Perfect Image NZ Ltd: WACC, Portfolio Analysis, Case Study, ACCT 706

VerifiedAdded on 2023/02/01

|14

|3759

|61

Project

AI Summary

This document presents a comprehensive solution to a Managerial Finance assignment focusing on Weighted Average Cost of Capital (WACC) and portfolio analysis, specifically for Perfect Image NZ Ltd. The solution begins with the calculation of WACC, detailing the initial investment, changes in net working capital, and opportunity cost of lost land sale. It then proceeds to determine the cost of equity using the dividend growth model and the cost of debt by calculating the yield to maturity of the company's bonds. The cost of preference shares is also calculated. Subsequently, the document determines the weights of debt, equity, and preference shares to compute the WACC. Additionally, the solution includes a detailed financial analysis, including the assumptions, annual net cash flow estimates, and discounted cash flow analysis to determine the Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index, concluding with a recommendation for the investment in a new plant. The document also analyzes factors affecting the cost of capital. Furthermore, the assignment covers portfolio analysis, providing calculations of average monthly returns, standard deviations, and covariances for different securities. The analysis includes portfolio returns, risks, ratios, and the construction of an investment opportunity set, culminating in the determination of optimal portfolio weights and beta calculations for the securities.

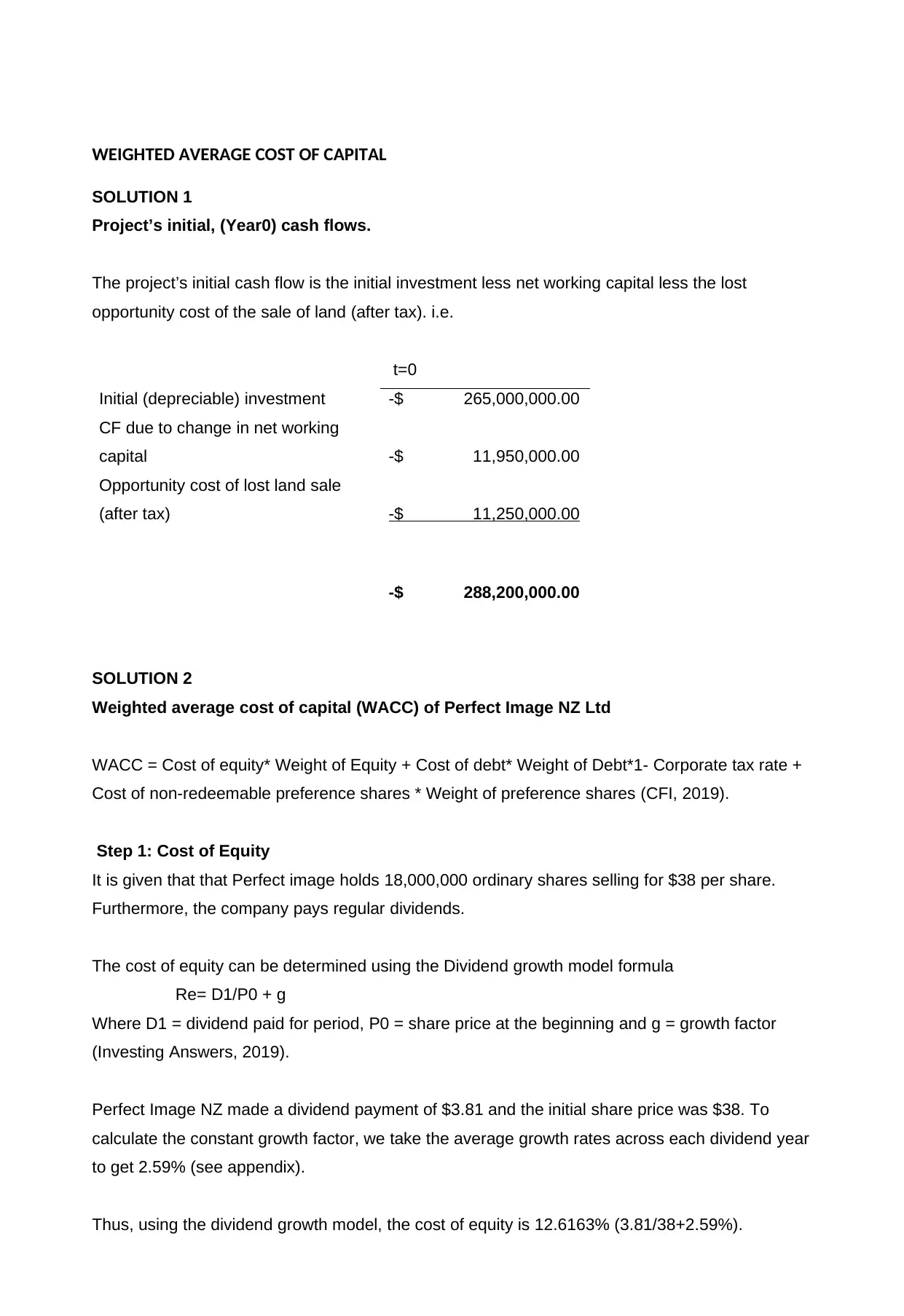

WEIGHTED AVERAGE COST OF CAPITAL

SOLUTION 1

Project’s initial, (Year0) cash flows.

The project’s initial cash flow is the initial investment less net working capital less the lost

opportunity cost of the sale of land (after tax). i.e.

t=0

Initial (depreciable) investment -$ 265,000,000.00

CF due to change in net working

capital -$ 11,950,000.00

Opportunity cost of lost land sale

(after tax) -$ 11,250,000.00

-$ 288,200,000.00

SOLUTION 2

Weighted average cost of capital (WACC) of Perfect Image NZ Ltd

WACC = Cost of equity* Weight of Equity + Cost of debt* Weight of Debt*1- Corporate tax rate +

Cost of non-redeemable preference shares * Weight of preference shares (CFI, 2019).

Step 1: Cost of Equity

It is given that that Perfect image holds 18,000,000 ordinary shares selling for $38 per share.

Furthermore, the company pays regular dividends.

The cost of equity can be determined using the Dividend growth model formula

Re= D1/P0 + g

Where D1 = dividend paid for period, P0 = share price at the beginning and g = growth factor

(Investing Answers, 2019).

Perfect Image NZ made a dividend payment of $3.81 and the initial share price was $38. To

calculate the constant growth factor, we take the average growth rates across each dividend year

to get 2.59% (see appendix).

Thus, using the dividend growth model, the cost of equity is 12.6163% (3.81/38+2.59%).

SOLUTION 1

Project’s initial, (Year0) cash flows.

The project’s initial cash flow is the initial investment less net working capital less the lost

opportunity cost of the sale of land (after tax). i.e.

t=0

Initial (depreciable) investment -$ 265,000,000.00

CF due to change in net working

capital -$ 11,950,000.00

Opportunity cost of lost land sale

(after tax) -$ 11,250,000.00

-$ 288,200,000.00

SOLUTION 2

Weighted average cost of capital (WACC) of Perfect Image NZ Ltd

WACC = Cost of equity* Weight of Equity + Cost of debt* Weight of Debt*1- Corporate tax rate +

Cost of non-redeemable preference shares * Weight of preference shares (CFI, 2019).

Step 1: Cost of Equity

It is given that that Perfect image holds 18,000,000 ordinary shares selling for $38 per share.

Furthermore, the company pays regular dividends.

The cost of equity can be determined using the Dividend growth model formula

Re= D1/P0 + g

Where D1 = dividend paid for period, P0 = share price at the beginning and g = growth factor

(Investing Answers, 2019).

Perfect Image NZ made a dividend payment of $3.81 and the initial share price was $38. To

calculate the constant growth factor, we take the average growth rates across each dividend year

to get 2.59% (see appendix).

Thus, using the dividend growth model, the cost of equity is 12.6163% (3.81/38+2.59%).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

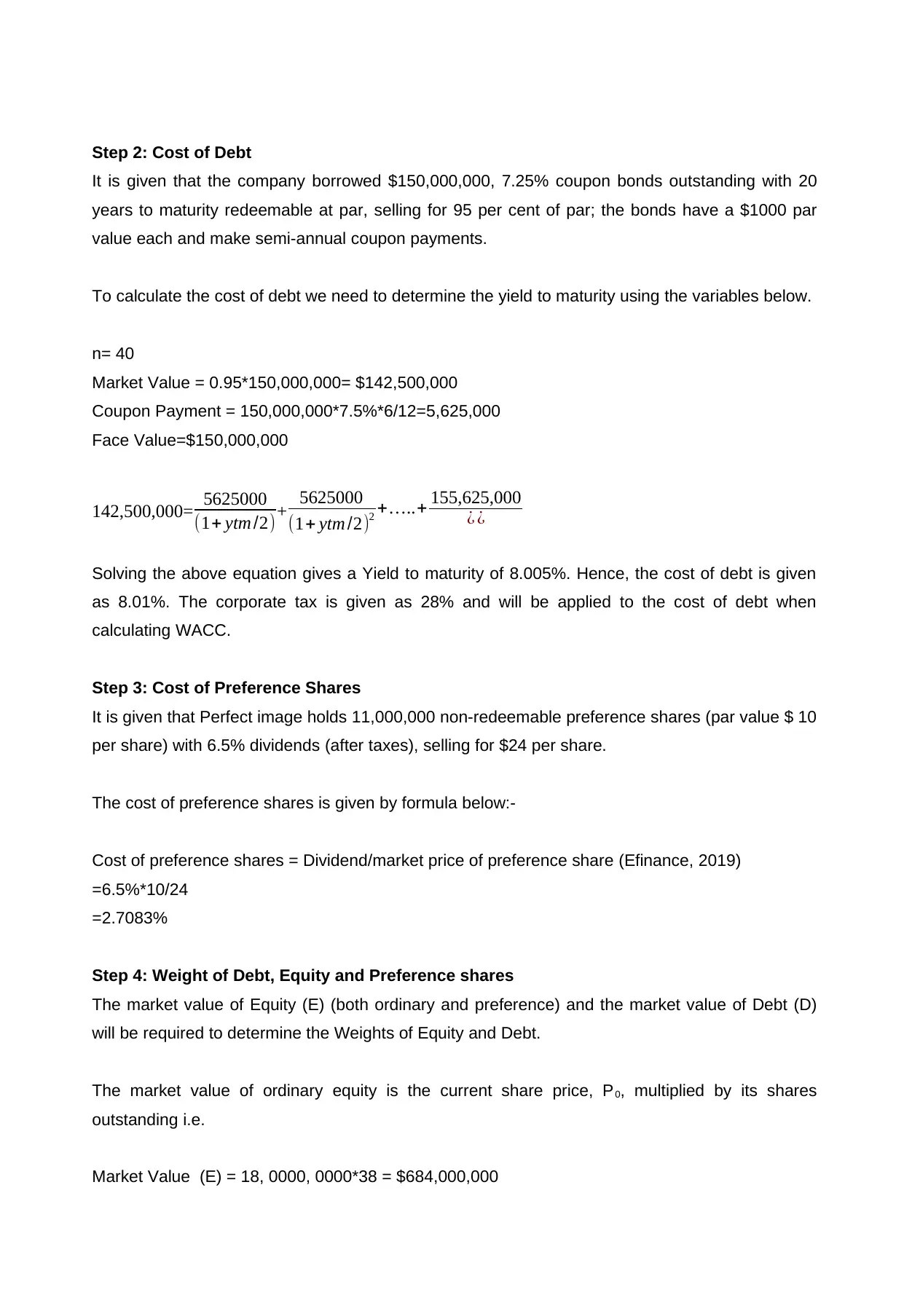

Step 2: Cost of Debt

It is given that the company borrowed $150,000,000, 7.25% coupon bonds outstanding with 20

years to maturity redeemable at par, selling for 95 per cent of par; the bonds have a $1000 par

value each and make semi-annual coupon payments.

To calculate the cost of debt we need to determine the yield to maturity using the variables below.

n= 40

Market Value = 0.95*150,000,000= $142,500,000

Coupon Payment = 150,000,000*7.5%*6/12=5,625,000

Face Value=$150,000,000

142,500,000= 5625000

(1+ ytm /2)+ 5625000

(1+ ytm /2)2 + …..+ 155,625,000

¿ ¿

Solving the above equation gives a Yield to maturity of 8.005%. Hence, the cost of debt is given

as 8.01%. The corporate tax is given as 28% and will be applied to the cost of debt when

calculating WACC.

Step 3: Cost of Preference Shares

It is given that Perfect image holds 11,000,000 non-redeemable preference shares (par value $ 10

per share) with 6.5% dividends (after taxes), selling for $24 per share.

The cost of preference shares is given by formula below:-

Cost of preference shares = Dividend/market price of preference share (Efinance, 2019)

=6.5%*10/24

=2.7083%

Step 4: Weight of Debt, Equity and Preference shares

The market value of Equity (E) (both ordinary and preference) and the market value of Debt (D)

will be required to determine the Weights of Equity and Debt.

The market value of ordinary equity is the current share price, P0, multiplied by its shares

outstanding i.e.

Market Value (E) = 18, 0000, 0000*38 = $684,000,000

It is given that the company borrowed $150,000,000, 7.25% coupon bonds outstanding with 20

years to maturity redeemable at par, selling for 95 per cent of par; the bonds have a $1000 par

value each and make semi-annual coupon payments.

To calculate the cost of debt we need to determine the yield to maturity using the variables below.

n= 40

Market Value = 0.95*150,000,000= $142,500,000

Coupon Payment = 150,000,000*7.5%*6/12=5,625,000

Face Value=$150,000,000

142,500,000= 5625000

(1+ ytm /2)+ 5625000

(1+ ytm /2)2 + …..+ 155,625,000

¿ ¿

Solving the above equation gives a Yield to maturity of 8.005%. Hence, the cost of debt is given

as 8.01%. The corporate tax is given as 28% and will be applied to the cost of debt when

calculating WACC.

Step 3: Cost of Preference Shares

It is given that Perfect image holds 11,000,000 non-redeemable preference shares (par value $ 10

per share) with 6.5% dividends (after taxes), selling for $24 per share.

The cost of preference shares is given by formula below:-

Cost of preference shares = Dividend/market price of preference share (Efinance, 2019)

=6.5%*10/24

=2.7083%

Step 4: Weight of Debt, Equity and Preference shares

The market value of Equity (E) (both ordinary and preference) and the market value of Debt (D)

will be required to determine the Weights of Equity and Debt.

The market value of ordinary equity is the current share price, P0, multiplied by its shares

outstanding i.e.

Market Value (E) = 18, 0000, 0000*38 = $684,000,000

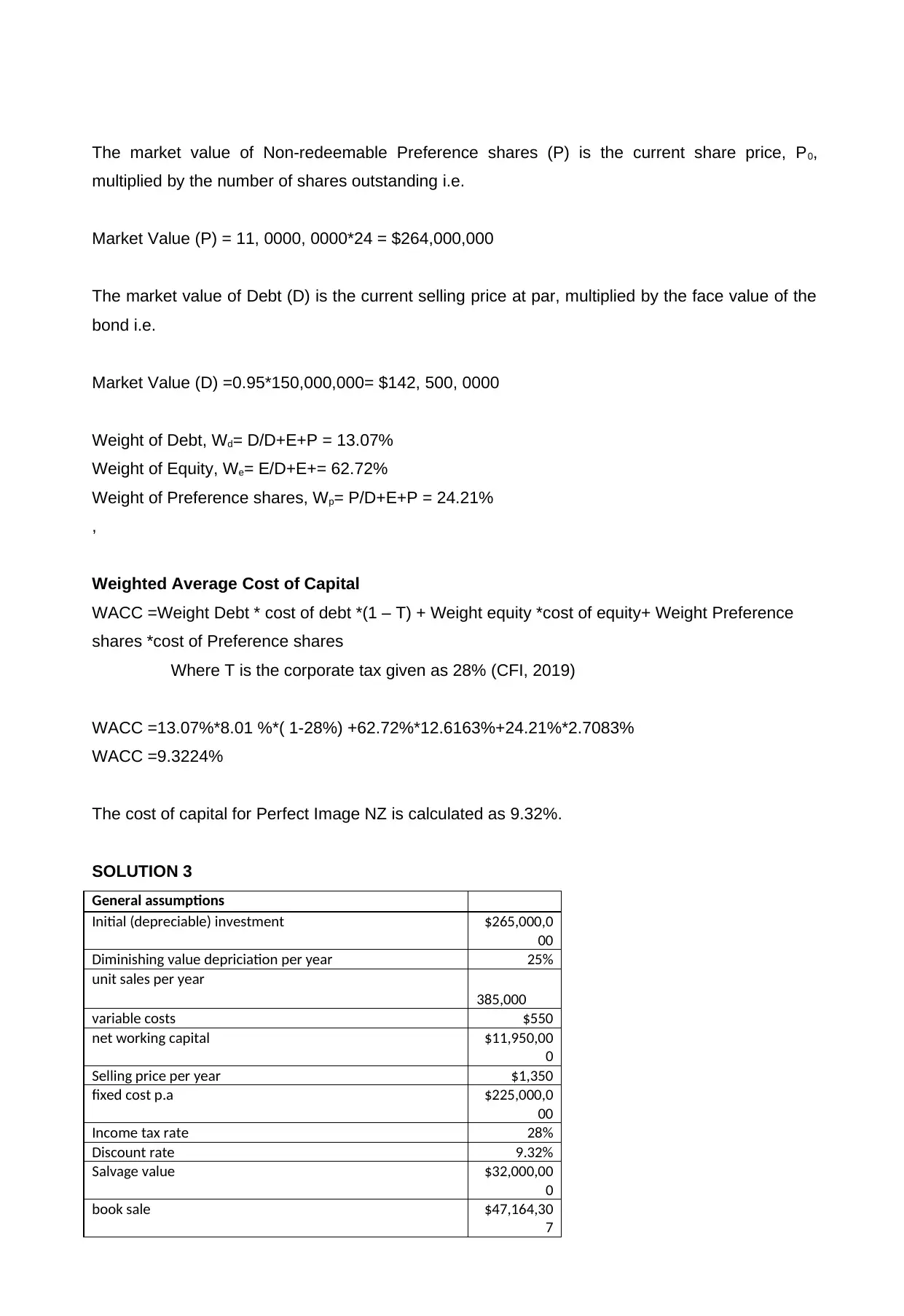

The market value of Non-redeemable Preference shares (P) is the current share price, P0,

multiplied by the number of shares outstanding i.e.

Market Value (P) = 11, 0000, 0000*24 = $264,000,000

The market value of Debt (D) is the current selling price at par, multiplied by the face value of the

bond i.e.

Market Value (D) =0.95*150,000,000= $142, 500, 0000

Weight of Debt, Wd= D/D+E+P = 13.07%

Weight of Equity, We= E/D+E+= 62.72%

Weight of Preference shares, Wp= P/D+E+P = 24.21%

,

Weighted Average Cost of Capital

WACC =Weight Debt * cost of debt *(1 – T) + Weight equity *cost of equity+ Weight Preference

shares *cost of Preference shares

Where T is the corporate tax given as 28% (CFI, 2019)

WACC =13.07%*8.01 %*( 1-28%) +62.72%*12.6163%+24.21%*2.7083%

WACC =9.3224%

The cost of capital for Perfect Image NZ is calculated as 9.32%.

SOLUTION 3

General assumptions

Initial (depreciable) investment $265,000,0

00

Diminishing value depriciation per year 25%

unit sales per year

385,000

variable costs $550

net working capital $11,950,00

0

Selling price per year $1,350

fixed cost p.a $225,000,0

00

Income tax rate 28%

Discount rate 9.32%

Salvage value $32,000,00

0

book sale $47,164,30

7

multiplied by the number of shares outstanding i.e.

Market Value (P) = 11, 0000, 0000*24 = $264,000,000

The market value of Debt (D) is the current selling price at par, multiplied by the face value of the

bond i.e.

Market Value (D) =0.95*150,000,000= $142, 500, 0000

Weight of Debt, Wd= D/D+E+P = 13.07%

Weight of Equity, We= E/D+E+= 62.72%

Weight of Preference shares, Wp= P/D+E+P = 24.21%

,

Weighted Average Cost of Capital

WACC =Weight Debt * cost of debt *(1 – T) + Weight equity *cost of equity+ Weight Preference

shares *cost of Preference shares

Where T is the corporate tax given as 28% (CFI, 2019)

WACC =13.07%*8.01 %*( 1-28%) +62.72%*12.6163%+24.21%*2.7083%

WACC =9.3224%

The cost of capital for Perfect Image NZ is calculated as 9.32%.

SOLUTION 3

General assumptions

Initial (depreciable) investment $265,000,0

00

Diminishing value depriciation per year 25%

unit sales per year

385,000

variable costs $550

net working capital $11,950,00

0

Selling price per year $1,350

fixed cost p.a $225,000,0

00

Income tax rate 28%

Discount rate 9.32%

Salvage value $32,000,00

0

book sale $47,164,30

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

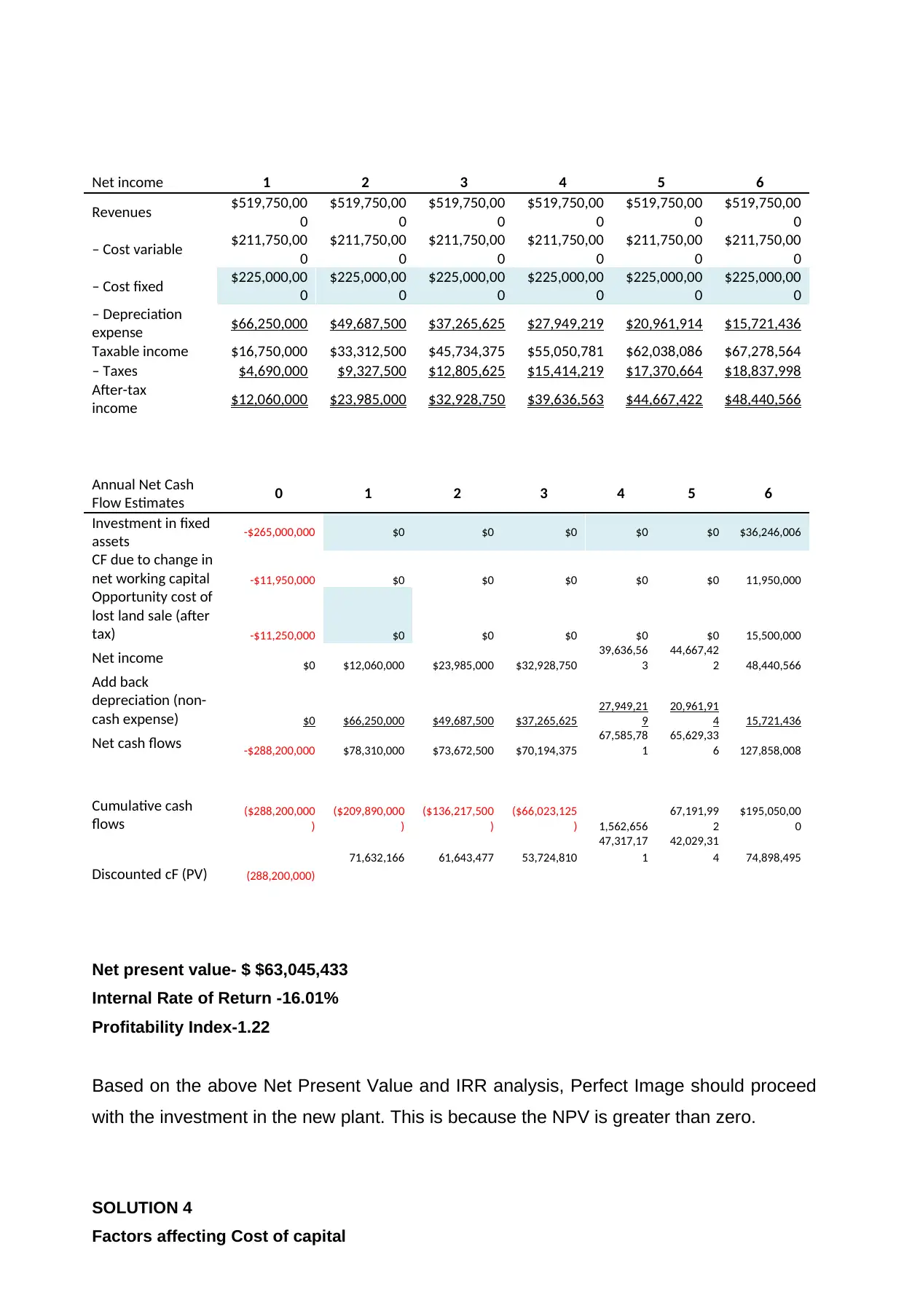

Net income 1 2 3 4 5 6

Revenues $519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

– Cost variable $211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

– Cost fixed $225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

– Depreciation

expense $66,250,000 $49,687,500 $37,265,625 $27,949,219 $20,961,914 $15,721,436

Taxable income $16,750,000 $33,312,500 $45,734,375 $55,050,781 $62,038,086 $67,278,564

– Taxes $4,690,000 $9,327,500 $12,805,625 $15,414,219 $17,370,664 $18,837,998

After-tax

income $12,060,000 $23,985,000 $32,928,750 $39,636,563 $44,667,422 $48,440,566

Annual Net Cash

Flow Estimates 0 1 2 3 4 5 6

Investment in fixed

assets -$265,000,000 $0 $0 $0 $0 $0 $36,246,006

CF due to change in

net working capital -$11,950,000 $0 $0 $0 $0 $0 11,950,000

Opportunity cost of

lost land sale (after

tax) -$11,250,000 $0 $0 $0 $0 $0 15,500,000

Net income $0 $12,060,000 $23,985,000 $32,928,750

39,636,56

3

44,667,42

2 48,440,566

Add back

depreciation (non-

cash expense) $0 $66,250,000 $49,687,500 $37,265,625

27,949,21

9

20,961,91

4 15,721,436

Net cash flows -$288,200,000 $78,310,000 $73,672,500 $70,194,375

67,585,78

1

65,629,33

6 127,858,008

Cumulative cash

flows ($288,200,000

)

($209,890,000

)

($136,217,500

)

($66,023,125

) 1,562,656

67,191,99

2

$195,050,00

0

Discounted cF (PV) (288,200,000)

71,632,166 61,643,477 53,724,810

47,317,17

1

42,029,31

4 74,898,495

Net present value- $ $63,045,433

Internal Rate of Return -16.01%

Profitability Index-1.22

Based on the above Net Present Value and IRR analysis, Perfect Image should proceed

with the investment in the new plant. This is because the NPV is greater than zero.

SOLUTION 4

Factors affecting Cost of capital

Revenues $519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

$519,750,00

0

– Cost variable $211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

$211,750,00

0

– Cost fixed $225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

$225,000,00

0

– Depreciation

expense $66,250,000 $49,687,500 $37,265,625 $27,949,219 $20,961,914 $15,721,436

Taxable income $16,750,000 $33,312,500 $45,734,375 $55,050,781 $62,038,086 $67,278,564

– Taxes $4,690,000 $9,327,500 $12,805,625 $15,414,219 $17,370,664 $18,837,998

After-tax

income $12,060,000 $23,985,000 $32,928,750 $39,636,563 $44,667,422 $48,440,566

Annual Net Cash

Flow Estimates 0 1 2 3 4 5 6

Investment in fixed

assets -$265,000,000 $0 $0 $0 $0 $0 $36,246,006

CF due to change in

net working capital -$11,950,000 $0 $0 $0 $0 $0 11,950,000

Opportunity cost of

lost land sale (after

tax) -$11,250,000 $0 $0 $0 $0 $0 15,500,000

Net income $0 $12,060,000 $23,985,000 $32,928,750

39,636,56

3

44,667,42

2 48,440,566

Add back

depreciation (non-

cash expense) $0 $66,250,000 $49,687,500 $37,265,625

27,949,21

9

20,961,91

4 15,721,436

Net cash flows -$288,200,000 $78,310,000 $73,672,500 $70,194,375

67,585,78

1

65,629,33

6 127,858,008

Cumulative cash

flows ($288,200,000

)

($209,890,000

)

($136,217,500

)

($66,023,125

) 1,562,656

67,191,99

2

$195,050,00

0

Discounted cF (PV) (288,200,000)

71,632,166 61,643,477 53,724,810

47,317,17

1

42,029,31

4 74,898,495

Net present value- $ $63,045,433

Internal Rate of Return -16.01%

Profitability Index-1.22

Based on the above Net Present Value and IRR analysis, Perfect Image should proceed

with the investment in the new plant. This is because the NPV is greater than zero.

SOLUTION 4

Factors affecting Cost of capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Market opportunities-Increased market opportunities increase the need for capital by

organizations, which in turn increase the cost of capital (EFINANCE, 2019).

Risk- An investor would require a higher cost of capital for projects that are considered

riskier than others. This higher cost will be commensurate with the level of risk taken. In

other words, riskier projects have a higher cost of capital (EFINANCE, 2019).

Dividend policy- If a company retains more of its profits or does not declare dividends

regularly, then it will be adding capital to the cost of equity. This will affect the cost of

capital (EFINANCE, 2019).

Capital Structure- The capital structure policy of a company will affect its cost of capital as

these have an effect on the weights (EFINANCE, 2019).

organizations, which in turn increase the cost of capital (EFINANCE, 2019).

Risk- An investor would require a higher cost of capital for projects that are considered

riskier than others. This higher cost will be commensurate with the level of risk taken. In

other words, riskier projects have a higher cost of capital (EFINANCE, 2019).

Dividend policy- If a company retains more of its profits or does not declare dividends

regularly, then it will be adding capital to the cost of equity. This will affect the cost of

capital (EFINANCE, 2019).

Capital Structure- The capital structure policy of a company will affect its cost of capital as

these have an effect on the weights (EFINANCE, 2019).

PORTFOLIO ANALYSIS

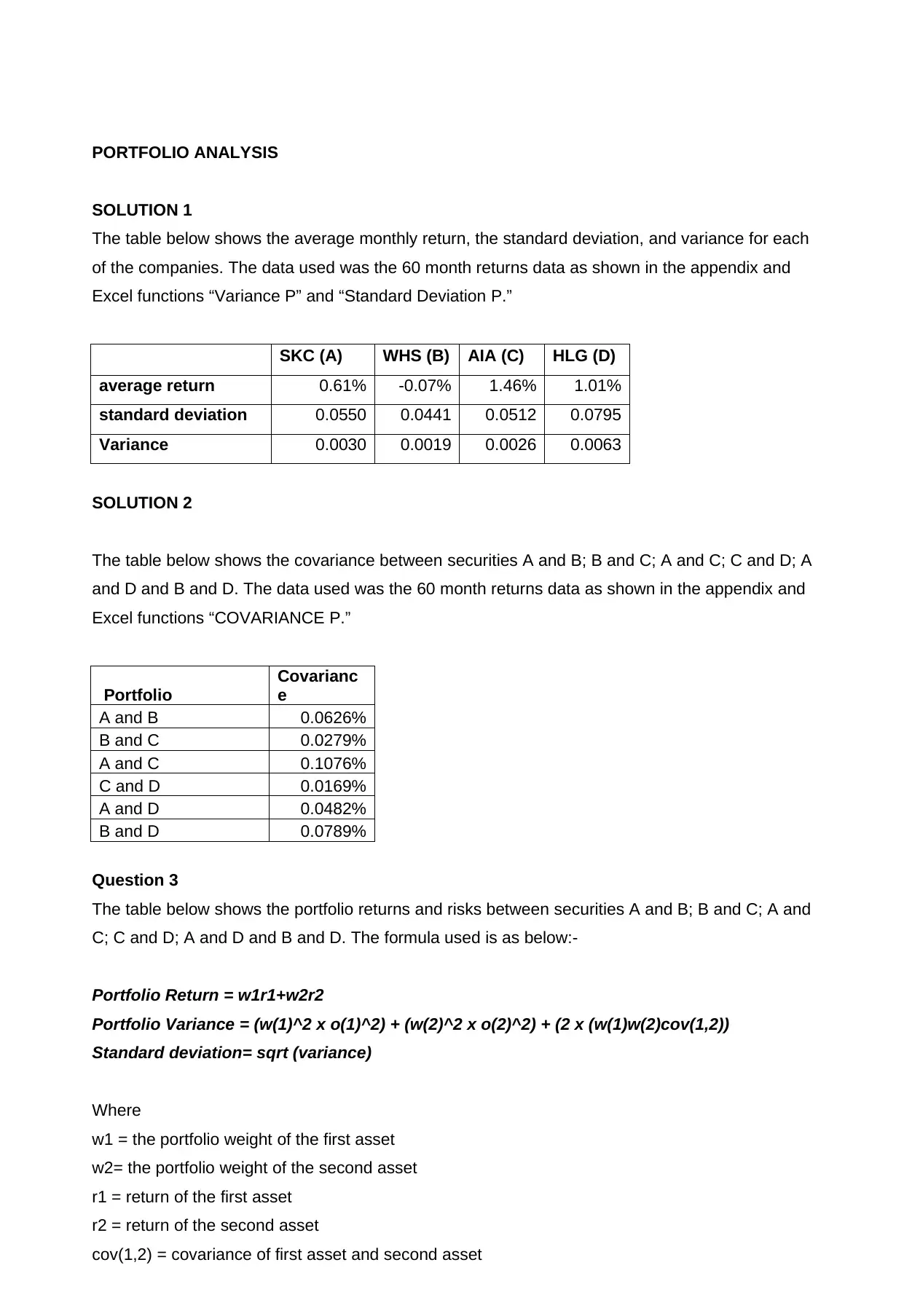

SOLUTION 1

The table below shows the average monthly return, the standard deviation, and variance for each

of the companies. The data used was the 60 month returns data as shown in the appendix and

Excel functions “Variance P” and “Standard Deviation P.”

SKC (A) WHS (B) AIA (C) HLG (D)

average return 0.61% -0.07% 1.46% 1.01%

standard deviation 0.0550 0.0441 0.0512 0.0795

Variance 0.0030 0.0019 0.0026 0.0063

SOLUTION 2

The table below shows the covariance between securities A and B; B and C; A and C; C and D; A

and D and B and D. The data used was the 60 month returns data as shown in the appendix and

Excel functions “COVARIANCE P.”

Portfolio

Covarianc

e

A and B 0.0626%

B and C 0.0279%

A and C 0.1076%

C and D 0.0169%

A and D 0.0482%

B and D 0.0789%

Question 3

The table below shows the portfolio returns and risks between securities A and B; B and C; A and

C; C and D; A and D and B and D. The formula used is as below:-

Portfolio Return = w1r1+w2r2

Portfolio Variance = (w(1)^2 x o(1)^2) + (w(2)^2 x o(2)^2) + (2 x (w(1)w(2)cov(1,2))

Standard deviation= sqrt (variance)

Where

w1 = the portfolio weight of the first asset

w2= the portfolio weight of the second asset

r1 = return of the first asset

r2 = return of the second asset

cov(1,2) = covariance of first asset and second asset

SOLUTION 1

The table below shows the average monthly return, the standard deviation, and variance for each

of the companies. The data used was the 60 month returns data as shown in the appendix and

Excel functions “Variance P” and “Standard Deviation P.”

SKC (A) WHS (B) AIA (C) HLG (D)

average return 0.61% -0.07% 1.46% 1.01%

standard deviation 0.0550 0.0441 0.0512 0.0795

Variance 0.0030 0.0019 0.0026 0.0063

SOLUTION 2

The table below shows the covariance between securities A and B; B and C; A and C; C and D; A

and D and B and D. The data used was the 60 month returns data as shown in the appendix and

Excel functions “COVARIANCE P.”

Portfolio

Covarianc

e

A and B 0.0626%

B and C 0.0279%

A and C 0.1076%

C and D 0.0169%

A and D 0.0482%

B and D 0.0789%

Question 3

The table below shows the portfolio returns and risks between securities A and B; B and C; A and

C; C and D; A and D and B and D. The formula used is as below:-

Portfolio Return = w1r1+w2r2

Portfolio Variance = (w(1)^2 x o(1)^2) + (w(2)^2 x o(2)^2) + (2 x (w(1)w(2)cov(1,2))

Standard deviation= sqrt (variance)

Where

w1 = the portfolio weight of the first asset

w2= the portfolio weight of the second asset

r1 = return of the first asset

r2 = return of the second asset

cov(1,2) = covariance of first asset and second asset

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

o1 = the standard deviation of the first asset

o2 = the standard deviation of the second asset (Investopedia, 2019)

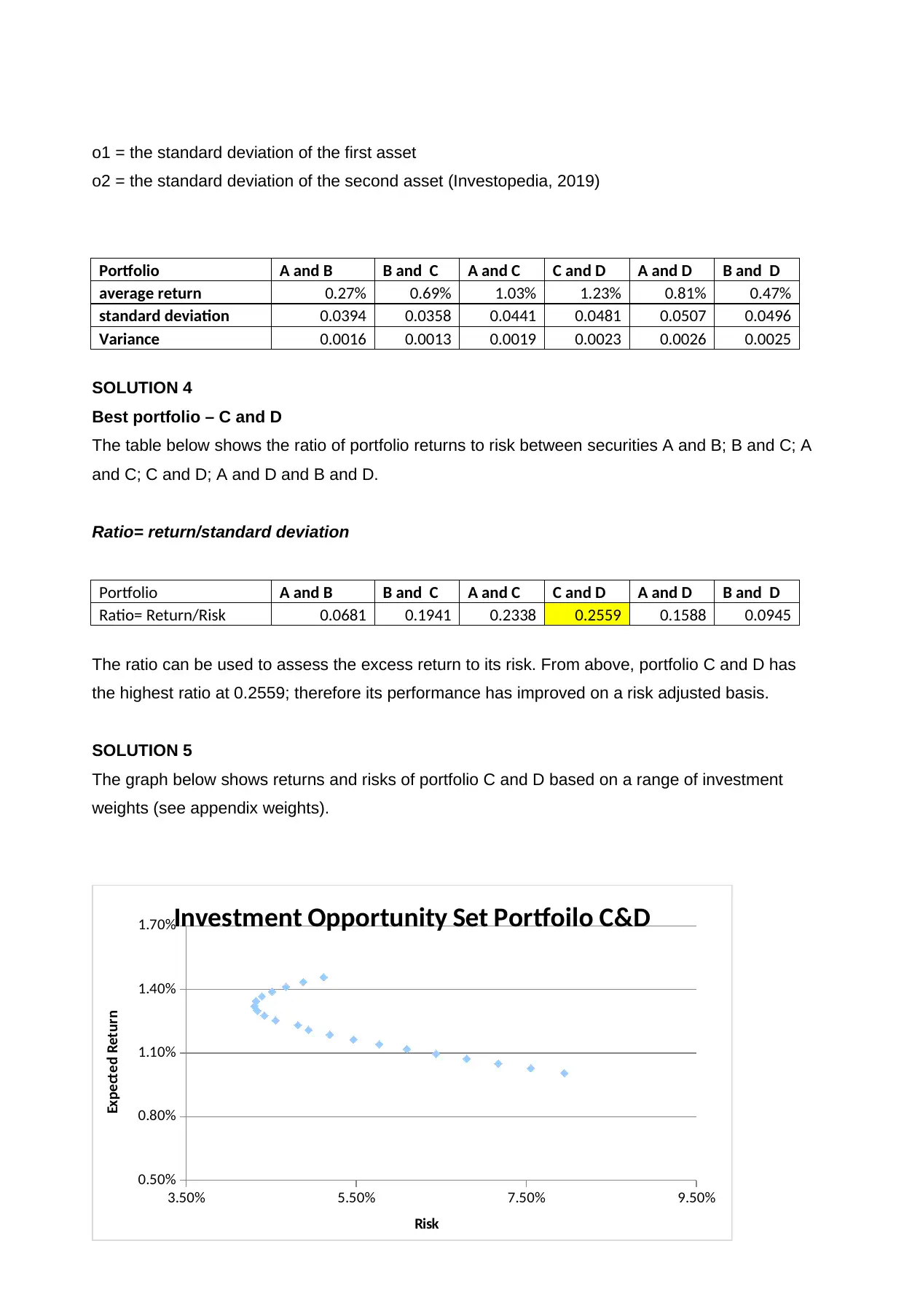

Portfolio A and B B and C A and C C and D A and D B and D

average return 0.27% 0.69% 1.03% 1.23% 0.81% 0.47%

standard deviation 0.0394 0.0358 0.0441 0.0481 0.0507 0.0496

Variance 0.0016 0.0013 0.0019 0.0023 0.0026 0.0025

SOLUTION 4

Best portfolio – C and D

The table below shows the ratio of portfolio returns to risk between securities A and B; B and C; A

and C; C and D; A and D and B and D.

Ratio= return/standard deviation

Portfolio A and B B and C A and C C and D A and D B and D

Ratio= Return/Risk 0.0681 0.1941 0.2338 0.2559 0.1588 0.0945

The ratio can be used to assess the excess return to its risk. From above, portfolio C and D has

the highest ratio at 0.2559; therefore its performance has improved on a risk adjusted basis.

SOLUTION 5

The graph below shows returns and risks of portfolio C and D based on a range of investment

weights (see appendix weights).

3.50% 5.50% 7.50% 9.50%

0.50%

0.80%

1.10%

1.40%

1.70%Investment Opportunity Set Portfoilo C&D

Risk

Expected Return

o2 = the standard deviation of the second asset (Investopedia, 2019)

Portfolio A and B B and C A and C C and D A and D B and D

average return 0.27% 0.69% 1.03% 1.23% 0.81% 0.47%

standard deviation 0.0394 0.0358 0.0441 0.0481 0.0507 0.0496

Variance 0.0016 0.0013 0.0019 0.0023 0.0026 0.0025

SOLUTION 4

Best portfolio – C and D

The table below shows the ratio of portfolio returns to risk between securities A and B; B and C; A

and C; C and D; A and D and B and D.

Ratio= return/standard deviation

Portfolio A and B B and C A and C C and D A and D B and D

Ratio= Return/Risk 0.0681 0.1941 0.2338 0.2559 0.1588 0.0945

The ratio can be used to assess the excess return to its risk. From above, portfolio C and D has

the highest ratio at 0.2559; therefore its performance has improved on a risk adjusted basis.

SOLUTION 5

The graph below shows returns and risks of portfolio C and D based on a range of investment

weights (see appendix weights).

3.50% 5.50% 7.50% 9.50%

0.50%

0.80%

1.10%

1.40%

1.70%Investment Opportunity Set Portfoilo C&D

Risk

Expected Return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The efficient frontier is the region in the graph where the portfolio expected returns are above

1.32%. This is the point where the portfolio offers the highest returns for the minimum level of risk

at 4.39%.

That is at weights of 75% invested stock AIA and 25% invested in stock D (HLG, the portfolio will

be at minimum risk of 4.39%. Therefore, an investor should invest in a portfolio with increasing

weights of stock C (AIA).

SOLUTION 6

Betas

The table below shows the betas for the four securities. The beta was calculated by regressing

the returns of each of the company on the returns for the S&P/NZX50 Index

SKC WHS AIA HLG NZ50

Beta 1.3461 0.3666 1.1971 0.6586 1.0000

A beta coefficient is a measure of the volatility in comparison to the unsystematic risk of the entire

market. A beta <1.0 means that the security is less volatile than the market. A beta >1.0 means

that the security is more volatile than the market. The amount of Debt will affect a company’s beta.

The industry the company is in may also affect the beta of the stock (Investopedia, 2019).

1.32%. This is the point where the portfolio offers the highest returns for the minimum level of risk

at 4.39%.

That is at weights of 75% invested stock AIA and 25% invested in stock D (HLG, the portfolio will

be at minimum risk of 4.39%. Therefore, an investor should invest in a portfolio with increasing

weights of stock C (AIA).

SOLUTION 6

Betas

The table below shows the betas for the four securities. The beta was calculated by regressing

the returns of each of the company on the returns for the S&P/NZX50 Index

SKC WHS AIA HLG NZ50

Beta 1.3461 0.3666 1.1971 0.6586 1.0000

A beta coefficient is a measure of the volatility in comparison to the unsystematic risk of the entire

market. A beta <1.0 means that the security is less volatile than the market. A beta >1.0 means

that the security is more volatile than the market. The amount of Debt will affect a company’s beta.

The industry the company is in may also affect the beta of the stock (Investopedia, 2019).

REFERENCES

CFI, 2019. Definition of WACC. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/what-is-wacc-formula/

Efinance, 2019. Cost of Preference Share Capital. [Online]

Available at: https://efinancemanagement.com/investment-decisions/cost-of-preference-share-capital

EFINANCE, 2019. Factors Affecting Cost of Capital. [Online]

Available at: https://efinancemanagement.com/investment-decisions/factors-affecting-cost-of-capital

Investing Answers, 2019. Gordon Growth Model. [Online]

Available at: https://investinganswers.com/financial-dictionary/income-dividends/gordon-growth-model-

5270

Investopedia, 2019. How can I Measure Portfolio Variance?. [Online]

Available at: https://www.investopedia.com/ask/answers/071515/how-can-i-measure-portfolio-

variance.asp

Investopedia, 2019. What Beta Means When Considering a Stock's Risk. [Online]

Available at: https://www.investopedia.com/investing/beta-know-risk/

CFI, 2019. Definition of WACC. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/what-is-wacc-formula/

Efinance, 2019. Cost of Preference Share Capital. [Online]

Available at: https://efinancemanagement.com/investment-decisions/cost-of-preference-share-capital

EFINANCE, 2019. Factors Affecting Cost of Capital. [Online]

Available at: https://efinancemanagement.com/investment-decisions/factors-affecting-cost-of-capital

Investing Answers, 2019. Gordon Growth Model. [Online]

Available at: https://investinganswers.com/financial-dictionary/income-dividends/gordon-growth-model-

5270

Investopedia, 2019. How can I Measure Portfolio Variance?. [Online]

Available at: https://www.investopedia.com/ask/answers/071515/how-can-i-measure-portfolio-

variance.asp

Investopedia, 2019. What Beta Means When Considering a Stock's Risk. [Online]

Available at: https://www.investopedia.com/investing/beta-know-risk/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

Average growth returns

Year (-4) ($) Year (-3)

($)

Year (-2)

($)

Year (-1)

($)

Year

(0) ($)

di 3.44 3.54 3.62 3.71 3.81

gi - 2.91% 2.26% 2.49% 2.70%

average 2.59%

Book sale value = Cost of plant less depreciable value at time 6

Monthly Return

Adj close Monthly Return

Date SKC WHS AIA HLG NZ50 SKC WHS AIA HLG NZ50

2/28/2019 3.87 2.09 8.03 4.69 9,844.95 5.40% 3.81% 4.76% 13.01% 5.58%

1/31/2019 3.67 2.01 7.66 4.15 9,325.03 -1.82% 2.44% 5.71% 3.75% 3.78%

12/31/2018 3.74 1.97 7.25 4.00 8,985.34 8.17% 0.00% 2.37% -4.31% 1.98%

11/30/2018 3.46 1.97 7.08 4.18 8,811.27 -1.39% -3.30% -0.28% -25.49% -0.14%

10/31/2018 3.51 2.03 7.10 5.61 8,823.54 -6.01% 0.95% 4.58% -4.75% 0.81%

9/30/2018 3.73 2.01 6.79 5.89 8,752.31 -4.49% 1.94% -4.25% 0.68% -6.40%

8/31/2018 3.91 1.97 7.09 5.85 9,351.06 1.17% 0.98% 2.17% -7.00% 0.41%

7/31/2018 3.86 1.96 6.94 6.29 9,313.20 2.53% 0.99% 7.04% 23.09% 4.38%

6/30/2018 3.77 1.94 6.48 5.11 8,922.09 -1.98% -1.94% -1.55% 7.58% -0.24%

5/31/2018 3.84 1.97 6.59 4.75 8,943.13 1.25% 1.48% 2.73% 8.45% 3.28%

4/30/2018 3.79 1.95 6.41 4.38 8,658.79 -1.48% 0.50% 3.45% -4.16% 2.55%

3/31/2018 3.85 1.94 6.20 4.57 8,443.58 6.58% 5.38% 6.09% -9.50% 1.50%

2/28/2018 3.61 1.84 5.84 5.05 8,319.07 0.00% 0.00% -5.12% 8.84% -0.65%

1/31/2018 3.61 1.84 6.16 4.64 8,373.82 -6.02% -2.43% -3.66% 8.92% -0.81%

12/31/2017 3.84 1.88 6.39 4.26 8,442.01 0.00% -0.96% 3.32% 7.85% 0.52%

11/30/2017 3.84 1.90 6.19 3.95 8,398.08 5.06% 4.92% 1.57% 18.26% 2.58%

10/31/2017 3.66 1.81 6.09 3.34 8,186.82 1.54% -3.32% 4.11% 0.00% 0.50%

9/30/2017 3.60 1.87 5.85 3.34 8,146.34 3.73% -3.21% -3.26% -0.30% 2.72%

8/31/2017 3.47 1.94 6.05 3.35 7,930.40 1.41% 3.32% -5.14% 2.45% 1.45%

7/31/2017 3.43 1.87 6.37 3.27 7,817.10 -5.60% -2.31% -2.33% 5.48% 1.60%

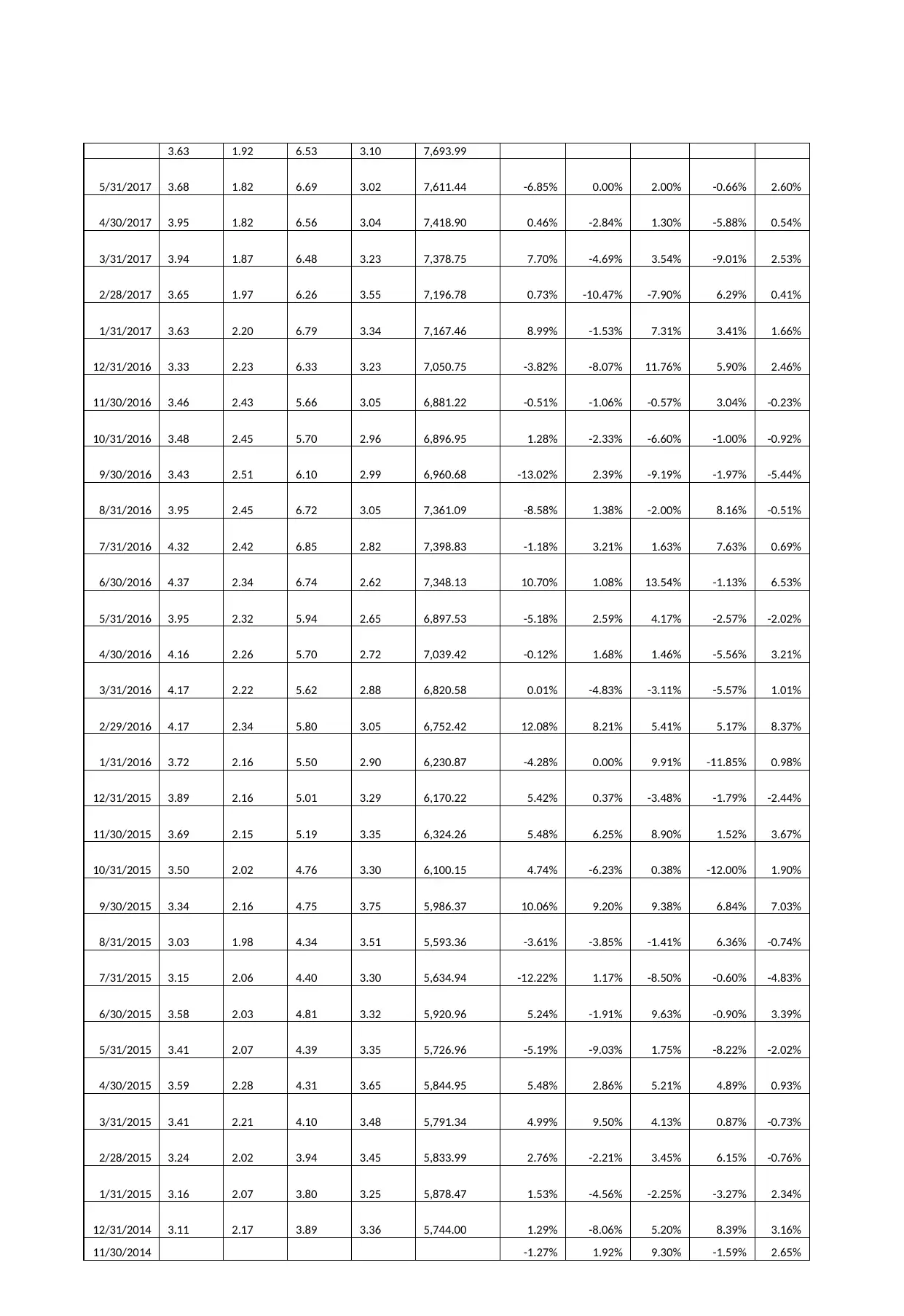

6/30/2017 -1.47% 5.37% -2.51% 2.65% 1.08%

Average growth returns

Year (-4) ($) Year (-3)

($)

Year (-2)

($)

Year (-1)

($)

Year

(0) ($)

di 3.44 3.54 3.62 3.71 3.81

gi - 2.91% 2.26% 2.49% 2.70%

average 2.59%

Book sale value = Cost of plant less depreciable value at time 6

Monthly Return

Adj close Monthly Return

Date SKC WHS AIA HLG NZ50 SKC WHS AIA HLG NZ50

2/28/2019 3.87 2.09 8.03 4.69 9,844.95 5.40% 3.81% 4.76% 13.01% 5.58%

1/31/2019 3.67 2.01 7.66 4.15 9,325.03 -1.82% 2.44% 5.71% 3.75% 3.78%

12/31/2018 3.74 1.97 7.25 4.00 8,985.34 8.17% 0.00% 2.37% -4.31% 1.98%

11/30/2018 3.46 1.97 7.08 4.18 8,811.27 -1.39% -3.30% -0.28% -25.49% -0.14%

10/31/2018 3.51 2.03 7.10 5.61 8,823.54 -6.01% 0.95% 4.58% -4.75% 0.81%

9/30/2018 3.73 2.01 6.79 5.89 8,752.31 -4.49% 1.94% -4.25% 0.68% -6.40%

8/31/2018 3.91 1.97 7.09 5.85 9,351.06 1.17% 0.98% 2.17% -7.00% 0.41%

7/31/2018 3.86 1.96 6.94 6.29 9,313.20 2.53% 0.99% 7.04% 23.09% 4.38%

6/30/2018 3.77 1.94 6.48 5.11 8,922.09 -1.98% -1.94% -1.55% 7.58% -0.24%

5/31/2018 3.84 1.97 6.59 4.75 8,943.13 1.25% 1.48% 2.73% 8.45% 3.28%

4/30/2018 3.79 1.95 6.41 4.38 8,658.79 -1.48% 0.50% 3.45% -4.16% 2.55%

3/31/2018 3.85 1.94 6.20 4.57 8,443.58 6.58% 5.38% 6.09% -9.50% 1.50%

2/28/2018 3.61 1.84 5.84 5.05 8,319.07 0.00% 0.00% -5.12% 8.84% -0.65%

1/31/2018 3.61 1.84 6.16 4.64 8,373.82 -6.02% -2.43% -3.66% 8.92% -0.81%

12/31/2017 3.84 1.88 6.39 4.26 8,442.01 0.00% -0.96% 3.32% 7.85% 0.52%

11/30/2017 3.84 1.90 6.19 3.95 8,398.08 5.06% 4.92% 1.57% 18.26% 2.58%

10/31/2017 3.66 1.81 6.09 3.34 8,186.82 1.54% -3.32% 4.11% 0.00% 0.50%

9/30/2017 3.60 1.87 5.85 3.34 8,146.34 3.73% -3.21% -3.26% -0.30% 2.72%

8/31/2017 3.47 1.94 6.05 3.35 7,930.40 1.41% 3.32% -5.14% 2.45% 1.45%

7/31/2017 3.43 1.87 6.37 3.27 7,817.10 -5.60% -2.31% -2.33% 5.48% 1.60%

6/30/2017 -1.47% 5.37% -2.51% 2.65% 1.08%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.63 1.92 6.53 3.10 7,693.99

5/31/2017 3.68 1.82 6.69 3.02 7,611.44 -6.85% 0.00% 2.00% -0.66% 2.60%

4/30/2017 3.95 1.82 6.56 3.04 7,418.90 0.46% -2.84% 1.30% -5.88% 0.54%

3/31/2017 3.94 1.87 6.48 3.23 7,378.75 7.70% -4.69% 3.54% -9.01% 2.53%

2/28/2017 3.65 1.97 6.26 3.55 7,196.78 0.73% -10.47% -7.90% 6.29% 0.41%

1/31/2017 3.63 2.20 6.79 3.34 7,167.46 8.99% -1.53% 7.31% 3.41% 1.66%

12/31/2016 3.33 2.23 6.33 3.23 7,050.75 -3.82% -8.07% 11.76% 5.90% 2.46%

11/30/2016 3.46 2.43 5.66 3.05 6,881.22 -0.51% -1.06% -0.57% 3.04% -0.23%

10/31/2016 3.48 2.45 5.70 2.96 6,896.95 1.28% -2.33% -6.60% -1.00% -0.92%

9/30/2016 3.43 2.51 6.10 2.99 6,960.68 -13.02% 2.39% -9.19% -1.97% -5.44%

8/31/2016 3.95 2.45 6.72 3.05 7,361.09 -8.58% 1.38% -2.00% 8.16% -0.51%

7/31/2016 4.32 2.42 6.85 2.82 7,398.83 -1.18% 3.21% 1.63% 7.63% 0.69%

6/30/2016 4.37 2.34 6.74 2.62 7,348.13 10.70% 1.08% 13.54% -1.13% 6.53%

5/31/2016 3.95 2.32 5.94 2.65 6,897.53 -5.18% 2.59% 4.17% -2.57% -2.02%

4/30/2016 4.16 2.26 5.70 2.72 7,039.42 -0.12% 1.68% 1.46% -5.56% 3.21%

3/31/2016 4.17 2.22 5.62 2.88 6,820.58 0.01% -4.83% -3.11% -5.57% 1.01%

2/29/2016 4.17 2.34 5.80 3.05 6,752.42 12.08% 8.21% 5.41% 5.17% 8.37%

1/31/2016 3.72 2.16 5.50 2.90 6,230.87 -4.28% 0.00% 9.91% -11.85% 0.98%

12/31/2015 3.89 2.16 5.01 3.29 6,170.22 5.42% 0.37% -3.48% -1.79% -2.44%

11/30/2015 3.69 2.15 5.19 3.35 6,324.26 5.48% 6.25% 8.90% 1.52% 3.67%

10/31/2015 3.50 2.02 4.76 3.30 6,100.15 4.74% -6.23% 0.38% -12.00% 1.90%

9/30/2015 3.34 2.16 4.75 3.75 5,986.37 10.06% 9.20% 9.38% 6.84% 7.03%

8/31/2015 3.03 1.98 4.34 3.51 5,593.36 -3.61% -3.85% -1.41% 6.36% -0.74%

7/31/2015 3.15 2.06 4.40 3.30 5,634.94 -12.22% 1.17% -8.50% -0.60% -4.83%

6/30/2015 3.58 2.03 4.81 3.32 5,920.96 5.24% -1.91% 9.63% -0.90% 3.39%

5/31/2015 3.41 2.07 4.39 3.35 5,726.96 -5.19% -9.03% 1.75% -8.22% -2.02%

4/30/2015 3.59 2.28 4.31 3.65 5,844.95 5.48% 2.86% 5.21% 4.89% 0.93%

3/31/2015 3.41 2.21 4.10 3.48 5,791.34 4.99% 9.50% 4.13% 0.87% -0.73%

2/28/2015 3.24 2.02 3.94 3.45 5,833.99 2.76% -2.21% 3.45% 6.15% -0.76%

1/31/2015 3.16 2.07 3.80 3.25 5,878.47 1.53% -4.56% -2.25% -3.27% 2.34%

12/31/2014 3.11 2.17 3.89 3.36 5,744.00 1.29% -8.06% 5.20% 8.39% 3.16%

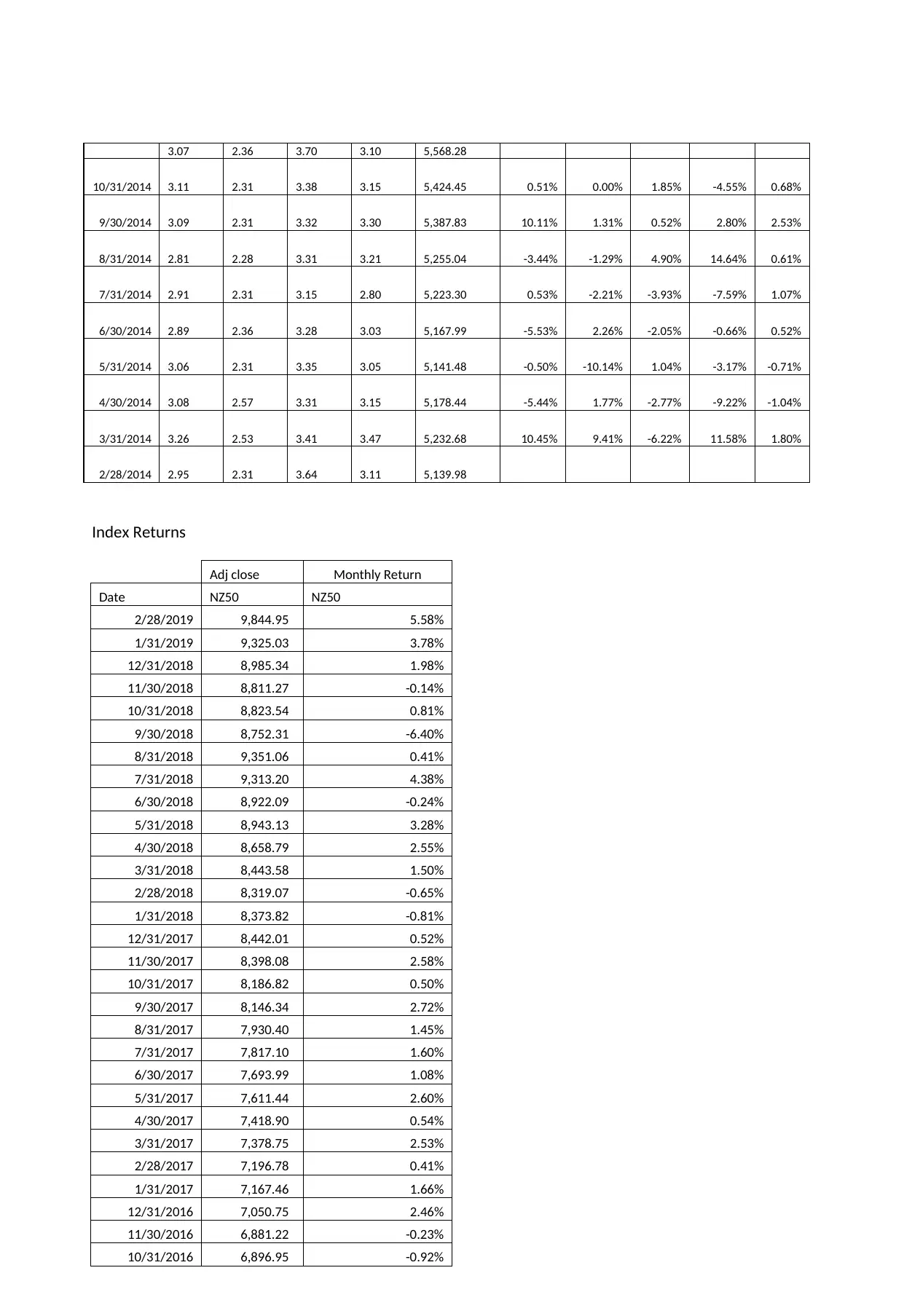

11/30/2014 -1.27% 1.92% 9.30% -1.59% 2.65%

5/31/2017 3.68 1.82 6.69 3.02 7,611.44 -6.85% 0.00% 2.00% -0.66% 2.60%

4/30/2017 3.95 1.82 6.56 3.04 7,418.90 0.46% -2.84% 1.30% -5.88% 0.54%

3/31/2017 3.94 1.87 6.48 3.23 7,378.75 7.70% -4.69% 3.54% -9.01% 2.53%

2/28/2017 3.65 1.97 6.26 3.55 7,196.78 0.73% -10.47% -7.90% 6.29% 0.41%

1/31/2017 3.63 2.20 6.79 3.34 7,167.46 8.99% -1.53% 7.31% 3.41% 1.66%

12/31/2016 3.33 2.23 6.33 3.23 7,050.75 -3.82% -8.07% 11.76% 5.90% 2.46%

11/30/2016 3.46 2.43 5.66 3.05 6,881.22 -0.51% -1.06% -0.57% 3.04% -0.23%

10/31/2016 3.48 2.45 5.70 2.96 6,896.95 1.28% -2.33% -6.60% -1.00% -0.92%

9/30/2016 3.43 2.51 6.10 2.99 6,960.68 -13.02% 2.39% -9.19% -1.97% -5.44%

8/31/2016 3.95 2.45 6.72 3.05 7,361.09 -8.58% 1.38% -2.00% 8.16% -0.51%

7/31/2016 4.32 2.42 6.85 2.82 7,398.83 -1.18% 3.21% 1.63% 7.63% 0.69%

6/30/2016 4.37 2.34 6.74 2.62 7,348.13 10.70% 1.08% 13.54% -1.13% 6.53%

5/31/2016 3.95 2.32 5.94 2.65 6,897.53 -5.18% 2.59% 4.17% -2.57% -2.02%

4/30/2016 4.16 2.26 5.70 2.72 7,039.42 -0.12% 1.68% 1.46% -5.56% 3.21%

3/31/2016 4.17 2.22 5.62 2.88 6,820.58 0.01% -4.83% -3.11% -5.57% 1.01%

2/29/2016 4.17 2.34 5.80 3.05 6,752.42 12.08% 8.21% 5.41% 5.17% 8.37%

1/31/2016 3.72 2.16 5.50 2.90 6,230.87 -4.28% 0.00% 9.91% -11.85% 0.98%

12/31/2015 3.89 2.16 5.01 3.29 6,170.22 5.42% 0.37% -3.48% -1.79% -2.44%

11/30/2015 3.69 2.15 5.19 3.35 6,324.26 5.48% 6.25% 8.90% 1.52% 3.67%

10/31/2015 3.50 2.02 4.76 3.30 6,100.15 4.74% -6.23% 0.38% -12.00% 1.90%

9/30/2015 3.34 2.16 4.75 3.75 5,986.37 10.06% 9.20% 9.38% 6.84% 7.03%

8/31/2015 3.03 1.98 4.34 3.51 5,593.36 -3.61% -3.85% -1.41% 6.36% -0.74%

7/31/2015 3.15 2.06 4.40 3.30 5,634.94 -12.22% 1.17% -8.50% -0.60% -4.83%

6/30/2015 3.58 2.03 4.81 3.32 5,920.96 5.24% -1.91% 9.63% -0.90% 3.39%

5/31/2015 3.41 2.07 4.39 3.35 5,726.96 -5.19% -9.03% 1.75% -8.22% -2.02%

4/30/2015 3.59 2.28 4.31 3.65 5,844.95 5.48% 2.86% 5.21% 4.89% 0.93%

3/31/2015 3.41 2.21 4.10 3.48 5,791.34 4.99% 9.50% 4.13% 0.87% -0.73%

2/28/2015 3.24 2.02 3.94 3.45 5,833.99 2.76% -2.21% 3.45% 6.15% -0.76%

1/31/2015 3.16 2.07 3.80 3.25 5,878.47 1.53% -4.56% -2.25% -3.27% 2.34%

12/31/2014 3.11 2.17 3.89 3.36 5,744.00 1.29% -8.06% 5.20% 8.39% 3.16%

11/30/2014 -1.27% 1.92% 9.30% -1.59% 2.65%

3.07 2.36 3.70 3.10 5,568.28

10/31/2014 3.11 2.31 3.38 3.15 5,424.45 0.51% 0.00% 1.85% -4.55% 0.68%

9/30/2014 3.09 2.31 3.32 3.30 5,387.83 10.11% 1.31% 0.52% 2.80% 2.53%

8/31/2014 2.81 2.28 3.31 3.21 5,255.04 -3.44% -1.29% 4.90% 14.64% 0.61%

7/31/2014 2.91 2.31 3.15 2.80 5,223.30 0.53% -2.21% -3.93% -7.59% 1.07%

6/30/2014 2.89 2.36 3.28 3.03 5,167.99 -5.53% 2.26% -2.05% -0.66% 0.52%

5/31/2014 3.06 2.31 3.35 3.05 5,141.48 -0.50% -10.14% 1.04% -3.17% -0.71%

4/30/2014 3.08 2.57 3.31 3.15 5,178.44 -5.44% 1.77% -2.77% -9.22% -1.04%

3/31/2014 3.26 2.53 3.41 3.47 5,232.68 10.45% 9.41% -6.22% 11.58% 1.80%

2/28/2014 2.95 2.31 3.64 3.11 5,139.98

Index Returns

Adj close Monthly Return

Date NZ50 NZ50

2/28/2019 9,844.95 5.58%

1/31/2019 9,325.03 3.78%

12/31/2018 8,985.34 1.98%

11/30/2018 8,811.27 -0.14%

10/31/2018 8,823.54 0.81%

9/30/2018 8,752.31 -6.40%

8/31/2018 9,351.06 0.41%

7/31/2018 9,313.20 4.38%

6/30/2018 8,922.09 -0.24%

5/31/2018 8,943.13 3.28%

4/30/2018 8,658.79 2.55%

3/31/2018 8,443.58 1.50%

2/28/2018 8,319.07 -0.65%

1/31/2018 8,373.82 -0.81%

12/31/2017 8,442.01 0.52%

11/30/2017 8,398.08 2.58%

10/31/2017 8,186.82 0.50%

9/30/2017 8,146.34 2.72%

8/31/2017 7,930.40 1.45%

7/31/2017 7,817.10 1.60%

6/30/2017 7,693.99 1.08%

5/31/2017 7,611.44 2.60%

4/30/2017 7,418.90 0.54%

3/31/2017 7,378.75 2.53%

2/28/2017 7,196.78 0.41%

1/31/2017 7,167.46 1.66%

12/31/2016 7,050.75 2.46%

11/30/2016 6,881.22 -0.23%

10/31/2016 6,896.95 -0.92%

10/31/2014 3.11 2.31 3.38 3.15 5,424.45 0.51% 0.00% 1.85% -4.55% 0.68%

9/30/2014 3.09 2.31 3.32 3.30 5,387.83 10.11% 1.31% 0.52% 2.80% 2.53%

8/31/2014 2.81 2.28 3.31 3.21 5,255.04 -3.44% -1.29% 4.90% 14.64% 0.61%

7/31/2014 2.91 2.31 3.15 2.80 5,223.30 0.53% -2.21% -3.93% -7.59% 1.07%

6/30/2014 2.89 2.36 3.28 3.03 5,167.99 -5.53% 2.26% -2.05% -0.66% 0.52%

5/31/2014 3.06 2.31 3.35 3.05 5,141.48 -0.50% -10.14% 1.04% -3.17% -0.71%

4/30/2014 3.08 2.57 3.31 3.15 5,178.44 -5.44% 1.77% -2.77% -9.22% -1.04%

3/31/2014 3.26 2.53 3.41 3.47 5,232.68 10.45% 9.41% -6.22% 11.58% 1.80%

2/28/2014 2.95 2.31 3.64 3.11 5,139.98

Index Returns

Adj close Monthly Return

Date NZ50 NZ50

2/28/2019 9,844.95 5.58%

1/31/2019 9,325.03 3.78%

12/31/2018 8,985.34 1.98%

11/30/2018 8,811.27 -0.14%

10/31/2018 8,823.54 0.81%

9/30/2018 8,752.31 -6.40%

8/31/2018 9,351.06 0.41%

7/31/2018 9,313.20 4.38%

6/30/2018 8,922.09 -0.24%

5/31/2018 8,943.13 3.28%

4/30/2018 8,658.79 2.55%

3/31/2018 8,443.58 1.50%

2/28/2018 8,319.07 -0.65%

1/31/2018 8,373.82 -0.81%

12/31/2017 8,442.01 0.52%

11/30/2017 8,398.08 2.58%

10/31/2017 8,186.82 0.50%

9/30/2017 8,146.34 2.72%

8/31/2017 7,930.40 1.45%

7/31/2017 7,817.10 1.60%

6/30/2017 7,693.99 1.08%

5/31/2017 7,611.44 2.60%

4/30/2017 7,418.90 0.54%

3/31/2017 7,378.75 2.53%

2/28/2017 7,196.78 0.41%

1/31/2017 7,167.46 1.66%

12/31/2016 7,050.75 2.46%

11/30/2016 6,881.22 -0.23%

10/31/2016 6,896.95 -0.92%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.