Negative Gearing Investment Analysis

VerifiedAdded on 2020/02/19

|14

|3684

|72

AI Summary

The assignment delves into the complexities of negative gearing in property investments. It outlines the benefits of negative gearing, such as leveraging capital growth for expansion and targeting high-growth areas. Conversely, it highlights the risks associated with negative gearing, including potential financial strain from increased interest rates or decreased income. The assignment also examines the tax implications of negative gearing, suggesting that investments be held in the name of the main income earner to maximize tax benefits. It provides a numerical example illustrating how negative gearing can reduce taxable income and subsequent tax payable.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ADFP Module 3 Taxation Assignment1707

ADFP Module3

Taxation Assignment – Version B

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the bottom of this page.

Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS)

to submit your assessment.

In the LMS, click on the file ”Submit ADFP Module 3Taxation Assignment” in the

Module 3section of your course and upload your assessment file/s by following

the prompts.

Please be sure to click “Continue” after clicking “submit”.This ensures your

assessor receives notification – very important!

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the

purposeof detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by

the above student declaration.

ADFP Module3

Taxation Assignment – Version B

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the bottom of this page.

Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS)

to submit your assessment.

In the LMS, click on the file ”Submit ADFP Module 3Taxation Assignment” in the

Module 3section of your course and upload your assessment file/s by following

the prompts.

Please be sure to click “Continue” after clicking “submit”.This ensures your

assessor receives notification – very important!

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the

purposeof detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by

the above student declaration.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADFP Module 3 Taxation Assignment1707

Important assessment information

Aims of this assessment

This assessment focusses on taxation in a financial planning context. Tax on superannuation

lump sum withdrawals is covered, as is tax on the receipt of an account based pension prior

to Age 60. Various tax implications across different ownership structures is addressed, as

are tax deductions available under negative gearing scenarios. Capital Gains tax is also

covered.

Marking and feedback

This assignment contains 2 assessment activities eachcontaining specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSFPL601A

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line

with specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s

with limited serious errors in fact or application. If incorrect information is contained in an

answer, it must be fundamentally outweighed by the accurate information provided. This

will be assessed against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from

a legislative perspective, or are incorrectly applied. Answers that omit to provide a

response to any significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty reasoning, a poor

standard of expression or include plagiarism may also be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy is contained in

the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will

be given one more opportunity to re-submit the assessment after consultation with your

Important assessment information

Aims of this assessment

This assessment focusses on taxation in a financial planning context. Tax on superannuation

lump sum withdrawals is covered, as is tax on the receipt of an account based pension prior

to Age 60. Various tax implications across different ownership structures is addressed, as

are tax deductions available under negative gearing scenarios. Capital Gains tax is also

covered.

Marking and feedback

This assignment contains 2 assessment activities eachcontaining specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSFPL601A

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line

with specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s

with limited serious errors in fact or application. If incorrect information is contained in an

answer, it must be fundamentally outweighed by the accurate information provided. This

will be assessed against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from

a legislative perspective, or are incorrectly applied. Answers that omit to provide a

response to any significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty reasoning, a poor

standard of expression or include plagiarism may also be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy is contained in

the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will

be given one more opportunity to re-submit the assessment after consultation with your

ADFP Module 3 Taxation Assignment1707

Trainer/ Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your

grade book in the Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all

areas deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in

meeting competency after resubmitting your assessment, you will be required to repeat

those units.

In the event that you have concerns about the assessment decision then you can refer to

our Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject

matter areas raised in the question in full as part of the response.

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must

show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here

to assist you

Trainer/ Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your

grade book in the Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all

areas deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in

meeting competency after resubmitting your assessment, you will be required to repeat

those units.

In the event that you have concerns about the assessment decision then you can refer to

our Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject

matter areas raised in the question in full as part of the response.

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must

show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here

to assist you

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 4 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 1 hour

Assessment Activity 1

Case Study

Taxation Planning Strategies – Sean and Pam

Unit: FNSFPL601A

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 4 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 1 hour

Assessment Activity 1

Case Study

Taxation Planning Strategies – Sean and Pam

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

Background

Sean and Pam are new clients. They purchased a 1 hectare block of land 8 months ago with the

intention of building a house. They paid $300,000 for the land. They have been living with Sean’s

parents in order to save as much as possible for their new home. Pam has recently been offered a huge

promotion which would mean moving interstate for at least six years. She has accepted the new job

and she and Sean have decided to sell the land which is now being valued at $410,000.

Required:

In providing advice to Sean and Pam, consider the following questions:

1) If Sean and Pam sell the land this month, will the land be exempt from capital gains tax? Why or

why not?

Capital gain tax is exempted for mainly for pre-CGT assets, acquired before 20th September,

1985, main residence and assets, used for generating exempt or non-assessable non-exempt

income and depreciating assets for taxation purpose.

Sean and pam have acquired the land after 21st September, 1984 and therefore, it would not be

considered as pre-CGT asset. It is a vacant land and cannot be used for main residence. It has not been

used for generating income purpose also. Moreover, being a vacant land, it would not be considered for

depreciating purpose also.

Hence, If Sean and Pam would sell the land this month, they will not get any tax exemption for the capital

gains, earned from the selling of the land.

2) To attract the discount of 50%, what strategy could you suggest to Sean and Pam?

50% discount on capital gain tax is available for the individuals, trust or complying super fund.

Apart from the that, the CGT event should be occurred after 21st September,1999 and must be

possessed by the owner at least for the period of 12 months before the CGT event.

Sean and Pam are individual taxpayer and they plan to sell the land after 21st September, 1999. Hence,

they are eligible to get 50% discount on CGT. However, they have acquired the assets only for 8 months.

To avail 50% discount on the capital gain tax on the sale of land, they should delay the sale for next 4

months and sell it only after completing the 1 year of ownership.

3) If Sean and Pam had bought the land, built a house on it, lived in the house and sold it 3 years

later what would be the capital gains tax from the disposal? Explain.

The land, including the house, built on it, is exempt from capital gain tax for the shorter period

of the following:

Unit: FNSFPL601A

Background

Sean and Pam are new clients. They purchased a 1 hectare block of land 8 months ago with the

intention of building a house. They paid $300,000 for the land. They have been living with Sean’s

parents in order to save as much as possible for their new home. Pam has recently been offered a huge

promotion which would mean moving interstate for at least six years. She has accepted the new job

and she and Sean have decided to sell the land which is now being valued at $410,000.

Required:

In providing advice to Sean and Pam, consider the following questions:

1) If Sean and Pam sell the land this month, will the land be exempt from capital gains tax? Why or

why not?

Capital gain tax is exempted for mainly for pre-CGT assets, acquired before 20th September,

1985, main residence and assets, used for generating exempt or non-assessable non-exempt

income and depreciating assets for taxation purpose.

Sean and pam have acquired the land after 21st September, 1984 and therefore, it would not be

considered as pre-CGT asset. It is a vacant land and cannot be used for main residence. It has not been

used for generating income purpose also. Moreover, being a vacant land, it would not be considered for

depreciating purpose also.

Hence, If Sean and Pam would sell the land this month, they will not get any tax exemption for the capital

gains, earned from the selling of the land.

2) To attract the discount of 50%, what strategy could you suggest to Sean and Pam?

50% discount on capital gain tax is available for the individuals, trust or complying super fund.

Apart from the that, the CGT event should be occurred after 21st September,1999 and must be

possessed by the owner at least for the period of 12 months before the CGT event.

Sean and Pam are individual taxpayer and they plan to sell the land after 21st September, 1999. Hence,

they are eligible to get 50% discount on CGT. However, they have acquired the assets only for 8 months.

To avail 50% discount on the capital gain tax on the sale of land, they should delay the sale for next 4

months and sell it only after completing the 1 year of ownership.

3) If Sean and Pam had bought the land, built a house on it, lived in the house and sold it 3 years

later what would be the capital gains tax from the disposal? Explain.

The land, including the house, built on it, is exempt from capital gain tax for the shorter period

of the following:

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

a) 4 years immediately before the house is used for main residence

b) The period between the acquisition of the land and the house becomes the main residence

If Sean and Pam built house immediately on the alnd and moved in the house immediately after

completion within 4 years after the acquisition of the land, then they can get full exemption on the capital

gain, from the sale of the land, including the house.

However, it should be noted that they would be eligible for full exemption only if they would use the

house as their man residence and not use it for any form income generating activities.

4) Sean and Pam have sold some shares which resulted in a capital loss. Can they use these capital

losses as a tax deduction to reduce their assessable income? Explain.

As per the Australian tax regulations, capital loss, incurred from selling of any CGT assets can

only be set off against any capital gain of the taxpayer.

Shares are considered as CGT assets. Therefore, the capital loss from the sale of shares are can be used to

decrease the capital gain. However, it is not specified whether the assessable income of Sean and Pam

includes any capital gain or not.

If the assessable income includes any capital gains from general CGT assets, like real estate, other shares,

units and similar investments then the capital loss can be used to reduce the assessable income.

It cannot be set off against the assessable income, if the income does not include any capital gain from the

general CGT assets or include capital gains from CGT assets, like collectables and personal assets

Activity instructions to candidates

This is an open book assessment activity.

Assessment Activity 2

Calculation Exercise

Taxation

Unit: FNSFPL601A

a) 4 years immediately before the house is used for main residence

b) The period between the acquisition of the land and the house becomes the main residence

If Sean and Pam built house immediately on the alnd and moved in the house immediately after

completion within 4 years after the acquisition of the land, then they can get full exemption on the capital

gain, from the sale of the land, including the house.

However, it should be noted that they would be eligible for full exemption only if they would use the

house as their man residence and not use it for any form income generating activities.

4) Sean and Pam have sold some shares which resulted in a capital loss. Can they use these capital

losses as a tax deduction to reduce their assessable income? Explain.

As per the Australian tax regulations, capital loss, incurred from selling of any CGT assets can

only be set off against any capital gain of the taxpayer.

Shares are considered as CGT assets. Therefore, the capital loss from the sale of shares are can be used to

decrease the capital gain. However, it is not specified whether the assessable income of Sean and Pam

includes any capital gain or not.

If the assessable income includes any capital gains from general CGT assets, like real estate, other shares,

units and similar investments then the capital loss can be used to reduce the assessable income.

It cannot be set off against the assessable income, if the income does not include any capital gain from the

general CGT assets or include capital gains from CGT assets, like collectables and personal assets

Activity instructions to candidates

This is an open book assessment activity.

Assessment Activity 2

Calculation Exercise

Taxation

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 3 hours

Unit: FNSFPL601A

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 3 hours

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

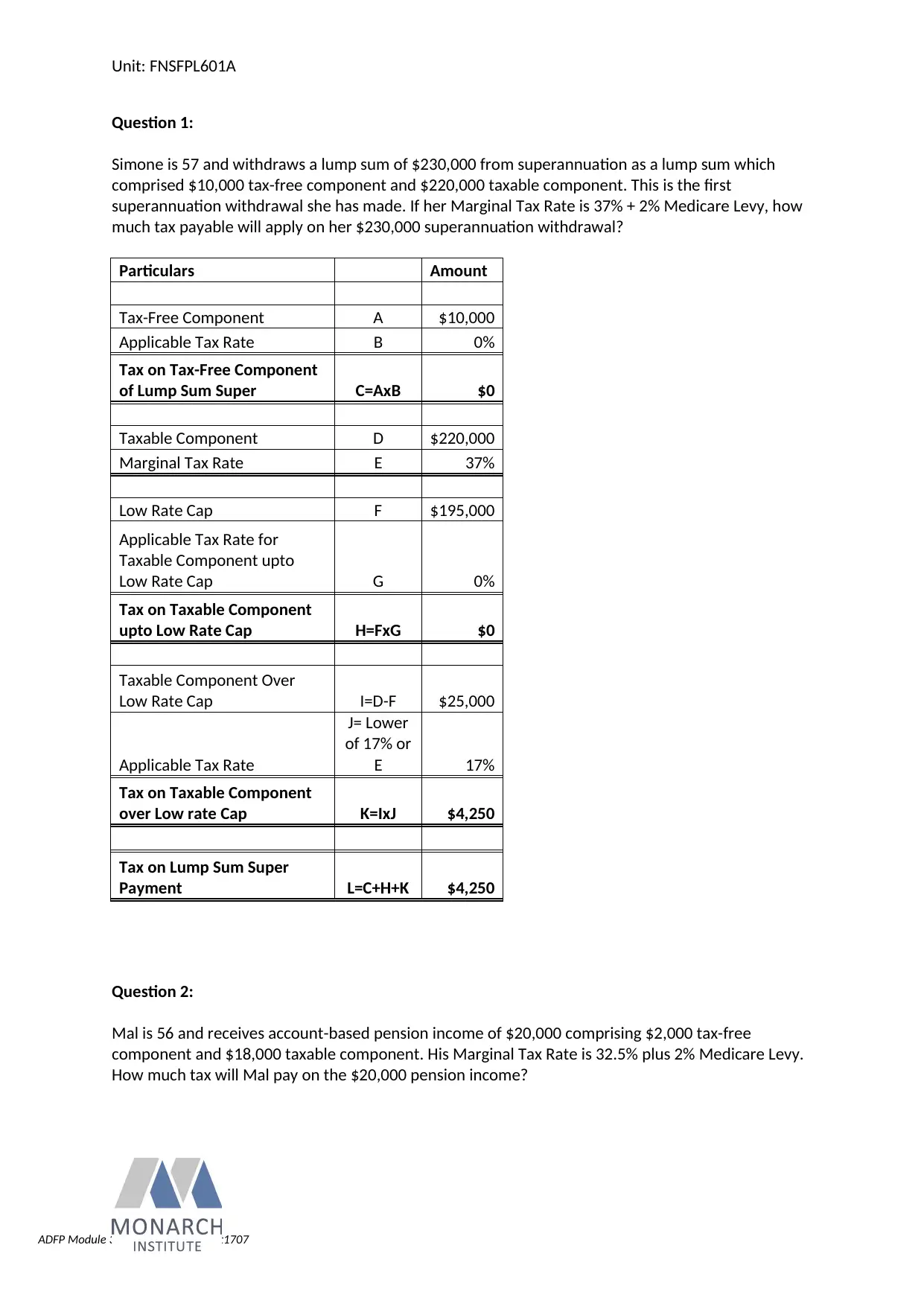

Question 1:

Simone is 57 and withdraws a lump sum of $230,000 from superannuation as a lump sum which

comprised $10,000 tax-free component and $220,000 taxable component. This is the first

superannuation withdrawal she has made. If her Marginal Tax Rate is 37% + 2% Medicare Levy, how

much tax payable will apply on her $230,000 superannuation withdrawal?

Particulars Amount

Tax-Free Component A $10,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component

of Lump Sum Super C=AxB $0

Taxable Component D $220,000

Marginal Tax Rate E 37%

Low Rate Cap F $195,000

Applicable Tax Rate for

Taxable Component upto

Low Rate Cap G 0%

Tax on Taxable Component

upto Low Rate Cap H=FxG $0

Taxable Component Over

Low Rate Cap I=D-F $25,000

Applicable Tax Rate

J= Lower

of 17% or

E 17%

Tax on Taxable Component

over Low rate Cap K=IxJ $4,250

Tax on Lump Sum Super

Payment L=C+H+K $4,250

Question 2:

Mal is 56 and receives account-based pension income of $20,000 comprising $2,000 tax-free

component and $18,000 taxable component. His Marginal Tax Rate is 32.5% plus 2% Medicare Levy.

How much tax will Mal pay on the $20,000 pension income?

Unit: FNSFPL601A

Question 1:

Simone is 57 and withdraws a lump sum of $230,000 from superannuation as a lump sum which

comprised $10,000 tax-free component and $220,000 taxable component. This is the first

superannuation withdrawal she has made. If her Marginal Tax Rate is 37% + 2% Medicare Levy, how

much tax payable will apply on her $230,000 superannuation withdrawal?

Particulars Amount

Tax-Free Component A $10,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component

of Lump Sum Super C=AxB $0

Taxable Component D $220,000

Marginal Tax Rate E 37%

Low Rate Cap F $195,000

Applicable Tax Rate for

Taxable Component upto

Low Rate Cap G 0%

Tax on Taxable Component

upto Low Rate Cap H=FxG $0

Taxable Component Over

Low Rate Cap I=D-F $25,000

Applicable Tax Rate

J= Lower

of 17% or

E 17%

Tax on Taxable Component

over Low rate Cap K=IxJ $4,250

Tax on Lump Sum Super

Payment L=C+H+K $4,250

Question 2:

Mal is 56 and receives account-based pension income of $20,000 comprising $2,000 tax-free

component and $18,000 taxable component. His Marginal Tax Rate is 32.5% plus 2% Medicare Levy.

How much tax will Mal pay on the $20,000 pension income?

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

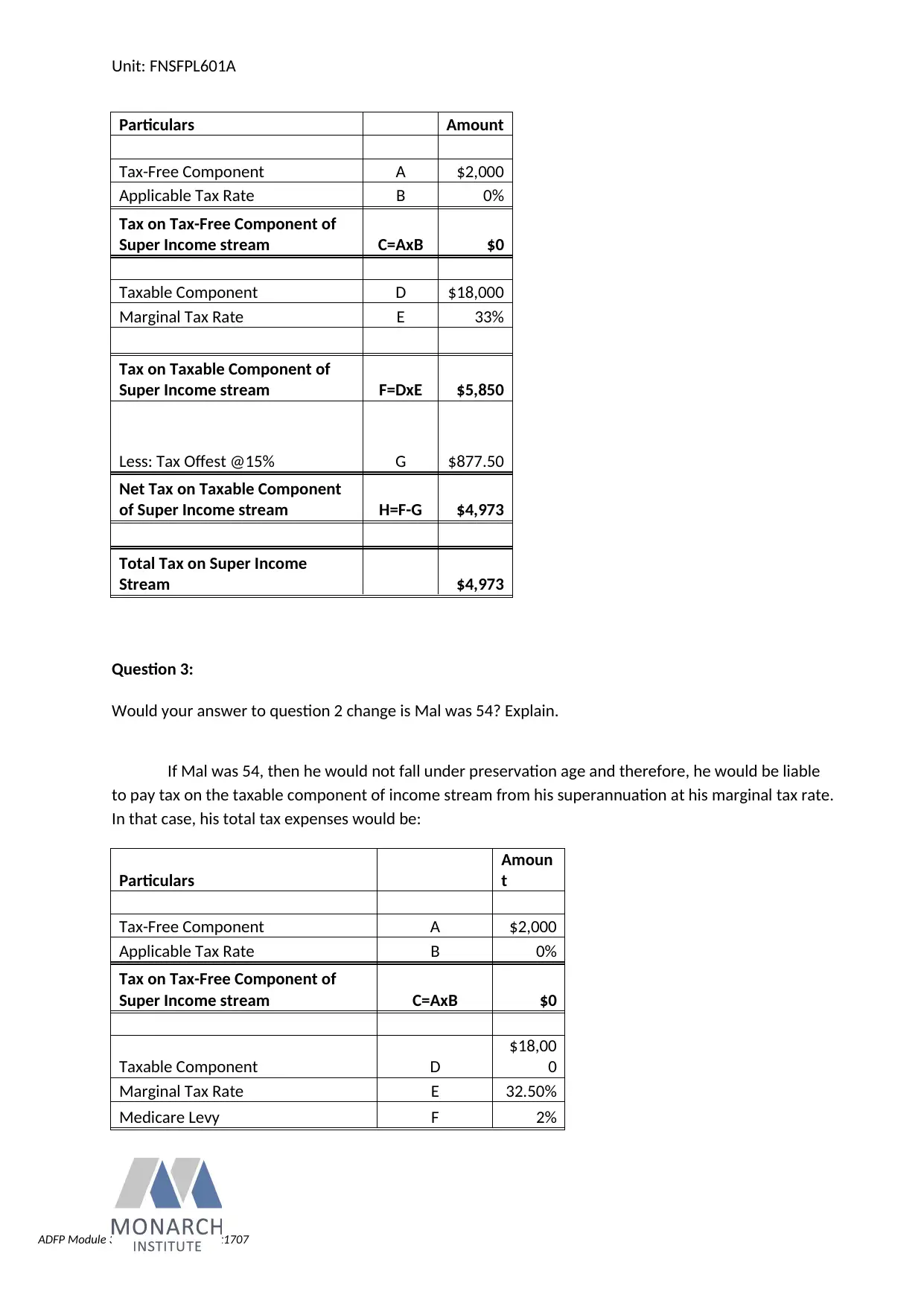

Particulars Amount

Tax-Free Component A $2,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component of

Super Income stream C=AxB $0

Taxable Component D $18,000

Marginal Tax Rate E 33%

Tax on Taxable Component of

Super Income stream F=DxE $5,850

Less: Tax Offest @15% G $877.50

Net Tax on Taxable Component

of Super Income stream H=F-G $4,973

Total Tax on Super Income

Stream $4,973

Question 3:

Would your answer to question 2 change is Mal was 54? Explain.

If Mal was 54, then he would not fall under preservation age and therefore, he would be liable

to pay tax on the taxable component of income stream from his superannuation at his marginal tax rate.

In that case, his total tax expenses would be:

Particulars

Amoun

t

Tax-Free Component A $2,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component of

Super Income stream C=AxB $0

Taxable Component D

$18,00

0

Marginal Tax Rate E 32.50%

Medicare Levy F 2%

Unit: FNSFPL601A

Particulars Amount

Tax-Free Component A $2,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component of

Super Income stream C=AxB $0

Taxable Component D $18,000

Marginal Tax Rate E 33%

Tax on Taxable Component of

Super Income stream F=DxE $5,850

Less: Tax Offest @15% G $877.50

Net Tax on Taxable Component

of Super Income stream H=F-G $4,973

Total Tax on Super Income

Stream $4,973

Question 3:

Would your answer to question 2 change is Mal was 54? Explain.

If Mal was 54, then he would not fall under preservation age and therefore, he would be liable

to pay tax on the taxable component of income stream from his superannuation at his marginal tax rate.

In that case, his total tax expenses would be:

Particulars

Amoun

t

Tax-Free Component A $2,000

Applicable Tax Rate B 0%

Tax on Tax-Free Component of

Super Income stream C=AxB $0

Taxable Component D

$18,00

0

Marginal Tax Rate E 32.50%

Medicare Levy F 2%

ADFP Module 3 Taxation Assignment1707

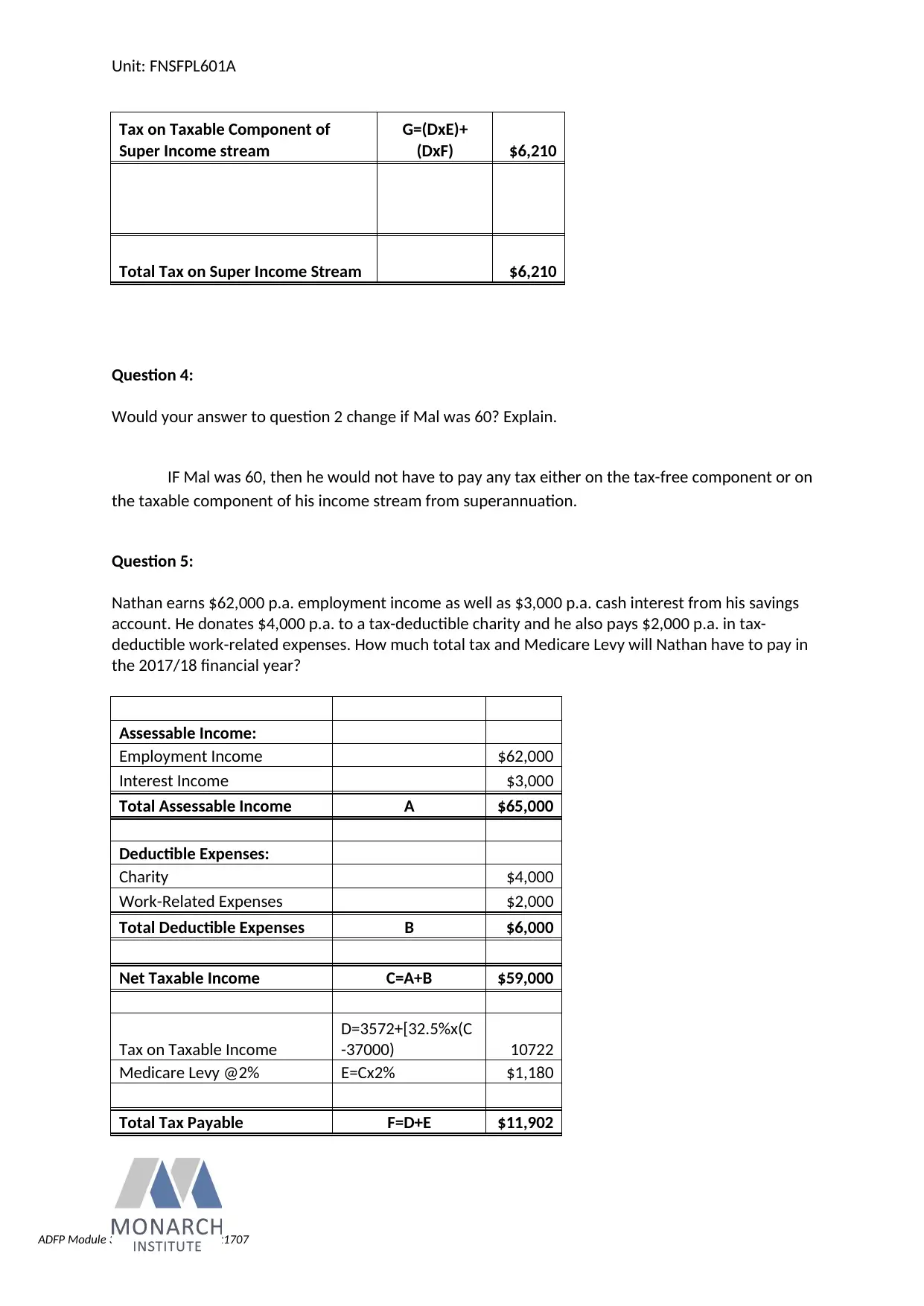

Unit: FNSFPL601A

Tax on Taxable Component of

Super Income stream

G=(DxE)+

(DxF) $6,210

Total Tax on Super Income Stream $6,210

Question 4:

Would your answer to question 2 change if Mal was 60? Explain.

IF Mal was 60, then he would not have to pay any tax either on the tax-free component or on

the taxable component of his income stream from superannuation.

Question 5:

Nathan earns $62,000 p.a. employment income as well as $3,000 p.a. cash interest from his savings

account. He donates $4,000 p.a. to a tax-deductible charity and he also pays $2,000 p.a. in tax-

deductible work-related expenses. How much total tax and Medicare Levy will Nathan have to pay in

the 2017/18 financial year?

Assessable Income:

Employment Income $62,000

Interest Income $3,000

Total Assessable Income A $65,000

Deductible Expenses:

Charity $4,000

Work-Related Expenses $2,000

Total Deductible Expenses B $6,000

Net Taxable Income C=A+B $59,000

Tax on Taxable Income

D=3572+[32.5%x(C

-37000) 10722

Medicare Levy @2% E=Cx2% $1,180

Total Tax Payable F=D+E $11,902

Unit: FNSFPL601A

Tax on Taxable Component of

Super Income stream

G=(DxE)+

(DxF) $6,210

Total Tax on Super Income Stream $6,210

Question 4:

Would your answer to question 2 change if Mal was 60? Explain.

IF Mal was 60, then he would not have to pay any tax either on the tax-free component or on

the taxable component of his income stream from superannuation.

Question 5:

Nathan earns $62,000 p.a. employment income as well as $3,000 p.a. cash interest from his savings

account. He donates $4,000 p.a. to a tax-deductible charity and he also pays $2,000 p.a. in tax-

deductible work-related expenses. How much total tax and Medicare Levy will Nathan have to pay in

the 2017/18 financial year?

Assessable Income:

Employment Income $62,000

Interest Income $3,000

Total Assessable Income A $65,000

Deductible Expenses:

Charity $4,000

Work-Related Expenses $2,000

Total Deductible Expenses B $6,000

Net Taxable Income C=A+B $59,000

Tax on Taxable Income

D=3572+[32.5%x(C

-37000) 10722

Medicare Levy @2% E=Cx2% $1,180

Total Tax Payable F=D+E $11,902

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

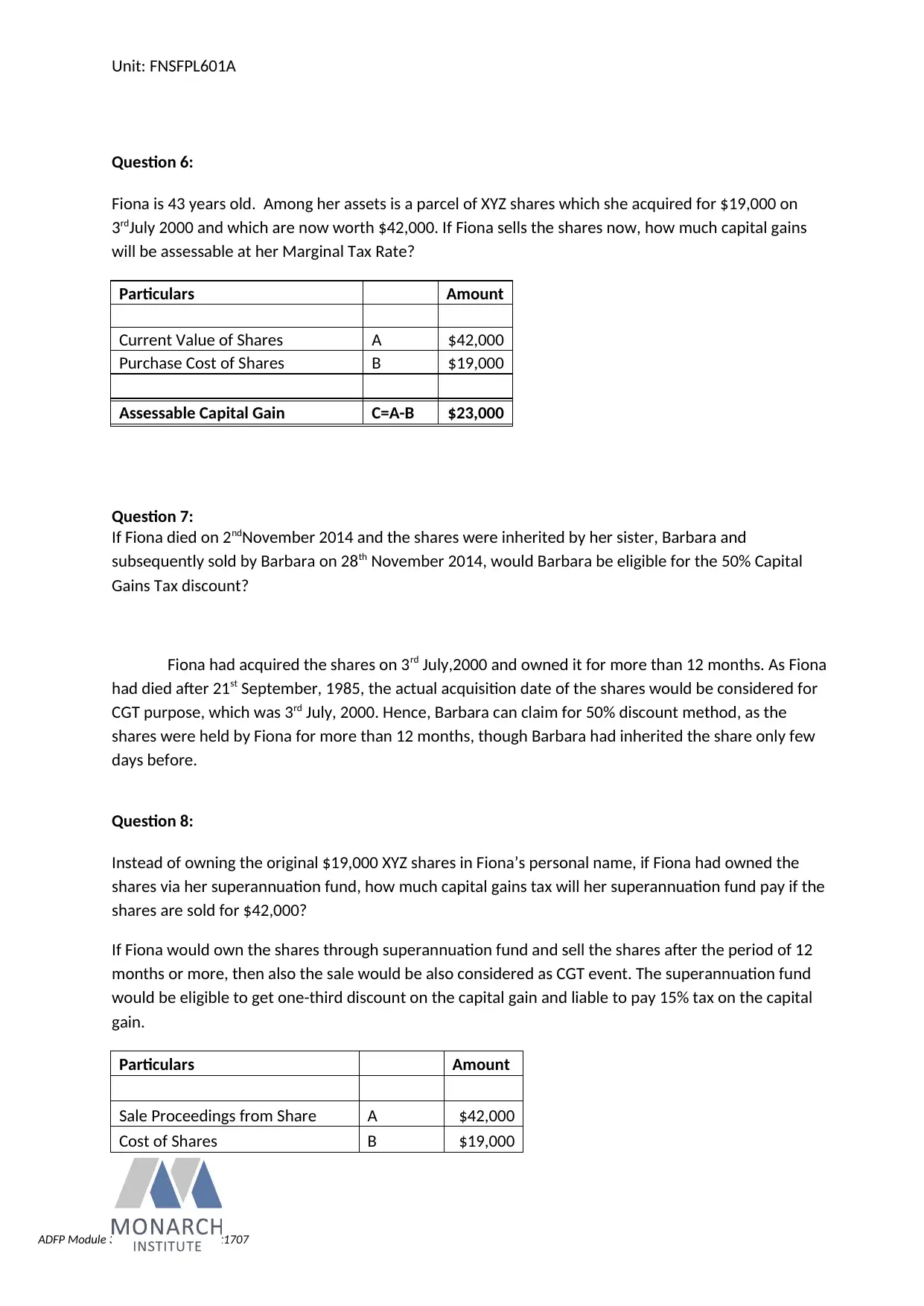

Question 6:

Fiona is 43 years old. Among her assets is a parcel of XYZ shares which she acquired for $19,000 on

3rdJuly 2000 and which are now worth $42,000. If Fiona sells the shares now, how much capital gains

will be assessable at her Marginal Tax Rate?

Particulars Amount

Current Value of Shares A $42,000

Purchase Cost of Shares B $19,000

Assessable Capital Gain C=A-B $23,000

Question 7:

If Fiona died on 2ndNovember 2014 and the shares were inherited by her sister, Barbara and

subsequently sold by Barbara on 28th November 2014, would Barbara be eligible for the 50% Capital

Gains Tax discount?

Fiona had acquired the shares on 3rd July,2000 and owned it for more than 12 months. As Fiona

had died after 21st September, 1985, the actual acquisition date of the shares would be considered for

CGT purpose, which was 3rd July, 2000. Hence, Barbara can claim for 50% discount method, as the

shares were held by Fiona for more than 12 months, though Barbara had inherited the share only few

days before.

Question 8:

Instead of owning the original $19,000 XYZ shares in Fiona’s personal name, if Fiona had owned the

shares via her superannuation fund, how much capital gains tax will her superannuation fund pay if the

shares are sold for $42,000?

If Fiona would own the shares through superannuation fund and sell the shares after the period of 12

months or more, then also the sale would be also considered as CGT event. The superannuation fund

would be eligible to get one-third discount on the capital gain and liable to pay 15% tax on the capital

gain.

Particulars Amount

Sale Proceedings from Share A $42,000

Cost of Shares B $19,000

Unit: FNSFPL601A

Question 6:

Fiona is 43 years old. Among her assets is a parcel of XYZ shares which she acquired for $19,000 on

3rdJuly 2000 and which are now worth $42,000. If Fiona sells the shares now, how much capital gains

will be assessable at her Marginal Tax Rate?

Particulars Amount

Current Value of Shares A $42,000

Purchase Cost of Shares B $19,000

Assessable Capital Gain C=A-B $23,000

Question 7:

If Fiona died on 2ndNovember 2014 and the shares were inherited by her sister, Barbara and

subsequently sold by Barbara on 28th November 2014, would Barbara be eligible for the 50% Capital

Gains Tax discount?

Fiona had acquired the shares on 3rd July,2000 and owned it for more than 12 months. As Fiona

had died after 21st September, 1985, the actual acquisition date of the shares would be considered for

CGT purpose, which was 3rd July, 2000. Hence, Barbara can claim for 50% discount method, as the

shares were held by Fiona for more than 12 months, though Barbara had inherited the share only few

days before.

Question 8:

Instead of owning the original $19,000 XYZ shares in Fiona’s personal name, if Fiona had owned the

shares via her superannuation fund, how much capital gains tax will her superannuation fund pay if the

shares are sold for $42,000?

If Fiona would own the shares through superannuation fund and sell the shares after the period of 12

months or more, then also the sale would be also considered as CGT event. The superannuation fund

would be eligible to get one-third discount on the capital gain and liable to pay 15% tax on the capital

gain.

Particulars Amount

Sale Proceedings from Share A $42,000

Cost of Shares B $19,000

ADFP Module 3 Taxation Assignment1707

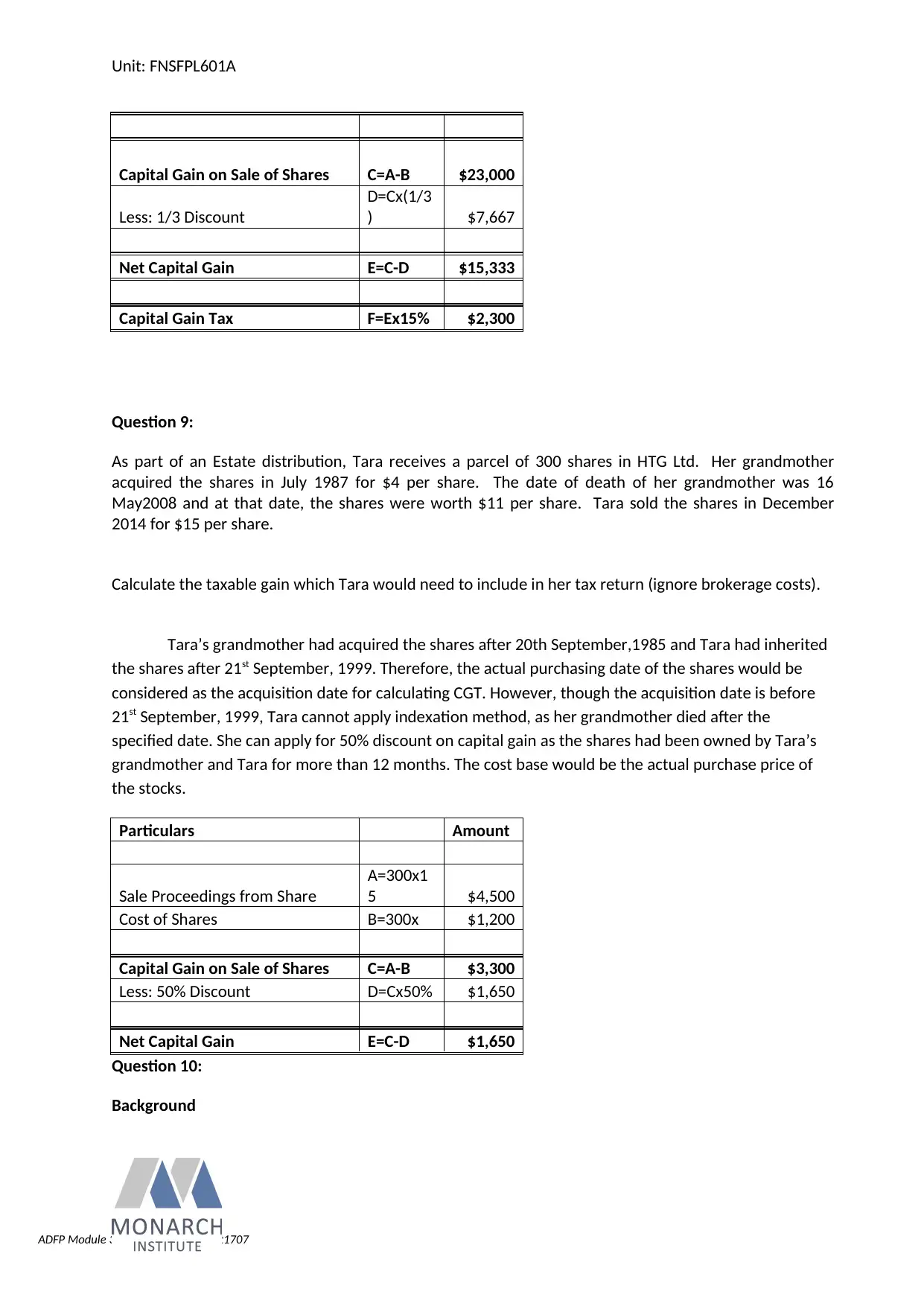

Unit: FNSFPL601A

Capital Gain on Sale of Shares C=A-B $23,000

Less: 1/3 Discount

D=Cx(1/3

) $7,667

Net Capital Gain E=C-D $15,333

Capital Gain Tax F=Ex15% $2,300

Question 9:

As part of an Estate distribution, Tara receives a parcel of 300 shares in HTG Ltd. Her grandmother

acquired the shares in July 1987 for $4 per share. The date of death of her grandmother was 16

May2008 and at that date, the shares were worth $11 per share. Tara sold the shares in December

2014 for $15 per share.

Calculate the taxable gain which Tara would need to include in her tax return (ignore brokerage costs).

Tara’s grandmother had acquired the shares after 20th September,1985 and Tara had inherited

the shares after 21st September, 1999. Therefore, the actual purchasing date of the shares would be

considered as the acquisition date for calculating CGT. However, though the acquisition date is before

21st September, 1999, Tara cannot apply indexation method, as her grandmother died after the

specified date. She can apply for 50% discount on capital gain as the shares had been owned by Tara’s

grandmother and Tara for more than 12 months. The cost base would be the actual purchase price of

the stocks.

Particulars Amount

Sale Proceedings from Share

A=300x1

5 $4,500

Cost of Shares B=300x $1,200

Capital Gain on Sale of Shares C=A-B $3,300

Less: 50% Discount D=Cx50% $1,650

Net Capital Gain E=C-D $1,650

Question 10:

Background

Unit: FNSFPL601A

Capital Gain on Sale of Shares C=A-B $23,000

Less: 1/3 Discount

D=Cx(1/3

) $7,667

Net Capital Gain E=C-D $15,333

Capital Gain Tax F=Ex15% $2,300

Question 9:

As part of an Estate distribution, Tara receives a parcel of 300 shares in HTG Ltd. Her grandmother

acquired the shares in July 1987 for $4 per share. The date of death of her grandmother was 16

May2008 and at that date, the shares were worth $11 per share. Tara sold the shares in December

2014 for $15 per share.

Calculate the taxable gain which Tara would need to include in her tax return (ignore brokerage costs).

Tara’s grandmother had acquired the shares after 20th September,1985 and Tara had inherited

the shares after 21st September, 1999. Therefore, the actual purchasing date of the shares would be

considered as the acquisition date for calculating CGT. However, though the acquisition date is before

21st September, 1999, Tara cannot apply indexation method, as her grandmother died after the

specified date. She can apply for 50% discount on capital gain as the shares had been owned by Tara’s

grandmother and Tara for more than 12 months. The cost base would be the actual purchase price of

the stocks.

Particulars Amount

Sale Proceedings from Share

A=300x1

5 $4,500

Cost of Shares B=300x $1,200

Capital Gain on Sale of Shares C=A-B $3,300

Less: 50% Discount D=Cx50% $1,650

Net Capital Gain E=C-D $1,650

Question 10:

Background

ADFP Module 3 Taxation Assignment1707

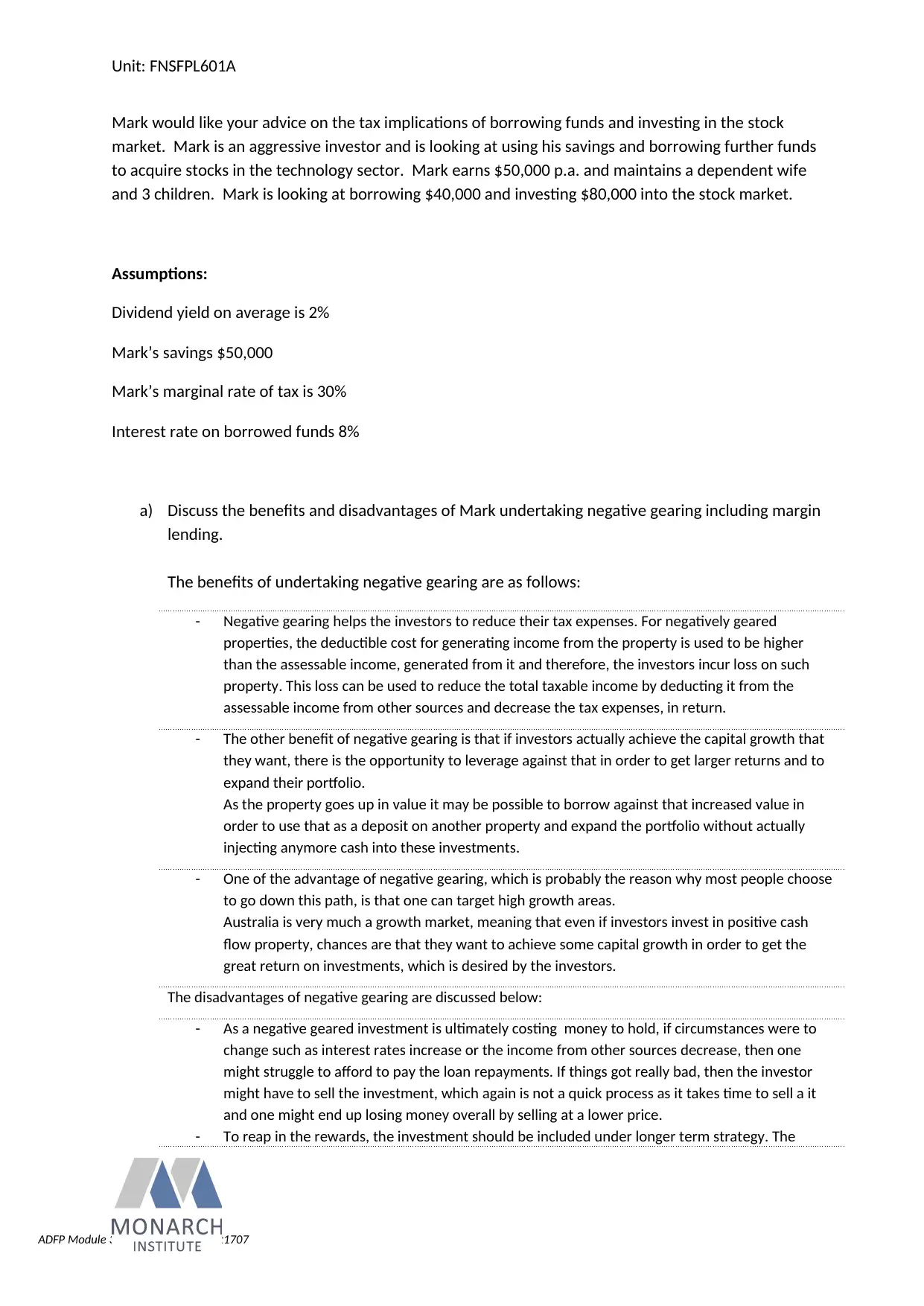

Unit: FNSFPL601A

Mark would like your advice on the tax implications of borrowing funds and investing in the stock

market. Mark is an aggressive investor and is looking at using his savings and borrowing further funds

to acquire stocks in the technology sector. Mark earns $50,000 p.a. and maintains a dependent wife

and 3 children. Mark is looking at borrowing $40,000 and investing $80,000 into the stock market.

Assumptions:

Dividend yield on average is 2%

Mark’s savings $50,000

Mark’s marginal rate of tax is 30%

Interest rate on borrowed funds 8%

a) Discuss the benefits and disadvantages of Mark undertaking negative gearing including margin

lending.

The benefits of undertaking negative gearing are as follows:

- Negative gearing helps the investors to reduce their tax expenses. For negatively geared

properties, the deductible cost for generating income from the property is used to be higher

than the assessable income, generated from it and therefore, the investors incur loss on such

property. This loss can be used to reduce the total taxable income by deducting it from the

assessable income from other sources and decrease the tax expenses, in return.

- The other benefit of negative gearing is that if investors actually achieve the capital growth that

they want, there is the opportunity to leverage against that in order to get larger returns and to

expand their portfolio.

As the property goes up in value it may be possible to borrow against that increased value in

order to use that as a deposit on another property and expand the portfolio without actually

injecting anymore cash into these investments.

- One of the advantage of negative gearing, which is probably the reason why most people choose

to go down this path, is that one can target high growth areas.

Australia is very much a growth market, meaning that even if investors invest in positive cash

flow property, chances are that they want to achieve some capital growth in order to get the

great return on investments, which is desired by the investors.

The disadvantages of negative gearing are discussed below:

- As a negative geared investment is ultimately costing money to hold, if circumstances were to

change such as interest rates increase or the income from other sources decrease, then one

might struggle to afford to pay the loan repayments. If things got really bad, then the investor

might have to sell the investment, which again is not a quick process as it takes time to sell a it

and one might end up losing money overall by selling at a lower price.

- To reap in the rewards, the investment should be included under longer term strategy. The

Unit: FNSFPL601A

Mark would like your advice on the tax implications of borrowing funds and investing in the stock

market. Mark is an aggressive investor and is looking at using his savings and borrowing further funds

to acquire stocks in the technology sector. Mark earns $50,000 p.a. and maintains a dependent wife

and 3 children. Mark is looking at borrowing $40,000 and investing $80,000 into the stock market.

Assumptions:

Dividend yield on average is 2%

Mark’s savings $50,000

Mark’s marginal rate of tax is 30%

Interest rate on borrowed funds 8%

a) Discuss the benefits and disadvantages of Mark undertaking negative gearing including margin

lending.

The benefits of undertaking negative gearing are as follows:

- Negative gearing helps the investors to reduce their tax expenses. For negatively geared

properties, the deductible cost for generating income from the property is used to be higher

than the assessable income, generated from it and therefore, the investors incur loss on such

property. This loss can be used to reduce the total taxable income by deducting it from the

assessable income from other sources and decrease the tax expenses, in return.

- The other benefit of negative gearing is that if investors actually achieve the capital growth that

they want, there is the opportunity to leverage against that in order to get larger returns and to

expand their portfolio.

As the property goes up in value it may be possible to borrow against that increased value in

order to use that as a deposit on another property and expand the portfolio without actually

injecting anymore cash into these investments.

- One of the advantage of negative gearing, which is probably the reason why most people choose

to go down this path, is that one can target high growth areas.

Australia is very much a growth market, meaning that even if investors invest in positive cash

flow property, chances are that they want to achieve some capital growth in order to get the

great return on investments, which is desired by the investors.

The disadvantages of negative gearing are discussed below:

- As a negative geared investment is ultimately costing money to hold, if circumstances were to

change such as interest rates increase or the income from other sources decrease, then one

might struggle to afford to pay the loan repayments. If things got really bad, then the investor

might have to sell the investment, which again is not a quick process as it takes time to sell a it

and one might end up losing money overall by selling at a lower price.

- To reap in the rewards, the investment should be included under longer term strategy. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 3 Taxation Assignment1707

Unit: FNSFPL601A

longer one hold on to the investment, the greater the chance the investment will grow and

double in value, particularly if it is held for ten years over a full investment cycle. It will not work

if it is hold for one year or so

- If any investor is making a loss, then if he/she requires future loans, then a lender might be more

reluctant to increase the borrowing capacity as the investment in not generating any positive net

income.

b) In whose name should the acquisition of a negatively geared investment be generally held

within the family? Would it make a difference if the investment were positively geared?

Explain.

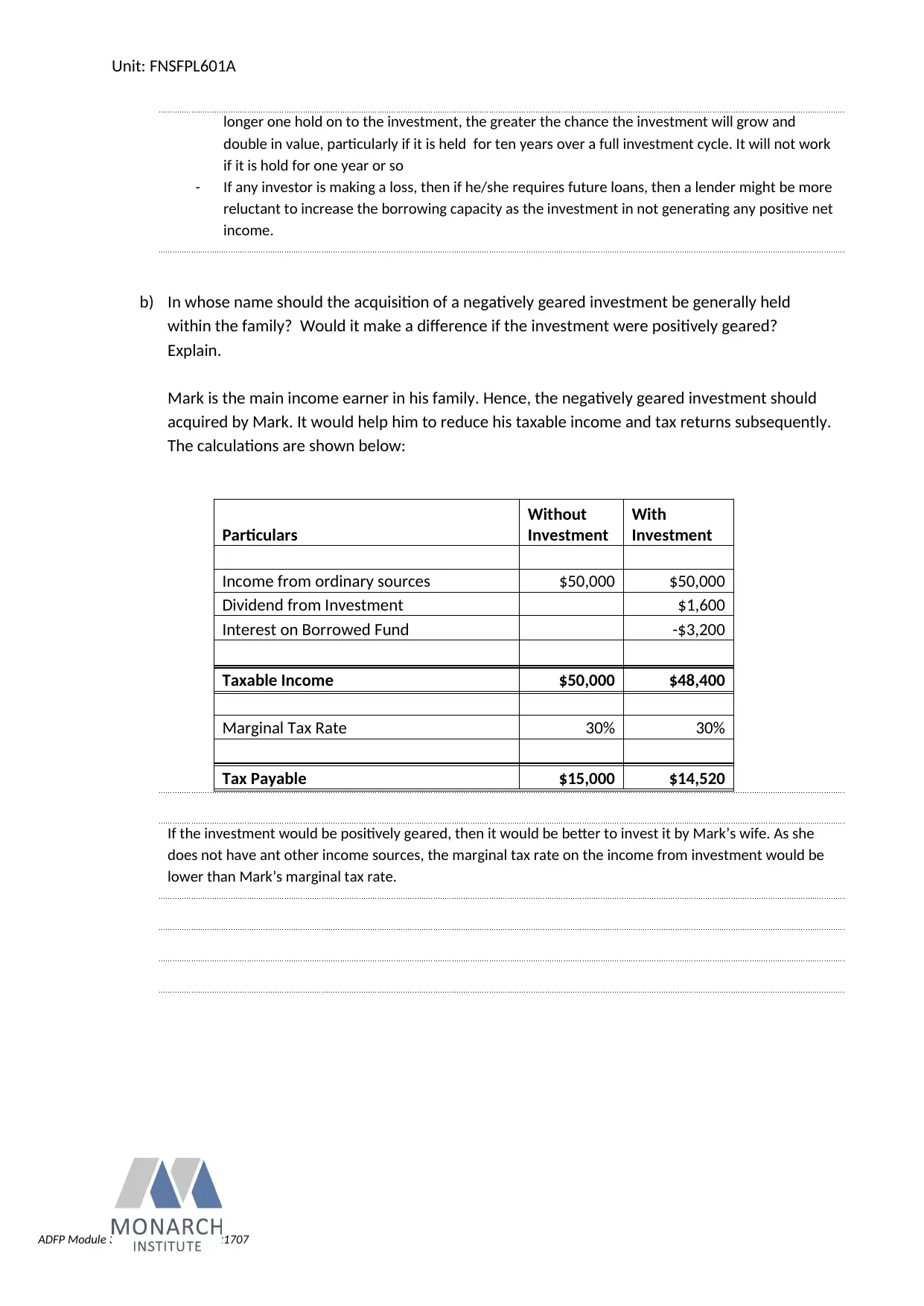

Mark is the main income earner in his family. Hence, the negatively geared investment should

acquired by Mark. It would help him to reduce his taxable income and tax returns subsequently.

The calculations are shown below:

Particulars

Without

Investment

With

Investment

Income from ordinary sources $50,000 $50,000

Dividend from Investment $1,600

Interest on Borrowed Fund -$3,200

Taxable Income $50,000 $48,400

Marginal Tax Rate 30% 30%

Tax Payable $15,000 $14,520

If the investment would be positively geared, then it would be better to invest it by Mark’s wife. As she

does not have ant other income sources, the marginal tax rate on the income from investment would be

lower than Mark’s marginal tax rate.

Unit: FNSFPL601A

longer one hold on to the investment, the greater the chance the investment will grow and

double in value, particularly if it is held for ten years over a full investment cycle. It will not work

if it is hold for one year or so

- If any investor is making a loss, then if he/she requires future loans, then a lender might be more

reluctant to increase the borrowing capacity as the investment in not generating any positive net

income.

b) In whose name should the acquisition of a negatively geared investment be generally held

within the family? Would it make a difference if the investment were positively geared?

Explain.

Mark is the main income earner in his family. Hence, the negatively geared investment should

acquired by Mark. It would help him to reduce his taxable income and tax returns subsequently.

The calculations are shown below:

Particulars

Without

Investment

With

Investment

Income from ordinary sources $50,000 $50,000

Dividend from Investment $1,600

Interest on Borrowed Fund -$3,200

Taxable Income $50,000 $48,400

Marginal Tax Rate 30% 30%

Tax Payable $15,000 $14,520

If the investment would be positively geared, then it would be better to invest it by Mark’s wife. As she

does not have ant other income sources, the marginal tax rate on the income from investment would be

lower than Mark’s marginal tax rate.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.