Arden University, FIN4001 Introduction to Finance Assignment

VerifiedAdded on 2022/12/13

|14

|3255

|269

Homework Assignment

AI Summary

This assignment solution for FIN4001, Introduction to Finance, addresses several key financial concepts and techniques. It begins with a ratio analysis of Quinn Ltd., evaluating its profitability, efficiency, and liquidity using financial ratios from 2019 and 2020, followed by an interpretation of the company's financial performance. The solution then delves into inventory management using the Economic Order Quantity (EOQ) model, calculating the optimal order quantity and comparing costs. The assignment further explores investment decision-making, including the Accounting Rate of Return (ARR) and Net Present Value (NPV) methods for evaluating project profitability, with critical evaluations of each technique. Finally, it examines principles of effective corporate governance and the traditional aims of financial management, offering advice to the company on various aspects discussed.

WELCOME TO FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

Question 1.............................................................................................................................................3

Question 2.............................................................................................................................................6

Economic order quantity....................................................................................................................6

Annual cost of graphite......................................................................................................................6

Critical evaluation of EOQ decision..................................................................................................7

D) Advise to company.......................................................................................................................8

Question 3.............................................................................................................................................8

Accounting rate of return...................................................................................................................8

Net present value...............................................................................................................................9

C) Critical evaluation of net present value technique......................................................................10

D) Advise to organisation................................................................................................................11

Question 4...........................................................................................................................................11

a) Principles of effective corporate governance...........................................................................11

b) Traditional aim of financial management encourage short termism............................................12

C) Three effective corporate governance.........................................................................................12

CONCLUSION...................................................................................................................................13

REFERENCES....................................................................................................................................14

INTRODUCTION.................................................................................................................................3

Question 1.............................................................................................................................................3

Question 2.............................................................................................................................................6

Economic order quantity....................................................................................................................6

Annual cost of graphite......................................................................................................................6

Critical evaluation of EOQ decision..................................................................................................7

D) Advise to company.......................................................................................................................8

Question 3.............................................................................................................................................8

Accounting rate of return...................................................................................................................8

Net present value...............................................................................................................................9

C) Critical evaluation of net present value technique......................................................................10

D) Advise to organisation................................................................................................................11

Question 4...........................................................................................................................................11

a) Principles of effective corporate governance...........................................................................11

b) Traditional aim of financial management encourage short termism............................................12

C) Three effective corporate governance.........................................................................................12

CONCLUSION...................................................................................................................................13

REFERENCES....................................................................................................................................14

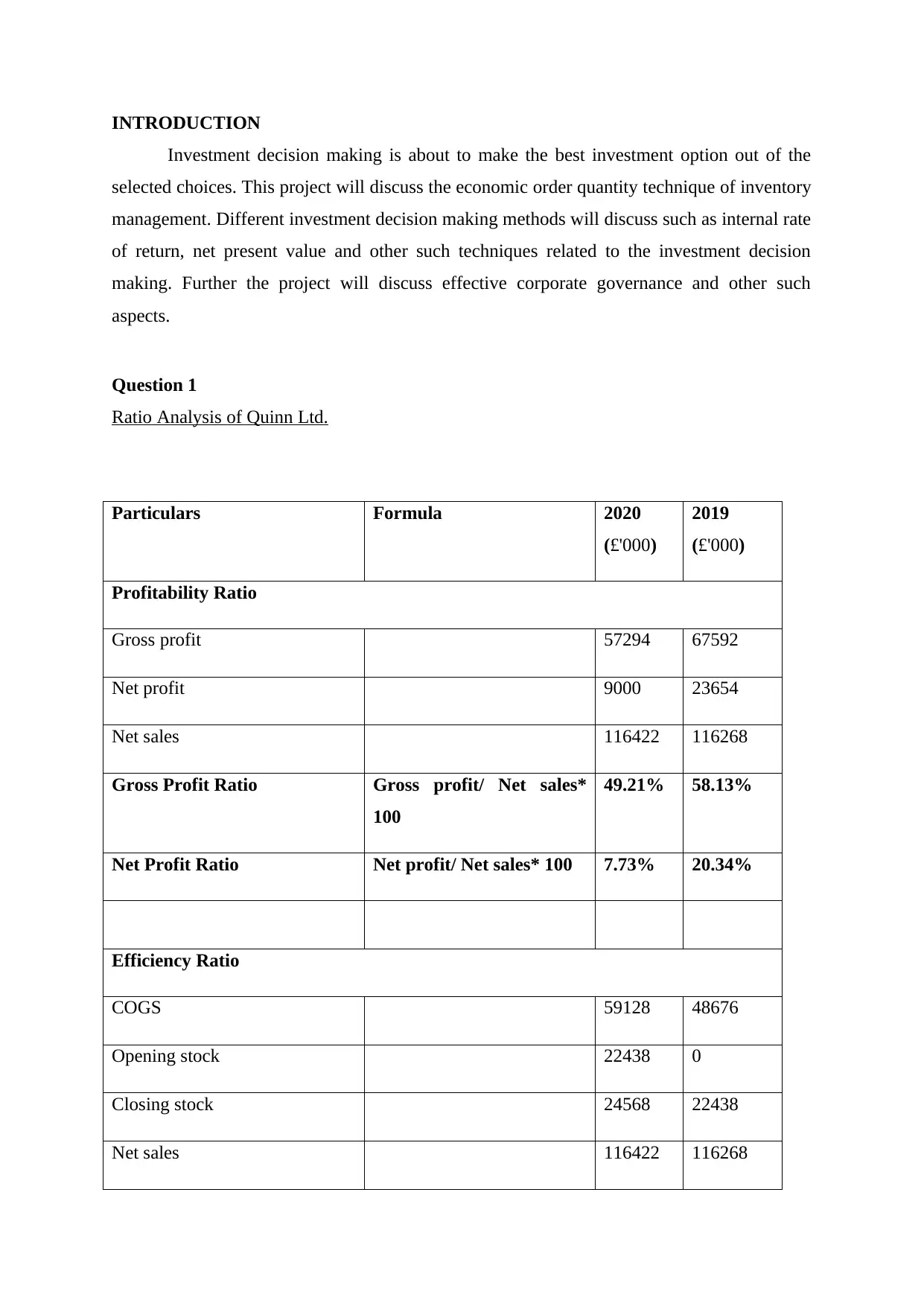

INTRODUCTION

Investment decision making is about to make the best investment option out of the

selected choices. This project will discuss the economic order quantity technique of inventory

management. Different investment decision making methods will discuss such as internal rate

of return, net present value and other such techniques related to the investment decision

making. Further the project will discuss effective corporate governance and other such

aspects.

Question 1

Ratio Analysis of Quinn Ltd.

Particulars Formula 2020

(£'000)

2019

(£'000)

Profitability Ratio

Gross profit 57294 67592

Net profit 9000 23654

Net sales 116422 116268

Gross Profit Ratio Gross profit/ Net sales*

100

49.21% 58.13%

Net Profit Ratio Net profit/ Net sales* 100 7.73% 20.34%

Efficiency Ratio

COGS 59128 48676

Opening stock 22438 0

Closing stock 24568 22438

Net sales 116422 116268

Investment decision making is about to make the best investment option out of the

selected choices. This project will discuss the economic order quantity technique of inventory

management. Different investment decision making methods will discuss such as internal rate

of return, net present value and other such techniques related to the investment decision

making. Further the project will discuss effective corporate governance and other such

aspects.

Question 1

Ratio Analysis of Quinn Ltd.

Particulars Formula 2020

(£'000)

2019

(£'000)

Profitability Ratio

Gross profit 57294 67592

Net profit 9000 23654

Net sales 116422 116268

Gross Profit Ratio Gross profit/ Net sales*

100

49.21% 58.13%

Net Profit Ratio Net profit/ Net sales* 100 7.73% 20.34%

Efficiency Ratio

COGS 59128 48676

Opening stock 22438 0

Closing stock 24568 22438

Net sales 116422 116268

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

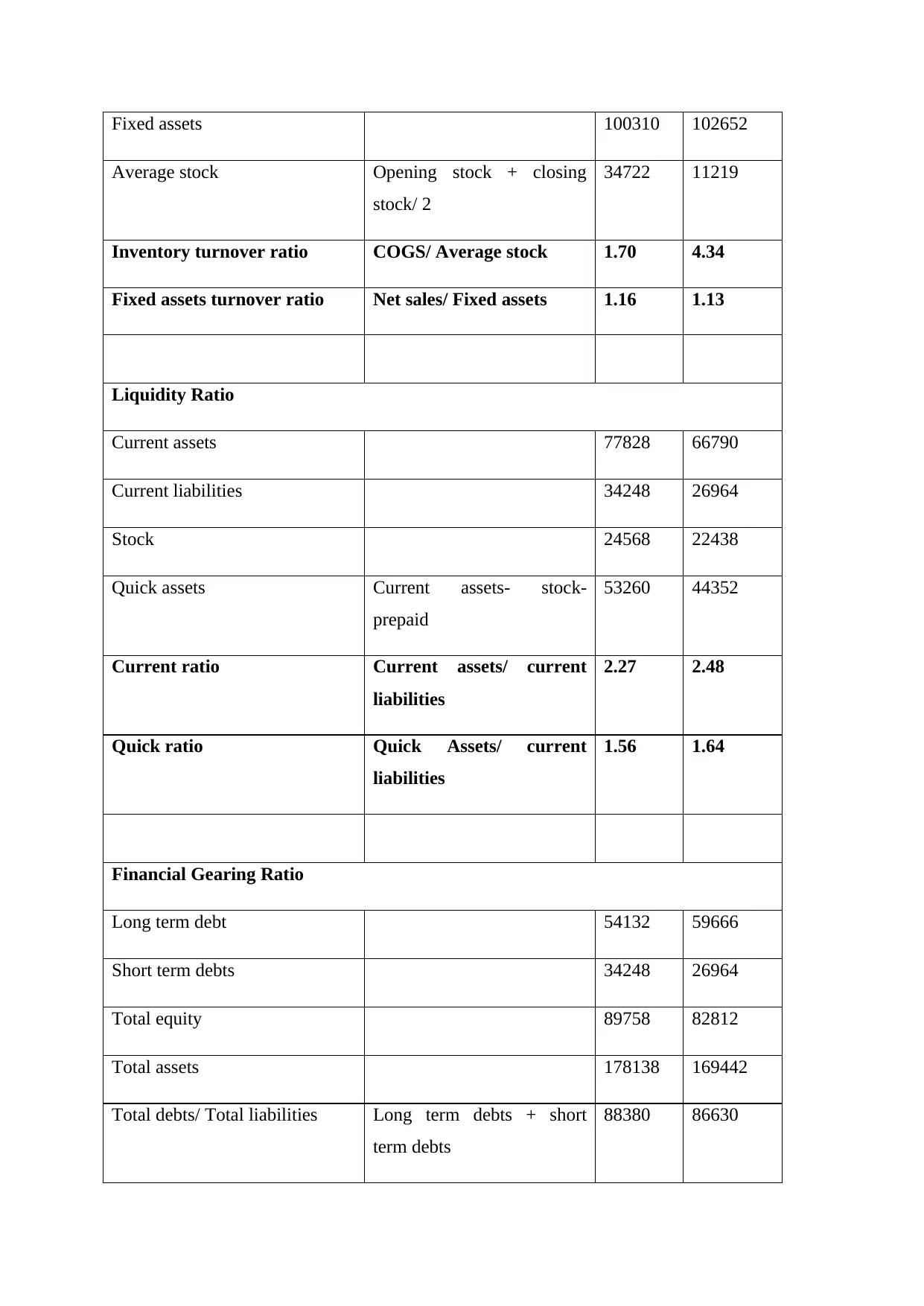

Fixed assets 100310 102652

Average stock Opening stock + closing

stock/ 2

34722 11219

Inventory turnover ratio COGS/ Average stock 1.70 4.34

Fixed assets turnover ratio Net sales/ Fixed assets 1.16 1.13

Liquidity Ratio

Current assets 77828 66790

Current liabilities 34248 26964

Stock 24568 22438

Quick assets Current assets- stock-

prepaid

53260 44352

Current ratio Current assets/ current

liabilities

2.27 2.48

Quick ratio Quick Assets/ current

liabilities

1.56 1.64

Financial Gearing Ratio

Long term debt 54132 59666

Short term debts 34248 26964

Total equity 89758 82812

Total assets 178138 169442

Total debts/ Total liabilities Long term debts + short

term debts

88380 86630

Average stock Opening stock + closing

stock/ 2

34722 11219

Inventory turnover ratio COGS/ Average stock 1.70 4.34

Fixed assets turnover ratio Net sales/ Fixed assets 1.16 1.13

Liquidity Ratio

Current assets 77828 66790

Current liabilities 34248 26964

Stock 24568 22438

Quick assets Current assets- stock-

prepaid

53260 44352

Current ratio Current assets/ current

liabilities

2.27 2.48

Quick ratio Quick Assets/ current

liabilities

1.56 1.64

Financial Gearing Ratio

Long term debt 54132 59666

Short term debts 34248 26964

Total equity 89758 82812

Total assets 178138 169442

Total debts/ Total liabilities Long term debts + short

term debts

88380 86630

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

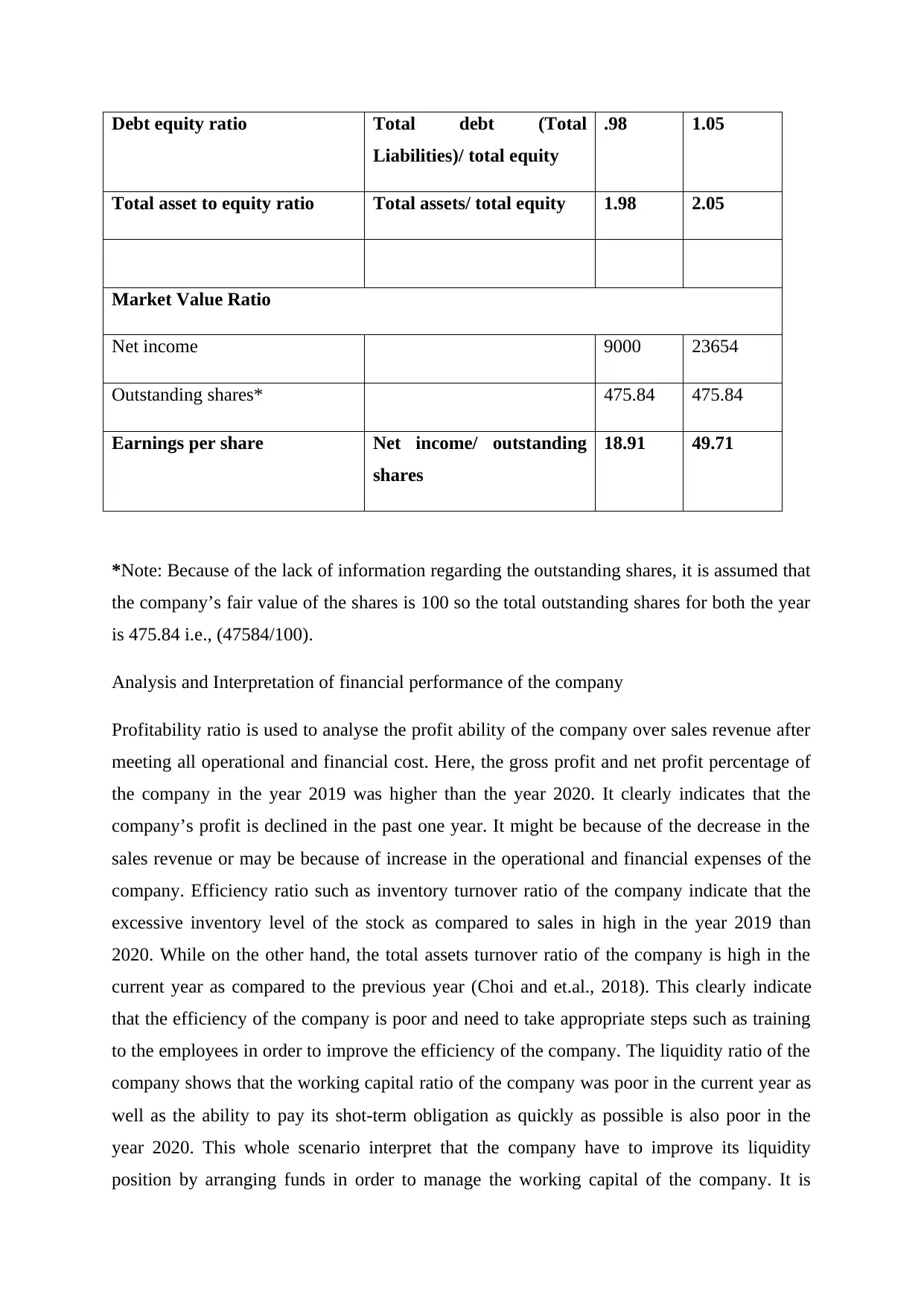

Debt equity ratio Total debt (Total

Liabilities)/ total equity

.98 1.05

Total asset to equity ratio Total assets/ total equity 1.98 2.05

Market Value Ratio

Net income 9000 23654

Outstanding shares* 475.84 475.84

Earnings per share Net income/ outstanding

shares

18.91 49.71

*Note: Because of the lack of information regarding the outstanding shares, it is assumed that

the company’s fair value of the shares is 100 so the total outstanding shares for both the year

is 475.84 i.e., (47584/100).

Analysis and Interpretation of financial performance of the company

Profitability ratio is used to analyse the profit ability of the company over sales revenue after

meeting all operational and financial cost. Here, the gross profit and net profit percentage of

the company in the year 2019 was higher than the year 2020. It clearly indicates that the

company’s profit is declined in the past one year. It might be because of the decrease in the

sales revenue or may be because of increase in the operational and financial expenses of the

company. Efficiency ratio such as inventory turnover ratio of the company indicate that the

excessive inventory level of the stock as compared to sales in high in the year 2019 than

2020. While on the other hand, the total assets turnover ratio of the company is high in the

current year as compared to the previous year (Choi and et.al., 2018). This clearly indicate

that the efficiency of the company is poor and need to take appropriate steps such as training

to the employees in order to improve the efficiency of the company. The liquidity ratio of the

company shows that the working capital ratio of the company was poor in the current year as

well as the ability to pay its shot-term obligation as quickly as possible is also poor in the

year 2020. This whole scenario interpret that the company have to improve its liquidity

position by arranging funds in order to manage the working capital of the company. It is

Liabilities)/ total equity

.98 1.05

Total asset to equity ratio Total assets/ total equity 1.98 2.05

Market Value Ratio

Net income 9000 23654

Outstanding shares* 475.84 475.84

Earnings per share Net income/ outstanding

shares

18.91 49.71

*Note: Because of the lack of information regarding the outstanding shares, it is assumed that

the company’s fair value of the shares is 100 so the total outstanding shares for both the year

is 475.84 i.e., (47584/100).

Analysis and Interpretation of financial performance of the company

Profitability ratio is used to analyse the profit ability of the company over sales revenue after

meeting all operational and financial cost. Here, the gross profit and net profit percentage of

the company in the year 2019 was higher than the year 2020. It clearly indicates that the

company’s profit is declined in the past one year. It might be because of the decrease in the

sales revenue or may be because of increase in the operational and financial expenses of the

company. Efficiency ratio such as inventory turnover ratio of the company indicate that the

excessive inventory level of the stock as compared to sales in high in the year 2019 than

2020. While on the other hand, the total assets turnover ratio of the company is high in the

current year as compared to the previous year (Choi and et.al., 2018). This clearly indicate

that the efficiency of the company is poor and need to take appropriate steps such as training

to the employees in order to improve the efficiency of the company. The liquidity ratio of the

company shows that the working capital ratio of the company was poor in the current year as

well as the ability to pay its shot-term obligation as quickly as possible is also poor in the

year 2020. This whole scenario interpret that the company have to improve its liquidity

position by arranging funds in order to manage the working capital of the company. It is

because this capital is used in the daily operations of the business which need to perfect so

that company produce the high-quality products in the less time as well as minimum wastage.

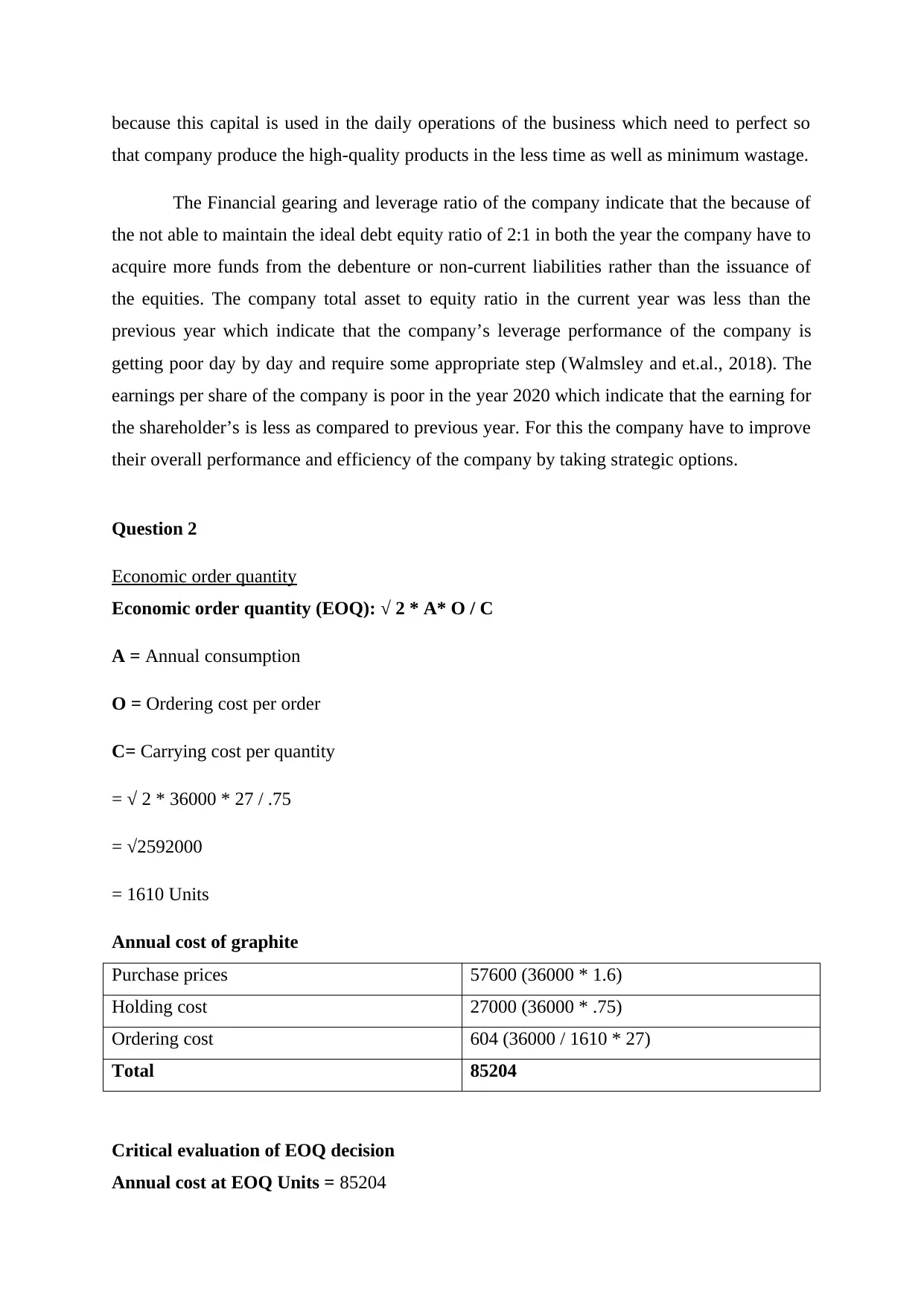

The Financial gearing and leverage ratio of the company indicate that the because of

the not able to maintain the ideal debt equity ratio of 2:1 in both the year the company have to

acquire more funds from the debenture or non-current liabilities rather than the issuance of

the equities. The company total asset to equity ratio in the current year was less than the

previous year which indicate that the company’s leverage performance of the company is

getting poor day by day and require some appropriate step (Walmsley and et.al., 2018). The

earnings per share of the company is poor in the year 2020 which indicate that the earning for

the shareholder’s is less as compared to previous year. For this the company have to improve

their overall performance and efficiency of the company by taking strategic options.

Question 2

Economic order quantity

Economic order quantity (EOQ): √ 2 * A* O / C

A = Annual consumption

O = Ordering cost per order

C= Carrying cost per quantity

= √ 2 * 36000 * 27 / .75

= √2592000

= 1610 Units

Annual cost of graphite

Purchase prices 57600 (36000 * 1.6)

Holding cost 27000 (36000 * .75)

Ordering cost 604 (36000 / 1610 * 27)

Total 85204

Critical evaluation of EOQ decision

Annual cost at EOQ Units = 85204

that company produce the high-quality products in the less time as well as minimum wastage.

The Financial gearing and leverage ratio of the company indicate that the because of

the not able to maintain the ideal debt equity ratio of 2:1 in both the year the company have to

acquire more funds from the debenture or non-current liabilities rather than the issuance of

the equities. The company total asset to equity ratio in the current year was less than the

previous year which indicate that the company’s leverage performance of the company is

getting poor day by day and require some appropriate step (Walmsley and et.al., 2018). The

earnings per share of the company is poor in the year 2020 which indicate that the earning for

the shareholder’s is less as compared to previous year. For this the company have to improve

their overall performance and efficiency of the company by taking strategic options.

Question 2

Economic order quantity

Economic order quantity (EOQ): √ 2 * A* O / C

A = Annual consumption

O = Ordering cost per order

C= Carrying cost per quantity

= √ 2 * 36000 * 27 / .75

= √2592000

= 1610 Units

Annual cost of graphite

Purchase prices 57600 (36000 * 1.6)

Holding cost 27000 (36000 * .75)

Ordering cost 604 (36000 / 1610 * 27)

Total 85204

Critical evaluation of EOQ decision

Annual cost at EOQ Units = 85204

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

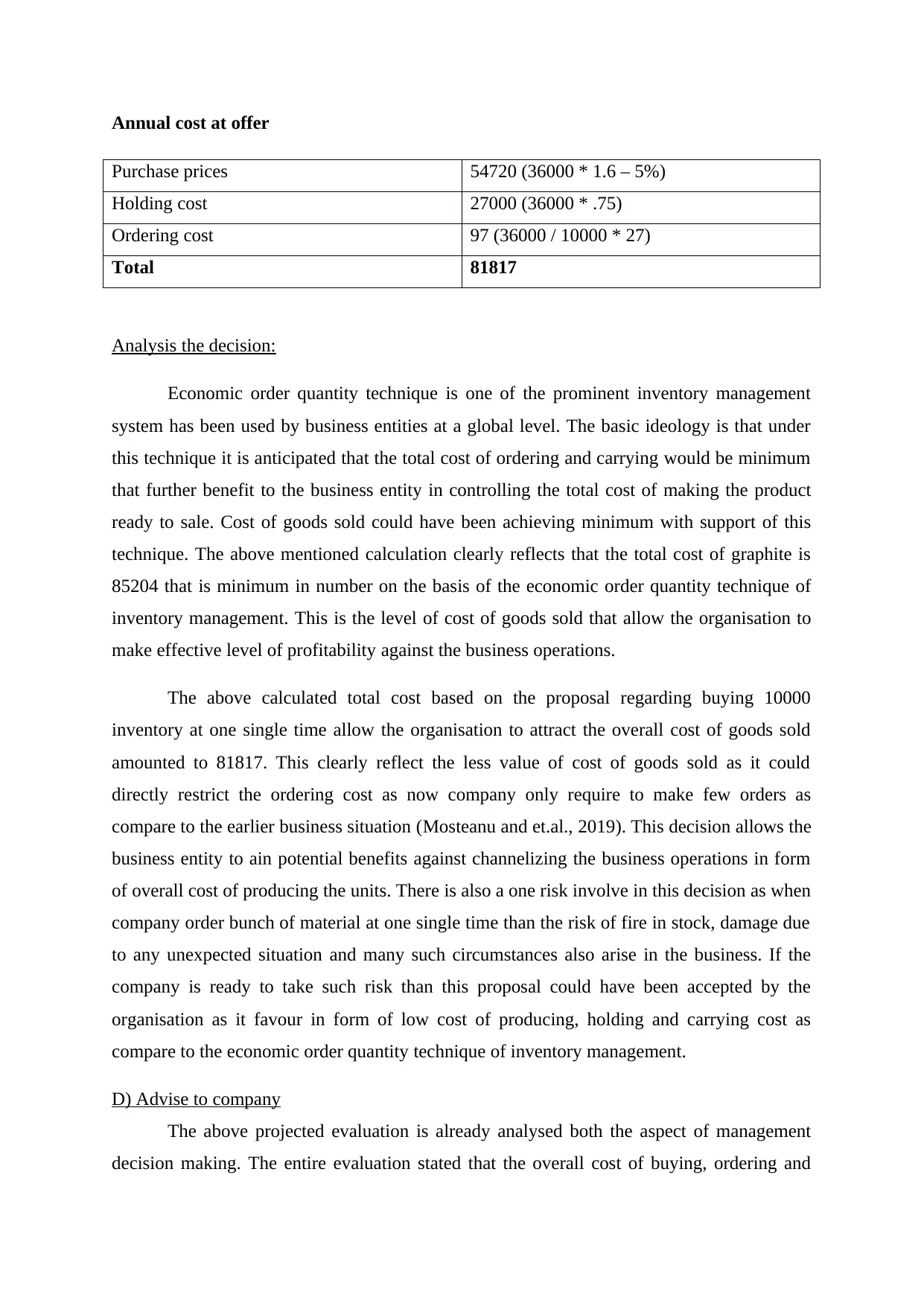

Annual cost at offer

Purchase prices 54720 (36000 * 1.6 – 5%)

Holding cost 27000 (36000 * .75)

Ordering cost 97 (36000 / 10000 * 27)

Total 81817

Analysis the decision:

Economic order quantity technique is one of the prominent inventory management

system has been used by business entities at a global level. The basic ideology is that under

this technique it is anticipated that the total cost of ordering and carrying would be minimum

that further benefit to the business entity in controlling the total cost of making the product

ready to sale. Cost of goods sold could have been achieving minimum with support of this

technique. The above mentioned calculation clearly reflects that the total cost of graphite is

85204 that is minimum in number on the basis of the economic order quantity technique of

inventory management. This is the level of cost of goods sold that allow the organisation to

make effective level of profitability against the business operations.

The above calculated total cost based on the proposal regarding buying 10000

inventory at one single time allow the organisation to attract the overall cost of goods sold

amounted to 81817. This clearly reflect the less value of cost of goods sold as it could

directly restrict the ordering cost as now company only require to make few orders as

compare to the earlier business situation (Mosteanu and et.al., 2019). This decision allows the

business entity to ain potential benefits against channelizing the business operations in form

of overall cost of producing the units. There is also a one risk involve in this decision as when

company order bunch of material at one single time than the risk of fire in stock, damage due

to any unexpected situation and many such circumstances also arise in the business. If the

company is ready to take such risk than this proposal could have been accepted by the

organisation as it favour in form of low cost of producing, holding and carrying cost as

compare to the economic order quantity technique of inventory management.

D) Advise to company

The above projected evaluation is already analysed both the aspect of management

decision making. The entire evaluation stated that the overall cost of buying, ordering and

Purchase prices 54720 (36000 * 1.6 – 5%)

Holding cost 27000 (36000 * .75)

Ordering cost 97 (36000 / 10000 * 27)

Total 81817

Analysis the decision:

Economic order quantity technique is one of the prominent inventory management

system has been used by business entities at a global level. The basic ideology is that under

this technique it is anticipated that the total cost of ordering and carrying would be minimum

that further benefit to the business entity in controlling the total cost of making the product

ready to sale. Cost of goods sold could have been achieving minimum with support of this

technique. The above mentioned calculation clearly reflects that the total cost of graphite is

85204 that is minimum in number on the basis of the economic order quantity technique of

inventory management. This is the level of cost of goods sold that allow the organisation to

make effective level of profitability against the business operations.

The above calculated total cost based on the proposal regarding buying 10000

inventory at one single time allow the organisation to attract the overall cost of goods sold

amounted to 81817. This clearly reflect the less value of cost of goods sold as it could

directly restrict the ordering cost as now company only require to make few orders as

compare to the earlier business situation (Mosteanu and et.al., 2019). This decision allows the

business entity to ain potential benefits against channelizing the business operations in form

of overall cost of producing the units. There is also a one risk involve in this decision as when

company order bunch of material at one single time than the risk of fire in stock, damage due

to any unexpected situation and many such circumstances also arise in the business. If the

company is ready to take such risk than this proposal could have been accepted by the

organisation as it favour in form of low cost of producing, holding and carrying cost as

compare to the economic order quantity technique of inventory management.

D) Advise to company

The above projected evaluation is already analysed both the aspect of management

decision making. The entire evaluation stated that the overall cost of buying, ordering and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

carrying is minimum when the management order 10000 units at a one single time. In case of

the economic order quantity technique the total cost incurred is 85204 and in the current

situation the total cost incurred as 81817. This clearly reflect the difference in the total cost of

storing the material (Ibtasam and et.al., 2018). The difference is arise out of the controlled

ordering cost as now the number of order require to place in the whole year get very

minimum that could allow the organisation to save the respective capital or resources.

Question 3

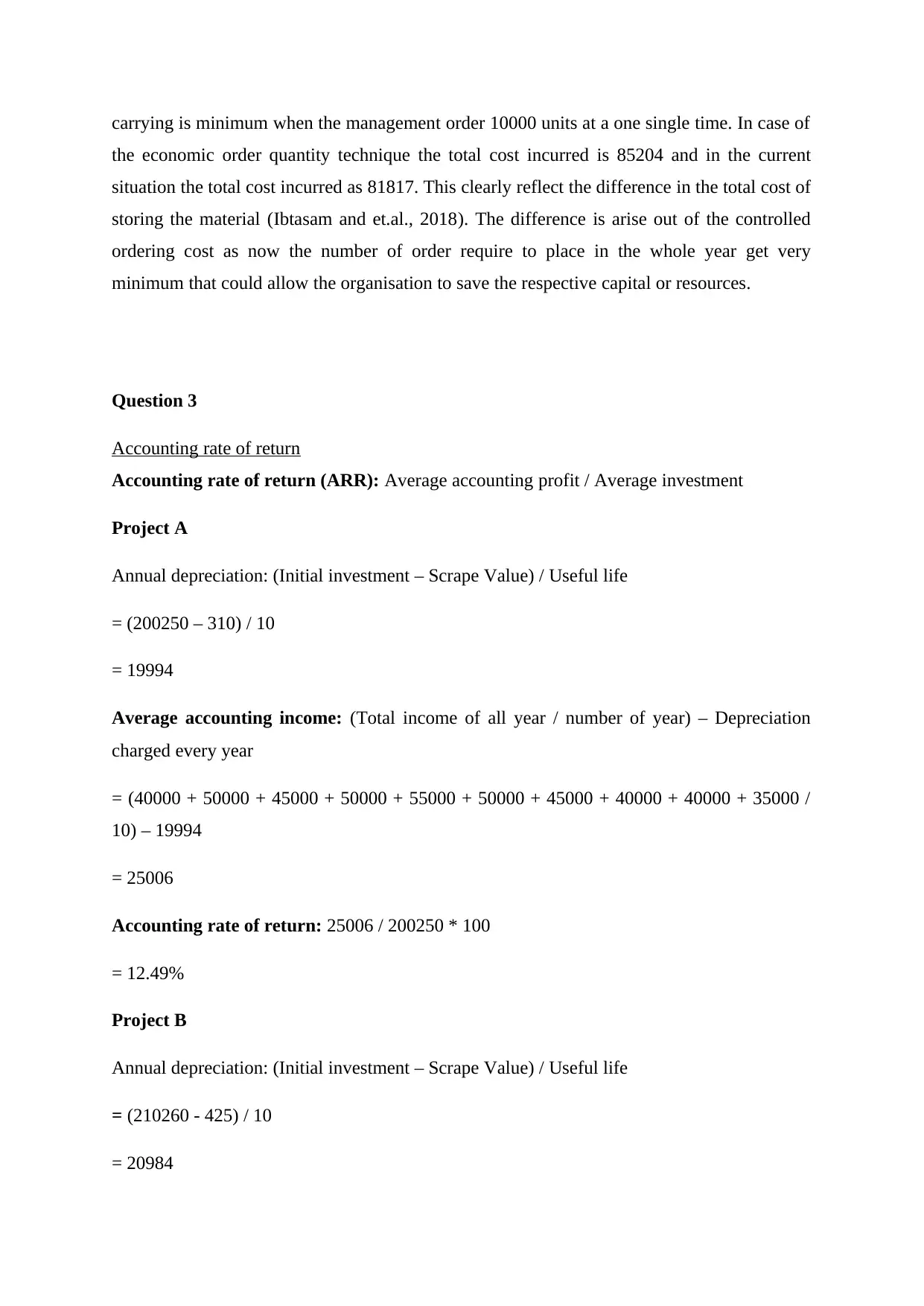

Accounting rate of return

Accounting rate of return (ARR): Average accounting profit / Average investment

Project A

Annual depreciation: (Initial investment – Scrape Value) / Useful life

= (200250 – 310) / 10

= 19994

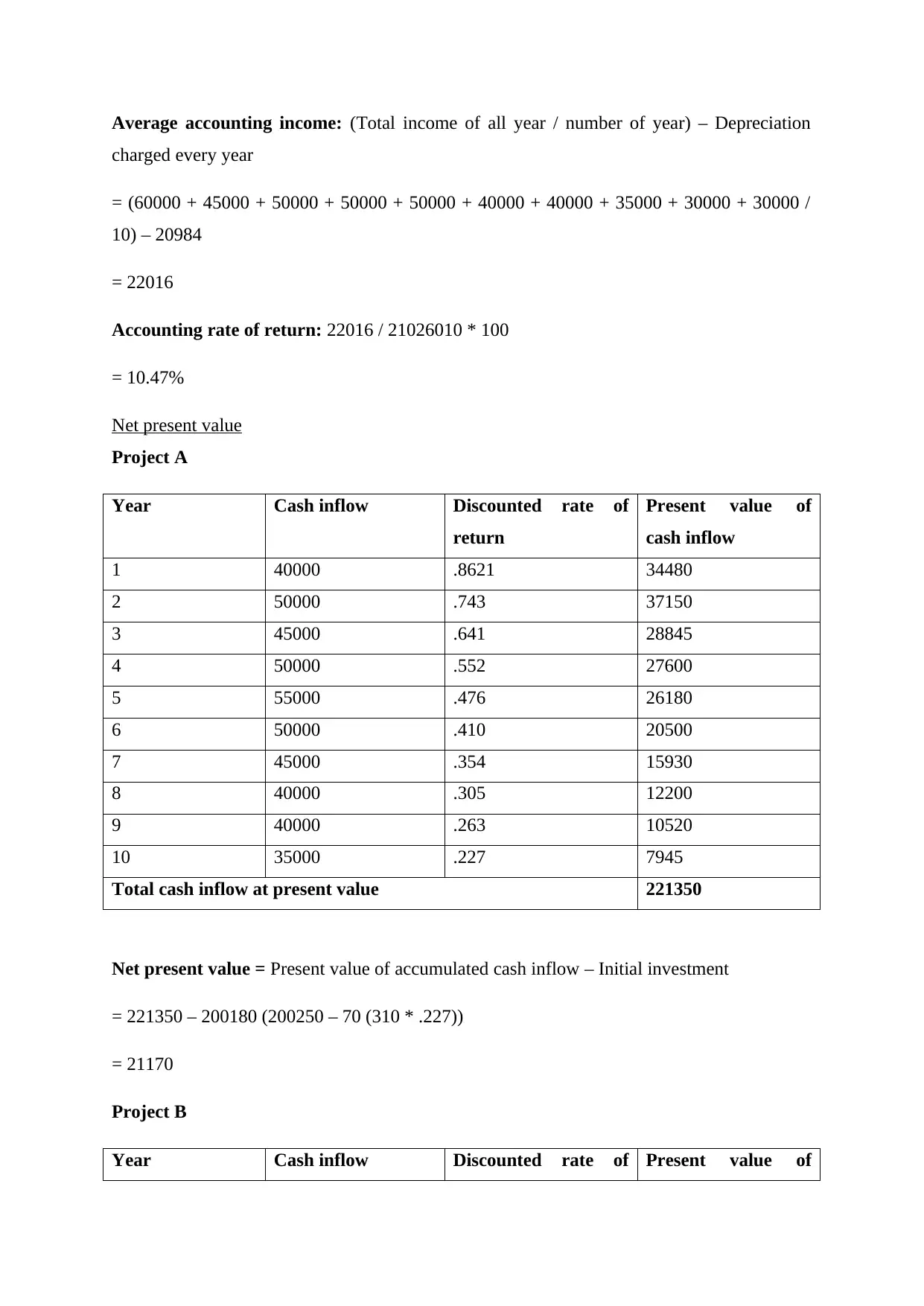

Average accounting income: (Total income of all year / number of year) – Depreciation

charged every year

= (40000 + 50000 + 45000 + 50000 + 55000 + 50000 + 45000 + 40000 + 40000 + 35000 /

10) – 19994

= 25006

Accounting rate of return: 25006 / 200250 * 100

= 12.49%

Project B

Annual depreciation: (Initial investment – Scrape Value) / Useful life

= (210260 - 425) / 10

= 20984

the economic order quantity technique the total cost incurred is 85204 and in the current

situation the total cost incurred as 81817. This clearly reflect the difference in the total cost of

storing the material (Ibtasam and et.al., 2018). The difference is arise out of the controlled

ordering cost as now the number of order require to place in the whole year get very

minimum that could allow the organisation to save the respective capital or resources.

Question 3

Accounting rate of return

Accounting rate of return (ARR): Average accounting profit / Average investment

Project A

Annual depreciation: (Initial investment – Scrape Value) / Useful life

= (200250 – 310) / 10

= 19994

Average accounting income: (Total income of all year / number of year) – Depreciation

charged every year

= (40000 + 50000 + 45000 + 50000 + 55000 + 50000 + 45000 + 40000 + 40000 + 35000 /

10) – 19994

= 25006

Accounting rate of return: 25006 / 200250 * 100

= 12.49%

Project B

Annual depreciation: (Initial investment – Scrape Value) / Useful life

= (210260 - 425) / 10

= 20984

Average accounting income: (Total income of all year / number of year) – Depreciation

charged every year

= (60000 + 45000 + 50000 + 50000 + 50000 + 40000 + 40000 + 35000 + 30000 + 30000 /

10) – 20984

= 22016

Accounting rate of return: 22016 / 21026010 * 100

= 10.47%

Net present value

Project A

Year Cash inflow Discounted rate of

return

Present value of

cash inflow

1 40000 .8621 34480

2 50000 .743 37150

3 45000 .641 28845

4 50000 .552 27600

5 55000 .476 26180

6 50000 .410 20500

7 45000 .354 15930

8 40000 .305 12200

9 40000 .263 10520

10 35000 .227 7945

Total cash inflow at present value 221350

Net present value = Present value of accumulated cash inflow – Initial investment

= 221350 – 200180 (200250 – 70 (310 * .227))

= 21170

Project B

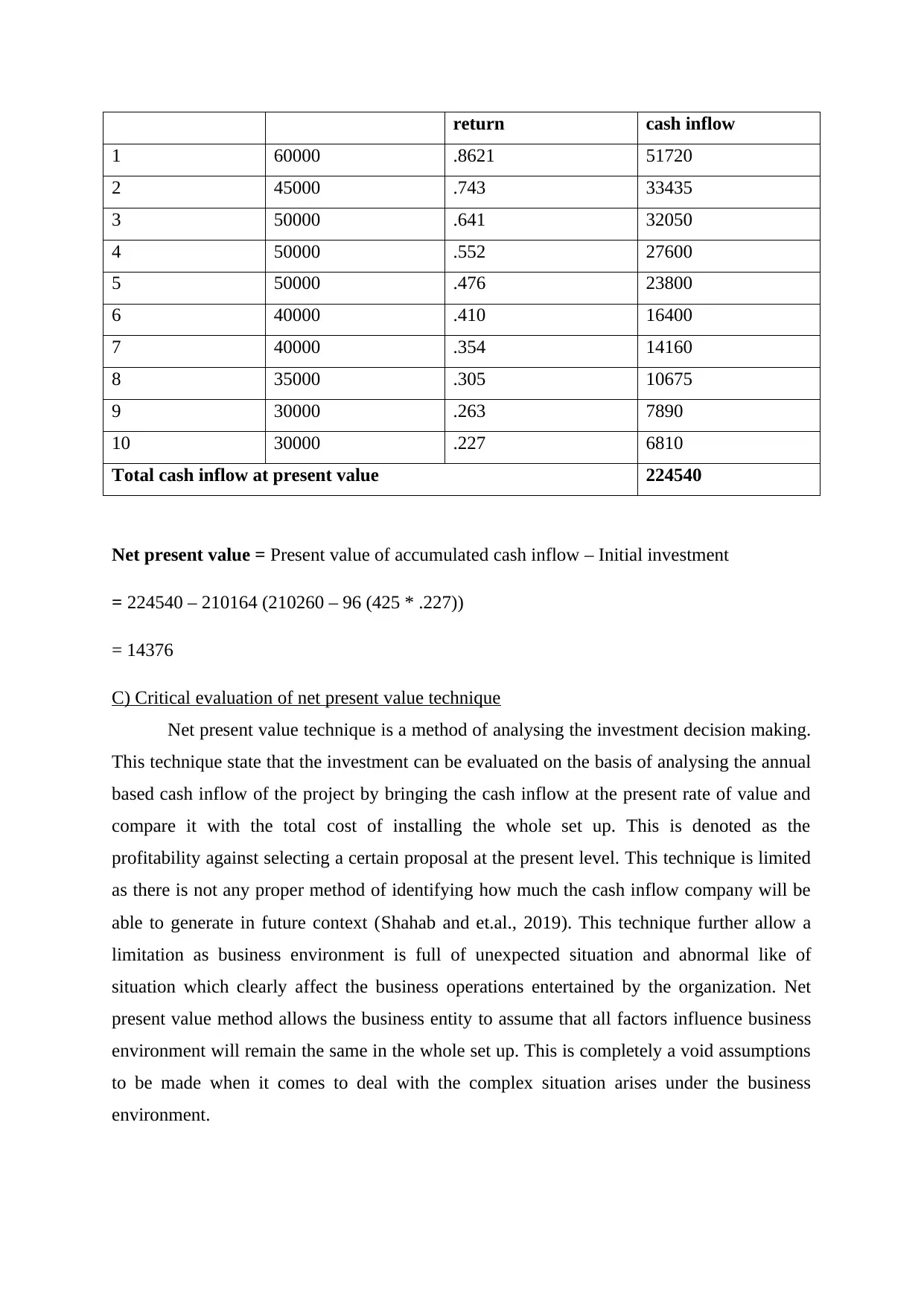

Year Cash inflow Discounted rate of Present value of

charged every year

= (60000 + 45000 + 50000 + 50000 + 50000 + 40000 + 40000 + 35000 + 30000 + 30000 /

10) – 20984

= 22016

Accounting rate of return: 22016 / 21026010 * 100

= 10.47%

Net present value

Project A

Year Cash inflow Discounted rate of

return

Present value of

cash inflow

1 40000 .8621 34480

2 50000 .743 37150

3 45000 .641 28845

4 50000 .552 27600

5 55000 .476 26180

6 50000 .410 20500

7 45000 .354 15930

8 40000 .305 12200

9 40000 .263 10520

10 35000 .227 7945

Total cash inflow at present value 221350

Net present value = Present value of accumulated cash inflow – Initial investment

= 221350 – 200180 (200250 – 70 (310 * .227))

= 21170

Project B

Year Cash inflow Discounted rate of Present value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return cash inflow

1 60000 .8621 51720

2 45000 .743 33435

3 50000 .641 32050

4 50000 .552 27600

5 50000 .476 23800

6 40000 .410 16400

7 40000 .354 14160

8 35000 .305 10675

9 30000 .263 7890

10 30000 .227 6810

Total cash inflow at present value 224540

Net present value = Present value of accumulated cash inflow – Initial investment

= 224540 – 210164 (210260 – 96 (425 * .227))

= 14376

C) Critical evaluation of net present value technique

Net present value technique is a method of analysing the investment decision making.

This technique state that the investment can be evaluated on the basis of analysing the annual

based cash inflow of the project by bringing the cash inflow at the present rate of value and

compare it with the total cost of installing the whole set up. This is denoted as the

profitability against selecting a certain proposal at the present level. This technique is limited

as there is not any proper method of identifying how much the cash inflow company will be

able to generate in future context (Shahab and et.al., 2019). This technique further allow a

limitation as business environment is full of unexpected situation and abnormal like of

situation which clearly affect the business operations entertained by the organization. Net

present value method allows the business entity to assume that all factors influence business

environment will remain the same in the whole set up. This is completely a void assumptions

to be made when it comes to deal with the complex situation arises under the business

environment.

1 60000 .8621 51720

2 45000 .743 33435

3 50000 .641 32050

4 50000 .552 27600

5 50000 .476 23800

6 40000 .410 16400

7 40000 .354 14160

8 35000 .305 10675

9 30000 .263 7890

10 30000 .227 6810

Total cash inflow at present value 224540

Net present value = Present value of accumulated cash inflow – Initial investment

= 224540 – 210164 (210260 – 96 (425 * .227))

= 14376

C) Critical evaluation of net present value technique

Net present value technique is a method of analysing the investment decision making.

This technique state that the investment can be evaluated on the basis of analysing the annual

based cash inflow of the project by bringing the cash inflow at the present rate of value and

compare it with the total cost of installing the whole set up. This is denoted as the

profitability against selecting a certain proposal at the present level. This technique is limited

as there is not any proper method of identifying how much the cash inflow company will be

able to generate in future context (Shahab and et.al., 2019). This technique further allow a

limitation as business environment is full of unexpected situation and abnormal like of

situation which clearly affect the business operations entertained by the organization. Net

present value method allows the business entity to assume that all factors influence business

environment will remain the same in the whole set up. This is completely a void assumptions

to be made when it comes to deal with the complex situation arises under the business

environment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

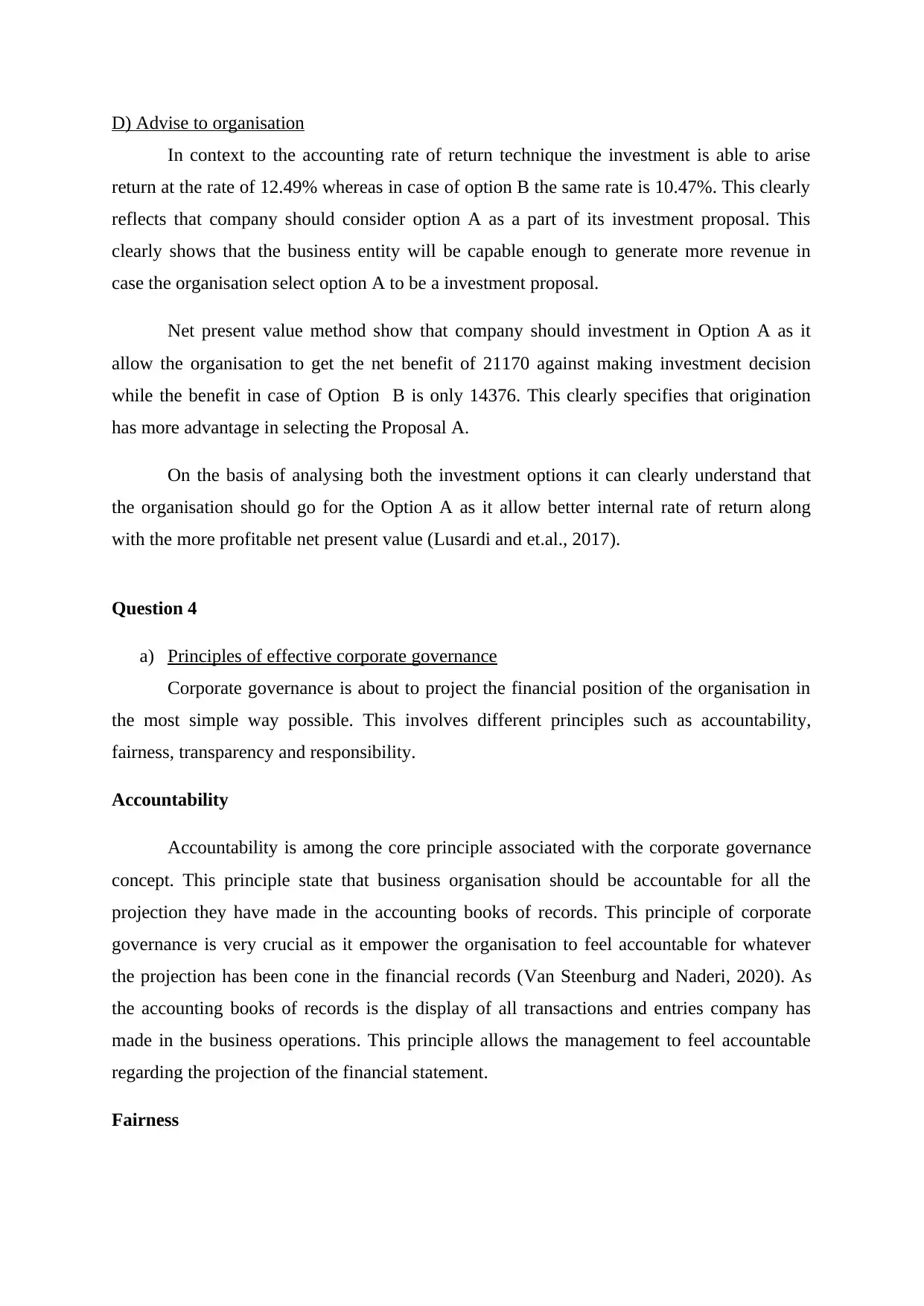

D) Advise to organisation

In context to the accounting rate of return technique the investment is able to arise

return at the rate of 12.49% whereas in case of option B the same rate is 10.47%. This clearly

reflects that company should consider option A as a part of its investment proposal. This

clearly shows that the business entity will be capable enough to generate more revenue in

case the organisation select option A to be a investment proposal.

Net present value method show that company should investment in Option A as it

allow the organisation to get the net benefit of 21170 against making investment decision

while the benefit in case of Option B is only 14376. This clearly specifies that origination

has more advantage in selecting the Proposal A.

On the basis of analysing both the investment options it can clearly understand that

the organisation should go for the Option A as it allow better internal rate of return along

with the more profitable net present value (Lusardi and et.al., 2017).

Question 4

a) Principles of effective corporate governance

Corporate governance is about to project the financial position of the organisation in

the most simple way possible. This involves different principles such as accountability,

fairness, transparency and responsibility.

Accountability

Accountability is among the core principle associated with the corporate governance

concept. This principle state that business organisation should be accountable for all the

projection they have made in the accounting books of records. This principle of corporate

governance is very crucial as it empower the organisation to feel accountable for whatever

the projection has been cone in the financial records (Van Steenburg and Naderi, 2020). As

the accounting books of records is the display of all transactions and entries company has

made in the business operations. This principle allows the management to feel accountable

regarding the projection of the financial statement.

Fairness

In context to the accounting rate of return technique the investment is able to arise

return at the rate of 12.49% whereas in case of option B the same rate is 10.47%. This clearly

reflects that company should consider option A as a part of its investment proposal. This

clearly shows that the business entity will be capable enough to generate more revenue in

case the organisation select option A to be a investment proposal.

Net present value method show that company should investment in Option A as it

allow the organisation to get the net benefit of 21170 against making investment decision

while the benefit in case of Option B is only 14376. This clearly specifies that origination

has more advantage in selecting the Proposal A.

On the basis of analysing both the investment options it can clearly understand that

the organisation should go for the Option A as it allow better internal rate of return along

with the more profitable net present value (Lusardi and et.al., 2017).

Question 4

a) Principles of effective corporate governance

Corporate governance is about to project the financial position of the organisation in

the most simple way possible. This involves different principles such as accountability,

fairness, transparency and responsibility.

Accountability

Accountability is among the core principle associated with the corporate governance

concept. This principle state that business organisation should be accountable for all the

projection they have made in the accounting books of records. This principle of corporate

governance is very crucial as it empower the organisation to feel accountable for whatever

the projection has been cone in the financial records (Van Steenburg and Naderi, 2020). As

the accounting books of records is the display of all transactions and entries company has

made in the business operations. This principle allows the management to feel accountable

regarding the projection of the financial statement.

Fairness

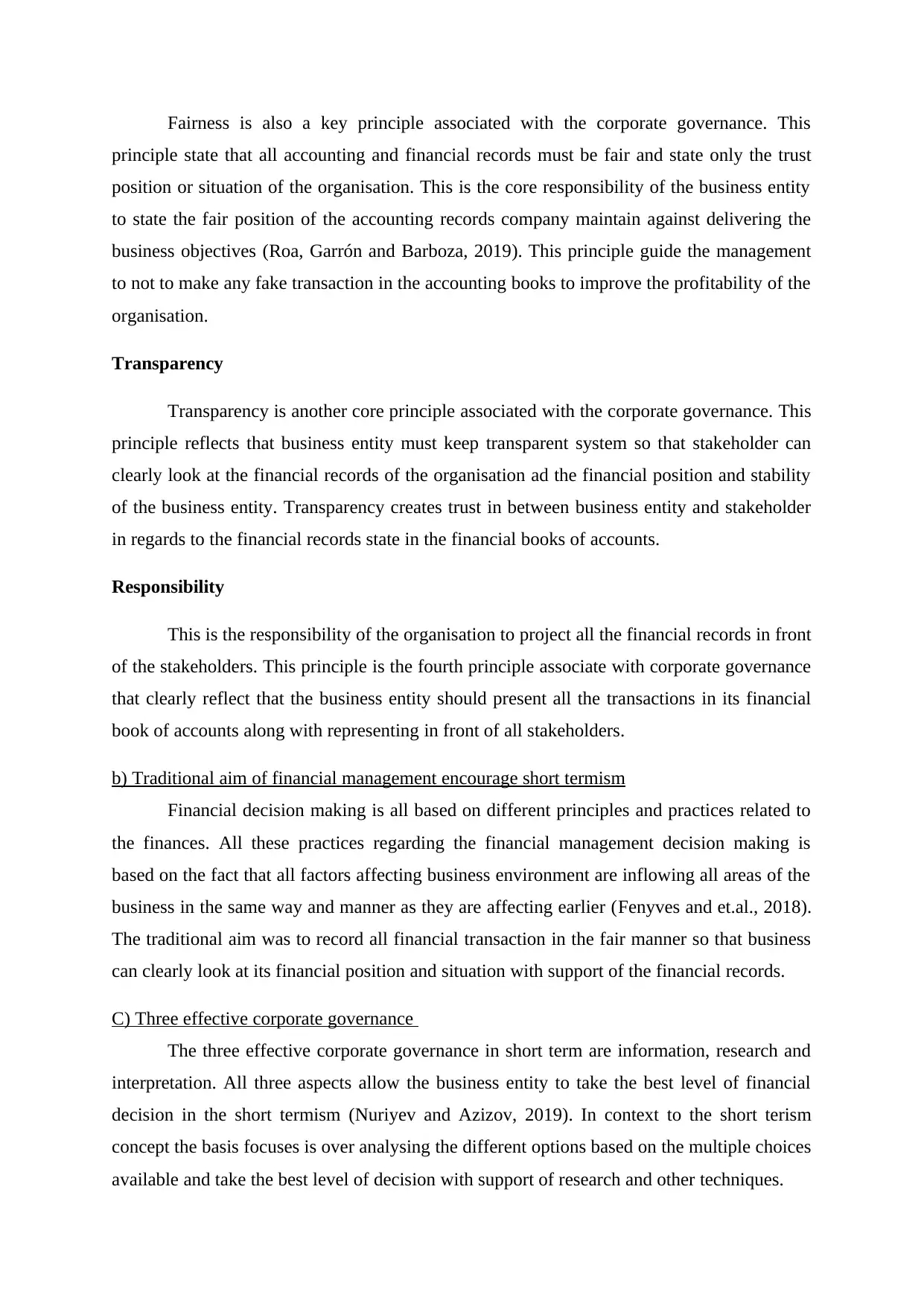

Fairness is also a key principle associated with the corporate governance. This

principle state that all accounting and financial records must be fair and state only the trust

position or situation of the organisation. This is the core responsibility of the business entity

to state the fair position of the accounting records company maintain against delivering the

business objectives (Roa, Garrón and Barboza, 2019). This principle guide the management

to not to make any fake transaction in the accounting books to improve the profitability of the

organisation.

Transparency

Transparency is another core principle associated with the corporate governance. This

principle reflects that business entity must keep transparent system so that stakeholder can

clearly look at the financial records of the organisation ad the financial position and stability

of the business entity. Transparency creates trust in between business entity and stakeholder

in regards to the financial records state in the financial books of accounts.

Responsibility

This is the responsibility of the organisation to project all the financial records in front

of the stakeholders. This principle is the fourth principle associate with corporate governance

that clearly reflect that the business entity should present all the transactions in its financial

book of accounts along with representing in front of all stakeholders.

b) Traditional aim of financial management encourage short termism

Financial decision making is all based on different principles and practices related to

the finances. All these practices regarding the financial management decision making is

based on the fact that all factors affecting business environment are inflowing all areas of the

business in the same way and manner as they are affecting earlier (Fenyves and et.al., 2018).

The traditional aim was to record all financial transaction in the fair manner so that business

can clearly look at its financial position and situation with support of the financial records.

C) Three effective corporate governance

The three effective corporate governance in short term are information, research and

interpretation. All three aspects allow the business entity to take the best level of financial

decision in the short termism (Nuriyev and Azizov, 2019). In context to the short terism

concept the basis focuses is over analysing the different options based on the multiple choices

available and take the best level of decision with support of research and other techniques.

principle state that all accounting and financial records must be fair and state only the trust

position or situation of the organisation. This is the core responsibility of the business entity

to state the fair position of the accounting records company maintain against delivering the

business objectives (Roa, Garrón and Barboza, 2019). This principle guide the management

to not to make any fake transaction in the accounting books to improve the profitability of the

organisation.

Transparency

Transparency is another core principle associated with the corporate governance. This

principle reflects that business entity must keep transparent system so that stakeholder can

clearly look at the financial records of the organisation ad the financial position and stability

of the business entity. Transparency creates trust in between business entity and stakeholder

in regards to the financial records state in the financial books of accounts.

Responsibility

This is the responsibility of the organisation to project all the financial records in front

of the stakeholders. This principle is the fourth principle associate with corporate governance

that clearly reflect that the business entity should present all the transactions in its financial

book of accounts along with representing in front of all stakeholders.

b) Traditional aim of financial management encourage short termism

Financial decision making is all based on different principles and practices related to

the finances. All these practices regarding the financial management decision making is

based on the fact that all factors affecting business environment are inflowing all areas of the

business in the same way and manner as they are affecting earlier (Fenyves and et.al., 2018).

The traditional aim was to record all financial transaction in the fair manner so that business

can clearly look at its financial position and situation with support of the financial records.

C) Three effective corporate governance

The three effective corporate governance in short term are information, research and

interpretation. All three aspects allow the business entity to take the best level of financial

decision in the short termism (Nuriyev and Azizov, 2019). In context to the short terism

concept the basis focuses is over analysing the different options based on the multiple choices

available and take the best level of decision with support of research and other techniques.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.