Accounting Journal Entries and Statements

VerifiedAdded on 2019/10/12

|26

|4134

|750

Report

AI Summary

Sovereign Ltd.'s financial information for the years ended 30 June 2015, 2016, and 2017 includes goodwill impairment at 30 June each year. The company's share capital increased from $63,000 on June 30, 2015 to $73,000 on June 30, 2017. There were no journal entries required for 30 June 2016. The financial statements also include the acquisition of Yellow Ltd by Red Ltd in July 2015, which eliminated the investment in Yellow Ltd. The worksheet extract shows the consolidated financial statements for Red Ltd and its subsidiary, Yellow Ltd. Additionally, Roberto Limited's financial information includes the sale of goods, interest income, consultancy fees received, cost of sales, finance costs, distribution expenses, marketing expenses, warehouse services expenses, administration expenses, other expenses, and income tax expense. The company also has an asset revaluation reserve with a balance of $40,000 as at July 1, 2016, which increased by $150,000 on June 30, 2017 due to the restatement of land carrying value. The statements required are the Statement of Comprehensive Income, Statement of Changes in Equity, and Notes to the Financial Statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FNS5017 Diploma of Accounting

Module 1.2 Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file “Submit Diploma of Accounting Module 1.2

Assignment” in the Module 1 section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 1 of 26

Module 1.2 Assignment

Instructions:

This assignment contains multiple Assessment Activities

Please complete the Declaration of Authenticity at the bottom of this page

Save this assignment (e.g. on your desktop)

To complete the assignment, read the instructions for each question carefully.

You may be required to refer to your learning materials or other sources to complete

this assessment.

You are required to type all your responses in the spaces provided

Once you have completed all parts of the assignment and saved it, login to the

Monarch Institute LMS to submit your assignment for grading

To submit your assignment click on the file “Submit Diploma of Accounting Module 1.2

Assignment” in the Module 1 section of your course and upload your assignment file.

Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification of your submission – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 1 of 26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Units Covered: FNSACC514

Important assessment information

Aims of this assessment

This assessment focuses on the preparation of financial reports for corporate entities.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC514 Prepare financial reports for corporate entities

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with specified

educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with limited

serious errors in fact or application. If incorrect information is contained in an answer, it must be

fundamentally outweighed by the accurate information provided. This will be assessed against a

marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to assessors.

These answers either do not address the question specifically, or are wrong from a legislative

perspective, or are incorrectly applied. Answers that omit to provide a response to any significant issue

(where multiple issues must be addressed in a question) may also be deemed not-yet-competent.

Answers that have faulty reasoning, a poor standard of expression or include plagiarism may also be

deemed not-yet-competent. Please note, additional information regarding Monarch’s plagiarism policy

is contained in the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 2 of 26

Important assessment information

Aims of this assessment

This assessment focuses on the preparation of financial reports for corporate entities.

Marking and feedback

This assignment contains multiple Assessment Activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following unit(s) of

competency:

FNSACC514 Prepare financial reports for corporate entities

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with specified

educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with limited

serious errors in fact or application. If incorrect information is contained in an answer, it must be

fundamentally outweighed by the accurate information provided. This will be assessed against a

marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to assessors.

These answers either do not address the question specifically, or are wrong from a legislative

perspective, or are incorrectly applied. Answers that omit to provide a response to any significant issue

(where multiple issues must be addressed in a question) may also be deemed not-yet-competent.

Answers that have faulty reasoning, a poor standard of expression or include plagiarism may also be

deemed not-yet-competent. Please note, additional information regarding Monarch’s plagiarism policy

is contained in the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 2 of 26

Units Covered: FNSACC514

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be given

one more opportunity to re-submit the assessment after consultation with your Trainer/ Assessor. You

will know your assessment is deemed ‘not-yet-competent’ if your grade book in the Monarch LMS says

“NYC” after you have received an email from your assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter areas

raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete certain

tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to assist

you

The following questions are based on the material in the text “Prepare Financial Reports for Corporate

Entities” (3rd or 4th Edition) by Gavin Dumbrell & Damien Kelly.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 3 of 26

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC514 Financial Reports for Corporate Entities

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be given

one more opportunity to re-submit the assessment after consultation with your Trainer/ Assessor. You

will know your assessment is deemed ‘not-yet-competent’ if your grade book in the Monarch LMS says

“NYC” after you have received an email from your assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter areas

raised in the question in full as part of the response.

Performance based questions:

A performance based question requires you to clearly demonstrate your ability to complete certain

tasks, that is, to perform these tasks.

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to assist

you

The following questions are based on the material in the text “Prepare Financial Reports for Corporate

Entities” (3rd or 4th Edition) by Gavin Dumbrell & Damien Kelly.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 3 of 26

Assessment Activities

Short Answer and Worked Answer Questions

FNSACC514 Financial Reports for Corporate Entities

Units Covered: FNSACC514

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 4 of 26

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 4 of 26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Units Covered: FNSACC514

The following questions are based on the material in Chapter 1:

1. List three (3) differences between a small and a large proprietary company?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 5 of 26

1.

2.

3.

The following questions are based on the material in Chapter 1:

1. List three (3) differences between a small and a large proprietary company?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 5 of 26

1.

2.

3.

Units Covered: FNSACC514

The following questions are based on the material in Chapter 2:

2. Rufflander Ltd offered for subscription 300,000 $1 ordinary shares payable in full on application.

All 300,000 shares were applied for and allotted.

Required: Prepare general journal entries to record the share issue. (Ignore dates).

Rufflander Ltd. – General Journal Entries

Date Accounts Debit Credit

Receipt of application money

Issue of 300,000 $1 fully paid ordinary

shares

Transfer of application funds to

bank

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 6 of 26

The following questions are based on the material in Chapter 2:

2. Rufflander Ltd offered for subscription 300,000 $1 ordinary shares payable in full on application.

All 300,000 shares were applied for and allotted.

Required: Prepare general journal entries to record the share issue. (Ignore dates).

Rufflander Ltd. – General Journal Entries

Date Accounts Debit Credit

Receipt of application money

Issue of 300,000 $1 fully paid ordinary

shares

Transfer of application funds to

bank

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 6 of 26

Units Covered: FNSACC514

The following questions are based on the material in Chapter 3:

3. Prepare general journal entries to record the issue of 1,000 $100 8% debentures at par, payable in

full on application. (Ignore dates).

Date Account Debit Credit

Receipt of application money for debentures

Issue of Debentures

Transfer of application funds to bank on

issue of debentures

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 7 of 26

The following questions are based on the material in Chapter 3:

3. Prepare general journal entries to record the issue of 1,000 $100 8% debentures at par, payable in

full on application. (Ignore dates).

Date Account Debit Credit

Receipt of application money for debentures

Issue of Debentures

Transfer of application funds to bank on

issue of debentures

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 7 of 26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC514

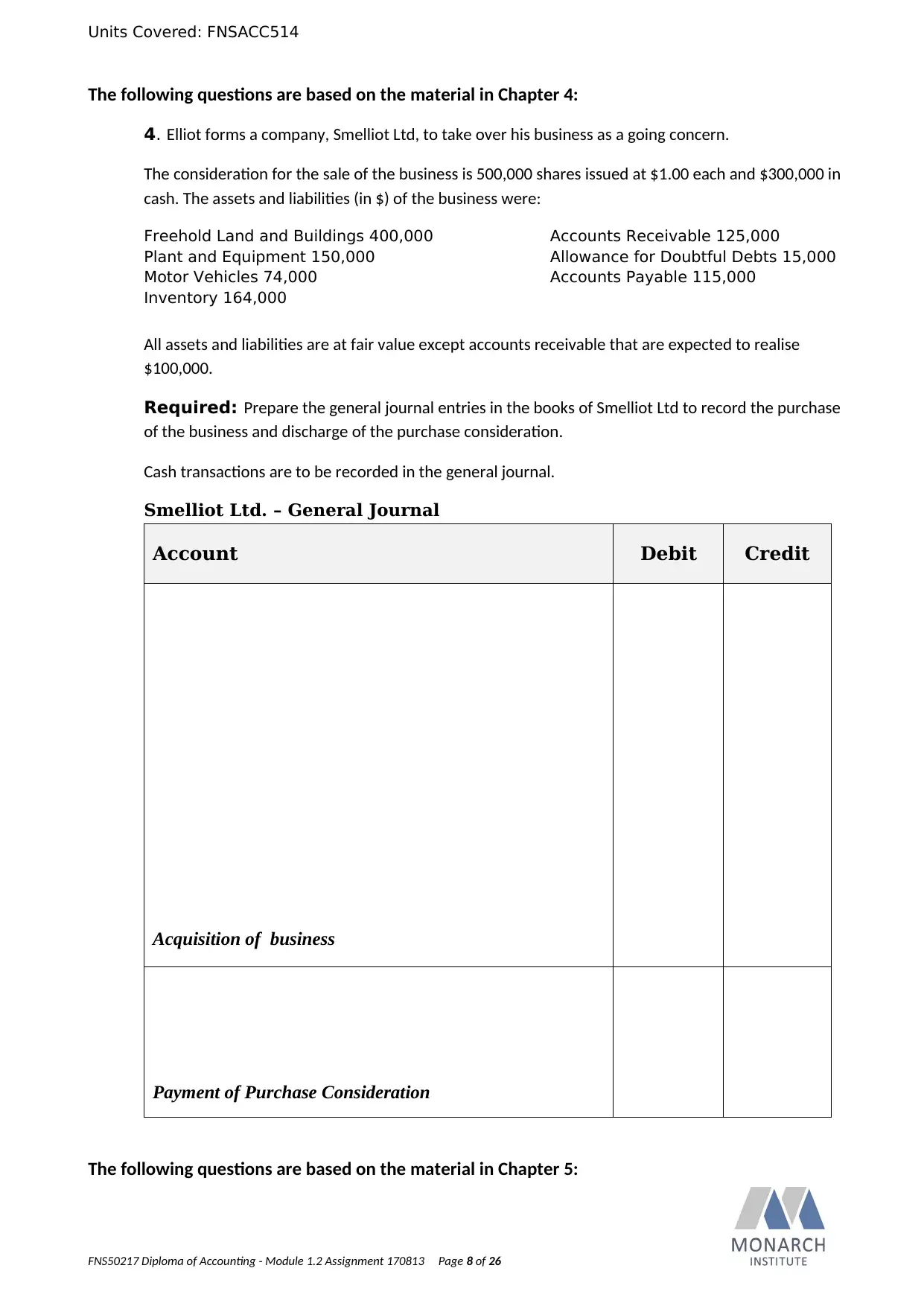

The following questions are based on the material in Chapter 4:

4. Elliot forms a company, Smelliot Ltd, to take over his business as a going concern.

The consideration for the sale of the business is 500,000 shares issued at $1.00 each and $300,000 in

cash. The assets and liabilities (in $) of the business were:

Freehold Land and Buildings 400,000

Plant and Equipment 150,000

Motor Vehicles 74,000

Inventory 164,000

Accounts Receivable 125,000

Allowance for Doubtful Debts 15,000

Accounts Payable 115,000

All assets and liabilities are at fair value except accounts receivable that are expected to realise

$100,000.

Required: Prepare the general journal entries in the books of Smelliot Ltd to record the purchase

of the business and discharge of the purchase consideration.

Cash transactions are to be recorded in the general journal.

Smelliot Ltd. – General Journal

Account Debit Credit

Acquisition of business

Payment of Purchase Consideration

The following questions are based on the material in Chapter 5:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 8 of 26

The following questions are based on the material in Chapter 4:

4. Elliot forms a company, Smelliot Ltd, to take over his business as a going concern.

The consideration for the sale of the business is 500,000 shares issued at $1.00 each and $300,000 in

cash. The assets and liabilities (in $) of the business were:

Freehold Land and Buildings 400,000

Plant and Equipment 150,000

Motor Vehicles 74,000

Inventory 164,000

Accounts Receivable 125,000

Allowance for Doubtful Debts 15,000

Accounts Payable 115,000

All assets and liabilities are at fair value except accounts receivable that are expected to realise

$100,000.

Required: Prepare the general journal entries in the books of Smelliot Ltd to record the purchase

of the business and discharge of the purchase consideration.

Cash transactions are to be recorded in the general journal.

Smelliot Ltd. – General Journal

Account Debit Credit

Acquisition of business

Payment of Purchase Consideration

The following questions are based on the material in Chapter 5:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 8 of 26

Units Covered: FNSACC514

5 a. Why would a company establish a reserve?

5 b. List three (3) types of reserves which may be established?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 9 of 26

1.

2.

3.

5 a. Why would a company establish a reserve?

5 b. List three (3) types of reserves which may be established?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 9 of 26

1.

2.

3.

Units Covered: FNSACC514

6. Cool Hats Ltd has paid the following PAYG tax instalments for the year ended 30 June:

September Quarter 11,000

December Quarter 11,000

March Quarter 11,000

June Quarter 11,000

Total 44,000

Taxable income for the year ended 30 June, was $168,000. Company tax rate is 30%.

Required:

Prepare general journal entries to record the company’s income tax instalments and final payment.

Cool Hats Ltd. – General Journals

Date Account Debit Credit

1st Qtr

PAYG Tax Instalment due for quarter

1st Qtr

Payment of PAYG tax instalment for

2nd Qtr

PAYG Tax Instalment due for quarter

2nd Qtr

Payment of PAYG tax instalment for

3rd Qtr

PAYG Tax Instalment due for quarter

3rd Qtr

Payment of PAYG tax instalment for

4th Qtr

PAYG Tax Instalment due for quarter

4th Qtr

Payment of PAYG tax instalment for

4th Qtr

Additional tax payable for year

4th Qtr

Balance transferred

The following questions are based on the material in Chapter 6:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 10 of 26

6. Cool Hats Ltd has paid the following PAYG tax instalments for the year ended 30 June:

September Quarter 11,000

December Quarter 11,000

March Quarter 11,000

June Quarter 11,000

Total 44,000

Taxable income for the year ended 30 June, was $168,000. Company tax rate is 30%.

Required:

Prepare general journal entries to record the company’s income tax instalments and final payment.

Cool Hats Ltd. – General Journals

Date Account Debit Credit

1st Qtr

PAYG Tax Instalment due for quarter

1st Qtr

Payment of PAYG tax instalment for

2nd Qtr

PAYG Tax Instalment due for quarter

2nd Qtr

Payment of PAYG tax instalment for

3rd Qtr

PAYG Tax Instalment due for quarter

3rd Qtr

Payment of PAYG tax instalment for

4th Qtr

PAYG Tax Instalment due for quarter

4th Qtr

Payment of PAYG tax instalment for

4th Qtr

Additional tax payable for year

4th Qtr

Balance transferred

The following questions are based on the material in Chapter 6:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 10 of 26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Units Covered: FNSACC514

7. (a) Describe the difference between the tax payable method and tax effect method of accounting for

income tax.

(b) Provide two (2) examples of items treated differently under the two methods, that is, treated differently

under the accounting treatment and the tax effect method.

Item Accounting

treatment Tax treatment

1.

2.

(c) Which method must be used by reporting entities?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 11 of 26

7. (a) Describe the difference between the tax payable method and tax effect method of accounting for

income tax.

(b) Provide two (2) examples of items treated differently under the two methods, that is, treated differently

under the accounting treatment and the tax effect method.

Item Accounting

treatment Tax treatment

1.

2.

(c) Which method must be used by reporting entities?

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 11 of 26

Units Covered: FNSACC514

8. Prepare the tax effect Journal Entries for the following independent situations and explain why each gives

rise to a Deferred Tax Asset or a Deferred Tax Liability at June 2016.

Tax Rate is 30%.

Enter your answers in the grids provided.

(a)The current period Doubtful Debts expense for a company was $9,000. The balance in the Allowance for

Doubtful Debts account at the beginning of the period was $7,000. During the current period $6,000 of

Bad Debts had been written off against the Allowance for Doubtful Debts.

Account Debit Credit

$

$

Explanation:

(b)A publishing company has received $20,000 of subscriptions in advance of publications. This revenue will

be recognised in the accounting records over the next four years. This amount is treated as assessable

income for income tax purposes.

Account Debit Credit

$

$

Explanation:

(c) Plant and Machinery was acquired for $200,000 on 1 July 2015. Accounting depreciation is 25% p.a. and

tax depreciation is 30% p.a.

Account Debit Credit

$

$

Explanation:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 12 of 26

8. Prepare the tax effect Journal Entries for the following independent situations and explain why each gives

rise to a Deferred Tax Asset or a Deferred Tax Liability at June 2016.

Tax Rate is 30%.

Enter your answers in the grids provided.

(a)The current period Doubtful Debts expense for a company was $9,000. The balance in the Allowance for

Doubtful Debts account at the beginning of the period was $7,000. During the current period $6,000 of

Bad Debts had been written off against the Allowance for Doubtful Debts.

Account Debit Credit

$

$

Explanation:

(b)A publishing company has received $20,000 of subscriptions in advance of publications. This revenue will

be recognised in the accounting records over the next four years. This amount is treated as assessable

income for income tax purposes.

Account Debit Credit

$

$

Explanation:

(c) Plant and Machinery was acquired for $200,000 on 1 July 2015. Accounting depreciation is 25% p.a. and

tax depreciation is 30% p.a.

Account Debit Credit

$

$

Explanation:

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 12 of 26

Units Covered: FNSACC514

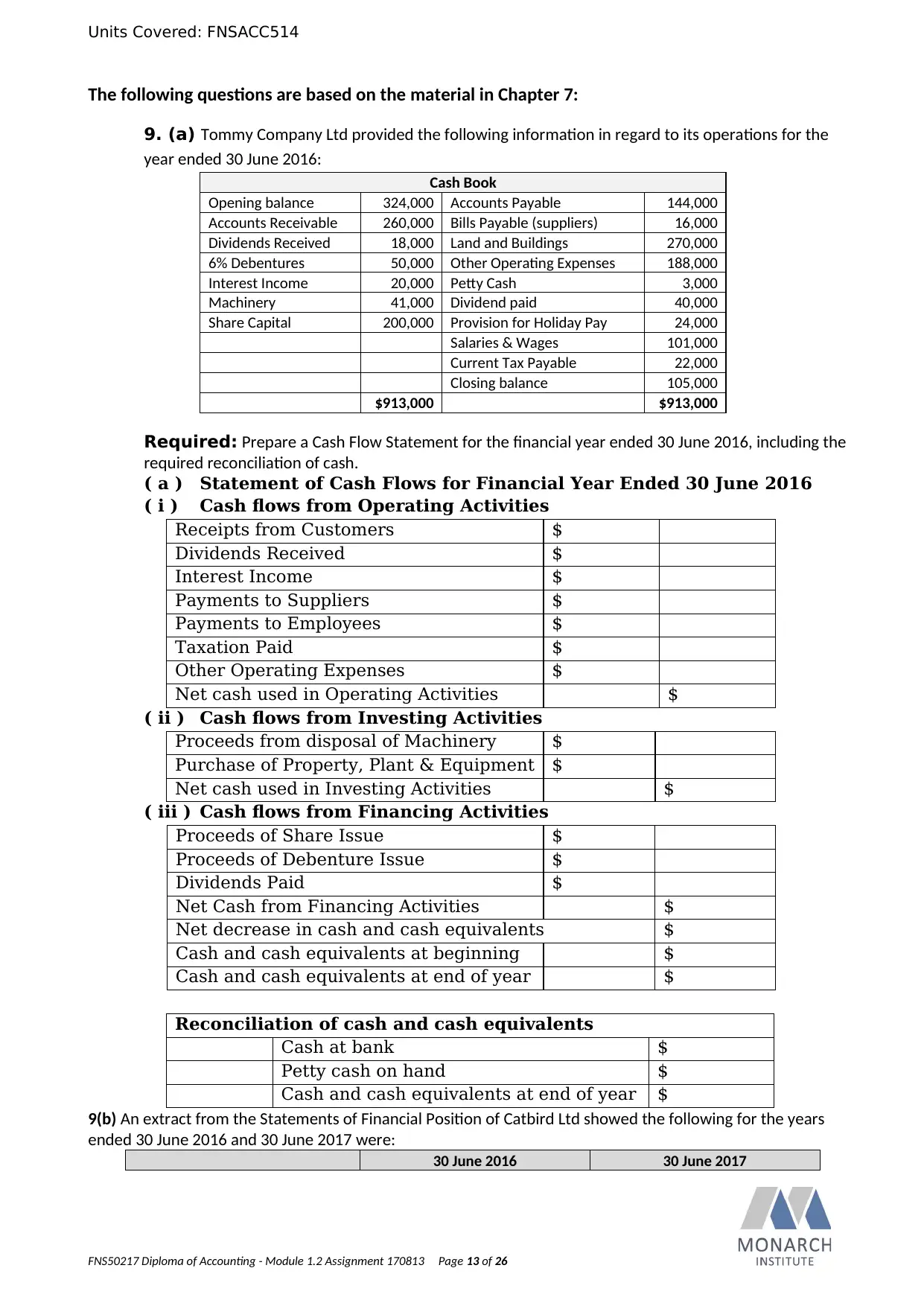

The following questions are based on the material in Chapter 7:

9. (a) Tommy Company Ltd provided the following information in regard to its operations for the

year ended 30 June 2016:

Cash Book

Opening balance 324,000 Accounts Payable 144,000

Accounts Receivable 260,000 Bills Payable (suppliers) 16,000

Dividends Received 18,000 Land and Buildings 270,000

6% Debentures 50,000 Other Operating Expenses 188,000

Interest Income 20,000 Petty Cash 3,000

Machinery 41,000 Dividend paid 40,000

Share Capital 200,000 Provision for Holiday Pay 24,000

Salaries & Wages 101,000

Current Tax Payable 22,000

Closing balance 105,000

$913,000 $913,000

Required: Prepare a Cash Flow Statement for the financial year ended 30 June 2016, including the

required reconciliation of cash.

( a ) Statement of Cash Flows for Financial Year Ended 30 June 2016

( i ) Cash flows from Operating Activities

Receipts from Customers $

Dividends Received $

Interest Income $

Payments to Suppliers $

Payments to Employees $

Taxation Paid $

Other Operating Expenses $

Net cash used in Operating Activities $

( ii ) Cash flows from Investing Activities

Proceeds from disposal of Machinery $

Purchase of Property, Plant & Equipment $

Net cash used in Investing Activities $

( iii ) Cash flows from Financing Activities

Proceeds of Share Issue $

Proceeds of Debenture Issue $

Dividends Paid $

Net Cash from Financing Activities $

Net decrease in cash and cash equivalents $

Cash and cash equivalents at beginning $

Cash and cash equivalents at end of year $

Reconciliation of cash and cash equivalents

Cash at bank $

Petty cash on hand $

Cash and cash equivalents at end of year $

9(b) An extract from the Statements of Financial Position of Catbird Ltd showed the following for the years

ended 30 June 2016 and 30 June 2017 were:

30 June 2016 30 June 2017

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 13 of 26

The following questions are based on the material in Chapter 7:

9. (a) Tommy Company Ltd provided the following information in regard to its operations for the

year ended 30 June 2016:

Cash Book

Opening balance 324,000 Accounts Payable 144,000

Accounts Receivable 260,000 Bills Payable (suppliers) 16,000

Dividends Received 18,000 Land and Buildings 270,000

6% Debentures 50,000 Other Operating Expenses 188,000

Interest Income 20,000 Petty Cash 3,000

Machinery 41,000 Dividend paid 40,000

Share Capital 200,000 Provision for Holiday Pay 24,000

Salaries & Wages 101,000

Current Tax Payable 22,000

Closing balance 105,000

$913,000 $913,000

Required: Prepare a Cash Flow Statement for the financial year ended 30 June 2016, including the

required reconciliation of cash.

( a ) Statement of Cash Flows for Financial Year Ended 30 June 2016

( i ) Cash flows from Operating Activities

Receipts from Customers $

Dividends Received $

Interest Income $

Payments to Suppliers $

Payments to Employees $

Taxation Paid $

Other Operating Expenses $

Net cash used in Operating Activities $

( ii ) Cash flows from Investing Activities

Proceeds from disposal of Machinery $

Purchase of Property, Plant & Equipment $

Net cash used in Investing Activities $

( iii ) Cash flows from Financing Activities

Proceeds of Share Issue $

Proceeds of Debenture Issue $

Dividends Paid $

Net Cash from Financing Activities $

Net decrease in cash and cash equivalents $

Cash and cash equivalents at beginning $

Cash and cash equivalents at end of year $

Reconciliation of cash and cash equivalents

Cash at bank $

Petty cash on hand $

Cash and cash equivalents at end of year $

9(b) An extract from the Statements of Financial Position of Catbird Ltd showed the following for the years

ended 30 June 2016 and 30 June 2017 were:

30 June 2016 30 June 2017

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 13 of 26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC514

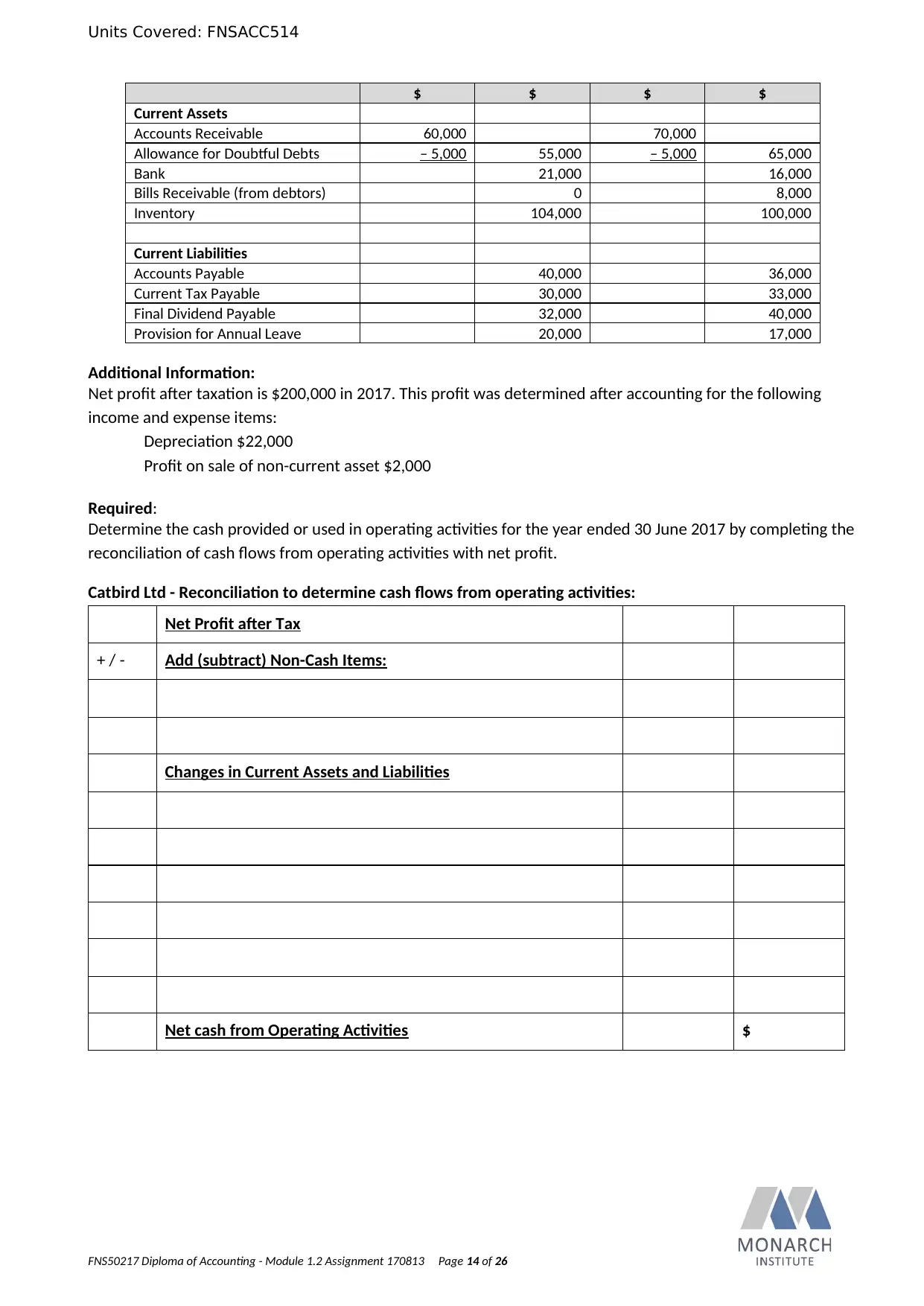

$ $ $ $

Current Assets

Accounts Receivable 60,000 70,000

Allowance for Doubtful Debts – 5,000 55,000 – 5,000 65,000

Bank 21,000 16,000

Bills Receivable (from debtors) 0 8,000

Inventory 104,000 100,000

Current Liabilities

Accounts Payable 40,000 36,000

Current Tax Payable 30,000 33,000

Final Dividend Payable 32,000 40,000

Provision for Annual Leave 20,000 17,000

Additional Information:

Net profit after taxation is $200,000 in 2017. This profit was determined after accounting for the following

income and expense items:

Depreciation $22,000

Profit on sale of non-current asset $2,000

Required:

Determine the cash provided or used in operating activities for the year ended 30 June 2017 by completing the

reconciliation of cash flows from operating activities with net profit.

Catbird Ltd - Reconciliation to determine cash flows from operating activities:

Net Profit after Tax

+ / - Add (subtract) Non-Cash Items:

Changes in Current Assets and Liabilities

Net cash from Operating Activities $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 14 of 26

$ $ $ $

Current Assets

Accounts Receivable 60,000 70,000

Allowance for Doubtful Debts – 5,000 55,000 – 5,000 65,000

Bank 21,000 16,000

Bills Receivable (from debtors) 0 8,000

Inventory 104,000 100,000

Current Liabilities

Accounts Payable 40,000 36,000

Current Tax Payable 30,000 33,000

Final Dividend Payable 32,000 40,000

Provision for Annual Leave 20,000 17,000

Additional Information:

Net profit after taxation is $200,000 in 2017. This profit was determined after accounting for the following

income and expense items:

Depreciation $22,000

Profit on sale of non-current asset $2,000

Required:

Determine the cash provided or used in operating activities for the year ended 30 June 2017 by completing the

reconciliation of cash flows from operating activities with net profit.

Catbird Ltd - Reconciliation to determine cash flows from operating activities:

Net Profit after Tax

+ / - Add (subtract) Non-Cash Items:

Changes in Current Assets and Liabilities

Net cash from Operating Activities $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 14 of 26

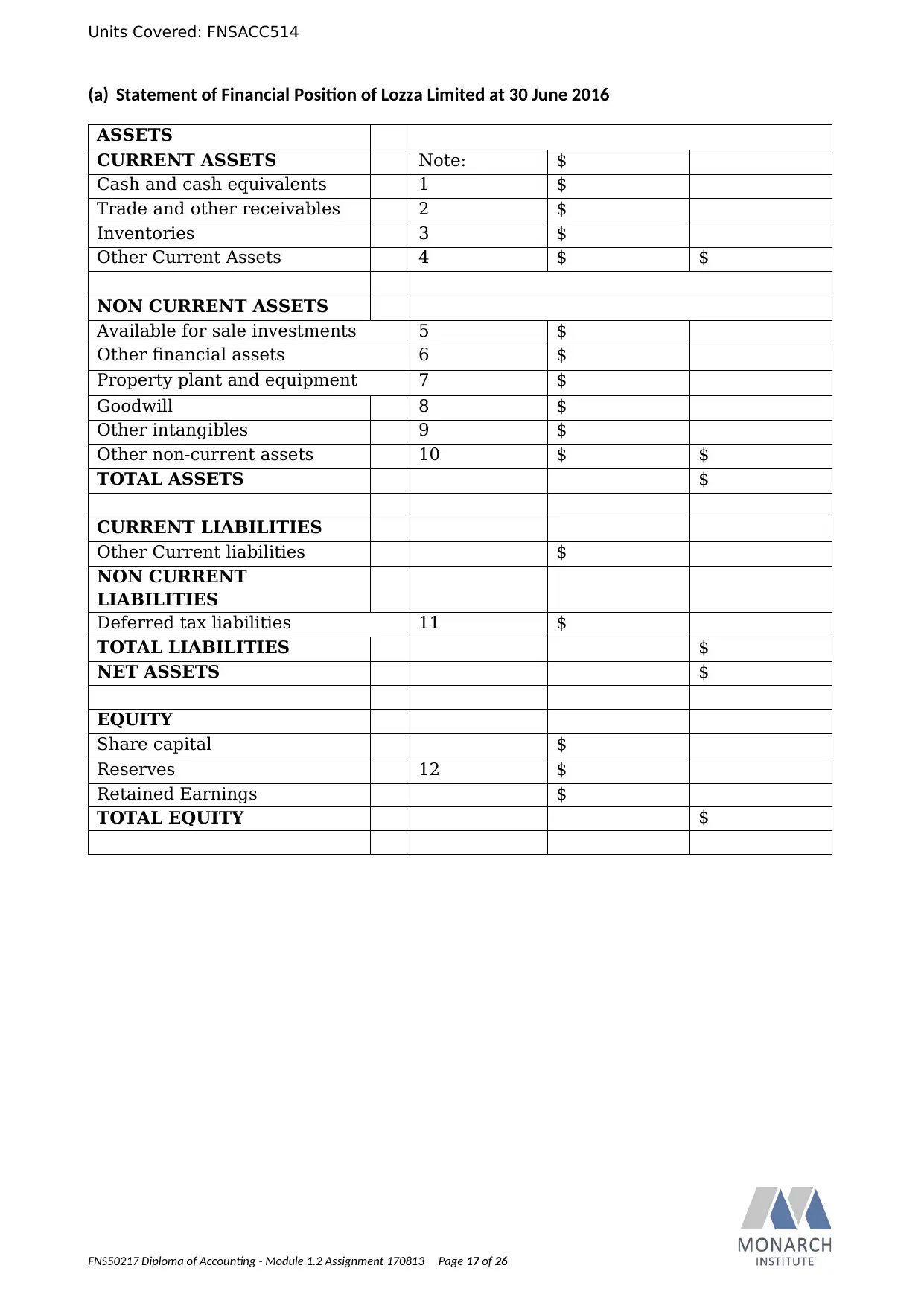

Units Covered: FNSACC514

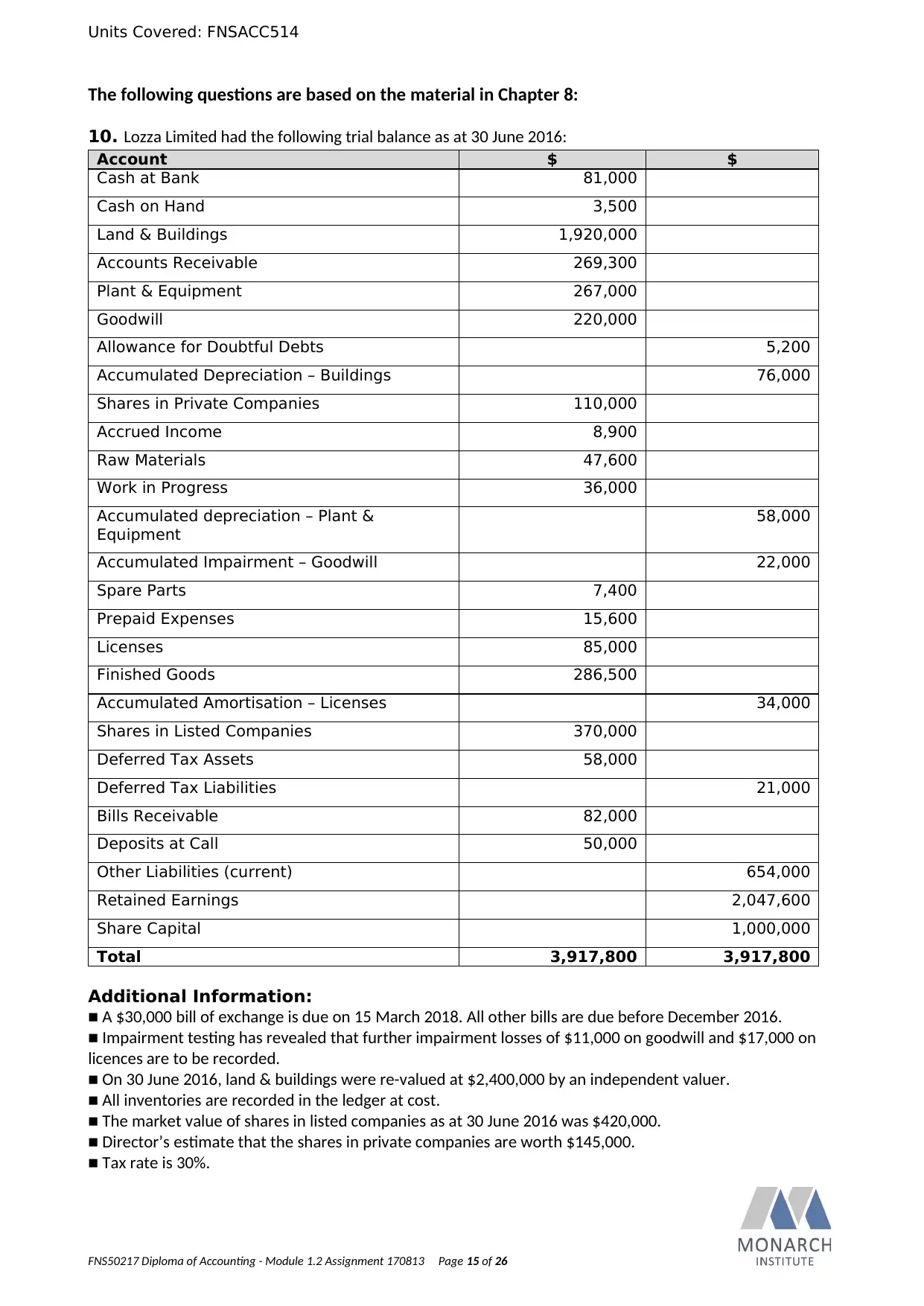

The following questions are based on the material in Chapter 8:

10. Lozza Limited had the following trial balance as at 30 June 2016:

Account $ $

Cash at Bank 81,000

Cash on Hand 3,500

Land & Buildings 1,920,000

Accounts Receivable 269,300

Plant & Equipment 267,000

Goodwill 220,000

Allowance for Doubtful Debts 5,200

Accumulated Depreciation – Buildings 76,000

Shares in Private Companies 110,000

Accrued Income 8,900

Raw Materials 47,600

Work in Progress 36,000

Accumulated depreciation – Plant &

Equipment

58,000

Accumulated Impairment – Goodwill 22,000

Spare Parts 7,400

Prepaid Expenses 15,600

Licenses 85,000

Finished Goods 286,500

Accumulated Amortisation – Licenses 34,000

Shares in Listed Companies 370,000

Deferred Tax Assets 58,000

Deferred Tax Liabilities 21,000

Bills Receivable 82,000

Deposits at Call 50,000

Other Liabilities (current) 654,000

Retained Earnings 2,047,600

Share Capital 1,000,000

Total 3,917,800 3,917,800

Additional Information:

■ A $30,000 bill of exchange is due on 15 March 2018. All other bills are due before December 2016.

■ Impairment testing has revealed that further impairment losses of $11,000 on goodwill and $17,000 on

licences are to be recorded.

■ On 30 June 2016, land & buildings were re-valued at $2,400,000 by an independent valuer.

■ All inventories are recorded in the ledger at cost.

■ The market value of shares in listed companies as at 30 June 2016 was $420,000.

■ Director’s estimate that the shares in private companies are worth $145,000.

■ Tax rate is 30%.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 15 of 26

The following questions are based on the material in Chapter 8:

10. Lozza Limited had the following trial balance as at 30 June 2016:

Account $ $

Cash at Bank 81,000

Cash on Hand 3,500

Land & Buildings 1,920,000

Accounts Receivable 269,300

Plant & Equipment 267,000

Goodwill 220,000

Allowance for Doubtful Debts 5,200

Accumulated Depreciation – Buildings 76,000

Shares in Private Companies 110,000

Accrued Income 8,900

Raw Materials 47,600

Work in Progress 36,000

Accumulated depreciation – Plant &

Equipment

58,000

Accumulated Impairment – Goodwill 22,000

Spare Parts 7,400

Prepaid Expenses 15,600

Licenses 85,000

Finished Goods 286,500

Accumulated Amortisation – Licenses 34,000

Shares in Listed Companies 370,000

Deferred Tax Assets 58,000

Deferred Tax Liabilities 21,000

Bills Receivable 82,000

Deposits at Call 50,000

Other Liabilities (current) 654,000

Retained Earnings 2,047,600

Share Capital 1,000,000

Total 3,917,800 3,917,800

Additional Information:

■ A $30,000 bill of exchange is due on 15 March 2018. All other bills are due before December 2016.

■ Impairment testing has revealed that further impairment losses of $11,000 on goodwill and $17,000 on

licences are to be recorded.

■ On 30 June 2016, land & buildings were re-valued at $2,400,000 by an independent valuer.

■ All inventories are recorded in the ledger at cost.

■ The market value of shares in listed companies as at 30 June 2016 was $420,000.

■ Director’s estimate that the shares in private companies are worth $145,000.

■ Tax rate is 30%.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 15 of 26

Units Covered: FNSACC514

Required:

(a) Complete a Statement of Financial Position as at 30 June 2016.

(b) Complete notes accompanying the Statement of Financial Position for assets.

Tips:

We suggest you follow these steps in completing your answer:

1. Transfer all of the items from the Trial Balance items to the respective "(b) Notes to Statement of Financial

Position".

Now transfer the total from each "Note" at (b) to the "(a) Statement of Financial Position".

Total the "(a) Statement of Financial Position" and ensure that it balances.

2. Next, one at a time, process each "Additional Information" adjustment and record each adjustment in the

relevant "Note" at (b).

Now, transfer the revised total of any adjusted "Notes" to the "Statement of Financial Position". You may need

to revise some values in the "Statement of Financial Position" that you previously reported (in Step 1).

After processing each adjustment, again total the "Statement of Financial Position" and ensure that it

balances.

3. Any income or expense adjustments should be posted to Retained Earnings.

4. Any revaluation adjustment should be applied to the asset value after allowing for accumulated

depreciation. This also means that any accumulated depreciation is reset to nil upon revaluation of the asset.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 16 of 26

Required:

(a) Complete a Statement of Financial Position as at 30 June 2016.

(b) Complete notes accompanying the Statement of Financial Position for assets.

Tips:

We suggest you follow these steps in completing your answer:

1. Transfer all of the items from the Trial Balance items to the respective "(b) Notes to Statement of Financial

Position".

Now transfer the total from each "Note" at (b) to the "(a) Statement of Financial Position".

Total the "(a) Statement of Financial Position" and ensure that it balances.

2. Next, one at a time, process each "Additional Information" adjustment and record each adjustment in the

relevant "Note" at (b).

Now, transfer the revised total of any adjusted "Notes" to the "Statement of Financial Position". You may need

to revise some values in the "Statement of Financial Position" that you previously reported (in Step 1).

After processing each adjustment, again total the "Statement of Financial Position" and ensure that it

balances.

3. Any income or expense adjustments should be posted to Retained Earnings.

4. Any revaluation adjustment should be applied to the asset value after allowing for accumulated

depreciation. This also means that any accumulated depreciation is reset to nil upon revaluation of the asset.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 16 of 26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Units Covered: FNSACC514

(a) Statement of Financial Position of Lozza Limited at 30 June 2016

ASSETS

CURRENT ASSETS Note: $

Cash and cash equivalents 1 $

Trade and other receivables 2 $

Inventories 3 $

Other Current Assets 4 $ $

NON CURRENT ASSETS

Available for sale investments 5 $

Other financial assets 6 $

Property plant and equipment 7 $

Goodwill 8 $

Other intangibles 9 $

Other non-current assets 10 $ $

TOTAL ASSETS $

CURRENT LIABILITIES

Other Current liabilities $

NON CURRENT

LIABILITIES

Deferred tax liabilities 11 $

TOTAL LIABILITIES $

NET ASSETS $

EQUITY

Share capital $

Reserves 12 $

Retained Earnings $

TOTAL EQUITY $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 17 of 26

(a) Statement of Financial Position of Lozza Limited at 30 June 2016

ASSETS

CURRENT ASSETS Note: $

Cash and cash equivalents 1 $

Trade and other receivables 2 $

Inventories 3 $

Other Current Assets 4 $ $

NON CURRENT ASSETS

Available for sale investments 5 $

Other financial assets 6 $

Property plant and equipment 7 $

Goodwill 8 $

Other intangibles 9 $

Other non-current assets 10 $ $

TOTAL ASSETS $

CURRENT LIABILITIES

Other Current liabilities $

NON CURRENT

LIABILITIES

Deferred tax liabilities 11 $

TOTAL LIABILITIES $

NET ASSETS $

EQUITY

Share capital $

Reserves 12 $

Retained Earnings $

TOTAL EQUITY $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 17 of 26

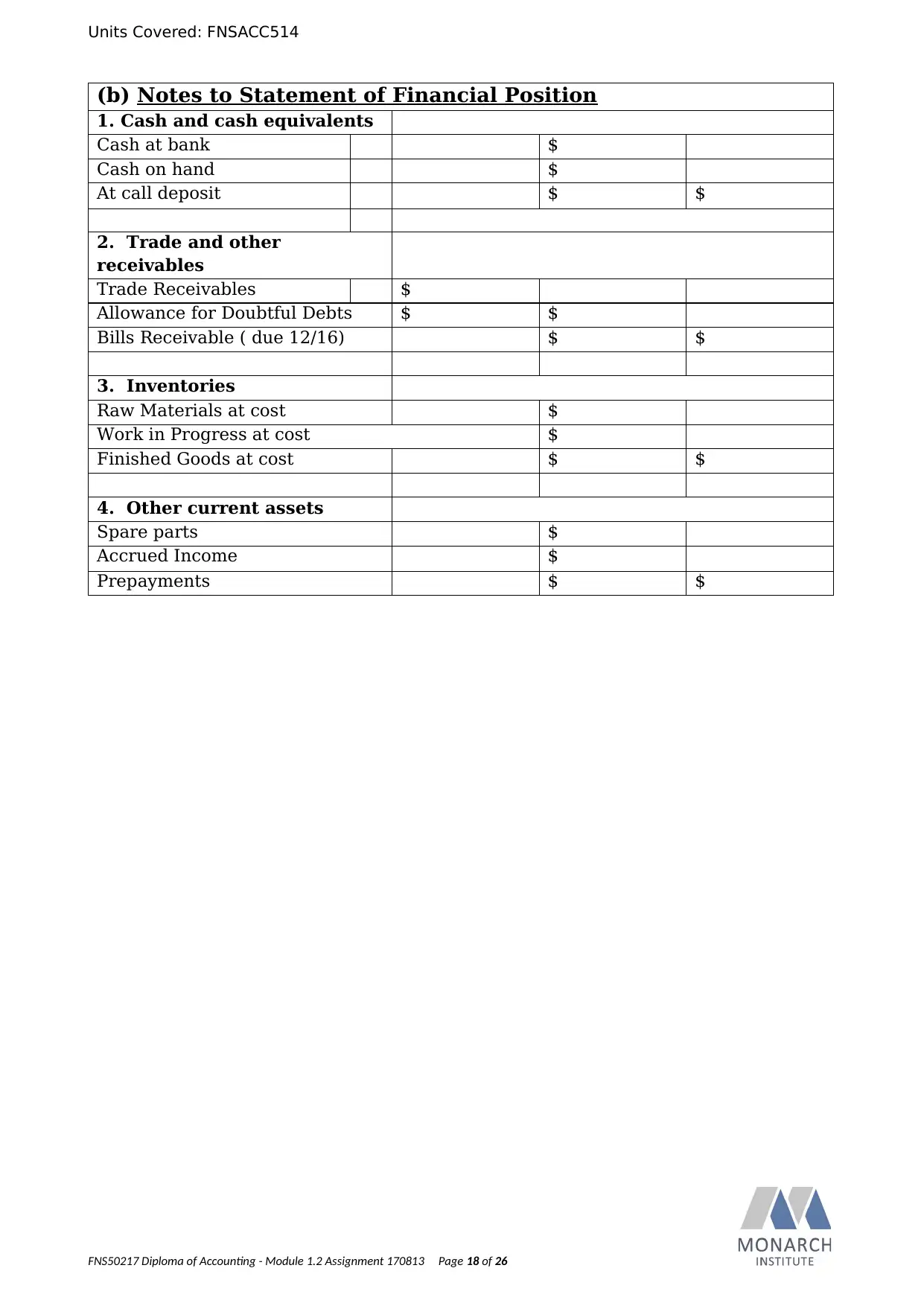

Units Covered: FNSACC514

(b) Notes to Statement of Financial Position

1. Cash and cash equivalents

Cash at bank $

Cash on hand $

At call deposit $ $

2. Trade and other

receivables

Trade Receivables $

Allowance for Doubtful Debts $ $

Bills Receivable ( due 12/16) $ $

3. Inventories

Raw Materials at cost $

Work in Progress at cost $

Finished Goods at cost $ $

4. Other current assets

Spare parts $

Accrued Income $

Prepayments $ $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 18 of 26

(b) Notes to Statement of Financial Position

1. Cash and cash equivalents

Cash at bank $

Cash on hand $

At call deposit $ $

2. Trade and other

receivables

Trade Receivables $

Allowance for Doubtful Debts $ $

Bills Receivable ( due 12/16) $ $

3. Inventories

Raw Materials at cost $

Work in Progress at cost $

Finished Goods at cost $ $

4. Other current assets

Spare parts $

Accrued Income $

Prepayments $ $

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 18 of 26

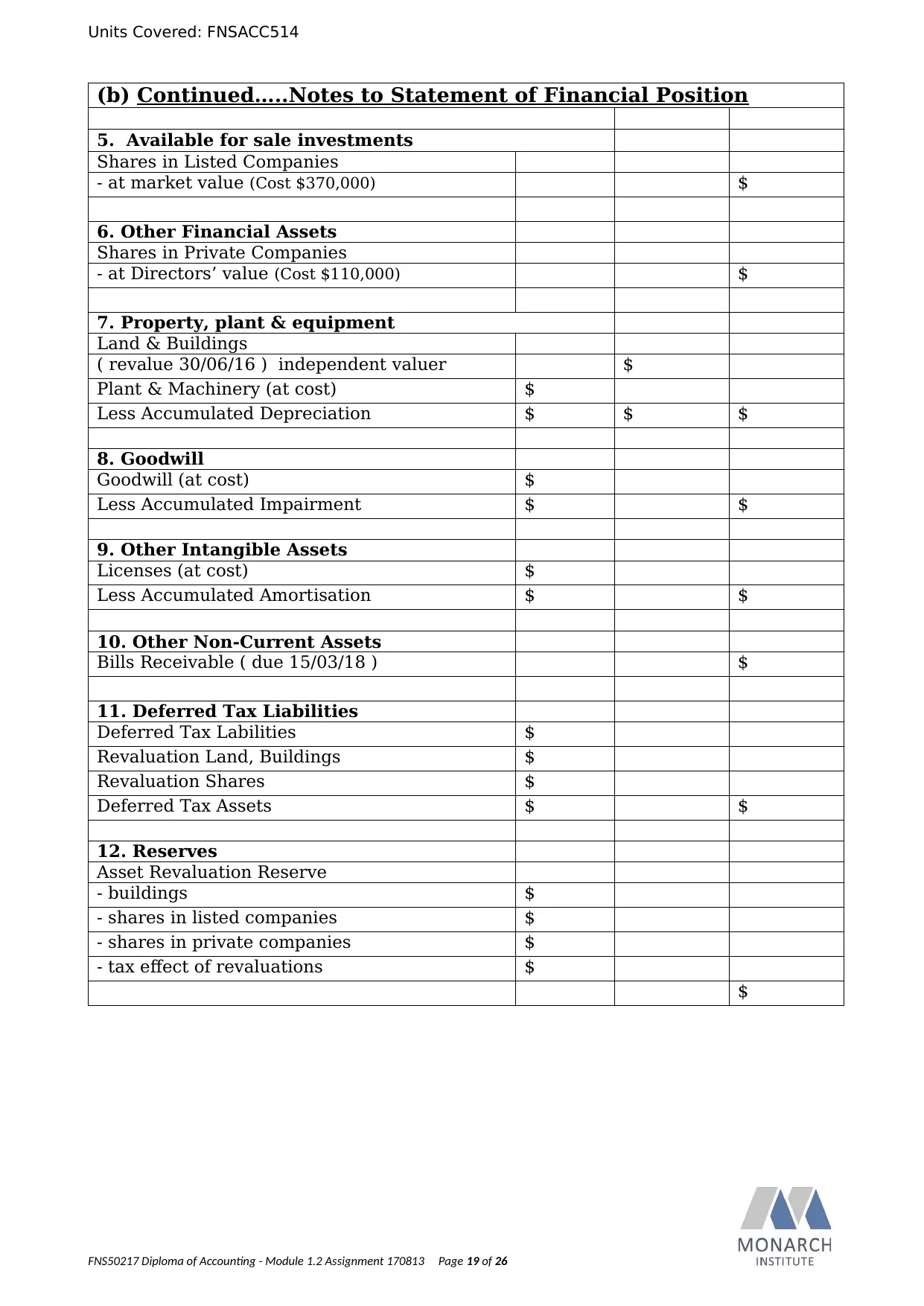

Units Covered: FNSACC514

(b) Continued…..Notes to Statement of Financial Position

5. Available for sale investments

Shares in Listed Companies

- at market value (Cost $370,000) $

6. Other Financial Assets

Shares in Private Companies

- at Directors’ value (Cost $110,000) $

7. Property, plant & equipment

Land & Buildings

( revalue 30/06/16 ) independent valuer $

Plant & Machinery (at cost) $

Less Accumulated Depreciation $ $ $

8. Goodwill

Goodwill (at cost) $

Less Accumulated Impairment $ $

9. Other Intangible Assets

Licenses (at cost) $

Less Accumulated Amortisation $ $

10. Other Non-Current Assets

Bills Receivable ( due 15/03/18 ) $

11. Deferred Tax Liabilities

Deferred Tax Labilities $

Revaluation Land, Buildings $

Revaluation Shares $

Deferred Tax Assets $ $

12. Reserves

Asset Revaluation Reserve

- buildings $

- shares in listed companies $

- shares in private companies $

- tax effect of revaluations $

$

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 19 of 26

(b) Continued…..Notes to Statement of Financial Position

5. Available for sale investments

Shares in Listed Companies

- at market value (Cost $370,000) $

6. Other Financial Assets

Shares in Private Companies

- at Directors’ value (Cost $110,000) $

7. Property, plant & equipment

Land & Buildings

( revalue 30/06/16 ) independent valuer $

Plant & Machinery (at cost) $

Less Accumulated Depreciation $ $ $

8. Goodwill

Goodwill (at cost) $

Less Accumulated Impairment $ $

9. Other Intangible Assets

Licenses (at cost) $

Less Accumulated Amortisation $ $

10. Other Non-Current Assets

Bills Receivable ( due 15/03/18 ) $

11. Deferred Tax Liabilities

Deferred Tax Labilities $

Revaluation Land, Buildings $

Revaluation Shares $

Deferred Tax Assets $ $

12. Reserves

Asset Revaluation Reserve

- buildings $

- shares in listed companies $

- shares in private companies $

- tax effect of revaluations $

$

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 19 of 26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC514

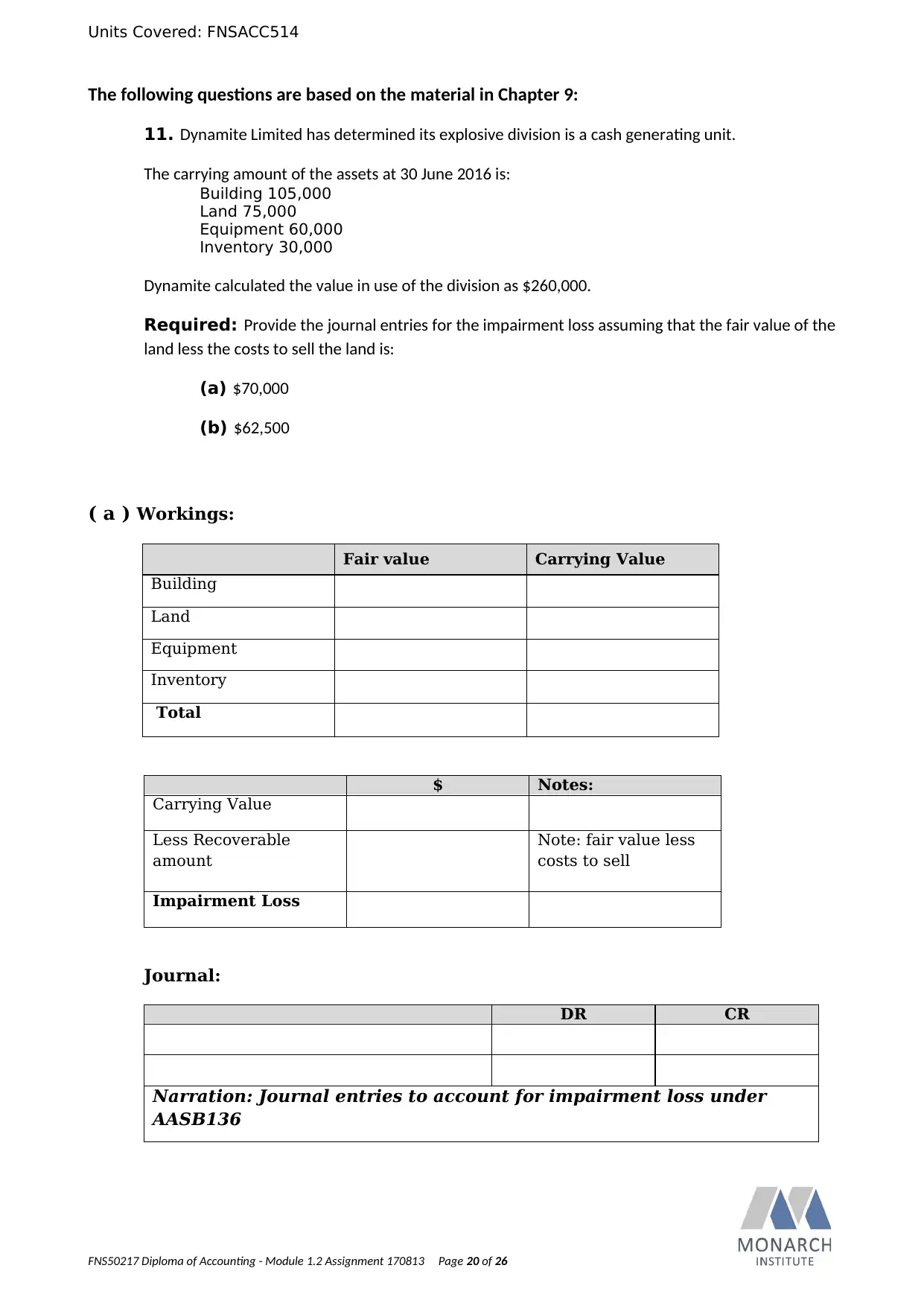

The following questions are based on the material in Chapter 9:

11. Dynamite Limited has determined its explosive division is a cash generating unit.

The carrying amount of the assets at 30 June 2016 is:

Building 105,000

Land 75,000

Equipment 60,000

Inventory 30,000

Dynamite calculated the value in use of the division as $260,000.

Required: Provide the journal entries for the impairment loss assuming that the fair value of the

land less the costs to sell the land is:

(a) $70,000

(b) $62,500

( a ) Workings:

Fair value Carrying Value

Building

Land

Equipment

Inventory

Total

$ Notes:

Carrying Value

Less Recoverable

amount

Note: fair value less

costs to sell

Impairment Loss

Journal:

DR CR

Narration: Journal entries to account for impairment loss under

AASB136

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 20 of 26

The following questions are based on the material in Chapter 9:

11. Dynamite Limited has determined its explosive division is a cash generating unit.

The carrying amount of the assets at 30 June 2016 is:

Building 105,000

Land 75,000

Equipment 60,000

Inventory 30,000

Dynamite calculated the value in use of the division as $260,000.

Required: Provide the journal entries for the impairment loss assuming that the fair value of the

land less the costs to sell the land is:

(a) $70,000

(b) $62,500

( a ) Workings:

Fair value Carrying Value

Building

Land

Equipment

Inventory

Total

$ Notes:

Carrying Value

Less Recoverable

amount

Note: fair value less

costs to sell

Impairment Loss

Journal:

DR CR

Narration: Journal entries to account for impairment loss under

AASB136

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 20 of 26

Units Covered: FNSACC514

( b )

Fair value $ Carrying Value $

Building

Land

Equipment

Inventory

Total

$ Notes:

Carrying Value

Less Recoverable

amount

Note: value in use

Impairment Loss

Journal:

DR CR

Narration: Journal entries to account for impairment loss under

AASB136

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 21 of 26

( b )

Fair value $ Carrying Value $

Building

Land

Equipment

Inventory

Total

$ Notes:

Carrying Value

Less Recoverable

amount

Note: value in use

Impairment Loss

Journal:

DR CR

Narration: Journal entries to account for impairment loss under

AASB136

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 21 of 26

Units Covered: FNSACC514

12. The acquired goodwill value for Sovereign Ltd is $73,000. The goodwill is tested for impairment and the

appropriate carrying amounts were established at:

30 June 2015 $68,000

30 June 2016 $73,000

30 June 2017 $63,000

Required:

Journal entries, if necessary, to account for any goodwill impairment at 30 June of each year.

Sovereign Ltd.

Date Account Debit Credit

30 June

2015

$

$

Impairment allowance for the year

$

$

Balance transferred

30 June 2016 Hint: Carefully consider whether you think a journal is required at 30/6/16.

Provide your explanation if no journal is required:

Date Account Debit Credit

30 June

2017

$

$

Impairment allowance for the year

$

$

Balance transferred

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 22 of 26

12. The acquired goodwill value for Sovereign Ltd is $73,000. The goodwill is tested for impairment and the

appropriate carrying amounts were established at:

30 June 2015 $68,000

30 June 2016 $73,000

30 June 2017 $63,000

Required:

Journal entries, if necessary, to account for any goodwill impairment at 30 June of each year.

Sovereign Ltd.

Date Account Debit Credit

30 June

2015

$

$

Impairment allowance for the year

$

$

Balance transferred

30 June 2016 Hint: Carefully consider whether you think a journal is required at 30/6/16.

Provide your explanation if no journal is required:

Date Account Debit Credit

30 June

2017

$

$

Impairment allowance for the year

$

$

Balance transferred

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 22 of 26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Units Covered: FNSACC514

The following questions are based on the material in Chapter 10:

13. Red Limited acquired 100% of the issued capital of Yellow Limited on 1 July 2015 for $80,000.

At that date the shareholders’ equity of Yellow Limited was:

Share Capital $60,000

Reserves $15,000

Retained Earnings $ 5,000

Required:

(a) Prepare the journal entry to eliminate the investment in Yellow Ltd by Red Ltd.

Date Account Debit Credit

30 June

2016

$

$

$

$

Journal entry to eliminate the

investment in Yellow Ltd by Red Ltd.

(b) Complete the worksheet extract, as at 30 June 2016.

Worksheet extract

as at 30 June 2016 Red Ltd Yellow Ltd Eliminations Consolidation

Balance

Dr Cr

Operating Profit after tax 48,000 33,000

Retained Earnings 01/07/15 20,000 5,000

68,000 38,000

Appropriations 28,000 14,000

Retained Earnings 30/06/16 40,000 24,000

Share Capital 200,000 60,000

Reserves 72,000 15,000

Shares in Yellow Ltd 80,000

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 23 of 26

The following questions are based on the material in Chapter 10:

13. Red Limited acquired 100% of the issued capital of Yellow Limited on 1 July 2015 for $80,000.

At that date the shareholders’ equity of Yellow Limited was:

Share Capital $60,000

Reserves $15,000

Retained Earnings $ 5,000

Required:

(a) Prepare the journal entry to eliminate the investment in Yellow Ltd by Red Ltd.

Date Account Debit Credit

30 June

2016

$

$

$

$

Journal entry to eliminate the

investment in Yellow Ltd by Red Ltd.

(b) Complete the worksheet extract, as at 30 June 2016.

Worksheet extract

as at 30 June 2016 Red Ltd Yellow Ltd Eliminations Consolidation

Balance

Dr Cr

Operating Profit after tax 48,000 33,000

Retained Earnings 01/07/15 20,000 5,000

68,000 38,000

Appropriations 28,000 14,000

Retained Earnings 30/06/16 40,000 24,000

Share Capital 200,000 60,000

Reserves 72,000 15,000

Shares in Yellow Ltd 80,000

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 23 of 26

Units Covered: FNSACC514

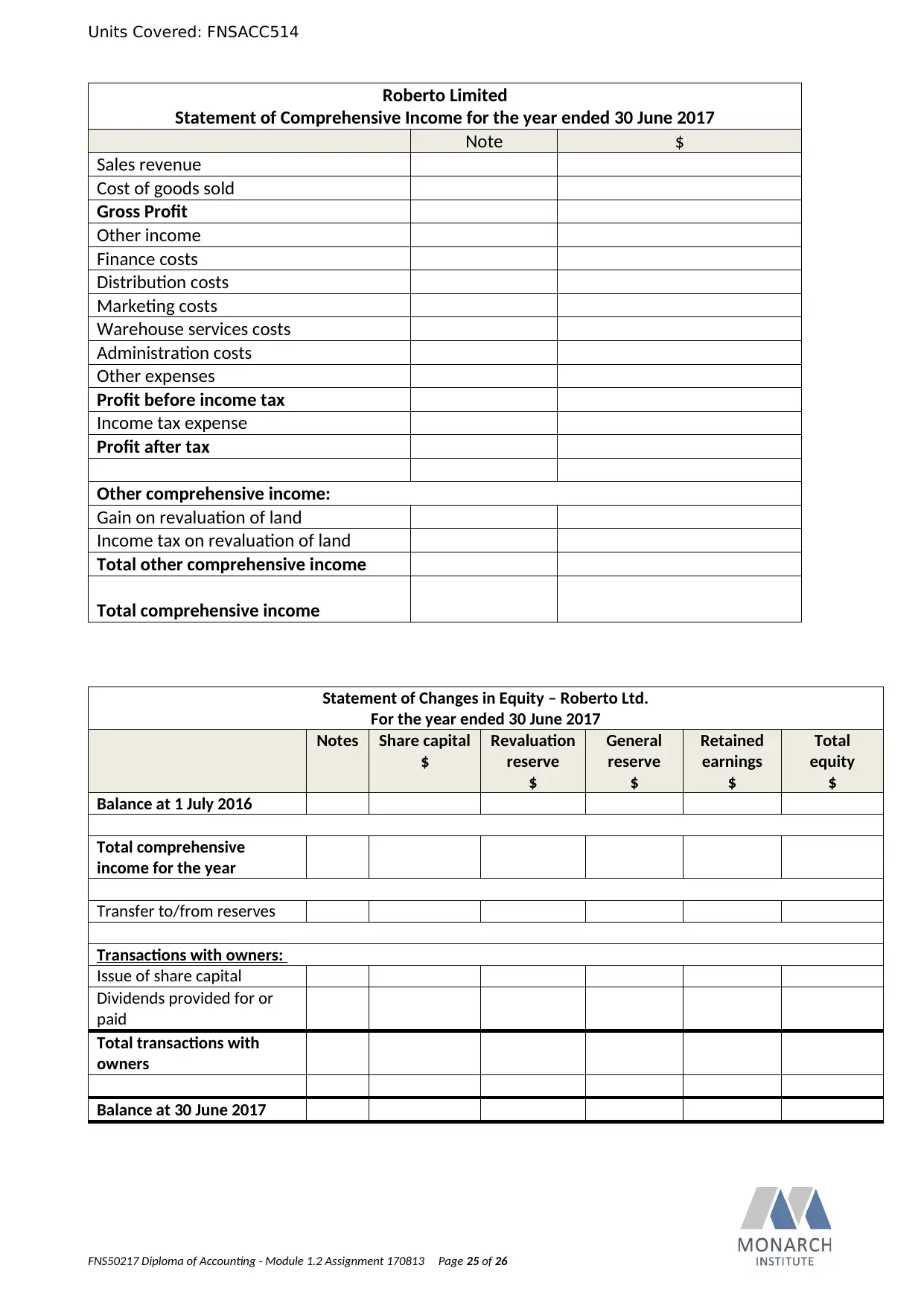

The following questions are based on the material in Chapter 8:

14. The following relates to Roberto Limited for the year ended 30 June 2017:

Sale of goods $2,050,000

Interest income 12,500

Consultancy fees received 60,000

Cost of sales 325,000

Finance costs 44,500

Distribution expenses 60,000

Marketing expenses 115,000

Warehouse services expenses 250,000

Administration expenses 55,000

Other expenses 110,000

Income tax expense 440,000

Additional information:

The balance of the asset revaluation Reserve at 1 July 2016 was $40,000. On 30 June 2017 the carrying

value of land was restated to a directors’ valuation resulting in a credit to the asset revaluation

Reserve of $150,000. Assume a company tax rate of 30%.

Retained earnings at 1 July 2016 $150,000

As at 1 July 2016 there were 400,000 fully paid ordinary shares on issue $400,000

Dividends paid and proposed during the FY:

o Interim dividend paid, fully franked $30,000

o Final dividend proposed, fully franked $22,500

Transfer from retained earnings to General Reserve $35,000

General Reserve at 1 July 2016 $nil

During the FY, a further $100,000 ordinary shares were issued and fully paid on application $100,000

Pending legal action against the company for infringement of a patent for $500,000. Directors’ don't

believe that this action will be successful.

One of the directors provided warehouse services for $50,000 in the current financial year. The service

was provided at arm’s length. This transaction has already been included the financial values provided

in the table (above).

Required: Prepare the following:

a Statement of Comprehensive Income,

a Statement of Changes in Equity and

Notes to the Financial Statements at 30 June 2017.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 24 of 26

The following questions are based on the material in Chapter 8:

14. The following relates to Roberto Limited for the year ended 30 June 2017:

Sale of goods $2,050,000

Interest income 12,500

Consultancy fees received 60,000

Cost of sales 325,000

Finance costs 44,500

Distribution expenses 60,000

Marketing expenses 115,000

Warehouse services expenses 250,000

Administration expenses 55,000

Other expenses 110,000

Income tax expense 440,000

Additional information:

The balance of the asset revaluation Reserve at 1 July 2016 was $40,000. On 30 June 2017 the carrying

value of land was restated to a directors’ valuation resulting in a credit to the asset revaluation

Reserve of $150,000. Assume a company tax rate of 30%.

Retained earnings at 1 July 2016 $150,000

As at 1 July 2016 there were 400,000 fully paid ordinary shares on issue $400,000

Dividends paid and proposed during the FY:

o Interim dividend paid, fully franked $30,000

o Final dividend proposed, fully franked $22,500

Transfer from retained earnings to General Reserve $35,000

General Reserve at 1 July 2016 $nil

During the FY, a further $100,000 ordinary shares were issued and fully paid on application $100,000

Pending legal action against the company for infringement of a patent for $500,000. Directors’ don't

believe that this action will be successful.

One of the directors provided warehouse services for $50,000 in the current financial year. The service

was provided at arm’s length. This transaction has already been included the financial values provided

in the table (above).

Required: Prepare the following:

a Statement of Comprehensive Income,

a Statement of Changes in Equity and

Notes to the Financial Statements at 30 June 2017.

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 24 of 26

Units Covered: FNSACC514

Roberto Limited

Statement of Comprehensive Income for the year ended 30 June 2017

Note $

Sales revenue

Cost of goods sold

Gross Profit

Other income

Finance costs

Distribution costs

Marketing costs

Warehouse services costs

Administration costs

Other expenses

Profit before income tax

Income tax expense

Profit after tax

Other comprehensive income:

Gain on revaluation of land

Income tax on revaluation of land

Total other comprehensive income

Total comprehensive income

Statement of Changes in Equity – Roberto Ltd.

For the year ended 30 June 2017

Notes Share capital

$

Revaluation

reserve

$

General

reserve

$

Retained

earnings

$

Total

equity

$

Balance at 1 July 2016

Total comprehensive

income for the year

Transfer to/from reserves

Transactions with owners:

Issue of share capital

Dividends provided for or

paid

Total transactions with

owners

Balance at 30 June 2017

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 25 of 26

Roberto Limited

Statement of Comprehensive Income for the year ended 30 June 2017

Note $

Sales revenue

Cost of goods sold

Gross Profit

Other income

Finance costs

Distribution costs

Marketing costs

Warehouse services costs

Administration costs

Other expenses

Profit before income tax

Income tax expense

Profit after tax

Other comprehensive income:

Gain on revaluation of land

Income tax on revaluation of land

Total other comprehensive income

Total comprehensive income

Statement of Changes in Equity – Roberto Ltd.

For the year ended 30 June 2017

Notes Share capital

$

Revaluation

reserve

$

General

reserve

$

Retained

earnings

$

Total

equity

$

Balance at 1 July 2016

Total comprehensive

income for the year

Transfer to/from reserves

Transactions with owners:

Issue of share capital

Dividends provided for or

paid

Total transactions with

owners

Balance at 30 June 2017

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 25 of 26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Units Covered: FNSACC514

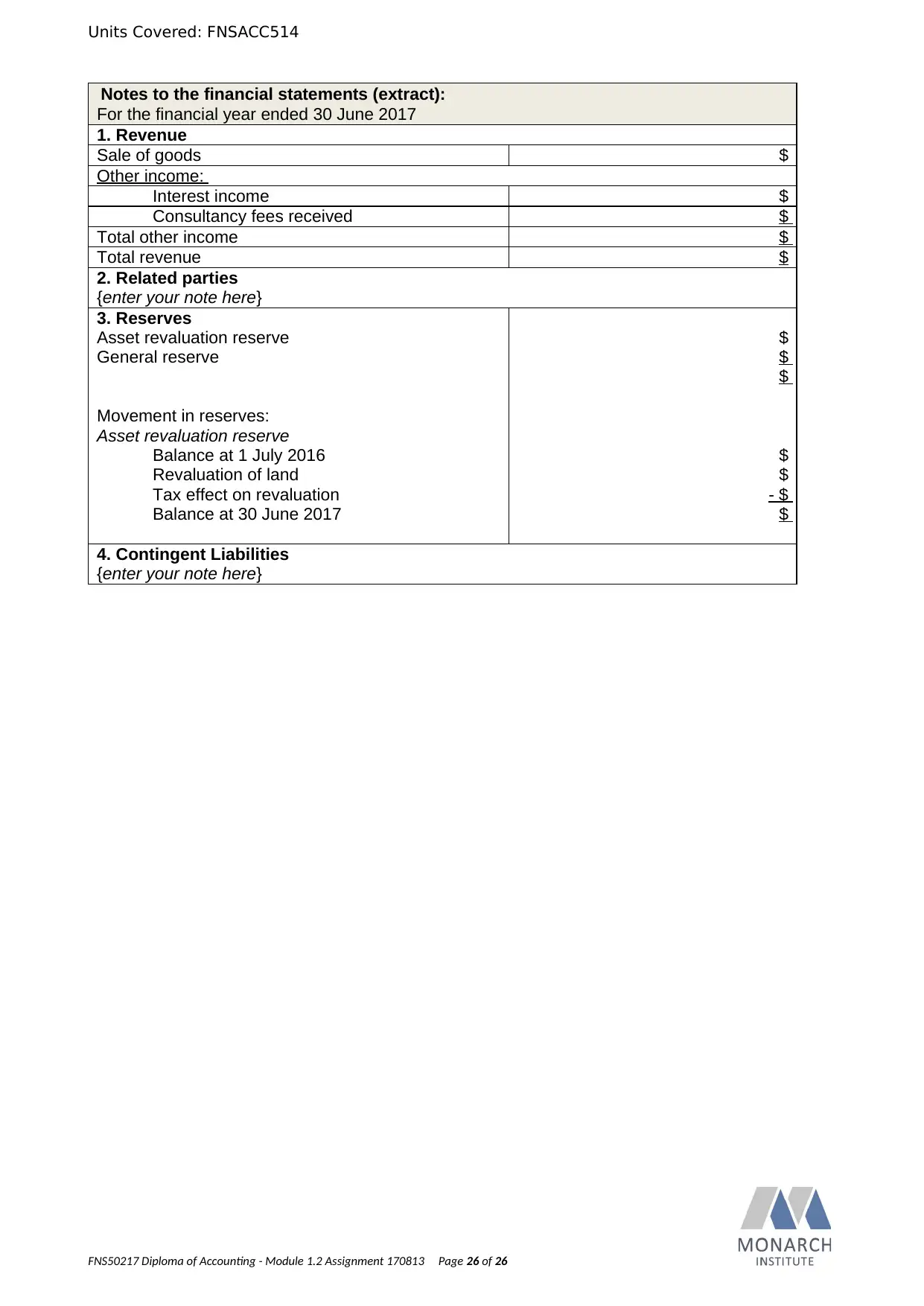

Notes to the financial statements (extract):

For the financial year ended 30 June 2017

1. Revenue

Sale of goods $

Other income:

Interest income $

Consultancy fees received $

Total other income $

Total revenue $

2. Related parties

{enter your note here}

3. Reserves

Asset revaluation reserve

General reserve

Movement in reserves:

Asset revaluation reserve

Balance at 1 July 2016

Revaluation of land

Tax effect on revaluation

Balance at 30 June 2017

$

$

$

$

$

- $

$

4. Contingent Liabilities

{enter your note here}

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 26 of 26

Notes to the financial statements (extract):

For the financial year ended 30 June 2017

1. Revenue

Sale of goods $

Other income:

Interest income $

Consultancy fees received $

Total other income $

Total revenue $

2. Related parties

{enter your note here}

3. Reserves

Asset revaluation reserve

General reserve

Movement in reserves:

Asset revaluation reserve

Balance at 1 July 2016

Revaluation of land

Tax effect on revaluation

Balance at 30 June 2017

$

$

$

$

$

- $

$

4. Contingent Liabilities

{enter your note here}

FNS50217 Diploma of Accounting - Module 1.2 Assignment 170813 Page 26 of 26

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.