A Detailed Analysis of Depreciation Practices at Wesfarmers Limited

VerifiedAdded on 2020/02/24

|13

|2698

|168

Report

AI Summary

This report provides a comprehensive analysis of Wesfarmers Limited's depreciation practices, focusing on the company's approach to property, plant, and equipment (PPE). It examines the classification of assets, useful lives, and the quantum of depreciation, referencing the 2016 financial statements. The report explores the methods used, primarily the straight-line method, and the reporting of PPE in the balance sheet and cash flow statements. It delves into the composition and valuation of PPE, including the impact of historical cost, accumulated depreciation, and impairment. The analysis covers depreciation rates, useful lives, and the impact of asset additions, disposals, and foreign currency movements. The report concludes by highlighting Wesfarmers' adherence to accounting standards and proper disclosures, including the capitalization of finance costs related to construction projects. The report provides an overview of the company's financial reporting of depreciation and the management estimates and judgements used in this representation.

By student name

Professor

University

Date: 01 September 2017.

Professor

University

Date: 01 September 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Introduction ……………………………………………………………………..2

Reporting of PPE…………………………………………………….………...3

Composition of PPE…………………………………………………………..6

Methods of depreciation………….……………………………….....….7

Rates and useful life of depreciation………….…………………….7

Amount of depreciation………….……………………………….....…..8

Other reporting……………………….……………………………….....…..8

Refrences.....……………………………………………………………….......11

1 | P a g e

Contents

Introduction ……………………………………………………………………..2

Reporting of PPE…………………………………………………….………...3

Composition of PPE…………………………………………………………..6

Methods of depreciation………….……………………………….....….7

Rates and useful life of depreciation………….…………………….7

Amount of depreciation………….……………………………….....…..8

Other reporting……………………….……………………………….....…..8

Refrences.....……………………………………………………………….......11

1 | P a g e

2

Introduction

Wesfarmers Limited is one of the Australian conglomerate founded in 1914 and listed on the

Australian Stock Exchange. It deals in retail, coal mining, fertilizer, chemical and other industrial products

both in the Australian and in New Zealand markets. It is headquartered in Perth, Western Australia and

is one of the largest retail conglomerate in Australia overpowering companies like BHP Billiton and

Woolworth in terms of revenue. It is the largest company in the private sector in Australia giving

employment to around 220,000 employees. It started as the Western Australian Farmer’s cooperative

and turned into the listed public company. (Jones, 2017)

Depreciation is one of the major costs affecting the financial results and depends on many

factors. For a company like Wesfarmers, where there is a huge volume of the fixed assets, it becomes

important to know how they are classifying the assets into different asset classes, what is the useful life

they are allocating to the assets and what the quantum of depreciation is. It also becomes interesting

that how the same is disclosed in the financials under the head “property, plant and equipment’s” and

what is the management estimate and judgements used in this representation; whether there are any

annual true up or revalidation of the estimated useful life of the assets. (Raiborn, et al., 2016)

As per the revised IFRS reporting and financial management, depreciation can be calculated

either by straight line method or the written down value method and the cost of the asset needs to be

apportioned within the estimated useful life of the asset. In straight-line method, the depreciation is

calculated by dividing the cost of the asset less the salvage value by the estimated useful life of the

asset.

2 | P a g e

Introduction

Wesfarmers Limited is one of the Australian conglomerate founded in 1914 and listed on the

Australian Stock Exchange. It deals in retail, coal mining, fertilizer, chemical and other industrial products

both in the Australian and in New Zealand markets. It is headquartered in Perth, Western Australia and

is one of the largest retail conglomerate in Australia overpowering companies like BHP Billiton and

Woolworth in terms of revenue. It is the largest company in the private sector in Australia giving

employment to around 220,000 employees. It started as the Western Australian Farmer’s cooperative

and turned into the listed public company. (Jones, 2017)

Depreciation is one of the major costs affecting the financial results and depends on many

factors. For a company like Wesfarmers, where there is a huge volume of the fixed assets, it becomes

important to know how they are classifying the assets into different asset classes, what is the useful life

they are allocating to the assets and what the quantum of depreciation is. It also becomes interesting

that how the same is disclosed in the financials under the head “property, plant and equipment’s” and

what is the management estimate and judgements used in this representation; whether there are any

annual true up or revalidation of the estimated useful life of the assets. (Raiborn, et al., 2016)

As per the revised IFRS reporting and financial management, depreciation can be calculated

either by straight line method or the written down value method and the cost of the asset needs to be

apportioned within the estimated useful life of the asset. In straight-line method, the depreciation is

calculated by dividing the cost of the asset less the salvage value by the estimated useful life of the

asset.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

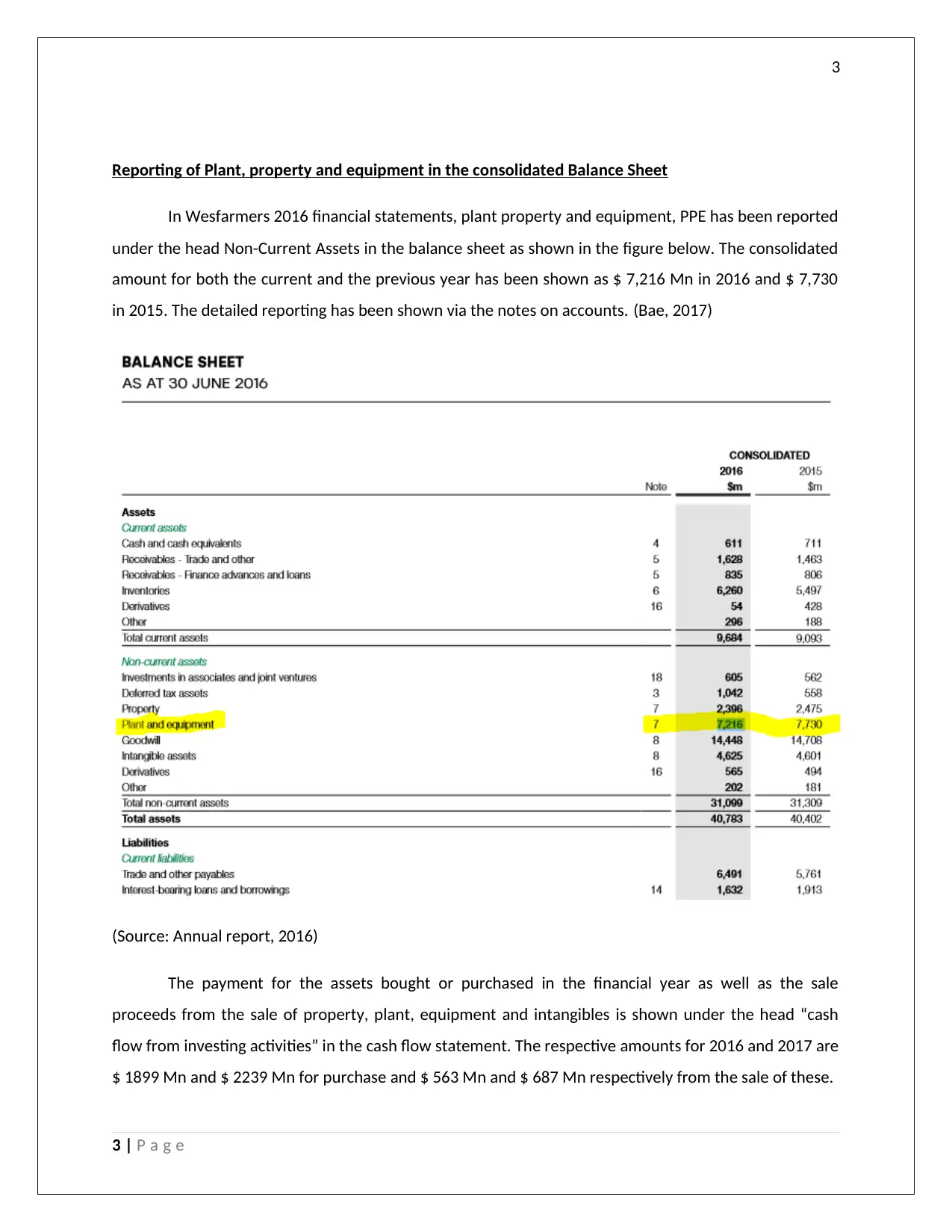

Reporting of Plant, property and equipment in the consolidated Balance Sheet

In Wesfarmers 2016 financial statements, plant property and equipment, PPE has been reported

under the head Non-Current Assets in the balance sheet as shown in the figure below. The consolidated

amount for both the current and the previous year has been shown as $ 7,216 Mn in 2016 and $ 7,730

in 2015. The detailed reporting has been shown via the notes on accounts. (Bae, 2017)

(Source: Annual report, 2016)

The payment for the assets bought or purchased in the financial year as well as the sale

proceeds from the sale of property, plant, equipment and intangibles is shown under the head “cash

flow from investing activities” in the cash flow statement. The respective amounts for 2016 and 2017 are

$ 1899 Mn and $ 2239 Mn for purchase and $ 563 Mn and $ 687 Mn respectively from the sale of these.

3 | P a g e

Reporting of Plant, property and equipment in the consolidated Balance Sheet

In Wesfarmers 2016 financial statements, plant property and equipment, PPE has been reported

under the head Non-Current Assets in the balance sheet as shown in the figure below. The consolidated

amount for both the current and the previous year has been shown as $ 7,216 Mn in 2016 and $ 7,730

in 2015. The detailed reporting has been shown via the notes on accounts. (Bae, 2017)

(Source: Annual report, 2016)

The payment for the assets bought or purchased in the financial year as well as the sale

proceeds from the sale of property, plant, equipment and intangibles is shown under the head “cash

flow from investing activities” in the cash flow statement. The respective amounts for 2016 and 2017 are

$ 1899 Mn and $ 2239 Mn for purchase and $ 563 Mn and $ 687 Mn respectively from the sale of these.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

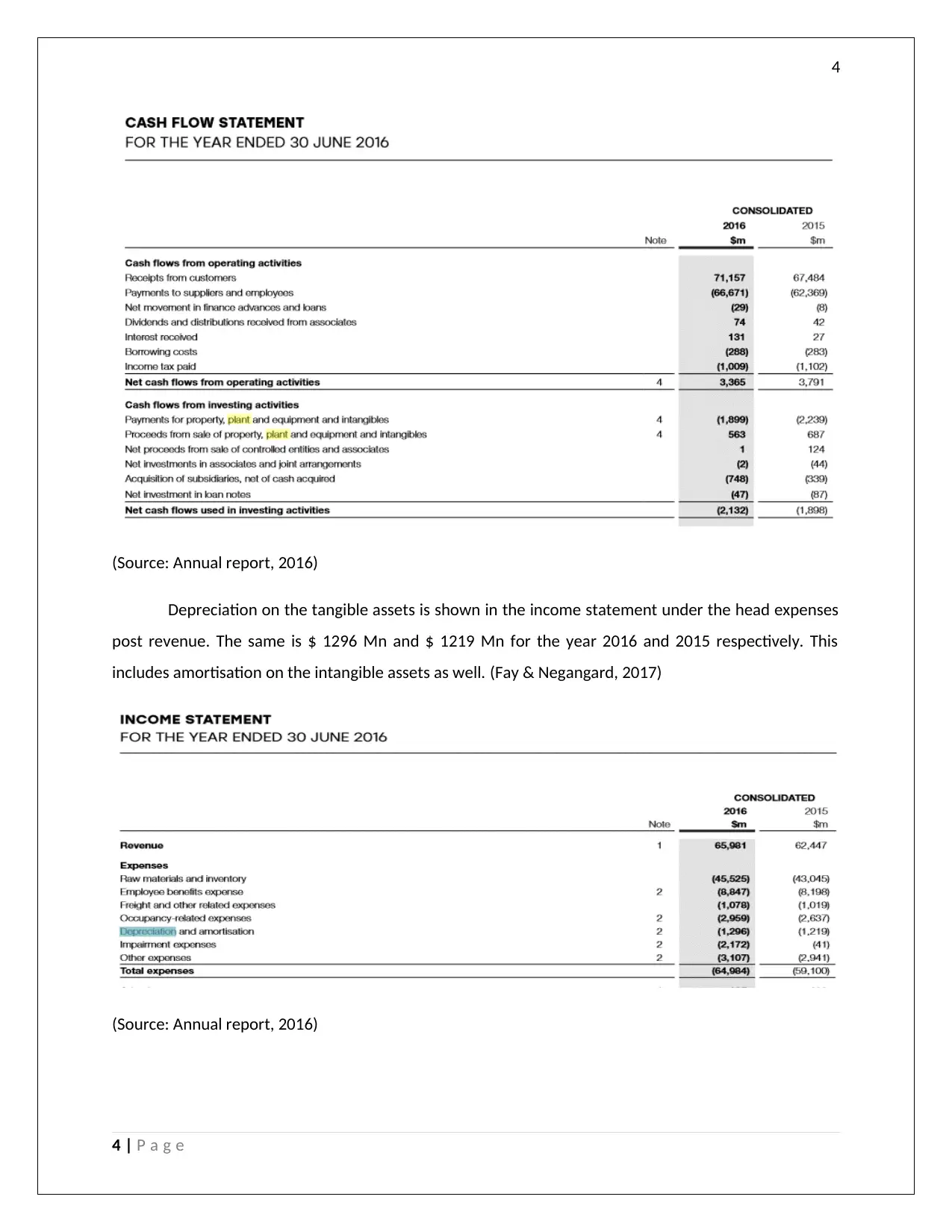

(Source: Annual report, 2016)

Depreciation on the tangible assets is shown in the income statement under the head expenses

post revenue. The same is $ 1296 Mn and $ 1219 Mn for the year 2016 and 2015 respectively. This

includes amortisation on the intangible assets as well. (Fay & Negangard, 2017)

(Source: Annual report, 2016)

4 | P a g e

(Source: Annual report, 2016)

Depreciation on the tangible assets is shown in the income statement under the head expenses

post revenue. The same is $ 1296 Mn and $ 1219 Mn for the year 2016 and 2015 respectively. This

includes amortisation on the intangible assets as well. (Fay & Negangard, 2017)

(Source: Annual report, 2016)

4 | P a g e

5

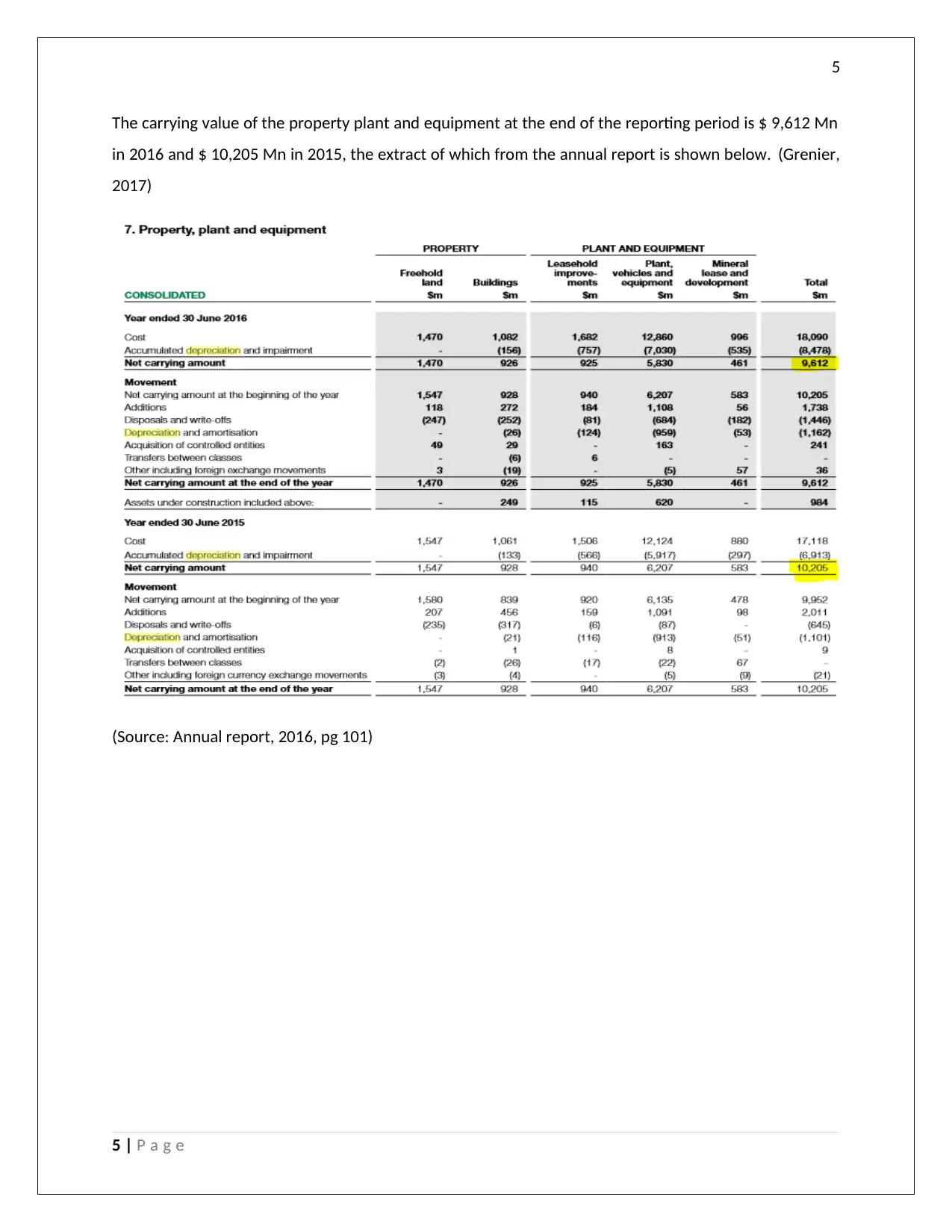

The carrying value of the property plant and equipment at the end of the reporting period is $ 9,612 Mn

in 2016 and $ 10,205 Mn in 2015, the extract of which from the annual report is shown below. (Grenier,

2017)

(Source: Annual report, 2016, pg 101)

5 | P a g e

The carrying value of the property plant and equipment at the end of the reporting period is $ 9,612 Mn

in 2016 and $ 10,205 Mn in 2015, the extract of which from the annual report is shown below. (Grenier,

2017)

(Source: Annual report, 2016, pg 101)

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Composition of Property, Plant and Equipment and valuation of the same:

The property, plant and equipment of Wesfarmers consists of different asset classes namely

Freehold Land and Building comprising the property and leasehold improvements, Plant, vehicles and

equipment, Mineral lease and developments together comprising the Plant and Equipment. The

reported figure of carrying value is calculated by historical cost of the asset less accumulated

depreciation less impairment on the asset, if any. Any cost incurred on the development of the asset

that increases the future economic benefits of the assets or increase the life of the asset are capitalised

in the value of the asset. Any major inspection cost incurred, if any, is also considered for capitalisation

with the value of the main asset. Generally, the assets are valued at historical cost but the useful life as

well as the methods of amortization are being reviewed annually to check for impairment, if any. These

are purely based on management estimates and judgements and thus, depends on the circumstances of

the case. In case any modification is done in the value or estimated useful life of the assets, the same is

done prospectively for the remainder life of the assets including the current as well as the future years.

Such reassessment is generally required in case of specific changes in the business environment like

huge changes in the price of raw material or change in the performance of store. This impact a specific

group of assets and a reasonable call is generally taken by the management such that there is no

material change in the financials or estimated useful lives, or methods of depreciation. In case the

business combination is done and assets are acquired as a part of it, the assets are generally valued

using the fair valuation approach and a reasonable discount rate is applied which helps to determine the

amount to be paid as purchase consideration. (Knechel & Salterio, 2016)

6 | P a g e

Composition of Property, Plant and Equipment and valuation of the same:

The property, plant and equipment of Wesfarmers consists of different asset classes namely

Freehold Land and Building comprising the property and leasehold improvements, Plant, vehicles and

equipment, Mineral lease and developments together comprising the Plant and Equipment. The

reported figure of carrying value is calculated by historical cost of the asset less accumulated

depreciation less impairment on the asset, if any. Any cost incurred on the development of the asset

that increases the future economic benefits of the assets or increase the life of the asset are capitalised

in the value of the asset. Any major inspection cost incurred, if any, is also considered for capitalisation

with the value of the main asset. Generally, the assets are valued at historical cost but the useful life as

well as the methods of amortization are being reviewed annually to check for impairment, if any. These

are purely based on management estimates and judgements and thus, depends on the circumstances of

the case. In case any modification is done in the value or estimated useful life of the assets, the same is

done prospectively for the remainder life of the assets including the current as well as the future years.

Such reassessment is generally required in case of specific changes in the business environment like

huge changes in the price of raw material or change in the performance of store. This impact a specific

group of assets and a reasonable call is generally taken by the management such that there is no

material change in the financials or estimated useful lives, or methods of depreciation. In case the

business combination is done and assets are acquired as a part of it, the assets are generally valued

using the fair valuation approach and a reasonable discount rate is applied which helps to determine the

amount to be paid as purchase consideration. (Knechel & Salterio, 2016)

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Methods of depreciation used for various categories of assets:

The depreciation on the assets is generally charged using the straight-line method over the

estimated useful life of most of the asset classes. In case, the rate or the useful life is revised in between,

the same is taken on the prospective basis and adjusted in the value of the asset. Leasehold

improvements are also depreciated over the lease contract period or the useful life, whichever is lower,

using the straight-line method. In case the asset is no longer usable or when it is expected to give no

future economic benefits, the same is sold or disposed off and the income or loss arising on it is

recognised in the income statement or profit and loss account. (Sonu, et al., 2017)

Rates of depreciation or the useful lives of the assets used by the company

The Wesfarmers group has disclosed the useful life of the asset over which the company

depreciated its assets. Though not very specific, but it has given the range within which the useful life of

the asset class lies. The specific estimation of the useful life of the particular assets depends on the

management judgement and decision. Buildings is usually depreciated over the period of 20-40 years

whereas plant and equipment consisting of vehicles too, are depreciated over the life ranging between 3

to 40 years. The expenditure which is done on the mining areas and which require the research

expenditure are depreciated when the same is capitalised to use and over the period for which the

economically recoverable resources will last. In case, the production has not yet started from the mine,

the depreciation will not start. The other category is land, being non-depreciable resources, depreciation

is not charged on it. Finally, in case of the leasehold improvement or assets acquired under lease, the

asset are depreciated over the life of the lease term or the estimated useful life of the individual assets,

whichever is lower. (Das, 2017)

7 | P a g e

Methods of depreciation used for various categories of assets:

The depreciation on the assets is generally charged using the straight-line method over the

estimated useful life of most of the asset classes. In case, the rate or the useful life is revised in between,

the same is taken on the prospective basis and adjusted in the value of the asset. Leasehold

improvements are also depreciated over the lease contract period or the useful life, whichever is lower,

using the straight-line method. In case the asset is no longer usable or when it is expected to give no

future economic benefits, the same is sold or disposed off and the income or loss arising on it is

recognised in the income statement or profit and loss account. (Sonu, et al., 2017)

Rates of depreciation or the useful lives of the assets used by the company

The Wesfarmers group has disclosed the useful life of the asset over which the company

depreciated its assets. Though not very specific, but it has given the range within which the useful life of

the asset class lies. The specific estimation of the useful life of the particular assets depends on the

management judgement and decision. Buildings is usually depreciated over the period of 20-40 years

whereas plant and equipment consisting of vehicles too, are depreciated over the life ranging between 3

to 40 years. The expenditure which is done on the mining areas and which require the research

expenditure are depreciated when the same is capitalised to use and over the period for which the

economically recoverable resources will last. In case, the production has not yet started from the mine,

the depreciation will not start. The other category is land, being non-depreciable resources, depreciation

is not charged on it. Finally, in case of the leasehold improvement or assets acquired under lease, the

asset are depreciated over the life of the lease term or the estimated useful life of the individual assets,

whichever is lower. (Das, 2017)

7 | P a g e

8

Amount of depreciation charged on the asset for the current and the previous years

As per the extracts given in the financials, depreciation charged for the year 2016 has increased

marginally over the year 2015. This is primarily because of the additions done in 2016 amounting to $

1,738 Mn, majorly comprising of Plant, vehicles and equipment ($ 1,108 Mn). The total depreciated

reported for the year 2016 is $ 1,162 Mn comprising of $ 26 Mn on buildings, $124 Mn on leasehold

improvement assets, $ 959 Mn on plant, equipment and vehicles and $ 53 Mn on the mineral lease and

development asset class. Whereas the depreciation for the year 2015 was reported to be $ 1,101 Mn on

aggregate basis, comprising of $ 21 Mn on buildings, $116 Mn on leasehold improvement assets, $ 913

Mn on plant, equipment and vehicles and $ 51 Mn on the mineral lease and development asset class.

The accumulated depreciation as on 30th June 2016 and 30th June 2015 stands to $ 8,478 Mn and $ 6,913

Mn respectively. (David, 2005)

Other reporting on the Plant, Property and Equipment

From the financial statements, it is clear that the company has had many transactions pertaining

to the purchase, sale, inter unit transfers, inter entity transfer, etc. The total additions for the year 2016

is $ 1,738 Mn comprising of $ 118 Mn to the Freehold building asset class, $ 272 Mn to buildings, $184

Mn to leasehold improvement assets, $ 1,108 Mn to plant, equipment and vehicles and $ 56 Mn to the

mineral lease and development asset class. Whereas the additions for the year 2015 were to the tune of

$ 2,011 Mn on aggregate basis, comprising of $ 207 Mn on Freehold land, $ 456 Mn on buildings, $ 159

Mn on leasehold improvement assets, $ 1,091 Mn on plant, equipment and vehicles and $ 98 Mn on the

mineral lease and development asset class. Apart from the addition, there has been disposals and write

off the assets because of end of life, or non-traceable or not in use or those that are having no future

economic benefit to the tune of $ 1,446 Mn in 2016 and $ 645 Mn in 2015. This is reported in terms of

the Gross Block. There has also been acquisition of some of the assets of the controlled entities

amounting $ 241 Mn and $ 9 Mn in 2016 and 2015 respectively. The inter unit transfer of the assets and

also the inter movement of the assets between the asset classes in case they are wrongly classified in

the previous year becomes zero in the net position. Since the assets are generally reported in the

respective entity currency, they can be different from the reporting currency of the group because of

which there is a foreign currency movement, which needs to be adjusted in the PPE. In case of

8 | P a g e

Amount of depreciation charged on the asset for the current and the previous years

As per the extracts given in the financials, depreciation charged for the year 2016 has increased

marginally over the year 2015. This is primarily because of the additions done in 2016 amounting to $

1,738 Mn, majorly comprising of Plant, vehicles and equipment ($ 1,108 Mn). The total depreciated

reported for the year 2016 is $ 1,162 Mn comprising of $ 26 Mn on buildings, $124 Mn on leasehold

improvement assets, $ 959 Mn on plant, equipment and vehicles and $ 53 Mn on the mineral lease and

development asset class. Whereas the depreciation for the year 2015 was reported to be $ 1,101 Mn on

aggregate basis, comprising of $ 21 Mn on buildings, $116 Mn on leasehold improvement assets, $ 913

Mn on plant, equipment and vehicles and $ 51 Mn on the mineral lease and development asset class.

The accumulated depreciation as on 30th June 2016 and 30th June 2015 stands to $ 8,478 Mn and $ 6,913

Mn respectively. (David, 2005)

Other reporting on the Plant, Property and Equipment

From the financial statements, it is clear that the company has had many transactions pertaining

to the purchase, sale, inter unit transfers, inter entity transfer, etc. The total additions for the year 2016

is $ 1,738 Mn comprising of $ 118 Mn to the Freehold building asset class, $ 272 Mn to buildings, $184

Mn to leasehold improvement assets, $ 1,108 Mn to plant, equipment and vehicles and $ 56 Mn to the

mineral lease and development asset class. Whereas the additions for the year 2015 were to the tune of

$ 2,011 Mn on aggregate basis, comprising of $ 207 Mn on Freehold land, $ 456 Mn on buildings, $ 159

Mn on leasehold improvement assets, $ 1,091 Mn on plant, equipment and vehicles and $ 98 Mn on the

mineral lease and development asset class. Apart from the addition, there has been disposals and write

off the assets because of end of life, or non-traceable or not in use or those that are having no future

economic benefit to the tune of $ 1,446 Mn in 2016 and $ 645 Mn in 2015. This is reported in terms of

the Gross Block. There has also been acquisition of some of the assets of the controlled entities

amounting $ 241 Mn and $ 9 Mn in 2016 and 2015 respectively. The inter unit transfer of the assets and

also the inter movement of the assets between the asset classes in case they are wrongly classified in

the previous year becomes zero in the net position. Since the assets are generally reported in the

respective entity currency, they can be different from the reporting currency of the group because of

which there is a foreign currency movement, which needs to be adjusted in the PPE. In case of

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Wesfarmers, the same was $ 36 Mn gain and $ 21 Mn loss in the year 2016 and 2015 respectively. (Félix,

2017)

Asset under construction is shown separately in the financials but the same is reported under

the head Property, plant and equipment’s only and included in the Gross Block. The total amount of

asset under construction for year 2016 and 2015 were $ 984 Mn and $ 1,104 Mn respectively. These

mainly comprise of leasehold improvement and plant, vehicles and equipments. (Murray & Markey‐

Towler, 2017)

Conclusion

Finance costs which are incurred on the major capital projects, which are under construction

and will require substantial development are categorized under the head borrowing costs and are

capitalised as part of the construction costs. This is in compliance of the accounting standards and IFRS

which says the the interest and the finance costs in case of the qualifying asset can be capitalized in the

value of the project. To arrive at the value of the amount of interest to be capitalised, the Wesfarmers

group makes use of the weighted average interest rate on the borrowing, which are outstanding over

the year. The computation which has been used to calculate interest rates has given 4.15% and 5% as

the rates of interest for the year 2016 and 2015 respectively. (J, 2016) Hence we see that the company

has followed all the relevant provisions that are related to the accounting process overall and all the

relevant disclosure in respect to the same has been given properly. All the calculations and working are

properly explained and provided for. The company is following a method of fair value of accounting and

all the important disclosures have been provided for.

9 | P a g e

Wesfarmers, the same was $ 36 Mn gain and $ 21 Mn loss in the year 2016 and 2015 respectively. (Félix,

2017)

Asset under construction is shown separately in the financials but the same is reported under

the head Property, plant and equipment’s only and included in the Gross Block. The total amount of

asset under construction for year 2016 and 2015 were $ 984 Mn and $ 1,104 Mn respectively. These

mainly comprise of leasehold improvement and plant, vehicles and equipments. (Murray & Markey‐

Towler, 2017)

Conclusion

Finance costs which are incurred on the major capital projects, which are under construction

and will require substantial development are categorized under the head borrowing costs and are

capitalised as part of the construction costs. This is in compliance of the accounting standards and IFRS

which says the the interest and the finance costs in case of the qualifying asset can be capitalized in the

value of the project. To arrive at the value of the amount of interest to be capitalised, the Wesfarmers

group makes use of the weighted average interest rate on the borrowing, which are outstanding over

the year. The computation which has been used to calculate interest rates has given 4.15% and 5% as

the rates of interest for the year 2016 and 2015 respectively. (J, 2016) Hence we see that the company

has followed all the relevant provisions that are related to the accounting process overall and all the

relevant disclosure in respect to the same has been given properly. All the calculations and working are

properly explained and provided for. The company is following a method of fair value of accounting and

all the important disclosures have been provided for.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

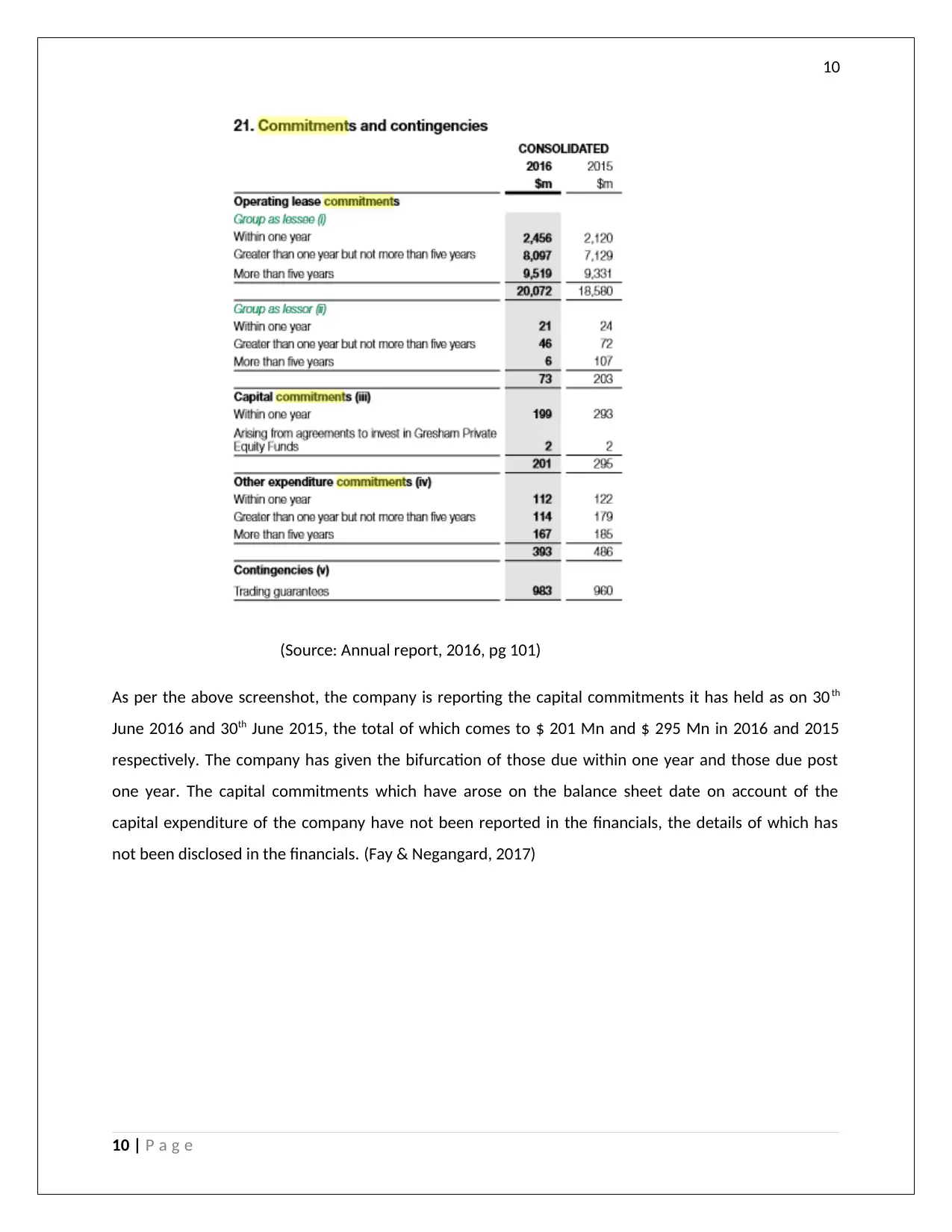

(Source: Annual report, 2016, pg 101)

As per the above screenshot, the company is reporting the capital commitments it has held as on 30 th

June 2016 and 30th June 2015, the total of which comes to $ 201 Mn and $ 295 Mn in 2016 and 2015

respectively. The company has given the bifurcation of those due within one year and those due post

one year. The capital commitments which have arose on the balance sheet date on account of the

capital expenditure of the company have not been reported in the financials, the details of which has

not been disclosed in the financials. (Fay & Negangard, 2017)

10 | P a g e

(Source: Annual report, 2016, pg 101)

As per the above screenshot, the company is reporting the capital commitments it has held as on 30 th

June 2016 and 30th June 2015, the total of which comes to $ 201 Mn and $ 295 Mn in 2016 and 2015

respectively. The company has given the bifurcation of those due within one year and those due post

one year. The capital commitments which have arose on the balance sheet date on account of the

capital expenditure of the company have not been reported in the financials, the details of which has

not been disclosed in the financials. (Fay & Negangard, 2017)

10 | P a g e

11

References

Bae, S., 2017. The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea. Journal of Applied Business Research, 33(1), pp. 153-172.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

David, 2005. [Online].

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Félix, M., 2017. A study on the expected impact of IFRS 17 on the transparency of financial statements of

insurance companies. MASTER THESIS, pp. 1-69.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

J, G., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

11 | P a g e

References

Bae, S., 2017. The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea. Journal of Applied Business Research, 33(1), pp. 153-172.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

David, 2005. [Online].

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Félix, M., 2017. A study on the expected impact of IFRS 17 on the transparency of financial statements of

insurance companies. MASTER THESIS, pp. 1-69.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

J, G., 2016. Principles of Australian Contract Law. Australia: Lexis Nexis.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13