ACCT20075 - Auditing and Ethics: Vanguard FTSE Fund Analysis

VerifiedAdded on 2023/06/07

|12

|2711

|87

Report

AI Summary

This report provides a comprehensive analysis of the Vanguard FTSE All-World ex-US Index Fund, focusing on key auditing aspects. It assesses the materiality concept, determining quantitative estimates of materiality and its importance from an audit perspective. The report includes a preliminary analytical review using ratio and trend analysis of the profit and loss account and balance sheet. An audit plan is developed for specific audit risk activities with management assertions. Furthermore, the cash flow statement is analyzed to identify major inflows and outflows, along with non-cash investing and financing activities. The going concern assumption and the auditor's opinion are examined for potential audit risks and concerns, ensuring compliance with accounting standards and principles.

Finance Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

A report has been prepared on the company Vanguard FTSE All-World ex-US Index Fund,

which is involved in trading and other such activities over the trade counter. In the given

assignment, the annual report of the company has been analysed in terms of materiality concept,

the quantitative estimate of the materiality for the company has been determined and why it is

important from the audit perspective has been discussed. The draft notes and disclosures in the

annual report has also been studied to determine what the preliminary analytical audit review

procedures are. The same has been conducted using the profit and loss account and the balance

sheet ratio and trend analysis over the years. The audit plan has been prepared for few of the

audit risk activities with management assertion. Finally, in section 3 of the report, the cash flow

statement of the company has been analysed as to what are the major activities which are

contributing to the inflow and the outflows and what are the major non cash investing and

financing activities for the company. The going concern assumption as well the the opinion of

the auditors in the financial statement has been analysed to check if there are any audit risks or

concerns.

2 | P a g e

Executive Summary

A report has been prepared on the company Vanguard FTSE All-World ex-US Index Fund,

which is involved in trading and other such activities over the trade counter. In the given

assignment, the annual report of the company has been analysed in terms of materiality concept,

the quantitative estimate of the materiality for the company has been determined and why it is

important from the audit perspective has been discussed. The draft notes and disclosures in the

annual report has also been studied to determine what the preliminary analytical audit review

procedures are. The same has been conducted using the profit and loss account and the balance

sheet ratio and trend analysis over the years. The audit plan has been prepared for few of the

audit risk activities with management assertion. Finally, in section 3 of the report, the cash flow

statement of the company has been analysed as to what are the major activities which are

contributing to the inflow and the outflows and what are the major non cash investing and

financing activities for the company. The going concern assumption as well the the opinion of

the auditors in the financial statement has been analysed to check if there are any audit risks or

concerns.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Section 1: Materiality concern of the entity................................................................................................4

Section 2: Preliminary analytical review of the company............................................................................5

Section 3: Review of the cash flow statement of the company...................................................................8

References.................................................................................................................................................10

3 | P a g e

Contents

Section 1: Materiality concern of the entity................................................................................................4

Section 2: Preliminary analytical review of the company............................................................................5

Section 3: Review of the cash flow statement of the company...................................................................8

References.................................................................................................................................................10

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Section 1: Materiality concern of the entity

Materiality is one of the major components, which is being considered for audit purposes, and

the auditors in determining the audit planning are using this and what are the audit procedures,

which will be taken up. The concept of materiality has been extensively covered in ASA 320

which mentions materiality plays a major role in helping understand the entity and its

environment and thereby determining what the areas to be checked for materiality (Choy, 2018).

The misstatements, errors and omissions whether individually or in aggregate will be considered

material if the same has the ability to change the economic decision of the users or the relevant

stakeholders. Since materiality is something, which depends upon individual-to-individual

auditor and can change from company to company, it is said to be a subjective matter and

depends largely on the professional judgement. The amount of $ 50000 may be material for an

unlisted company, whereas for the listed company, an amount of $ 200000 may also not

considered material. Furthermore, the it is not necessary that the materiality will always be

quantitative; it can be qualitative as well quantitative. From qualitative perspective, it needs to be

seen that whether or not the company has sufficient internal control, whether or not it has

followed the relevant GAAP and IFRS standard in the presentation and preparation of the

financial statements, whether sufficient disclosures have been given on the accounting policies

followed, the contingent liability and the related party transaction (Goldmann, 2016). On the

other hand, from the quantitative aspect, the company materiality level can be defined as a

percentage like 0.5 – 1% of sales, 5-10% of the nest profits, 1-2% of the gross profits, 1-2% of

the total assets, 5-10% of the shareholder’s equity.

In the given case, the company, which has been chosen, is Vanguard FTSE All-World ex-US

Index Fund (VEU). It closed its books on 31st October 2017. It is one of the exchange-traded

funds, which deals in Australia and America. They trade based on specific underlying basket of

securities and are rather governed by the rules implemented by Securities exchange commission.

These companies are audited in a different fashion but they are compulsorily required to Form N

– Certified Shareholders Report with the SEC annually on a compulsory basis (Trieu, 2017). The

quantitative materiality of the company has been computed in the below mentioned table.

4 | P a g e

Section 1: Materiality concern of the entity

Materiality is one of the major components, which is being considered for audit purposes, and

the auditors in determining the audit planning are using this and what are the audit procedures,

which will be taken up. The concept of materiality has been extensively covered in ASA 320

which mentions materiality plays a major role in helping understand the entity and its

environment and thereby determining what the areas to be checked for materiality (Choy, 2018).

The misstatements, errors and omissions whether individually or in aggregate will be considered

material if the same has the ability to change the economic decision of the users or the relevant

stakeholders. Since materiality is something, which depends upon individual-to-individual

auditor and can change from company to company, it is said to be a subjective matter and

depends largely on the professional judgement. The amount of $ 50000 may be material for an

unlisted company, whereas for the listed company, an amount of $ 200000 may also not

considered material. Furthermore, the it is not necessary that the materiality will always be

quantitative; it can be qualitative as well quantitative. From qualitative perspective, it needs to be

seen that whether or not the company has sufficient internal control, whether or not it has

followed the relevant GAAP and IFRS standard in the presentation and preparation of the

financial statements, whether sufficient disclosures have been given on the accounting policies

followed, the contingent liability and the related party transaction (Goldmann, 2016). On the

other hand, from the quantitative aspect, the company materiality level can be defined as a

percentage like 0.5 – 1% of sales, 5-10% of the nest profits, 1-2% of the gross profits, 1-2% of

the total assets, 5-10% of the shareholder’s equity.

In the given case, the company, which has been chosen, is Vanguard FTSE All-World ex-US

Index Fund (VEU). It closed its books on 31st October 2017. It is one of the exchange-traded

funds, which deals in Australia and America. They trade based on specific underlying basket of

securities and are rather governed by the rules implemented by Securities exchange commission.

These companies are audited in a different fashion but they are compulsorily required to Form N

– Certified Shareholders Report with the SEC annually on a compulsory basis (Trieu, 2017). The

quantitative materiality of the company has been computed in the below mentioned table.

4 | P a g e

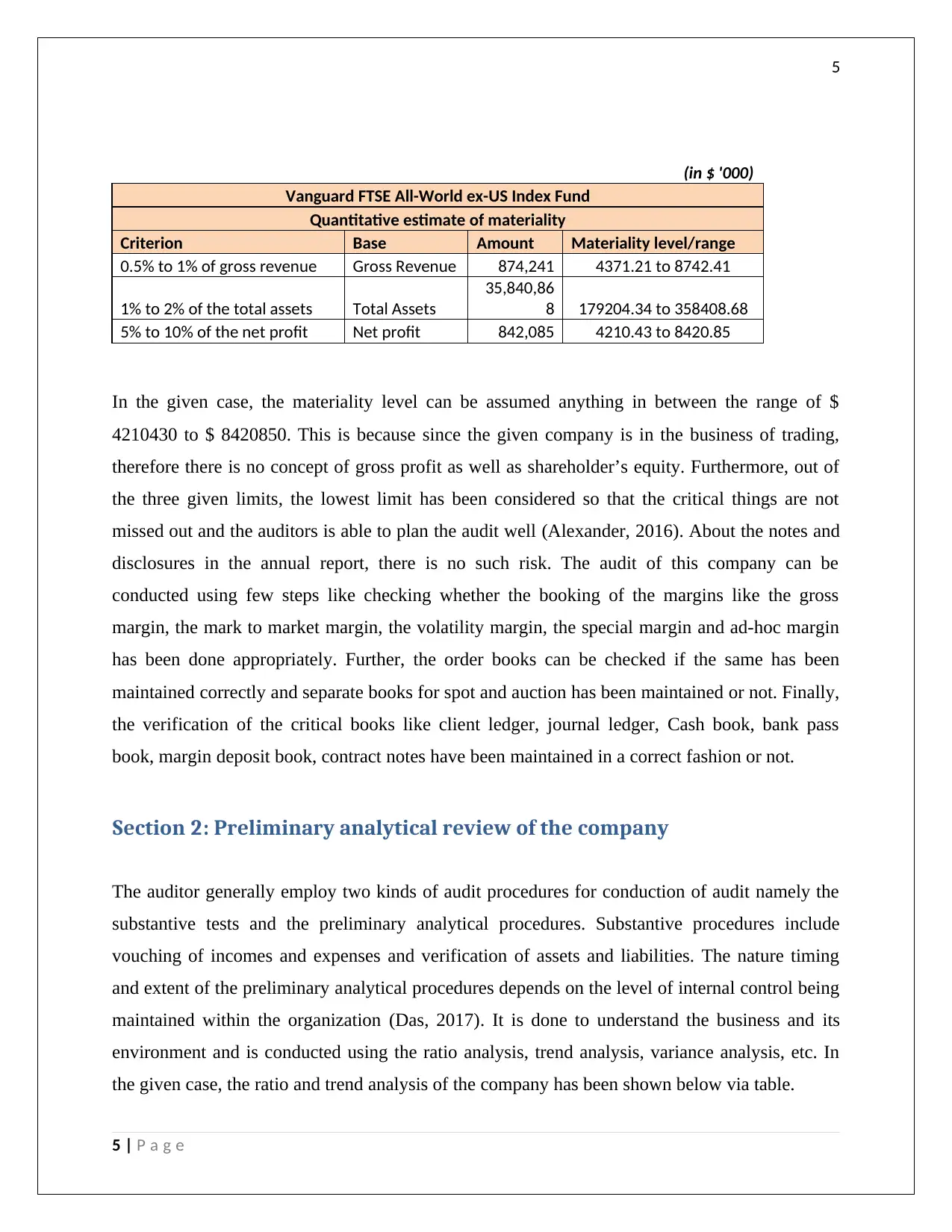

5

(in $ '000)

Vanguard FTSE All-World ex-US Index Fund

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 874,241 4371.21 to 8742.41

1% to 2% of the total assets Total Assets

35,840,86

8 179204.34 to 358408.68

5% to 10% of the net profit Net profit 842,085 4210.43 to 8420.85

In the given case, the materiality level can be assumed anything in between the range of $

4210430 to $ 8420850. This is because since the given company is in the business of trading,

therefore there is no concept of gross profit as well as shareholder’s equity. Furthermore, out of

the three given limits, the lowest limit has been considered so that the critical things are not

missed out and the auditors is able to plan the audit well (Alexander, 2016). About the notes and

disclosures in the annual report, there is no such risk. The audit of this company can be

conducted using few steps like checking whether the booking of the margins like the gross

margin, the mark to market margin, the volatility margin, the special margin and ad-hoc margin

has been done appropriately. Further, the order books can be checked if the same has been

maintained correctly and separate books for spot and auction has been maintained or not. Finally,

the verification of the critical books like client ledger, journal ledger, Cash book, bank pass

book, margin deposit book, contract notes have been maintained in a correct fashion or not.

Section 2: Preliminary analytical review of the company

The auditor generally employ two kinds of audit procedures for conduction of audit namely the

substantive tests and the preliminary analytical procedures. Substantive procedures include

vouching of incomes and expenses and verification of assets and liabilities. The nature timing

and extent of the preliminary analytical procedures depends on the level of internal control being

maintained within the organization (Das, 2017). It is done to understand the business and its

environment and is conducted using the ratio analysis, trend analysis, variance analysis, etc. In

the given case, the ratio and trend analysis of the company has been shown below via table.

5 | P a g e

(in $ '000)

Vanguard FTSE All-World ex-US Index Fund

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 874,241 4371.21 to 8742.41

1% to 2% of the total assets Total Assets

35,840,86

8 179204.34 to 358408.68

5% to 10% of the net profit Net profit 842,085 4210.43 to 8420.85

In the given case, the materiality level can be assumed anything in between the range of $

4210430 to $ 8420850. This is because since the given company is in the business of trading,

therefore there is no concept of gross profit as well as shareholder’s equity. Furthermore, out of

the three given limits, the lowest limit has been considered so that the critical things are not

missed out and the auditors is able to plan the audit well (Alexander, 2016). About the notes and

disclosures in the annual report, there is no such risk. The audit of this company can be

conducted using few steps like checking whether the booking of the margins like the gross

margin, the mark to market margin, the volatility margin, the special margin and ad-hoc margin

has been done appropriately. Further, the order books can be checked if the same has been

maintained correctly and separate books for spot and auction has been maintained or not. Finally,

the verification of the critical books like client ledger, journal ledger, Cash book, bank pass

book, margin deposit book, contract notes have been maintained in a correct fashion or not.

Section 2: Preliminary analytical review of the company

The auditor generally employ two kinds of audit procedures for conduction of audit namely the

substantive tests and the preliminary analytical procedures. Substantive procedures include

vouching of incomes and expenses and verification of assets and liabilities. The nature timing

and extent of the preliminary analytical procedures depends on the level of internal control being

maintained within the organization (Das, 2017). It is done to understand the business and its

environment and is conducted using the ratio analysis, trend analysis, variance analysis, etc. In

the given case, the ratio and trend analysis of the company has been shown below via table.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

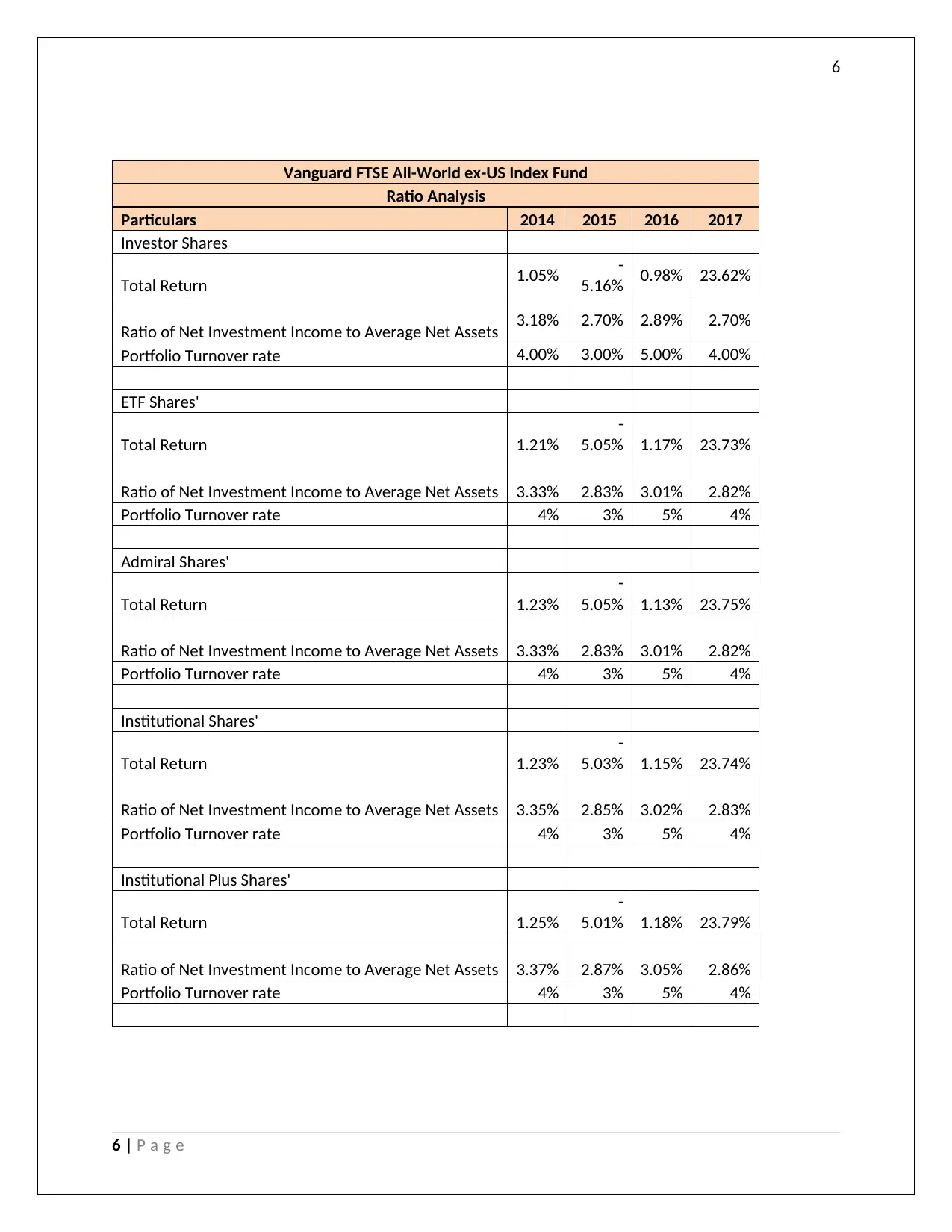

Vanguard FTSE All-World ex-US Index Fund

Ratio Analysis

Particulars 2014 2015 2016 2017

Investor Shares

Total Return 1.05% -

5.16% 0.98% 23.62%

Ratio of Net Investment Income to Average Net Assets 3.18% 2.70% 2.89% 2.70%

Portfolio Turnover rate 4.00% 3.00% 5.00% 4.00%

ETF Shares'

Total Return 1.21%

-

5.05% 1.17% 23.73%

Ratio of Net Investment Income to Average Net Assets 3.33% 2.83% 3.01% 2.82%

Portfolio Turnover rate 4% 3% 5% 4%

Admiral Shares'

Total Return 1.23%

-

5.05% 1.13% 23.75%

Ratio of Net Investment Income to Average Net Assets 3.33% 2.83% 3.01% 2.82%

Portfolio Turnover rate 4% 3% 5% 4%

Institutional Shares'

Total Return 1.23%

-

5.03% 1.15% 23.74%

Ratio of Net Investment Income to Average Net Assets 3.35% 2.85% 3.02% 2.83%

Portfolio Turnover rate 4% 3% 5% 4%

Institutional Plus Shares'

Total Return 1.25%

-

5.01% 1.18% 23.79%

Ratio of Net Investment Income to Average Net Assets 3.37% 2.87% 3.05% 2.86%

Portfolio Turnover rate 4% 3% 5% 4%

6 | P a g e

Vanguard FTSE All-World ex-US Index Fund

Ratio Analysis

Particulars 2014 2015 2016 2017

Investor Shares

Total Return 1.05% -

5.16% 0.98% 23.62%

Ratio of Net Investment Income to Average Net Assets 3.18% 2.70% 2.89% 2.70%

Portfolio Turnover rate 4.00% 3.00% 5.00% 4.00%

ETF Shares'

Total Return 1.21%

-

5.05% 1.17% 23.73%

Ratio of Net Investment Income to Average Net Assets 3.33% 2.83% 3.01% 2.82%

Portfolio Turnover rate 4% 3% 5% 4%

Admiral Shares'

Total Return 1.23%

-

5.05% 1.13% 23.75%

Ratio of Net Investment Income to Average Net Assets 3.33% 2.83% 3.01% 2.82%

Portfolio Turnover rate 4% 3% 5% 4%

Institutional Shares'

Total Return 1.23%

-

5.03% 1.15% 23.74%

Ratio of Net Investment Income to Average Net Assets 3.35% 2.85% 3.02% 2.83%

Portfolio Turnover rate 4% 3% 5% 4%

Institutional Plus Shares'

Total Return 1.25%

-

5.01% 1.18% 23.79%

Ratio of Net Investment Income to Average Net Assets 3.37% 2.87% 3.05% 2.86%

Portfolio Turnover rate 4% 3% 5% 4%

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

In the given case, we can see that the portfolio turnover rate over the past years in each of the

trading section has been around 4-5%. It shows the extent to which the mutual fund exchanges or

turns over its assets and underlying stocks over the past year (Belton, 2017). The more the

turnover ratio, the more the turnover. Therefore, we can see that the company has improved over

last year from 3% to 4%. Similarly, in terms of net investment income to the average net assets

ratio, the income ratio has increase over the past years from ~2.70% to 3.35%, which is a

positive indication that the company is growing in terms of returns on investment and the net

income. Finally, if the total returns is analysed over the years, which includes all the types of

returns we can see that the returns were ~23% in the year 2014 which then dropped to nearby 1%

and then decreased to ~5% in the year 2016 and finally in the last year 2017, it has increased to

~1.2%. This shows the company is moderately growing in terms of total returns (Grenier, 2017).

For ratio analysis, 5 major types of shares were being considered namely investor shares, ETF

shares, admiral shares, institutional shares and institutional plus shares.

Audit assertion means the claims and the representation, which is being done by the management

of the company, that all the possible risks have been taken care; off and mitigated while

preparation of the financial statements. The audit risk is the risk that the misstatements would not

be identified in the course of audit (Erik & Jan, 2017). It may be due to the detection, inherent or

control risk. With respect to the company in hand, the risks and audit procedures have been

shown below:

Sl

No.

Key risk areas Relevant assertion Audit procedure

1 There is an investment risk as

the funds are invested in the

securities of the foreign

issuers and in the US

corporations (Farmer, 2018).

As per the management, the

risk is minimised as the

portfolio consists of 5

classes of shares namely

Investor Shares, ETF

Shares, Admiral Shares,

Institutional Shares, and

Institutional Plus Shares.

To check the validity of

this risk the fluctuation

over the past 2-3 year can

be seen and analysed and

what are the possible

measures to hedge this

risk can be suggested to

the client.

2 There is a risk associated

with the future contract being

Counterparty risks in this

case is eliminated as there is

Relevant records and

papers for the registration

7 | P a g e

In the given case, we can see that the portfolio turnover rate over the past years in each of the

trading section has been around 4-5%. It shows the extent to which the mutual fund exchanges or

turns over its assets and underlying stocks over the past year (Belton, 2017). The more the

turnover ratio, the more the turnover. Therefore, we can see that the company has improved over

last year from 3% to 4%. Similarly, in terms of net investment income to the average net assets

ratio, the income ratio has increase over the past years from ~2.70% to 3.35%, which is a

positive indication that the company is growing in terms of returns on investment and the net

income. Finally, if the total returns is analysed over the years, which includes all the types of

returns we can see that the returns were ~23% in the year 2014 which then dropped to nearby 1%

and then decreased to ~5% in the year 2016 and finally in the last year 2017, it has increased to

~1.2%. This shows the company is moderately growing in terms of total returns (Grenier, 2017).

For ratio analysis, 5 major types of shares were being considered namely investor shares, ETF

shares, admiral shares, institutional shares and institutional plus shares.

Audit assertion means the claims and the representation, which is being done by the management

of the company, that all the possible risks have been taken care; off and mitigated while

preparation of the financial statements. The audit risk is the risk that the misstatements would not

be identified in the course of audit (Erik & Jan, 2017). It may be due to the detection, inherent or

control risk. With respect to the company in hand, the risks and audit procedures have been

shown below:

Sl

No.

Key risk areas Relevant assertion Audit procedure

1 There is an investment risk as

the funds are invested in the

securities of the foreign

issuers and in the US

corporations (Farmer, 2018).

As per the management, the

risk is minimised as the

portfolio consists of 5

classes of shares namely

Investor Shares, ETF

Shares, Admiral Shares,

Institutional Shares, and

Institutional Plus Shares.

To check the validity of

this risk the fluctuation

over the past 2-3 year can

be seen and analysed and

what are the possible

measures to hedge this

risk can be suggested to

the client.

2 There is a risk associated

with the future contract being

Counterparty risks in this

case is eliminated as there is

Relevant records and

papers for the registration

7 | P a g e

8

entered into by the company

as there is imperfect

correlation between the

changes in the market value

of the stock and the prices of

future contracts.

a regulated clearing house

and also the financial

strength of the clearing

brokers and the clearing

houses is also being

monitored. Also, the initial

margin requirement is being

taken care off so that there

is no default and loss to the

company.

of the clearing agent on

the exchange can be

checked and then the

number of default cases

over the past 2- years can

be seen as to whether or

not a provision is

required in this aspect.

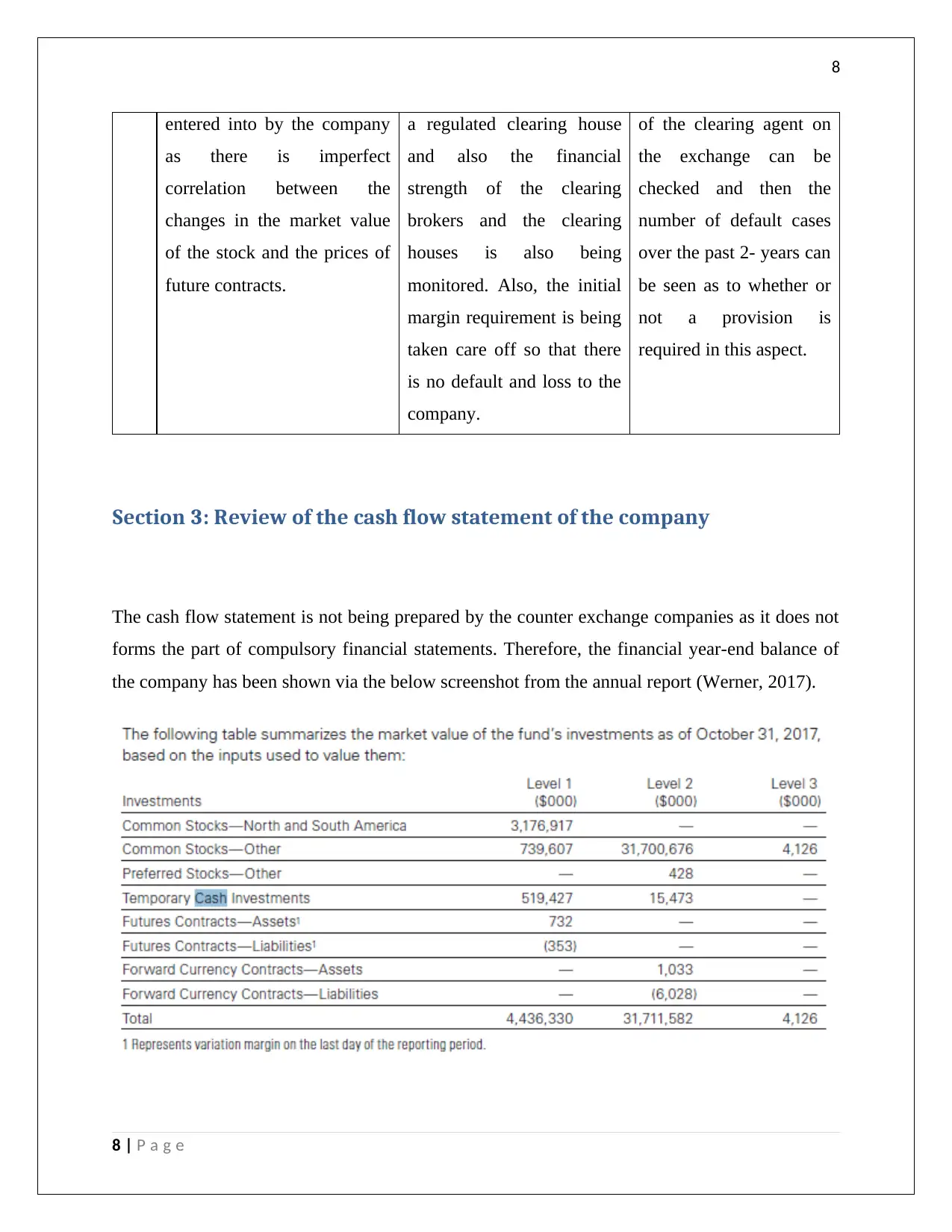

Section 3: Review of the cash flow statement of the company

The cash flow statement is not being prepared by the counter exchange companies as it does not

forms the part of compulsory financial statements. Therefore, the financial year-end balance of

the company has been shown via the below screenshot from the annual report (Werner, 2017).

8 | P a g e

entered into by the company

as there is imperfect

correlation between the

changes in the market value

of the stock and the prices of

future contracts.

a regulated clearing house

and also the financial

strength of the clearing

brokers and the clearing

houses is also being

monitored. Also, the initial

margin requirement is being

taken care off so that there

is no default and loss to the

company.

of the clearing agent on

the exchange can be

checked and then the

number of default cases

over the past 2- years can

be seen as to whether or

not a provision is

required in this aspect.

Section 3: Review of the cash flow statement of the company

The cash flow statement is not being prepared by the counter exchange companies as it does not

forms the part of compulsory financial statements. Therefore, the financial year-end balance of

the company has been shown via the below screenshot from the annual report (Werner, 2017).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

From the above screenshot, we can see that the temporary cash investment of the company for

the year 2017 stands at a cumulative $ 534900. In case the major inflows and the outflows are

being analysed, we can see that the fund purchased $2,048,894,000 of investment securities and

sold $642,934,000 of investment securities during this given period, besides the temporary cash

investment (Mun, 2018). The company is an investment management company so there is no

financing and investing activity, everything falls within the ambit of the cash flow from

operating activities.

Considering the discussion above, it can be said that the company is making the going concern

assumption true, as there are no material errors, omissions and misstatements being reported in

the annual report. The audit procedures to check the risk and to mitigate the existing risk has

already been discussed in above sections (Jefferson, 2017).

The annual report has just been submitted to the SEC and the auditor of the company Price water

house Coopers has given a clear opinion that the accounts of the company has been prepared as

per the standards of the Public Company Accounting Oversight Board (United States) and that

all the relevant US accounting principles have been adhered to. In the disclosure section, it has

been mentioned that no material event or transaction has occurred beyond October 31, 2017 and

hence the same has not been reported (Sithole, Chandler, Abeysekera, & Paas, 2017).

9 | P a g e

From the above screenshot, we can see that the temporary cash investment of the company for

the year 2017 stands at a cumulative $ 534900. In case the major inflows and the outflows are

being analysed, we can see that the fund purchased $2,048,894,000 of investment securities and

sold $642,934,000 of investment securities during this given period, besides the temporary cash

investment (Mun, 2018). The company is an investment management company so there is no

financing and investing activity, everything falls within the ambit of the cash flow from

operating activities.

Considering the discussion above, it can be said that the company is making the going concern

assumption true, as there are no material errors, omissions and misstatements being reported in

the annual report. The audit procedures to check the risk and to mitigate the existing risk has

already been discussed in above sections (Jefferson, 2017).

The annual report has just been submitted to the SEC and the auditor of the company Price water

house Coopers has given a clear opinion that the accounts of the company has been prepared as

per the standards of the Public Company Accounting Oversight Board (United States) and that

all the relevant US accounting principles have been adhered to. In the disclosure section, it has

been mentioned that no material event or transaction has occurred beyond October 31, 2017 and

hence the same has not been reported (Sithole, Chandler, Abeysekera, & Paas, 2017).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

Farmer, Y. (2018). Ethical Decision Making and Reputation Management in Public Relations. Journal of

Media Ethics, 1-12.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4, 103-112.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Mun, K. a. (2018). A close look at the role of regulatory fit in consumers’ responses to unethical firms.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

10 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), 10-17.

Erik, H., & Jan, B. (2017). Supply chain management and activity-based costing: Current status and

directions for the future. International Journal of Physical Distribution & Logistics Management,

47(8), 712-735.

Farmer, Y. (2018). Ethical Decision Making and Reputation Management in Public Relations. Journal of

Media Ethics, 1-12.

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4, 103-112.

Grenier, J. (2017). Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), 241-256.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Mun, K. a. (2018). A close look at the role of regulatory fit in consumers’ responses to unethical firms.

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved from

http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

10 | P a g e

11

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

11 | P a g e

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.