Management Accounting Report: KEF LTD Financial Analysis

VerifiedAdded on 2023/01/03

|16

|4594

|63

Report

AI Summary

This report delves into the core concepts of management accounting, emphasizing its role in strategic decision-making for companies like KEF LTD. It covers diverse management accounting systems such as inventory management, cost accounting, job costing, and price optimization, highlighting their benefits. The report also explores different types of management accounting reports, including budget studies, cost analyses, performance reports, and receivable aging reports. Furthermore, it examines a range of management accounting techniques, such as absorption costing and marginal costing, providing income statements and reconciliation statements. The report also discusses planning tools used in management accounting, such as flexible budgets. Overall, the report offers a detailed analysis of management accounting's applications and techniques within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................6

P3. Range of management accounting techniques......................................................................6

TASK 3..........................................................................................................................................10

P4.Planning tools used in management accounting...................................................................10

TASK 4..........................................................................................................................................12

P5. Comparison of organisations adapting management accounting to respond to financial

problems....................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................6

P3. Range of management accounting techniques......................................................................6

TASK 3..........................................................................................................................................10

P4.Planning tools used in management accounting...................................................................10

TASK 4..........................................................................................................................................12

P5. Comparison of organisations adapting management accounting to respond to financial

problems....................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

Introduction

The today's market condition demands an appropriate technical management style which can

track the company's valuable operation to increase the competitiveness of companies (Collis and

Hussey, 2017). Management accounting is characterised as an essential method in which useful

financial information may, for the purpose of reaching a strategic decision by the Manager of

certain organisations to maximise income over a particular time span is measured, tracked and

managed. The entire expenditures or budgetary control process starts when the valuable

company financial information is gathered, processed, recorded, calculated, assessed and

circulated, which leads in such a predetermined period to the achieving goals required. KEF

LTD, a manufacturing corporation, is selected to help illustrate the purpose of accounting

management. This study reveals a knowledge of many systems and studies, calculates the

outgoing costs per unit, P&L accounts over the budget duration, etc. by helpful assessment

models. The research further discusses use of such various methods for predicting operational

efficiency as well as how various perspectives can better facilitate the organisation approach.

TASK 1

P1. Different type of management accounting system

The concepts of MA are understood to be unique to each company and make it easy for the

overall production of different classes within the organization to be measured or assessed.

Supervisors usually set performance evaluation criteria by reviewing various methodologies

which facilitate the achievement of defined objectives and also help to provide true explanation

for differences in the actual schedule (Schaltegger, Burritt and Petersen, 2017). MA usually

offers non-financial and also financial proof to the managers and now all operational staff to

produce the most suitable decisions for optimising sales, productivity and meeting goals.

Managing financial statements sponsored KEF Ltd leadership have indeed been various

significant, and are described below:

Inventory management system: This software provides supplies of handle firms, goods

transacted and the finished commodity in the appropriate amounts. There are alternative

techniques like FIFO, LIFO and Average for controlling financial assets that give the process

management trust. KEF Ltd follows the FIFO approach, but old products must be eliminated

with this methodology and therefore losses due to faulty products must be minimised. To start

The today's market condition demands an appropriate technical management style which can

track the company's valuable operation to increase the competitiveness of companies (Collis and

Hussey, 2017). Management accounting is characterised as an essential method in which useful

financial information may, for the purpose of reaching a strategic decision by the Manager of

certain organisations to maximise income over a particular time span is measured, tracked and

managed. The entire expenditures or budgetary control process starts when the valuable

company financial information is gathered, processed, recorded, calculated, assessed and

circulated, which leads in such a predetermined period to the achieving goals required. KEF

LTD, a manufacturing corporation, is selected to help illustrate the purpose of accounting

management. This study reveals a knowledge of many systems and studies, calculates the

outgoing costs per unit, P&L accounts over the budget duration, etc. by helpful assessment

models. The research further discusses use of such various methods for predicting operational

efficiency as well as how various perspectives can better facilitate the organisation approach.

TASK 1

P1. Different type of management accounting system

The concepts of MA are understood to be unique to each company and make it easy for the

overall production of different classes within the organization to be measured or assessed.

Supervisors usually set performance evaluation criteria by reviewing various methodologies

which facilitate the achievement of defined objectives and also help to provide true explanation

for differences in the actual schedule (Schaltegger, Burritt and Petersen, 2017). MA usually

offers non-financial and also financial proof to the managers and now all operational staff to

produce the most suitable decisions for optimising sales, productivity and meeting goals.

Managing financial statements sponsored KEF Ltd leadership have indeed been various

significant, and are described below:

Inventory management system: This software provides supplies of handle firms, goods

transacted and the finished commodity in the appropriate amounts. There are alternative

techniques like FIFO, LIFO and Average for controlling financial assets that give the process

management trust. KEF Ltd follows the FIFO approach, but old products must be eliminated

with this methodology and therefore losses due to faulty products must be minimised. To start

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with, KEF Ltd allows manufacturing goods that serve markets and consumers, while maximising

benefit.

Cost accounting system: this will be used to evaluate the cost of the very same net

production of the goods of a particular business. It generally includes gross costs on various

occasions, requiring even fixed costs to help assess the profit. There are comparable financial

techniques like median cost and fixed cost, lean charging, activity and a daily expense method.

Throughout the respective business, the ABC stock estimation approach is applied, primarily

assigning total costs for products marketing and product (Humphrey and Miller, 2012).

Job Coasting system: the expense of delivering efficient governance in the business is

mostly understood in this strategy. The product manager and auditor have evidence of each type

of product, and it allows manufacturing costs to be passed to each other commodity. This method

therefore facilitates the measurement during the same duration of the expense of the various

goods manufactured by the firm. This method therefore allows in KEF Ltd to determine and

predict the expense of various goods of valuable firms to satisfy customer demand.

Price optimization method: this is considered the largest system of the business as it aims

to recognise the customers' reaction to the firm's set production revenue volumes. Managers are

being used to set respectable retail prices that can satisfy consumers and raise profits. KEF Ltd

targets at providing the highest import pricing in terms of overcharge cognitive impairment and

enticing customers to maximum profit.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It helps organisations to use available goods and services

to meet particular goals.

This approach facilitates a thorough monitoring of the

current inventory and certain requests of suppliers so as to

increase profitability (Holsapple, 2013).

Job Costing system This approach provides reasonable stability in estimating

and mitigating costs for single employees of KEF Ltd.

Workers performance records are kept to prepare for the

benefit.

Cost accounting system: this will be used to evaluate the cost of the very same net

production of the goods of a particular business. It generally includes gross costs on various

occasions, requiring even fixed costs to help assess the profit. There are comparable financial

techniques like median cost and fixed cost, lean charging, activity and a daily expense method.

Throughout the respective business, the ABC stock estimation approach is applied, primarily

assigning total costs for products marketing and product (Humphrey and Miller, 2012).

Job Coasting system: the expense of delivering efficient governance in the business is

mostly understood in this strategy. The product manager and auditor have evidence of each type

of product, and it allows manufacturing costs to be passed to each other commodity. This method

therefore facilitates the measurement during the same duration of the expense of the various

goods manufactured by the firm. This method therefore allows in KEF Ltd to determine and

predict the expense of various goods of valuable firms to satisfy customer demand.

Price optimization method: this is considered the largest system of the business as it aims

to recognise the customers' reaction to the firm's set production revenue volumes. Managers are

being used to set respectable retail prices that can satisfy consumers and raise profits. KEF Ltd

targets at providing the highest import pricing in terms of overcharge cognitive impairment and

enticing customers to maximum profit.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It helps organisations to use available goods and services

to meet particular goals.

This approach facilitates a thorough monitoring of the

current inventory and certain requests of suppliers so as to

increase profitability (Holsapple, 2013).

Job Costing system This approach provides reasonable stability in estimating

and mitigating costs for single employees of KEF Ltd.

Workers performance records are kept to prepare for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required adjustments with the help of such a operating

system.

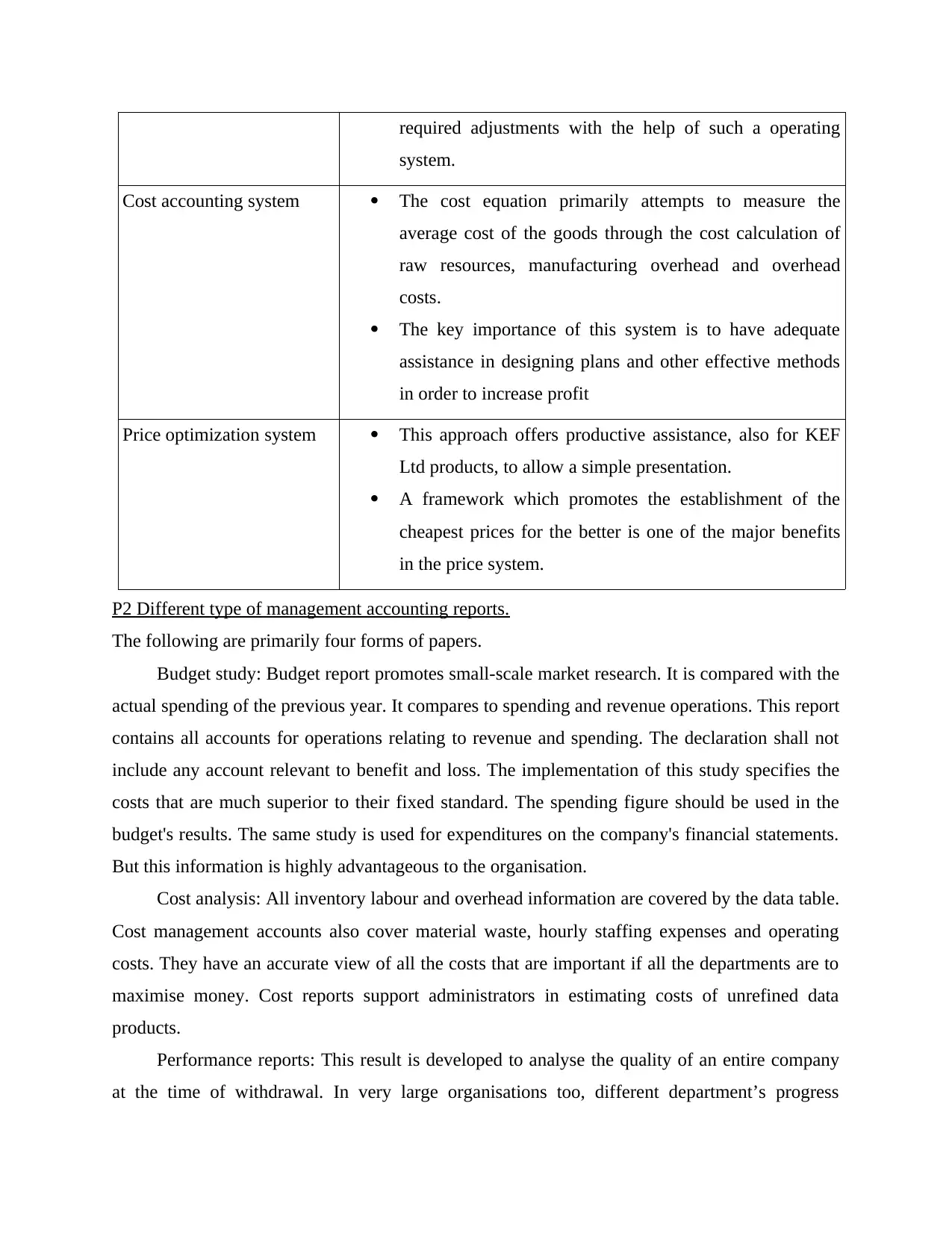

Cost accounting system The cost equation primarily attempts to measure the

average cost of the goods through the cost calculation of

raw resources, manufacturing overhead and overhead

costs.

The key importance of this system is to have adequate

assistance in designing plans and other effective methods

in order to increase profit

Price optimization system This approach offers productive assistance, also for KEF

Ltd products, to allow a simple presentation.

A framework which promotes the establishment of the

cheapest prices for the better is one of the major benefits

in the price system.

P2 Different type of management accounting reports.

The following are primarily four forms of papers.

Budget study: Budget report promotes small-scale market research. It is compared with the

actual spending of the previous year. It compares to spending and revenue operations. This report

contains all accounts for operations relating to revenue and spending. The declaration shall not

include any account relevant to benefit and loss. The implementation of this study specifies the

costs that are much superior to their fixed standard. The spending figure should be used in the

budget's results. The same study is used for expenditures on the company's financial statements.

But this information is highly advantageous to the organisation.

Cost analysis: All inventory labour and overhead information are covered by the data table.

Cost management accounts also cover material waste, hourly staffing expenses and operating

costs. They have an accurate view of all the costs that are important if all the departments are to

maximise money. Cost reports support administrators in estimating costs of unrefined data

products.

Performance reports: This result is developed to analyse the quality of an entire company

at the time of withdrawal. In very large organisations too, different department’s progress

system.

Cost accounting system The cost equation primarily attempts to measure the

average cost of the goods through the cost calculation of

raw resources, manufacturing overhead and overhead

costs.

The key importance of this system is to have adequate

assistance in designing plans and other effective methods

in order to increase profit

Price optimization system This approach offers productive assistance, also for KEF

Ltd products, to allow a simple presentation.

A framework which promotes the establishment of the

cheapest prices for the better is one of the major benefits

in the price system.

P2 Different type of management accounting reports.

The following are primarily four forms of papers.

Budget study: Budget report promotes small-scale market research. It is compared with the

actual spending of the previous year. It compares to spending and revenue operations. This report

contains all accounts for operations relating to revenue and spending. The declaration shall not

include any account relevant to benefit and loss. The implementation of this study specifies the

costs that are much superior to their fixed standard. The spending figure should be used in the

budget's results. The same study is used for expenditures on the company's financial statements.

But this information is highly advantageous to the organisation.

Cost analysis: All inventory labour and overhead information are covered by the data table.

Cost management accounts also cover material waste, hourly staffing expenses and operating

costs. They have an accurate view of all the costs that are important if all the departments are to

maximise money. Cost reports support administrators in estimating costs of unrefined data

products.

Performance reports: This result is developed to analyse the quality of an entire company

at the time of withdrawal. In very large organisations too, different department’s progress

statements are prepared. Managers make critical decisions about the growth of the industry using

these success reports. Individuals are also rewarded to the Company for their contribution and

are fired off or processed as necessary by performers. Management accounting reviews on results

often provide a deep glimpse into some kind of company's operations. If companies conclude

that the company must do so but that does not, these documents will point out that the

management of a company to defect in the schedule. The task of performance reviews is

important for every organisation to maintain a detailed measure of its project strategy.

Receivable Aging Reports: Monitoring business AR ageing in daily rates Weekly/monthly

lets businesses detect problems before becoming a corporate cash flow problem. This is a

monthly audit, which classifies the finances of a corporation by the span of an invoice. It is used

as a tool to assess consumers' financial wellbeing. When a single client pays late, the company

will assess the terms of service of payments and make appropriate adjustments. That also lets the

organisation keep the supply of products/services before the buyer spends the price on a set due

date.

In order to obtain the desired outcome, the management most valuable knowledge is to

evaluate the actual activity of the organisation as well as the net income and cost produced on

these activities. The internal administrators, who are often concerned to make significant plans to

improve market efficiency and intend to raise revenues, are often needed to include this valuable

details. The information gathered is important on a daily basis primarily at the end of a busy day

in order for management to assess the overall efficiency and the areas needed for potential

progress. The key sources of knowledge are the daily briefing by the internal employees and the

administrators are active in various external operations.

TASK 2

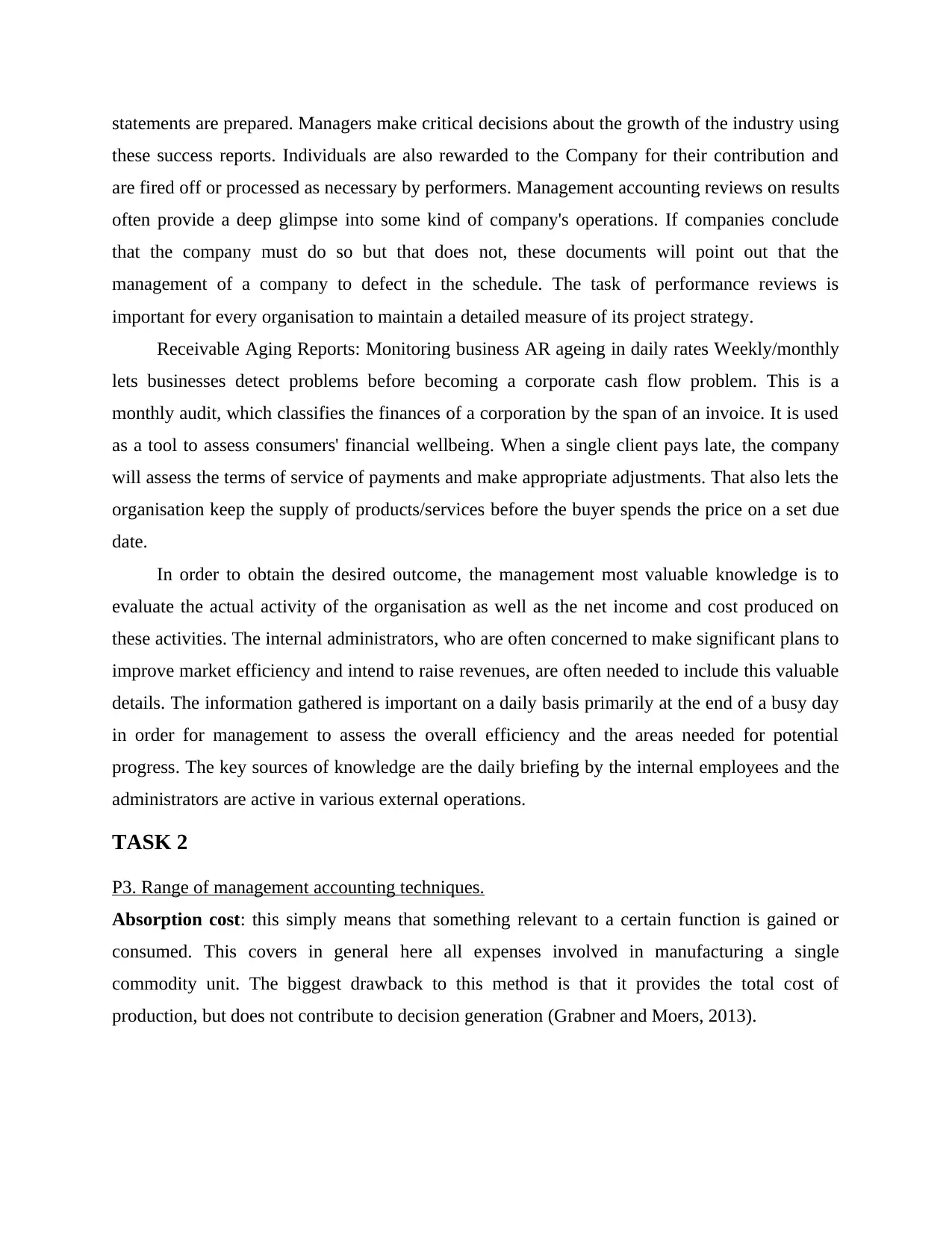

P3. Range of management accounting techniques.

Absorption cost: this simply means that something relevant to a certain function is gained or

consumed. This covers in general here all expenses involved in manufacturing a single

commodity unit. The biggest drawback to this method is that it provides the total cost of

production, but does not contribute to decision generation (Grabner and Moers, 2013).

these success reports. Individuals are also rewarded to the Company for their contribution and

are fired off or processed as necessary by performers. Management accounting reviews on results

often provide a deep glimpse into some kind of company's operations. If companies conclude

that the company must do so but that does not, these documents will point out that the

management of a company to defect in the schedule. The task of performance reviews is

important for every organisation to maintain a detailed measure of its project strategy.

Receivable Aging Reports: Monitoring business AR ageing in daily rates Weekly/monthly

lets businesses detect problems before becoming a corporate cash flow problem. This is a

monthly audit, which classifies the finances of a corporation by the span of an invoice. It is used

as a tool to assess consumers' financial wellbeing. When a single client pays late, the company

will assess the terms of service of payments and make appropriate adjustments. That also lets the

organisation keep the supply of products/services before the buyer spends the price on a set due

date.

In order to obtain the desired outcome, the management most valuable knowledge is to

evaluate the actual activity of the organisation as well as the net income and cost produced on

these activities. The internal administrators, who are often concerned to make significant plans to

improve market efficiency and intend to raise revenues, are often needed to include this valuable

details. The information gathered is important on a daily basis primarily at the end of a busy day

in order for management to assess the overall efficiency and the areas needed for potential

progress. The key sources of knowledge are the daily briefing by the internal employees and the

administrators are active in various external operations.

TASK 2

P3. Range of management accounting techniques.

Absorption cost: this simply means that something relevant to a certain function is gained or

consumed. This covers in general here all expenses involved in manufacturing a single

commodity unit. The biggest drawback to this method is that it provides the total cost of

production, but does not contribute to decision generation (Grabner and Moers, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Costing margin: it is defined by the added costs incurred by businesses in order to purchase an

extra factor to maximise performance. Throughout this cost accounting only variable costs are

included, although now operating costs are calculated against investments.

The income statements of Capital Joinery Ltd by using both the methods are shown below:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

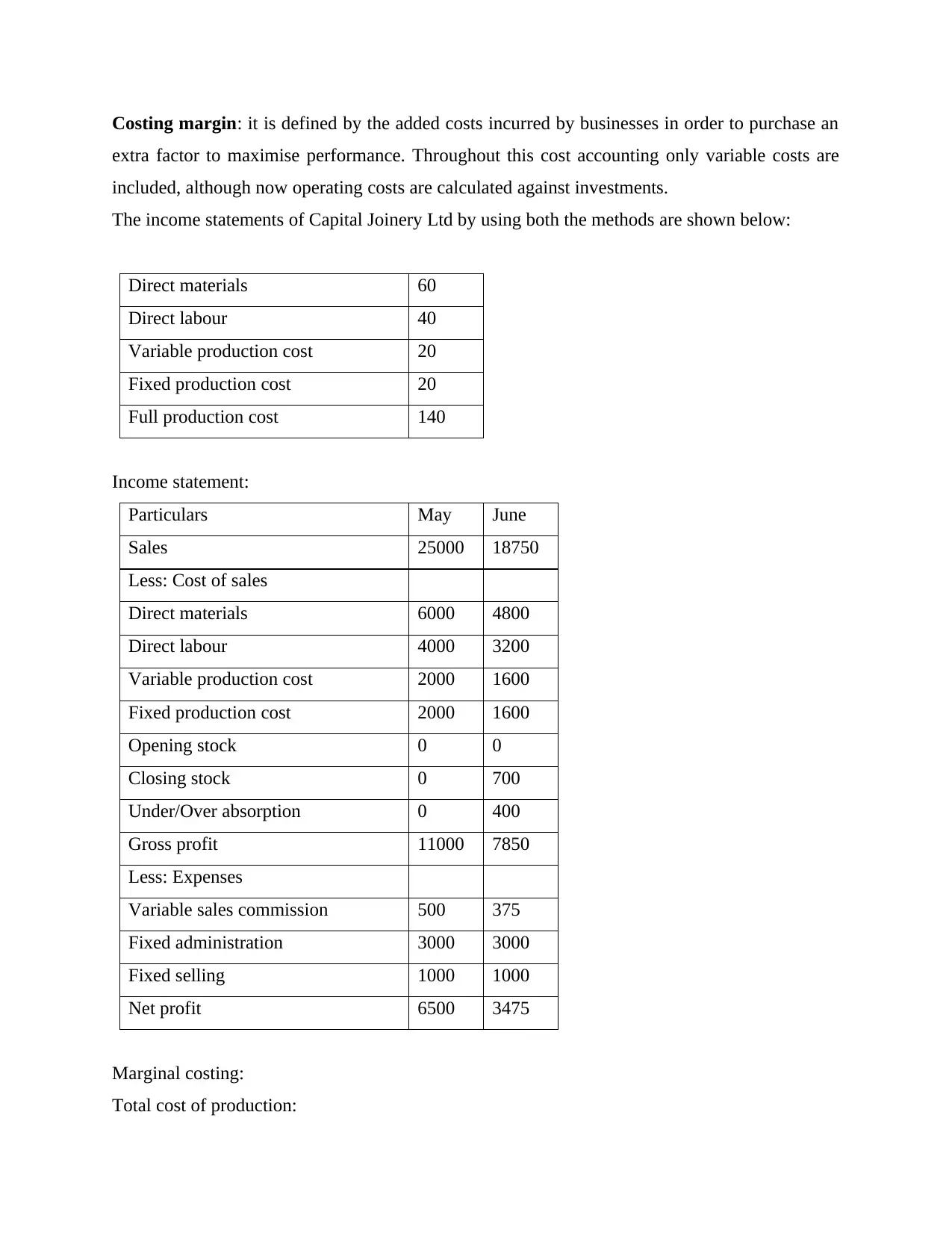

Marginal costing:

Total cost of production:

extra factor to maximise performance. Throughout this cost accounting only variable costs are

included, although now operating costs are calculated against investments.

The income statements of Capital Joinery Ltd by using both the methods are shown below:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

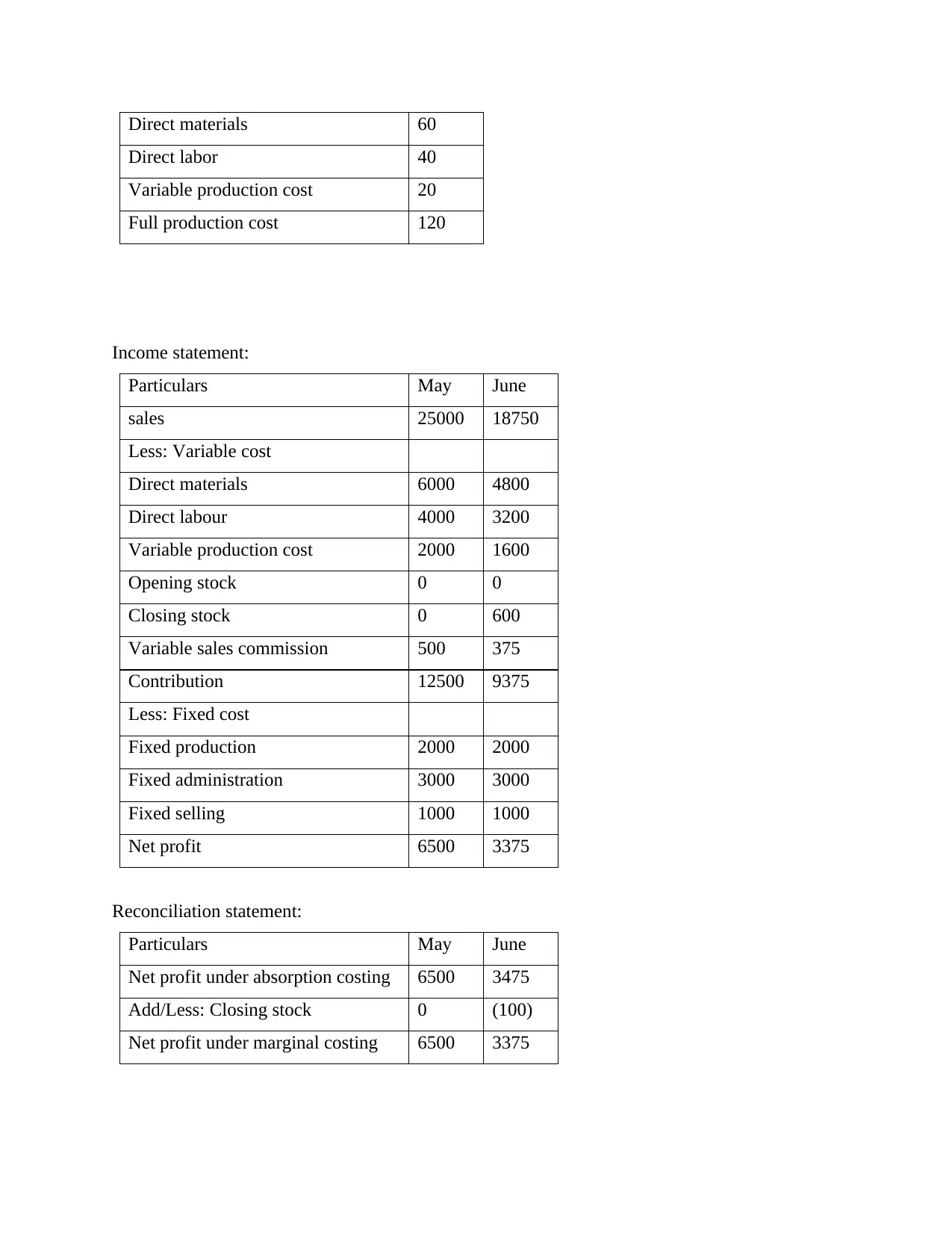

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

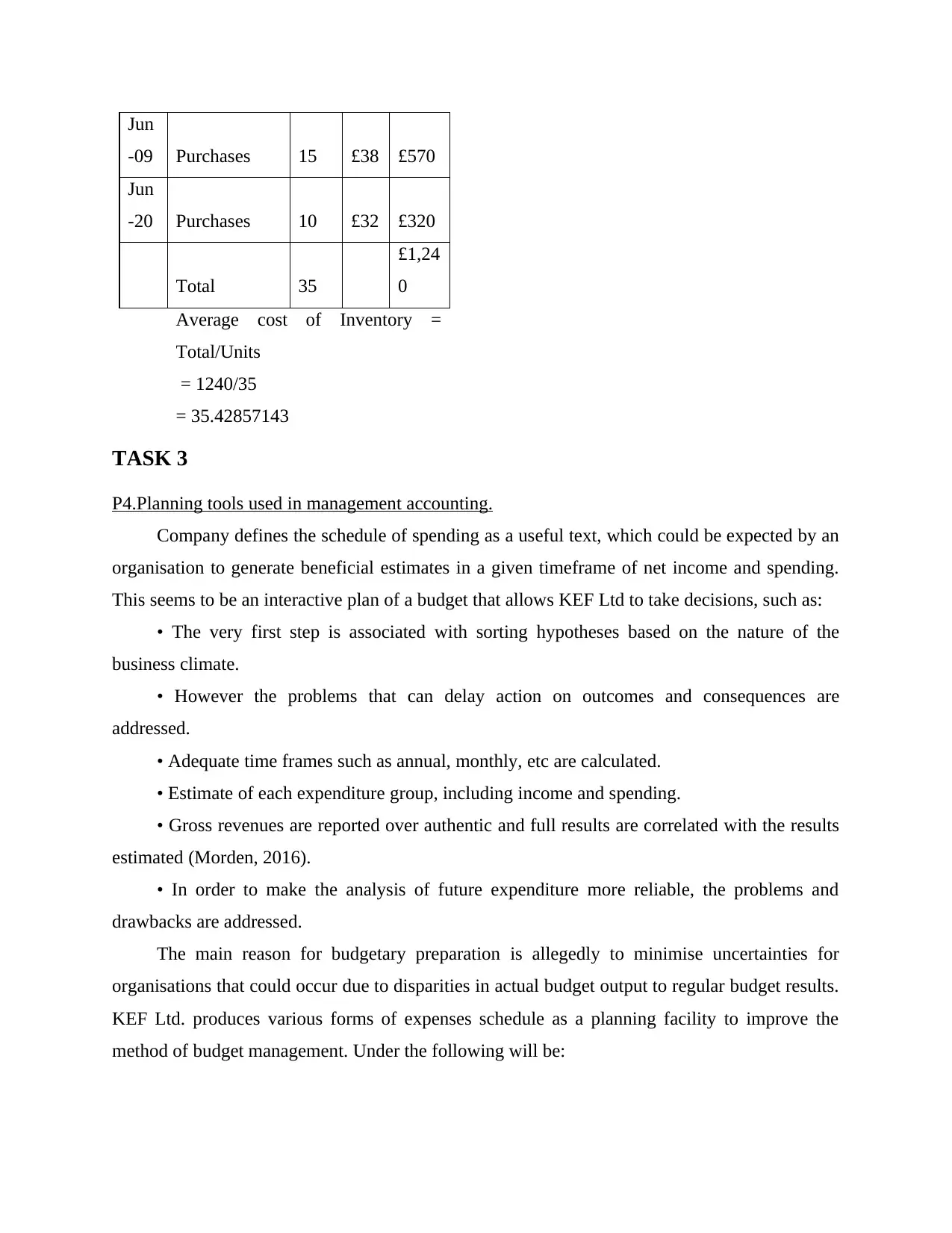

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

TASK 3

P4.Planning tools used in management accounting.

Company defines the schedule of spending as a useful text, which could be expected by an

organisation to generate beneficial estimates in a given timeframe of net income and spending.

This seems to be an interactive plan of a budget that allows KEF Ltd to take decisions, such as:

• The very first step is associated with sorting hypotheses based on the nature of the

business climate.

• However the problems that can delay action on outcomes and consequences are

addressed.

• Adequate time frames such as annual, monthly, etc are calculated.

• Estimate of each expenditure group, including income and spending.

• Gross revenues are reported over authentic and full results are correlated with the results

estimated (Morden, 2016).

• In order to make the analysis of future expenditure more reliable, the problems and

drawbacks are addressed.

The main reason for budgetary preparation is allegedly to minimise uncertainties for

organisations that could occur due to disparities in actual budget output to regular budget results.

KEF Ltd. produces various forms of expenses schedule as a planning facility to improve the

method of budget management. Under the following will be:

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

TASK 3

P4.Planning tools used in management accounting.

Company defines the schedule of spending as a useful text, which could be expected by an

organisation to generate beneficial estimates in a given timeframe of net income and spending.

This seems to be an interactive plan of a budget that allows KEF Ltd to take decisions, such as:

• The very first step is associated with sorting hypotheses based on the nature of the

business climate.

• However the problems that can delay action on outcomes and consequences are

addressed.

• Adequate time frames such as annual, monthly, etc are calculated.

• Estimate of each expenditure group, including income and spending.

• Gross revenues are reported over authentic and full results are correlated with the results

estimated (Morden, 2016).

• In order to make the analysis of future expenditure more reliable, the problems and

drawbacks are addressed.

The main reason for budgetary preparation is allegedly to minimise uncertainties for

organisations that could occur due to disparities in actual budget output to regular budget results.

KEF Ltd. produces various forms of expenses schedule as a planning facility to improve the

method of budget management. Under the following will be:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Flexible schedules budget: This software is helpful in adjusting the annual transactions of

the company because of a catastrophe or misunderstanding that really cannot run according to

the old rate of financing. This budget is intended to include new investment which can be

generated from any conceivable KEF Ltd situation, but it seeks to regularly track new prospects

for profit development for a fiscal year. The flexible budget of KEF Ltd is focused on

improvements that emerge from new semi-variable oversight output. The below are the different

advantages and disadvantages:

Advantages:

It makes internal managers take necessary action to cut costs since it is essentially ready

for the current trends of business (Siverbo, 2014). This budget allows KEF Ltd management to

enable possible enhancements and adjustments to the total costs and to maximise revenues

through various activities.

Disadvanatges:

This form of budget, including skilled work, is difficult and complex. There is little

incentive for the employee of KEF Ltd, who has to invest more capital into the recruiting of

skilled workers.

Zero-based budgeting: the much more effective form of fiscal management is known to

promote the mechanism of establishing a new spending schedule without any applicable

legislation. The protocol of ZBB reassesses each object within the cash flow but also describes

the additional fees incurred in separate fields. In KEF Ltd, the entire budget relates to calculating

the overall costs of the output of luxury goods on the basis of actual past knowledge spending.

The advantages and disadvantages listed below are distinct:

Advantages:

This strategy provides for performance, accuracy, and results as all working capital

elements are reassessed. Basically, ZBB provides stronger and more open interdepartmental

connectivity, such that decisions are taken more efficient and precise (Booth, 2018). This is a key

budget that help to eliminate KEF Ltd's several features to increase sales.

Disadvantage:

The major challenge which requires professional work and far more time to forecast

performance. The budget itself does not have the experience to plan a proposal. In order to

the company because of a catastrophe or misunderstanding that really cannot run according to

the old rate of financing. This budget is intended to include new investment which can be

generated from any conceivable KEF Ltd situation, but it seeks to regularly track new prospects

for profit development for a fiscal year. The flexible budget of KEF Ltd is focused on

improvements that emerge from new semi-variable oversight output. The below are the different

advantages and disadvantages:

Advantages:

It makes internal managers take necessary action to cut costs since it is essentially ready

for the current trends of business (Siverbo, 2014). This budget allows KEF Ltd management to

enable possible enhancements and adjustments to the total costs and to maximise revenues

through various activities.

Disadvanatges:

This form of budget, including skilled work, is difficult and complex. There is little

incentive for the employee of KEF Ltd, who has to invest more capital into the recruiting of

skilled workers.

Zero-based budgeting: the much more effective form of fiscal management is known to

promote the mechanism of establishing a new spending schedule without any applicable

legislation. The protocol of ZBB reassesses each object within the cash flow but also describes

the additional fees incurred in separate fields. In KEF Ltd, the entire budget relates to calculating

the overall costs of the output of luxury goods on the basis of actual past knowledge spending.

The advantages and disadvantages listed below are distinct:

Advantages:

This strategy provides for performance, accuracy, and results as all working capital

elements are reassessed. Basically, ZBB provides stronger and more open interdepartmental

connectivity, such that decisions are taken more efficient and precise (Booth, 2018). This is a key

budget that help to eliminate KEF Ltd's several features to increase sales.

Disadvantage:

The major challenge which requires professional work and far more time to forecast

performance. The budget itself does not have the experience to plan a proposal. In order to

explain how this budget functions, the organisation has to schedule daily meetings to raise

external expenses and harmful effects on the benefit.

Cash Budget - Receipts and cash transfers for a defined duration shall be reflected on in

cash Budget. It is a study after a certain duration of revenues and expenses. The cash budget

indicates possible taxes and funds transfers. If payments are greater than revenues, successful

cash management is enforced. When there's any excess supply, spending is smaller than income,

so there is a decision to use the surplus.

Benefits- In crises, when money is scarce as well as the spacing is full. A correct bank

balance allows customers to pay on deadlines, allowing managers to collect monthly payment

rewards.

Drawbacks- This budget focuses only on money and disregards both these factors that

diminish this current budget relevance in strategic policy.

SWOT analysis- A business, group of companies may initiate a SWOT analysis. In truth,

the study represents a variety of project objectives. The SWOT approach can be used in order to

evaluate and try to reduce a commodity or company, transaction or strategic alliance. SWOT

assessment also helps evaluate the origin, sequence, item or technology requirements (van der

Steen, 2011).

Benefits - An organisation, coordination system can be influenced by the SWOT analysis.

In fact, a number of project goals will be achieved. For example, SWOT method could be used to

assess and outsource a service or company, a method or connection. SWOT assessment also

helps quantify accurate production sources, sales cycles and demands for commodities or

technical acceptance.

Drawbacks: The SWOT evaluation is based on the four different types of assets,

weaknesses, perspectives and threats.

Budget operating – Budgets within more future earnings as well as expenditure periods

are expected for operating costs. The management team generally establishes an overall budget

well before beginning of the year because specifies the associated confidence thresholds over the

entire period. This budget has some major advantages and disadvantages, as follows:

Benefits: The company's advantages in effectively managing its activities by evaluating

and forecasting the true efficiency of the various operations.

external expenses and harmful effects on the benefit.

Cash Budget - Receipts and cash transfers for a defined duration shall be reflected on in

cash Budget. It is a study after a certain duration of revenues and expenses. The cash budget

indicates possible taxes and funds transfers. If payments are greater than revenues, successful

cash management is enforced. When there's any excess supply, spending is smaller than income,

so there is a decision to use the surplus.

Benefits- In crises, when money is scarce as well as the spacing is full. A correct bank

balance allows customers to pay on deadlines, allowing managers to collect monthly payment

rewards.

Drawbacks- This budget focuses only on money and disregards both these factors that

diminish this current budget relevance in strategic policy.

SWOT analysis- A business, group of companies may initiate a SWOT analysis. In truth,

the study represents a variety of project objectives. The SWOT approach can be used in order to

evaluate and try to reduce a commodity or company, transaction or strategic alliance. SWOT

assessment also helps evaluate the origin, sequence, item or technology requirements (van der

Steen, 2011).

Benefits - An organisation, coordination system can be influenced by the SWOT analysis.

In fact, a number of project goals will be achieved. For example, SWOT method could be used to

assess and outsource a service or company, a method or connection. SWOT assessment also

helps quantify accurate production sources, sales cycles and demands for commodities or

technical acceptance.

Drawbacks: The SWOT evaluation is based on the four different types of assets,

weaknesses, perspectives and threats.

Budget operating – Budgets within more future earnings as well as expenditure periods

are expected for operating costs. The management team generally establishes an overall budget

well before beginning of the year because specifies the associated confidence thresholds over the

entire period. This budget has some major advantages and disadvantages, as follows:

Benefits: The company's advantages in effectively managing its activities by evaluating

and forecasting the true efficiency of the various operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.