Weighted Average Cost of Capital Analysis for BHP Billiton Ltd

VerifiedAdded on 2024/04/26

|19

|3239

|171

AI Summary

This analysis focuses on evaluating the Weighted Average Cost of Capital (WACC) for BHP Billiton Ltd, a multinational mining company. It includes calculations, interpretations, and recommendations based on WACC, gearing ratios, and the Capital Asset Pricing Model (CAPM).

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

WACC

BHP BILLTON

1

BHP BILLTON

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

BHP Billiton Ltd is a multinational company, which is Anglo Australian and involved in mining

metals and petroleum. It is a dual listed public company whose headquarters are in Melbourne,

Australia. The CEO of BHP Billiton Ltd is Andrew Stewart Mackenzie. It is the second largest

mining company in the world in terms of revenue with 69.4 billion US dollars. It has many

subsidiaries including BHP Billiton Finance B. V., BHP Billiton Finance Plc and many more.

The weighted average cost of capital through dividend growth model and capital asset pricing

model will be evaluated for BHP Billiton Ltd. Also, the gearing ratios will be calculated so that

the long-term debt of the company can be compared to its capital employed or equity capital.

The weighted average cost of capital is a rate that a company expects to pay to all the

shareholders so that its assets can be financed.

2

BHP Billiton Ltd is a multinational company, which is Anglo Australian and involved in mining

metals and petroleum. It is a dual listed public company whose headquarters are in Melbourne,

Australia. The CEO of BHP Billiton Ltd is Andrew Stewart Mackenzie. It is the second largest

mining company in the world in terms of revenue with 69.4 billion US dollars. It has many

subsidiaries including BHP Billiton Finance B. V., BHP Billiton Finance Plc and many more.

The weighted average cost of capital through dividend growth model and capital asset pricing

model will be evaluated for BHP Billiton Ltd. Also, the gearing ratios will be calculated so that

the long-term debt of the company can be compared to its capital employed or equity capital.

The weighted average cost of capital is a rate that a company expects to pay to all the

shareholders so that its assets can be financed.

2

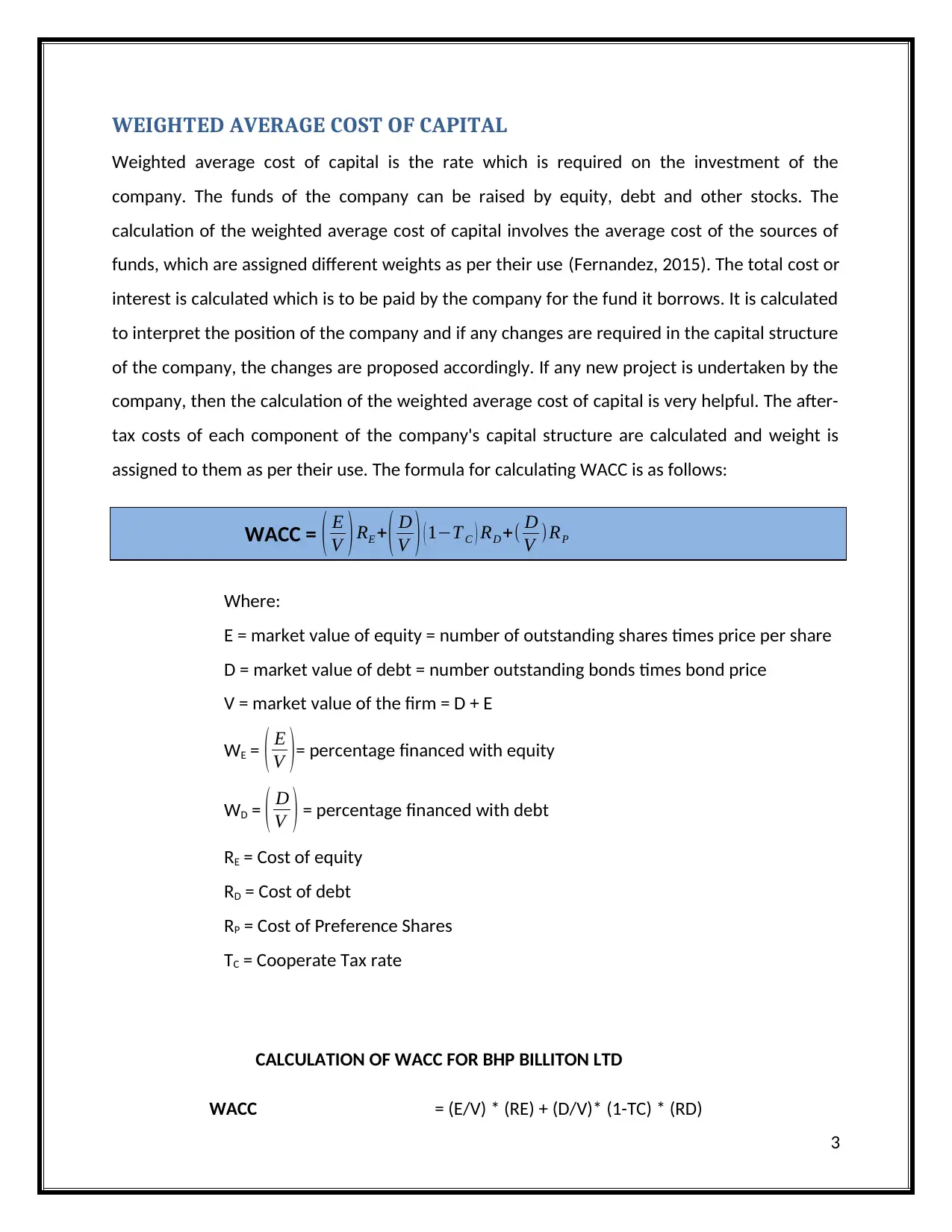

WEIGHTED AVERAGE COST OF CAPITAL

Weighted average cost of capital is the rate which is required on the investment of the

company. The funds of the company can be raised by equity, debt and other stocks. The

calculation of the weighted average cost of capital involves the average cost of the sources of

funds, which are assigned different weights as per their use (Fernandez, 2015). The total cost or

interest is calculated which is to be paid by the company for the fund it borrows. It is calculated

to interpret the position of the company and if any changes are required in the capital structure

of the company, the changes are proposed accordingly. If any new project is undertaken by the

company, then the calculation of the weighted average cost of capital is very helpful. The after-

tax costs of each component of the company's capital structure are calculated and weight is

assigned to them as per their use. The formula for calculating WACC is as follows:

WACC = ( E

V ) RE + ( D

V ) ( 1−T C ) RD +( D

V )RP

Where:

E = market value of equity = number of outstanding shares times price per share

D = market value of debt = number outstanding bonds times bond price

V = market value of the firm = D + E

WE = ( E

V )= percentage financed with equity

WD = ( D

V ) = percentage financed with debt

RE = Cost of equity

RD = Cost of debt

RP = Cost of Preference Shares

TC = Cooperate Tax rate

CALCULATION OF WACC FOR BHP BILLITON LTD

WACC = (E/V) * (RE) + (D/V)* (1-TC) * (RD)

3

Weighted average cost of capital is the rate which is required on the investment of the

company. The funds of the company can be raised by equity, debt and other stocks. The

calculation of the weighted average cost of capital involves the average cost of the sources of

funds, which are assigned different weights as per their use (Fernandez, 2015). The total cost or

interest is calculated which is to be paid by the company for the fund it borrows. It is calculated

to interpret the position of the company and if any changes are required in the capital structure

of the company, the changes are proposed accordingly. If any new project is undertaken by the

company, then the calculation of the weighted average cost of capital is very helpful. The after-

tax costs of each component of the company's capital structure are calculated and weight is

assigned to them as per their use. The formula for calculating WACC is as follows:

WACC = ( E

V ) RE + ( D

V ) ( 1−T C ) RD +( D

V )RP

Where:

E = market value of equity = number of outstanding shares times price per share

D = market value of debt = number outstanding bonds times bond price

V = market value of the firm = D + E

WE = ( E

V )= percentage financed with equity

WD = ( D

V ) = percentage financed with debt

RE = Cost of equity

RD = Cost of debt

RP = Cost of Preference Shares

TC = Cooperate Tax rate

CALCULATION OF WACC FOR BHP BILLITON LTD

WACC = (E/V) * (RE) + (D/V)* (1-TC) * (RD)

3

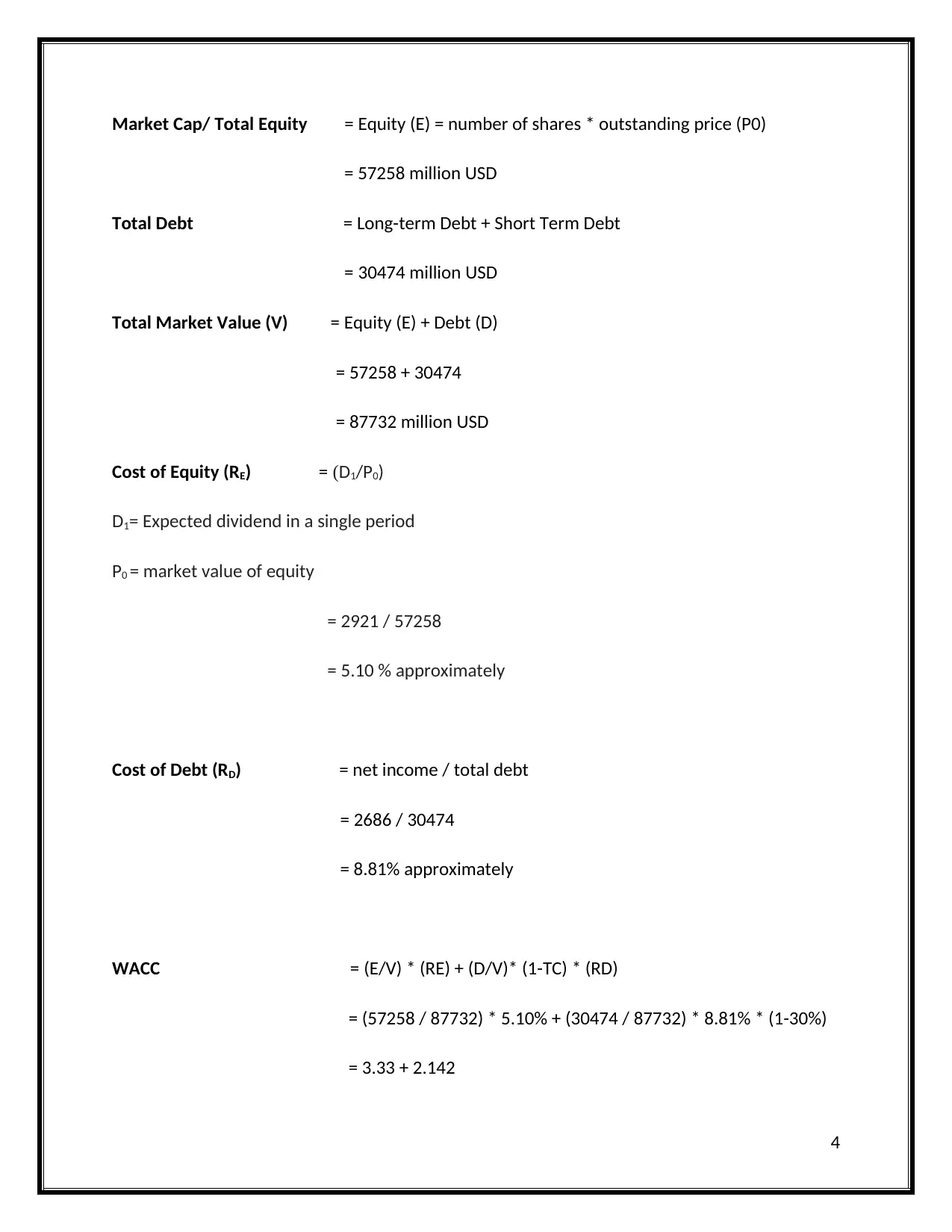

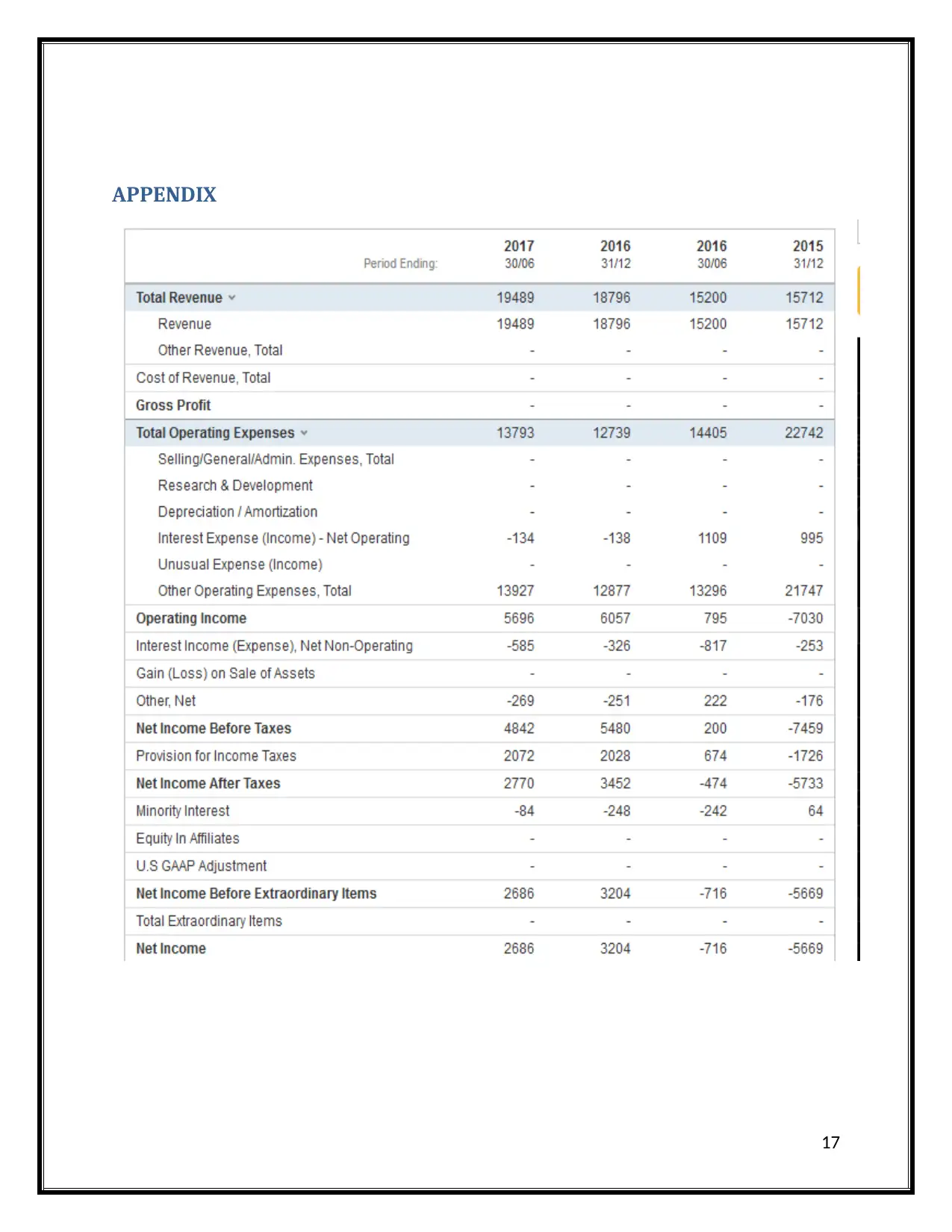

Market Cap/ Total Equity = Equity (E) = number of shares * outstanding price (P0)

= 57258 million USD

Total Debt = Long-term Debt + Short Term Debt

= 30474 million USD

Total Market Value (V) = Equity (E) + Debt (D)

= 57258 + 30474

= 87732 million USD

Cost of Equity (RE) = (D1/P0)

D1= Expected dividend in a single period

P0 = market value of equity

= 2921 / 57258

= 5.10 % approximately

Cost of Debt (RD) = net income / total debt

= 2686 / 30474

= 8.81% approximately

WACC = (E/V) * (RE) + (D/V)* (1-TC) * (RD)

= (57258 / 87732) * 5.10% + (30474 / 87732) * 8.81% * (1-30%)

= 3.33 + 2.142

4

= 57258 million USD

Total Debt = Long-term Debt + Short Term Debt

= 30474 million USD

Total Market Value (V) = Equity (E) + Debt (D)

= 57258 + 30474

= 87732 million USD

Cost of Equity (RE) = (D1/P0)

D1= Expected dividend in a single period

P0 = market value of equity

= 2921 / 57258

= 5.10 % approximately

Cost of Debt (RD) = net income / total debt

= 2686 / 30474

= 8.81% approximately

WACC = (E/V) * (RE) + (D/V)* (1-TC) * (RD)

= (57258 / 87732) * 5.10% + (30474 / 87732) * 8.81% * (1-30%)

= 3.33 + 2.142

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

WACC = 5.47%

The weighted average cost of capital for BHP Billiton is 5.47%, which can be useful information

for the investors as well as company for making the investing decisions. It has to be used very

carefully as the components of capital are expressed in the terms of market value. The

investments decisions are directly affected by the calculation of the weighted average cost of

capital, therefore it should not be faulty (MARKET PORTFOLIO, 2016). BHP Billiton works with a

WACC of 5.47%, which means that the investments which give a higher return than 5.47%, only

those investments should be made. Weighted average cost of capital is thus the after-tax cost

of capital which takes into account the weightings of the relative market value of each debt and

equity. In the model of dividend growth, the value of equity of the company is linked with the

market cost of equity and same is done with the debt element of the company.

TOTAL MARKET VALUE OF EQUITY

The market value of equity is the total value of outstanding shares or stocks of the company,

measured by their market price. It can include share capital, treasury shares, various types of

reserves and retained earnings. All types of outstanding shares should be taken into calculation

whether they are common stock or preferred stock (Campbell, et al. 2016). It is the value of the

company which is available to the owners or shareholders. The total market value of equity as

per the balance sheet of the company is 57258 million USD.

TOTAL MARKET VALUE OF DEBT

The total market value of debt of any company can be defined as the total fund which is

borrowed by the company whether it is commercial paper, bonds, debentures or other debts. A

commercial paper is a short-term debt which is issued by the company to cover its short-term

finance needs. Bonds can be of short-term as well as long-term that is issued by a government

company or a public company (BHP Billiton, 2017). As per the balance sheet of BHP Billiton Ltd,

for the year 2017, the total debt amounts to 30,474 million USD.

5

The weighted average cost of capital for BHP Billiton is 5.47%, which can be useful information

for the investors as well as company for making the investing decisions. It has to be used very

carefully as the components of capital are expressed in the terms of market value. The

investments decisions are directly affected by the calculation of the weighted average cost of

capital, therefore it should not be faulty (MARKET PORTFOLIO, 2016). BHP Billiton works with a

WACC of 5.47%, which means that the investments which give a higher return than 5.47%, only

those investments should be made. Weighted average cost of capital is thus the after-tax cost

of capital which takes into account the weightings of the relative market value of each debt and

equity. In the model of dividend growth, the value of equity of the company is linked with the

market cost of equity and same is done with the debt element of the company.

TOTAL MARKET VALUE OF EQUITY

The market value of equity is the total value of outstanding shares or stocks of the company,

measured by their market price. It can include share capital, treasury shares, various types of

reserves and retained earnings. All types of outstanding shares should be taken into calculation

whether they are common stock or preferred stock (Campbell, et al. 2016). It is the value of the

company which is available to the owners or shareholders. The total market value of equity as

per the balance sheet of the company is 57258 million USD.

TOTAL MARKET VALUE OF DEBT

The total market value of debt of any company can be defined as the total fund which is

borrowed by the company whether it is commercial paper, bonds, debentures or other debts. A

commercial paper is a short-term debt which is issued by the company to cover its short-term

finance needs. Bonds can be of short-term as well as long-term that is issued by a government

company or a public company (BHP Billiton, 2017). As per the balance sheet of BHP Billiton Ltd,

for the year 2017, the total debt amounts to 30,474 million USD.

5

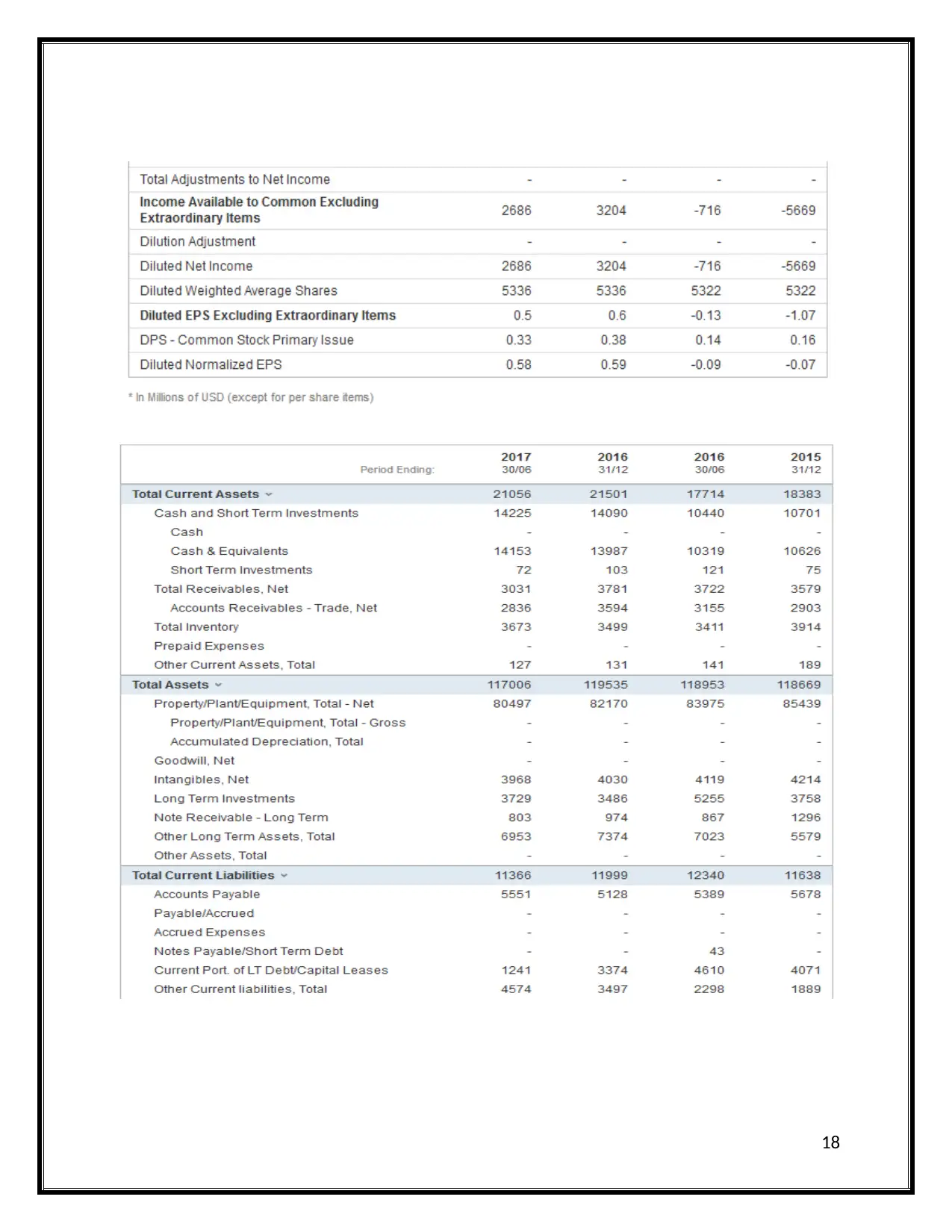

TOTAL MARKET VALUE

Total market value of the company is calculated by adding the total debt and total equity of the

company. Total debt includes the long-term debt and short-term debt of the company and total

equity as given in the balance sheet of the company.

TOTAL DEBT + TOTAL EQUITY = 57258 + 30474 = 87732 million USD

In the total debt of the company, both long term and short term debts are included. In the total

equity of the company, the common stock, retained earnings and treasury stock are included.

COST OF EQUITY

The cost of equity is the rate of return equalise the value of expected dividends present value

and the share price of the market. It is the return that shareholders require for investment in

the shares and stocks of a particular company (Billett, et al. 2015). The cost of equity can be

calculated as follows:

RE= (D1/P0)

in which RE= Cost of equity

D1= Expected dividend in a single period

P0 = market value of equity

= 2921 / 57258

= 5.10 % approximately

COST OF DEBT

Cost of debt is the rate at which the company pays interest on its borrowings. A debt can be in

the form of bond or debenture. Bond is a long-term instrument which does not carry any type

of risk as they are issued by Government Company or a public company. Debentures are also

6

Total market value of the company is calculated by adding the total debt and total equity of the

company. Total debt includes the long-term debt and short-term debt of the company and total

equity as given in the balance sheet of the company.

TOTAL DEBT + TOTAL EQUITY = 57258 + 30474 = 87732 million USD

In the total debt of the company, both long term and short term debts are included. In the total

equity of the company, the common stock, retained earnings and treasury stock are included.

COST OF EQUITY

The cost of equity is the rate of return equalise the value of expected dividends present value

and the share price of the market. It is the return that shareholders require for investment in

the shares and stocks of a particular company (Billett, et al. 2015). The cost of equity can be

calculated as follows:

RE= (D1/P0)

in which RE= Cost of equity

D1= Expected dividend in a single period

P0 = market value of equity

= 2921 / 57258

= 5.10 % approximately

COST OF DEBT

Cost of debt is the rate at which the company pays interest on its borrowings. A debt can be in

the form of bond or debenture. Bond is a long-term instrument which does not carry any type

of risk as they are issued by Government Company or a public company. Debentures are also

6

long-term instruments which carry a risk as the rate of interest on them is also not fixed. With

the evaluation of the cost of debt, the investors come to know about the risk in investing in the

company when compared to other companies (Goh, et al. 2017). The cost of debt can be

calculated as follows:

COST OF DEBT = NET INCOME / TOTAL DEBT

= 2686 / 30474

= 8.81% approximately

The cost of debt is 8.81%, which means for every dollar which investors lend to BHP Billiton Ltd,

they expect a return of 8.81. This cost of debt is calculated on the after-tax income of the

company.

7

the evaluation of the cost of debt, the investors come to know about the risk in investing in the

company when compared to other companies (Goh, et al. 2017). The cost of debt can be

calculated as follows:

COST OF DEBT = NET INCOME / TOTAL DEBT

= 2686 / 30474

= 8.81% approximately

The cost of debt is 8.81%, which means for every dollar which investors lend to BHP Billiton Ltd,

they expect a return of 8.81. This cost of debt is calculated on the after-tax income of the

company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

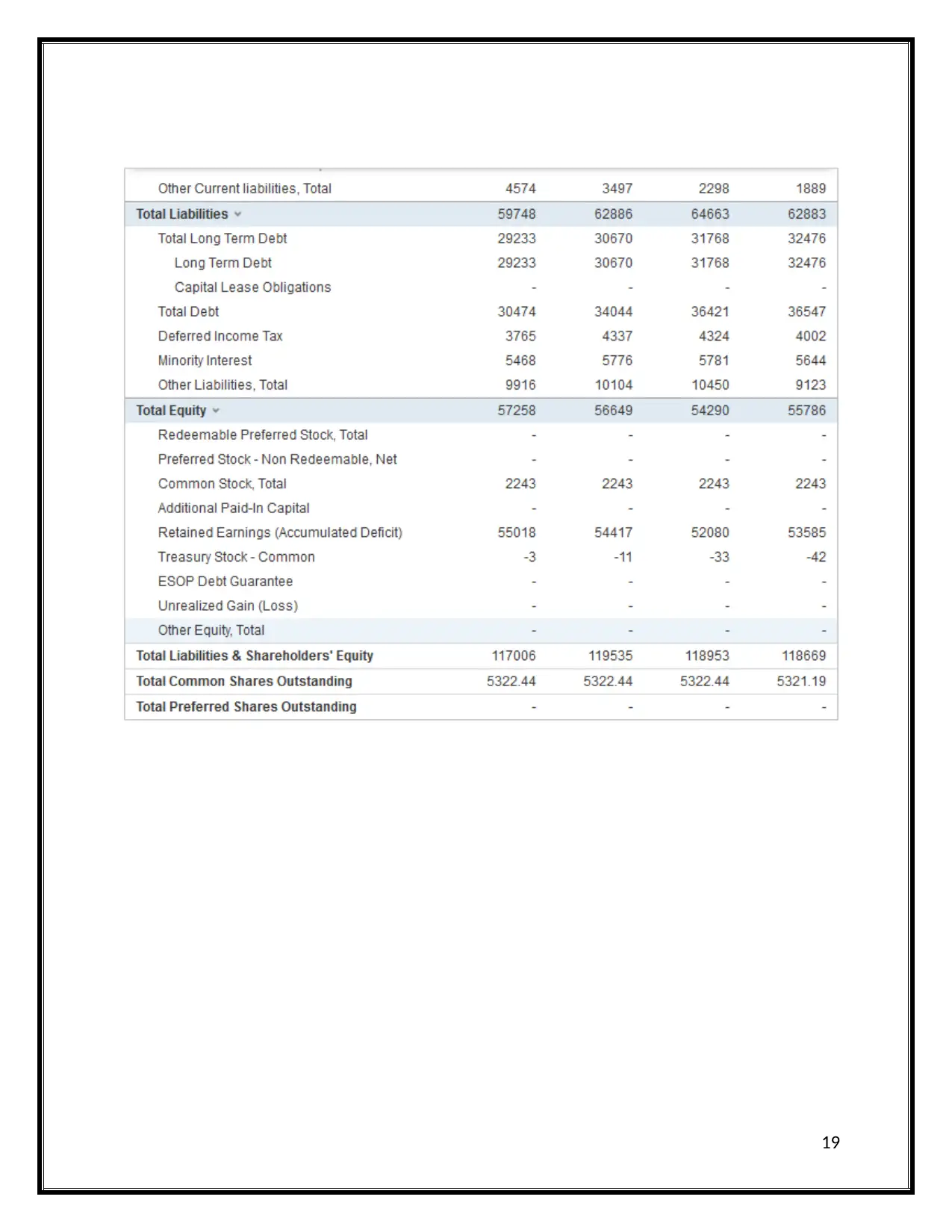

GEARING RATIOS

When analysing BHP Billiton this is a fundamental ratio that is used for analysis portion so as to

analyse the level of the long-term debt that it has as compared to the equity of the firm. This

ratio will give the investors an idea of the survival of the company at economic downturns. It

will help in depicting the leverage of the BHP Billiton and will represent the quantity of the

business funds that come from the creditors and stockholders. The gearing ratios include the

calculation of the interest earned ratio, debt ratio, debt-to-equity ratio and the equity ratio

(Rosemary Peavler, 2018). These all ratios will help to know the suitability of capitalisation of

BHP Billiton.

CALCULATIONS

Debt-to-equity ratio= Total debt / Total Equity

= (30474 / 57258)

= 0.5326

Total debt to total asset ratio = Total debt/ Total Assets

= (30474 / 117006)

= 0.2604

Capitalisation ratio= Long-Term Debt / (Long-Term Debt + Shareholder’s Equity)

= 29233/ (29233 + 57258)

= 0.3380

INTERPRETATIONS

From the above calculations performed and the data gathered BHP Billiton has a current ratio

of 1.85 (Market Watch, 2018) that shows the strong liquidity of the firm that in case of issues it

has sufficient assets that can be converted to cash within 90 days to pay off the current

liabilities in future. The gearing ratios calculated above for NHP Billiton will be useful for the

8

When analysing BHP Billiton this is a fundamental ratio that is used for analysis portion so as to

analyse the level of the long-term debt that it has as compared to the equity of the firm. This

ratio will give the investors an idea of the survival of the company at economic downturns. It

will help in depicting the leverage of the BHP Billiton and will represent the quantity of the

business funds that come from the creditors and stockholders. The gearing ratios include the

calculation of the interest earned ratio, debt ratio, debt-to-equity ratio and the equity ratio

(Rosemary Peavler, 2018). These all ratios will help to know the suitability of capitalisation of

BHP Billiton.

CALCULATIONS

Debt-to-equity ratio= Total debt / Total Equity

= (30474 / 57258)

= 0.5326

Total debt to total asset ratio = Total debt/ Total Assets

= (30474 / 117006)

= 0.2604

Capitalisation ratio= Long-Term Debt / (Long-Term Debt + Shareholder’s Equity)

= 29233/ (29233 + 57258)

= 0.3380

INTERPRETATIONS

From the above calculations performed and the data gathered BHP Billiton has a current ratio

of 1.85 (Market Watch, 2018) that shows the strong liquidity of the firm that in case of issues it

has sufficient assets that can be converted to cash within 90 days to pay off the current

liabilities in future. The gearing ratios calculated above for NHP Billiton will be useful for the

8

investors and will help in maintaining the consistent dividend policies. Together with this, it can

be drawn out that it will also attract more risk towards the firm as the capital structure of the

firm is highly geared. The debt-to-equity ratio is that key ratio that is set as a financial standard

used to judge BHP Billiton's financial standing. An ideal ratio should be near to 1 but in case of

BHP Billiton, it is 0.53 which depicts that this company is not successful in taking advantage of

the increased profits from the financial leverage of the firm.

Whereas the total debt to total asset ratio is less than 0.5 i.e. it is 0.26 in case of BHP Billiton

that depicts that the majority of the assets are financed by equity. And this ratio is low which

indicates that there is the availability of opportunity with BHP Billiton to borrow at no

significant risk involved in future.

The capitalisation ratio defines the capital structure of BHP Billiton that compares the total debt

with that to the total capitalisation. This ratio depicts the risk such as the risk of insolvency. A

high ratio creates difficulties for the companies to get more loans in future. We have a lower

capitalisation ratio which shows that BHP Billiton can access more loans in future. But this may

not be always true as sometimes a high capitalisation ratio can render an opportunity to reap

high return s on a shareholder's investment due to the tax advantages on borrowings (Morning

Star, 2017).

9

be drawn out that it will also attract more risk towards the firm as the capital structure of the

firm is highly geared. The debt-to-equity ratio is that key ratio that is set as a financial standard

used to judge BHP Billiton's financial standing. An ideal ratio should be near to 1 but in case of

BHP Billiton, it is 0.53 which depicts that this company is not successful in taking advantage of

the increased profits from the financial leverage of the firm.

Whereas the total debt to total asset ratio is less than 0.5 i.e. it is 0.26 in case of BHP Billiton

that depicts that the majority of the assets are financed by equity. And this ratio is low which

indicates that there is the availability of opportunity with BHP Billiton to borrow at no

significant risk involved in future.

The capitalisation ratio defines the capital structure of BHP Billiton that compares the total debt

with that to the total capitalisation. This ratio depicts the risk such as the risk of insolvency. A

high ratio creates difficulties for the companies to get more loans in future. We have a lower

capitalisation ratio which shows that BHP Billiton can access more loans in future. But this may

not be always true as sometimes a high capitalisation ratio can render an opportunity to reap

high return s on a shareholder's investment due to the tax advantages on borrowings (Morning

Star, 2017).

9

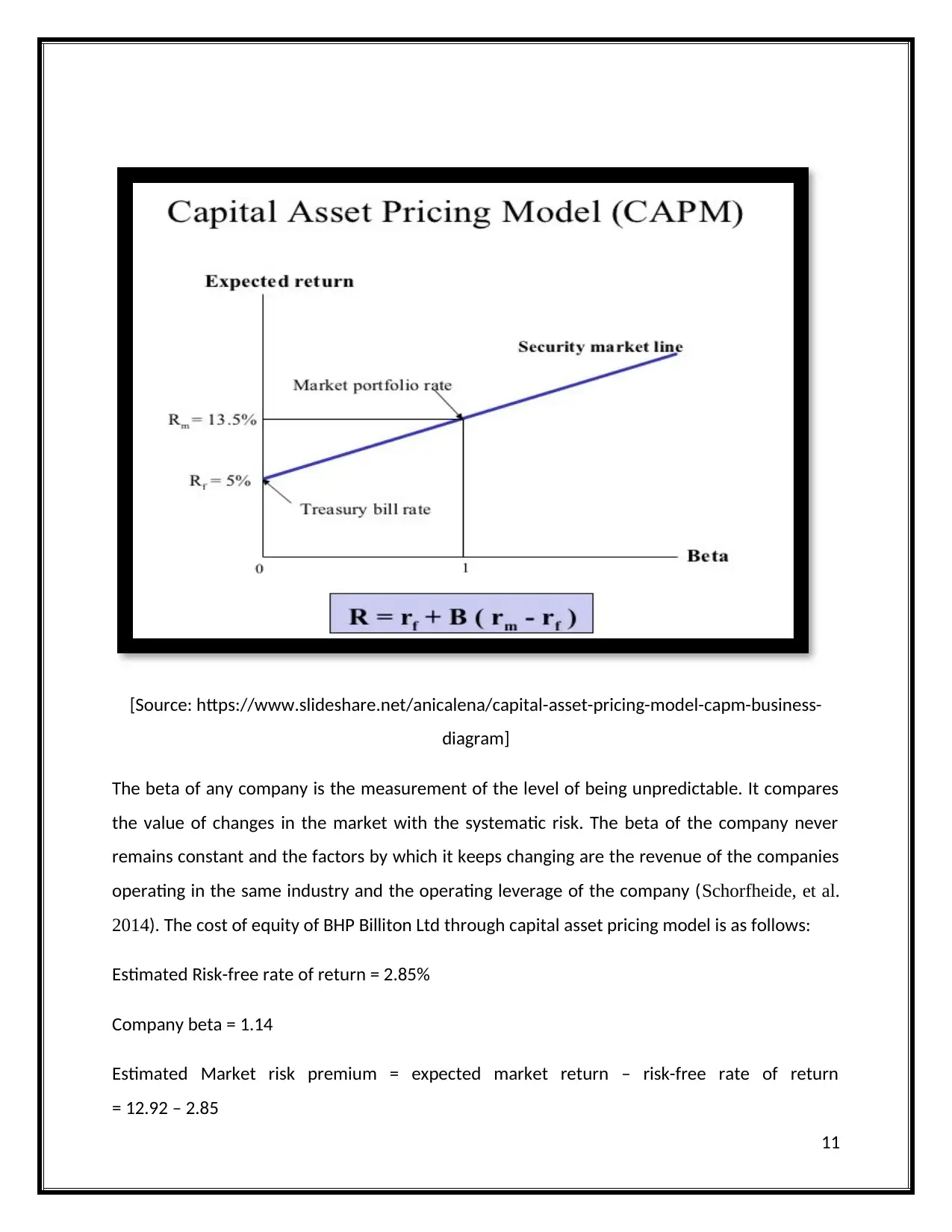

CAPITAL ASSET PRICING MODEL

It represents a relationship between the required rate of return and the systematic risk

associated with an investment. This model is used to describe the linear relationship between

return and risk for securities (Barberis, et al. 2015). This model is widely used for pricing of the

securities which carries higher risk. The formula for calculating the cost of equity through

capital asset pricing model is as follows:

RE= RF + βE (RM – RF)

in which RE= Cost of equity

RF= Risk-free rate

βE= Beta i.e. asset’s exposure to systematic risk

(RM) – RF= Market risk premium

The risk-free rate of return is the rate when the investment is done with no risk at all. There is

no risk of loss of the risk-free rate of return and these instruments can be treasury bills,

government bonds etc. (BHP STOCKS, 2017). The rate of risk-free is important for the capital

asset pricing model as it sets an aim or benchmark, above which the assets of the company

have to perform, only those who carry risk. In practical terms, the risk-free rate of return is not

possible for any market, as this rate is definitely affected by the rate of inflation.

The market risk premium is the difference between the risk-free rate of return and the rate of

return which is expected from the market portfolio (Fama, and French, 2017). It is the

additional rate of return which the investor gets over and above for not investing in the risk-

free asset and for taking the risk. Market risk premium can be calculated as follows:

Market risk premium = expected market return – risk-free rate of return

10

It represents a relationship between the required rate of return and the systematic risk

associated with an investment. This model is used to describe the linear relationship between

return and risk for securities (Barberis, et al. 2015). This model is widely used for pricing of the

securities which carries higher risk. The formula for calculating the cost of equity through

capital asset pricing model is as follows:

RE= RF + βE (RM – RF)

in which RE= Cost of equity

RF= Risk-free rate

βE= Beta i.e. asset’s exposure to systematic risk

(RM) – RF= Market risk premium

The risk-free rate of return is the rate when the investment is done with no risk at all. There is

no risk of loss of the risk-free rate of return and these instruments can be treasury bills,

government bonds etc. (BHP STOCKS, 2017). The rate of risk-free is important for the capital

asset pricing model as it sets an aim or benchmark, above which the assets of the company

have to perform, only those who carry risk. In practical terms, the risk-free rate of return is not

possible for any market, as this rate is definitely affected by the rate of inflation.

The market risk premium is the difference between the risk-free rate of return and the rate of

return which is expected from the market portfolio (Fama, and French, 2017). It is the

additional rate of return which the investor gets over and above for not investing in the risk-

free asset and for taking the risk. Market risk premium can be calculated as follows:

Market risk premium = expected market return – risk-free rate of return

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

[Source: https://www.slideshare.net/anicalena/capital-asset-pricing-model-capm-business-

diagram]

The beta of any company is the measurement of the level of being unpredictable. It compares

the value of changes in the market with the systematic risk. The beta of the company never

remains constant and the factors by which it keeps changing are the revenue of the companies

operating in the same industry and the operating leverage of the company (Schorfheide, et al.

2014). The cost of equity of BHP Billiton Ltd through capital asset pricing model is as follows:

Estimated Risk-free rate of return = 2.85%

Company beta = 1.14

Estimated Market risk premium = expected market return – risk-free rate of return

= 12.92 – 2.85

11

diagram]

The beta of any company is the measurement of the level of being unpredictable. It compares

the value of changes in the market with the systematic risk. The beta of the company never

remains constant and the factors by which it keeps changing are the revenue of the companies

operating in the same industry and the operating leverage of the company (Schorfheide, et al.

2014). The cost of equity of BHP Billiton Ltd through capital asset pricing model is as follows:

Estimated Risk-free rate of return = 2.85%

Company beta = 1.14

Estimated Market risk premium = expected market return – risk-free rate of return

= 12.92 – 2.85

11

= 10.07%

Estimated cost of equity by capital asset pricing model –

= 2.85 + (1.14 * 10.07)

= 14.33%

The estimated cost of equity is 14.33% as derived by using capital asset pricing model. There

can be many shortcomings of following this approach as the company beta may be unrealistic

because of the historical nature of data (BHP RATIOS, 2017). The imperfections of the market

may mislead the investors and cause unsystematic risk. But when the company is suffering from

losses, this approach proves to be very helpful.

12

Estimated cost of equity by capital asset pricing model –

= 2.85 + (1.14 * 10.07)

= 14.33%

The estimated cost of equity is 14.33% as derived by using capital asset pricing model. There

can be many shortcomings of following this approach as the company beta may be unrealistic

because of the historical nature of data (BHP RATIOS, 2017). The imperfections of the market

may mislead the investors and cause unsystematic risk. But when the company is suffering from

losses, this approach proves to be very helpful.

12

RECOMMENDATION

It is recommended for BHP Billiton Ltd that its debt should be reduced to improvise the

weighted average cost of capital. By this, they will be able to increase the shareholder's wealth

and thus the value of the company. With the changes to be done in the total debt and total

equity of the firm, the total value of the company will also increase, it will be seen that the debt

financing is lowered and the equity financing is increased (BHP RATIOS, 2017). But the financing

through equity should not be increased to a very high level as the higher weighted average cost

of capital denotes the higher amount of risk regarding the operations of the company. The

gearing ratios of the companies signify the level of debt in the capital structure of the company,

the debt to equity ratio is 53.26%, which is really high and not a good sign for the company. It

should reduce its debt and increase the financing through equity.

13

It is recommended for BHP Billiton Ltd that its debt should be reduced to improvise the

weighted average cost of capital. By this, they will be able to increase the shareholder's wealth

and thus the value of the company. With the changes to be done in the total debt and total

equity of the firm, the total value of the company will also increase, it will be seen that the debt

financing is lowered and the equity financing is increased (BHP RATIOS, 2017). But the financing

through equity should not be increased to a very high level as the higher weighted average cost

of capital denotes the higher amount of risk regarding the operations of the company. The

gearing ratios of the companies signify the level of debt in the capital structure of the company,

the debt to equity ratio is 53.26%, which is really high and not a good sign for the company. It

should reduce its debt and increase the financing through equity.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From this assignment, it can be concluded that the BHP Billiton Ltd is a strong competitor in its

business of mining. Through the calculations in the assignment, it can be said that the financial

position of the company is relatively stronger when compared to the other companies within

the same industry. By the evaluation of the weighted average cost of capital, it can be said that

the company is operating at a risk because the level of debt financing is high in the capital

structure, which needs to be reduced. In the capital asset pricing model, the estimated cost of

equity is evaluated and the market risk premium was also understood.

14

From this assignment, it can be concluded that the BHP Billiton Ltd is a strong competitor in its

business of mining. Through the calculations in the assignment, it can be said that the financial

position of the company is relatively stronger when compared to the other companies within

the same industry. By the evaluation of the weighted average cost of capital, it can be said that

the company is operating at a risk because the level of debt financing is high in the capital

structure, which needs to be reduced. In the capital asset pricing model, the estimated cost of

equity is evaluated and the market risk premium was also understood.

14

REFERENCES

MARKET PORTFOLIO, 2016 [online available at:

https://www.stock-analysis-on.net/NYSE/Market-Risk-Premium]

BHP Billiton, 2017 [online available at:

https://www.reuters.com/finance/stocks/overview/BHP.AX]

BHP RATIOS, 2017 [online available at: https://au.investing.com/equities/bhp-billiton-

limited-ratios]

BHP STOCKS, 2017[online available at:

https://www.marketwatch.com/investing/stock/bhp/profile]

Fernandez, P., 2015. WACC: Definition, Misconceptions and Errors.

Campbell, T.C., Galpin, N. and Johnson, S.A., 2016. Optimal inside debt compensation

and the value of equity and debt. Journal of Financial Economics, 119(2), pp.336-352.

Billett, M.T., Hribar, P. and Liu, Y., 2015. Shareholder-manager alignment and the cost of

debt.

Goh, B.W., Lim, C.Y., Lobo, G.J. and Tong, Y.H., 2017. Conditional conservatism and debt

versus equity financing. Contemporary Accounting Research, 34(1), pp.216-251.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of Financial Economics, 115(1), pp.1-24.

Fama, E.F. and French, K.R., 2017. International tests of a five-factor asset pricing model.

Journal of Financial Economics, 123(3), pp.441-463.

Schorfheide, F., Song, D. and Yaron, A., 2014. Identifying long-run risks: A bayesian

mixed-frequency approach (No. w20303). National Bureau of Economic Research.

Rosemary Peavler, (2018), The Balance- What Does Gearing Ratio Mean, and How is it

Calculated? Online available at (https://www.thebalance.com/calculating-gearing-ratio-

393228) Last accessed January 24, 2018.

Morning Star, (2017), BHP Billiton PLC- BLT Online available at

(http://tools.morningstar.co.uk/uk/stockreport/default.aspx?

15

MARKET PORTFOLIO, 2016 [online available at:

https://www.stock-analysis-on.net/NYSE/Market-Risk-Premium]

BHP Billiton, 2017 [online available at:

https://www.reuters.com/finance/stocks/overview/BHP.AX]

BHP RATIOS, 2017 [online available at: https://au.investing.com/equities/bhp-billiton-

limited-ratios]

BHP STOCKS, 2017[online available at:

https://www.marketwatch.com/investing/stock/bhp/profile]

Fernandez, P., 2015. WACC: Definition, Misconceptions and Errors.

Campbell, T.C., Galpin, N. and Johnson, S.A., 2016. Optimal inside debt compensation

and the value of equity and debt. Journal of Financial Economics, 119(2), pp.336-352.

Billett, M.T., Hribar, P. and Liu, Y., 2015. Shareholder-manager alignment and the cost of

debt.

Goh, B.W., Lim, C.Y., Lobo, G.J. and Tong, Y.H., 2017. Conditional conservatism and debt

versus equity financing. Contemporary Accounting Research, 34(1), pp.216-251.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of Financial Economics, 115(1), pp.1-24.

Fama, E.F. and French, K.R., 2017. International tests of a five-factor asset pricing model.

Journal of Financial Economics, 123(3), pp.441-463.

Schorfheide, F., Song, D. and Yaron, A., 2014. Identifying long-run risks: A bayesian

mixed-frequency approach (No. w20303). National Bureau of Economic Research.

Rosemary Peavler, (2018), The Balance- What Does Gearing Ratio Mean, and How is it

Calculated? Online available at (https://www.thebalance.com/calculating-gearing-ratio-

393228) Last accessed January 24, 2018.

Morning Star, (2017), BHP Billiton PLC- BLT Online available at

(http://tools.morningstar.co.uk/uk/stockreport/default.aspx?

15

id=0P00007O0M&SecurityToken=0P00007O0M%5D3%5D0%5DE0EXG

%24XLON&ClientFund=0&LanguageId=en-GB&CurrencyId=GBP&UniverseId=E0EXG

%24XLON&BaseCurrencyId=GBP) last accessed January 24, 2018.

Market Watch, (2018), BHP Billiton Ltd ADR online available at

(https://www.marketwatch.com/investing/stock/bhp/profile) last accessed January 24,

2018.

Investing.com, (2017) BHP Billiton Ltd (BHP) income statement. Online available at

(https://au.investing.com/equities/bhp-billiton-limited-income-statement) last accessed

January 24, 2018.

16

%24XLON&ClientFund=0&LanguageId=en-GB&CurrencyId=GBP&UniverseId=E0EXG

%24XLON&BaseCurrencyId=GBP) last accessed January 24, 2018.

Market Watch, (2018), BHP Billiton Ltd ADR online available at

(https://www.marketwatch.com/investing/stock/bhp/profile) last accessed January 24,

2018.

Investing.com, (2017) BHP Billiton Ltd (BHP) income statement. Online available at

(https://au.investing.com/equities/bhp-billiton-limited-income-statement) last accessed

January 24, 2018.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

APPENDIX

17

17

18

19

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.