University of South Australia: MATH 1053 Quber Case Study Report

VerifiedAdded on 2022/11/29

|16

|1853

|72

Report

AI Summary

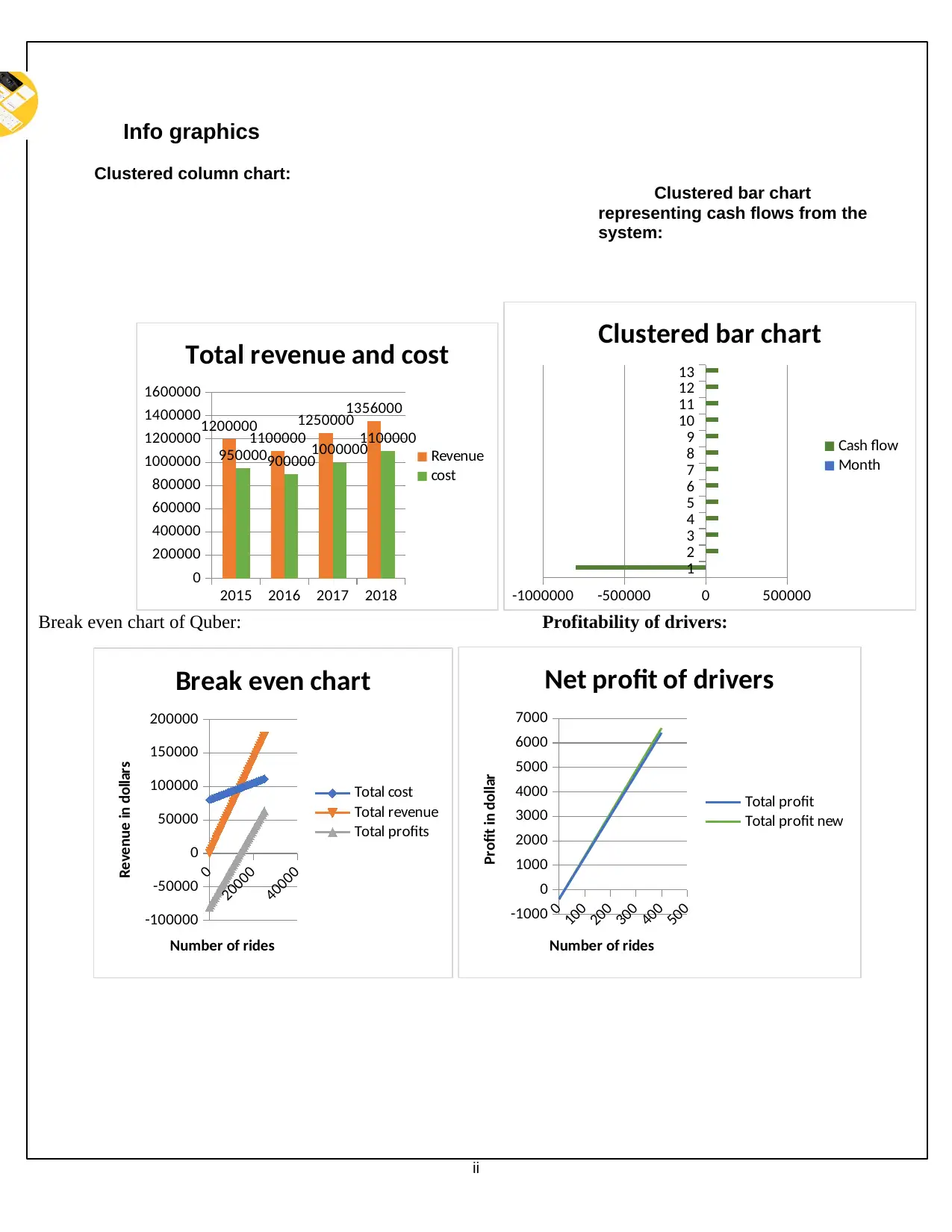

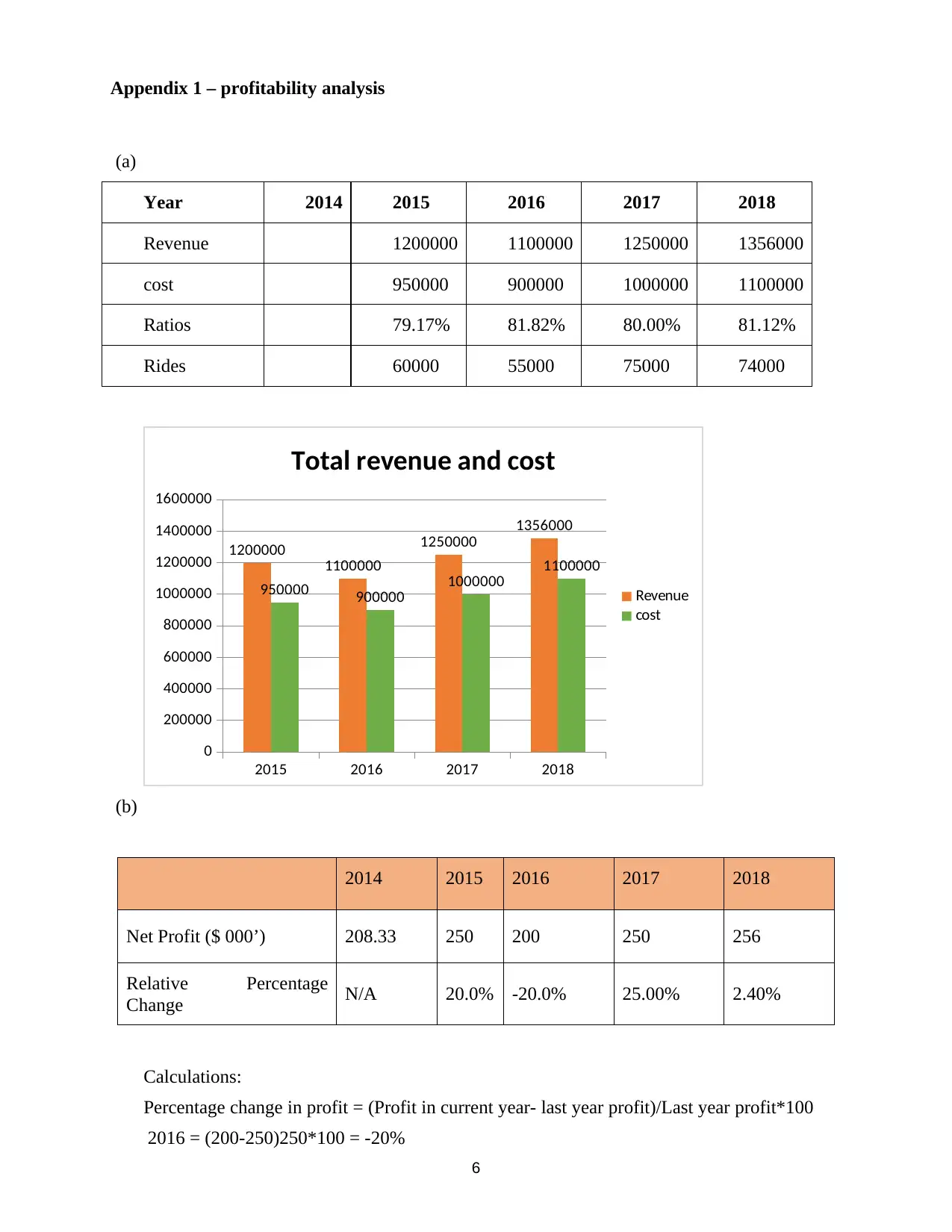

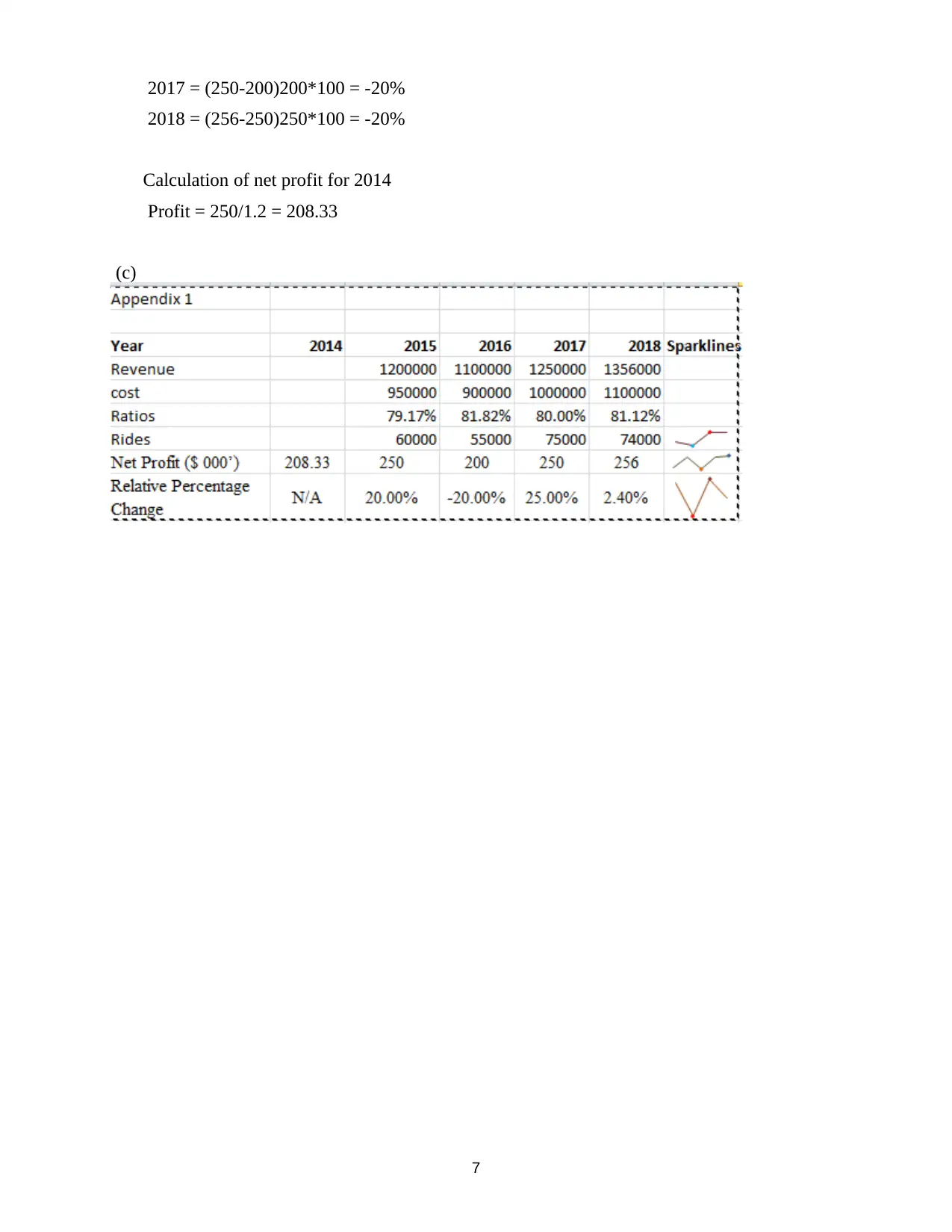

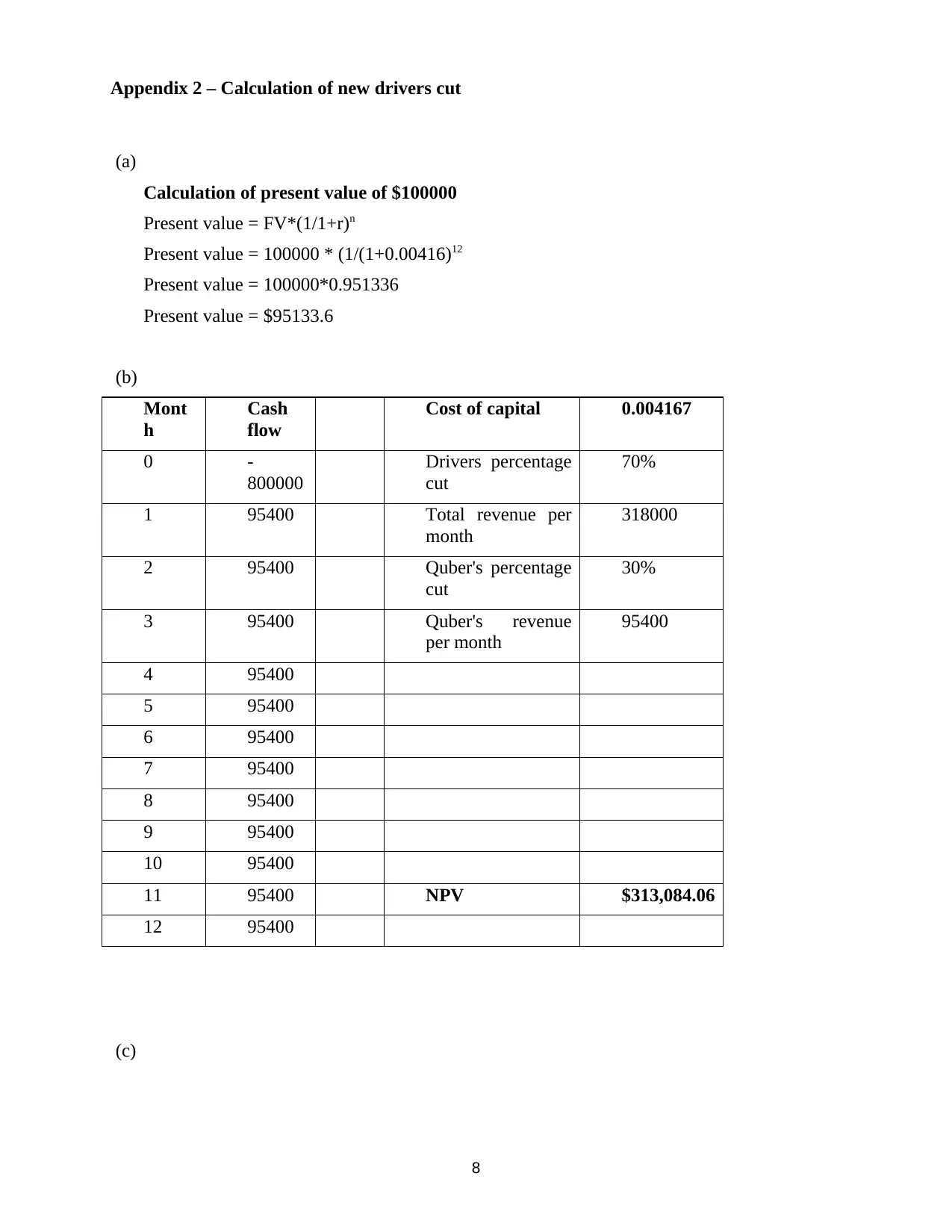

This report provides a quantitative analysis of Quber's financial performance, including revenue, costs, and profitability. The analysis covers break-even points, driver cuts, and the impact of changes in petrol costs. The report utilizes various techniques such as break-even analysis and profitability testing, supported by financial data, clustered column charts, and sparklines. It examines the impact of a new driver cut on the company's revenue and profitability, calculates break-even rides for both the company and drivers, and explores the effect of reduced petrol costs on profitability. The report concludes with recommendations based on the findings and references relevant sources.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.