University BUS0002: Data Analysis and Financial Statement Report

VerifiedAdded on 2022/10/05

|11

|3383

|198

Report

AI Summary

This report provides a comprehensive analysis of data types, including qualitative and quantitative data, and explores the differences between horizontal and vertical analysis. It delves into the concept of data quality and its importance in financial statements, highlighting its impact on decision-making, transparency, and error mitigation. The report further assesses the performance of British Airways, using provided data to determine the aircraft manufacturer with the largest fleet and calculate relevant financial ratios such as return on capital employed, return on equity, and the current ratio. Finally, it identifies and discusses various risk factors that could negatively affect British Airways' market position and revenue, drawing on the provided annual report and supplementary materials.

Using Information

1

<University>

Using information

<Author>

31 August 2024

<Professor’s name>

<Program of Study>

1

<University>

Using information

<Author>

31 August 2024

<Professor’s name>

<Program of Study>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Using Information

2

1.

a) Difference between qualitative data and quantitative data

The term Qualitative data

This refers to a type of data that approximates, characterizes and includes techniques designs

and estimates that do not give discrete arithmetical data

Types of qualitative data include

i. Binomial data –this refers to qualitative data which put items in one of the two

absolutely conjoint categories, example right or wrong

ii. Nominal data – this refer to qualitative data that put items in one of the two named

categories that do not have inferred or original value

iii. Ordinal data – refers to qualitative data that assign items to categories that do have

some type of inferred or original rank or value

Examples include tastes, textures, smells, attractiveness, and color

Whereas,

Quantitative data

This refers to a data type that is quantifiable and which entails designs, methods, and

estimates that give discrete arithmetical data (Lewin, 2015, pp.215-225.)

Types of quantitative data include

i. Continuous data- this refers to data that can be distributed, apportioned and given to

smaller levels. To mention one can measure the width of a field into more accurate

measures such as into centimetres, meters, and kilometres

ii. Discrete data -these are counts that cannot be accurately quantifiable or made more

precise with indivisible entities. For instance, you cannot have 1.4 adults

Examples are humidity, temperature, prices, area, and volume

b) Difference between horizontal analysis and vertical analysis

Horizontal analysis

Trend analysis also referred to as horizontal analysis which is a financial statement analysis

method that depicts fluctuations in the numbers relating to financial statement units or objects

over a given span of time (Lakada, Lapian, and Tumiwa, 2017. 2012-2016, pg53).

An example of horizontal analysis for instance when comparing sale in the year 2017 and

2018 shows how to prepare horizontal analysis between the two years

The horizontal analysis is extremely effective in understanding the performance of an

organization in a period. The financial statements of an organization shows the financial state

of the organization as well as its performance during a period. Horizontal analysis contains

data about an organization in stepwise format. It helps in analysing the financial state and

performance of the organization during a period without going into any comparative analysis.

Vertical analysis

2

1.

a) Difference between qualitative data and quantitative data

The term Qualitative data

This refers to a type of data that approximates, characterizes and includes techniques designs

and estimates that do not give discrete arithmetical data

Types of qualitative data include

i. Binomial data –this refers to qualitative data which put items in one of the two

absolutely conjoint categories, example right or wrong

ii. Nominal data – this refer to qualitative data that put items in one of the two named

categories that do not have inferred or original value

iii. Ordinal data – refers to qualitative data that assign items to categories that do have

some type of inferred or original rank or value

Examples include tastes, textures, smells, attractiveness, and color

Whereas,

Quantitative data

This refers to a data type that is quantifiable and which entails designs, methods, and

estimates that give discrete arithmetical data (Lewin, 2015, pp.215-225.)

Types of quantitative data include

i. Continuous data- this refers to data that can be distributed, apportioned and given to

smaller levels. To mention one can measure the width of a field into more accurate

measures such as into centimetres, meters, and kilometres

ii. Discrete data -these are counts that cannot be accurately quantifiable or made more

precise with indivisible entities. For instance, you cannot have 1.4 adults

Examples are humidity, temperature, prices, area, and volume

b) Difference between horizontal analysis and vertical analysis

Horizontal analysis

Trend analysis also referred to as horizontal analysis which is a financial statement analysis

method that depicts fluctuations in the numbers relating to financial statement units or objects

over a given span of time (Lakada, Lapian, and Tumiwa, 2017. 2012-2016, pg53).

An example of horizontal analysis for instance when comparing sale in the year 2017 and

2018 shows how to prepare horizontal analysis between the two years

The horizontal analysis is extremely effective in understanding the performance of an

organization in a period. The financial statements of an organization shows the financial state

of the organization as well as its performance during a period. Horizontal analysis contains

data about an organization in stepwise format. It helps in analysing the financial state and

performance of the organization during a period without going into any comparative analysis.

Vertical analysis

Using Information

3

This refers to a financial statement analysis technique that expresses each amount on a

financial statement as a percentage of another given amount (Rahman, 2019.)

For example, vertical analysis can be used in analysis of the balance sheet to result in every

amount in the balance sheet expressed as a percentage of the total assets.

The vertical analysis on the other hand is extremely useful for comparative analysis of

financial statements of an organization. Vertical analysis is useful in comparing the

performance of an organization in the current period with its performance in preceding year

or two or more preceding years. Vertical balance sheet containing information about assets

and liabilities of an organization again will be easier to compare due to the comparative data

provided in such statement.

Statistical data

This refers to a branch of mathematics that deals with numerical data collection, organization,

analysis and interpretation (Agrawal, and Gopal, 2018, pp. 93-99).

Statistics as a scientific discipline is fundamental in facilitating quantifiable and accurate

information is extracted from big data

Whereas

Big data

This refers to the process of obtaining and interpreting complex data types in terms of

variation and volume, in other situations the speed at which they should be assembled

(Sagiroglu, and Sinanc, 2019, pp. 42-47).

2. Meaning of data quality.

Data quality this refers to an intricate way of measuring data properties from different

perspectives as a function of its ability to be conveniently processed and interpreted for other

applications such as data warehouse, database or data analytics system (Jarke, Jeusfeld,

Quix, and Vassiliadis, 2019. pp.229-253).

Importance of data quality in the financial statements

Financial statements refer to written reports produced by an organization’s management that

convey the business operations, the financial position and the financial performance of an

organization for a given accounting period

i. It enhances improved and informed decision making

Improved data quality leads to better and informed decision making across the company. A

thorough analysis of the financial statements for example balance sheet enables the financial

manager to know the value of the existing assets if they afford more and in severe

depreciation if assets can be disposed of

ii. Increased transparency of the financial statements

3

This refers to a financial statement analysis technique that expresses each amount on a

financial statement as a percentage of another given amount (Rahman, 2019.)

For example, vertical analysis can be used in analysis of the balance sheet to result in every

amount in the balance sheet expressed as a percentage of the total assets.

The vertical analysis on the other hand is extremely useful for comparative analysis of

financial statements of an organization. Vertical analysis is useful in comparing the

performance of an organization in the current period with its performance in preceding year

or two or more preceding years. Vertical balance sheet containing information about assets

and liabilities of an organization again will be easier to compare due to the comparative data

provided in such statement.

Statistical data

This refers to a branch of mathematics that deals with numerical data collection, organization,

analysis and interpretation (Agrawal, and Gopal, 2018, pp. 93-99).

Statistics as a scientific discipline is fundamental in facilitating quantifiable and accurate

information is extracted from big data

Whereas

Big data

This refers to the process of obtaining and interpreting complex data types in terms of

variation and volume, in other situations the speed at which they should be assembled

(Sagiroglu, and Sinanc, 2019, pp. 42-47).

2. Meaning of data quality.

Data quality this refers to an intricate way of measuring data properties from different

perspectives as a function of its ability to be conveniently processed and interpreted for other

applications such as data warehouse, database or data analytics system (Jarke, Jeusfeld,

Quix, and Vassiliadis, 2019. pp.229-253).

Importance of data quality in the financial statements

Financial statements refer to written reports produced by an organization’s management that

convey the business operations, the financial position and the financial performance of an

organization for a given accounting period

i. It enhances improved and informed decision making

Improved data quality leads to better and informed decision making across the company. A

thorough analysis of the financial statements for example balance sheet enables the financial

manager to know the value of the existing assets if they afford more and in severe

depreciation if assets can be disposed of

ii. Increased transparency of the financial statements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Using Information

4

Improved data quality will help to ensure that even the least details in the statement of

financial position can make a great impact on the organization. This can be made possible for

instance by providing figure like profit earned before tax, profit retained after tax and

depreciation of assets which are able to inform the financial manager a lot

iii. Mitigation of errors

High and improved data quality is able to mitigate errors by ensuring accurate and detailed

financial statements which are important to avoid and cut on costly mistakes. If an error has

occurred reconciliation procedures are able to find them

iv. Trust building and confidence in the financial statements

Most importantly an improved data quality is able to result in an accurate financial statement

that induces trust in the business. Investors and creditors need to know that the business is

doing well before putting in their funds this can be made possible if the balance is showing

profit rather than losses

v. Better payment cycles

Ultimately, high data quality can lead to improved payment cycles as it optimizes on the

accounts payable and accounts receivable cycles, which help to ensure accurate financial

statements on the outgoing payments such as dividends to shareholders

vi. Evaluation of tax liability

High data quality will enable the company to reduce its tax burden through the loopholes that

exist in tax laws because when the company makes high profit the corporate tax rates is

equally high, therefore tax evaluation is necessary

vii. Better strategic planning and forecasting

High data quality in the financial statements is able to create opportunities for educated and

informed strategic management planning and forecasting through the cash flow statements

and trading accounts

viii. Competitive advantage

If a business is using high data quality than the competitors, then they gain competitive

advantage since data is the most valuable resource in today’s businesses

Assessment of two

1.

a. Below is the ascertainment of the aircraft manufacturer with the greatest

number of the fleet from the year 2017 data report

Boeing, with a fleet number of eight with airbus having six and Embraer having a fleet

number of 2. Therefore, Boeing having the largest fleet

b. Determining the aircraft manufacturer with the biggest or largest fleet depiction

from the given data for the year ended 2017

Using addition to determine the total of each aircraft manufacturer to find British air

fleet with the largest presentation

Ultimately, adding the number of the fleet under each of the three aircraft

Airbus total= 1+44+67+18+12= 142

4

Improved data quality will help to ensure that even the least details in the statement of

financial position can make a great impact on the organization. This can be made possible for

instance by providing figure like profit earned before tax, profit retained after tax and

depreciation of assets which are able to inform the financial manager a lot

iii. Mitigation of errors

High and improved data quality is able to mitigate errors by ensuring accurate and detailed

financial statements which are important to avoid and cut on costly mistakes. If an error has

occurred reconciliation procedures are able to find them

iv. Trust building and confidence in the financial statements

Most importantly an improved data quality is able to result in an accurate financial statement

that induces trust in the business. Investors and creditors need to know that the business is

doing well before putting in their funds this can be made possible if the balance is showing

profit rather than losses

v. Better payment cycles

Ultimately, high data quality can lead to improved payment cycles as it optimizes on the

accounts payable and accounts receivable cycles, which help to ensure accurate financial

statements on the outgoing payments such as dividends to shareholders

vi. Evaluation of tax liability

High data quality will enable the company to reduce its tax burden through the loopholes that

exist in tax laws because when the company makes high profit the corporate tax rates is

equally high, therefore tax evaluation is necessary

vii. Better strategic planning and forecasting

High data quality in the financial statements is able to create opportunities for educated and

informed strategic management planning and forecasting through the cash flow statements

and trading accounts

viii. Competitive advantage

If a business is using high data quality than the competitors, then they gain competitive

advantage since data is the most valuable resource in today’s businesses

Assessment of two

1.

a. Below is the ascertainment of the aircraft manufacturer with the greatest

number of the fleet from the year 2017 data report

Boeing, with a fleet number of eight with airbus having six and Embraer having a fleet

number of 2. Therefore, Boeing having the largest fleet

b. Determining the aircraft manufacturer with the biggest or largest fleet depiction

from the given data for the year ended 2017

Using addition to determine the total of each aircraft manufacturer to find British air

fleet with the largest presentation

Ultimately, adding the number of the fleet under each of the three aircraft

Airbus total= 1+44+67+18+12= 142

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Using Information

5

Boeing total = 36+3+8+46+12+9+16= 130

Embraer total = 6+15 =21

Airbus fleet has the biggest representation with 142 fleet

c. Calculated below is the percentage of the aircraft with the biggest representation

from the solutions in b) above expressed as a fraction of the total in 2017

The percentage of Airbus fleet is determined by expressing the value that is 142 then

dividing it by the total number of fleets from all the three manufacturers multiplied by

one hundred percent

The total number of the fleet is 293

Airbus with 142 represents 142 * 100 =48%

293

The airbus, therefore, has a percentage of 48%

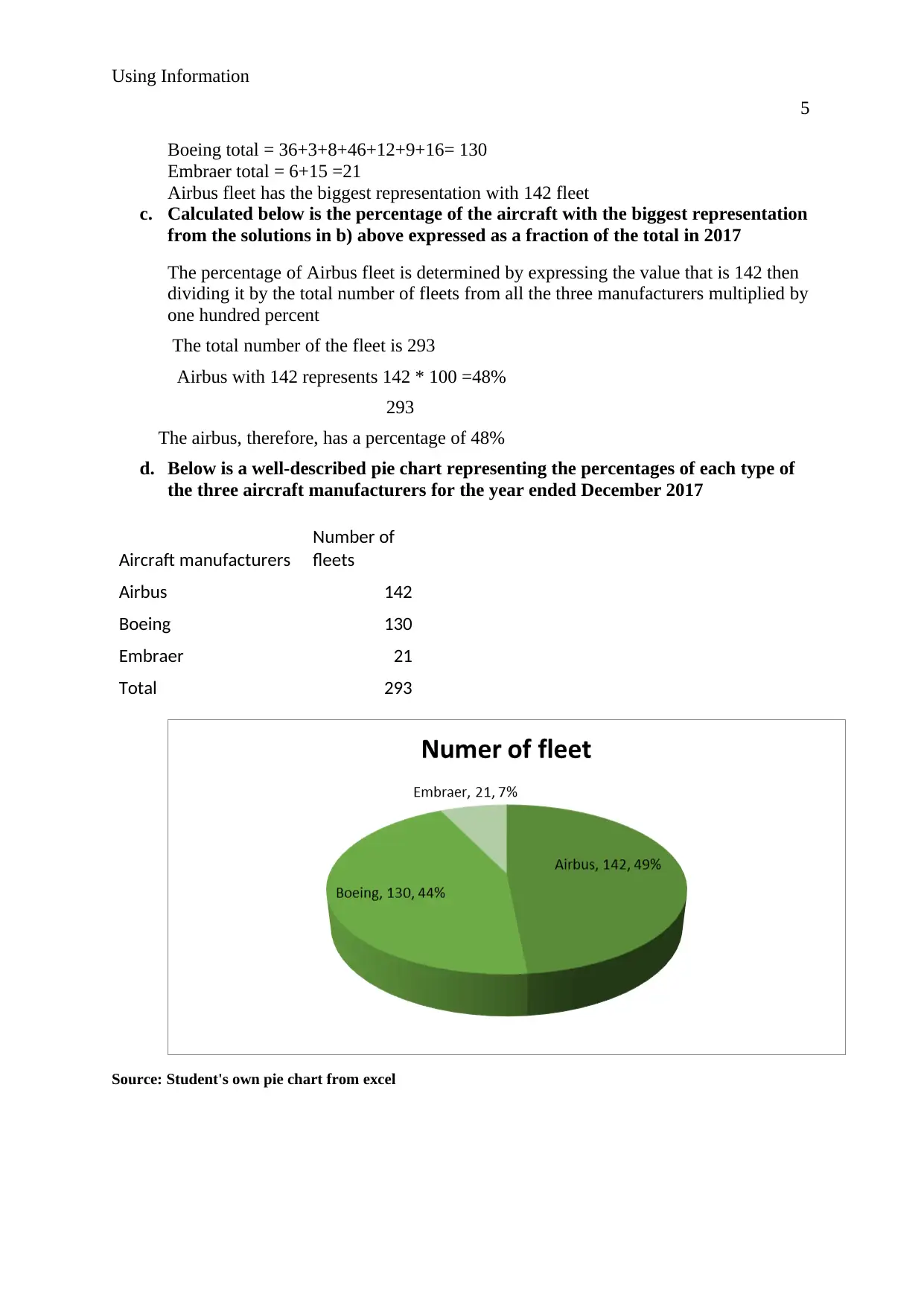

d. Below is a well-described pie chart representing the percentages of each type of

the three aircraft manufacturers for the year ended December 2017

Aircraft manufacturers

Number of

fleets

Airbus 142

Boeing 130

Embraer 21

Total 293

Source: Student's own pie chart from excel

5

Boeing total = 36+3+8+46+12+9+16= 130

Embraer total = 6+15 =21

Airbus fleet has the biggest representation with 142 fleet

c. Calculated below is the percentage of the aircraft with the biggest representation

from the solutions in b) above expressed as a fraction of the total in 2017

The percentage of Airbus fleet is determined by expressing the value that is 142 then

dividing it by the total number of fleets from all the three manufacturers multiplied by

one hundred percent

The total number of the fleet is 293

Airbus with 142 represents 142 * 100 =48%

293

The airbus, therefore, has a percentage of 48%

d. Below is a well-described pie chart representing the percentages of each type of

the three aircraft manufacturers for the year ended December 2017

Aircraft manufacturers

Number of

fleets

Airbus 142

Boeing 130

Embraer 21

Total 293

Source: Student's own pie chart from excel

Using Information

6

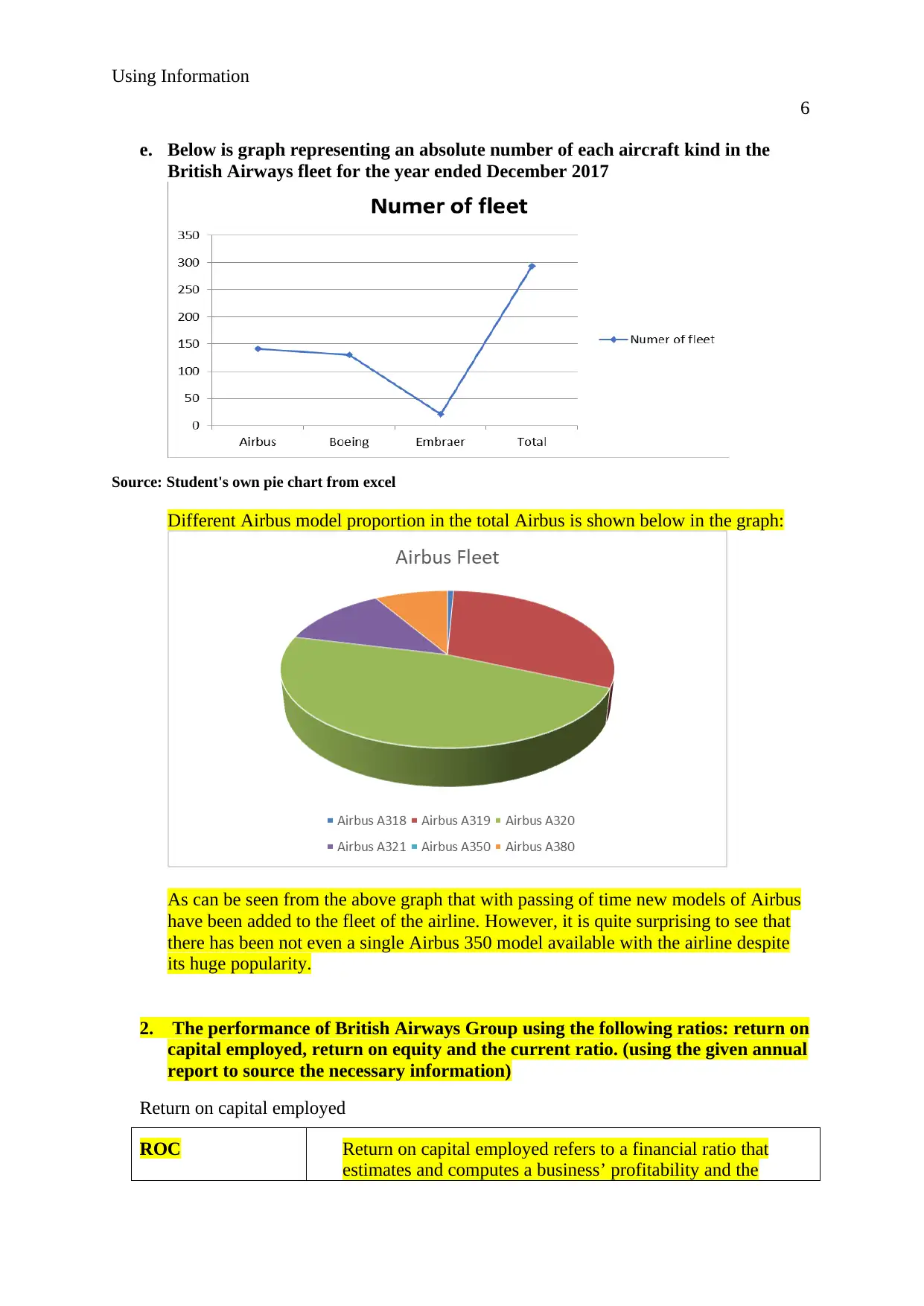

e. Below is graph representing an absolute number of each aircraft kind in the

British Airways fleet for the year ended December 2017

Source: Student's own pie chart from excel

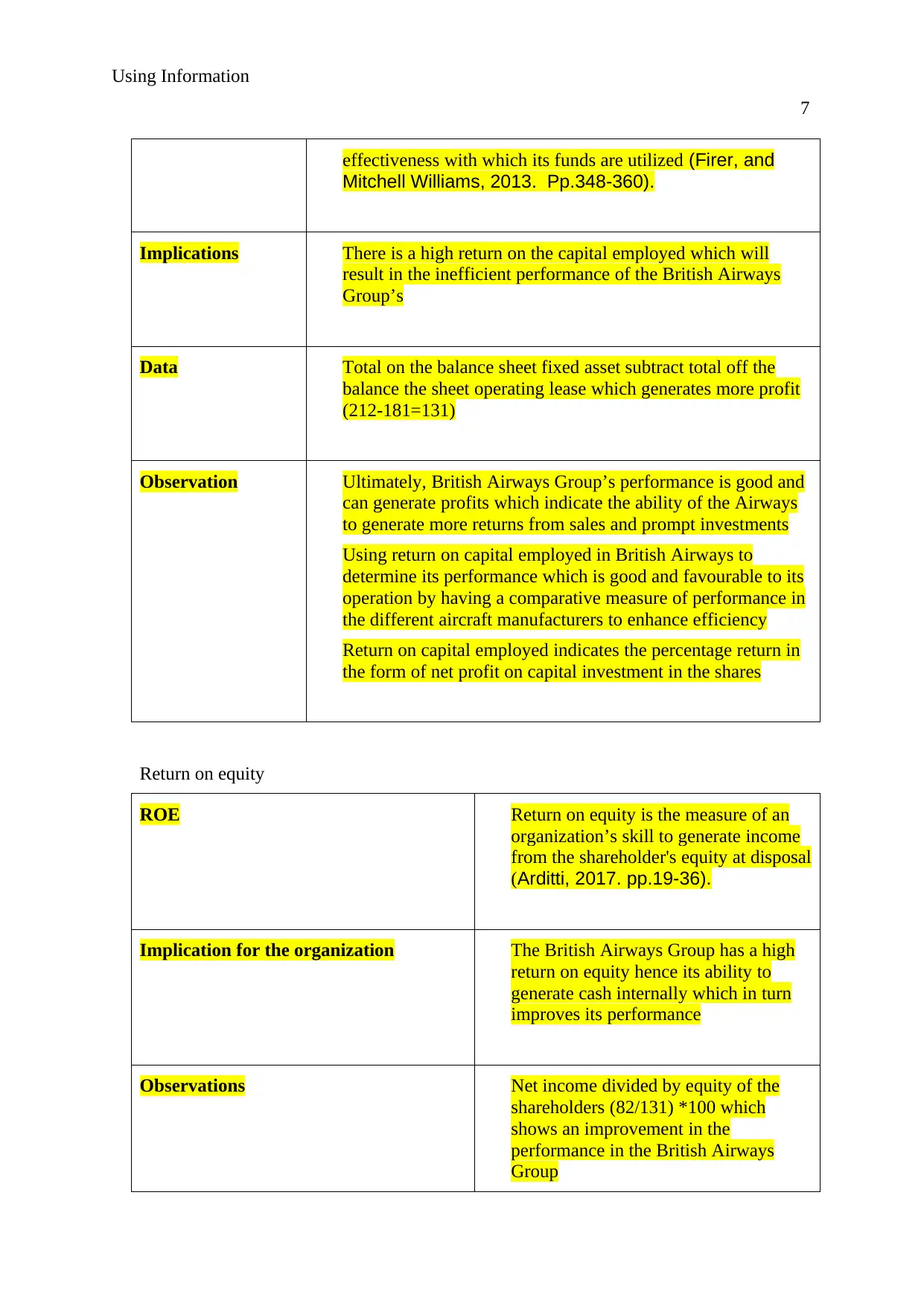

Different Airbus model proportion in the total Airbus is shown below in the graph:

As can be seen from the above graph that with passing of time new models of Airbus

have been added to the fleet of the airline. However, it is quite surprising to see that

there has been not even a single Airbus 350 model available with the airline despite

its huge popularity.

2. The performance of British Airways Group using the following ratios: return on

capital employed, return on equity and the current ratio. (using the given annual

report to source the necessary information)

Return on capital employed

ROC Return on capital employed refers to a financial ratio that

estimates and computes a business’ profitability and the

6

e. Below is graph representing an absolute number of each aircraft kind in the

British Airways fleet for the year ended December 2017

Source: Student's own pie chart from excel

Different Airbus model proportion in the total Airbus is shown below in the graph:

As can be seen from the above graph that with passing of time new models of Airbus

have been added to the fleet of the airline. However, it is quite surprising to see that

there has been not even a single Airbus 350 model available with the airline despite

its huge popularity.

2. The performance of British Airways Group using the following ratios: return on

capital employed, return on equity and the current ratio. (using the given annual

report to source the necessary information)

Return on capital employed

ROC Return on capital employed refers to a financial ratio that

estimates and computes a business’ profitability and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Using Information

7

effectiveness with which its funds are utilized (Firer, and

Mitchell Williams, 2013. Pp.348-360).

Implications There is a high return on the capital employed which will

result in the inefficient performance of the British Airways

Group’s

Data Total on the balance sheet fixed asset subtract total off the

balance the sheet operating lease which generates more profit

(212-181=131)

Observation Ultimately, British Airways Group’s performance is good and

can generate profits which indicate the ability of the Airways

to generate more returns from sales and prompt investments

Using return on capital employed in British Airways to

determine its performance which is good and favourable to its

operation by having a comparative measure of performance in

the different aircraft manufacturers to enhance efficiency

Return on capital employed indicates the percentage return in

the form of net profit on capital investment in the shares

Return on equity

ROE Return on equity is the measure of an

organization’s skill to generate income

from the shareholder's equity at disposal

(Arditti, 2017. pp.19-36).

Implication for the organization The British Airways Group has a high

return on equity hence its ability to

generate cash internally which in turn

improves its performance

Observations Net income divided by equity of the

shareholders (82/131) *100 which

shows an improvement in the

performance in the British Airways

Group

7

effectiveness with which its funds are utilized (Firer, and

Mitchell Williams, 2013. Pp.348-360).

Implications There is a high return on the capital employed which will

result in the inefficient performance of the British Airways

Group’s

Data Total on the balance sheet fixed asset subtract total off the

balance the sheet operating lease which generates more profit

(212-181=131)

Observation Ultimately, British Airways Group’s performance is good and

can generate profits which indicate the ability of the Airways

to generate more returns from sales and prompt investments

Using return on capital employed in British Airways to

determine its performance which is good and favourable to its

operation by having a comparative measure of performance in

the different aircraft manufacturers to enhance efficiency

Return on capital employed indicates the percentage return in

the form of net profit on capital investment in the shares

Return on equity

ROE Return on equity is the measure of an

organization’s skill to generate income

from the shareholder's equity at disposal

(Arditti, 2017. pp.19-36).

Implication for the organization The British Airways Group has a high

return on equity hence its ability to

generate cash internally which in turn

improves its performance

Observations Net income divided by equity of the

shareholders (82/131) *100 which

shows an improvement in the

performance in the British Airways

Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Using Information

8

Return on net worth indicates a

percentage return on the equity or net

worth of shareholders

Current ratios

Current ratio The current ratio of the above-stated

operation refers to the capacity of the

organization to reimburse its lasting

debt Leader (Module, 2014).

Implication for the organization British Airways Company has a current

ratio of one which is (82/81) to mean

the company is just able to cover all its

short-term obligations hence a good

production of the group

Factors of risk which may detrimentally upset British Airways Group’s market position

and revenue referring to the information from the stated annual report and

supplementary applicable material sources

Risk refers to the potential events expected or unexpected to have an adverse effect on the

business’ earnings or capital

The following factors of risk may be adversely disrupted and upset British Airways Group’s

market position and revenue

1) Competitive risk

This entails the potentiality of non-performance that one’s competition will have added

advantages that will prevent the organization from meeting its objectives with regards to the

set targets.

For instance, when the competitors deliver services at an affordable cost or have an improved

quality product

2) Compliance risk

This involves the chance that the organization will fail to adhere to the laws and regulations

resulting in outflow of funds to meet legal fees

This could result in a capital outflow when the organization as a whole or part of the fails to

comply and work under the provided laws and regulations

3) Economical risk

8

Return on net worth indicates a

percentage return on the equity or net

worth of shareholders

Current ratios

Current ratio The current ratio of the above-stated

operation refers to the capacity of the

organization to reimburse its lasting

debt Leader (Module, 2014).

Implication for the organization British Airways Company has a current

ratio of one which is (82/81) to mean

the company is just able to cover all its

short-term obligations hence a good

production of the group

Factors of risk which may detrimentally upset British Airways Group’s market position

and revenue referring to the information from the stated annual report and

supplementary applicable material sources

Risk refers to the potential events expected or unexpected to have an adverse effect on the

business’ earnings or capital

The following factors of risk may be adversely disrupted and upset British Airways Group’s

market position and revenue

1) Competitive risk

This entails the potentiality of non-performance that one’s competition will have added

advantages that will prevent the organization from meeting its objectives with regards to the

set targets.

For instance, when the competitors deliver services at an affordable cost or have an improved

quality product

2) Compliance risk

This involves the chance that the organization will fail to adhere to the laws and regulations

resulting in outflow of funds to meet legal fees

This could result in a capital outflow when the organization as a whole or part of the fails to

comply and work under the provided laws and regulations

3) Economical risk

Using Information

9

This refers to the potential loss resulting from the factors and conditions within the economy

will reduce the sales as a result of its earnings or increase the costs incurred

During adverse economic conditions, the operations of the business may be majorly affected

since the factors affecting the economy would, in turn, affect the business

4) Operational risk

This refers to the potential risk of failure associated with less and inappropriate or failed

internal procedures, labor, systems or outside events connected with the everyday functioning

of the business

The chance of failure to have adequate and proper internal control processes would determine

and have an impact on the efficiency of the organization in terms of its operation

5) Legal risk

This involves the chance of failures resulting from new directives that may shatter the

organization's activities necessitating the organization to suffer capital outflow to levies and

liabilities due to legal discourse

The company should be able to operate in accordance with every legal law and regulations

set to enable effectiveness and efficiency to reduce the chances of legal risk associated with

ignorance

6) Program risk

The chance of failure associated with a given business program or projects

The chance of loss arising from this risk may affect the business adversely which may prompt

the business to develop a program risk management

7) Strategy risk

This refers to the chance of failures associated with several courses of action taken by the

organization

8) Risk of reputation

The possibility of failure associated with the risk of damage to the organization image or

public standing resulting from dubious actions, conventions or events which are discerned as

fraudulent, uncivilized or unskillful

9) Country risk

This is the potential to loss resulting from particular constrains within the economy in which

the business undertakes its workings such as political episodes and occurrence that could

adversely affect its day to day operations

10) Risk of projects

This is the chance of risk associated with investments and from the management of such

projects

It is an unknown event that when occurs has an adverse effect on more than one project.

11) Innovation risk

9

This refers to the potential loss resulting from the factors and conditions within the economy

will reduce the sales as a result of its earnings or increase the costs incurred

During adverse economic conditions, the operations of the business may be majorly affected

since the factors affecting the economy would, in turn, affect the business

4) Operational risk

This refers to the potential risk of failure associated with less and inappropriate or failed

internal procedures, labor, systems or outside events connected with the everyday functioning

of the business

The chance of failure to have adequate and proper internal control processes would determine

and have an impact on the efficiency of the organization in terms of its operation

5) Legal risk

This involves the chance of failures resulting from new directives that may shatter the

organization's activities necessitating the organization to suffer capital outflow to levies and

liabilities due to legal discourse

The company should be able to operate in accordance with every legal law and regulations

set to enable effectiveness and efficiency to reduce the chances of legal risk associated with

ignorance

6) Program risk

The chance of failure associated with a given business program or projects

The chance of loss arising from this risk may affect the business adversely which may prompt

the business to develop a program risk management

7) Strategy risk

This refers to the chance of failures associated with several courses of action taken by the

organization

8) Risk of reputation

The possibility of failure associated with the risk of damage to the organization image or

public standing resulting from dubious actions, conventions or events which are discerned as

fraudulent, uncivilized or unskillful

9) Country risk

This is the potential to loss resulting from particular constrains within the economy in which

the business undertakes its workings such as political episodes and occurrence that could

adversely affect its day to day operations

10) Risk of projects

This is the chance of risk associated with investments and from the management of such

projects

It is an unknown event that when occurs has an adverse effect on more than one project.

11) Innovation risk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Using Information

10

This refers to the possibility of loss that is associated with the innovative sections of the

company that could necessitate the organization to embrace risk management procedures to

fast ahead and relatively control elevated risk operations

12) Exchange rate risk

The potential that inconsistency in the foreign exchange rates could affect the price put on an

organisation’s undertakings and assets. Most universal and international businesses have

greater exposure to a variety of currencies that may contribute to inconsistency in the

financial reports such as operating profit margins

13) Risk on credit

This refers to the possibility of loss resulting from a debtor’s failure to meet his or her

payment obligations in accordance with the agreed term which is mostly associated with

accounts receivable risk

14) Risk of interest rates

This is risk associated with fluctuating interest rates that could distort the organization’s

operation, for example in case, interest rates increase the amount of capital incurred would in

turn rise affecting the company’s profitability

15) Risk of taxation

This is the probability that new tax laws and adjustments will be implemented resulting in

higher tax than expected

The organization should, therefore, be on watch to keep up with the changing tax laws and

interpretations made. This could help mitigate the chance of failure result

16) Resource risk

It is the chance of failure and loss connected to the inability of the business to attain its

objectives and set targets due to lack of resources The business resource include labor which

entails the people working in the organization to enable the organization to meet its

operational needs, resources which are the stock, capital, and assets within the organization

which is used in its day to day operation and finances which are the sources of income to the

organization.

This can result from the organization’s inability to secure important resources, labor and

finances needed for effective and efficient operation.

17) Process risk

This is the potential of failures associated with an intense process. The procedures often aim

at controlling possible failures and losses, as mitigating risks is the fundamental business

procedures yielding reductions and high revenue

It exists when the process that supports the business activity lacks both efficiency and

effectiveness leading to financial loss, customer loss and reputational loss.

18) Seasonal risk

The chance of a business having low revenue associated with a concentration in a single

season production

10

This refers to the possibility of loss that is associated with the innovative sections of the

company that could necessitate the organization to embrace risk management procedures to

fast ahead and relatively control elevated risk operations

12) Exchange rate risk

The potential that inconsistency in the foreign exchange rates could affect the price put on an

organisation’s undertakings and assets. Most universal and international businesses have

greater exposure to a variety of currencies that may contribute to inconsistency in the

financial reports such as operating profit margins

13) Risk on credit

This refers to the possibility of loss resulting from a debtor’s failure to meet his or her

payment obligations in accordance with the agreed term which is mostly associated with

accounts receivable risk

14) Risk of interest rates

This is risk associated with fluctuating interest rates that could distort the organization’s

operation, for example in case, interest rates increase the amount of capital incurred would in

turn rise affecting the company’s profitability

15) Risk of taxation

This is the probability that new tax laws and adjustments will be implemented resulting in

higher tax than expected

The organization should, therefore, be on watch to keep up with the changing tax laws and

interpretations made. This could help mitigate the chance of failure result

16) Resource risk

It is the chance of failure and loss connected to the inability of the business to attain its

objectives and set targets due to lack of resources The business resource include labor which

entails the people working in the organization to enable the organization to meet its

operational needs, resources which are the stock, capital, and assets within the organization

which is used in its day to day operation and finances which are the sources of income to the

organization.

This can result from the organization’s inability to secure important resources, labor and

finances needed for effective and efficient operation.

17) Process risk

This is the potential of failures associated with an intense process. The procedures often aim

at controlling possible failures and losses, as mitigating risks is the fundamental business

procedures yielding reductions and high revenue

It exists when the process that supports the business activity lacks both efficiency and

effectiveness leading to financial loss, customer loss and reputational loss.

18) Seasonal risk

The chance of a business having low revenue associated with a concentration in a single

season production

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Using Information

11

During off-peak, the capital inflow would be greatly reduced as a result of single-season

production by the company

The seasonal risk may prompt the company to come up with risk management and control to

mitigate the adverse effects of seasonal risk

19) Political risk

The chance of failure associated with political events and consequences to delay and affect

the organization operations

During unfavorable political conditions, the operations of the organization in terms of sales

and returns may be majorly affected by cases like violence and riots within the country.

References

Agrawal, A. and Gopal, K., 2013. Principles of Statistics and Reporting of Data.

In Biomonitoring of Water and Wastewater (pp. 93-99). Springer, India.

Arditti, F.D., 2017. Risk and the required return on equity. The Journal of Finance, 22(1),

pp.19-36.

Firer, S. and Mitchell Williams, S., 2013. Intellectual capital and traditional measures of

corporate performance. Journal of intellectual capital, 4(3), pp.348-360.

Jarke, M., Jeusfeld, M.A., Quix, C. and Vassiliadis, P., 2019. Architecture and quality in data

warehouses: An extended repository approach. Information Systems, 24(3), pp.229-253.

Lakada, M.N., Lapian, S.J. and Tumiwa, J.R., 2017. ANALYZING THE FINANCIAL

STATEMENT USING HORIZONTAL–VERTICAL ANALYSIS TO EVALUATING THE

COMPANY FINANCIAL PERFORMANCE PERIOD 2012-2016 (Case Study at PT.

Unilever Indonesia Tbk). Jurnal EMBA: Jurnal Riset Ekonomi, Manajemen, Bisnis dan

Akuntansi, 5(3).

Leader, M.M., Module: Financial Analysis & Management Module Code: MD003404

Module Leader: Dr. D Acquaye Student ID: 1361534 Assignment Submission Date:

24/10/2014.

Lewin, C., 2015. Elementary quantitative methods. Research methods in the social sciences,

pp.215-225.

Miles, M.B., Huberman, A.M., Huberman, M.A., and Huberman, M., 2014. Qualitative data

analysis: An expanded sourcebook. sage.

Rahman, M., 2019. Financial performance analysis was of Janata bank limited.

11

During off-peak, the capital inflow would be greatly reduced as a result of single-season

production by the company

The seasonal risk may prompt the company to come up with risk management and control to

mitigate the adverse effects of seasonal risk

19) Political risk

The chance of failure associated with political events and consequences to delay and affect

the organization operations

During unfavorable political conditions, the operations of the organization in terms of sales

and returns may be majorly affected by cases like violence and riots within the country.

References

Agrawal, A. and Gopal, K., 2013. Principles of Statistics and Reporting of Data.

In Biomonitoring of Water and Wastewater (pp. 93-99). Springer, India.

Arditti, F.D., 2017. Risk and the required return on equity. The Journal of Finance, 22(1),

pp.19-36.

Firer, S. and Mitchell Williams, S., 2013. Intellectual capital and traditional measures of

corporate performance. Journal of intellectual capital, 4(3), pp.348-360.

Jarke, M., Jeusfeld, M.A., Quix, C. and Vassiliadis, P., 2019. Architecture and quality in data

warehouses: An extended repository approach. Information Systems, 24(3), pp.229-253.

Lakada, M.N., Lapian, S.J. and Tumiwa, J.R., 2017. ANALYZING THE FINANCIAL

STATEMENT USING HORIZONTAL–VERTICAL ANALYSIS TO EVALUATING THE

COMPANY FINANCIAL PERFORMANCE PERIOD 2012-2016 (Case Study at PT.

Unilever Indonesia Tbk). Jurnal EMBA: Jurnal Riset Ekonomi, Manajemen, Bisnis dan

Akuntansi, 5(3).

Leader, M.M., Module: Financial Analysis & Management Module Code: MD003404

Module Leader: Dr. D Acquaye Student ID: 1361534 Assignment Submission Date:

24/10/2014.

Lewin, C., 2015. Elementary quantitative methods. Research methods in the social sciences,

pp.215-225.

Miles, M.B., Huberman, A.M., Huberman, M.A., and Huberman, M., 2014. Qualitative data

analysis: An expanded sourcebook. sage.

Rahman, M., 2019. Financial performance analysis was of Janata bank limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.