Understanding of Managerial Accounting System

VerifiedAdded on 2023/01/03

|17

|4601

|111

AI Summary

This report provides an understanding of the managerial accounting system and its benefits. It discusses different techniques and tools used in management accounting, such as cost accounting, price optimization, inventory management, and job costing. The report also explores the relevance of management accounting reports and the use of planning tools in solving financial problems. The subject of the report is management accounting, and it is applicable to the course code XYZ123 in the College/University of ABC.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Understanding of managerial accounting system with their benefits....................................3

P2) Relevance of management accounting reports......................................................................5

TASK2.............................................................................................................................................7

P3) Brief explanation regarding management accounting techniques.........................................7

TASK3.............................................................................................................................................9

P4) Explanation of benefits and drawbacks of planning tools.....................................................9

TASK4...........................................................................................................................................12

P5) Explanation regarding use of management accounting tools for solve financial problems.

....................................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Understanding of managerial accounting system with their benefits....................................3

P2) Relevance of management accounting reports......................................................................5

TASK2.............................................................................................................................................7

P3) Brief explanation regarding management accounting techniques.........................................7

TASK3.............................................................................................................................................9

P4) Explanation of benefits and drawbacks of planning tools.....................................................9

TASK4...........................................................................................................................................12

P5) Explanation regarding use of management accounting tools for solve financial problems.

....................................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management accounting is tool of accounting which help in assist management

department to formulate better plan and control over the business organization. To understand

this concept Rio Tinto has been taken. It is manufacturing organization which is incorporate as

Anglo Australian corporation it is famous for run its business activities in mining sector and

provides metals products. This report has been formulated to define the use of management

accounting system relevance of management reports with theses system and how accounting

technique useful for determine value of business transactions. It also measure the benefits and

drawbacks of applying various planning tools and relevance of theses tools to solve financial

problems with using benchmarking. Key performance indicator and relevant tools of managerial

accounting.

TASK 1

P1)Understanding of managerial accounting system.

Management accounting: The term management accounting is refer as a system which

business entities apply for recording transaction and collect information , represent theses data in

effective way. Main purpose of apply this system is take relevant decision. This approach is also

know as managerial or decision making accounting (Messner, 2016). Following are different

kinds of managerial accounting system which Rio Tinto can apply are define below:

Cost accounting systematic: Organizations implement approach of cost accounting

system through which they can identify value of their profit by recognizing or calculate cost of

running business activities. Various technique has been apply for identifying cost value which

include, marginal costing, absorption as well as standard costing method. This system is useful to

calculate the value of purchasing raw material, process of running or acquiring assets and all

theses activities which help in convert raw materiel in to finished goods (Kostyukova and

er.al.2018). Cost value of theses activities has been determine

Essential requirements: This system is use by cost department of Rio Tinto. They use

this system to determine the cost value of each department. By using information from cost

management system manager of Rio Tinto able to take decision regarding cost of purchasing raw

materiel from those suppler who can provides quality of raw material at minimum cost. As well

Management accounting is tool of accounting which help in assist management

department to formulate better plan and control over the business organization. To understand

this concept Rio Tinto has been taken. It is manufacturing organization which is incorporate as

Anglo Australian corporation it is famous for run its business activities in mining sector and

provides metals products. This report has been formulated to define the use of management

accounting system relevance of management reports with theses system and how accounting

technique useful for determine value of business transactions. It also measure the benefits and

drawbacks of applying various planning tools and relevance of theses tools to solve financial

problems with using benchmarking. Key performance indicator and relevant tools of managerial

accounting.

TASK 1

P1)Understanding of managerial accounting system.

Management accounting: The term management accounting is refer as a system which

business entities apply for recording transaction and collect information , represent theses data in

effective way. Main purpose of apply this system is take relevant decision. This approach is also

know as managerial or decision making accounting (Messner, 2016). Following are different

kinds of managerial accounting system which Rio Tinto can apply are define below:

Cost accounting systematic: Organizations implement approach of cost accounting

system through which they can identify value of their profit by recognizing or calculate cost of

running business activities. Various technique has been apply for identifying cost value which

include, marginal costing, absorption as well as standard costing method. This system is useful to

calculate the value of purchasing raw material, process of running or acquiring assets and all

theses activities which help in convert raw materiel in to finished goods (Kostyukova and

er.al.2018). Cost value of theses activities has been determine

Essential requirements: This system is use by cost department of Rio Tinto. They use

this system to determine the cost value of each department. By using information from cost

management system manager of Rio Tinto able to take decision regarding cost of purchasing raw

materiel from those suppler who can provides quality of raw material at minimum cost. As well

as on the basis of this information manager can compare their budget cost with actual cost incur

and formulate policies which beneficial or their internal users.

Price optimization system: There are various types of pricing strategies which

organization can be adopt. By using price optimization system manager take decision which

pricing strategy beneficial for their business entity which help in attaining business gain. In

competitive business market organization use price skimming, price discounting, premium, and

price penetration strategy ((Bedford, and Speklé, 2018). Every strategy is useful according to the

stage of business life cycle thus by using management accounting price statement Rio Tinto able

to take decision which pricing policy useful for selling metal products.

Essential requirements:Price optimization system is used by sales manager of Rio

Tinto. On the basis of information collected by internal source, their sale manager choose the

price penetration strategy accounting to the stage of business life cycle. This strategy is

beneficial for organization as it will provides satisfaction to customers as well as useful for attain

profits. Shareholders also took their decision on the basis of recognize demand and preference of

their target market customers.

Inventory management system: Stock is consider as essential or valid element of every

organization. Managing stock help in controlling cost and useful for identify the requirement of

maximum or minimum number of order require for particular time period. Manager of Rio Tinto

by using ABC analysis, inventory management technique, help in determine level of stock. By

applying theses technique manager recognize cost of storing as well as time taken to fulfil the

order of customer. Stock management system is useful in determiner the value of inventory for

particular period of time .

Essential requirements:Information collected form inventory management system is

useful for production department of Rio Tinto. As it is the largest manufacturing organization

and to manage and control the materiel and stack of metal in efficient manner. This information

is reliable for internal department by using essential data from using various system of inventory

manager can present information in systematic manner which useful for further business

activities. Manger of Rio Tinto on the basis of identifying cost of each stock can able to divided

each segment of cost.

Job costing system: By using job costing system manger could recognize the value or

cost arising for fulfil demand of each customer. This system is separate and useful for calculate

and formulate policies which beneficial or their internal users.

Price optimization system: There are various types of pricing strategies which

organization can be adopt. By using price optimization system manager take decision which

pricing strategy beneficial for their business entity which help in attaining business gain. In

competitive business market organization use price skimming, price discounting, premium, and

price penetration strategy ((Bedford, and Speklé, 2018). Every strategy is useful according to the

stage of business life cycle thus by using management accounting price statement Rio Tinto able

to take decision which pricing policy useful for selling metal products.

Essential requirements:Price optimization system is used by sales manager of Rio

Tinto. On the basis of information collected by internal source, their sale manager choose the

price penetration strategy accounting to the stage of business life cycle. This strategy is

beneficial for organization as it will provides satisfaction to customers as well as useful for attain

profits. Shareholders also took their decision on the basis of recognize demand and preference of

their target market customers.

Inventory management system: Stock is consider as essential or valid element of every

organization. Managing stock help in controlling cost and useful for identify the requirement of

maximum or minimum number of order require for particular time period. Manager of Rio Tinto

by using ABC analysis, inventory management technique, help in determine level of stock. By

applying theses technique manager recognize cost of storing as well as time taken to fulfil the

order of customer. Stock management system is useful in determiner the value of inventory for

particular period of time .

Essential requirements:Information collected form inventory management system is

useful for production department of Rio Tinto. As it is the largest manufacturing organization

and to manage and control the materiel and stack of metal in efficient manner. This information

is reliable for internal department by using essential data from using various system of inventory

manager can present information in systematic manner which useful for further business

activities. Manger of Rio Tinto on the basis of identifying cost of each stock can able to divided

each segment of cost.

Job costing system: By using job costing system manger could recognize the value or

cost arising for fulfil demand of each customer. This system is separate and useful for calculate

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

value of each transaction. Cost department of Rio Tinto us information collected from job

costing system.

Essential requirements: By collecting essential information from using job costing

system manager of Rio Tinto able to take decision regarding which activities which may become

the reason of arising high rate of cash outflow as well as useful for collect information which

help in attain business profit. Job costing system help in manage profits and control cost .This is

relevant for internal user for organization.

Differences between marginal coasting and Absorption costing

Marginal costing Absorption costing

In this only variable cost are consider by

organizations during the time of calculate

profit.

In this fixed as well as variable both cost are

considers.

In this fixed cost are considers as period cost.

And profit volume ratio has been calculated by

judging the difference of profitably.

Each cost are charged according to their

department. Every cost bear particular share of

fixed cost.

During the time of calculating marginal costing

the rate of cost per unit remain constant or

same.

In this method of costing cost per unit has been

reduce due to the impact of reduction in fixed

cost.

P2) Managerial reports

Report: This is relevant term for every business organization. It is mandatory document

which have all the essential information regarding business activities. The main purpose of

preparing report is to provide direction for running business activities. Following are the report

has been formulated by Rio Tinto

Cost report: This document has been prepared to summarise information regarding each

cost element or activities which incurred cost. All the information has been collected or

communicated through using cost accounting system. By formulating cost accounting

report , ,manager of Performance report: can able to easily find out the value of their each

business activities as well as cost required for fulfilling demand of customer. This report define

costing system.

Essential requirements: By collecting essential information from using job costing

system manager of Rio Tinto able to take decision regarding which activities which may become

the reason of arising high rate of cash outflow as well as useful for collect information which

help in attain business profit. Job costing system help in manage profits and control cost .This is

relevant for internal user for organization.

Differences between marginal coasting and Absorption costing

Marginal costing Absorption costing

In this only variable cost are consider by

organizations during the time of calculate

profit.

In this fixed as well as variable both cost are

considers.

In this fixed cost are considers as period cost.

And profit volume ratio has been calculated by

judging the difference of profitably.

Each cost are charged according to their

department. Every cost bear particular share of

fixed cost.

During the time of calculating marginal costing

the rate of cost per unit remain constant or

same.

In this method of costing cost per unit has been

reduce due to the impact of reduction in fixed

cost.

P2) Managerial reports

Report: This is relevant term for every business organization. It is mandatory document

which have all the essential information regarding business activities. The main purpose of

preparing report is to provide direction for running business activities. Following are the report

has been formulated by Rio Tinto

Cost report: This document has been prepared to summarise information regarding each

cost element or activities which incurred cost. All the information has been collected or

communicated through using cost accounting system. By formulating cost accounting

report , ,manager of Performance report: can able to easily find out the value of their each

business activities as well as cost required for fulfilling demand of customer. This report define

summery of each transaction and activities which may cause of generating higher business

revenue. Cost report has been formulated for identifying each transaction cost which beneficial

for internal as well as external business stockholder (Samuel, 2018).

Performance report: Management department of Rio Tinto formulated this report to

recognize performance of each department. In every organization, sales, marketing, research,

manufacturing and finance all department are categories. In case of Rio Tinto this organization is

run business in manufacturing sector thus their main focus of formulating performance report is

to analysis whether production department is able to fulfilled budgeted quality criteria. They also

measure that wherever department attain the quality or not. On the basis of recognizing

performance report manager able to compare their financial performance with other

organizations as well as they can able to take decision regarding providing reward business

policies.

Budget report: This report is the summery of all the report formulated by Rio Tinto.

Budget report define future expected profit as well as values of business activities. All these are

project on the basis of data collected from difference management accounting reports. This

report useful for Rio Tinto to recognize the value of future business asset and impact of decision

they take at present time period. On the basis of finding out budgeted value of each business

transactions manager took their decision and change further business policies which useful to

attain business gains.

Account receivable report: This is consider as essential business report. Rio Tinto done

their most of transaction on credit thus it is really difficult for them to manage their cash assets.

By formulating report of account receivables organization can able to manage and collect

essential information regarding their debtors. On the basis of collecting essential or reliable

business information regarding position of debtors manager could able to find out number of

debtors which may be consider or treated as doubtful debtors as well as those debtors which are

not given their debt amount or many consider as non performing assets. Manager of Rio Tinto

took decision and implement those policies and offer which help in control the number of bed

debts by providing attractive offer and cash discount. They also formulate policies which can be

control the cash outflow activities and increase cash inflow business activities.

Management accounting system is play vital role following are the benefits which Rio

Tinto gain by implementing of theses system:

revenue. Cost report has been formulated for identifying each transaction cost which beneficial

for internal as well as external business stockholder (Samuel, 2018).

Performance report: Management department of Rio Tinto formulated this report to

recognize performance of each department. In every organization, sales, marketing, research,

manufacturing and finance all department are categories. In case of Rio Tinto this organization is

run business in manufacturing sector thus their main focus of formulating performance report is

to analysis whether production department is able to fulfilled budgeted quality criteria. They also

measure that wherever department attain the quality or not. On the basis of recognizing

performance report manager able to compare their financial performance with other

organizations as well as they can able to take decision regarding providing reward business

policies.

Budget report: This report is the summery of all the report formulated by Rio Tinto.

Budget report define future expected profit as well as values of business activities. All these are

project on the basis of data collected from difference management accounting reports. This

report useful for Rio Tinto to recognize the value of future business asset and impact of decision

they take at present time period. On the basis of finding out budgeted value of each business

transactions manager took their decision and change further business policies which useful to

attain business gains.

Account receivable report: This is consider as essential business report. Rio Tinto done

their most of transaction on credit thus it is really difficult for them to manage their cash assets.

By formulating report of account receivables organization can able to manage and collect

essential information regarding their debtors. On the basis of collecting essential or reliable

business information regarding position of debtors manager could able to find out number of

debtors which may be consider or treated as doubtful debtors as well as those debtors which are

not given their debt amount or many consider as non performing assets. Manager of Rio Tinto

took decision and implement those policies and offer which help in control the number of bed

debts by providing attractive offer and cash discount. They also formulate policies which can be

control the cash outflow activities and increase cash inflow business activities.

Management accounting system is play vital role following are the benefits which Rio

Tinto gain by implementing of theses system:

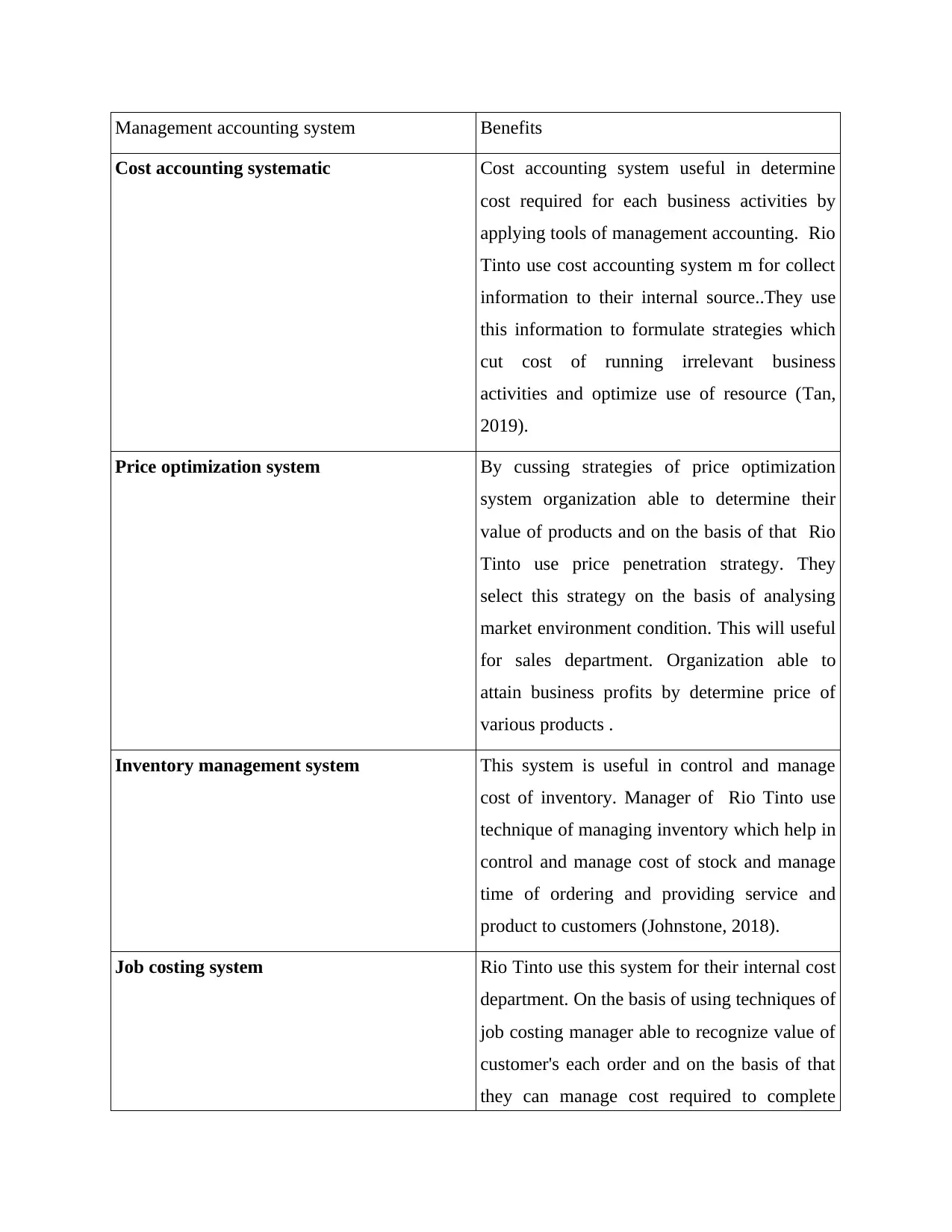

Management accounting system Benefits

Cost accounting systematic Cost accounting system useful in determine

cost required for each business activities by

applying tools of management accounting. Rio

Tinto use cost accounting system m for collect

information to their internal source..They use

this information to formulate strategies which

cut cost of running irrelevant business

activities and optimize use of resource (Tan,

2019).

Price optimization system By cussing strategies of price optimization

system organization able to determine their

value of products and on the basis of that Rio

Tinto use price penetration strategy. They

select this strategy on the basis of analysing

market environment condition. This will useful

for sales department. Organization able to

attain business profits by determine price of

various products .

Inventory management system This system is useful in control and manage

cost of inventory. Manager of Rio Tinto use

technique of managing inventory which help in

control and manage cost of stock and manage

time of ordering and providing service and

product to customers (Johnstone, 2018).

Job costing system Rio Tinto use this system for their internal cost

department. On the basis of using techniques of

job costing manager able to recognize value of

customer's each order and on the basis of that

they can manage cost required to complete

Cost accounting systematic Cost accounting system useful in determine

cost required for each business activities by

applying tools of management accounting. Rio

Tinto use cost accounting system m for collect

information to their internal source..They use

this information to formulate strategies which

cut cost of running irrelevant business

activities and optimize use of resource (Tan,

2019).

Price optimization system By cussing strategies of price optimization

system organization able to determine their

value of products and on the basis of that Rio

Tinto use price penetration strategy. They

select this strategy on the basis of analysing

market environment condition. This will useful

for sales department. Organization able to

attain business profits by determine price of

various products .

Inventory management system This system is useful in control and manage

cost of inventory. Manager of Rio Tinto use

technique of managing inventory which help in

control and manage cost of stock and manage

time of ordering and providing service and

product to customers (Johnstone, 2018).

Job costing system Rio Tinto use this system for their internal cost

department. On the basis of using techniques of

job costing manager able to recognize value of

customer's each order and on the basis of that

they can manage cost required to complete

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demand of customers.

TASK2

P3)

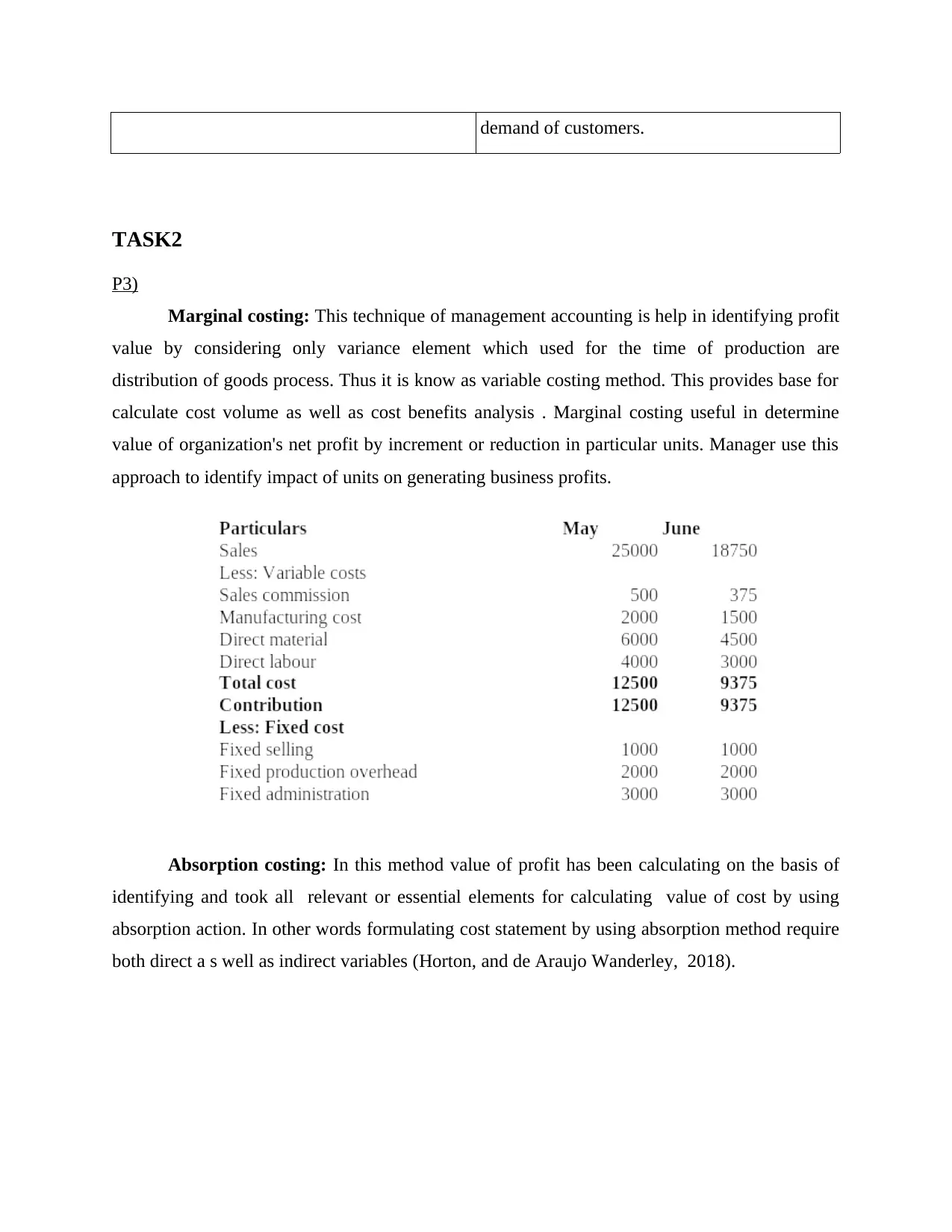

Marginal costing: This technique of management accounting is help in identifying profit

value by considering only variance element which used for the time of production are

distribution of goods process. Thus it is know as variable costing method. This provides base for

calculate cost volume as well as cost benefits analysis . Marginal costing useful in determine

value of organization's net profit by increment or reduction in particular units. Manager use this

approach to identify impact of units on generating business profits.

Absorption costing: In this method value of profit has been calculating on the basis of

identifying and took all relevant or essential elements for calculating value of cost by using

absorption action. In other words formulating cost statement by using absorption method require

both direct a s well as indirect variables (Horton, and de Araujo Wanderley, 2018).

TASK2

P3)

Marginal costing: This technique of management accounting is help in identifying profit

value by considering only variance element which used for the time of production are

distribution of goods process. Thus it is know as variable costing method. This provides base for

calculate cost volume as well as cost benefits analysis . Marginal costing useful in determine

value of organization's net profit by increment or reduction in particular units. Manager use this

approach to identify impact of units on generating business profits.

Absorption costing: In this method value of profit has been calculating on the basis of

identifying and took all relevant or essential elements for calculating value of cost by using

absorption action. In other words formulating cost statement by using absorption method require

both direct a s well as indirect variables (Horton, and de Araujo Wanderley, 2018).

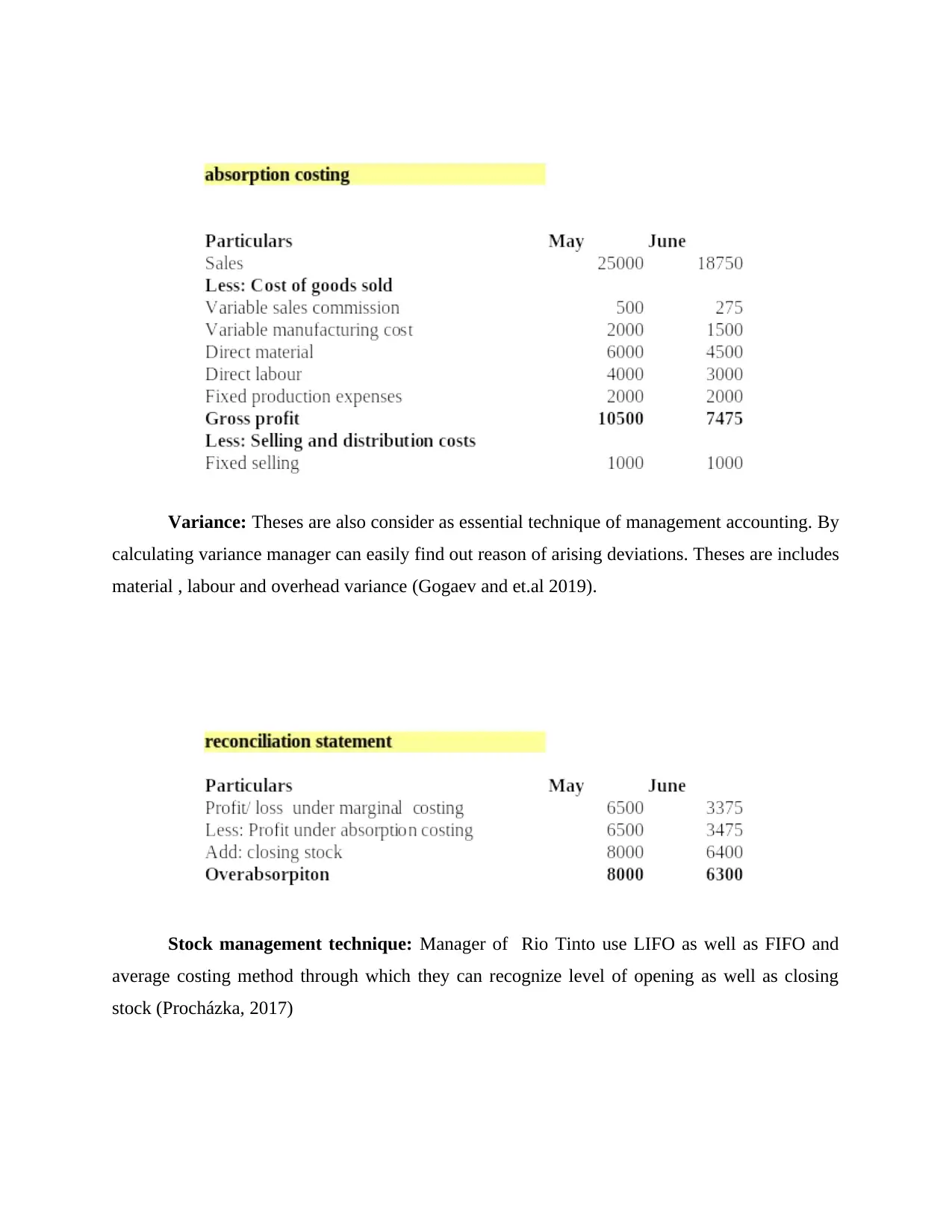

Variance: Theses are also consider as essential technique of management accounting. By

calculating variance manager can easily find out reason of arising deviations. Theses are includes

material , labour and overhead variance (Gogaev and et.al 2019).

Stock management technique: Manager of Rio Tinto use LIFO as well as FIFO and

average costing method through which they can recognize level of opening as well as closing

stock (Procházka, 2017)

calculating variance manager can easily find out reason of arising deviations. Theses are includes

material , labour and overhead variance (Gogaev and et.al 2019).

Stock management technique: Manager of Rio Tinto use LIFO as well as FIFO and

average costing method through which they can recognize level of opening as well as closing

stock (Procházka, 2017)

TASK3

P4)

Planning tools: Techniques which use to formulate plan are known as planning tool. In

other words planning tool are consider as those tools which provides direction for future business

planning. Following are various types of planning tool which Rio Tinto use

Budgetary techniques: Theses consider as those techniques which useful in formulate

budget. Theses budgets help in providing direction as well as define value of future profit.

Organizations have many choice to formulate their budget (Granlund, and Lukka, 2017). Theses

are consider as essential tool of management accounting. On the basis of formulate budget

organization able to take decision regrading business policies.

Activity based budgeting: In this type of budget, manager prepared financial statement on

the basis of recognizing allocation of activities and resources . In this type of budgeting resource

are allocated and distribute on the basis of activities run by different departments. Following are

its benefits and drawbacks

Advantage:

Activity based budget help in providing accurate business information by allocating

resource in effective way.

This tool of budgettiing help in utlized and mangge resource in effectve way.

This budget is useful in cutting unnecessary business activities.

Disadvantage

Formulate budget on the basis of allocation of activities require time.

Manager need to hire person who have great knowledge and understanding regarding

market and accounting norms.

Zero based budgeting: This is consider as modern method of formulate budget. In case

of Zero based budgeting manager prepare budget on the basis of information collected from

initial source or zero level.

Advantage:

This method is useful for motivating staff to find new ways of functioning and run

business activities.

P4)

Planning tools: Techniques which use to formulate plan are known as planning tool. In

other words planning tool are consider as those tools which provides direction for future business

planning. Following are various types of planning tool which Rio Tinto use

Budgetary techniques: Theses consider as those techniques which useful in formulate

budget. Theses budgets help in providing direction as well as define value of future profit.

Organizations have many choice to formulate their budget (Granlund, and Lukka, 2017). Theses

are consider as essential tool of management accounting. On the basis of formulate budget

organization able to take decision regrading business policies.

Activity based budgeting: In this type of budget, manager prepared financial statement on

the basis of recognizing allocation of activities and resources . In this type of budgeting resource

are allocated and distribute on the basis of activities run by different departments. Following are

its benefits and drawbacks

Advantage:

Activity based budget help in providing accurate business information by allocating

resource in effective way.

This tool of budgettiing help in utlized and mangge resource in effectve way.

This budget is useful in cutting unnecessary business activities.

Disadvantage

Formulate budget on the basis of allocation of activities require time.

Manager need to hire person who have great knowledge and understanding regarding

market and accounting norms.

Zero based budgeting: This is consider as modern method of formulate budget. In case

of Zero based budgeting manager prepare budget on the basis of information collected from

initial source or zero level.

Advantage:

This method is useful for motivating staff to find new ways of functioning and run

business activities.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Disadvantage

It is difficult for finance manager to justified each item cost when there will be no use of

production units (Oyewo, Ajibolade, and Obazee, 2019).

This type of method not useful for multinational organizations.

Pricing strategies: There will be various strategies are use for determine value of

product which organizations offer to their customers. By applying price penetration, discounting

or premium strategy manager formulate plan ans took decision regarding rate of profitability as

well as cost arise during their time of setting value of products. All these decision are take by

using pricing strategies.

Advantage:

Price strategies help in attain business profits by increasing value of products.

By applying pricing strategies organization able to attract more customer by achieving

higher sales target.

Disadvantage

Formulating business policies on the basis of using pricing strategies may not provides

accurate result as value of price are not rigid.

Costing techniques: Cost is essential elements ,manager of business entity by applying

technique of measuring cost can able to determine value of each product's cost. This will useful

in formulate business plan. Manager by using marginal, absorption costing can able to determine

cost of each business activities.

Advantage:

By using cost technique manager took decision regarding which plan is beneficial for future

business activities which help in generate business profits.

Cost strategies useful in find out those activities which help in controlling cost.

Disadvantage

For determine cost of each department 's working activities manager need to hire cost

accountant who has knowledge regarding accounting standard norms (Van der Stede, 2017).

calculation of cost is complex process. It is not necessary that cost statement gives correct

statements. Manager use absorption costing method thus they are not able to accurate identify the

value of profit.

It is difficult for finance manager to justified each item cost when there will be no use of

production units (Oyewo, Ajibolade, and Obazee, 2019).

This type of method not useful for multinational organizations.

Pricing strategies: There will be various strategies are use for determine value of

product which organizations offer to their customers. By applying price penetration, discounting

or premium strategy manager formulate plan ans took decision regarding rate of profitability as

well as cost arise during their time of setting value of products. All these decision are take by

using pricing strategies.

Advantage:

Price strategies help in attain business profits by increasing value of products.

By applying pricing strategies organization able to attract more customer by achieving

higher sales target.

Disadvantage

Formulating business policies on the basis of using pricing strategies may not provides

accurate result as value of price are not rigid.

Costing techniques: Cost is essential elements ,manager of business entity by applying

technique of measuring cost can able to determine value of each product's cost. This will useful

in formulate business plan. Manager by using marginal, absorption costing can able to determine

cost of each business activities.

Advantage:

By using cost technique manager took decision regarding which plan is beneficial for future

business activities which help in generate business profits.

Cost strategies useful in find out those activities which help in controlling cost.

Disadvantage

For determine cost of each department 's working activities manager need to hire cost

accountant who has knowledge regarding accounting standard norms (Van der Stede, 2017).

calculation of cost is complex process. It is not necessary that cost statement gives correct

statements. Manager use absorption costing method thus they are not able to accurate identify the

value of profit.

Other strategically tools: Manager by using tools of strategic management can also

formulate business plan. It consider SWOT , PESTLE and porter's 5 model. On the basis of

collecting information by using these tools manager able to formulate their plan to attain future

business target.

Advantage:

By using SWOT analysis manager able to find out strength and weakness of their

organization. Which help in formulate policies to enhance weakness.

PESTLE analysis help in collecting information regarding external environment factors.

On the basis of that manager able to determine the strategies use by competitors and trends run

preference of customer. All these are help in formulate business plan.

Disadvantage

For using strategic management tool manager require to hire expertise who have

knowledge regarding the market area.

Manager of Rio Tinto use activity based budgeting as it is manufacturing organization

and it is essential for them to allocate resource in effective manner, to manageorganization.. By

applying price penetration strategy they able to raise profits. Manager also use strategical tool

for guideline and took direction for formulate business plan.

TASK4

P5)

Financial problem: It is situation which arises due to lack of financial resource.

Organization specially small or medium size business entities. The main reason of organizations

face from these problems is that they are not able to manage their assets as well as businesses

liabilities which become the reason of cash outflow business activities. Thus organization face

from monetary business issue. Rio Tinto is facing financial issue they by observing technique

use by multinational organization can apply business policies (Setiawan, Rahmawati, Djuminah.

and Widagdo, 2019).

Mismanagement of financial assets: Nestle suffers from financial problem as they are not

able to manage their cash assets. They use policies which are not reliable for collecting cash

from debtors, moreover organization also face problem as their value of asset is comparatively

low and they are not able to control wastage business activities.

formulate business plan. It consider SWOT , PESTLE and porter's 5 model. On the basis of

collecting information by using these tools manager able to formulate their plan to attain future

business target.

Advantage:

By using SWOT analysis manager able to find out strength and weakness of their

organization. Which help in formulate policies to enhance weakness.

PESTLE analysis help in collecting information regarding external environment factors.

On the basis of that manager able to determine the strategies use by competitors and trends run

preference of customer. All these are help in formulate business plan.

Disadvantage

For using strategic management tool manager require to hire expertise who have

knowledge regarding the market area.

Manager of Rio Tinto use activity based budgeting as it is manufacturing organization

and it is essential for them to allocate resource in effective manner, to manageorganization.. By

applying price penetration strategy they able to raise profits. Manager also use strategical tool

for guideline and took direction for formulate business plan.

TASK4

P5)

Financial problem: It is situation which arises due to lack of financial resource.

Organization specially small or medium size business entities. The main reason of organizations

face from these problems is that they are not able to manage their assets as well as businesses

liabilities which become the reason of cash outflow business activities. Thus organization face

from monetary business issue. Rio Tinto is facing financial issue they by observing technique

use by multinational organization can apply business policies (Setiawan, Rahmawati, Djuminah.

and Widagdo, 2019).

Mismanagement of financial assets: Nestle suffers from financial problem as they are not

able to manage their cash assets. They use policies which are not reliable for collecting cash

from debtors, moreover organization also face problem as their value of asset is comparatively

low and they are not able to control wastage business activities.

Reduction in rate of revenue: Cadbury is one to the popular brand in chocolate sector

however this organization is also face financial problem due to decrement in selling rate. They

are not utilized techniques and work in according with customer preference thus their rate of

selling has been decline.

Management

accounting

techniques

Responding to the financial issues using

management accounting systems

Nestle Cadbury

Benchmarkin

g

Benchmarking is a technique of

measuring performance of

organization on the basis of setting

benchmark. Manager set

benchmark on the basis of using

past record as well as on the basis

of finding rival industries bench

mark. Nestle use this technique for

evaluate their performance by

setting target for increase sell and

performances. On the basis of

setting benchmark they can

increase performance and cash foe

activities by improving

performance of organization 's

human resources.

This organization is face financial

problem due to the reduction in sales

unit. By using benchmark management

department of Cadbury set their sale

target and give incentive to department

on the basis of completion of set target.

This method help in increases sales as

well as inner motivation of employee.

Which influence them to work in

effective manner.

Advice for Rio Tinto to use

‘benchmarking’ technique:

Rio Tinto use benchmarking, this will help in setting target for

sales and on the basis of that management department of this

organization can raise their sales volume which help in increases

cash inflow activities. Through which organization able to

overcome their financial problems.

This is consider as quantifiable This tool is useful for setting target

however this organization is also face financial problem due to decrement in selling rate. They

are not utilized techniques and work in according with customer preference thus their rate of

selling has been decline.

Management

accounting

techniques

Responding to the financial issues using

management accounting systems

Nestle Cadbury

Benchmarkin

g

Benchmarking is a technique of

measuring performance of

organization on the basis of setting

benchmark. Manager set

benchmark on the basis of using

past record as well as on the basis

of finding rival industries bench

mark. Nestle use this technique for

evaluate their performance by

setting target for increase sell and

performances. On the basis of

setting benchmark they can

increase performance and cash foe

activities by improving

performance of organization 's

human resources.

This organization is face financial

problem due to the reduction in sales

unit. By using benchmark management

department of Cadbury set their sale

target and give incentive to department

on the basis of completion of set target.

This method help in increases sales as

well as inner motivation of employee.

Which influence them to work in

effective manner.

Advice for Rio Tinto to use

‘benchmarking’ technique:

Rio Tinto use benchmarking, this will help in setting target for

sales and on the basis of that management department of this

organization can raise their sales volume which help in increases

cash inflow activities. Through which organization able to

overcome their financial problems.

This is consider as quantifiable This tool is useful for setting target

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

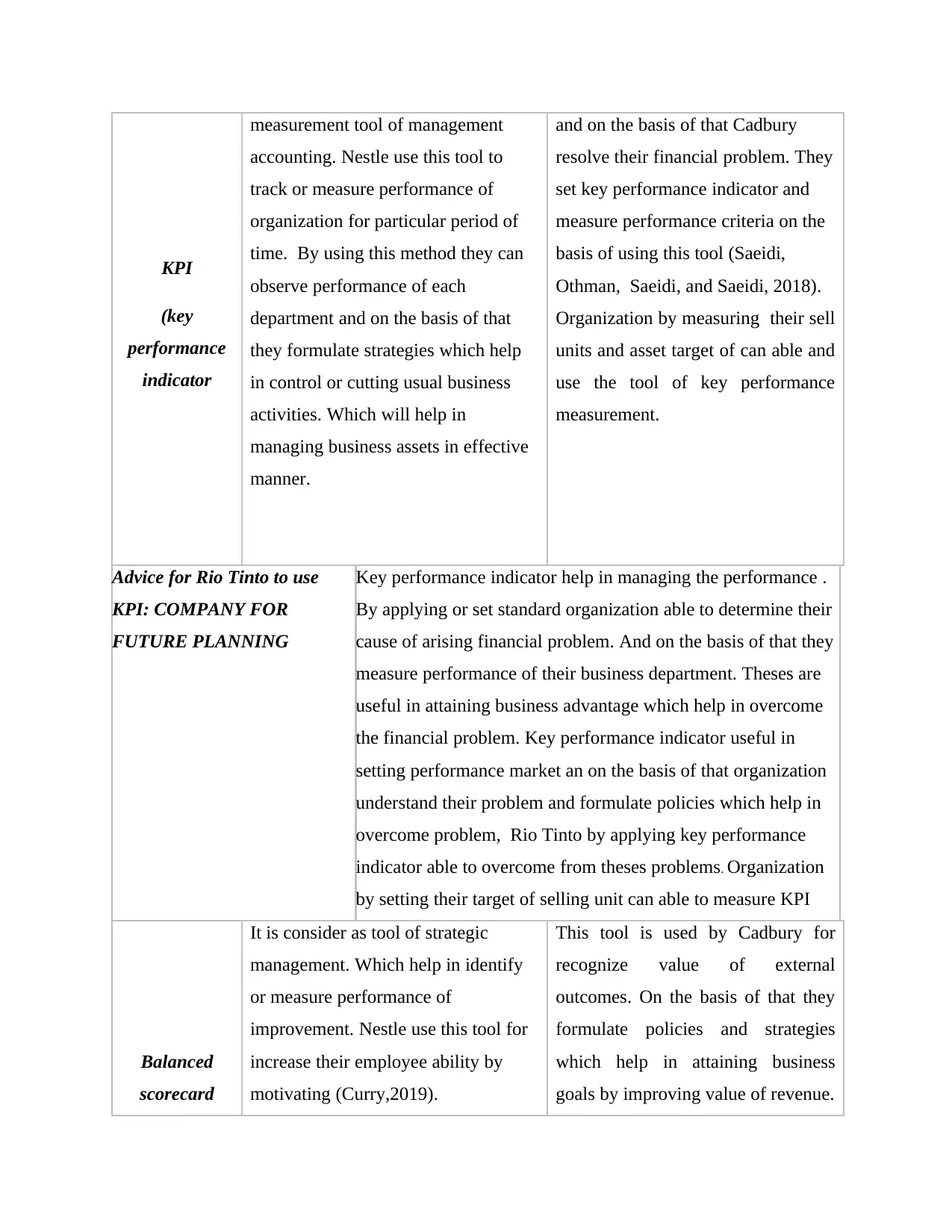

KPI

(key

performance

indicator

measurement tool of management

accounting. Nestle use this tool to

track or measure performance of

organization for particular period of

time. By using this method they can

observe performance of each

department and on the basis of that

they formulate strategies which help

in control or cutting usual business

activities. Which will help in

managing business assets in effective

manner.

and on the basis of that Cadbury

resolve their financial problem. They

set key performance indicator and

measure performance criteria on the

basis of using this tool (Saeidi,

Othman, Saeidi, and Saeidi, 2018).

Organization by measuring their sell

units and asset target of can able and

use the tool of key performance

measurement.

Advice for Rio Tinto to use

KPI: COMPANY FOR

FUTURE PLANNING

Key performance indicator help in managing the performance .

By applying or set standard organization able to determine their

cause of arising financial problem. And on the basis of that they

measure performance of their business department. Theses are

useful in attaining business advantage which help in overcome

the financial problem. Key performance indicator useful in

setting performance market an on the basis of that organization

understand their problem and formulate policies which help in

overcome problem, Rio Tinto by applying key performance

indicator able to overcome from theses problems. Organization

by setting their target of selling unit can able to measure KPI

Balanced

scorecard

It is consider as tool of strategic

management. Which help in identify

or measure performance of

improvement. Nestle use this tool for

increase their employee ability by

motivating (Curry,2019).

This tool is used by Cadbury for

recognize value of external

outcomes. On the basis of that they

formulate policies and strategies

which help in attaining business

goals by improving value of revenue.

(key

performance

indicator

measurement tool of management

accounting. Nestle use this tool to

track or measure performance of

organization for particular period of

time. By using this method they can

observe performance of each

department and on the basis of that

they formulate strategies which help

in control or cutting usual business

activities. Which will help in

managing business assets in effective

manner.

and on the basis of that Cadbury

resolve their financial problem. They

set key performance indicator and

measure performance criteria on the

basis of using this tool (Saeidi,

Othman, Saeidi, and Saeidi, 2018).

Organization by measuring their sell

units and asset target of can able and

use the tool of key performance

measurement.

Advice for Rio Tinto to use

KPI: COMPANY FOR

FUTURE PLANNING

Key performance indicator help in managing the performance .

By applying or set standard organization able to determine their

cause of arising financial problem. And on the basis of that they

measure performance of their business department. Theses are

useful in attaining business advantage which help in overcome

the financial problem. Key performance indicator useful in

setting performance market an on the basis of that organization

understand their problem and formulate policies which help in

overcome problem, Rio Tinto by applying key performance

indicator able to overcome from theses problems. Organization

by setting their target of selling unit can able to measure KPI

Balanced

scorecard

It is consider as tool of strategic

management. Which help in identify

or measure performance of

improvement. Nestle use this tool for

increase their employee ability by

motivating (Curry,2019).

This tool is used by Cadbury for

recognize value of external

outcomes. On the basis of that they

formulate policies and strategies

which help in attaining business

goals by improving value of revenue.

Manager of Rio Tinto by using planning tools and benchmark as well as key

performance indicator tool can able to set target and on the basis of information collected from

strategic planing tool they formulate budget which help in cut throat wastage business activities.

This will useful in attaining business profits and overcome financial problem.

CONCLUSION

From the above analysis it has been concluded that business entities for maintain their

position in market economy require to manage their resource, specially financial resource. To

control and manage resource manager use management accounting approach. Which by using

system of managing cost, took price decision and control wastage of investor can able to manage

their financial resource. By using absorption as well as marginal costing and variance,

organization able to find out value of deviation,to reduce this deviation manager apply planning

tool which help in reduce rate of deviations. Manager by applying benchmarking, balance

scorecard and finance governance overcome problem and issue arise due to lack of monetary

resources.

performance indicator tool can able to set target and on the basis of information collected from

strategic planing tool they formulate budget which help in cut throat wastage business activities.

This will useful in attaining business profits and overcome financial problem.

CONCLUSION

From the above analysis it has been concluded that business entities for maintain their

position in market economy require to manage their resource, specially financial resource. To

control and manage resource manager use management accounting approach. Which by using

system of managing cost, took price decision and control wastage of investor can able to manage

their financial resource. By using absorption as well as marginal costing and variance,

organization able to find out value of deviation,to reduce this deviation manager apply planning

tool which help in reduce rate of deviations. Manager by applying benchmarking, balance

scorecard and finance governance overcome problem and issue arise due to lack of monetary

resources.

REFERENCES

Books and journals

Kostyukova, E. I., Vakhrushina, M. A., Shirobokov, V. G. E., Feskova, M. V. and

Neshchadimova, T. A., 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical Sciences,

9(2). pp.775-779.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Bedford, D. S. and Speklé, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research, 30(2),

pp.23-58.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44, pp.25-34.

Tan, H.C., 2019. Using a structured collaborative learning approach in a case-based

management accounting course. Journal of Accounting Education, 49, p.100638.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal, 38(1), pp.30-48.

Horton, K.E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research, 38, pp.39-50.

Gogaev, O. K., Ostaev, G. Y., Khosiev, B. N., Kravchenko, N. A., Kondratiev, D. V. and

Nekrasova, E.V., 2019. Zootechnical and management accounting factors of beef cattle:

cost optimization Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 10(2), pp.221-231.

Procházka, D., 2017. The unintended consequences of accounting harmonization in a transition

country: A case study of management accounting of private Czech companies.

Contemporary Economics, 11(4), pp.443-458.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting, 45, pp.63-80.

Oyewo, B., Ajibolade, S. and Obazee, A., 2019. The influence of stakeholders on management

accounting practice. Journal of Sustainable Finance & Investment, 9(4), pp.295-324.

Van der Stede, W. A., 2017. “Global” management accounting research: some reflections.

Journal of International Accounting Research, 16(2), pp.1-8.

Setiawan, A.S., Rahmawati, R., Djuminah, D. and Widagdo, A. K., 2019. Owner power,

deliberate strategy formulation, and strategic management accounting. Opcion, 35(89),

pp.254-270.

Saeidi, S. P., Othman, M. S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management,

19(3), pp.326-348.

Curry, A., 2019. Across the great divide: a literature review of management accounting and

operations management at the shop floor. Management Review Quarterly, 69(1), pp.75-

119.

Books and journals

Kostyukova, E. I., Vakhrushina, M. A., Shirobokov, V. G. E., Feskova, M. V. and

Neshchadimova, T. A., 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical Sciences,

9(2). pp.775-779.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Bedford, D. S. and Speklé, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research, 30(2),

pp.23-58.

Samuel, S., 2018. A conceptual framework for teaching management accounting. Journal of

Accounting Education, 44, pp.25-34.

Tan, H.C., 2019. Using a structured collaborative learning approach in a case-based

management accounting course. Journal of Accounting Education, 49, p.100638.

Johnstone, L., 2018. Theorising and modelling social control in environmental management

accounting research. Social and Environmental Accountability Journal, 38(1), pp.30-48.

Horton, K.E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: Adding a new piece to the theoretical

jigsaw. Management Accounting Research, 38, pp.39-50.

Gogaev, O. K., Ostaev, G. Y., Khosiev, B. N., Kravchenko, N. A., Kondratiev, D. V. and

Nekrasova, E.V., 2019. Zootechnical and management accounting factors of beef cattle:

cost optimization Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 10(2), pp.221-231.

Procházka, D., 2017. The unintended consequences of accounting harmonization in a transition

country: A case study of management accounting of private Czech companies.

Contemporary Economics, 11(4), pp.443-458.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting, 45, pp.63-80.

Oyewo, B., Ajibolade, S. and Obazee, A., 2019. The influence of stakeholders on management

accounting practice. Journal of Sustainable Finance & Investment, 9(4), pp.295-324.

Van der Stede, W. A., 2017. “Global” management accounting research: some reflections.

Journal of International Accounting Research, 16(2), pp.1-8.

Setiawan, A.S., Rahmawati, R., Djuminah, D. and Widagdo, A. K., 2019. Owner power,

deliberate strategy formulation, and strategic management accounting. Opcion, 35(89),

pp.254-270.

Saeidi, S. P., Othman, M. S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management,

19(3), pp.326-348.

Curry, A., 2019. Across the great divide: a literature review of management accounting and

operations management at the shop floor. Management Review Quarterly, 69(1), pp.75-

119.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

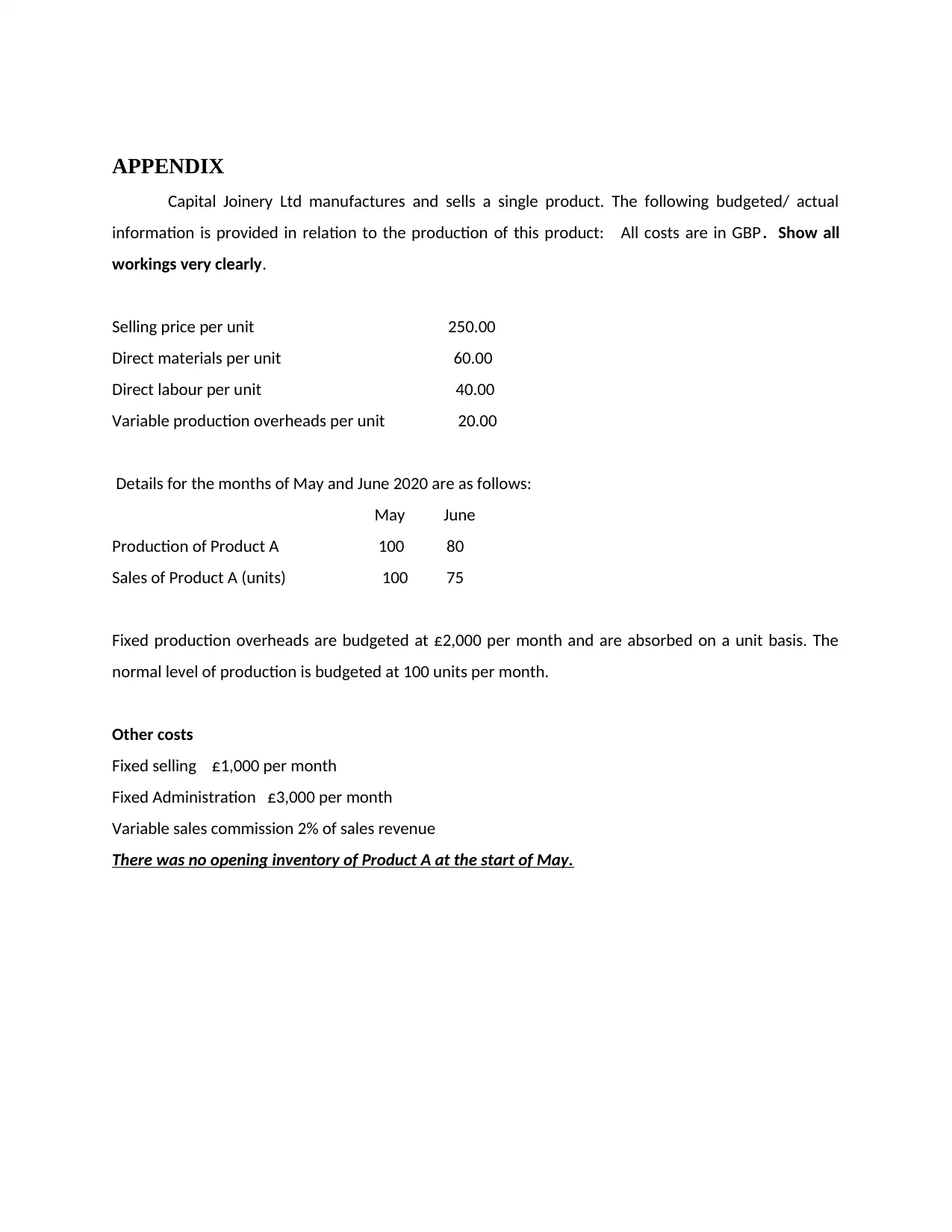

APPENDIX

Capital Joinery Ltd manufactures and sells a single product. The following budgeted/ actual

information is provided in relation to the production of this product: All costs are in GBP. Show all

workings very clearly.

Selling price per unit 250.00

Direct materials per unit 60.00

Direct labour per unit 40.00

Variable production overheads per unit 20.00

Details for the months of May and June 2020 are as follows:

May June

Production of Product A 100 80

Sales of Product A (units) 100 75

Fixed production overheads are budgeted at £2,000 per month and are absorbed on a unit basis. The

normal level of production is budgeted at 100 units per month.

Other costs

Fixed selling £1,000 per month

Fixed Administration £3,000 per month

Variable sales commission 2% of sales revenue

There was no opening inventory of Product A at the start of May.

Capital Joinery Ltd manufactures and sells a single product. The following budgeted/ actual

information is provided in relation to the production of this product: All costs are in GBP. Show all

workings very clearly.

Selling price per unit 250.00

Direct materials per unit 60.00

Direct labour per unit 40.00

Variable production overheads per unit 20.00

Details for the months of May and June 2020 are as follows:

May June

Production of Product A 100 80

Sales of Product A (units) 100 75

Fixed production overheads are budgeted at £2,000 per month and are absorbed on a unit basis. The

normal level of production is budgeted at 100 units per month.

Other costs

Fixed selling £1,000 per month

Fixed Administration £3,000 per month

Variable sales commission 2% of sales revenue

There was no opening inventory of Product A at the start of May.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.