BAP22 - Managerial Accounting: Value Chain Analysis in Rio Tinto

VerifiedAdded on 2023/06/04

|7

|1979

|426

Report

AI Summary

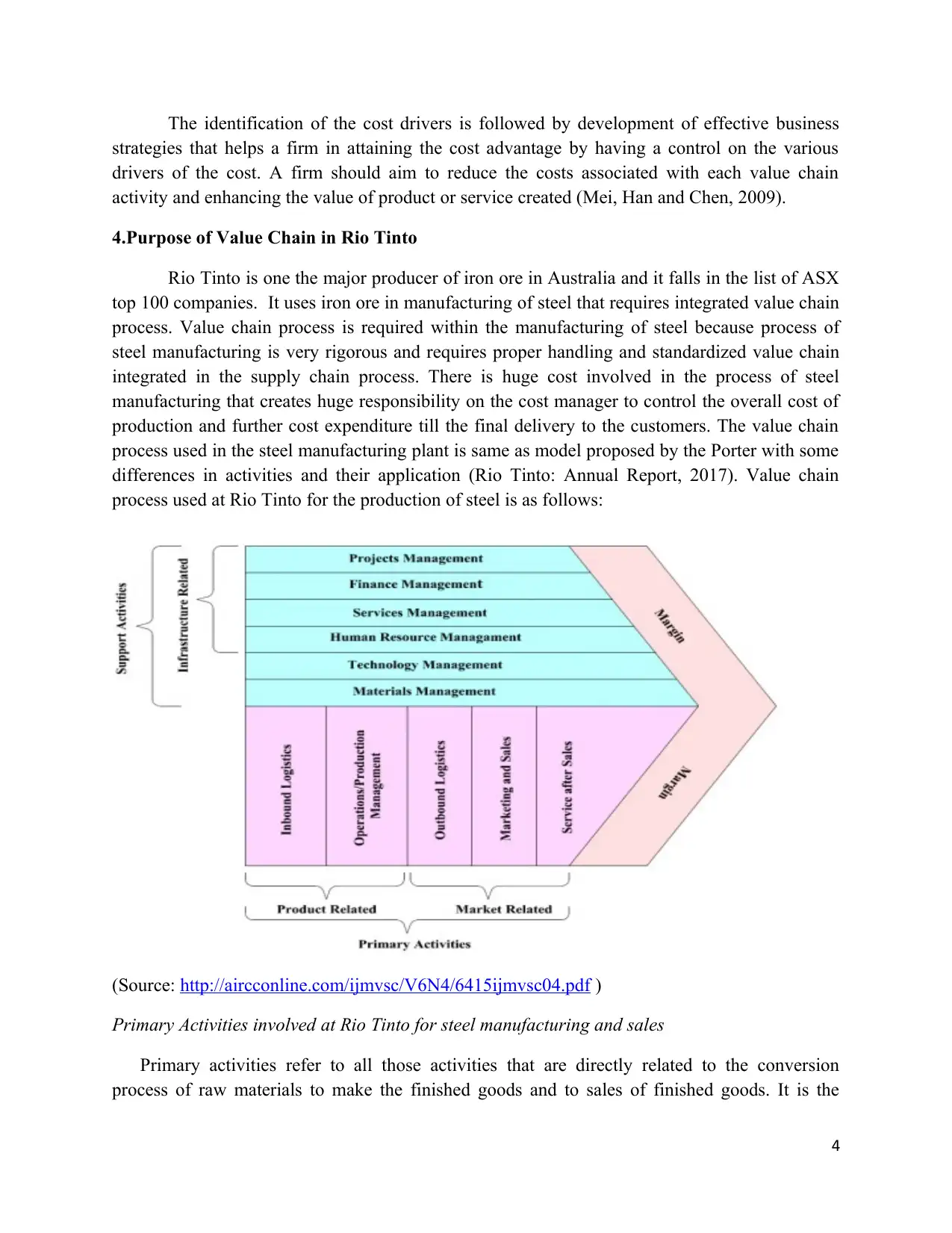

This report provides a comprehensive analysis of the value chain process within Rio Tinto, an Australian manufacturing company, focusing on its application in the steel manufacturing sector. It begins by explaining Porter's concept of the value chain as a tool for cost analysis and operational efficiency, dividing processes into primary and support activities. The report details how value chain analysis is used for cost estimation by identifying value-creating activities and eliminating wasteful ones. It further explores the information used in various value chain segments, including activity identification, cost evaluation, benchmarking, cost driver identification, and opportunities for cost reduction. The analysis then focuses on Rio Tinto, illustrating how the company uses the value chain process in its steel manufacturing operations, highlighting both primary activities (inbound logistics, operations, outbound logistics, marketing and sales, and after-sales service) and support activities (material, technology, human resource, service, finance, and project management). The report concludes that value chain analysis is essential for reducing costs and enhancing value within the supply chain process, particularly for manufacturing companies like Rio Tinto. Desklib provides access to similar solved assignments and study resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.