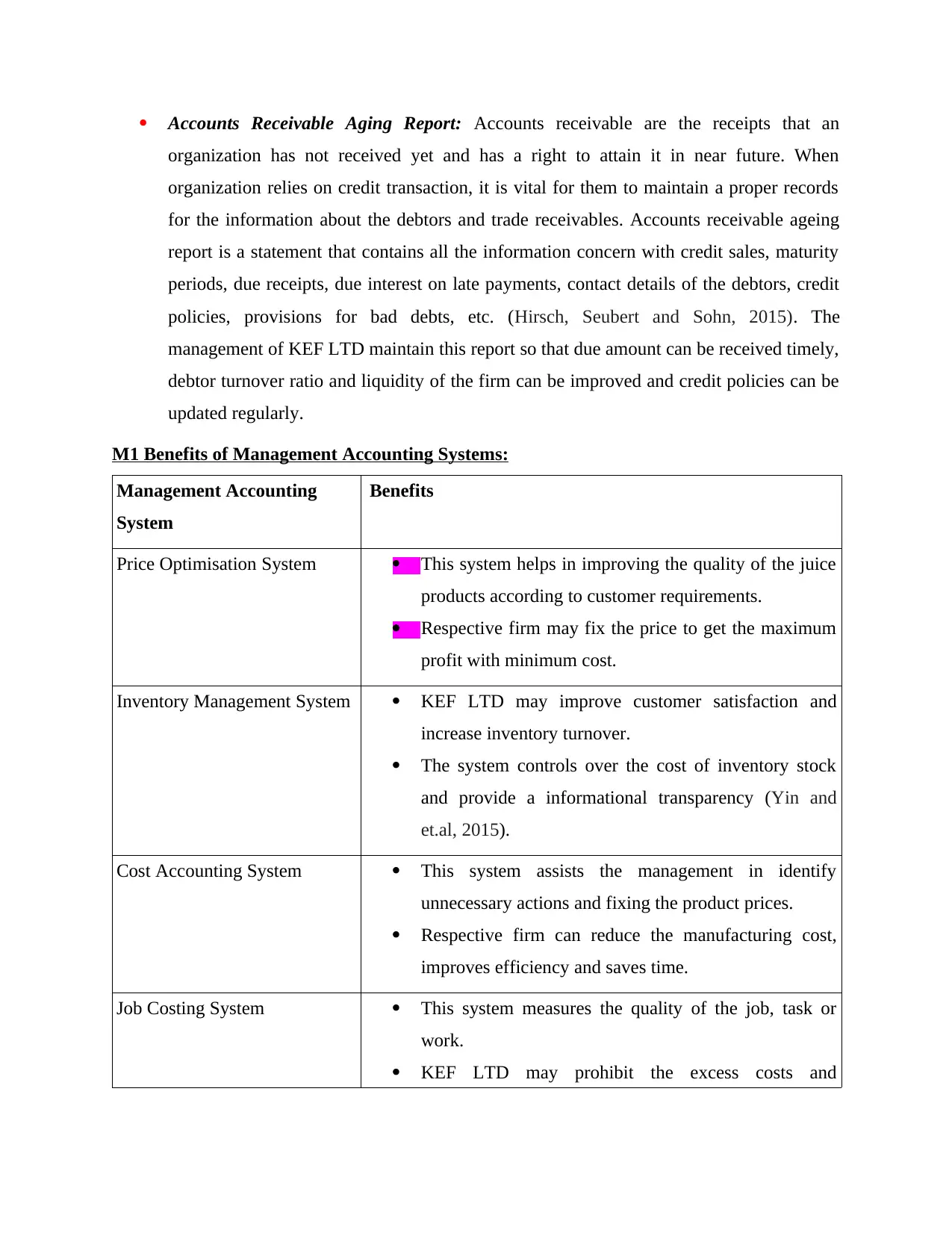

Accounts Receivable Aging Report: Accounts receivable are the receipts that an

organization has not received yet and has a right to attain it in near future. When

organization relies on credit transaction, it is vital for them to maintain a proper records

for the information about the debtors and trade receivables. Accounts receivable ageing

report is a statement that contains all the information concern with credit sales, maturity

periods, due receipts, due interest on late payments, contact details of the debtors, credit

policies, provisions for bad debts, etc. (Hirsch, Seubert and Sohn, 2015). The

management of KEF LTD maintain this report so that due amount can be received timely,

debtor turnover ratio and liquidity of the firm can be improved and credit policies can be

updated regularly.

M1 Benefits of Management Accounting Systems:

Management Accounting

System

Benefits

Price Optimisation System This system helps in improving the quality of the juice

products according to customer requirements.

Respective firm may fix the price to get the maximum

profit with minimum cost.

Inventory Management System KEF LTD may improve customer satisfaction and

increase inventory turnover.

The system controls over the cost of inventory stock

and provide a informational transparency (Yin and

et.al, 2015).

Cost Accounting System This system assists the management in identify

unnecessary actions and fixing the product prices.

Respective firm can reduce the manufacturing cost,

improves efficiency and saves time.

Job Costing System This system measures the quality of the job, task or

work.

KEF LTD may prohibit the excess costs and

organization has not received yet and has a right to attain it in near future. When

organization relies on credit transaction, it is vital for them to maintain a proper records

for the information about the debtors and trade receivables. Accounts receivable ageing

report is a statement that contains all the information concern with credit sales, maturity

periods, due receipts, due interest on late payments, contact details of the debtors, credit

policies, provisions for bad debts, etc. (Hirsch, Seubert and Sohn, 2015). The

management of KEF LTD maintain this report so that due amount can be received timely,

debtor turnover ratio and liquidity of the firm can be improved and credit policies can be

updated regularly.

M1 Benefits of Management Accounting Systems:

Management Accounting

System

Benefits

Price Optimisation System This system helps in improving the quality of the juice

products according to customer requirements.

Respective firm may fix the price to get the maximum

profit with minimum cost.

Inventory Management System KEF LTD may improve customer satisfaction and

increase inventory turnover.

The system controls over the cost of inventory stock

and provide a informational transparency (Yin and

et.al, 2015).

Cost Accounting System This system assists the management in identify

unnecessary actions and fixing the product prices.

Respective firm can reduce the manufacturing cost,

improves efficiency and saves time.

Job Costing System This system measures the quality of the job, task or

work.

KEF LTD may prohibit the excess costs and

duplication of work.

D1 Integration of management accounting system and management accounting reporting in

organizational processes:

Management accounting system and reporting both are the essential part of management

accounting processes. The system provides the policies, procedures and structure for the

reporting process. Without managing a proper accounting system, it is not possible for any

organization to collect and classified the data and information in such a systematic way that

management can utilize it (Wang and et.al, 2017). On the other hand, various reports provides

the variances and reasons behind them to the management which enables the administration to

co-ordinate different departments of an organization in order to create an effective system. For

example, if inventory management system will not work properly, it will be difficult to keep a

record of inventory and accurate variances cannot be measured in inventory management reports

and if reporting system will not provide accurate information to the system, management cannot

solve the queries of the customers. Hence it is must for the KEF LTD to maintain both the

system and the reporting process together in order to survive in the industry.

TASK 2

P3 Calculation of cost using management accounting techniques:

Meaning of cost: It is defined as the cash amount which is given up for an asset. This includes

all costs which are necessary to get and assets in the place and ready for use in appropriate

manner.

Different types of cost:

Direct cost is the price which can be directly tied to the production for specific goods and

services. Indirect cost: that is not directly accountable to the cost objects on the particular project

and services, function and products.

◦ Variable cost is the corporate expenses which vary in the direct proportion to the

quantity of outputs.

◦ Fixed cost: this defined as expenses which do not change as a function of all the

activities which are relevant to the function and period.

D1 Integration of management accounting system and management accounting reporting in

organizational processes:

Management accounting system and reporting both are the essential part of management

accounting processes. The system provides the policies, procedures and structure for the

reporting process. Without managing a proper accounting system, it is not possible for any

organization to collect and classified the data and information in such a systematic way that

management can utilize it (Wang and et.al, 2017). On the other hand, various reports provides

the variances and reasons behind them to the management which enables the administration to

co-ordinate different departments of an organization in order to create an effective system. For

example, if inventory management system will not work properly, it will be difficult to keep a

record of inventory and accurate variances cannot be measured in inventory management reports

and if reporting system will not provide accurate information to the system, management cannot

solve the queries of the customers. Hence it is must for the KEF LTD to maintain both the

system and the reporting process together in order to survive in the industry.

TASK 2

P3 Calculation of cost using management accounting techniques:

Meaning of cost: It is defined as the cash amount which is given up for an asset. This includes

all costs which are necessary to get and assets in the place and ready for use in appropriate

manner.

Different types of cost:

Direct cost is the price which can be directly tied to the production for specific goods and

services. Indirect cost: that is not directly accountable to the cost objects on the particular project

and services, function and products.

◦ Variable cost is the corporate expenses which vary in the direct proportion to the

quantity of outputs.

◦ Fixed cost: this defined as expenses which do not change as a function of all the

activities which are relevant to the function and period.

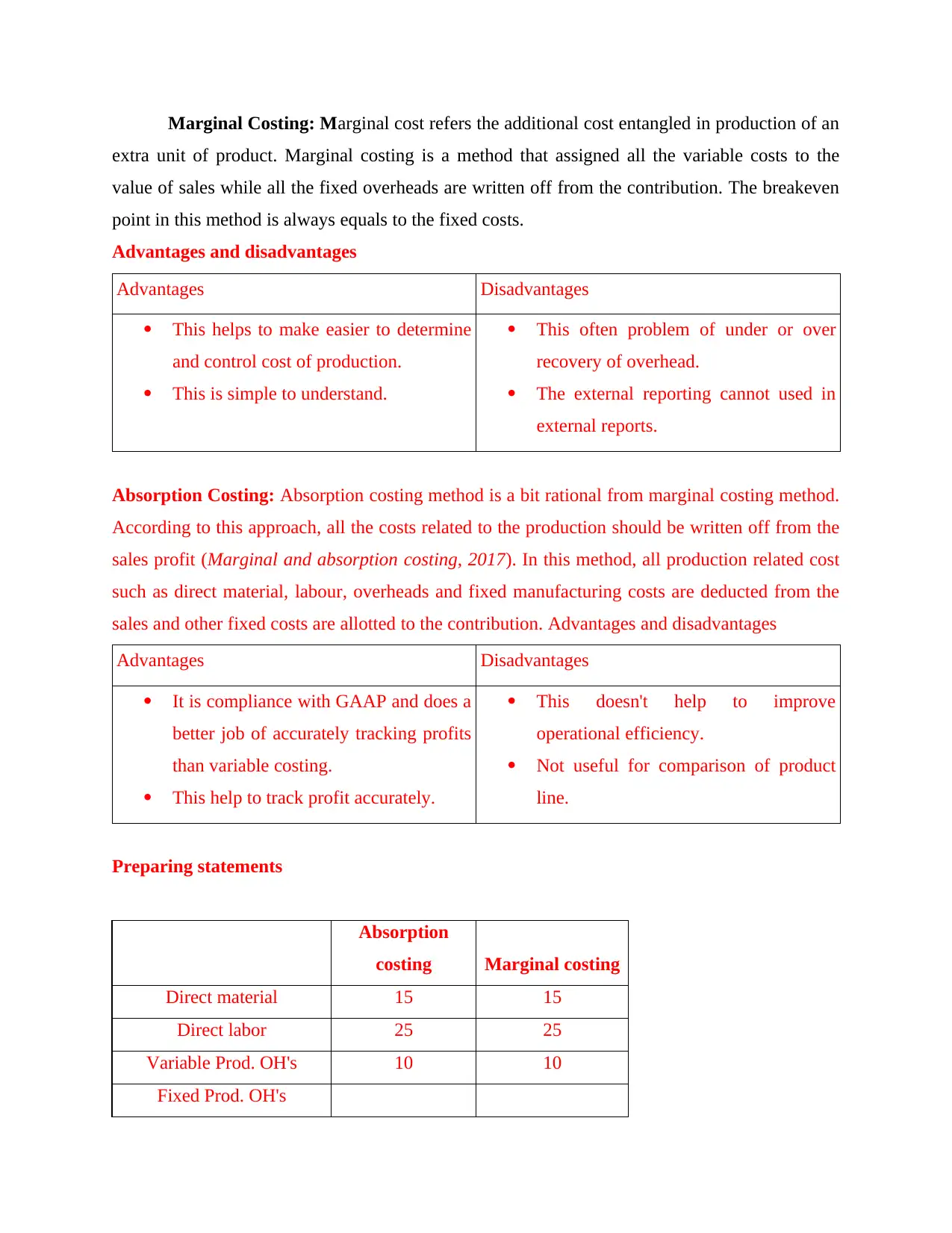

Marginal Costing: Marginal cost refers the additional cost entangled in production of an

extra unit of product. Marginal costing is a method that assigned all the variable costs to the

value of sales while all the fixed overheads are written off from the contribution. The breakeven

point in this method is always equals to the fixed costs.

Advantages and disadvantages

Advantages Disadvantages

This helps to make easier to determine

and control cost of production.

This is simple to understand.

This often problem of under or over

recovery of overhead.

The external reporting cannot used in

external reports.

Absorption Costing: Absorption costing method is a bit rational from marginal costing method.

According to this approach, all the costs related to the production should be written off from the

sales profit (Marginal and absorption costing, 2017). In this method, all production related cost

such as direct material, labour, overheads and fixed manufacturing costs are deducted from the

sales and other fixed costs are allotted to the contribution. Advantages and disadvantages

Advantages Disadvantages

It is compliance with GAAP and does a

better job of accurately tracking profits

than variable costing.

This help to track profit accurately.

This doesn't help to improve

operational efficiency.

Not useful for comparison of product

line.

Preparing statements

Absorption

costing Marginal costing

Direct material 15 15

Direct labor 25 25

Variable Prod. OH's 10 10

Fixed Prod. OH's

extra unit of product. Marginal costing is a method that assigned all the variable costs to the

value of sales while all the fixed overheads are written off from the contribution. The breakeven

point in this method is always equals to the fixed costs.

Advantages and disadvantages

Advantages Disadvantages

This helps to make easier to determine

and control cost of production.

This is simple to understand.

This often problem of under or over

recovery of overhead.

The external reporting cannot used in

external reports.

Absorption Costing: Absorption costing method is a bit rational from marginal costing method.

According to this approach, all the costs related to the production should be written off from the

sales profit (Marginal and absorption costing, 2017). In this method, all production related cost

such as direct material, labour, overheads and fixed manufacturing costs are deducted from the

sales and other fixed costs are allotted to the contribution. Advantages and disadvantages

Advantages Disadvantages

It is compliance with GAAP and does a

better job of accurately tracking profits

than variable costing.

This help to track profit accurately.

This doesn't help to improve

operational efficiency.

Not useful for comparison of product

line.

Preparing statements

Absorption

costing Marginal costing

Direct material 15 15

Direct labor 25 25

Variable Prod. OH's 10 10

Fixed Prod. OH's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

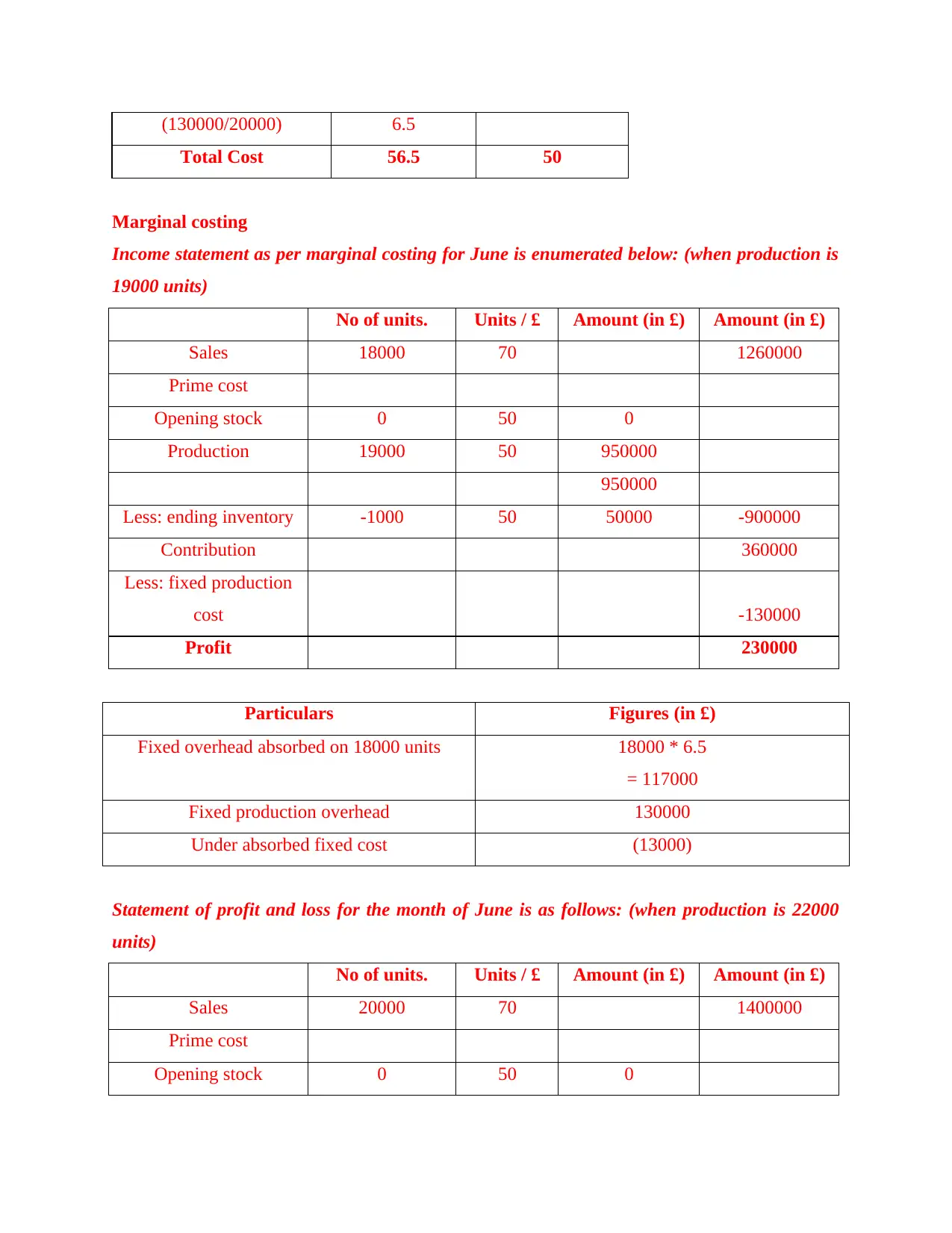

(130000/20000) 6.5

Total Cost 56.5 50

Marginal costing

Income statement as per marginal costing for June is enumerated below: (when production is

19000 units)

No of units. Units / £ Amount (in £) Amount (in £)

Sales 18000 70 1260000

Prime cost

Opening stock 0 50 0

Production 19000 50 950000

950000

Less: ending inventory -1000 50 50000 -900000

Contribution 360000

Less: fixed production

cost -130000

Profit 230000

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

Fixed production overhead 130000

Under absorbed fixed cost (13000)

Statement of profit and loss for the month of June is as follows: (when production is 22000

units)

No of units. Units / £ Amount (in £) Amount (in £)

Sales 20000 70 1400000

Prime cost

Opening stock 0 50 0

Total Cost 56.5 50

Marginal costing

Income statement as per marginal costing for June is enumerated below: (when production is

19000 units)

No of units. Units / £ Amount (in £) Amount (in £)

Sales 18000 70 1260000

Prime cost

Opening stock 0 50 0

Production 19000 50 950000

950000

Less: ending inventory -1000 50 50000 -900000

Contribution 360000

Less: fixed production

cost -130000

Profit 230000

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

Fixed production overhead 130000

Under absorbed fixed cost (13000)

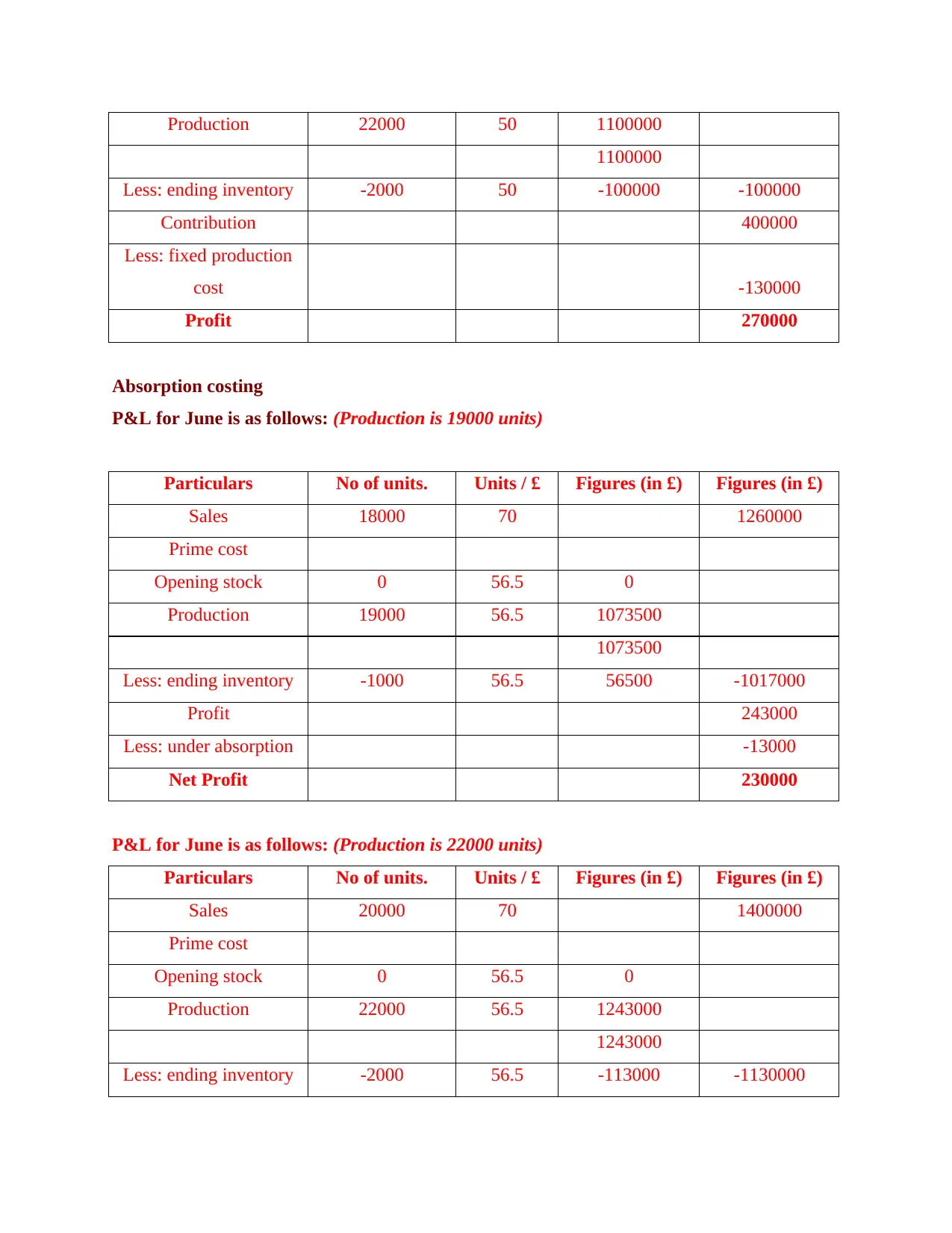

Statement of profit and loss for the month of June is as follows: (when production is 22000

units)

No of units. Units / £ Amount (in £) Amount (in £)

Sales 20000 70 1400000

Prime cost

Opening stock 0 50 0

Production 22000 50 1100000

1100000

Less: ending inventory -2000 50 -100000 -100000

Contribution 400000

Less: fixed production

cost -130000

Profit 270000

Absorption costing

P&L for June is as follows: (Production is 19000 units)

Particulars No of units. Units / £ Figures (in £) Figures (in £)

Sales 18000 70 1260000

Prime cost

Opening stock 0 56.5 0

Production 19000 56.5 1073500

1073500

Less: ending inventory -1000 56.5 56500 -1017000

Profit 243000

Less: under absorption -13000

Net Profit 230000

P&L for June is as follows: (Production is 22000 units)

Particulars No of units. Units / £ Figures (in £) Figures (in £)

Sales 20000 70 1400000

Prime cost

Opening stock 0 56.5 0

Production 22000 56.5 1243000

1243000

Less: ending inventory -2000 56.5 -113000 -1130000

1100000

Less: ending inventory -2000 50 -100000 -100000

Contribution 400000

Less: fixed production

cost -130000

Profit 270000

Absorption costing

P&L for June is as follows: (Production is 19000 units)

Particulars No of units. Units / £ Figures (in £) Figures (in £)

Sales 18000 70 1260000

Prime cost

Opening stock 0 56.5 0

Production 19000 56.5 1073500

1073500

Less: ending inventory -1000 56.5 56500 -1017000

Profit 243000

Less: under absorption -13000

Net Profit 230000

P&L for June is as follows: (Production is 22000 units)

Particulars No of units. Units / £ Figures (in £) Figures (in £)

Sales 20000 70 1400000

Prime cost

Opening stock 0 56.5 0

Production 22000 56.5 1243000

1243000

Less: ending inventory -2000 56.5 -113000 -1130000

Profit 270000

D2 Interpretation of the data:

As it may be seen that marginal costing and absorption costing approaches are having

differences in their presentation. In income statements, profit as per marginal and absorption

costing implies for £230000 respectively when 19000 units are produced. However, in the case

where 22000 units are produced profitability implies for £270000 significantly. Considering

overall evaluation it can be presented that firm should lay focus on undertaking absorption

costing system over marginal. Moreover, it provides suitable view of cost and profitability by

taking into account both fixed as well as variable cost of production.

TASK 3

P4 Different types of planning tools used for budgetary control:

In the context of business unit, planning tools are highly important which in turn facilitates

optimum utilization of financial resources. There are several planning that can be undertaken by

the firm for getting the desired level of outcome or success.

Budget: Budget can be defined as a statement or list of forecasted and estimated incomes

as well the expenditures of an organization that may take place in a specific time period. Budget

is a crucial part of management accounting that helps the management to plan its strategies and

make effective decisions in accordance with the potential of its employees and available

resources (Hoozée and Ngo, 2018). On the other side, budgetary control is a process that is used

to find out the variances between actual and budgeted figures. Management of the organizations

are habitant to compare the actual outcomes with budgeted figures so that variances can be

detected a time before they get worse.

With regards to KEF LTD, budgeting is highly significant which in turn helps in

managing and monitoring expenses effectually. By this, firm can do comparison of existing

performance and thereby identified loopholes. In this way, it enables firm to take appropriate

actions timely and thereby attain success. Further, through using budgeting tool firm can avoid

contingent situation pertaining to the near future effectually.

Flexible Budget: Flexible budget which is also known as variable budget is an easy

approach of preparing budget as it provides the estimations for various stages of production and

D2 Interpretation of the data:

As it may be seen that marginal costing and absorption costing approaches are having

differences in their presentation. In income statements, profit as per marginal and absorption

costing implies for £230000 respectively when 19000 units are produced. However, in the case

where 22000 units are produced profitability implies for £270000 significantly. Considering

overall evaluation it can be presented that firm should lay focus on undertaking absorption

costing system over marginal. Moreover, it provides suitable view of cost and profitability by

taking into account both fixed as well as variable cost of production.

TASK 3

P4 Different types of planning tools used for budgetary control:

In the context of business unit, planning tools are highly important which in turn facilitates

optimum utilization of financial resources. There are several planning that can be undertaken by

the firm for getting the desired level of outcome or success.

Budget: Budget can be defined as a statement or list of forecasted and estimated incomes

as well the expenditures of an organization that may take place in a specific time period. Budget

is a crucial part of management accounting that helps the management to plan its strategies and

make effective decisions in accordance with the potential of its employees and available

resources (Hoozée and Ngo, 2018). On the other side, budgetary control is a process that is used

to find out the variances between actual and budgeted figures. Management of the organizations

are habitant to compare the actual outcomes with budgeted figures so that variances can be

detected a time before they get worse.

With regards to KEF LTD, budgeting is highly significant which in turn helps in

managing and monitoring expenses effectually. By this, firm can do comparison of existing

performance and thereby identified loopholes. In this way, it enables firm to take appropriate

actions timely and thereby attain success. Further, through using budgeting tool firm can avoid

contingent situation pertaining to the near future effectually.

Flexible Budget: Flexible budget which is also known as variable budget is an easy

approach of preparing budget as it provides the estimations for various stages of production and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

easy to get moderate. The figures stated in that kind of budget flex or changes with the change in

activities (Sledgianowski, Gomaa and Tan, 2017). It doesn't mean that static values change

according to the actual outcome, it means that budget is prepared for different level of production

with the changes in variable costs and trend deltas in fixed costs.

Advantages:

This budget is more easy and flexible than fixed budget as it can be changed or modified

according to the market situation (Ríos, Bastida and Benito, 2016). This budget is prepared on the basis of principles and knowledge unlike the fixed budget

which is based upon judgement, assumptions and estimates.

Disadvantages:

This budget interrupt the discipline and increase the chances of cheating within the

organization as it avoid the rigidity. It may be time-consuming as it needs estimation for various levels which is a prime

factor at the time of budget preparation.

Capital Budget: Capital budget is related with the estimated revenues and expenses

which may be affected by the capital investments. All the aspects related with capital such as

long term loans, investments, share allotment and forfeiture, purchase and sale of assets, bonds

and debentures are covered in capital budget (Ismail and King, 2014). KEF LTD uses this budget

to calculate payback period, ARR, IRR, capital employed, ROI, etc.

Advantages:

This budget helps the management in making decisions related investments and maintain

the liquidity of the company. It also assists the management to evaluate the risk factor in any decision or activity.

Disadvantages:

Preparation of these kind of budget demands skills and professionalism which may be

expensive for the firm. All the techniques used in this budget are based on assumptions and future events are

always uncertain which increases the risk factor.

Implications: for instance KEF Ltd has two investment proposal A and B with same initial

investment but different cash flows. In this regard, by applying investment appraisal tool

decision can be taken for the selection or rejection of proposal.

activities (Sledgianowski, Gomaa and Tan, 2017). It doesn't mean that static values change

according to the actual outcome, it means that budget is prepared for different level of production

with the changes in variable costs and trend deltas in fixed costs.

Advantages:

This budget is more easy and flexible than fixed budget as it can be changed or modified

according to the market situation (Ríos, Bastida and Benito, 2016). This budget is prepared on the basis of principles and knowledge unlike the fixed budget

which is based upon judgement, assumptions and estimates.

Disadvantages:

This budget interrupt the discipline and increase the chances of cheating within the

organization as it avoid the rigidity. It may be time-consuming as it needs estimation for various levels which is a prime

factor at the time of budget preparation.

Capital Budget: Capital budget is related with the estimated revenues and expenses

which may be affected by the capital investments. All the aspects related with capital such as

long term loans, investments, share allotment and forfeiture, purchase and sale of assets, bonds

and debentures are covered in capital budget (Ismail and King, 2014). KEF LTD uses this budget

to calculate payback period, ARR, IRR, capital employed, ROI, etc.

Advantages:

This budget helps the management in making decisions related investments and maintain

the liquidity of the company. It also assists the management to evaluate the risk factor in any decision or activity.

Disadvantages:

Preparation of these kind of budget demands skills and professionalism which may be

expensive for the firm. All the techniques used in this budget are based on assumptions and future events are

always uncertain which increases the risk factor.

Implications: for instance KEF Ltd has two investment proposal A and B with same initial

investment but different cash flows. In this regard, by applying investment appraisal tool

decision can be taken for the selection or rejection of proposal.

Project A

Computation of NPV

Year Cash inflows (in £)

PV

factor

@

10%

Discounted

cash inflows

(in £)

1 45000 0.909 40909.09091

2 58000 0.826 47934

3 52000 0.751 39068

4 66000 0.683 45079

5 78000 0.621 48432

Total discounted cash inflow 221422

Initial investment 190000

NPV (Total discounted cash inflows - initial

investment) 31422

Project B

Computation of NPV

Year Cash inflows (in £)

PV

factor

@

10%

Discounted

cash inflows

(in £)

1 47000 0.909 42727.27273

2 62000 0.826 51240

3 58000 0.751 43576

4 72000 0.683 49177

5 84000 0.621 52157

Total discounted cash inflow 238878

Initial investment 190000

NPV (Total discounted cash inflows - initial

investment) 48878

By applying investment appraisal tool on data set it has identified that KEF Ltd should

invest funds in project B over A which in turn proves to be more beneficial for it. Moreover, as

Computation of NPV

Year Cash inflows (in £)

PV

factor

@

10%

Discounted

cash inflows

(in £)

1 45000 0.909 40909.09091

2 58000 0.826 47934

3 52000 0.751 39068

4 66000 0.683 45079

5 78000 0.621 48432

Total discounted cash inflow 221422

Initial investment 190000

NPV (Total discounted cash inflows - initial

investment) 31422

Project B

Computation of NPV

Year Cash inflows (in £)

PV

factor

@

10%

Discounted

cash inflows

(in £)

1 47000 0.909 42727.27273

2 62000 0.826 51240

3 58000 0.751 43576

4 72000 0.683 49177

5 84000 0.621 52157

Total discounted cash inflow 238878

Initial investment 190000

NPV (Total discounted cash inflows - initial

investment) 48878

By applying investment appraisal tool on data set it has identified that KEF Ltd should

invest funds in project B over A which in turn proves to be more beneficial for it. Moreover, as

per NPV Assessment Company will generate higher return in monetary by investing money in

project B.

In this way, capital budgeting method facilitates selection of best project out of several

alternatives available.

Pricing: For fulfilling objective pertaining to profit attainment business unit is required to set

appropriate prices for the products or services offered. Hence, by taking into account below

mentioned methods KEF LTD can set competent prices for the offerings. Cost-plus pricing: According to this, by adding mark-up in unit cost calculated price can

be determined by the firm for offerings. For instance: Unit cost of the product is £50 and

company wants to attain 15% mark-up then price will be determined in the following

manner:

Price = Unit cost + (Unit cost * profit %)

Price = 50 + (50 * 15%)

= 50 + 7.5

=£57.5 or 58 Competitive pricing: In accordance with this framework, to remain competitive at

marketplace, KEF Ltd can set prices of the products or services in line with the rivals.

Through this, firm can get enough profit by influencing decision making of customers.

Penetration pricing: KEF LTD can set lower prices initially for attracting large number

of customers. Once, customer loyalty has been built regarding services then firm can

generate profit by increasing prices.

Along with this, pricing decisions are also highly influence from the aspects of supply and

demand. Usually, demand for the product increases when prices are lower and vice versa.

Further, in the case of low supply price tends to higher comparatively. Thus, at the time of

setting prices management team of KEF LTD should keep in mind demand and supply related

aspects.

M3 Use of planning tools and their application in forecasting budgets:

Managerial accounting process provides material data and information to the

administration so that it can make plans and decision effectively in order to achieve

organizational goals. For this purpose, it has developed some planning tools which are known as

budgets. Various kind of budgets such as cash budget, capital budget, operating budget, fixed

project B.

In this way, capital budgeting method facilitates selection of best project out of several

alternatives available.

Pricing: For fulfilling objective pertaining to profit attainment business unit is required to set

appropriate prices for the products or services offered. Hence, by taking into account below

mentioned methods KEF LTD can set competent prices for the offerings. Cost-plus pricing: According to this, by adding mark-up in unit cost calculated price can

be determined by the firm for offerings. For instance: Unit cost of the product is £50 and

company wants to attain 15% mark-up then price will be determined in the following

manner:

Price = Unit cost + (Unit cost * profit %)

Price = 50 + (50 * 15%)

= 50 + 7.5

=£57.5 or 58 Competitive pricing: In accordance with this framework, to remain competitive at

marketplace, KEF Ltd can set prices of the products or services in line with the rivals.

Through this, firm can get enough profit by influencing decision making of customers.

Penetration pricing: KEF LTD can set lower prices initially for attracting large number

of customers. Once, customer loyalty has been built regarding services then firm can

generate profit by increasing prices.

Along with this, pricing decisions are also highly influence from the aspects of supply and

demand. Usually, demand for the product increases when prices are lower and vice versa.

Further, in the case of low supply price tends to higher comparatively. Thus, at the time of

setting prices management team of KEF LTD should keep in mind demand and supply related

aspects.

M3 Use of planning tools and their application in forecasting budgets:

Managerial accounting process provides material data and information to the

administration so that it can make plans and decision effectively in order to achieve

organizational goals. For this purpose, it has developed some planning tools which are known as

budgets. Various kind of budgets such as cash budget, capital budget, operating budget, fixed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgets, flexible budgets, zero-based budget, etc. assist the management for forecasting

standards appropriately so that valuable resources of the company can be used effectively (Kale

and Carroll, 2016). The management of KEF LTD follows budgetary control techniques in order

to forecast the budget figures to measure them with accurately which ultimately helps in making

adequate decisions and increase the profitability of the company.

TASK 4

P5 Management accounting techniques used to identify financial problems:

Financial Problems: Financial problems can be defined as monetary or fund related

issues (McCrory and et.al, 2015). Some of the issues which are being faced by the respective

company are presented as under:

Late payment from customers: Now a days, organizations relies on credit term business

very much and that is why they have to sell their products and services on credit basis to their

customers. Sometimes customers, intentionally or unintentionally, fail to pay their due amount

on time which is known as delayed payment from debtors. It may cause a huge issue for the

manufacturing firms such as KEF LTD if it becomes a regular practise for the customers.

Key performance indicators: Key performance indicators which are also known as KPI are the

indicators that measures the performance of the establishment. These indicators are used for

measuring the efficiency of both financial as well as non-financial operations. This planning tool

is used to focus on the high performing activities which lead toward the achievement of main

objectives of the entire firm (Melitski and Manoharan, 2014). These indicators are mostly used

by the upper management which is responsible for solving major issues such as finance. The

upper management of the KEF LTD uses these indicators to identify the financial issues such as

unforeseen expenses and economic cycle as these are the major issues for any organization. In

that company have to motivate their employees by giving support to them and also use

appropriate techniques to achieve goals. This method is important to company to achieve success

by solving problems of company in an effective manner.

Benchmarking: Benchmarking is a process of setting some measurements and guidelines for

each operation and employee as well so that the set objectives may be achieved conveniently and

on time. In benchmarking process, the management analyse the strategies and working process

of those which are the best in the industry or sector and apply the procedure and standards within

the firm (Mohamed, Kerosi and Tirimba, 2016). With the help of this technique, the

standards appropriately so that valuable resources of the company can be used effectively (Kale

and Carroll, 2016). The management of KEF LTD follows budgetary control techniques in order

to forecast the budget figures to measure them with accurately which ultimately helps in making

adequate decisions and increase the profitability of the company.

TASK 4

P5 Management accounting techniques used to identify financial problems:

Financial Problems: Financial problems can be defined as monetary or fund related

issues (McCrory and et.al, 2015). Some of the issues which are being faced by the respective

company are presented as under:

Late payment from customers: Now a days, organizations relies on credit term business

very much and that is why they have to sell their products and services on credit basis to their

customers. Sometimes customers, intentionally or unintentionally, fail to pay their due amount

on time which is known as delayed payment from debtors. It may cause a huge issue for the

manufacturing firms such as KEF LTD if it becomes a regular practise for the customers.

Key performance indicators: Key performance indicators which are also known as KPI are the

indicators that measures the performance of the establishment. These indicators are used for

measuring the efficiency of both financial as well as non-financial operations. This planning tool

is used to focus on the high performing activities which lead toward the achievement of main

objectives of the entire firm (Melitski and Manoharan, 2014). These indicators are mostly used

by the upper management which is responsible for solving major issues such as finance. The

upper management of the KEF LTD uses these indicators to identify the financial issues such as

unforeseen expenses and economic cycle as these are the major issues for any organization. In

that company have to motivate their employees by giving support to them and also use

appropriate techniques to achieve goals. This method is important to company to achieve success

by solving problems of company in an effective manner.

Benchmarking: Benchmarking is a process of setting some measurements and guidelines for

each operation and employee as well so that the set objectives may be achieved conveniently and

on time. In benchmarking process, the management analyse the strategies and working process

of those which are the best in the industry or sector and apply the procedure and standards within

the firm (Mohamed, Kerosi and Tirimba, 2016). With the help of this technique, the

administration of KEF LTD is able to standardise its credit term policies and liquidity position

which helps in find out the problems of delayed payments from customers and weak fund

management. The bench marking policy is another important aspects which is help for solve this

problem by setting planning phase by considering research of products and services through

examining the competitors in the market place.

Balanced scorecard:

This is effective and best is a performance metric used in strategic management to

identify and improve various internal functions of a business and their resulting external

outcomes. That is used to measures and provide feedbacks to organization. This helps in future

in order to solve any issues and conditions which will faced by company. This helps to company

for build strategic planning and management system, by aligning shared vision of success and

get people working on the right things and focusing on results. This effectively provide feedback

to company for solving those problems in proper manner as per vision of company.

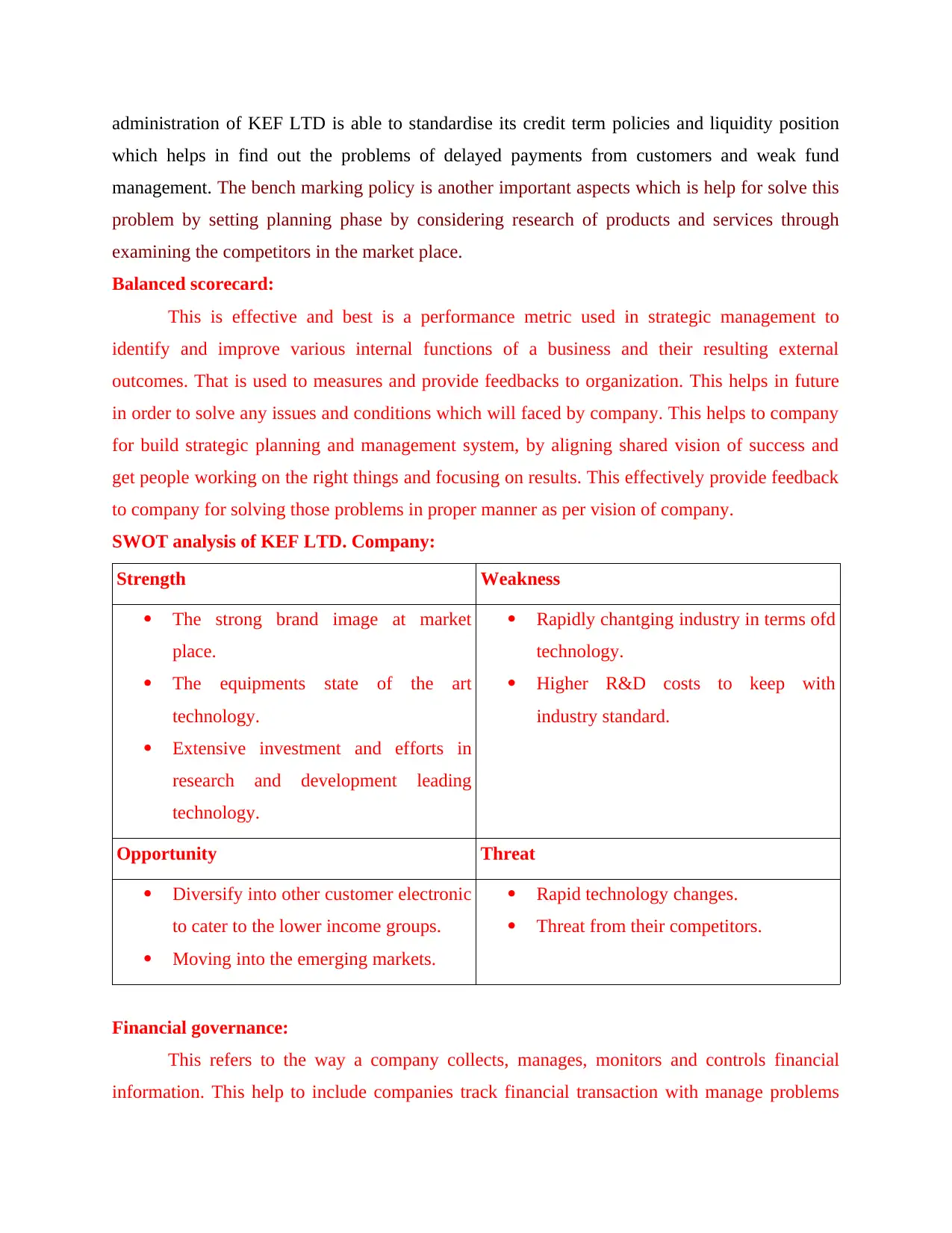

SWOT analysis of KEF LTD. Company:

Strength Weakness

The strong brand image at market

place.

The equipments state of the art

technology.

Extensive investment and efforts in

research and development leading

technology.

Rapidly chantging industry in terms ofd

technology.

Higher R&D costs to keep with

industry standard.

Opportunity Threat

Diversify into other customer electronic

to cater to the lower income groups.

Moving into the emerging markets.

Rapid technology changes.

Threat from their competitors.

Financial governance:

This refers to the way a company collects, manages, monitors and controls financial

information. This help to include companies track financial transaction with manage problems

which helps in find out the problems of delayed payments from customers and weak fund

management. The bench marking policy is another important aspects which is help for solve this

problem by setting planning phase by considering research of products and services through

examining the competitors in the market place.

Balanced scorecard:

This is effective and best is a performance metric used in strategic management to

identify and improve various internal functions of a business and their resulting external

outcomes. That is used to measures and provide feedbacks to organization. This helps in future

in order to solve any issues and conditions which will faced by company. This helps to company

for build strategic planning and management system, by aligning shared vision of success and

get people working on the right things and focusing on results. This effectively provide feedback

to company for solving those problems in proper manner as per vision of company.

SWOT analysis of KEF LTD. Company:

Strength Weakness

The strong brand image at market

place.

The equipments state of the art

technology.

Extensive investment and efforts in

research and development leading

technology.

Rapidly chantging industry in terms ofd

technology.

Higher R&D costs to keep with

industry standard.

Opportunity Threat

Diversify into other customer electronic

to cater to the lower income groups.

Moving into the emerging markets.

Rapid technology changes.

Threat from their competitors.

Financial governance:

This refers to the way a company collects, manages, monitors and controls financial

information. This help to include companies track financial transaction with manage problems

performance and control the data and operations. This help to manage this problem by using

research of market by using proper rules and regulations.

Management skills:

There are various management skills which are helpful for manage work properly in the

proper manner. Those management skills are planning, communication and decision-making.

This help to solve problems by making proper planning and communicate proper strategy in the

proper manner.

Strategic planning:

Here, is use proper and effective strategic planning which is KPIs and Benchmarking.

Those are helpful for check the mistake and make senses of work in a proper manner.

M4 Analysis of how management accounting can lead an organisation to sustainable success:

Management accounting plays an important role in solving financial difficulties and

getting and holding sustainable success and that can be understood with below given points This

accounting process renders various planning tools such as reports and budgets which aids the

administration in forecasting and planning profitable objectives for the success of whole

organization (Popesko, Papadaki and Novák, 2015).

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:

The strategic planning tools used by managerial accountants, are very utile in

determination of financial troubles. The budgetary planning tools such as capital and cash budget

are assistive in rendering information regarding investing and financial difficulties that may grow

in the establishment within a particular period and techniques like Key Performance Indicators

technique and benchmarking method are the best ways in distinguishing external as well as

internal manageable financial factors (Paul, Sarker and Essam, 2014). With the assistance of

managerial accounting methods such as corporate and financial governance, the monetary

problems can be detected before they take place and increase hugely and effective steps such as

following accounting principles and standards, applying provisions, etc. may be taken on time so

that KEF LTD may achieve sustainable success.

research of market by using proper rules and regulations.

Management skills:

There are various management skills which are helpful for manage work properly in the

proper manner. Those management skills are planning, communication and decision-making.

This help to solve problems by making proper planning and communicate proper strategy in the

proper manner.

Strategic planning:

Here, is use proper and effective strategic planning which is KPIs and Benchmarking.

Those are helpful for check the mistake and make senses of work in a proper manner.

M4 Analysis of how management accounting can lead an organisation to sustainable success:

Management accounting plays an important role in solving financial difficulties and

getting and holding sustainable success and that can be understood with below given points This

accounting process renders various planning tools such as reports and budgets which aids the

administration in forecasting and planning profitable objectives for the success of whole

organization (Popesko, Papadaki and Novák, 2015).

D3 Planning tools respond appropriately to solving financial problems to lead organisations to

sustainable success:

The strategic planning tools used by managerial accountants, are very utile in

determination of financial troubles. The budgetary planning tools such as capital and cash budget

are assistive in rendering information regarding investing and financial difficulties that may grow

in the establishment within a particular period and techniques like Key Performance Indicators

technique and benchmarking method are the best ways in distinguishing external as well as

internal manageable financial factors (Paul, Sarker and Essam, 2014). With the assistance of

managerial accounting methods such as corporate and financial governance, the monetary

problems can be detected before they take place and increase hugely and effective steps such as

following accounting principles and standards, applying provisions, etc. may be taken on time so

that KEF LTD may achieve sustainable success.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

With the above described report, it can be concluded that management accounting is a

process which is used by the internal stakeholders, specially the managers to generate such

material information and reports that may assist them for strategic planning and impressive

decision making. For this purpose, various tools, techniques, methods and frameworks are used

by the managerial accountants such as various accounting systems to generate reports, budgets,

budgetary control, financial governing tools like KPIs and benchmarking, etc. All of them assist

the administration to forecast future plans, prepare policies and policies, issuing guidelines,

measuring the performance and take remedial actions.

With the above described report, it can be concluded that management accounting is a

process which is used by the internal stakeholders, specially the managers to generate such

material information and reports that may assist them for strategic planning and impressive

decision making. For this purpose, various tools, techniques, methods and frameworks are used

by the managerial accountants such as various accounting systems to generate reports, budgets,

budgetary control, financial governing tools like KPIs and benchmarking, etc. All of them assist

the administration to forecast future plans, prepare policies and policies, issuing guidelines,

measuring the performance and take remedial actions.

REFERENCES

Books and Journals

Cuzzocrea, A. and et.al, 2018. An innovative framework for supporting big atmospheric data

analytics via clustering-based spatio-temporal analysis. Journal of Ambient Intelligence

and Humanized Computing. pp.1-16.

Eckardt, G., Selen, W. and Wynder, M., 2015. Recognising the effects of costing assumptions in

educational business simulation games. e-Journal of Business Education and

Scholarship of Teaching. 9(1). pp.43-60.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Giannarakis, G., Konteos, G. and Sariannidis, N., 2014. Financial, governance and

environmental determinants of corporate social responsible disclosure. Management

Decision. 52(10). pp.1928-1951.

Hirsch, B., Seubert, A. and Sohn, M., 2015. Visualisation of data in management accounting

reports: How supplementary graphs improve every-day management

judgments. Journal of Applied Accounting Research. 16(2). pp.221-239.

Hoozée, S. and Ngo, Q. H., 2018. The impact of managers’ participation in costing system

design on their perceived contributions to process improvement. European Accounting

Review. 27(4). pp.747-770.

Ismail, N. A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2). pp.1-20.

Kale, H. P. and Carroll, N. V., 2016. Self‐reported financial burden of cancer care and its effect

on physical and mental health‐related quality of life among US cancer

survivors. Cancer. 122(8). pp.283-289.

McCrory, C. C. and et.al, 2015. Benchmarking hydrogen evolving reaction and oxygen evolving

reaction electrocatalysts for solar water splitting devices. Journal of the American

Chemical Society. 137(13). pp.4347-4357.

Melitski, J. and Manoharan, A., 2014. Performance measurement, accountability, and

transparency of budgets and financial reports. Public Administration Quarterly. pp.38-

70.

Mohamed, I. A., Kerosi, E. and Tirimba, O. I., 2016. Analysis of the Effectiveness of Budgetary

Control Techniques on Organizational Performance at DaraSalaam Bank Headquarters

in Hargeisa Somaliland.

Paul, S. K., Sarker, R. and Essam, D., 2014. Real time disruption management for a two-stage

batch production–inventory system with reliability considerations. European Journal of

Operational Research. 237(1). pp.113-128.

Popesko, B., Papadaki, Š. and Novák, P., 2015. Cost and reimbursement analysis of selected

hospital diagnoses via activity-based costing. E+ M Ekonomie a Management.

Ríos, A. M., Bastida, F. and Benito, B., 2016. Budget transparency and legislative budgetary

oversight: An international approach. The American Review of Public

Administration. 46(5). pp.546-568.

Books and Journals

Cuzzocrea, A. and et.al, 2018. An innovative framework for supporting big atmospheric data

analytics via clustering-based spatio-temporal analysis. Journal of Ambient Intelligence

and Humanized Computing. pp.1-16.

Eckardt, G., Selen, W. and Wynder, M., 2015. Recognising the effects of costing assumptions in

educational business simulation games. e-Journal of Business Education and

Scholarship of Teaching. 9(1). pp.43-60.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Giannarakis, G., Konteos, G. and Sariannidis, N., 2014. Financial, governance and

environmental determinants of corporate social responsible disclosure. Management

Decision. 52(10). pp.1928-1951.

Hirsch, B., Seubert, A. and Sohn, M., 2015. Visualisation of data in management accounting

reports: How supplementary graphs improve every-day management

judgments. Journal of Applied Accounting Research. 16(2). pp.221-239.

Hoozée, S. and Ngo, Q. H., 2018. The impact of managers’ participation in costing system

design on their perceived contributions to process improvement. European Accounting

Review. 27(4). pp.747-770.

Ismail, N. A. and King, M., 2014. Factors influencing the alignment of accounting information

systems in small and medium sized Malaysian manufacturing firms. Journal of

Information Systems and Small Business. 1(1-2). pp.1-20.

Kale, H. P. and Carroll, N. V., 2016. Self‐reported financial burden of cancer care and its effect

on physical and mental health‐related quality of life among US cancer

survivors. Cancer. 122(8). pp.283-289.

McCrory, C. C. and et.al, 2015. Benchmarking hydrogen evolving reaction and oxygen evolving

reaction electrocatalysts for solar water splitting devices. Journal of the American

Chemical Society. 137(13). pp.4347-4357.

Melitski, J. and Manoharan, A., 2014. Performance measurement, accountability, and

transparency of budgets and financial reports. Public Administration Quarterly. pp.38-

70.

Mohamed, I. A., Kerosi, E. and Tirimba, O. I., 2016. Analysis of the Effectiveness of Budgetary

Control Techniques on Organizational Performance at DaraSalaam Bank Headquarters

in Hargeisa Somaliland.

Paul, S. K., Sarker, R. and Essam, D., 2014. Real time disruption management for a two-stage

batch production–inventory system with reliability considerations. European Journal of

Operational Research. 237(1). pp.113-128.

Popesko, B., Papadaki, Š. and Novák, P., 2015. Cost and reimbursement analysis of selected

hospital diagnoses via activity-based costing. E+ M Ekonomie a Management.

Ríos, A. M., Bastida, F. and Benito, B., 2016. Budget transparency and legislative budgetary

oversight: An international approach. The American Review of Public

Administration. 46(5). pp.546-568.

Sledgianowski, D., Gomaa, M. and Tan, C., 2017. Toward integration of Big Data, technology

and information systems competencies into the accounting curriculum. Journal of

Accounting Education. 38. pp.81-93.

Wang, F. and et.al, 2017. Multi-objective optimization model of source–load–storage synergetic

dispatch for a building energy management system based on TOU price demand

response. IEEE Transactions on Industry Applications. 54(2). pp.1017-1028.

Yin, S. and et.al, 2015. An improved incremental learning approach for KPI prognosis of

dynamic fuel cell system. IEEE transactions on cybernetics. 46(12). pp.3135-3144.

Online:

Marginal and absorption costing, 2017. Available through

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>

and information systems competencies into the accounting curriculum. Journal of

Accounting Education. 38. pp.81-93.

Wang, F. and et.al, 2017. Multi-objective optimization model of source–load–storage synergetic

dispatch for a building energy management system based on TOU price demand

response. IEEE Transactions on Industry Applications. 54(2). pp.1017-1028.

Yin, S. and et.al, 2015. An improved incremental learning approach for KPI prognosis of

dynamic fuel cell system. IEEE transactions on cybernetics. 46(12). pp.3135-3144.

Online:

Marginal and absorption costing, 2017. Available through

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.