Strategic Information Systems Analysis for Bell Studio (HI5019)

VerifiedAdded on 2023/01/18

Unit code: HI5019

Unit Title: Strategic Information Systems for Business and Enterprise

Name: MD SHAHRIAR ALAM

Student Id: OED2391

Paraphrase This Document

Table of Contents

Executive summary................................................................................................................................1

Introduction..............................................................................................................................................2

Data flow diagram of purchases and cash disbursement systems...........................................3

Internal control weakness and risks associated.........................................................................4

Remedies to the weaknesses in the purchasing and cash disbursement system.............5

Data flow diagram of payroll system.................................................................................................6

Internal Weaknesses of the payroll system and risks they pose............................................8

Remedies to the risks posed by the internal weakness of the payroll system...................8

System flowchart of purchases system............................................................................................9

Internal control weakness of purchases system and their risks..........................................11

Remedies to the weaknesses of the purchases system.........................................................11

System flowchart of cash disbursement system..........................................................................12

Internal control weakness of the cash disbursement system...............................................12

Remedy to the internal control weakness..................................................................................13

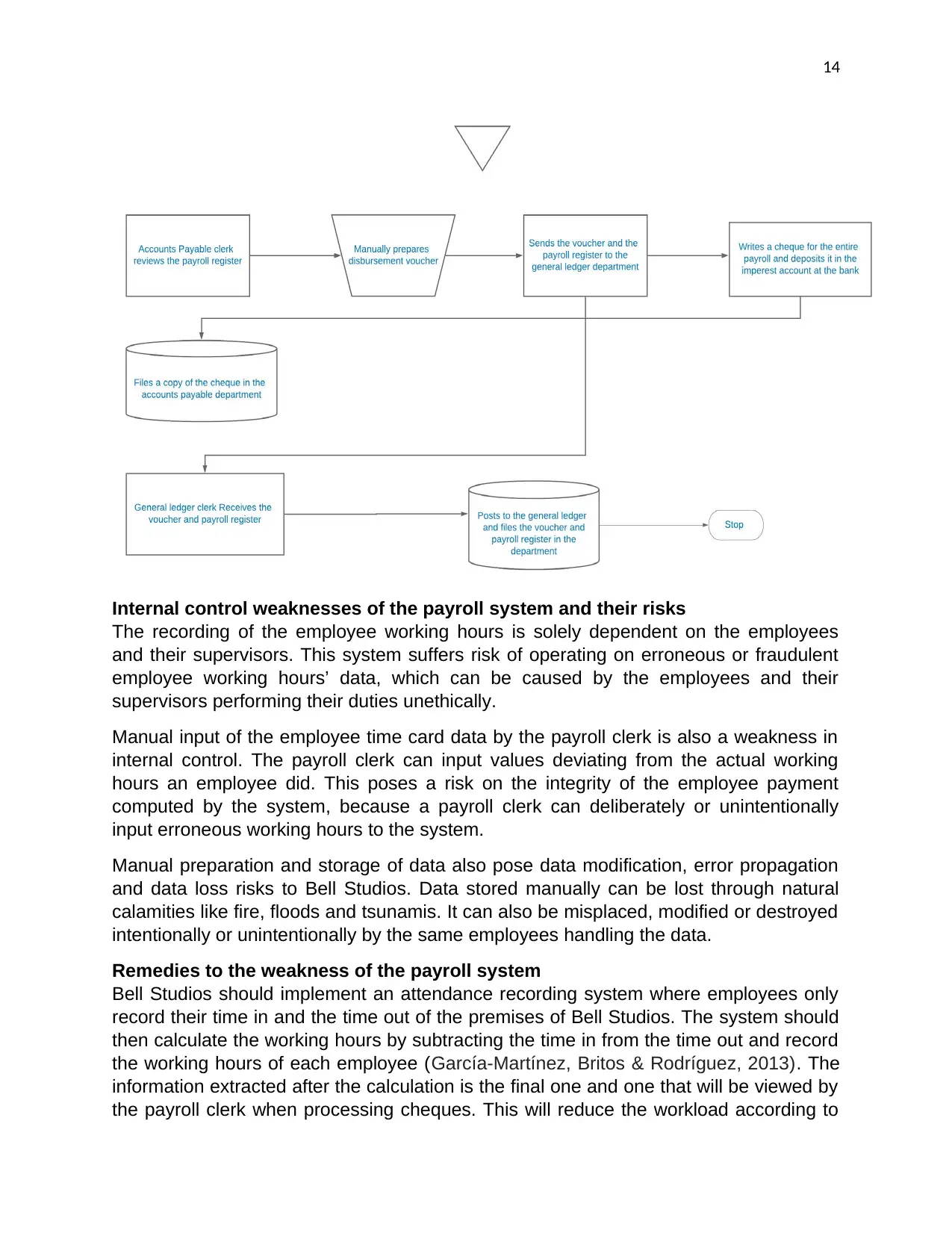

System flowchart of payroll system.................................................................................................13

Internal control weaknesses of the payroll system and their risks......................................14

Remedies to the weakness of the payroll system....................................................................14

Conclusion.............................................................................................................................................15

Recommendation..................................................................................................................................15

Bibliography..........................................................................................................................................16

Executive summary

This report comes as a response to the request made by the chief operating officer to

evaluate the processes, risks and internal controls of Bell Studios for its expenditure

cycle. When evaluating the processes, data flow diagrams and system flowcharts were

drawn to depict the operation of the individual systems; purchase and cash

disbursement system and the payroll system for proper analysis. The internal control

weaknesses identified are the failure of the system to automatically generate an alert

message or report when the quantity of certain goods is low, the allocation of system

responsibilities to humans, manual generation of reports, manual storage of data and

lack of proper measures to check the integrity, reliability and accuracy of data. The

report suggests remedies for internal control weaknesses as implementing a business

intelligent information system for generating reports and calculating employee working

hours.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The report depicts the flow of activities using data flow diagrams and system flow chart

diagrams that are; the data flow diagram of purchases and cash disbursements

systems, the data flow diagram of payroll system, system flowchart of purchases

system, system flowchart of cash disbursements and system flowchart of the payroll

system. The description of internal control weakness in each system and risks

associated with the identified weakness is also articulated in the report. The report

expounds on how these risks might affect Bell Studios and how they can be mitigated,

providing solutions for each and every internal control weakness experienced in the

system. At the end of the report, there is a conclusion that gives an informed summary

of the report and a recommendation on what Bell Studios can do to eliminate the

internal control weaknesses and avoid the risks associated with them.

Paraphrase This Document

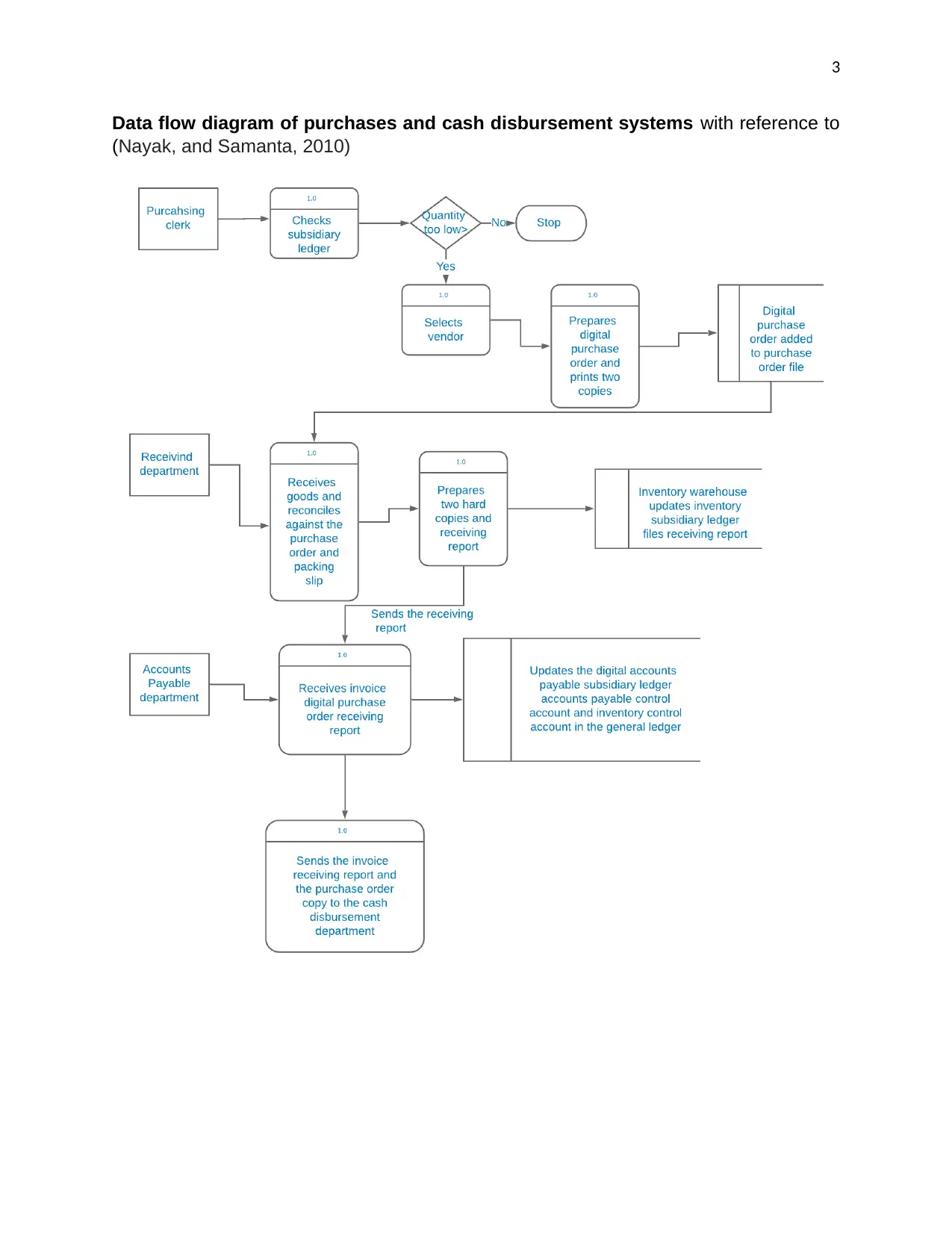

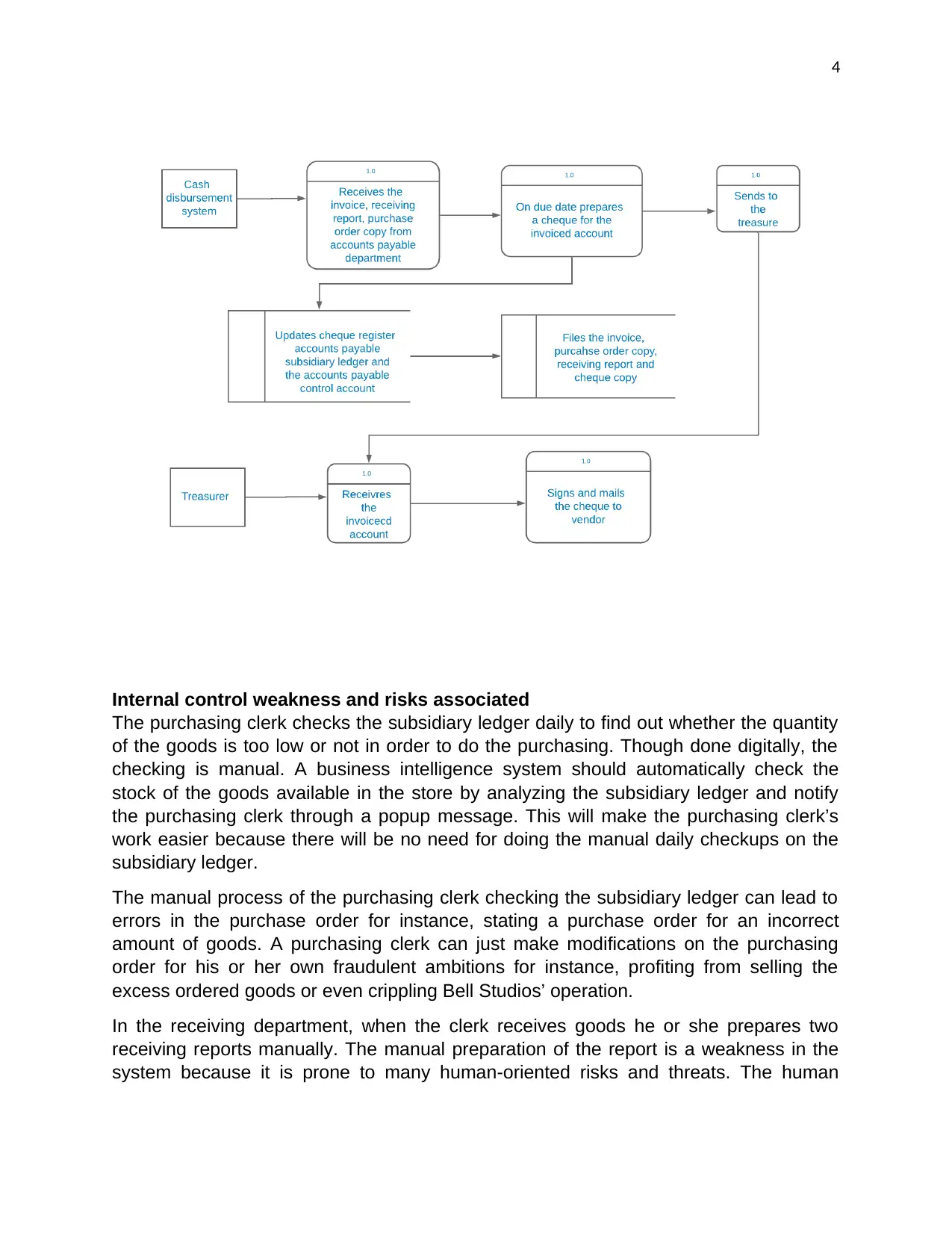

Data flow diagram of purchases and cash disbursement systems with reference to

(Nayak, and Samanta, 2010)

Internal control weakness and risks associated

The purchasing clerk checks the subsidiary ledger daily to find out whether the quantity

of the goods is too low or not in order to do the purchasing. Though done digitally, the

checking is manual. A business intelligence system should automatically check the

stock of the goods available in the store by analyzing the subsidiary ledger and notify

the purchasing clerk through a popup message. This will make the purchasing clerk’s

work easier because there will be no need for doing the manual daily checkups on the

subsidiary ledger.

The manual process of the purchasing clerk checking the subsidiary ledger can lead to

errors in the purchase order for instance, stating a purchase order for an incorrect

amount of goods. A purchasing clerk can just make modifications on the purchasing

order for his or her own fraudulent ambitions for instance, profiting from selling the

excess ordered goods or even crippling Bell Studios’ operation.

In the receiving department, when the clerk receives goods he or she prepares two

receiving reports manually. The manual preparation of the report is a weakness in the

system because it is prone to many human-oriented risks and threats. The human

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

component of a computer system is prone to make errors during the preparation of the

receiving report. The computation will never be accurate all the time.

The printed digital purchase order and the receiving report are filed manually in the

purchase and cash disbursement system. The manual filing of the reports is very

disastrous to Bell Studios business because of the following risks associated to the

data; data loss caused by natural calamities or misplacement of the files by the clerks

handling them. Hard copies of data are also easy to access, modify or destroy by

unauthorized personnel once they gain access to the store and purchasing

departments.

Remedies to the weaknesses in the purchasing and cash disbursement system.

Bell Studios need to implement a business intelligent system according to (Turban,

Sharda & Delen 2010) and (Duan, and Da Xu, 2012) that automatically checks whether

the quantity of goods is low or still in stock and generate an alert message alerting the

purchasing clerk of the stock level when the quantity of goods is too low. This will help

minimize the fraudulent risks that Bell Studios is up against leaving all the control issues

on the purchasing clerk.

Bell Studios should keep a record of all the transaction logs (Lee, Khan & Kim, 2011).

The logs record the information on when a transaction or an event was initiated, who

initiated the transaction and what effect the transaction had on the stored data or the

internal control of the system. Transaction logs help mitigate repudiation attacks where

a purchasing clerk or the clerk in the store denies performing or initiating a certain

process in the system.

The manual filling process should be eliminated from the system. All the records and

files should be stored in a centralized database where all the departments in Bell

Studios can update it whenever necessary. The files should also be backed up using

the available backup techniques like; online backup, offline backups using physical hard

drives placed in a separate location and cloud backup. Doing this, Bell Studios will avoid

unnecessary data loss caused by natural calamity or erroneous human actions.

The professional ethics framework should be set and upheld by the management of Bell

Studios. The ethics will be a guideline for professional responsibility and a depiction of

professional maturity (Bayou, Reinstein & Williams, 2011) for employees at Bell Studios.

The framework will help reduce the fraudulent behaviors that employees might develop.

It should also identify the pressure points in the work environment and find a way to

reduce or ease the pressure on the employees.

Paraphrase This Document

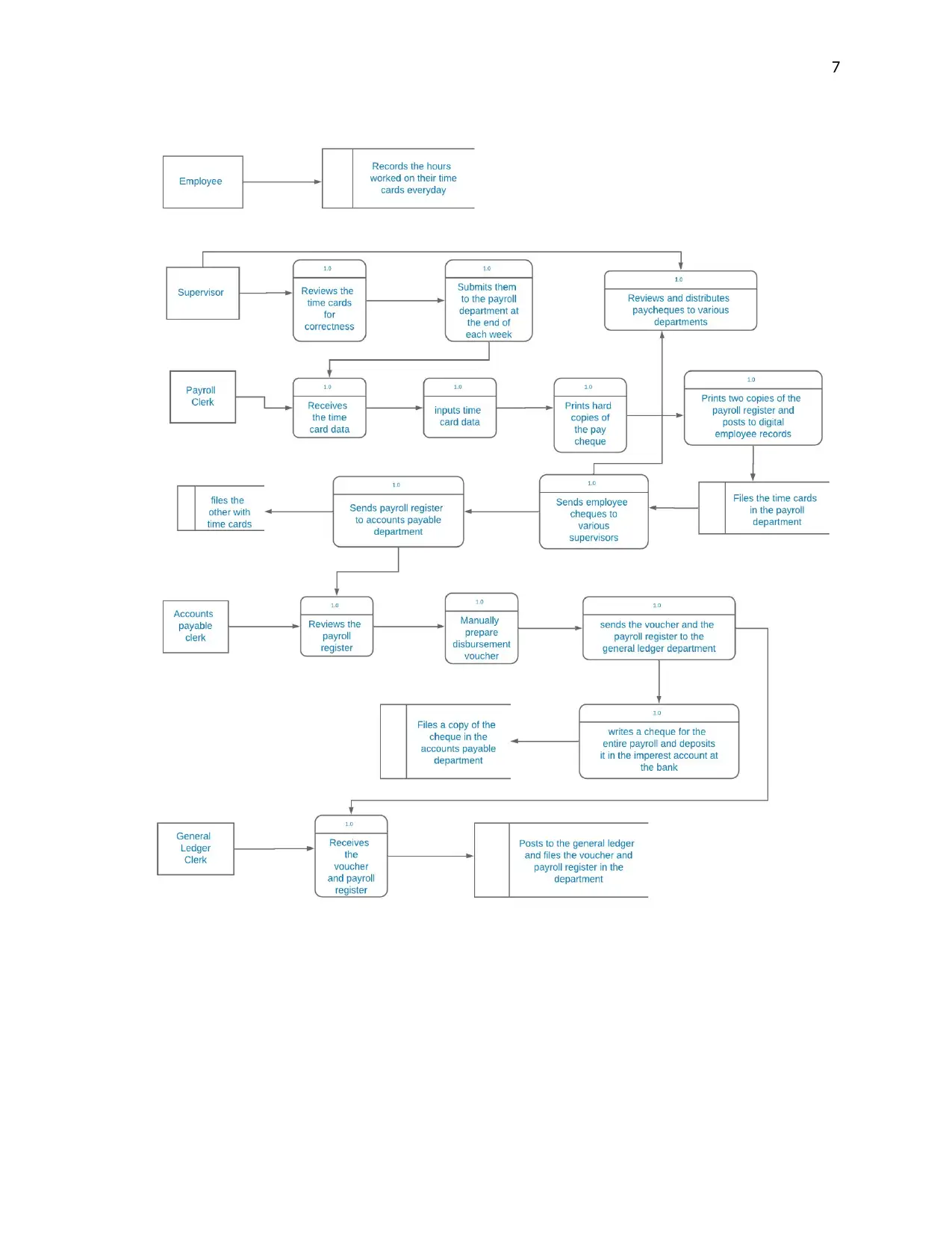

Data flow diagram of payroll system with reference to (Nayak, and Samanta, 2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal Weaknesses of the payroll system and risks they pose

Employees recording their own working hours in their time cards and having their

supervisors counter check the working hours of the employees poses a great financial

risk to Bell Studios. Employees can collude with their supervisors to enter more working

hours than they actually did. This translates to more payment than it is supposed to be

for the management of Bell Studios. The privilege a supervisor has can be misused

when a supervisor and an employee are not in good terms with each other. The system

hands a lot of power to the supervisor whereby, after the payroll clerk has input the

working hours of the employees he or she sends the pay cheques to the supervisor for

review and distribution.

Manual input of the employee time card data by the payroll clerk is also a weakness in

internal control. The payroll clerk can input values deviating from the actual working

hours an employee did. This poses a risk on the integrity of the employee payment

computed by the system, because a payroll clerk can deliberately or unintentionally

input erroneous working hours to the system.

Manual preparation and storage of data also pose data modification, error propagation

and data loss risks to Bell Studios. Data stored manually can be lost through natural

calamities like fire, floods and tsunamis. It can also be misplaced, modified or destroyed

intentionally or unintentionally by the same employees handling the data.

Remedies to the risks posed by the internal weakness of the payroll system.

Bell Studios should implement an attendance recording system (Chintalapati, and

Raghunadh, 2013) where employees only record their time in and the time out of the

premises of Bell Studios. The system should then calculate the working hours by

subtracting the time in from the time out and record the working hours of each

employee. The information extracted after the calculation is the final one and one that

will be viewed by the payroll clerk when processing cheques. This will reduce the

workload given to employee supervisors who do the counter checking of the employee

working hours and review the working hours’ details send from the payroll clerk.

The attendance recording system will eliminate the risk of fraud and collusion from the

employee and the supervisor to fraudulently acquire high payments. It will also eliminate

the risk originating from the payroll clerk, employee or supervisor deliberately or

unintentionally making erroneous inputs of the employee working hours that deviate

from the actual working hours that the employees actually did.

Paraphrase This Document

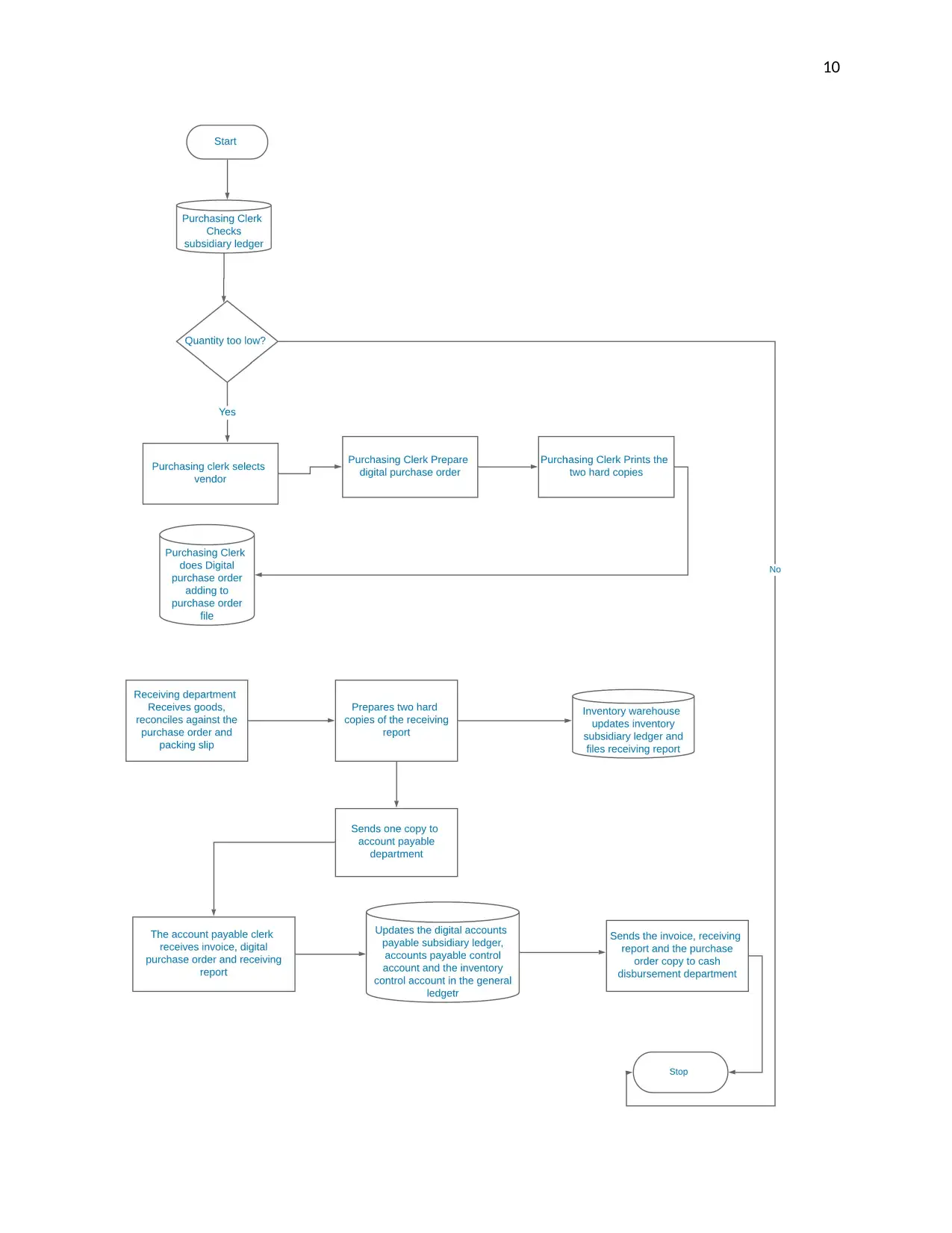

System flowchart of purchases system with reference to (Nayak, and Samanta,

2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal control weakness of purchases system and their risks

The purchase system hands a human; the purchasing clerk, the task of checking stock

or determining whether the quantity of certain goods is too low instead of handing the

task to the system. This may lead to inappropriate handling of the stock renewal

because the purchasing clerk might interpret the stock wrongly. For instance,

misquotation of the required amount of goods which may lead to over budgeting or

under budgeting.

The receiving clerk prepares and sends the receiving reports manually to the accounts

payable clerk. Hard copies of reports are vulnerable to natural calamities like fire and

floods, human manipulation and access by unauthorized personnel. This risks Bell

Studios losing their private and confidential data to natural calamities or to unauthorized

personnel.

Remedies to the weaknesses of the purchases system

The task of checking stock levels should be handed to the business intelligence system.

The systems should be checking the amount of each good from the stock every other

time it is updated and automatically generate a report or an alert for a purchase clerk

notifying him or her of a good gone out of stock or being low in quantity ( Atanasova

et.al; 2010). This reduces the responsibilities bestowed upon a purchases clerk and

reduces the possibilities of experiencing erroneous purchase orders that are the

probability of over budgeting and under-budgeting being experienced will be limited.

Having a computerized way of preparing reports helps in reducing the amount of time

needed to prepare the report (Gandomi, and Haider, 2015) and (Ko, Lee & Wah Lee,

2009). Handling and sending reports digitally reduces the risks of data loss through

natural calamities and unauthorized personnel because of the presence of backups for

data and encryption of data to ensure its safety during transit.

Paraphrase This Document

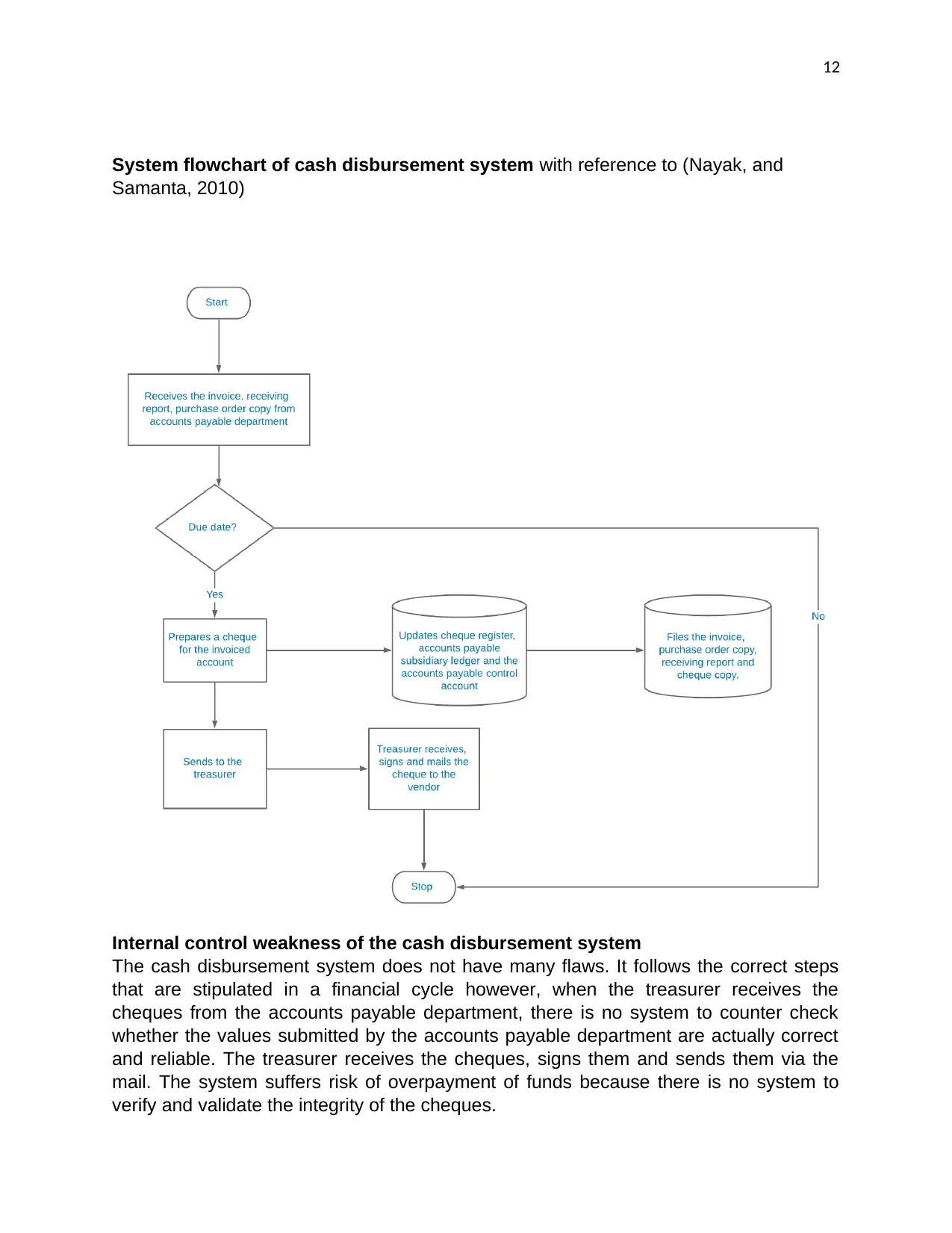

System flowchart of cash disbursement system with reference to (Nayak, and

Samanta, 2010)

Internal control weakness of the cash disbursement system

The cash disbursement system does not have many flaws. It follows the correct steps

that are stipulated in a financial cycle however, when the treasurer receives the

cheques from the accounts payable department, there is no system to counter check

whether the values submitted by the accounts payable department are actually correct

and reliable. The treasurer receives the cheques, signs them and sends them via the

mail. The system suffers risk of overpayment of funds because there is no system to

verify and validate the integrity of the cheques.

Remedy to the internal control weakness

The system should provide a module, process or a method through which the cheque

details handed to the treasurer for signing and mailing to the vendor can be verified for

reliability (Elbashir, Collier & Sutton, 2011) often termed as accounting.

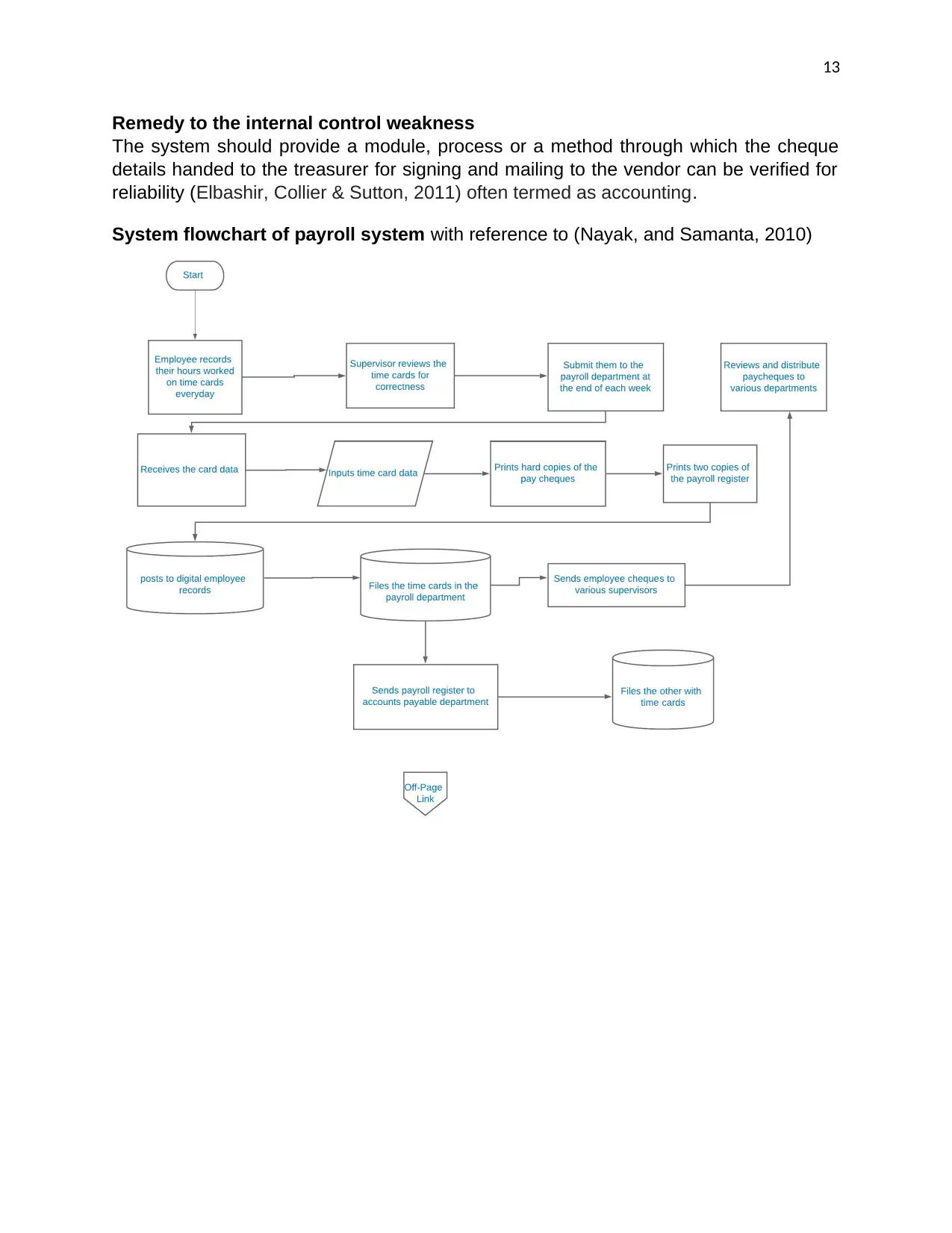

System flowchart of payroll system with reference to (Nayak, and Samanta, 2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal control weaknesses of the payroll system and their risks

The recording of the employee working hours is solely dependent on the employees

and their supervisors. This system suffers risk of operating on erroneous or fraudulent

employee working hours’ data, which can be caused by the employees and their

supervisors performing their duties unethically.

Manual input of the employee time card data by the payroll clerk is also a weakness in

internal control. The payroll clerk can input values deviating from the actual working

hours an employee did. This poses a risk on the integrity of the employee payment

computed by the system, because a payroll clerk can deliberately or unintentionally

input erroneous working hours to the system.

Manual preparation and storage of data also pose data modification, error propagation

and data loss risks to Bell Studios. Data stored manually can be lost through natural

calamities like fire, floods and tsunamis. It can also be misplaced, modified or destroyed

intentionally or unintentionally by the same employees handling the data.

Remedies to the weakness of the payroll system

Bell Studios should implement an attendance recording system where employees only

record their time in and the time out of the premises of Bell Studios. The system should

then calculate the working hours by subtracting the time in from the time out and record

the working hours of each employee (García-Martínez, Britos & Rodríguez, 2013). The

information extracted after the calculation is the final one and one that will be viewed by

the payroll clerk when processing cheques. This will reduce the workload according to

Paraphrase This Document

(Chen, Chiang & Storey, 2012) given to employee supervisors who do the counter

checking of the employee working hours and review the working hours’ details send

from the payroll clerk.

Conclusion

The systems face common internal control weaknesses; misallocation of system-

oriented tasks and responsibilities to humans, manual processing and storing of data,

repetition of the data input process, lack of measures to check the reliability of

information and manual generation of reports. These weaknesses cause error

propagation, data loss and fraudulent practices going against the professional code of

ethics. These weaknesses are evident through; employees filling their time cards,

supervisors being given an additional responsibility of verifying the working hours of

employees in the time cards and validating the cheques, payroll clerk doing inputs of the

working hours from the time cards to the payroll system and the data processing being

achieved manually.

Recommendation

Bell Studios should implement business intelligence aspect of information systems in all

their systems. For instance, the report auto-generation in the purchasing department

where the purchase system automatically displays an alert message when the quantity

of goods becomes too low in the store. Automatic calculation and recording of the

employee working hours through the use of an attendance information system that only

takes the employee’s time in and time out of Bell Studios premises when their allocated

work is complete. Bell Studios should also upgrade the processing of data from manual,

as observed in the receiving department where receiving reports are generated

manually, to digital.

Bibliography

Atanasova, T., Kasheva, M., Sulova, S. and Vasilev, J., 2010, May. Analysis of the

possible application of Data Mining, Text Mining and Web Mining in business intelligent

systems. In The 33rd International Convention MIPRO (pp. 1294-1297). Ukraine, IEEE.

Bayou, M.E., Reinstein, A. and Williams, P.F., 2011. To tell the truth: A discussion of

issues concerning truth and ethics in accounting. Accounting, Organizations and

Society, 36(2), pp.109-124. New York, Elsevier.

Chen, H., Chiang, R.H. and Storey, V.C., 2012. Business intelligence and analytics:

From big data to big impact. MIS quarterly, 36(4).

Chintalapati, S. and Raghunadh, M.V., 2013, December. Automated attendance

management system based on face recognition algorithms. In 2013 IEEE International

Conference on Computational Intelligence and Computing Research (pp. 1-5). Cavtat,

Croatia. IEEE

Duan, L. and Da Xu, L., 2012. Business intelligence for enterprise systems: a

survey. IEEE Transactions on Industrial Informatics, 8(3), pp.679-687. Heidelberg.

Springer.

Elbashir, M.Z., Collier, P.A. and Sutton, S.G., 2011. The role of organizational

absorptive capacity in strategic use of business intelligence to support integrated

management control systems. The Accounting Review, 86(1), pp.155-184. Florida,

American Accounting Association. Accessed [21 April 2019] Accessed from:

https://www.jstor.org/stable/29780228?seq=1#metadata_info_tab_contents

Gandomi, A. and Haider, M., 2015. Beyond the hype: Big data concepts, methods, and

analytics. International journal of information management, 35(2), pp.137-144. King

Saud University. Accessed [21 April 2019] Retrieved from:

https://www.sciencedirect.com/science/article/pii/S0268401214001066

García-Martínez, R., Britos, P. and Rodríguez, D., 2013, June. Information mining

processes based on intelligent systems. In International Conference on Industrial,

Engineering and Other Applications of Applied Intelligent Systems (pp. 402-410). Berlin,

Heidelberg. Springer

Ko, R.K., Lee, S.S. and Wah Lee, E., 2009. Business process management (BPM)

standards: a survey. Business Process Management Journal, 15(5), pp.744-791.

Singapore. Nanyang Technologica University.

Lee, M.W., Khan, A.M. and Kim, T.S., 2011. A single tri-axial accelerometer-based real-

time personal life log system capable of human activity recognition and exercise

information generation. Personal and Ubiquitous Computing, 15(8), pp.887-898. Varlag,

London. Springer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nayak, A. and Samanta, D., 2010. Automatic test data synthesis using uml sequence

diagrams. journal of Object Technology, 9(2), pp.75-104.MIT Library. Accessed [21 April

2019]. Retrieved from:

http://eprints.manipal.edu/id/eprint/261

Turban, E., Sharda, R. and Delen, D., 2010. Decision Support and Business Intelligence

Systems (required). Google Scholar.

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.