Investment Product Valuation for Smiths Group Plc: A Detailed Analysis

VerifiedAdded on 2023/01/13

|13

|3251

|44

Report

AI Summary

This report presents a detailed valuation analysis of investment products for Smiths Group Plc. It begins with an overview of the company, including its strengths, weaknesses, opportunities, and threats, analyzed using a SWOT framework. The report then delves into share valuation, employing the Dividend Discount Model, Earnings and Investments Model, P/E Multiple, and Free Cash Flow Model to determine the intrinsic value of the company's shares. A critical discussion compares the results obtained from these various models. The report also assesses bond valuation, calculating the market value of a bond and examining its investment suitability under different interest rate scenarios. Furthermore, the report includes the valuation of options using the Black-Scholes Model, determining the price of call and put options and evaluating the validity of calculations through Put-Call Parity. The analysis concludes with a summary of the total net profit or loss. The report provides a comprehensive understanding of investment analysis techniques and their application in evaluating the financial performance of Smiths Group Plc.

Valuation of Investment

Products

1

Products

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART A: Company Overview.........................................................................................................4

PART B: Share Valuation...............................................................................................................5

1. Dividend Discount Model........................................................................................................5

2. Earnings and Investments Model.............................................................................................6

3. P/E Multiple.............................................................................................................................7

4. Free Cash Flow Model.............................................................................................................7

5. Critical discussion of the results..............................................................................................8

PART C: Bond Valuation................................................................................................................8

1. Market value of the bond as of 4 February 2020.....................................................................8

2. Investment suitability...............................................................................................................9

3. Calculation of modified duration...........................................................................................10

4. Concept of modified duration................................................................................................10

PART D: Valuation of Options.....................................................................................................11

1. Price of a 3-month European call option...............................................................................11

2. Price of a put option with similar characteristics as the call option......................................11

3. Validity of calculations using Put call parity.........................................................................11

4. Total net profit or loss............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

PART A: Company Overview.........................................................................................................4

PART B: Share Valuation...............................................................................................................5

1. Dividend Discount Model........................................................................................................5

2. Earnings and Investments Model.............................................................................................6

3. P/E Multiple.............................................................................................................................7

4. Free Cash Flow Model.............................................................................................................7

5. Critical discussion of the results..............................................................................................8

PART C: Bond Valuation................................................................................................................8

1. Market value of the bond as of 4 February 2020.....................................................................8

2. Investment suitability...............................................................................................................9

3. Calculation of modified duration...........................................................................................10

4. Concept of modified duration................................................................................................10

PART D: Valuation of Options.....................................................................................................11

1. Price of a 3-month European call option...............................................................................11

2. Price of a put option with similar characteristics as the call option......................................11

3. Validity of calculations using Put call parity.........................................................................11

4. Total net profit or loss............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION

Investment products the stocks which are offered to investors by listed organisations. These

products are required to be effectively valued so that an informed investment decision can be

taken (Bauer and Smeets, 2015). The main aim of this report is to build an understanding about

the concept of investment analysis and enhance the skills of using various investment techniques

such as share and bond valuation. For this purpose, a large scale listed company is selected

which is Smiths Group Plc. This is an engineering company having headquarters in London,

United Kingdom. This organisation was founded in 1851 by Samuel Smith. The operations of

this company includes few principle divisions which are medical systems, defence and

Aerospace.

This report is divided in four parts; the first part will focus upon overview of the selected

company including its strengths, weaknesses, opportunities and challenges. The second part of

this report is related to share valuation in which selected company’s intrinsic value of share will

be computed using various techniques. In the third section of the report, value of the bond of

3

Investment products the stocks which are offered to investors by listed organisations. These

products are required to be effectively valued so that an informed investment decision can be

taken (Bauer and Smeets, 2015). The main aim of this report is to build an understanding about

the concept of investment analysis and enhance the skills of using various investment techniques

such as share and bond valuation. For this purpose, a large scale listed company is selected

which is Smiths Group Plc. This is an engineering company having headquarters in London,

United Kingdom. This organisation was founded in 1851 by Samuel Smith. The operations of

this company includes few principle divisions which are medical systems, defence and

Aerospace.

This report is divided in four parts; the first part will focus upon overview of the selected

company including its strengths, weaknesses, opportunities and challenges. The second part of

this report is related to share valuation in which selected company’s intrinsic value of share will

be computed using various techniques. In the third section of the report, value of the bond of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

selected company will be estimated using varied interest rate scenarios. In the last section,

options of the company will be valued using Black-Scholes Model.

PART A: Company Overview

Smith Group Plc. is a public limited company listed at London Stock Exchange and is a part

of FTSE 100 component. This company deals in engineering industry and has competitive image

in market. Being a 169 years old organisation, the brand image of this organisation is quite

influential. Like every other company, this company also faces challenges due to dynamic

market environment. In order to analyse the internal and external environment of this company a

framework named SWOT is used below by which strengths, weaknesses, opportunities and

threats (challenges) of this company are analysed:

Strengths

Strengths are the internal resources and competencies of an organisation which must be

enhanced through effective operations (Bernstrom, 2014). Smith Group Plc has a strong

distribution network which easily reaches their potential market is an essential strength of this

company. Other strengths of this company includes high level of customer satisfaction, strong

brand portfolio and high returns on Capital Expenditure. For the purpose of investment analysis,

it must be noted that this company is effective when it comes to gaining high returns of their

expenditures which can be beneficial for potential investors.

Weaknesses

This company has comparatively low research and development skills which is a major

weakness of this company that must be resolved by investing in R&D department. Another

weakness of this company is the non-effective financial planning due to which liquidity of this

company gets impacted. This weakness must be considered by its potential investors as they can

face the issue of low liquidity if they invest in this company’s stocks.

Opportunities

There are various opportunities which can be grabbed by Smiths Group Plc. The industry in

which this company deals is a growing industry which can provide the future opportunity of

capturing new customers. This company can also enhance their online platform from which they

can reach larger market segments, this opportunity will need investment in big data analytics.

Decreasing transportation cost is also an opportunity for this company which can be grabbed by

operating in markets which has lower shipping prices (Enever, Isaac and Daley, 2014).

4

options of the company will be valued using Black-Scholes Model.

PART A: Company Overview

Smith Group Plc. is a public limited company listed at London Stock Exchange and is a part

of FTSE 100 component. This company deals in engineering industry and has competitive image

in market. Being a 169 years old organisation, the brand image of this organisation is quite

influential. Like every other company, this company also faces challenges due to dynamic

market environment. In order to analyse the internal and external environment of this company a

framework named SWOT is used below by which strengths, weaknesses, opportunities and

threats (challenges) of this company are analysed:

Strengths

Strengths are the internal resources and competencies of an organisation which must be

enhanced through effective operations (Bernstrom, 2014). Smith Group Plc has a strong

distribution network which easily reaches their potential market is an essential strength of this

company. Other strengths of this company includes high level of customer satisfaction, strong

brand portfolio and high returns on Capital Expenditure. For the purpose of investment analysis,

it must be noted that this company is effective when it comes to gaining high returns of their

expenditures which can be beneficial for potential investors.

Weaknesses

This company has comparatively low research and development skills which is a major

weakness of this company that must be resolved by investing in R&D department. Another

weakness of this company is the non-effective financial planning due to which liquidity of this

company gets impacted. This weakness must be considered by its potential investors as they can

face the issue of low liquidity if they invest in this company’s stocks.

Opportunities

There are various opportunities which can be grabbed by Smiths Group Plc. The industry in

which this company deals is a growing industry which can provide the future opportunity of

capturing new customers. This company can also enhance their online platform from which they

can reach larger market segments, this opportunity will need investment in big data analytics.

Decreasing transportation cost is also an opportunity for this company which can be grabbed by

operating in markets which has lower shipping prices (Enever, Isaac and Daley, 2014).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Threats (Challenges)

Threats and challenges are the situations which company has to face while operating in a

marketplace. These challenges can affect the productivity and profitability of an organisation.

Smith Group Plc. is operating in various markets and facing various challenges. The most

influencing challenge for this company is high prices of raw material due to which margin

market of this company will be negatively impacted. Other threats or challenges of this company

which they may face in future are shortage of skilled employees, intense competition and threats

of new entrants in the industry.

Smith Group Plc.’s position in industry

Smith Group Plc. is considered as one of the best organisation working in engineering

industry and is a largest provider of security and defence industry. This company holds a strong

and competitive position in market. This company faces the threat of new entrant in this industry

as continuously innovating new products requires high capital due to which Smith Group Plc.

lacks in providing new value proposition to their customers.

The engineering industry is a vast marketplace and includes various sectors. The most

important element in such sectors is the raw material which are procured from the suppliers. Due

to the dominant position of suppliers in this industry, Smith Group faces the high bargaining

power issue from which their margins can also be impacted. But on the other hand, when it

comes to the customers, Smith Group Plc. enjoys competitive position in market due to which

they can limit the bargain power of their clients.

The products developed by this company are highly innovative but they are imitable and not

rare due to which these products can easily be substituted (Kahn and Lemmon, 2016). This factor

implies the submissive position of this company in industry. Smith Group Plc. is operating in an

industry where competition is common but then also this group has proven to be the best due to

their low margins are competency to create innovative position.

PART B: Share Valuation

1. Dividend Discount Model

This model is a quantitative method of calculating and forecasting the intrinsic value of a

share of a company. The intrinsic value is the price of a share which is completely non effected

by the external environment. This value is based on only the internal affairs, capabilities and

5

Threats and challenges are the situations which company has to face while operating in a

marketplace. These challenges can affect the productivity and profitability of an organisation.

Smith Group Plc. is operating in various markets and facing various challenges. The most

influencing challenge for this company is high prices of raw material due to which margin

market of this company will be negatively impacted. Other threats or challenges of this company

which they may face in future are shortage of skilled employees, intense competition and threats

of new entrants in the industry.

Smith Group Plc.’s position in industry

Smith Group Plc. is considered as one of the best organisation working in engineering

industry and is a largest provider of security and defence industry. This company holds a strong

and competitive position in market. This company faces the threat of new entrant in this industry

as continuously innovating new products requires high capital due to which Smith Group Plc.

lacks in providing new value proposition to their customers.

The engineering industry is a vast marketplace and includes various sectors. The most

important element in such sectors is the raw material which are procured from the suppliers. Due

to the dominant position of suppliers in this industry, Smith Group faces the high bargaining

power issue from which their margins can also be impacted. But on the other hand, when it

comes to the customers, Smith Group Plc. enjoys competitive position in market due to which

they can limit the bargain power of their clients.

The products developed by this company are highly innovative but they are imitable and not

rare due to which these products can easily be substituted (Kahn and Lemmon, 2016). This factor

implies the submissive position of this company in industry. Smith Group Plc. is operating in an

industry where competition is common but then also this group has proven to be the best due to

their low margins are competency to create innovative position.

PART B: Share Valuation

1. Dividend Discount Model

This model is a quantitative method of calculating and forecasting the intrinsic value of a

share of a company. The intrinsic value is the price of a share which is completely non effected

by the external environment. This value is based on only the internal affairs, capabilities and

5

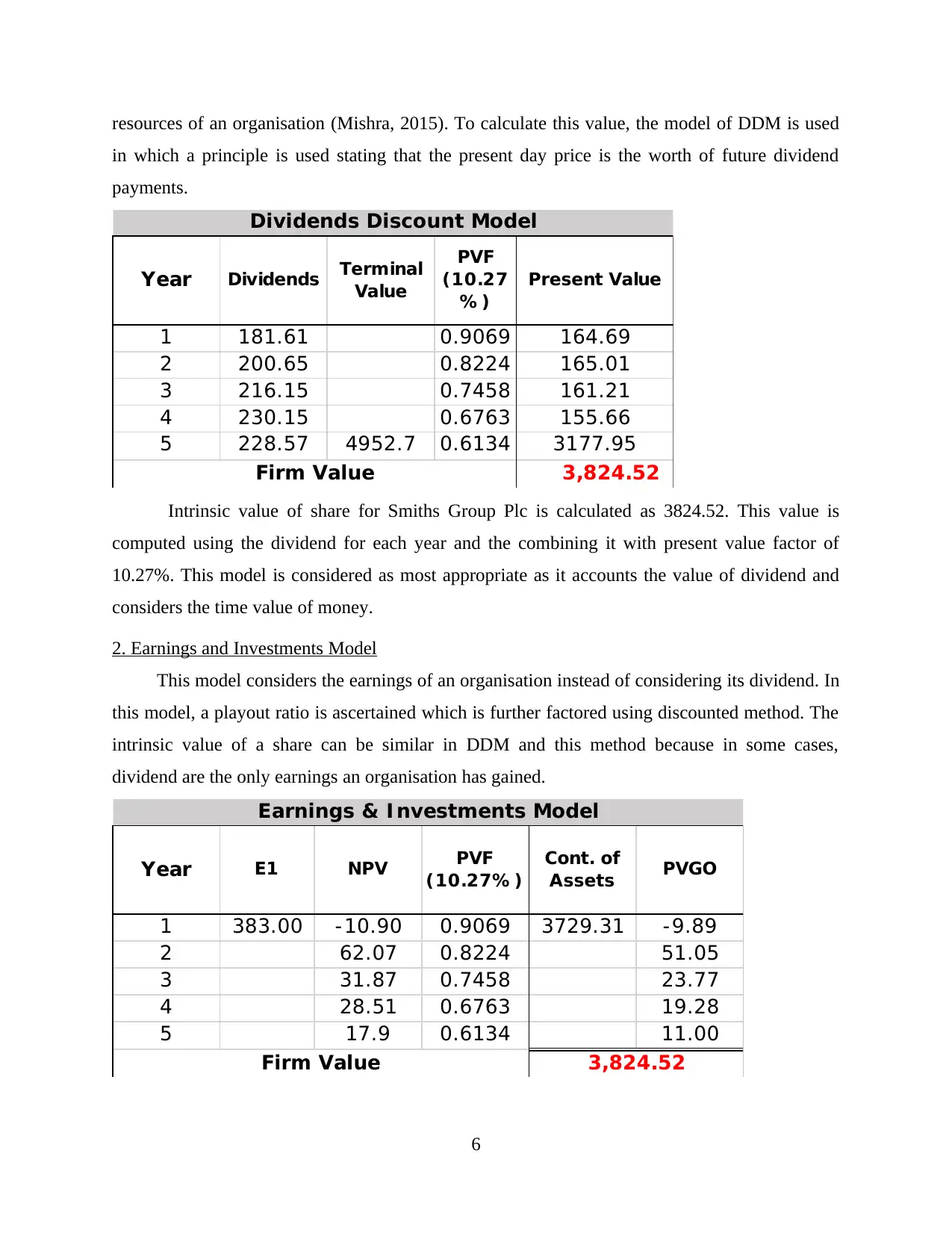

resources of an organisation (Mishra, 2015). To calculate this value, the model of DDM is used

in which a principle is used stating that the present day price is the worth of future dividend

payments.

Year Dividends Terminal

Value

PVF

(10.27

% )

Present Value

1 181.61 0.9069 164.69

2 200.65 0.8224 165.01

3 216.15 0.7458 161.21

4 230.15 0.6763 155.66

5 228.57 4952.7 0.6134 3177.95

3,824.52Firm Value

Dividends Discount Model

Intrinsic value of share for Smiths Group Plc is calculated as 3824.52. This value is

computed using the dividend for each year and the combining it with present value factor of

10.27%. This model is considered as most appropriate as it accounts the value of dividend and

considers the time value of money.

2. Earnings and Investments Model

This model considers the earnings of an organisation instead of considering its dividend. In

this model, a playout ratio is ascertained which is further factored using discounted method. The

intrinsic value of a share can be similar in DDM and this method because in some cases,

dividend are the only earnings an organisation has gained.

Year E1 NPV PVF

(10.27% )

Cont. of

Assets PVGO

1 383.00 - 10.90 0.9069 3729.31 - 9.89

2 62.07 0.8224 51.05

3 31.87 0.7458 23.77

4 28.51 0.6763 19.28

5 17.9 0.6134 11.00

Firm Value 3,824.52

Earnings & I nvestments Model

6

in which a principle is used stating that the present day price is the worth of future dividend

payments.

Year Dividends Terminal

Value

PVF

(10.27

% )

Present Value

1 181.61 0.9069 164.69

2 200.65 0.8224 165.01

3 216.15 0.7458 161.21

4 230.15 0.6763 155.66

5 228.57 4952.7 0.6134 3177.95

3,824.52Firm Value

Dividends Discount Model

Intrinsic value of share for Smiths Group Plc is calculated as 3824.52. This value is

computed using the dividend for each year and the combining it with present value factor of

10.27%. This model is considered as most appropriate as it accounts the value of dividend and

considers the time value of money.

2. Earnings and Investments Model

This model considers the earnings of an organisation instead of considering its dividend. In

this model, a playout ratio is ascertained which is further factored using discounted method. The

intrinsic value of a share can be similar in DDM and this method because in some cases,

dividend are the only earnings an organisation has gained.

Year E1 NPV PVF

(10.27% )

Cont. of

Assets PVGO

1 383.00 - 10.90 0.9069 3729.31 - 9.89

2 62.07 0.8224 51.05

3 31.87 0.7458 23.77

4 28.51 0.6763 19.28

5 17.9 0.6134 11.00

Firm Value 3,824.52

Earnings & I nvestments Model

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It can be seen that the intrinsic value of share using EIM method is 3824.52 which is

similar with DDM model as Smith Group Plc is distributing all their earnings to their

shareholders as dividend.

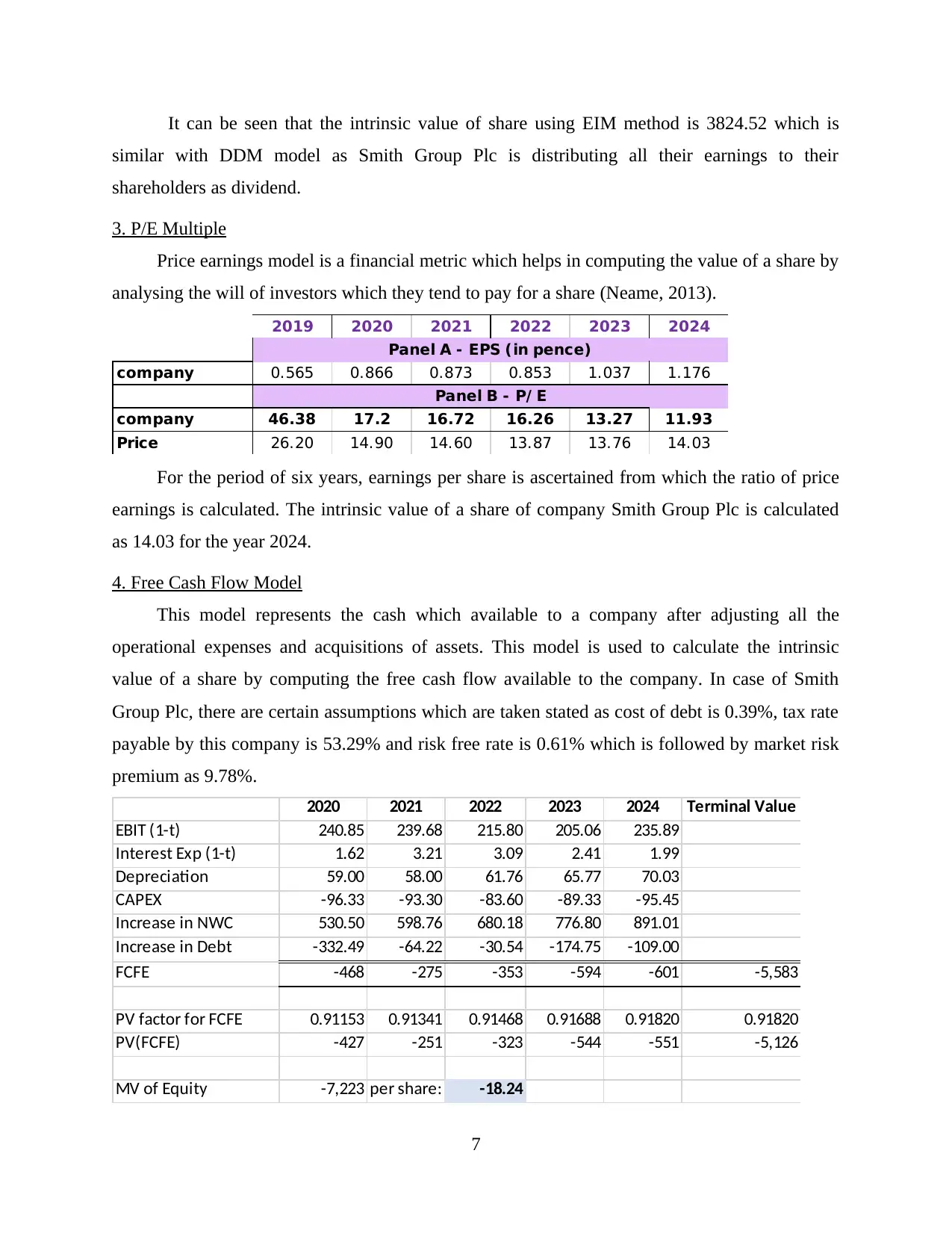

3. P/E Multiple

Price earnings model is a financial metric which helps in computing the value of a share by

analysing the will of investors which they tend to pay for a share (Neame, 2013).

2019 2020 2021 2022 2023 2024

company 0.565 0.866 0.873 0.853 1.037 1.176

company 46.38 17.2 16.72 16.26 13.27 11.93

Price 26.20 14.90 14.60 13.87 13.76 14.03

Panel A - EPS (in pence)

Panel B - P/ E

For the period of six years, earnings per share is ascertained from which the ratio of price

earnings is calculated. The intrinsic value of a share of company Smith Group Plc is calculated

as 14.03 for the year 2024.

4. Free Cash Flow Model

This model represents the cash which available to a company after adjusting all the

operational expenses and acquisitions of assets. This model is used to calculate the intrinsic

value of a share by computing the free cash flow available to the company. In case of Smith

Group Plc, there are certain assumptions which are taken stated as cost of debt is 0.39%, tax rate

payable by this company is 53.29% and risk free rate is 0.61% which is followed by market risk

premium as 9.78%.

2020 2021 2022 2023 2024 Terminal Value

EBIT (1-t) 240.85 239.68 215.80 205.06 235.89

Interest Exp (1-t) 1.62 3.21 3.09 2.41 1.99

Depreciation 59.00 58.00 61.76 65.77 70.03

CAPEX -96.33 -93.30 -83.60 -89.33 -95.45

Increase in NWC 530.50 598.76 680.18 776.80 891.01

Increase in Debt -332.49 -64.22 -30.54 -174.75 -109.00

FCFE -468 -275 -353 -594 -601 -5,583

PV factor for FCFE 0.91153 0.91341 0.91468 0.91688 0.91820 0.91820

PV(FCFE) -427 -251 -323 -544 -551 -5,126

MV of Equity -7,223 per share: -18.24

7

similar with DDM model as Smith Group Plc is distributing all their earnings to their

shareholders as dividend.

3. P/E Multiple

Price earnings model is a financial metric which helps in computing the value of a share by

analysing the will of investors which they tend to pay for a share (Neame, 2013).

2019 2020 2021 2022 2023 2024

company 0.565 0.866 0.873 0.853 1.037 1.176

company 46.38 17.2 16.72 16.26 13.27 11.93

Price 26.20 14.90 14.60 13.87 13.76 14.03

Panel A - EPS (in pence)

Panel B - P/ E

For the period of six years, earnings per share is ascertained from which the ratio of price

earnings is calculated. The intrinsic value of a share of company Smith Group Plc is calculated

as 14.03 for the year 2024.

4. Free Cash Flow Model

This model represents the cash which available to a company after adjusting all the

operational expenses and acquisitions of assets. This model is used to calculate the intrinsic

value of a share by computing the free cash flow available to the company. In case of Smith

Group Plc, there are certain assumptions which are taken stated as cost of debt is 0.39%, tax rate

payable by this company is 53.29% and risk free rate is 0.61% which is followed by market risk

premium as 9.78%.

2020 2021 2022 2023 2024 Terminal Value

EBIT (1-t) 240.85 239.68 215.80 205.06 235.89

Interest Exp (1-t) 1.62 3.21 3.09 2.41 1.99

Depreciation 59.00 58.00 61.76 65.77 70.03

CAPEX -96.33 -93.30 -83.60 -89.33 -95.45

Increase in NWC 530.50 598.76 680.18 776.80 891.01

Increase in Debt -332.49 -64.22 -30.54 -174.75 -109.00

FCFE -468 -275 -353 -594 -601 -5,583

PV factor for FCFE 0.91153 0.91341 0.91468 0.91688 0.91820 0.91820

PV(FCFE) -427 -251 -323 -544 -551 -5,126

MV of Equity -7,223 per share: -18.24

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above numerical analysis, it can be seen that intrinsic value per share is

calculated as -18.24. This value is presenting a negative amount which is the result of non

availability of free cash flow for Smith Group Plc.

5. Critical discussion of the results

Intrinsic value is the measure of calculating worth of a share of an organisation. There are

various models by which intrinsic value can be calculated. In context of Smith Group Plc,

various models are used (Snowball 2013). The intrinsic value using the dividend discount model

and Earnings and Investments Model is similar as dividend are the only earnings which Smith

Group Plc is gaining. The reason behind deviation in the intrinsic value computed from different

models is the different assumptions which are made. In DDM model, it is assumed that both

dividend growth rate and return on equity will be constant forever. On the other hand, free cash

flow assumes that there always will be tax rate and risk free rate.

From the implementation of various models, it has been found that potential investors of

Smith Group Plc. should use dividend discount model while computing share price of this

company. The reason behind this recommendation is that DDM is most suitable model for

companies which regularly provide dividend to their shareholders.

PART C: Bond Valuation

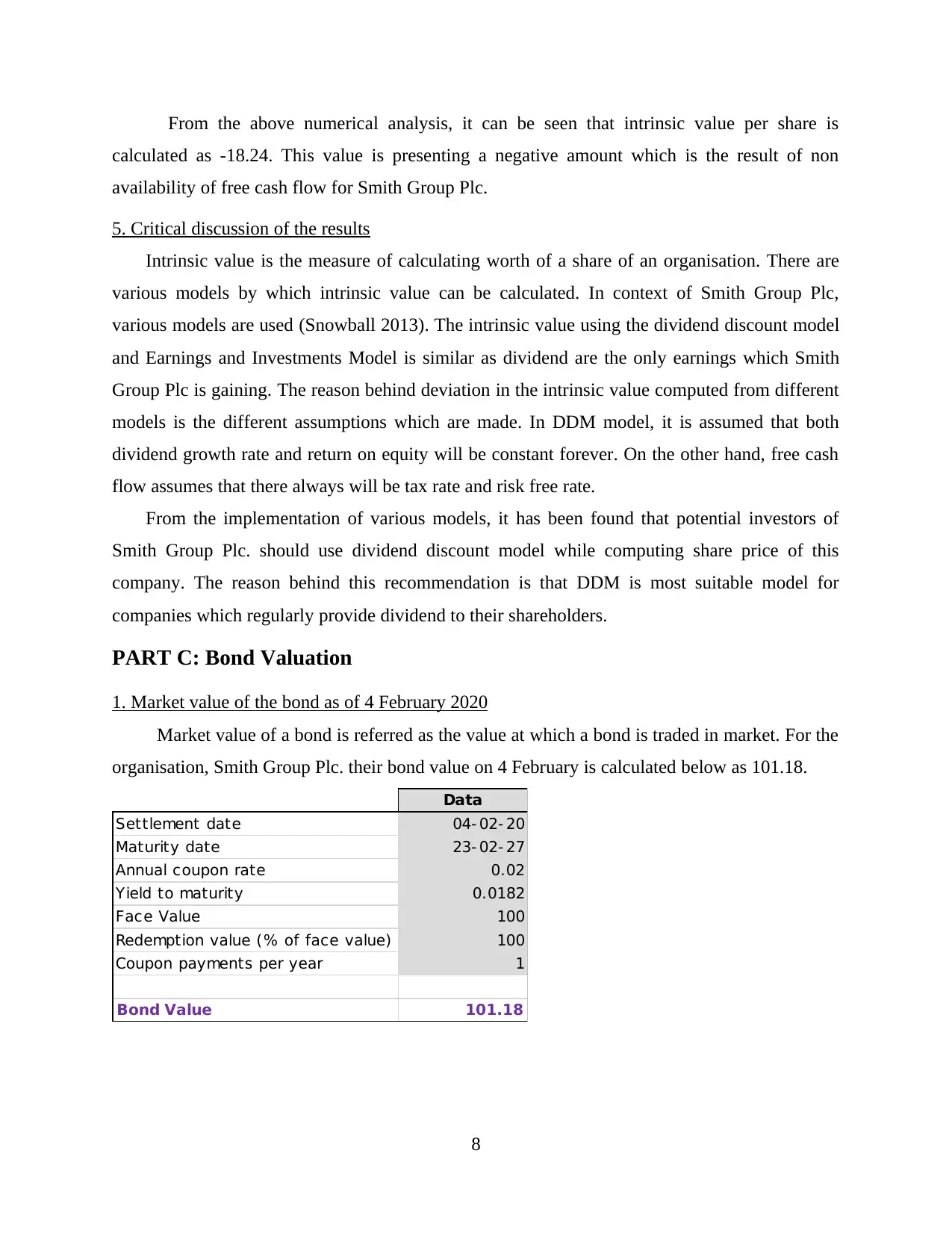

1. Market value of the bond as of 4 February 2020

Market value of a bond is referred as the value at which a bond is traded in market. For the

organisation, Smith Group Plc. their bond value on 4 February is calculated below as 101.18.

Data

Settlement date 04- 02- 20

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0182

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.18

8

calculated as -18.24. This value is presenting a negative amount which is the result of non

availability of free cash flow for Smith Group Plc.

5. Critical discussion of the results

Intrinsic value is the measure of calculating worth of a share of an organisation. There are

various models by which intrinsic value can be calculated. In context of Smith Group Plc,

various models are used (Snowball 2013). The intrinsic value using the dividend discount model

and Earnings and Investments Model is similar as dividend are the only earnings which Smith

Group Plc is gaining. The reason behind deviation in the intrinsic value computed from different

models is the different assumptions which are made. In DDM model, it is assumed that both

dividend growth rate and return on equity will be constant forever. On the other hand, free cash

flow assumes that there always will be tax rate and risk free rate.

From the implementation of various models, it has been found that potential investors of

Smith Group Plc. should use dividend discount model while computing share price of this

company. The reason behind this recommendation is that DDM is most suitable model for

companies which regularly provide dividend to their shareholders.

PART C: Bond Valuation

1. Market value of the bond as of 4 February 2020

Market value of a bond is referred as the value at which a bond is traded in market. For the

organisation, Smith Group Plc. their bond value on 4 February is calculated below as 101.18.

Data

Settlement date 04- 02- 20

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0182

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.18

8

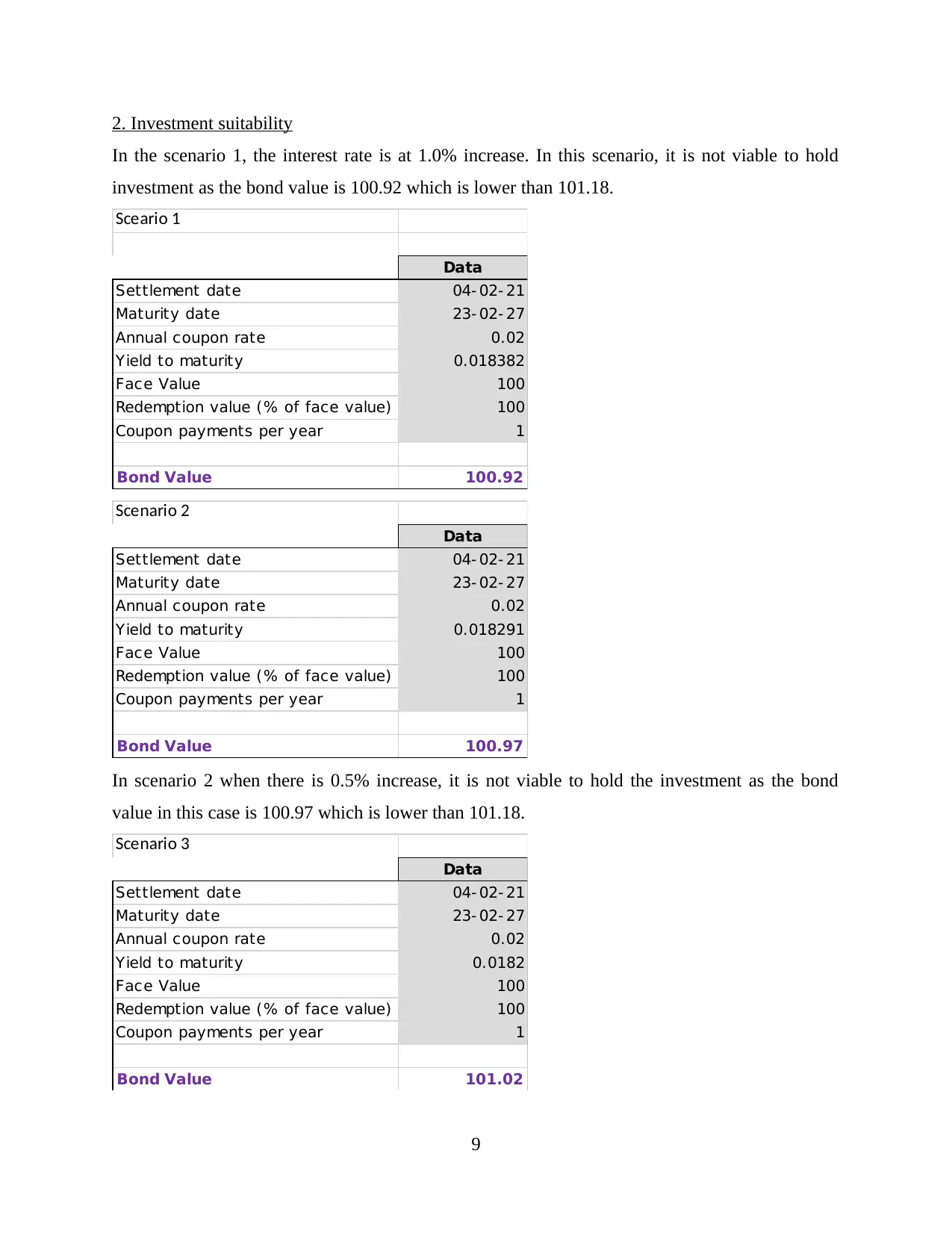

2. Investment suitability

In the scenario 1, the interest rate is at 1.0% increase. In this scenario, it is not viable to hold

investment as the bond value is 100.92 which is lower than 101.18.

Sceario 1

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.018382

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 100.92

Scenario 2

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.018291

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 100.97

In scenario 2 when there is 0.5% increase, it is not viable to hold the investment as the bond

value in this case is 100.97 which is lower than 101.18.

Scenario 3

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0182

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.02

9

In the scenario 1, the interest rate is at 1.0% increase. In this scenario, it is not viable to hold

investment as the bond value is 100.92 which is lower than 101.18.

Sceario 1

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.018382

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 100.92

Scenario 2

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.018291

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 100.97

In scenario 2 when there is 0.5% increase, it is not viable to hold the investment as the bond

value in this case is 100.97 which is lower than 101.18.

Scenario 3

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0182

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.02

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

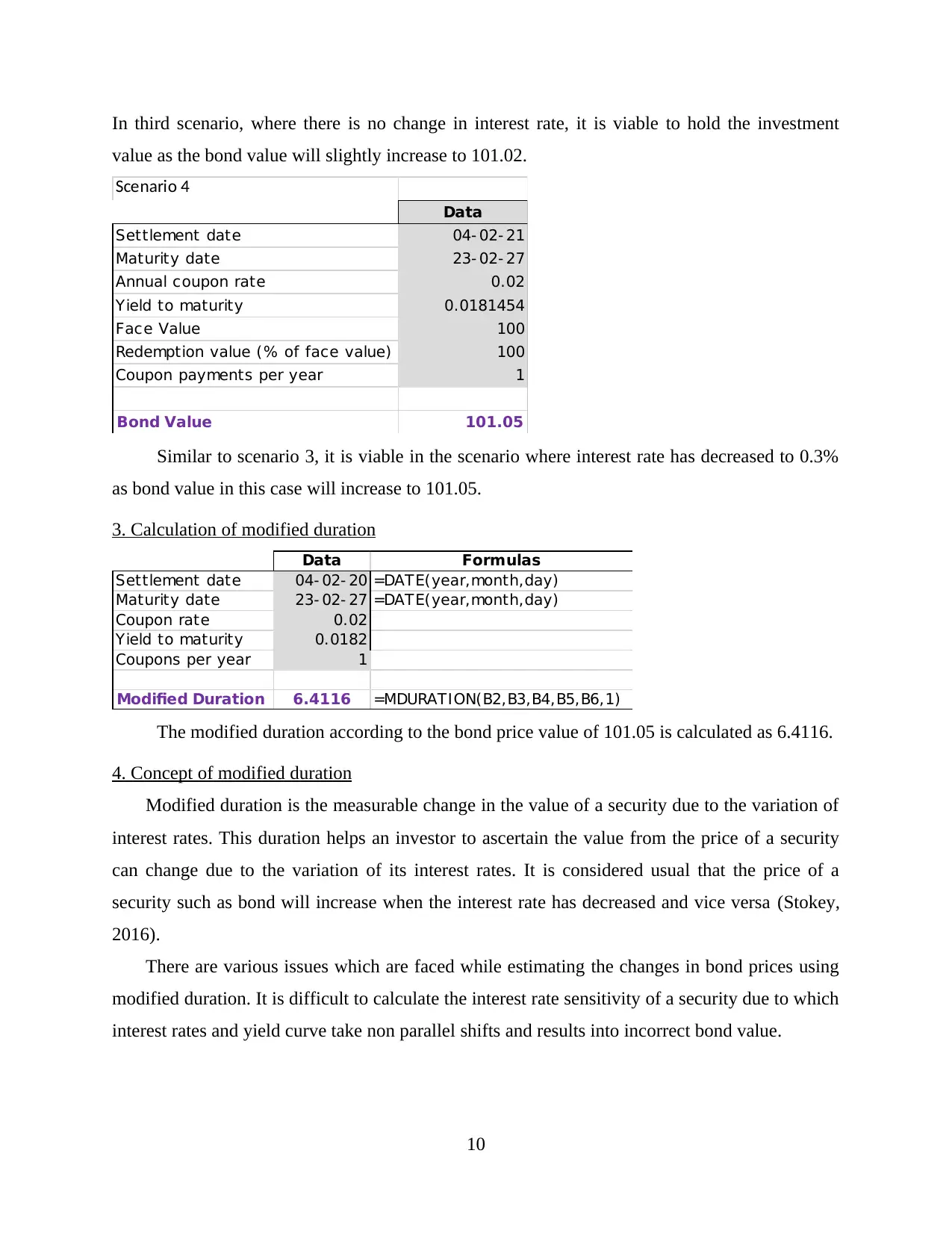

In third scenario, where there is no change in interest rate, it is viable to hold the investment

value as the bond value will slightly increase to 101.02.

Scenario 4

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0181454

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.05

Similar to scenario 3, it is viable in the scenario where interest rate has decreased to 0.3%

as bond value in this case will increase to 101.05.

3. Calculation of modified duration

Data Formulas

Settlement date 04- 02- 20 =DATE(year,month,day)

Maturity date 23- 02- 27 =DATE(year,month,day)

Coupon rate 0.02

Yield to maturity 0.0182

Coupons per year 1

Modified Duration 6.4116 =MDURATION(B2,B3,B4,B5,B6,1)

The modified duration according to the bond price value of 101.05 is calculated as 6.4116.

4. Concept of modified duration

Modified duration is the measurable change in the value of a security due to the variation of

interest rates. This duration helps an investor to ascertain the value from the price of a security

can change due to the variation of its interest rates. It is considered usual that the price of a

security such as bond will increase when the interest rate has decreased and vice versa (Stokey,

2016).

There are various issues which are faced while estimating the changes in bond prices using

modified duration. It is difficult to calculate the interest rate sensitivity of a security due to which

interest rates and yield curve take non parallel shifts and results into incorrect bond value.

10

value as the bond value will slightly increase to 101.02.

Scenario 4

Data

Settlement date 04- 02- 21

Maturity date 23- 02- 27

Annual coupon rate 0.02

Yield to maturity 0.0181454

Face Value 100

Redemption value (% of face value) 100

Coupon payments per year 1

Bond Value 101.05

Similar to scenario 3, it is viable in the scenario where interest rate has decreased to 0.3%

as bond value in this case will increase to 101.05.

3. Calculation of modified duration

Data Formulas

Settlement date 04- 02- 20 =DATE(year,month,day)

Maturity date 23- 02- 27 =DATE(year,month,day)

Coupon rate 0.02

Yield to maturity 0.0182

Coupons per year 1

Modified Duration 6.4116 =MDURATION(B2,B3,B4,B5,B6,1)

The modified duration according to the bond price value of 101.05 is calculated as 6.4116.

4. Concept of modified duration

Modified duration is the measurable change in the value of a security due to the variation of

interest rates. This duration helps an investor to ascertain the value from the price of a security

can change due to the variation of its interest rates. It is considered usual that the price of a

security such as bond will increase when the interest rate has decreased and vice versa (Stokey,

2016).

There are various issues which are faced while estimating the changes in bond prices using

modified duration. It is difficult to calculate the interest rate sensitivity of a security due to which

interest rates and yield curve take non parallel shifts and results into incorrect bond value.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART D: Valuation of Options

1. Price of a 3-month European call option

Standard Deviation (annual) 0.2063 d1 - 0.5911

Maturity (in years) 0.25 d2 - 0.6942

Risk- Free Rate (annual) 0.0061 N(d1) 0.2772

Stock Price 1,714.0 N(d2) 0.2438

Exercise Price 1,834.3 CALL PRICE 28.72

Options Pricing

Data Formulas

2. Price of a put option with similar characteristics as the call option

Standard Deviation (annual) 0.2063 d1 - 0.5911

Maturity (in years) 0.25 d2 - 0.6942

Risk- Free Rate (annual) 0.0061 N(d1) 0.2772

Stock Price 1,714.0 N(d2) 0.2438

Exercise Price 1,834.3 CALL PRICE 28.72

PUT PRICE 146.17

Options Pricing

Data Formulas

3. Validity of calculations using Put call parity

Put-Call Parity

Call (Call Price+PV(Exercise Price) 1860.14

Put (Put Price+Stock Price) 1,860.17

Assumptions in calculation of Put and Call option:

Purchase date 11-05-19

Current price 1714

Exercise price 1834.25

Maturity 02-04-20

Risk free rate 0.610%

Standard deviation 0.2063

Assumtion

11

1. Price of a 3-month European call option

Standard Deviation (annual) 0.2063 d1 - 0.5911

Maturity (in years) 0.25 d2 - 0.6942

Risk- Free Rate (annual) 0.0061 N(d1) 0.2772

Stock Price 1,714.0 N(d2) 0.2438

Exercise Price 1,834.3 CALL PRICE 28.72

Options Pricing

Data Formulas

2. Price of a put option with similar characteristics as the call option

Standard Deviation (annual) 0.2063 d1 - 0.5911

Maturity (in years) 0.25 d2 - 0.6942

Risk- Free Rate (annual) 0.0061 N(d1) 0.2772

Stock Price 1,714.0 N(d2) 0.2438

Exercise Price 1,834.3 CALL PRICE 28.72

PUT PRICE 146.17

Options Pricing

Data Formulas

3. Validity of calculations using Put call parity

Put-Call Parity

Call (Call Price+PV(Exercise Price) 1860.14

Put (Put Price+Stock Price) 1,860.17

Assumptions in calculation of Put and Call option:

Purchase date 11-05-19

Current price 1714

Exercise price 1834.25

Maturity 02-04-20

Risk free rate 0.610%

Standard deviation 0.2063

Assumtion

11

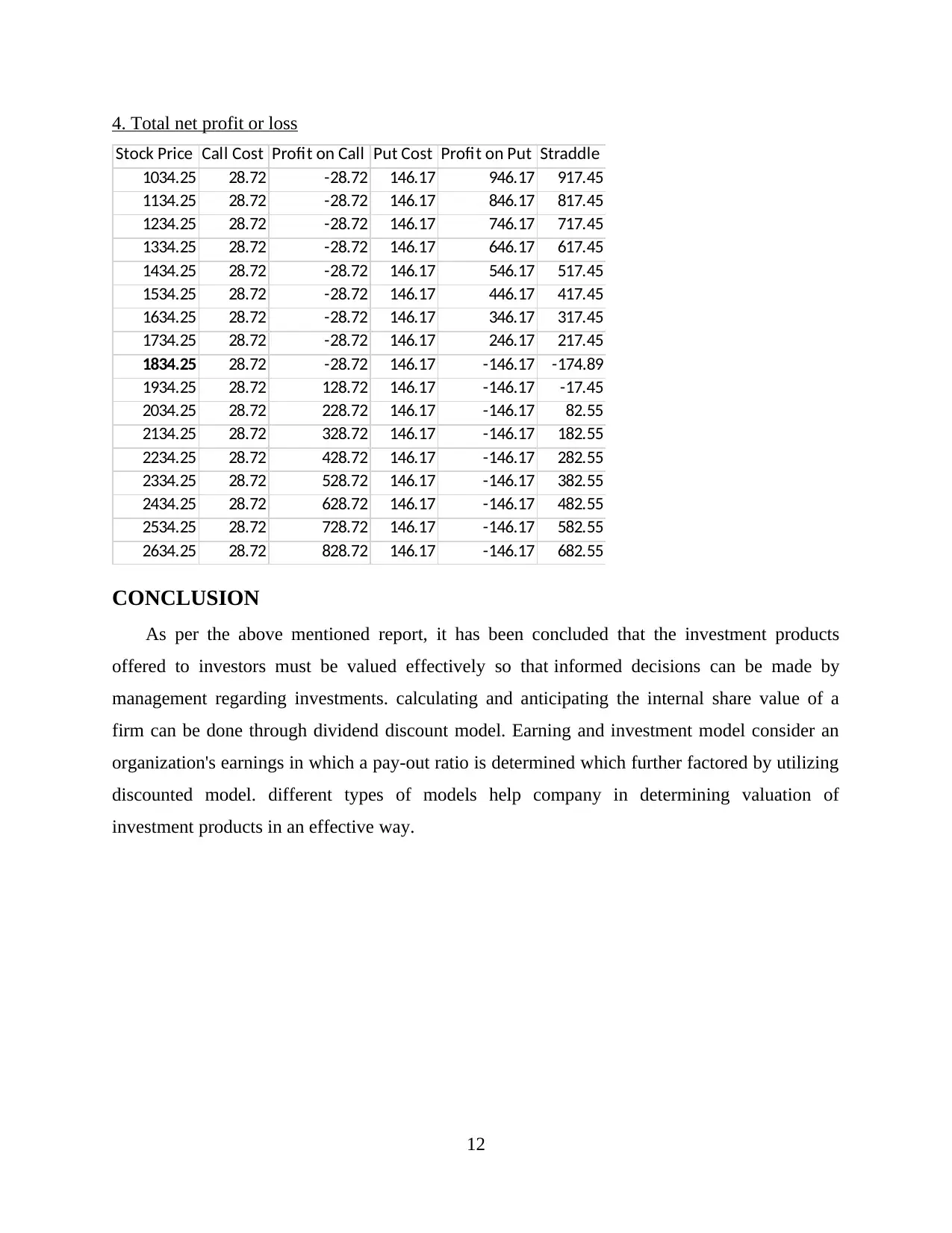

4. Total net profit or loss

Stock Price Call Cost Profit on Call Put Cost Profit on Put Straddle

1034.25 28.72 -28.72 146.17 946.17 917.45

1134.25 28.72 -28.72 146.17 846.17 817.45

1234.25 28.72 -28.72 146.17 746.17 717.45

1334.25 28.72 -28.72 146.17 646.17 617.45

1434.25 28.72 -28.72 146.17 546.17 517.45

1534.25 28.72 -28.72 146.17 446.17 417.45

1634.25 28.72 -28.72 146.17 346.17 317.45

1734.25 28.72 -28.72 146.17 246.17 217.45

1834.25 28.72 -28.72 146.17 -146.17 -174.89

1934.25 28.72 128.72 146.17 -146.17 -17.45

2034.25 28.72 228.72 146.17 -146.17 82.55

2134.25 28.72 328.72 146.17 -146.17 182.55

2234.25 28.72 428.72 146.17 -146.17 282.55

2334.25 28.72 528.72 146.17 -146.17 382.55

2434.25 28.72 628.72 146.17 -146.17 482.55

2534.25 28.72 728.72 146.17 -146.17 582.55

2634.25 28.72 828.72 146.17 -146.17 682.55

CONCLUSION

As per the above mentioned report, it has been concluded that the investment products

offered to investors must be valued effectively so that informed decisions can be made by

management regarding investments. calculating and anticipating the internal share value of a

firm can be done through dividend discount model. Earning and investment model consider an

organization's earnings in which a pay-out ratio is determined which further factored by utilizing

discounted model. different types of models help company in determining valuation of

investment products in an effective way.

12

Stock Price Call Cost Profit on Call Put Cost Profit on Put Straddle

1034.25 28.72 -28.72 146.17 946.17 917.45

1134.25 28.72 -28.72 146.17 846.17 817.45

1234.25 28.72 -28.72 146.17 746.17 717.45

1334.25 28.72 -28.72 146.17 646.17 617.45

1434.25 28.72 -28.72 146.17 546.17 517.45

1534.25 28.72 -28.72 146.17 446.17 417.45

1634.25 28.72 -28.72 146.17 346.17 317.45

1734.25 28.72 -28.72 146.17 246.17 217.45

1834.25 28.72 -28.72 146.17 -146.17 -174.89

1934.25 28.72 128.72 146.17 -146.17 -17.45

2034.25 28.72 228.72 146.17 -146.17 82.55

2134.25 28.72 328.72 146.17 -146.17 182.55

2234.25 28.72 428.72 146.17 -146.17 282.55

2334.25 28.72 528.72 146.17 -146.17 382.55

2434.25 28.72 628.72 146.17 -146.17 482.55

2534.25 28.72 728.72 146.17 -146.17 582.55

2634.25 28.72 828.72 146.17 -146.17 682.55

CONCLUSION

As per the above mentioned report, it has been concluded that the investment products

offered to investors must be valued effectively so that informed decisions can be made by

management regarding investments. calculating and anticipating the internal share value of a

firm can be done through dividend discount model. Earning and investment model consider an

organization's earnings in which a pay-out ratio is determined which further factored by utilizing

discounted model. different types of models help company in determining valuation of

investment products in an effective way.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.