Analyzing the 2008 Financial Crisis in Light of the COVID-19 Pandemic

VerifiedAdded on 2023/01/07

|10

|2672

|32

Report

AI Summary

This report delves into the 2008 global financial crisis, examining its causes, impacts, and potential lessons learned in the context of the COVID-19 pandemic. It analyzes the influence of externalities on the mortgage market, exploring the application of the Coase theorem and the role of shared responsibility mortgages in mitigating negative impacts. The report investigates the effects of securitization on supply and demand diagrams, considering the views of Amir Sufi and Atif Mian on the crisis's origins and the potential of shared responsibility mortgages in preventing future financial instability. It also explores the impact of changes in aggregate demand and supply, focusing on the Australian government's stimulus measures. Furthermore, it examines the debate around financial innovations aimed at creating safe debt, assessing whether they caused the crisis or were a consequence of the housing bubble's collapse. The report concludes with recommendations based on these analyses.

What does the Covid-19

pandemic teach us

about the global

financial crisis of 2008?

pandemic teach us

about the global

financial crisis of 2008?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Present report is mainly based upon the global financial crisis that affected the whole

world during the year 2008. the major impact of it was faced by housing industry and the prices

of houses and economy growth were two of the main factors which were impacted due to them.

This report focuses upon the externalities that are affecting these factors and resulting in changes

in demand and supply curve of the standard debt mortgage.

Present report is mainly based upon the global financial crisis that affected the whole

world during the year 2008. the major impact of it was faced by housing industry and the prices

of houses and economy growth were two of the main factors which were impacted due to them.

This report focuses upon the externalities that are affecting these factors and resulting in changes

in demand and supply curve of the standard debt mortgage.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 a. Diagram to show the demand and supply curve for standard debt mortgage and the way in

which externalities affect the diagram.........................................................................................1

1 b. Discussion of the applicability of Coase theorem in mitigating the negative externalities

that are associated with standard debt mortgage contract............................................................2

2. The way in which shared responsibility mortgages mitigate the negative externality

associated with standard debt mortgages.....................................................................................2

3. The effect of securitization in the diagram of supply and demand..........................................2

4. Explanation of the factors that caused the crisis in Amir Sufi and Atif Mian's view and the

way in which shared responsibility mortgages would prevent such crisis in future....................3

5. Impact of the changes in an aggregate demand and supply diagram.......................................3

6. Explanation of that if shared responsibility mortgages are widely adopted and they are

securitized to create sate debt would it prevent a future financial crisis.....................................4

7. Did financial innovations aimed at creating safe debt cause the crisis or was it primarily

caused by the collapse of the housing bubble?............................................................................4

CONCLUSION and RECOMMENDATION..................................................................................6

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 a. Diagram to show the demand and supply curve for standard debt mortgage and the way in

which externalities affect the diagram.........................................................................................1

1 b. Discussion of the applicability of Coase theorem in mitigating the negative externalities

that are associated with standard debt mortgage contract............................................................2

2. The way in which shared responsibility mortgages mitigate the negative externality

associated with standard debt mortgages.....................................................................................2

3. The effect of securitization in the diagram of supply and demand..........................................2

4. Explanation of the factors that caused the crisis in Amir Sufi and Atif Mian's view and the

way in which shared responsibility mortgages would prevent such crisis in future....................3

5. Impact of the changes in an aggregate demand and supply diagram.......................................3

6. Explanation of that if shared responsibility mortgages are widely adopted and they are

securitized to create sate debt would it prevent a future financial crisis.....................................4

7. Did financial innovations aimed at creating safe debt cause the crisis or was it primarily

caused by the collapse of the housing bubble?............................................................................4

CONCLUSION and RECOMMENDATION..................................................................................6

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

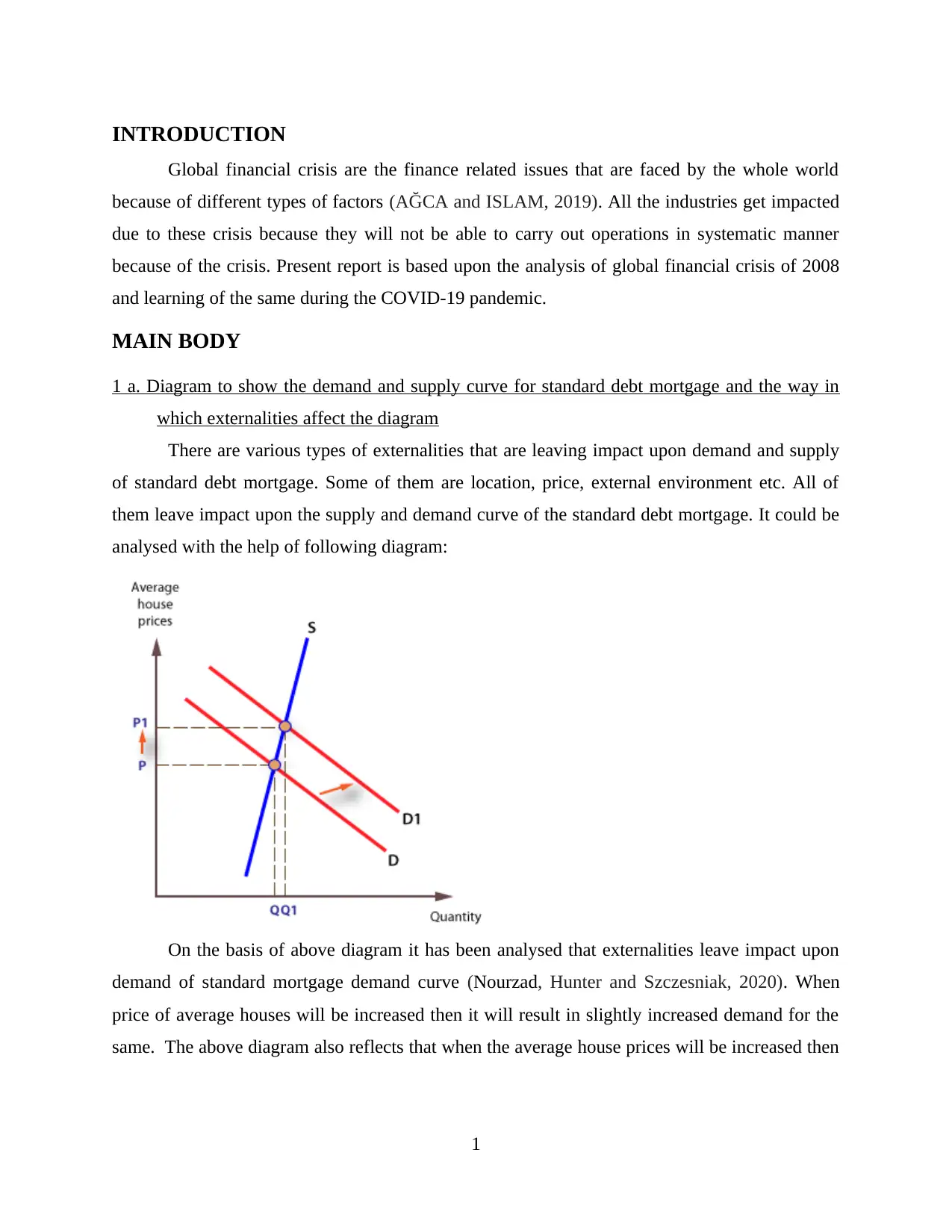

INTRODUCTION

Global financial crisis are the finance related issues that are faced by the whole world

because of different types of factors (AĞCA and ISLAM, 2019). All the industries get impacted

due to these crisis because they will not be able to carry out operations in systematic manner

because of the crisis. Present report is based upon the analysis of global financial crisis of 2008

and learning of the same during the COVID-19 pandemic.

MAIN BODY

1 a. Diagram to show the demand and supply curve for standard debt mortgage and the way in

which externalities affect the diagram

There are various types of externalities that are leaving impact upon demand and supply

of standard debt mortgage. Some of them are location, price, external environment etc. All of

them leave impact upon the supply and demand curve of the standard debt mortgage. It could be

analysed with the help of following diagram:

On the basis of above diagram it has been analysed that externalities leave impact upon

demand of standard mortgage demand curve (Nourzad, Hunter and Szczesniak, 2020). When

price of average houses will be increased then it will result in slightly increased demand for the

same. The above diagram also reflects that when the average house prices will be increased then

1

Global financial crisis are the finance related issues that are faced by the whole world

because of different types of factors (AĞCA and ISLAM, 2019). All the industries get impacted

due to these crisis because they will not be able to carry out operations in systematic manner

because of the crisis. Present report is based upon the analysis of global financial crisis of 2008

and learning of the same during the COVID-19 pandemic.

MAIN BODY

1 a. Diagram to show the demand and supply curve for standard debt mortgage and the way in

which externalities affect the diagram

There are various types of externalities that are leaving impact upon demand and supply

of standard debt mortgage. Some of them are location, price, external environment etc. All of

them leave impact upon the supply and demand curve of the standard debt mortgage. It could be

analysed with the help of following diagram:

On the basis of above diagram it has been analysed that externalities leave impact upon

demand of standard mortgage demand curve (Nourzad, Hunter and Szczesniak, 2020). When

price of average houses will be increased then it will result in slightly increased demand for the

same. The above diagram also reflects that when the average house prices will be increased then

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

it will result in increased supply of the houses because when the prices will be high competition

in the market will be increased.

1 b. Discussion of the applicability of Coase theorem in mitigating the negative externalities that

are associated with standard debt mortgage contract

Coase theorem was developed by Ronald Coase and it affirms that if the market will be

highly competitive then there will be no transaction cost. It could be applied for the purpose of

minimising the negative externalities which are associated with standard debt mortgage contract.

With the help of it, the way in which all the conflicts between the businesses that are competing

with each other could be resolved which will mitigate the negative impact of externalities which

is related to standard debt mortgage.

2. The way in which shared responsibility mortgages mitigate the negative externality associated

with standard debt mortgages

All the mortgages that are predominantly used in the housing finance and promoted by

the government and have a very small amount of risk are known as shared responsibility

mortgages. These are used for the purpose of mitigating the negative externality which is related

to the standard debt mortgages. The responsibility in such types of mortgages is shared with two

or more parties that results in decrement of the negative externalities in the standard debt. All the

parties which will be concerned with the property will share the risk as well as the issues related

to the mortgage (Lauretta, 2018).

3. The effect of securitization in the diagram of supply and demand

Securitization could be defined as the procedure of taking liquid assets or the groups of

the assets through financial engineering and transforming them into security. It may leave impact

upon the diagram of supply and demand curve because when the individuals will transform all

their assets and liabilities then it may increase the prices which will result in changes in the chart.

It has negative impact on the proxies of the supply side of the economy than the growth. Apart

from this, it is consistent with a shift from investment to consumption that constrains the supply

side of the economy. It also boosts the demand and lead to the highly muted impact on the GDP.

2

in the market will be increased.

1 b. Discussion of the applicability of Coase theorem in mitigating the negative externalities that

are associated with standard debt mortgage contract

Coase theorem was developed by Ronald Coase and it affirms that if the market will be

highly competitive then there will be no transaction cost. It could be applied for the purpose of

minimising the negative externalities which are associated with standard debt mortgage contract.

With the help of it, the way in which all the conflicts between the businesses that are competing

with each other could be resolved which will mitigate the negative impact of externalities which

is related to standard debt mortgage.

2. The way in which shared responsibility mortgages mitigate the negative externality associated

with standard debt mortgages

All the mortgages that are predominantly used in the housing finance and promoted by

the government and have a very small amount of risk are known as shared responsibility

mortgages. These are used for the purpose of mitigating the negative externality which is related

to the standard debt mortgages. The responsibility in such types of mortgages is shared with two

or more parties that results in decrement of the negative externalities in the standard debt. All the

parties which will be concerned with the property will share the risk as well as the issues related

to the mortgage (Lauretta, 2018).

3. The effect of securitization in the diagram of supply and demand

Securitization could be defined as the procedure of taking liquid assets or the groups of

the assets through financial engineering and transforming them into security. It may leave impact

upon the diagram of supply and demand curve because when the individuals will transform all

their assets and liabilities then it may increase the prices which will result in changes in the chart.

It has negative impact on the proxies of the supply side of the economy than the growth. Apart

from this, it is consistent with a shift from investment to consumption that constrains the supply

side of the economy. It also boosts the demand and lead to the highly muted impact on the GDP.

2

4. Explanation of the factors that caused the crisis in Amir Sufi and Atif Mian's view and the way

in which shared responsibility mortgages would prevent such crisis in future

There are various types if factors that are resulting in the crisis in Amir Sufi and Atif

Mian's view. These are debt contracts, foreclosure, price, locations etc. all of them are some of

the key externalities that are leaving impact upon the economy as well as housing prices. It is

very important to deal with all these factors in systematic manner. All the crisis could be dealt by

using shared responsibility mortgages (Nikolova, Rodionov and Mottaeva, 2016). These could

prevent the crisis such as decreased economy growth and increased housing prices. All the

shared responsibility mortgages have such owners who are sharing risks that are associated with

the property. It can help to deal with all the factors that may result in crisis as the negative

implications of them will be shared by two or more parties.

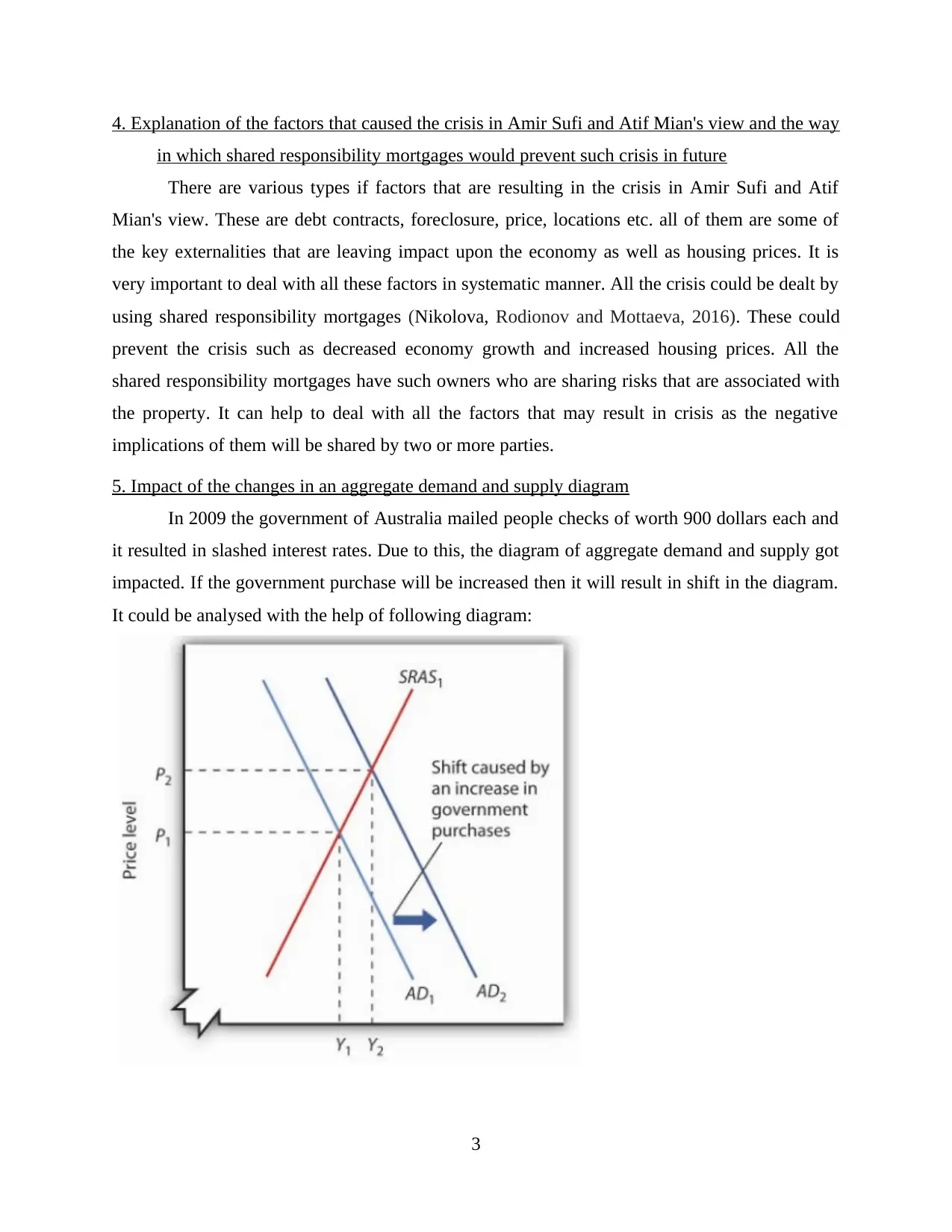

5. Impact of the changes in an aggregate demand and supply diagram

In 2009 the government of Australia mailed people checks of worth 900 dollars each and

it resulted in slashed interest rates. Due to this, the diagram of aggregate demand and supply got

impacted. If the government purchase will be increased then it will result in shift in the diagram.

It could be analysed with the help of following diagram:

3

in which shared responsibility mortgages would prevent such crisis in future

There are various types if factors that are resulting in the crisis in Amir Sufi and Atif

Mian's view. These are debt contracts, foreclosure, price, locations etc. all of them are some of

the key externalities that are leaving impact upon the economy as well as housing prices. It is

very important to deal with all these factors in systematic manner. All the crisis could be dealt by

using shared responsibility mortgages (Nikolova, Rodionov and Mottaeva, 2016). These could

prevent the crisis such as decreased economy growth and increased housing prices. All the

shared responsibility mortgages have such owners who are sharing risks that are associated with

the property. It can help to deal with all the factors that may result in crisis as the negative

implications of them will be shared by two or more parties.

5. Impact of the changes in an aggregate demand and supply diagram

In 2009 the government of Australia mailed people checks of worth 900 dollars each and

it resulted in slashed interest rates. Due to this, the diagram of aggregate demand and supply got

impacted. If the government purchase will be increased then it will result in shift in the diagram.

It could be analysed with the help of following diagram:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of above diagram it has been analysed that when the Australian Government

mailed people checks worth 900 dollar each then it can result in the increased aggregate demand

from AD1 to AD2. Apart from this, with the increment in the demand the supply will also be

enhanced which will result in increased price for the mortgages (Diop, Yavas and Zhu, 2020).

6. Explanation of that if shared responsibility mortgages are widely adopted and they are

securitized to create sate debt would it prevent a future financial crisis

As per articles of Hammad Siddiqi and Ricardo Caballero, it can be said that there

adoption of shared responsibility mortgages and securitisation to develop safe debt will prevent

future financial crisis as different religion of brain are part to evaluate safe as well as risky

choices that assist in treating upcoming crisis related to finance with new and innovative

solutions. Moreover, financial institutions comprises of incentive for carving out safe debt in best

possible manner that plays main role in preventing upcoming financial crisis through creating

financial innovations. Financial analyst properly forecast future and records situations that may

result in huge crisis (Keen, 2017). Along with this, various financial innovations and strategies

are also framed with the purpose of prevent occurrence of any type of big issue within the

industry. Furthermore, to prevent financial crisis, banks needs to become proactive and requires

to adopt effective regulations so to prevent excess creation of safe debt or other related crisis.

Various regulatory caution are also built into the system that helps in preventing financial related

crisis in future.

7. Did financial innovations aimed at creating safe debt cause the crisis or was it primarily

caused by the collapse of the housing bubble?

From the article of Ricardo Caballero, it is analysed that the main contributor of financial

innovations was creation of safe debt that caused the crisis. Financial innovators are the aspects

to develop new financial as well as investment products or processes. It was the main economic

villain prior to the crisis that is said to massive as well as persistent current account deficits that

was experienced by United States and financed by periphery. As per the understanding, it is

determined that the whole world including foreign investors along with central banks has

experiences insatiable demand for safe instruments which put huge pressure on financial system

and its incentives of the nation to craft financial innovations so to meet the situations and deal

with crisis. Moreover, the crisis was outcome of interaction among tremors which caused due to

to rise in sub-prime defaults within financial sector for supplying safe assets and panic related to

4

mailed people checks worth 900 dollar each then it can result in the increased aggregate demand

from AD1 to AD2. Apart from this, with the increment in the demand the supply will also be

enhanced which will result in increased price for the mortgages (Diop, Yavas and Zhu, 2020).

6. Explanation of that if shared responsibility mortgages are widely adopted and they are

securitized to create sate debt would it prevent a future financial crisis

As per articles of Hammad Siddiqi and Ricardo Caballero, it can be said that there

adoption of shared responsibility mortgages and securitisation to develop safe debt will prevent

future financial crisis as different religion of brain are part to evaluate safe as well as risky

choices that assist in treating upcoming crisis related to finance with new and innovative

solutions. Moreover, financial institutions comprises of incentive for carving out safe debt in best

possible manner that plays main role in preventing upcoming financial crisis through creating

financial innovations. Financial analyst properly forecast future and records situations that may

result in huge crisis (Keen, 2017). Along with this, various financial innovations and strategies

are also framed with the purpose of prevent occurrence of any type of big issue within the

industry. Furthermore, to prevent financial crisis, banks needs to become proactive and requires

to adopt effective regulations so to prevent excess creation of safe debt or other related crisis.

Various regulatory caution are also built into the system that helps in preventing financial related

crisis in future.

7. Did financial innovations aimed at creating safe debt cause the crisis or was it primarily

caused by the collapse of the housing bubble?

From the article of Ricardo Caballero, it is analysed that the main contributor of financial

innovations was creation of safe debt that caused the crisis. Financial innovators are the aspects

to develop new financial as well as investment products or processes. It was the main economic

villain prior to the crisis that is said to massive as well as persistent current account deficits that

was experienced by United States and financed by periphery. As per the understanding, it is

determined that the whole world including foreign investors along with central banks has

experiences insatiable demand for safe instruments which put huge pressure on financial system

and its incentives of the nation to craft financial innovations so to meet the situations and deal

with crisis. Moreover, the crisis was outcome of interaction among tremors which caused due to

to rise in sub-prime defaults within financial sector for supplying safe assets and panic related to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

chaotic unravelling of dynamic industry (Caballero, 2010). The point which played essential role

was the point or gap to emphasis on is safe debt factor. Shifts in emphasis provided a

parsimonious level to main events and during the crisis that other innovations failed to do. In the

context, safe debt was key factor behind rising leverage together with macroeconomic risk

concentration within financial institutions because institutions sought to generate profits through

bridging gap among rising demand and increasing natural supply. Safe debt was central force

behind development of complex financial instruments, equipments and linkage that exposed the

economy for panics that were triggered by uncertainty. Along with this, financial sector created

micro AAA assets from securitising lower quality tools at the time when the crisis took place.

At same time, it is also determined that connections among safe debts and more visible

international imbalances have resulted in generation of multiple financial innovations (Anyfantis,

Boustras and Karageorgiou, 2018). It was caused through funding nations' demand for

innovations in more of their competences to produce them. Furthermore, excess demand for safe

debts and others from periphery has also added in generation of financial innovations by variety

of regulatory, collateral as well as mandated requirements for financial institutions, insurance

companies and other types of banking firms.

It is also seen that demand for safe assets began to increase above the level that mortgage

borrowers could provide. For this, financial institutions have made various attempts to search for

innovate mechanisms from past untapped as well as riskier sources. For producing safe assets or

debts from loans, it became important and necessary for banks to produce complex innovations,

instruments and conduits which depends on law of huge numbers as well as tranchment of

liabilities. Similarly, innovative financial instruments were created through securitisation of all

types of payment streams that ranges from auto and last till students loans. In the way, reflecting

values related to creating financial instruments and created positive feedback loop in the era.

From the views presented in the article, it is also perceived that fundamental driver of

financial innovation was aimed to create safe debt resulting in the crisis was unquenchable

demand for safe debt instruments. Moreover, the past instruments or innovations such as triple

A debt failed in meeting demands for such instruments because of which many financial

institutions of United States have to develop developed innovations in financial industry that

meets causes of the crisis on time.

5

was the point or gap to emphasis on is safe debt factor. Shifts in emphasis provided a

parsimonious level to main events and during the crisis that other innovations failed to do. In the

context, safe debt was key factor behind rising leverage together with macroeconomic risk

concentration within financial institutions because institutions sought to generate profits through

bridging gap among rising demand and increasing natural supply. Safe debt was central force

behind development of complex financial instruments, equipments and linkage that exposed the

economy for panics that were triggered by uncertainty. Along with this, financial sector created

micro AAA assets from securitising lower quality tools at the time when the crisis took place.

At same time, it is also determined that connections among safe debts and more visible

international imbalances have resulted in generation of multiple financial innovations (Anyfantis,

Boustras and Karageorgiou, 2018). It was caused through funding nations' demand for

innovations in more of their competences to produce them. Furthermore, excess demand for safe

debts and others from periphery has also added in generation of financial innovations by variety

of regulatory, collateral as well as mandated requirements for financial institutions, insurance

companies and other types of banking firms.

It is also seen that demand for safe assets began to increase above the level that mortgage

borrowers could provide. For this, financial institutions have made various attempts to search for

innovate mechanisms from past untapped as well as riskier sources. For producing safe assets or

debts from loans, it became important and necessary for banks to produce complex innovations,

instruments and conduits which depends on law of huge numbers as well as tranchment of

liabilities. Similarly, innovative financial instruments were created through securitisation of all

types of payment streams that ranges from auto and last till students loans. In the way, reflecting

values related to creating financial instruments and created positive feedback loop in the era.

From the views presented in the article, it is also perceived that fundamental driver of

financial innovation was aimed to create safe debt resulting in the crisis was unquenchable

demand for safe debt instruments. Moreover, the past instruments or innovations such as triple

A debt failed in meeting demands for such instruments because of which many financial

institutions of United States have to develop developed innovations in financial industry that

meets causes of the crisis on time.

5

Throughout the period, aim of financial innovations to create safe debt resulting in crisis

was also one of powerful decision of financial institutions in the country. Essentially, the

contributions made by entire financial industry gained success in making safe assets but the cost

to expose the economy was more (Johannessen, Johannessen and Sangster, 2017).

CONCLUSION and RECOMMENDATION

From the discussion, it have been concluded that Covid -19 pandemic teaches huge things

about international financial crisis. Coase theorem is applied in the situation when there is

complete competitive market having no or limited transaction cost so that negative externalities

related to standard debt mortgage contract are mitigated properly. The theorem states that when

there are any conflicting property right, the bargaining among parties engrossed results in

efficient results regardless the party that is ultimately awarded property rights till transaction

costs concerned with bargaining are negligible. Shared responsibility mortgages mitigates

negative externality concerned with standard debt mortgage through securitising finance giants

and providing guidelines to deal or reduce painful bust and boom episodes. It is standard debt

contract that places huge deal of risk on banking institutions and individuals. Finance system

also plays significant role in overcoming addictions related to mortgage debt. Changes in

aggregate demand and aggregate supply of mortgages will impact on increase in prices due to

which inflation related situation. Moreover, it can impact in reduction of equity that may cause

loss to individual. This also makes no economic sense. It is recommended top financial

institutions that they should adopt and make effective utilisation of shared responsibility

mortgage in order to prevent upcoming financial crisis.

6

was also one of powerful decision of financial institutions in the country. Essentially, the

contributions made by entire financial industry gained success in making safe assets but the cost

to expose the economy was more (Johannessen, Johannessen and Sangster, 2017).

CONCLUSION and RECOMMENDATION

From the discussion, it have been concluded that Covid -19 pandemic teaches huge things

about international financial crisis. Coase theorem is applied in the situation when there is

complete competitive market having no or limited transaction cost so that negative externalities

related to standard debt mortgage contract are mitigated properly. The theorem states that when

there are any conflicting property right, the bargaining among parties engrossed results in

efficient results regardless the party that is ultimately awarded property rights till transaction

costs concerned with bargaining are negligible. Shared responsibility mortgages mitigates

negative externality concerned with standard debt mortgage through securitising finance giants

and providing guidelines to deal or reduce painful bust and boom episodes. It is standard debt

contract that places huge deal of risk on banking institutions and individuals. Finance system

also plays significant role in overcoming addictions related to mortgage debt. Changes in

aggregate demand and aggregate supply of mortgages will impact on increase in prices due to

which inflation related situation. Moreover, it can impact in reduction of equity that may cause

loss to individual. This also makes no economic sense. It is recommended top financial

institutions that they should adopt and make effective utilisation of shared responsibility

mortgage in order to prevent upcoming financial crisis.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Anyfantis, I., Boustras, G. and Karageorgiou, A., 2018. Maintaining occupational safety and

health levels during the financial crisis–A conceptual model. Safety science. 106.

pp.246-254.

Johannessen, J. A., Johannessen and Sangster, 2017. Innovations Lead to Economic Crises.

London: Palgrave Macmillan.

Keen, S., 2017. Can we avoid another financial crisis?. John Wiley & Sons.

AĞCA, Ş. and ISLAM, S. S., 2019. Securitized Debt Markets. Debt Markets and Investments,

p.131.

Nourzad, F., Hunter, W. and Szczesniak, K., 2020. Securitization of revolving debt and its

determinants. The Quarterly Review of Economics and Finance. 75. pp.240-246.

Lauretta, E., 2018. The hidden soul of financial innovation: An agent-based modelling of home

mortgage securitization and the finance-growth nexus. Economic Modelling. 68. pp.51-

73.

Nikolova, L. V., Rodionov, D. G. and Mottaeva, A. B., 2016. Securitization of bank assets as a

source of financing the innovation activity. International Journal of Economics and

Financial Issues. 6(2S).

Diop, M., Yavas, A. and Zhu, S., 2020. Appraisal Inflation and Private Mortgage

Securitization. Available at SSRN 3657595.

Online:

Caballero. J. R. 2010. The “Other” Imbalance and Financial crisis. [Online]. Available

through: < https://www.nber.org/papers/w15636>

7

Books and Journals:

Anyfantis, I., Boustras, G. and Karageorgiou, A., 2018. Maintaining occupational safety and

health levels during the financial crisis–A conceptual model. Safety science. 106.

pp.246-254.

Johannessen, J. A., Johannessen and Sangster, 2017. Innovations Lead to Economic Crises.

London: Palgrave Macmillan.

Keen, S., 2017. Can we avoid another financial crisis?. John Wiley & Sons.

AĞCA, Ş. and ISLAM, S. S., 2019. Securitized Debt Markets. Debt Markets and Investments,

p.131.

Nourzad, F., Hunter, W. and Szczesniak, K., 2020. Securitization of revolving debt and its

determinants. The Quarterly Review of Economics and Finance. 75. pp.240-246.

Lauretta, E., 2018. The hidden soul of financial innovation: An agent-based modelling of home

mortgage securitization and the finance-growth nexus. Economic Modelling. 68. pp.51-

73.

Nikolova, L. V., Rodionov, D. G. and Mottaeva, A. B., 2016. Securitization of bank assets as a

source of financing the innovation activity. International Journal of Economics and

Financial Issues. 6(2S).

Diop, M., Yavas, A. and Zhu, S., 2020. Appraisal Inflation and Private Mortgage

Securitization. Available at SSRN 3657595.

Online:

Caballero. J. R. 2010. The “Other” Imbalance and Financial crisis. [Online]. Available

through: < https://www.nber.org/papers/w15636>

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.