Management Accounting Systems Adaption for Financial Problems

VerifiedAdded on 2023/01/13

|16

|3499

|49

Report

AI Summary

This report delves into the application of management accounting techniques within Prime Furniture, focusing on how these tools aid in strategic decision-making and business expansion. It presents a comparative analysis of income statements generated through marginal and absorption costing techniques, highlighting the differences in net operating income and the importance of break-even point analysis. The report also explores various management accounting techniques such as margin analysis, constraint analysis, capital budgeting, inventory valuation, and trend analysis, discussing their roles in achieving business goals. Furthermore, it examines the advantages and disadvantages of planning tools like budgetary control, cost-volume-profit analysis, and pricing strategies, emphasizing their application in forecasting budgets. The report concludes by addressing how management accounting systems can be adapted to respond to financial problems and ensure sustainable success through demand forecasting and effective cost management, crucial for maintaining long-term performance.

B10781

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...................................................................................................................................................... 3

TASK 2......................................................................................................................................................................... 4

P3 Income statement through marginal costing and absorption costing technique:.................4

M2 Range of management accounting techniques:.................................................................................. 7

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control:........................................................................................................................................................................ 8

M3. Different planning tools and their application for forecasting budgets................................10

P5. Adaption of management accounting systems to respond to financial problems and

sustainable success:............................................................................................................................................ 11

CONCLUSION......................................................................................................................................................... 14

REFERENCES......................................................................................................................................................... 15

INTRODUCTION...................................................................................................................................................... 3

TASK 2......................................................................................................................................................................... 4

P3 Income statement through marginal costing and absorption costing technique:.................4

M2 Range of management accounting techniques:.................................................................................. 7

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control:........................................................................................................................................................................ 8

M3. Different planning tools and their application for forecasting budgets................................10

P5. Adaption of management accounting systems to respond to financial problems and

sustainable success:............................................................................................................................................ 11

CONCLUSION......................................................................................................................................................... 14

REFERENCES......................................................................................................................................................... 15

INTRODUCTION

Management accounting is new concept practicing by every organization. Previously accounting

was only used and applied by junior accountants and tally department due lack of understanding

about accounting reports; there were no gap filling tool available to interpret the result in simple

terms. Decision making team requires to understand what is written in report regardless it cannot

give its judgment whether to buy particular project or avoid it. The application of management

accounting technique makes it simple for strategic manager to understand the crux of report and

analyze the whole effect in single read. This project is based on these accounting tools which

help Prime furniture a leading furniture company to take several critical decisions on business

expansions. Additional to this report will show how depending on only one forecasting tool

could harm company’s yearly earnings and how mishandling of fund can impact company’s

profit.

Management accounting is new concept practicing by every organization. Previously accounting

was only used and applied by junior accountants and tally department due lack of understanding

about accounting reports; there were no gap filling tool available to interpret the result in simple

terms. Decision making team requires to understand what is written in report regardless it cannot

give its judgment whether to buy particular project or avoid it. The application of management

accounting technique makes it simple for strategic manager to understand the crux of report and

analyze the whole effect in single read. This project is based on these accounting tools which

help Prime furniture a leading furniture company to take several critical decisions on business

expansions. Additional to this report will show how depending on only one forecasting tool

could harm company’s yearly earnings and how mishandling of fund can impact company’s

profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

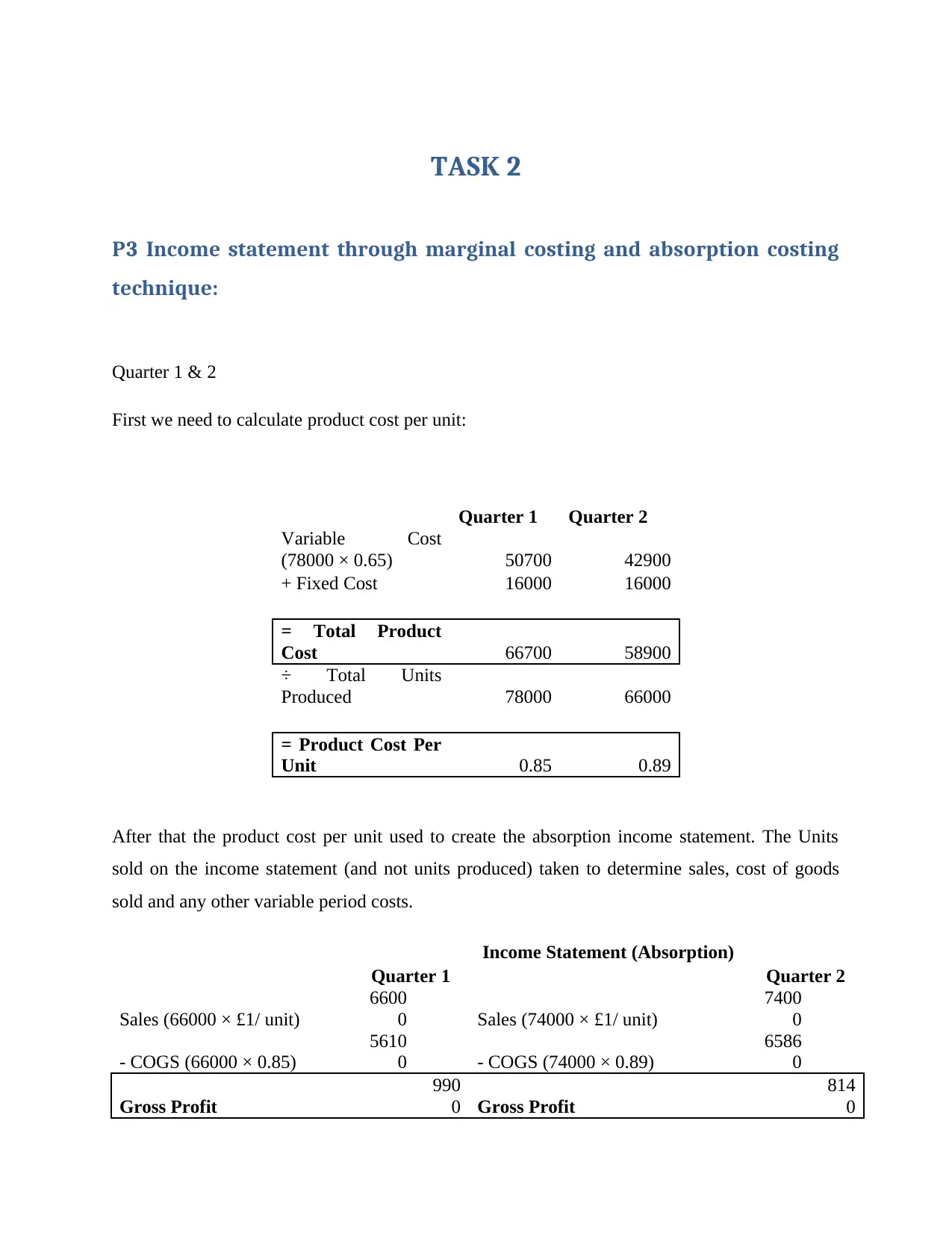

P3 Income statement through marginal costing and absorption costing

technique:

Quarter 1 & 2

First we need to calculate product cost per unit:

Quarter 1 Quarter 2

Variable Cost

(78000 × 0.65) 50700 42900

+ Fixed Cost 16000 16000

= Total Product

Cost 66700 58900

÷ Total Units

Produced 78000 66000

= Product Cost Per

Unit 0.85 0.89

After that the product cost per unit used to create the absorption income statement. The Units

sold on the income statement (and not units produced) taken to determine sales, cost of goods

sold and any other variable period costs.

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/ unit)

6600

0 Sales (74000 × £1/ unit)

7400

0

- COGS (66000 × 0.85)

5610

0 - COGS (74000 × 0.89)

6586

0

Gross Profit

990

0 Gross Profit

814

0

P3 Income statement through marginal costing and absorption costing

technique:

Quarter 1 & 2

First we need to calculate product cost per unit:

Quarter 1 Quarter 2

Variable Cost

(78000 × 0.65) 50700 42900

+ Fixed Cost 16000 16000

= Total Product

Cost 66700 58900

÷ Total Units

Produced 78000 66000

= Product Cost Per

Unit 0.85 0.89

After that the product cost per unit used to create the absorption income statement. The Units

sold on the income statement (and not units produced) taken to determine sales, cost of goods

sold and any other variable period costs.

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/ unit)

6600

0 Sales (74000 × £1/ unit)

7400

0

- COGS (66000 × 0.85)

5610

0 - COGS (74000 × 0.89)

6586

0

Gross Profit

990

0 Gross Profit

814

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

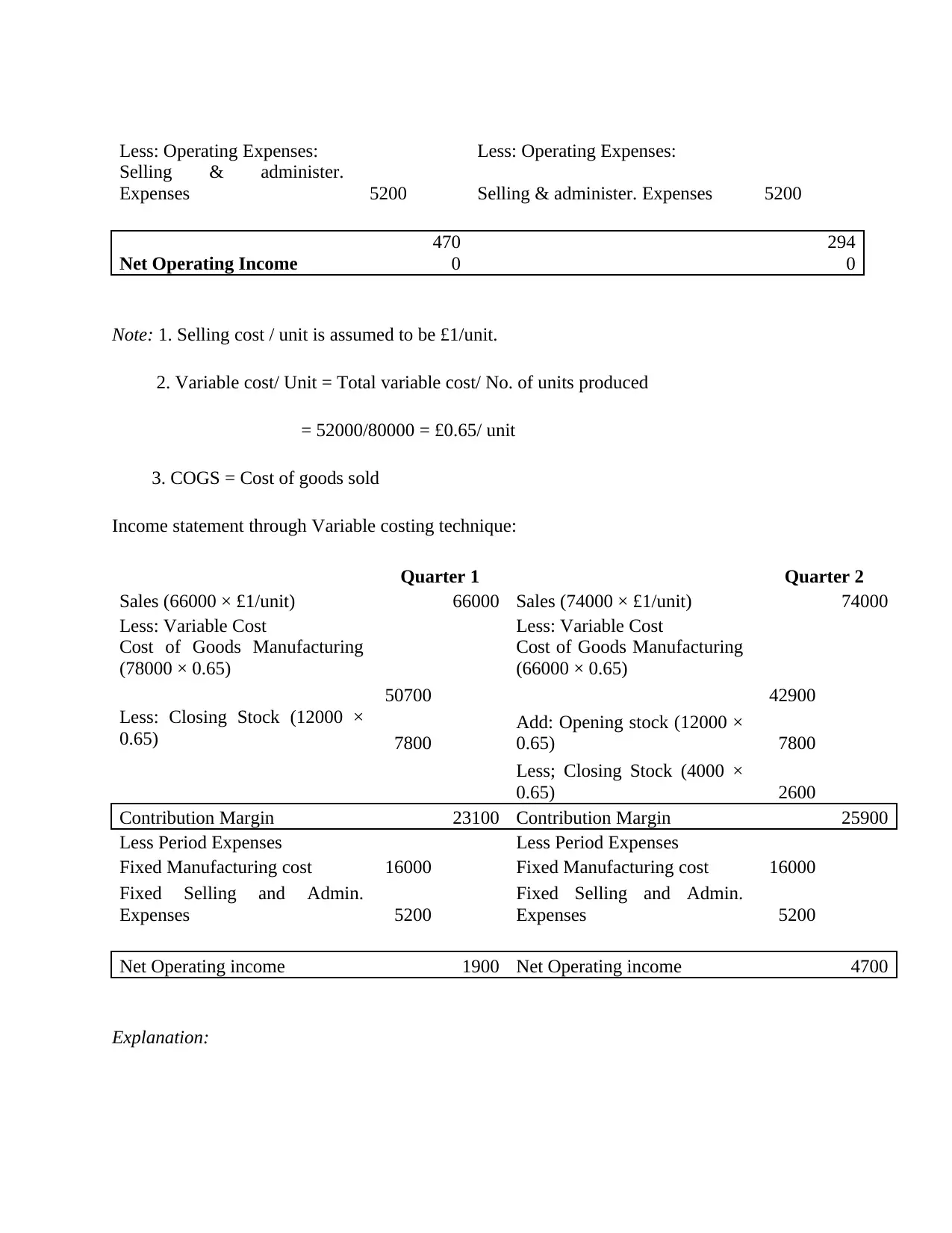

Less: Operating Expenses: Less: Operating Expenses:

Selling & administer.

Expenses 5200 Selling & administer. Expenses 5200

Net Operating Income

470

0

294

0

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 × £1/unit) 66000 Sales (74000 × £1/unit) 74000

Less: Variable Cost Less: Variable Cost

Cost of Goods Manufacturing

(78000 × 0.65)

50700

Cost of Goods Manufacturing

(66000 × 0.65)

42900

Less: Closing Stock (12000 ×

0.65) 7800

Add: Opening stock (12000 ×

0.65) 7800

Less; Closing Stock (4000 ×

0.65) 2600

Contribution Margin 23100 Contribution Margin 25900

Less Period Expenses Less Period Expenses

Fixed Manufacturing cost 16000 Fixed Manufacturing cost 16000

Fixed Selling and Admin.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 1900 Net Operating income 4700

Explanation:

Selling & administer.

Expenses 5200 Selling & administer. Expenses 5200

Net Operating Income

470

0

294

0

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 × £1/unit) 66000 Sales (74000 × £1/unit) 74000

Less: Variable Cost Less: Variable Cost

Cost of Goods Manufacturing

(78000 × 0.65)

50700

Cost of Goods Manufacturing

(66000 × 0.65)

42900

Less: Closing Stock (12000 ×

0.65) 7800

Add: Opening stock (12000 ×

0.65) 7800

Less; Closing Stock (4000 ×

0.65) 2600

Contribution Margin 23100 Contribution Margin 25900

Less Period Expenses Less Period Expenses

Fixed Manufacturing cost 16000 Fixed Manufacturing cost 16000

Fixed Selling and Admin.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 1900 Net Operating income 4700

Explanation:

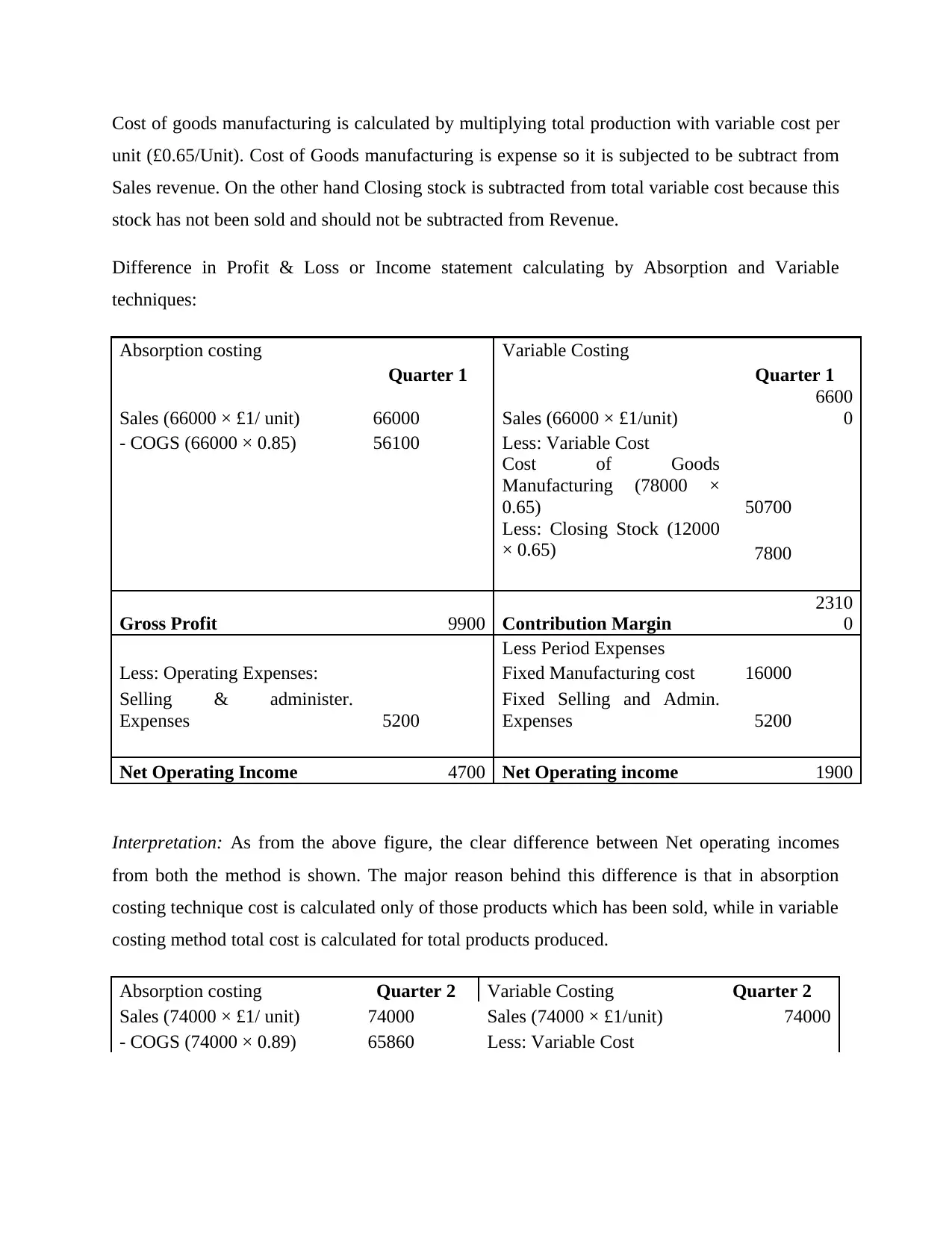

Cost of goods manufacturing is calculated by multiplying total production with variable cost per

unit (£0.65/Unit). Cost of Goods manufacturing is expense so it is subjected to be subtract from

Sales revenue. On the other hand Closing stock is subtracted from total variable cost because this

stock has not been sold and should not be subtracted from Revenue.

Difference in Profit & Loss or Income statement calculating by Absorption and Variable

techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/ unit) 66000 Sales (66000 × £1/unit)

6600

0

- COGS (66000 × 0.85) 56100 Less: Variable Cost

Cost of Goods

Manufacturing (78000 ×

0.65) 50700

Less: Closing Stock (12000

× 0.65) 7800

Gross Profit 9900 Contribution Margin

2310

0

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administer.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating Income 4700 Net Operating income 1900

Interpretation: As from the above figure, the clear difference between Net operating incomes

from both the method is shown. The major reason behind this difference is that in absorption

costing technique cost is calculated only of those products which has been sold, while in variable

costing method total cost is calculated for total products produced.

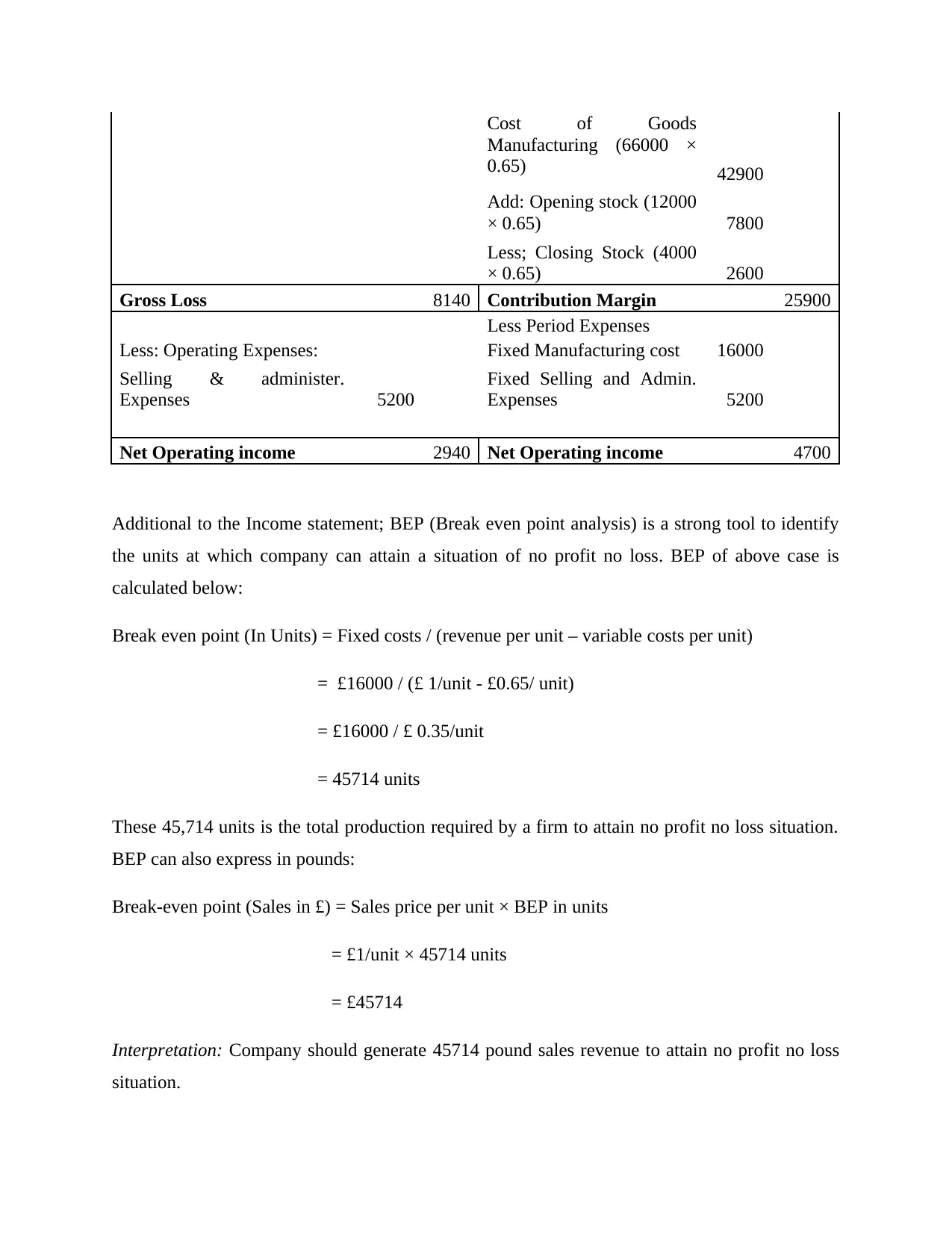

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/ unit) 74000 Sales (74000 × £1/unit) 74000

- COGS (74000 × 0.89) 65860 Less: Variable Cost

unit (£0.65/Unit). Cost of Goods manufacturing is expense so it is subjected to be subtract from

Sales revenue. On the other hand Closing stock is subtracted from total variable cost because this

stock has not been sold and should not be subtracted from Revenue.

Difference in Profit & Loss or Income statement calculating by Absorption and Variable

techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/ unit) 66000 Sales (66000 × £1/unit)

6600

0

- COGS (66000 × 0.85) 56100 Less: Variable Cost

Cost of Goods

Manufacturing (78000 ×

0.65) 50700

Less: Closing Stock (12000

× 0.65) 7800

Gross Profit 9900 Contribution Margin

2310

0

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administer.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating Income 4700 Net Operating income 1900

Interpretation: As from the above figure, the clear difference between Net operating incomes

from both the method is shown. The major reason behind this difference is that in absorption

costing technique cost is calculated only of those products which has been sold, while in variable

costing method total cost is calculated for total products produced.

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/ unit) 74000 Sales (74000 × £1/unit) 74000

- COGS (74000 × 0.89) 65860 Less: Variable Cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of Goods

Manufacturing (66000 ×

0.65) 42900

Add: Opening stock (12000

× 0.65) 7800

Less; Closing Stock (4000

× 0.65) 2600

Gross Loss 8140 Contribution Margin 25900

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administer.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 2940 Net Operating income 4700

Additional to the Income statement; BEP (Break even point analysis) is a strong tool to identify

the units at which company can attain a situation of no profit no loss. BEP of above case is

calculated below:

Break even point (In Units) = Fixed costs / (revenue per unit – variable costs per unit)

= £16000 / (£ 1/unit - £0.65/ unit)

= £16000 / £ 0.35/unit

= 45714 units

These 45,714 units is the total production required by a firm to attain no profit no loss situation.

BEP can also express in pounds:

Break-even point (Sales in £) = Sales price per unit × BEP in units

= £1/unit × 45714 units

= £45714

Interpretation: Company should generate 45714 pound sales revenue to attain no profit no loss

situation.

Manufacturing (66000 ×

0.65) 42900

Add: Opening stock (12000

× 0.65) 7800

Less; Closing Stock (4000

× 0.65) 2600

Gross Loss 8140 Contribution Margin 25900

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administer.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 2940 Net Operating income 4700

Additional to the Income statement; BEP (Break even point analysis) is a strong tool to identify

the units at which company can attain a situation of no profit no loss. BEP of above case is

calculated below:

Break even point (In Units) = Fixed costs / (revenue per unit – variable costs per unit)

= £16000 / (£ 1/unit - £0.65/ unit)

= £16000 / £ 0.35/unit

= 45714 units

These 45,714 units is the total production required by a firm to attain no profit no loss situation.

BEP can also express in pounds:

Break-even point (Sales in £) = Sales price per unit × BEP in units

= £1/unit × 45714 units

= £45714

Interpretation: Company should generate 45714 pound sales revenue to attain no profit no loss

situation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

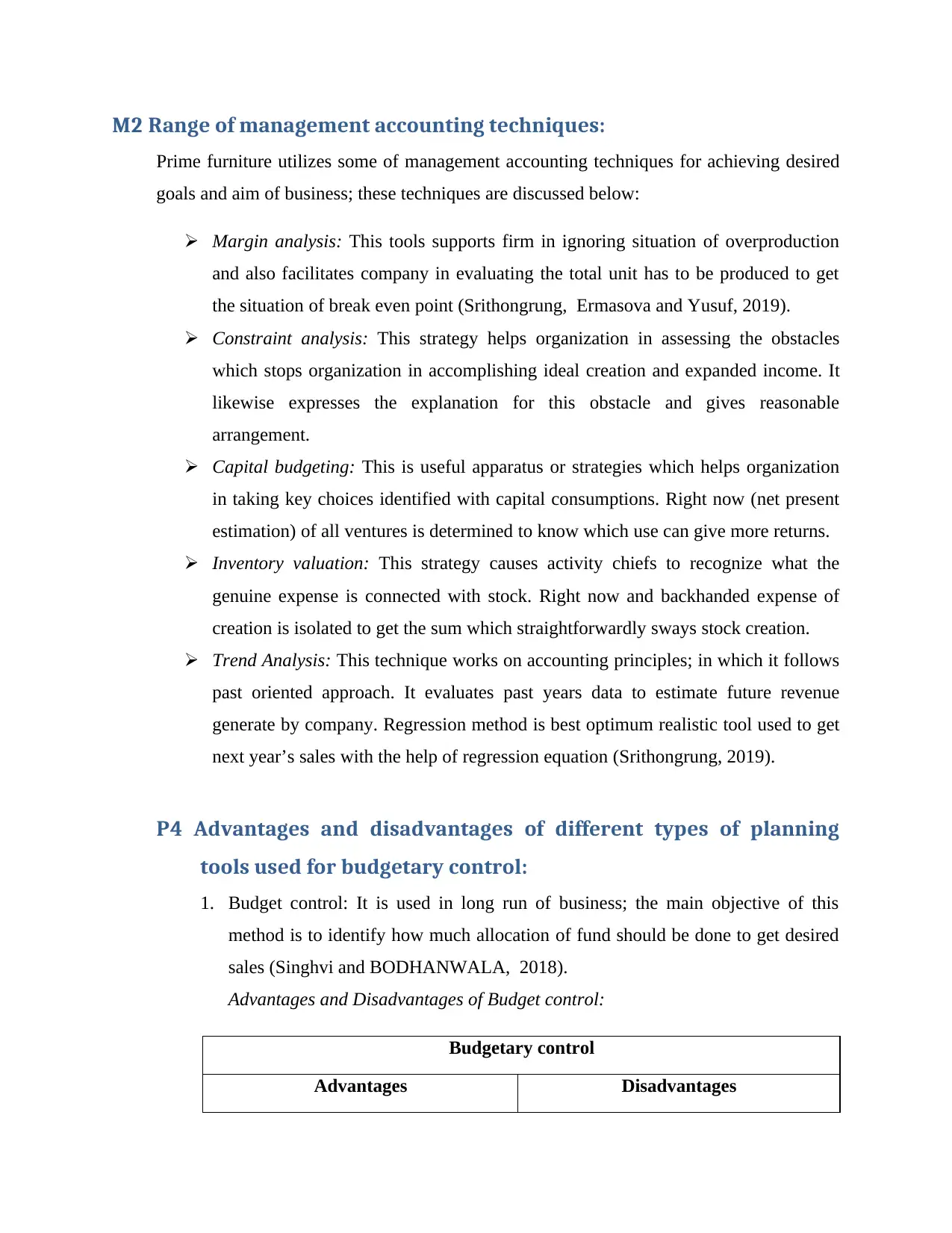

M2 Range of management accounting techniques:

Prime furniture utilizes some of management accounting techniques for achieving desired

goals and aim of business; these techniques are discussed below:

Margin analysis: This tools supports firm in ignoring situation of overproduction

and also facilitates company in evaluating the total unit has to be produced to get

the situation of break even point (Srithongrung, Ermasova and Yusuf, 2019).

Constraint analysis: This strategy helps organization in assessing the obstacles

which stops organization in accomplishing ideal creation and expanded income. It

likewise expresses the explanation for this obstacle and gives reasonable

arrangement.

Capital budgeting: This is useful apparatus or strategies which helps organization

in taking key choices identified with capital consumptions. Right now (net present

estimation) of all ventures is determined to know which use can give more returns.

Inventory valuation: This strategy causes activity chiefs to recognize what the

genuine expense is connected with stock. Right now and backhanded expense of

creation is isolated to get the sum which straightforwardly sways stock creation.

Trend Analysis: This technique works on accounting principles; in which it follows

past oriented approach. It evaluates past years data to estimate future revenue

generate by company. Regression method is best optimum realistic tool used to get

next year’s sales with the help of regression equation (Srithongrung, 2019).

P4 Advantages and disadvantages of different types of planning

tools used for budgetary control:

1. Budget control: It is used in long run of business; the main objective of this

method is to identify how much allocation of fund should be done to get desired

sales (Singhvi and BODHANWALA, 2018).

Advantages and Disadvantages of Budget control:

Budgetary control

Advantages Disadvantages

Prime furniture utilizes some of management accounting techniques for achieving desired

goals and aim of business; these techniques are discussed below:

Margin analysis: This tools supports firm in ignoring situation of overproduction

and also facilitates company in evaluating the total unit has to be produced to get

the situation of break even point (Srithongrung, Ermasova and Yusuf, 2019).

Constraint analysis: This strategy helps organization in assessing the obstacles

which stops organization in accomplishing ideal creation and expanded income. It

likewise expresses the explanation for this obstacle and gives reasonable

arrangement.

Capital budgeting: This is useful apparatus or strategies which helps organization

in taking key choices identified with capital consumptions. Right now (net present

estimation) of all ventures is determined to know which use can give more returns.

Inventory valuation: This strategy causes activity chiefs to recognize what the

genuine expense is connected with stock. Right now and backhanded expense of

creation is isolated to get the sum which straightforwardly sways stock creation.

Trend Analysis: This technique works on accounting principles; in which it follows

past oriented approach. It evaluates past years data to estimate future revenue

generate by company. Regression method is best optimum realistic tool used to get

next year’s sales with the help of regression equation (Srithongrung, 2019).

P4 Advantages and disadvantages of different types of planning

tools used for budgetary control:

1. Budget control: It is used in long run of business; the main objective of this

method is to identify how much allocation of fund should be done to get desired

sales (Singhvi and BODHANWALA, 2018).

Advantages and Disadvantages of Budget control:

Budgetary control

Advantages Disadvantages

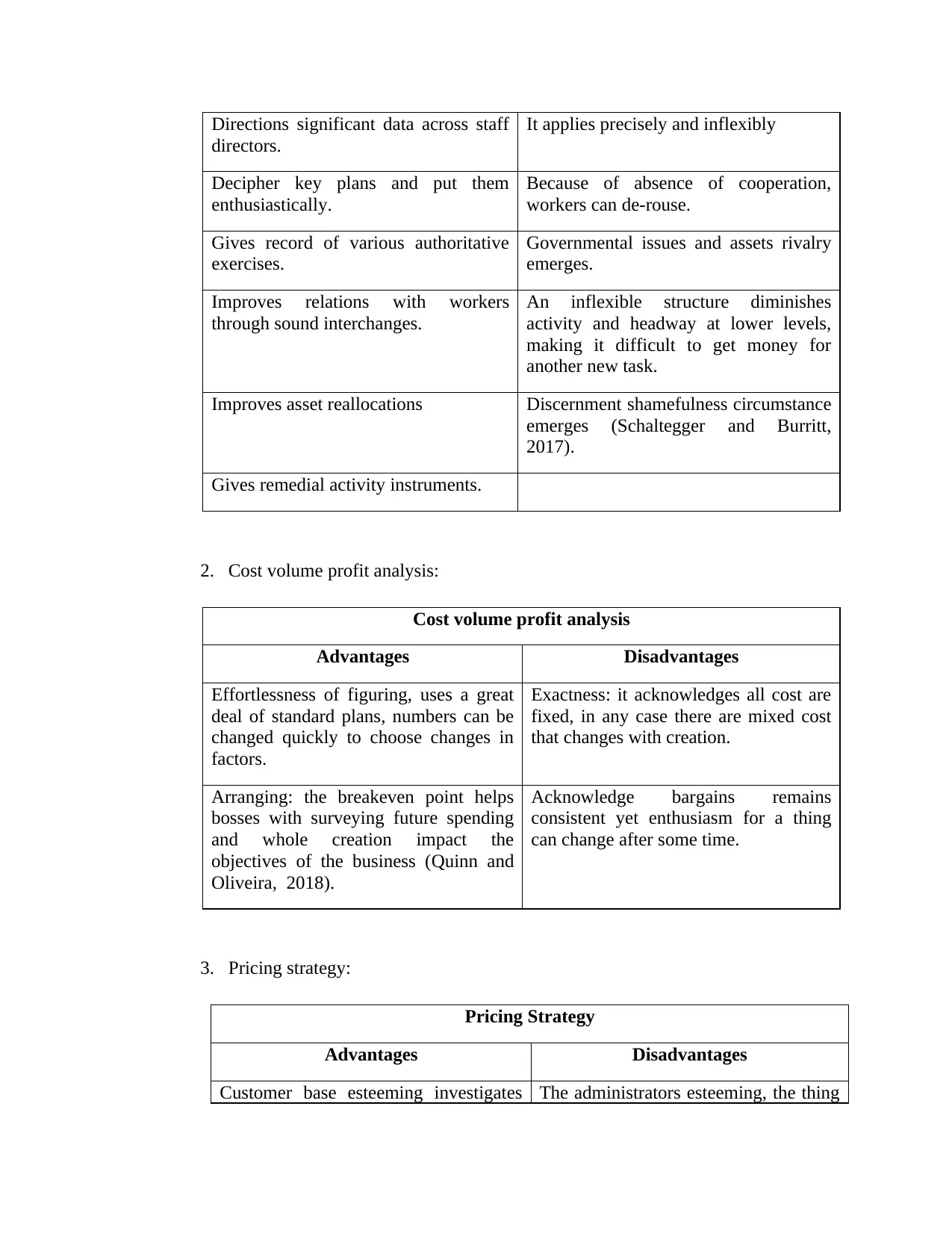

Directions significant data across staff

directors.

It applies precisely and inflexibly

Decipher key plans and put them

enthusiastically.

Because of absence of cooperation,

workers can de-rouse.

Gives record of various authoritative

exercises.

Governmental issues and assets rivalry

emerges.

Improves relations with workers

through sound interchanges.

An inflexible structure diminishes

activity and headway at lower levels,

making it difficult to get money for

another new task.

Improves asset reallocations Discernment shamefulness circumstance

emerges (Schaltegger and Burritt,

2017).

Gives remedial activity instruments.

2. Cost volume profit analysis:

Cost volume profit analysis

Advantages Disadvantages

Effortlessness of figuring, uses a great

deal of standard plans, numbers can be

changed quickly to choose changes in

factors.

Exactness: it acknowledges all cost are

fixed, in any case there are mixed cost

that changes with creation.

Arranging: the breakeven point helps

bosses with surveying future spending

and whole creation impact the

objectives of the business (Quinn and

Oliveira, 2018).

Acknowledge bargains remains

consistent yet enthusiasm for a thing

can change after some time.

3. Pricing strategy:

Pricing Strategy

Advantages Disadvantages

Customer base esteeming investigates The administrators esteeming, the thing

directors.

It applies precisely and inflexibly

Decipher key plans and put them

enthusiastically.

Because of absence of cooperation,

workers can de-rouse.

Gives record of various authoritative

exercises.

Governmental issues and assets rivalry

emerges.

Improves relations with workers

through sound interchanges.

An inflexible structure diminishes

activity and headway at lower levels,

making it difficult to get money for

another new task.

Improves asset reallocations Discernment shamefulness circumstance

emerges (Schaltegger and Burritt,

2017).

Gives remedial activity instruments.

2. Cost volume profit analysis:

Cost volume profit analysis

Advantages Disadvantages

Effortlessness of figuring, uses a great

deal of standard plans, numbers can be

changed quickly to choose changes in

factors.

Exactness: it acknowledges all cost are

fixed, in any case there are mixed cost

that changes with creation.

Arranging: the breakeven point helps

bosses with surveying future spending

and whole creation impact the

objectives of the business (Quinn and

Oliveira, 2018).

Acknowledge bargains remains

consistent yet enthusiasm for a thing

can change after some time.

3. Pricing strategy:

Pricing Strategy

Advantages Disadvantages

Customer base esteeming investigates The administrators esteeming, the thing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

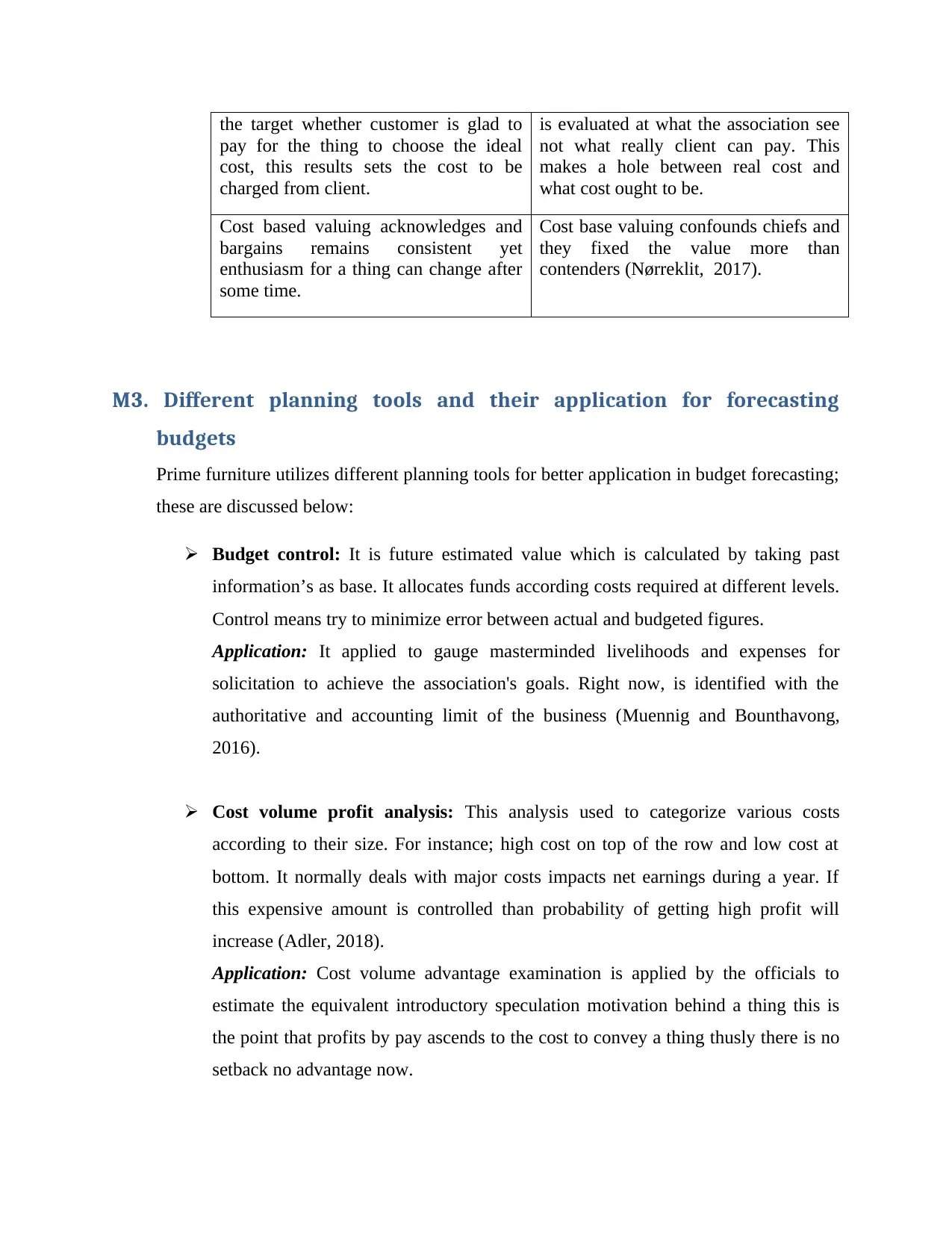

the target whether customer is glad to

pay for the thing to choose the ideal

cost, this results sets the cost to be

charged from client.

is evaluated at what the association see

not what really client can pay. This

makes a hole between real cost and

what cost ought to be.

Cost based valuing acknowledges and

bargains remains consistent yet

enthusiasm for a thing can change after

some time.

Cost base valuing confounds chiefs and

they fixed the value more than

contenders (Nørreklit, 2017).

M3. Different planning tools and their application for forecasting

budgets

Prime furniture utilizes different planning tools for better application in budget forecasting;

these are discussed below:

Budget control: It is future estimated value which is calculated by taking past

information’s as base. It allocates funds according costs required at different levels.

Control means try to minimize error between actual and budgeted figures.

Application: It applied to gauge masterminded livelihoods and expenses for

solicitation to achieve the association's goals. Right now, is identified with the

authoritative and accounting limit of the business (Muennig and Bounthavong,

2016).

Cost volume profit analysis: This analysis used to categorize various costs

according to their size. For instance; high cost on top of the row and low cost at

bottom. It normally deals with major costs impacts net earnings during a year. If

this expensive amount is controlled than probability of getting high profit will

increase (Adler, 2018).

Application: Cost volume advantage examination is applied by the officials to

estimate the equivalent introductory speculation motivation behind a thing this is

the point that profits by pay ascends to the cost to convey a thing thusly there is no

setback no advantage now.

pay for the thing to choose the ideal

cost, this results sets the cost to be

charged from client.

is evaluated at what the association see

not what really client can pay. This

makes a hole between real cost and

what cost ought to be.

Cost based valuing acknowledges and

bargains remains consistent yet

enthusiasm for a thing can change after

some time.

Cost base valuing confounds chiefs and

they fixed the value more than

contenders (Nørreklit, 2017).

M3. Different planning tools and their application for forecasting

budgets

Prime furniture utilizes different planning tools for better application in budget forecasting;

these are discussed below:

Budget control: It is future estimated value which is calculated by taking past

information’s as base. It allocates funds according costs required at different levels.

Control means try to minimize error between actual and budgeted figures.

Application: It applied to gauge masterminded livelihoods and expenses for

solicitation to achieve the association's goals. Right now, is identified with the

authoritative and accounting limit of the business (Muennig and Bounthavong,

2016).

Cost volume profit analysis: This analysis used to categorize various costs

according to their size. For instance; high cost on top of the row and low cost at

bottom. It normally deals with major costs impacts net earnings during a year. If

this expensive amount is controlled than probability of getting high profit will

increase (Adler, 2018).

Application: Cost volume advantage examination is applied by the officials to

estimate the equivalent introductory speculation motivation behind a thing this is

the point that profits by pay ascends to the cost to convey a thing thusly there is no

setback no advantage now.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pricing strategy: Price fixation of each commodity is not an easy task and requires

lots of real time analyses by company. As price of any product depends on how

much demand created in market and how much money is decided by customer to

willing to buy particular stock. It requires mathematical model and competitors

product price analyses prevailing in the same market and industry (Alawattage and

Wickramasinghe, 2018).

Application: It is applied to figure how firm can limit its expense to meet serious

cost lastly execute this methodology under specialists' watch. At that point the

objective is chosen, the executives pick a methodology considering interest, cost,

contenders expenses and offers, and esteeming technique. In budgetary control

estimating technique helps in getting the business income figure (Sales per unit ×

Units created).

P5. Adaption of management accounting systems to respond to

financial problems and sustainable success:

Financial problems are common in running business; these problems arises due to

lack of past report study, using outdated accounting regulations, not enough fund left

with company and improper settlement of cost of different heads (Malina, 2017).

Sustainable success is a term associated with maintaining better performance for

prolong period of time. Some of the management accounting tools is discussed

below:

1. Demand forecasting: It is the process of forecasting similarly as the

investigation of anticipating the conceivable enthusiasm for a thing or

organization later on. This figure relies upon past gauges of direct and the

procedure with designs in the present. From now on, it isn't simply guessing the

future intrigue yet is evaluating the intrigue tentatively and evenhandedly.

Through gauging request organization get data about most recent patterns of the

market and manufactured item appropriately to coordinate the interest (Jones and

et.al., 2018).

lots of real time analyses by company. As price of any product depends on how

much demand created in market and how much money is decided by customer to

willing to buy particular stock. It requires mathematical model and competitors

product price analyses prevailing in the same market and industry (Alawattage and

Wickramasinghe, 2018).

Application: It is applied to figure how firm can limit its expense to meet serious

cost lastly execute this methodology under specialists' watch. At that point the

objective is chosen, the executives pick a methodology considering interest, cost,

contenders expenses and offers, and esteeming technique. In budgetary control

estimating technique helps in getting the business income figure (Sales per unit ×

Units created).

P5. Adaption of management accounting systems to respond to

financial problems and sustainable success:

Financial problems are common in running business; these problems arises due to

lack of past report study, using outdated accounting regulations, not enough fund left

with company and improper settlement of cost of different heads (Malina, 2017).

Sustainable success is a term associated with maintaining better performance for

prolong period of time. Some of the management accounting tools is discussed

below:

1. Demand forecasting: It is the process of forecasting similarly as the

investigation of anticipating the conceivable enthusiasm for a thing or

organization later on. This figure relies upon past gauges of direct and the

procedure with designs in the present. From now on, it isn't simply guessing the

future intrigue yet is evaluating the intrigue tentatively and evenhandedly.

Through gauging request organization get data about most recent patterns of the

market and manufactured item appropriately to coordinate the interest (Jones and

et.al., 2018).

Solution to financial problem:

Through anticipating request organization can take care of money related issues

like lack of assets, underperformance, under valuation of advantages and

reduction in income through giving data ahead of time.

Comparison:

These arranging apparatuses are for the most part utilized assembling

associations to keep away from the circumstance of overproduction. Associations

which are in wholesaling don't have a lot of utilization of this.

2. Make or buy decisions: Make or buy decisions choices usually rise when a firm

that has built up a thing or part or essentially balanced a thing or part is

experiencing issue with current providers, or has lessening limit or propelling

sales. It's anything but a simple errand to take such choices regularly,

organization requires bunches of examinations like getting ready zero based

planning, seeing future relations with providers and assessing whether

organization has enough ability to deliver explicit item or not. Extra to this, it is

additionally required to discover whether the item which organization needs

make or purchase impact center business of the business in the event that Yes, at

that point it ought to go for making that stock else it should purchase or procure

specific business (Garvey, Book and Covert, 2016).

Solution to financial problem:

Monetary issues like over consumption, delay in preparing time, and so on. Can

be tackled through evaluating cost on whether to make or purchase item,

organization satisfied interest on schedule and furthermore increment its Net

income through limiting by and large expenses.

Comparison:

It is generally reasonable for assembling associations as they have to conclude

whether to create or purchase the item. Administration associations not utilize

this device since they just offer types of assistance like exchanging, client

support, friendliness, and so forth.

3. Activity based costing: Activity based costing (ABC) is a costing framework

that administers over headed and insidious expenses to related things and

Through anticipating request organization can take care of money related issues

like lack of assets, underperformance, under valuation of advantages and

reduction in income through giving data ahead of time.

Comparison:

These arranging apparatuses are for the most part utilized assembling

associations to keep away from the circumstance of overproduction. Associations

which are in wholesaling don't have a lot of utilization of this.

2. Make or buy decisions: Make or buy decisions choices usually rise when a firm

that has built up a thing or part or essentially balanced a thing or part is

experiencing issue with current providers, or has lessening limit or propelling

sales. It's anything but a simple errand to take such choices regularly,

organization requires bunches of examinations like getting ready zero based

planning, seeing future relations with providers and assessing whether

organization has enough ability to deliver explicit item or not. Extra to this, it is

additionally required to discover whether the item which organization needs

make or purchase impact center business of the business in the event that Yes, at

that point it ought to go for making that stock else it should purchase or procure

specific business (Garvey, Book and Covert, 2016).

Solution to financial problem:

Monetary issues like over consumption, delay in preparing time, and so on. Can

be tackled through evaluating cost on whether to make or purchase item,

organization satisfied interest on schedule and furthermore increment its Net

income through limiting by and large expenses.

Comparison:

It is generally reasonable for assembling associations as they have to conclude

whether to create or purchase the item. Administration associations not utilize

this device since they just offer types of assistance like exchanging, client

support, friendliness, and so forth.

3. Activity based costing: Activity based costing (ABC) is a costing framework

that administers over headed and insidious expenses to related things and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.