Western Sydney University Taxation Law 200187 Autumn 2019 Assignment

VerifiedAdded on 2023/01/18

|5

|1282

|99

Homework Assignment

AI Summary

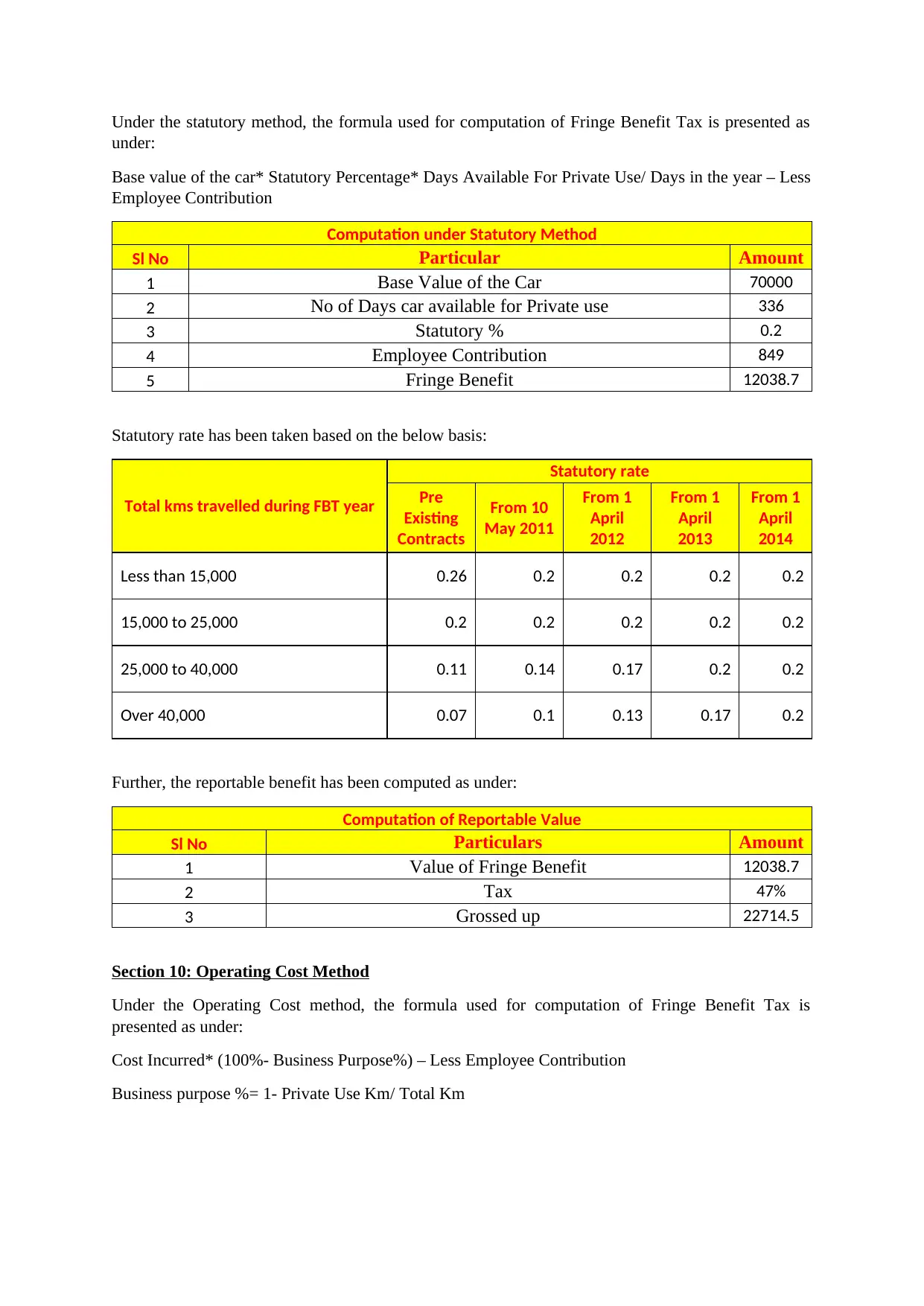

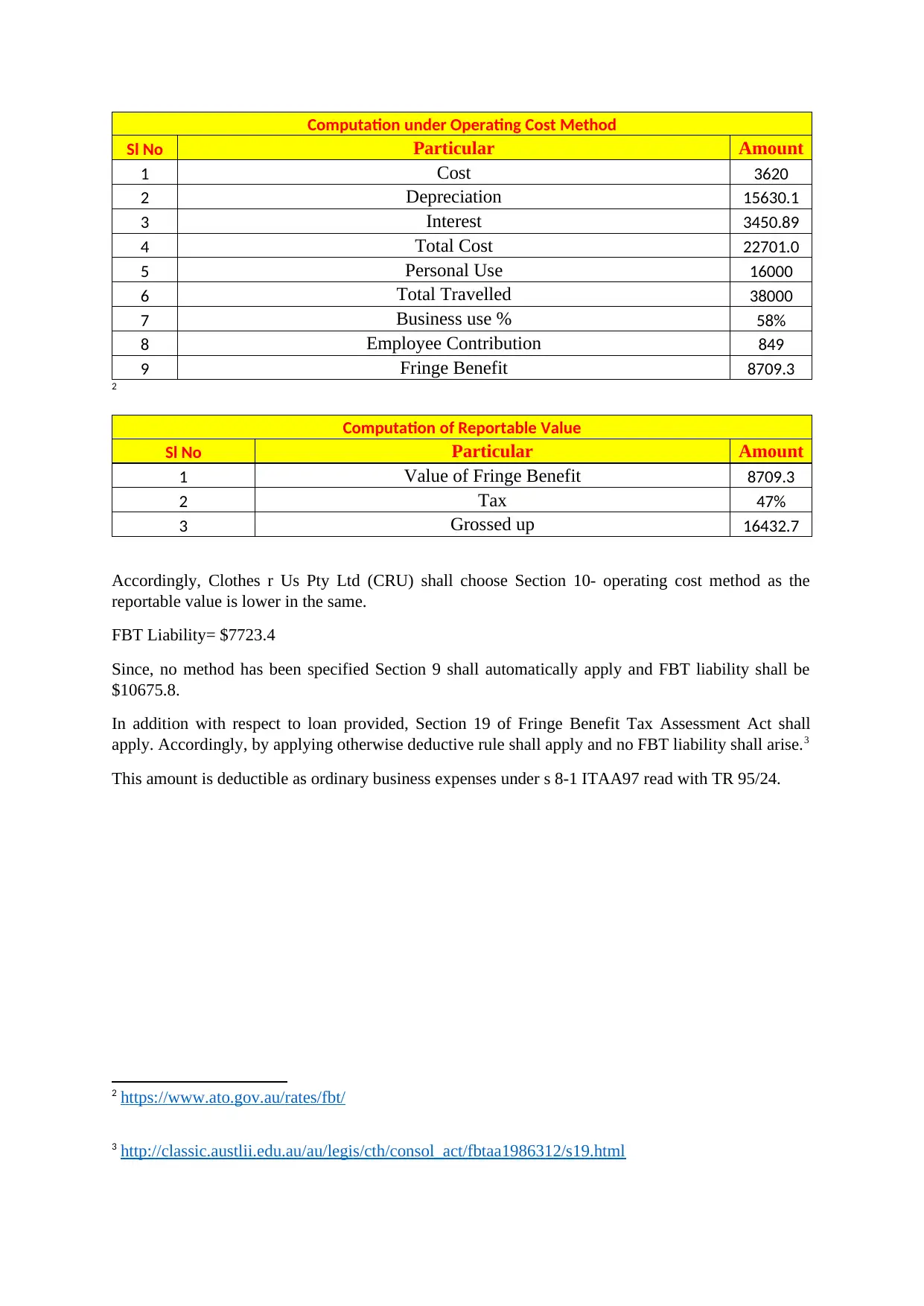

This document provides a comprehensive solution to a Taxation Law assignment from Western Sydney University, specifically for the 200187 course in Autumn 2019. The assignment consists of two questions. The first question focuses on determining the scope of a business, analyzing whether income from property renovation and sale constitutes ordinary income or capital income, referencing cases like Memorex v FCT, GP International Pipecoaters v FC, and FCT v Merv Brown. The second question addresses Fringe Benefit Tax (FBT) implications for a company director, calculating FBT liability using both the statutory method and the operating cost method, and considering the tax treatment of a company loan. The solution includes detailed calculations, legal analysis, and references to relevant legislation and case law, such as the Fringe Benefit Tax Assessment Act, and ATO rulings.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.